Deck 1: Accounting for Decision Making and Control

ملء الشاشة (f)

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

Cost, Volume, Profit Analysis

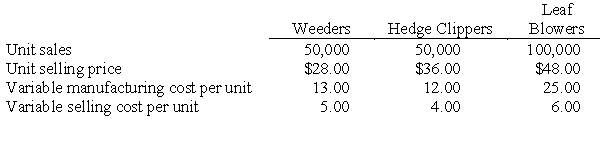

Kalifo Company manufactures a line of electric garden tools that are sold in general hardware stores. The company's controller, Sylvia Harlow, has just received the sales forecast for the coming year for Kalifo's three products: weeders, hedge clippers, and leaf blowers. Kalifo has experienced considerable variations in sales volumes and variable costs over the past two years, and Harlow believes the forecast should be carefully evaluated from a cost-volume-profit viewpoint. The preliminary budget information for 1996 is presented below. For 1996, Kalifo's fixed factory overhead is budgeted at $2 million, and the company's fixed selling and administrative expenses are forecast to be $600,000. Kalifo has a tax rate of 40 percent.

For 1996, Kalifo's fixed factory overhead is budgeted at $2 million, and the company's fixed selling and administrative expenses are forecast to be $600,000. Kalifo has a tax rate of 40 percent.

Required:

a. Determine Kalifo Co.'s budgeted net income for 1996.

b. Assuming that the sales mix remains as budgeted, determine how many units of each product Kalifo must sell in order to break even in 1996.

c. Determine the total dollar sales Kalifo must sell in 1996 in order to earn an after-tax net income of $450,000.

d. After preparing the original estimates, Kalifo determines that its variable manufacturing cost of leaf blowers will increase 20 percent and the variable selling cost of hedge clippers can be expected to increase $1 per unit. However, Kalifo has decided not to change the selling price of either product. In addition, Kalifo learns that its leaf blower is perceived as the best value on the market, and it can expect to sell three times as many leaf blowers as any other product. Under these circumstances, determine how many units of each product Kalifo will have to sell to break even in 1996.

e. Explain the limitations of cost-volume-profit analysis that Sylvia Harlow should consider when evaluating Kalifo's 1996 budget.

Kalifo Company manufactures a line of electric garden tools that are sold in general hardware stores. The company's controller, Sylvia Harlow, has just received the sales forecast for the coming year for Kalifo's three products: weeders, hedge clippers, and leaf blowers. Kalifo has experienced considerable variations in sales volumes and variable costs over the past two years, and Harlow believes the forecast should be carefully evaluated from a cost-volume-profit viewpoint. The preliminary budget information for 1996 is presented below.

For 1996, Kalifo's fixed factory overhead is budgeted at $2 million, and the company's fixed selling and administrative expenses are forecast to be $600,000. Kalifo has a tax rate of 40 percent.Required:

a. Determine Kalifo Co.'s budgeted net income for 1996.

b. Assuming that the sales mix remains as budgeted, determine how many units of each product Kalifo must sell in order to break even in 1996.

c. Determine the total dollar sales Kalifo must sell in 1996 in order to earn an after-tax net income of $450,000.

d. After preparing the original estimates, Kalifo determines that its variable manufacturing cost of leaf blowers will increase 20 percent and the variable selling cost of hedge clippers can be expected to increase $1 per unit. However, Kalifo has decided not to change the selling price of either product. In addition, Kalifo learns that its leaf blower is perceived as the best value on the market, and it can expect to sell three times as many leaf blowers as any other product. Under these circumstances, determine how many units of each product Kalifo will have to sell to break even in 1996.

e. Explain the limitations of cost-volume-profit analysis that Sylvia Harlow should consider when evaluating Kalifo's 1996 budget.

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

Fixed, Variable, and Average Costs

Midstate University is trying to decide whether to allow 100 more students into the university. Tuition is $5000 per year. The controller has determined the following schedule of costs to educate students: The current enrollment is 4200 students. The president of the university has calculated the cost per student in the following manner: $30,600,000/4200 students = $7286 per student. The president was wondering why the university should accept more students if the tuition is only $5000.

The current enrollment is 4200 students. The president of the university has calculated the cost per student in the following manner: $30,600,000/4200 students = $7286 per student. The president was wondering why the university should accept more students if the tuition is only $5000.

Required:

a. What is wrong with the president's calculation?

b. What are the fixed and variable costs of operating the university?

Midstate University is trying to decide whether to allow 100 more students into the university. Tuition is $5000 per year. The controller has determined the following schedule of costs to educate students:

The current enrollment is 4200 students. The president of the university has calculated the cost per student in the following manner: $30,600,000/4200 students = $7286 per student. The president was wondering why the university should accept more students if the tuition is only $5000.Required:

a. What is wrong with the president's calculation?

b. What are the fixed and variable costs of operating the university?

سؤال

ROI and Residual Income

The following investment opportunities are available to an investment center manager: Required:

Required:

a. If the investment manager is currently making a return on investment of 16 percent, which project(s) would the manager want to pursue?

b. If the cost of capital is 10 percent and the annual earnings approximate cash flows excluding finance charges, which project(s) should be chosen?

c. Suppose only one project can be chosen and the annual earnings approximate cash flows excluding finance charges. Which project should be chosen?

The following investment opportunities are available to an investment center manager:

Required:a. If the investment manager is currently making a return on investment of 16 percent, which project(s) would the manager want to pursue?

b. If the cost of capital is 10 percent and the annual earnings approximate cash flows excluding finance charges, which project(s) should be chosen?

c. Suppose only one project can be chosen and the annual earnings approximate cash flows excluding finance charges. Which project should be chosen?

سؤال

سؤال

Flexible Budgets

A chair manufacturer has established the following flexible budget for the month. Required:

Required:

a. What is the sales price per chair?

b. What is the expected profit if 1,600 chairs are made?

A chair manufacturer has established the following flexible budget for the month.

Required:a. What is the sales price per chair?

b. What is the expected profit if 1,600 chairs are made?

سؤال

سؤال

سؤال

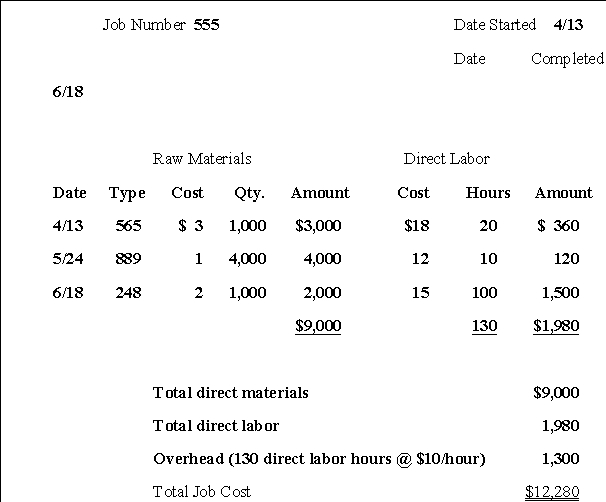

Job Cost Flows

The job cost sheet for 1,000 units of toy trucks is: All of the materials for the job were purchased on 4/10. The batch of 1,000 toy trucks is sold on 7/10.

All of the materials for the job were purchased on 4/10. The batch of 1,000 toy trucks is sold on 7/10.

What are the costs of this job order in the raw materials account, the work-in-process account, the finished goods account, and the cost of goods account on 4/30, 5/31, 6/30 and 7/31?

The job cost sheet for 1,000 units of toy trucks is:

All of the materials for the job were purchased on 4/10. The batch of 1,000 toy trucks is sold on 7/10.What are the costs of this job order in the raw materials account, the work-in-process account, the finished goods account, and the cost of goods account on 4/30, 5/31, 6/30 and 7/31?

سؤال

Pro-Forma Financial Statements

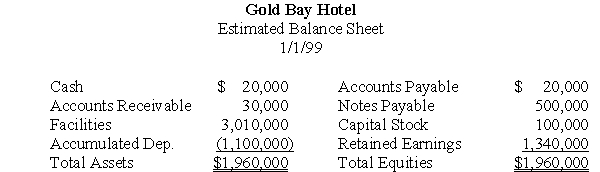

The Gold Bay Hotel is in the process of developing a master budget and pro-forma financial statements for 1999. The beginning balance sheet for the fiscal year 1999 is estimated to be: During the year the hotel expects to rent 30,000 rooms. Rooms rent for an average of $90 per night. The hotel expects to sell 40,000 meals during the year at an average price of $20 per meal. The variable cost per room rented is $30 and the variable cost per meal is $8. The fixed costs not including depreciation is expected to be $2,000,000. Depreciation is expected to be $500,000. The hotel also expects to refurbish the kitchen at a cost of $200,000, which is capitalized (included in the facility account). Interest of the note payable is expected to be $50,000 and $100,000 of the note payable will be retired during the year. The ending accounts receivable amount is expected to be $40,000 and the ending accounts payable is expected to be $30,000.

During the year the hotel expects to rent 30,000 rooms. Rooms rent for an average of $90 per night. The hotel expects to sell 40,000 meals during the year at an average price of $20 per meal. The variable cost per room rented is $30 and the variable cost per meal is $8. The fixed costs not including depreciation is expected to be $2,000,000. Depreciation is expected to be $500,000. The hotel also expects to refurbish the kitchen at a cost of $200,000, which is capitalized (included in the facility account). Interest of the note payable is expected to be $50,000 and $100,000 of the note payable will be retired during the year. The ending accounts receivable amount is expected to be $40,000 and the ending accounts payable is expected to be $30,000.

Prepare pro-forma financial statements for the end of the year.

The Gold Bay Hotel is in the process of developing a master budget and pro-forma financial statements for 1999. The beginning balance sheet for the fiscal year 1999 is estimated to be:

During the year the hotel expects to rent 30,000 rooms. Rooms rent for an average of $90 per night. The hotel expects to sell 40,000 meals during the year at an average price of $20 per meal. The variable cost per room rented is $30 and the variable cost per meal is $8. The fixed costs not including depreciation is expected to be $2,000,000. Depreciation is expected to be $500,000. The hotel also expects to refurbish the kitchen at a cost of $200,000, which is capitalized (included in the facility account). Interest of the note payable is expected to be $50,000 and $100,000 of the note payable will be retired during the year. The ending accounts receivable amount is expected to be $40,000 and the ending accounts payable is expected to be $30,000.Prepare pro-forma financial statements for the end of the year.

سؤال

سؤال

سؤال

Prorating Over/Underabsorbed Overhead

A computer manufacturer has the following account balances at the end of the year. These accounts contain $500,000 of allocated overhead. Actual overhead, however, is $600,000.

These accounts contain $500,000 of allocated overhead. Actual overhead, however, is $600,000.

What are the account balances after prorating the underabsorbed overhead?

A computer manufacturer has the following account balances at the end of the year.

These accounts contain $500,000 of allocated overhead. Actual overhead, however, is $600,000.What are the account balances after prorating the underabsorbed overhead?

سؤال

سؤال

سؤال

سؤال

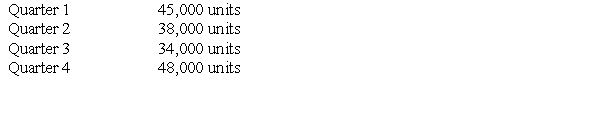

Budgeting Direct Materials

The Jung Corporation's budget calls for the following production: Each unit of production requires three pounds of direct material. The company's policy is to begin each quarter with an inventory of direct materials equal to 30 percent of that quarter's direct material requirements. Compute budgeted direct materials purchases for the third quarter.

Each unit of production requires three pounds of direct material. The company's policy is to begin each quarter with an inventory of direct materials equal to 30 percent of that quarter's direct material requirements. Compute budgeted direct materials purchases for the third quarter.

The Jung Corporation's budget calls for the following production:

Each unit of production requires three pounds of direct material. The company's policy is to begin each quarter with an inventory of direct materials equal to 30 percent of that quarter's direct material requirements. Compute budgeted direct materials purchases for the third quarter. سؤال

سؤال

سؤال

سؤال

سؤال

Performance Measures for Cost Centers

A soft drink company has three bottling plants throughout the country. Bottling occurs at the regional level because of the high cost of transporting bottled soft drinks. The parent company supplies each plant with the syrup. The bottling plants combine the syrup with carbonated soda to make and bottle the soft drinks. The bottled soft drinks are then sent to regional grocery stores.

The bottling plants are treated as costs centers. The managers of the bottling plants are evaluated based on minimizing the cost per soft drink bottled and delivered. Each bottling plant uses the same equipment, but some produce more bottles of soft drinks because of different demand. The costs and output for each bottling plant are: Required:

Required:

a. Estimate the average cost per unit for each plant.

b. Why would the manager of plant A be unhappy with using the average cost as the performance measure?

c. What is an alternative performance measure that would make the manager of plant A happier?

d. Under what circumstances might the average cost be a better performance measure?

A soft drink company has three bottling plants throughout the country. Bottling occurs at the regional level because of the high cost of transporting bottled soft drinks. The parent company supplies each plant with the syrup. The bottling plants combine the syrup with carbonated soda to make and bottle the soft drinks. The bottled soft drinks are then sent to regional grocery stores.

The bottling plants are treated as costs centers. The managers of the bottling plants are evaluated based on minimizing the cost per soft drink bottled and delivered. Each bottling plant uses the same equipment, but some produce more bottles of soft drinks because of different demand. The costs and output for each bottling plant are:

Required:a. Estimate the average cost per unit for each plant.

b. Why would the manager of plant A be unhappy with using the average cost as the performance measure?

c. What is an alternative performance measure that would make the manager of plant A happier?

d. Under what circumstances might the average cost be a better performance measure?

سؤال

سؤال

سؤال

سؤال

سؤال

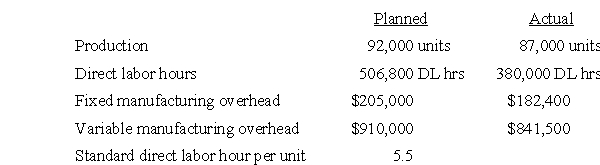

Overhead Variances

The following information is for the third quarter of this year: Required:

Required:

Calculate the following three overhead variances:

a. Overhead volume variance.

b. Overhead efficiency variance.

c. Overhead spending variance.

The following information is for the third quarter of this year:

Required:Calculate the following three overhead variances:

a. Overhead volume variance.

b. Overhead efficiency variance.

c. Overhead spending variance.

سؤال

سؤال

سؤال

ABC and Average Cost in a Service Industry

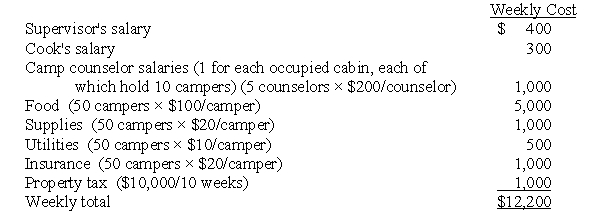

For many years the Honey Lake Summer Camp had used the number of campers per week to estimate weekly costs. The summer camp is open for ten weeks during the summer with a different number of campers each week. July is busiest with June and the end of August least busy. Costs from the last week of summer camp in 1998 are used to estimate costs for 1999 for pricing purposes. The following costs occurred during the last week of 1998 and the costs of each cost category are expected to be the same for 1999: Cost per camper: $12,200/50 campers = $244/camper

Cost per camper: $12,200/50 campers = $244/camper

The Honey Lake Summer Camp expects 75 campers during the second week of July.

Required:

a. What is the expected cost of that week using the average cost?

b. What is the expected cost of that week using ABC?

For many years the Honey Lake Summer Camp had used the number of campers per week to estimate weekly costs. The summer camp is open for ten weeks during the summer with a different number of campers each week. July is busiest with June and the end of August least busy. Costs from the last week of summer camp in 1998 are used to estimate costs for 1999 for pricing purposes. The following costs occurred during the last week of 1998 and the costs of each cost category are expected to be the same for 1999:

Cost per camper: $12,200/50 campers = $244/camperThe Honey Lake Summer Camp expects 75 campers during the second week of July.

Required:

a. What is the expected cost of that week using the average cost?

b. What is the expected cost of that week using ABC?

سؤال

سؤال

سؤال

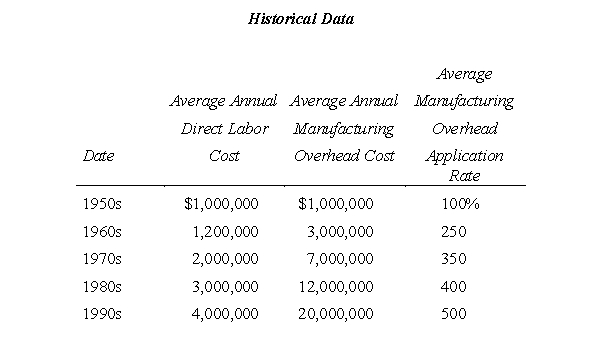

Plantwide vs. Department Overhead Rates

Rose Bach has recently been hired as controller of Empco Inc., a sheet-metal manufacturer. Empco has been in the sheet-metal business for many years and is currently investigating ways to modernize its manufacturing process. At the first staff meeting Bach attended, Bob Kelley, chief engineer, presented a proposal for automating the drilling department. Kelley recommended that Empco purchase two robots that could replace the eight direct labor workers in the department. The cost savings outlined in Kelley's proposal include two elements. First, direct labor cost in the drilling department is eliminated. Second, manufacturing overhead cost in the department is reduced to zero because Empco charges manufacturing overhead on the basis of direct labor dollars using a plantwide rate.

The president of Empco felt that Kelley's explanation of the cost savings made no sense. Bach agreed and explained that as firms become more automated, they should rethink their manufacturing overhead systems. The president asked Bach to look into the matter and prepare a report for the next staff meeting.

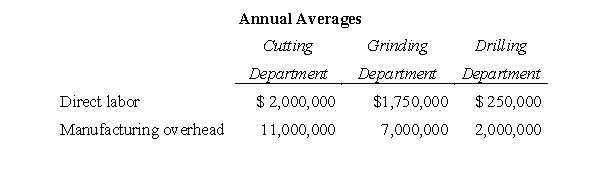

To refresh her knowledge, Bach reviewed articles on manufacturing overhead allocation for an automated factory and discussed the matter with some of her peers. She also gathered the historical data presented below on the manufacturing overhead rates experienced by Empco over the years. Bach also wanted to have some departmental data to present at the meeting. Using Empco's accounting records, she was able to estimate the annual averages presented below for each manufacturing department in the 1990s.

Required:

Required:

a. Disregarding the proposed use of robots in the drilling department, describe the shortcomings of Empco's current system for applying overhead.

b. Do you agree with Bob Kelley's statement that the manufacturing overhead cost in the drilling department will be reduced to zero if the automation proposal is implemented? Explain.

c. Recommend ways to improve Empco's method for applying overhead by describing how it should revise its overhead accounting system:

(i) in the cutting and grinding departments.

(ii) to accommodate the automation of the drilling department.

Source: CMA adapted.

Rose Bach has recently been hired as controller of Empco Inc., a sheet-metal manufacturer. Empco has been in the sheet-metal business for many years and is currently investigating ways to modernize its manufacturing process. At the first staff meeting Bach attended, Bob Kelley, chief engineer, presented a proposal for automating the drilling department. Kelley recommended that Empco purchase two robots that could replace the eight direct labor workers in the department. The cost savings outlined in Kelley's proposal include two elements. First, direct labor cost in the drilling department is eliminated. Second, manufacturing overhead cost in the department is reduced to zero because Empco charges manufacturing overhead on the basis of direct labor dollars using a plantwide rate.

The president of Empco felt that Kelley's explanation of the cost savings made no sense. Bach agreed and explained that as firms become more automated, they should rethink their manufacturing overhead systems. The president asked Bach to look into the matter and prepare a report for the next staff meeting.

To refresh her knowledge, Bach reviewed articles on manufacturing overhead allocation for an automated factory and discussed the matter with some of her peers. She also gathered the historical data presented below on the manufacturing overhead rates experienced by Empco over the years. Bach also wanted to have some departmental data to present at the meeting. Using Empco's accounting records, she was able to estimate the annual averages presented below for each manufacturing department in the 1990s.

Required:a. Disregarding the proposed use of robots in the drilling department, describe the shortcomings of Empco's current system for applying overhead.

b. Do you agree with Bob Kelley's statement that the manufacturing overhead cost in the drilling department will be reduced to zero if the automation proposal is implemented? Explain.

c. Recommend ways to improve Empco's method for applying overhead by describing how it should revise its overhead accounting system:

(i) in the cutting and grinding departments.

(ii) to accommodate the automation of the drilling department.

Source: CMA adapted.

سؤال

سؤال

سؤال

سؤال

Developing Additional Variances for Performance Evaluation

Maidwell Company manufactures washers and dryers on a single assembly line in its main factory. The market has deteriorated over the last five years and competition has made cost control very important. Management has been concerned about the materials costs of both washers and dryers. There have been no model changes in the past two years, and economic conditions have allowed the company to negotiate price reductions for many key parts.

Maidwell uses a standard cost system in accounting for materials. Purchases are charged to inventory at a standard price, and purchase discounts are considered an administrative cost reduction. Production is charged at the standard price of the materials used. Thus, the price variance is isolated at time of purchase as the difference between gross contract price and standard price multiplied by the quantity purchased. When a substitute part is used in production, a price variance equal to the difference in the standard prices of the materials is recognized at the time of substitution. The quantity variance is the actual quantity used compared with the standard quantity allowed, with the difference multiplied by the standard price.

The materials variances for several of the parts Maidwell uses are unfavorable. Part #4121 is one item that has an unfavorable variance. Maidwell knows that some of these parts are defective and will fail. The failure is discovered during production. The normal defective rate is 5 percent of normal input. The original contract price of this part was $0.285 per unit; thus, Maidwell set the standard unit price at $0.285. The unit contract purchase price of Part #4121 was increased to $0.325 from the original $0.285 due to a parts specification change. Maidwell chose not to change the standard; it treated the increase in price as a price variance. In addition, the contract terms were changed from payment due in 30 days to a 4 percent discount if paid in 10 days or full payment due in 30 days. These new contractual terms were the consequence of negotiations resulting from changes in the economy.

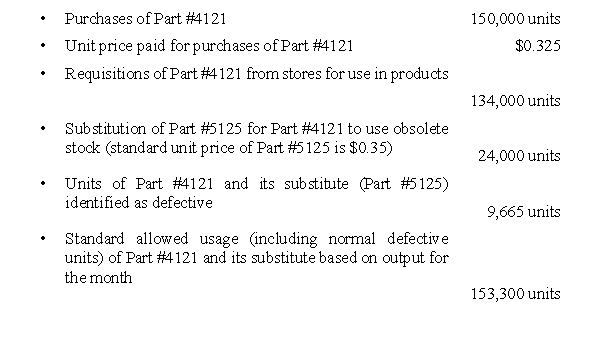

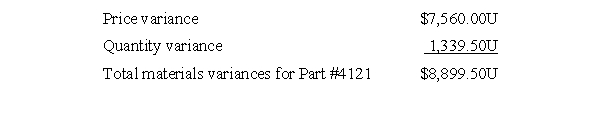

Data regarding the use of Part #4121 during December are as follows. Maidwell's material variances related to Part #4121 for December were reported as follows:

Maidwell's material variances related to Part #4121 for December were reported as follows:  Bob Speck, the purchasing director, claims the unfavorable price variance is misleading. Speck says that his department has worked hard to obtain price concessions and purchase discounts from suppliers. In addition, Speck says engineering changes in several parts have increased their prices, even though the part identification has not changed. These price increases are not his department's responsibility. Speck declares that price variances no longer measure purchasing's performance.

Bob Speck, the purchasing director, claims the unfavorable price variance is misleading. Speck says that his department has worked hard to obtain price concessions and purchase discounts from suppliers. In addition, Speck says engineering changes in several parts have increased their prices, even though the part identification has not changed. These price increases are not his department's responsibility. Speck declares that price variances no longer measure purchasing's performance.

Jim Buddle, the manufacturing manager, thinks the responsibility for the quantity variance should be shared. Buddle states that manufacturing cannot control quality associated with less expensive parts, substitutions of material to use up otherwise obsolete stock, or engineering changes that increase the quantity of materials used.

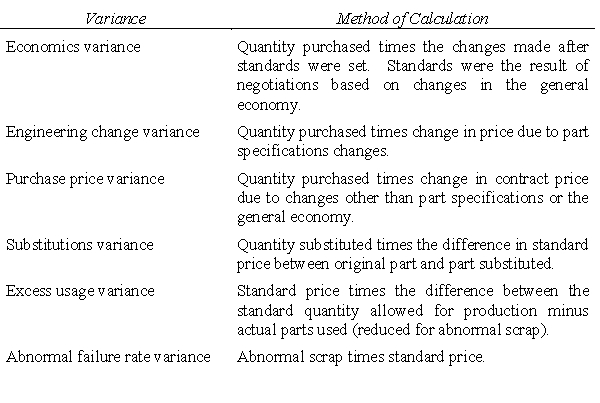

The accounting manager, Mike Kohl, suggests that the computation of variances be changed to identify variations from standard with the causes and functional areas responsible for the variances. Kohl recommends the following system of materials variances and the method of computation for each: Required:

Required:

a. Discuss the appropriateness of Maidwell Company's current method of variance analysis for materials and indicate whether the claims of Bob Speck and Jim Buddle are valid.

b. Compute the materials variances for Part #4121 for December using the system recommended by Mike Kohl.

c. Who would be responsible for each of the variances in Mike Kohl's system of variance analysis for materials?

Maidwell Company manufactures washers and dryers on a single assembly line in its main factory. The market has deteriorated over the last five years and competition has made cost control very important. Management has been concerned about the materials costs of both washers and dryers. There have been no model changes in the past two years, and economic conditions have allowed the company to negotiate price reductions for many key parts.

Maidwell uses a standard cost system in accounting for materials. Purchases are charged to inventory at a standard price, and purchase discounts are considered an administrative cost reduction. Production is charged at the standard price of the materials used. Thus, the price variance is isolated at time of purchase as the difference between gross contract price and standard price multiplied by the quantity purchased. When a substitute part is used in production, a price variance equal to the difference in the standard prices of the materials is recognized at the time of substitution. The quantity variance is the actual quantity used compared with the standard quantity allowed, with the difference multiplied by the standard price.

The materials variances for several of the parts Maidwell uses are unfavorable. Part #4121 is one item that has an unfavorable variance. Maidwell knows that some of these parts are defective and will fail. The failure is discovered during production. The normal defective rate is 5 percent of normal input. The original contract price of this part was $0.285 per unit; thus, Maidwell set the standard unit price at $0.285. The unit contract purchase price of Part #4121 was increased to $0.325 from the original $0.285 due to a parts specification change. Maidwell chose not to change the standard; it treated the increase in price as a price variance. In addition, the contract terms were changed from payment due in 30 days to a 4 percent discount if paid in 10 days or full payment due in 30 days. These new contractual terms were the consequence of negotiations resulting from changes in the economy.

Data regarding the use of Part #4121 during December are as follows.

Maidwell's material variances related to Part #4121 for December were reported as follows: Bob Speck, the purchasing director, claims the unfavorable price variance is misleading. Speck says that his department has worked hard to obtain price concessions and purchase discounts from suppliers. In addition, Speck says engineering changes in several parts have increased their prices, even though the part identification has not changed. These price increases are not his department's responsibility. Speck declares that price variances no longer measure purchasing's performance.Jim Buddle, the manufacturing manager, thinks the responsibility for the quantity variance should be shared. Buddle states that manufacturing cannot control quality associated with less expensive parts, substitutions of material to use up otherwise obsolete stock, or engineering changes that increase the quantity of materials used.

The accounting manager, Mike Kohl, suggests that the computation of variances be changed to identify variations from standard with the causes and functional areas responsible for the variances. Kohl recommends the following system of materials variances and the method of computation for each:

Required:a. Discuss the appropriateness of Maidwell Company's current method of variance analysis for materials and indicate whether the claims of Bob Speck and Jim Buddle are valid.

b. Compute the materials variances for Part #4121 for December using the system recommended by Mike Kohl.

c. Who would be responsible for each of the variances in Mike Kohl's system of variance analysis for materials?

سؤال

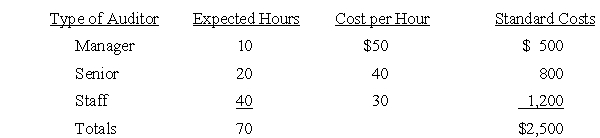

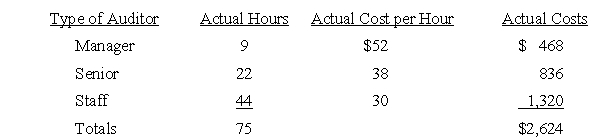

Standard Labor Variances

A CPA firm estimates that an audit will require the following work: The actual hours and costs were:

The actual hours and costs were:  Required:

Required:

Calculate the direct labor, wage rate, and labor efficiency variances for each type of auditor and interpret.

A CPA firm estimates that an audit will require the following work:

The actual hours and costs were: Required:Calculate the direct labor, wage rate, and labor efficiency variances for each type of auditor and interpret.

سؤال

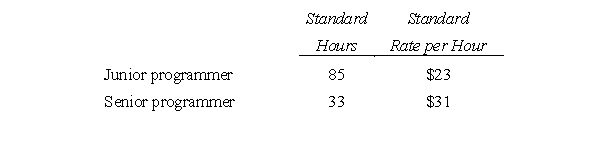

Labor Variances

Hospital Software sells and installs computer software used by hospitals for patient admissions and billing. Every sale requires that Hospital Services modify its proprietary software for the specific demands of the client. Prior to each installation, Hospital Software estimates the number of hours of programming time each job will require and the cost of the programmers. Programmers record the amount of time they spend on each modification, and variance reports are prepared at the end of each installation.

For the Denver General Hospital account, Hospital Software estimates the following labor standards: After the job was completed, the following costs were reported:

After the job was completed, the following costs were reported:  Required:

Required:

Calculate the labor efficiency and labor wage rate variances for the junior and senior programmers on the Denver General Hospital account.

Hospital Software sells and installs computer software used by hospitals for patient admissions and billing. Every sale requires that Hospital Services modify its proprietary software for the specific demands of the client. Prior to each installation, Hospital Software estimates the number of hours of programming time each job will require and the cost of the programmers. Programmers record the amount of time they spend on each modification, and variance reports are prepared at the end of each installation.

For the Denver General Hospital account, Hospital Software estimates the following labor standards:

After the job was completed, the following costs were reported: Required:Calculate the labor efficiency and labor wage rate variances for the junior and senior programmers on the Denver General Hospital account.

سؤال

سؤال

سؤال

سؤال

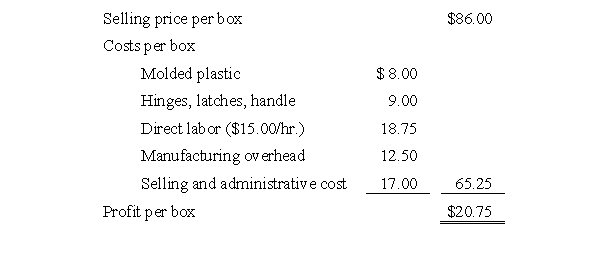

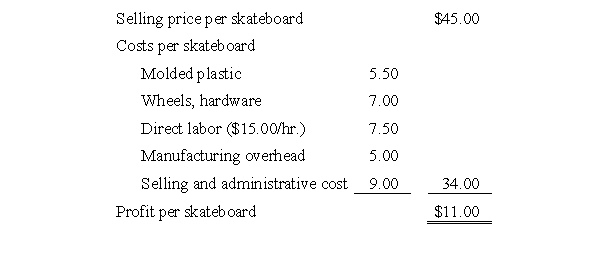

Product Profitability and Mix - Calculating Variable Overhead

Sportway Inc. is a wholesale distributor supplying a wide range of moderately priced sporting equipment to large chain stores. About 60 percent of Sportway's products are purchased from other companies and the remainder are manufactured by Sportway. The company has a plastics department that is currently manufacturing molded fishing tackle boxes. Sportway is able to manufacture and sell 8,000 tackle boxes annually, making full use of its direct labor capacity at available workstations. Presented below are the selling price and costs associated with Sportway's tackle boxes. Because Sportway believes it could sell 12,000 tackle boxes if it had sufficient manufacturing capacity, the company has looked into the possibility of purchasing the tackle boxes for distribution. Maple Products, a steady supplier of quality products, would be able to provide up to 9,000 tackle boxes per year at a price of $68 per box delivered to Sportway's facility.

Because Sportway believes it could sell 12,000 tackle boxes if it had sufficient manufacturing capacity, the company has looked into the possibility of purchasing the tackle boxes for distribution. Maple Products, a steady supplier of quality products, would be able to provide up to 9,000 tackle boxes per year at a price of $68 per box delivered to Sportway's facility.

Bart Johnson, Sportway's product manager, has suggested that the company could make better use of its plastics department by manufacturing skateboards. To support his position, Johnson has a market study that indicates an expanding market for skateboards and a need for additional suppliers. Johnson believes that Sportway could expect to sell 17,500 skateboards annually at $45 per skateboard. Johnson's estimate of the costs to manufacture the skateboards follows. In the plastics department, Sportway uses direct labor hours as the application base for manufacturing overhead. Included in manufacturing overhead for the current year is $50,000 of factorywide, fixed manufacturing overhead that has been allocated to the plastics department. For each product that Sportway sells, regardless of whether the product has been purchased or is manufactured by Sportway, a portion of the selling and administrative cost is fixed at $6 per unit. Total selling and administrative costs for the purchased tackle boxes would be $10 per unit.

In the plastics department, Sportway uses direct labor hours as the application base for manufacturing overhead. Included in manufacturing overhead for the current year is $50,000 of factorywide, fixed manufacturing overhead that has been allocated to the plastics department. For each product that Sportway sells, regardless of whether the product has been purchased or is manufactured by Sportway, a portion of the selling and administrative cost is fixed at $6 per unit. Total selling and administrative costs for the purchased tackle boxes would be $10 per unit.

Required:

Prepare an analysis based on the data presented that will show which product or products Sportway Inc. should manufacture and/or purchase to maximize the company's profitability. Show the associated financial impact. Support your answer with appropriate calculations.

Sportway Inc. is a wholesale distributor supplying a wide range of moderately priced sporting equipment to large chain stores. About 60 percent of Sportway's products are purchased from other companies and the remainder are manufactured by Sportway. The company has a plastics department that is currently manufacturing molded fishing tackle boxes. Sportway is able to manufacture and sell 8,000 tackle boxes annually, making full use of its direct labor capacity at available workstations. Presented below are the selling price and costs associated with Sportway's tackle boxes.

Because Sportway believes it could sell 12,000 tackle boxes if it had sufficient manufacturing capacity, the company has looked into the possibility of purchasing the tackle boxes for distribution. Maple Products, a steady supplier of quality products, would be able to provide up to 9,000 tackle boxes per year at a price of $68 per box delivered to Sportway's facility.Bart Johnson, Sportway's product manager, has suggested that the company could make better use of its plastics department by manufacturing skateboards. To support his position, Johnson has a market study that indicates an expanding market for skateboards and a need for additional suppliers. Johnson believes that Sportway could expect to sell 17,500 skateboards annually at $45 per skateboard. Johnson's estimate of the costs to manufacture the skateboards follows.

In the plastics department, Sportway uses direct labor hours as the application base for manufacturing overhead. Included in manufacturing overhead for the current year is $50,000 of factorywide, fixed manufacturing overhead that has been allocated to the plastics department. For each product that Sportway sells, regardless of whether the product has been purchased or is manufactured by Sportway, a portion of the selling and administrative cost is fixed at $6 per unit. Total selling and administrative costs for the purchased tackle boxes would be $10 per unit.Required:

Prepare an analysis based on the data presented that will show which product or products Sportway Inc. should manufacture and/or purchase to maximize the company's profitability. Show the associated financial impact. Support your answer with appropriate calculations.

سؤال

سؤال

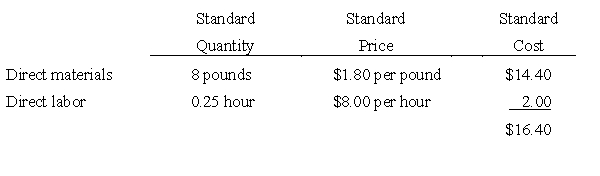

Basic Price and Quantity Variances for Labor and Materials

Arrow Industries employs a standard cost system in which direct materials inventory is carried at standard cost. Arrow has established the following standards for the direct costs of one unit of product. During May, Arrow purchased 160,000 pounds of direct materials at a total cost of $304,000. The total factory wages for May were $42,000, 90 percent of which were for direct labor. Arrow manufactured 19,000 units of product during May using 142,500 pounds of direct material and 5,000 direct labor hours.

During May, Arrow purchased 160,000 pounds of direct materials at a total cost of $304,000. The total factory wages for May were $42,000, 90 percent of which were for direct labor. Arrow manufactured 19,000 units of product during May using 142,500 pounds of direct material and 5,000 direct labor hours.

Required:

a. Calculate the direct materials price variance for May.

b. Calculate the direct materials quantity variance for May.

c. Calculate the direct labor wage rate variance for May.

d. Calculate the direct labor efficiency variance for May.

Arrow Industries employs a standard cost system in which direct materials inventory is carried at standard cost. Arrow has established the following standards for the direct costs of one unit of product.

During May, Arrow purchased 160,000 pounds of direct materials at a total cost of $304,000. The total factory wages for May were $42,000, 90 percent of which were for direct labor. Arrow manufactured 19,000 units of product during May using 142,500 pounds of direct material and 5,000 direct labor hours.Required:

a. Calculate the direct materials price variance for May.

b. Calculate the direct materials quantity variance for May.

c. Calculate the direct labor wage rate variance for May.

d. Calculate the direct labor efficiency variance for May.

سؤال

سؤال

سؤال

سؤال

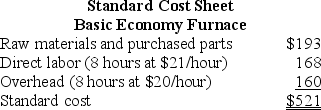

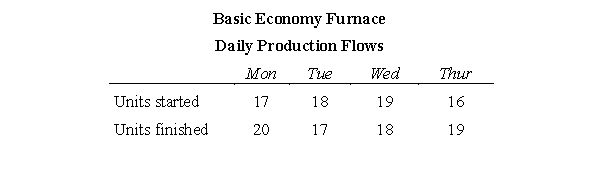

JIT Accounting

Warm Glo manufactures gas furnaces for residential use. It uses a standard cost system that isolates all variances at purchase so that all product costs are stated at standard cost. All variances are included as part of cost of goods sold. Overhead is allocated based on direct labor hours. Standard cost for the basic economy model furnace follows.

Warm Glo manufactures the basic economy furnace in a dedicated flow line using just-in-time production principles. All raw materials and purchased parts needed to assemble a complete furnace are delivered to the plant by 8:00 am of the day the furnace begins production. While each furnace requires eight direct labor hours, total throughput time for each furnace is two working days (16 hours). The difference between total throughput time and the eight direct labor hours is waiting time. Furnaces that are started in production one day are finished the next day. Four hours of direct labor are used the first day and four hours of direct labor are worked the second day. All production for the week is accumulated and shipped out to the distributor by train on Saturday.

Warm Glo manufactures the basic economy furnace in a dedicated flow line using just-in-time production principles. All raw materials and purchased parts needed to assemble a complete furnace are delivered to the plant by 8:00 am of the day the furnace begins production. While each furnace requires eight direct labor hours, total throughput time for each furnace is two working days (16 hours). The difference between total throughput time and the eight direct labor hours is waiting time. Furnaces that are started in production one day are finished the next day. Four hours of direct labor are used the first day and four hours of direct labor are worked the second day. All production for the week is accumulated and shipped out to the distributor by train on Saturday.

Warm Glo maintains a finished-goods inventory account for basic economy furnaces that reflects the standard cost of furnaces not yet shipped out. Warm Glo uses a raw and in-process materials account (RIP) and JIT backflushing accounting. All accounts are updated at the end of each day for all production and transactions occurring that day. Conversion costs are charged directly to the finished goods inventory account as work is performed on furnaces. Through the end of Thursday of the current week the following table contains information about the plant's production of basic economy furnaces: Required:

Required:

a. What is the balance in the RIP account for the basic economy model at the end of Thursday?

b. What is the balance in the finished goods account (basic economy model) at the end of Thursday?

Warm Glo manufactures gas furnaces for residential use. It uses a standard cost system that isolates all variances at purchase so that all product costs are stated at standard cost. All variances are included as part of cost of goods sold. Overhead is allocated based on direct labor hours. Standard cost for the basic economy model furnace follows.

Warm Glo manufactures the basic economy furnace in a dedicated flow line using just-in-time production principles. All raw materials and purchased parts needed to assemble a complete furnace are delivered to the plant by 8:00 am of the day the furnace begins production. While each furnace requires eight direct labor hours, total throughput time for each furnace is two working days (16 hours). The difference between total throughput time and the eight direct labor hours is waiting time. Furnaces that are started in production one day are finished the next day. Four hours of direct labor are used the first day and four hours of direct labor are worked the second day. All production for the week is accumulated and shipped out to the distributor by train on Saturday.Warm Glo maintains a finished-goods inventory account for basic economy furnaces that reflects the standard cost of furnaces not yet shipped out. Warm Glo uses a raw and in-process materials account (RIP) and JIT backflushing accounting. All accounts are updated at the end of each day for all production and transactions occurring that day. Conversion costs are charged directly to the finished goods inventory account as work is performed on furnaces. Through the end of Thursday of the current week the following table contains information about the plant's production of basic economy furnaces:

Required:a. What is the balance in the RIP account for the basic economy model at the end of Thursday?

b. What is the balance in the finished goods account (basic economy model) at the end of Thursday?

سؤال

سؤال

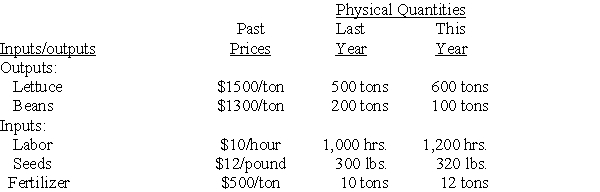

Productivity Measures With Multiple Inputs and Outputs

A farmer grows two crops: lettuce and beans. The farmer uses three inputs: labor, seed, and fertilizer. The past prices and the quantities of each are given in the following tables: Required:

Required:

a. Calculate productivity measures for last year and this year using past prices.

b. Calculate the percentage change in productivity.

A farmer grows two crops: lettuce and beans. The farmer uses three inputs: labor, seed, and fertilizer. The past prices and the quantities of each are given in the following tables:

Required:a. Calculate productivity measures for last year and this year using past prices.

b. Calculate the percentage change in productivity.

فتح الحزمة

قم بالتسجيل لفتح البطاقات في هذه المجموعة!

Unlock Deck

Unlock Deck

1/66

العب

ملء الشاشة (f)

Deck 1: Accounting for Decision Making and Control

1

Cost-volume-profit of a Make/buy Decision

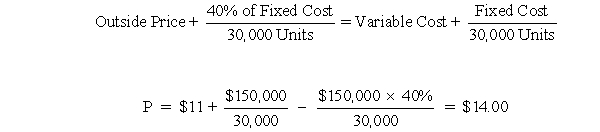

Elly Industries is a multiproduct company that currently manufactures 30,000 units of Part MR24 each month for use in production. The facilities now being used to produce Part MR24 have affixed monthly cost of $150,000 and a capacity to produce 84,000 units per month. If Elly were to buy Part MR24 from an outside supplier, the facilities would be idle, but its fixed costs would continue at 40 percent of its present amount. The variable production costs of Part MR24 are $11 per unit.

Required:

a. If Elly Industries continues to use 30,000 units of Part MR24 each month, it would realize a net benefit by purchasing Part MR24 from an outside supplier only if the supplier's unit price is less than how much?

b. If Elly Industries can obtain Part MR24 from an outside supplier at a unit purchase price of $12.875, what is the monthly usage at which it will be indifferent between purchasing and making Part MR24?

Source: CMA adapted

Elly Industries is a multiproduct company that currently manufactures 30,000 units of Part MR24 each month for use in production. The facilities now being used to produce Part MR24 have affixed monthly cost of $150,000 and a capacity to produce 84,000 units per month. If Elly were to buy Part MR24 from an outside supplier, the facilities would be idle, but its fixed costs would continue at 40 percent of its present amount. The variable production costs of Part MR24 are $11 per unit.

Required:

a. If Elly Industries continues to use 30,000 units of Part MR24 each month, it would realize a net benefit by purchasing Part MR24 from an outside supplier only if the supplier's unit price is less than how much?

b. If Elly Industries can obtain Part MR24 from an outside supplier at a unit purchase price of $12.875, what is the monthly usage at which it will be indifferent between purchasing and making Part MR24?

Source: CMA adapted

Cost-Volume-Profit of a Make/Buy Decision

a. Each month Elly incurs $150,000 of fixed cost to have capacity to produce 84,000 units. They are only using 30,000 units of that capacity now. If they outsource MR24, they will continue to incur 40% of the fixed costs, or $60,000. However, they save $90,000 ($150,000 - $60,000). Besides saving the fixed costs they save $330,000 of variable costs ($11 × 30,000) or a total cost savings of $420,000. To be indifferent between outsourcing and continuing to produce, the outside price must be $14 ($420,000 ÷ 30,000). An alternative way to solve the problem and get the same answer is: b. $12.875 +

b. $12.875 +  $12.875Q + $60,000 = $11Q + $150,000

$12.875Q + $60,000 = $11Q + $150,000

$1.875Q = $90,000

Q = 48,000 units

a. Each month Elly incurs $150,000 of fixed cost to have capacity to produce 84,000 units. They are only using 30,000 units of that capacity now. If they outsource MR24, they will continue to incur 40% of the fixed costs, or $60,000. However, they save $90,000 ($150,000 - $60,000). Besides saving the fixed costs they save $330,000 of variable costs ($11 × 30,000) or a total cost savings of $420,000. To be indifferent between outsourcing and continuing to produce, the outside price must be $14 ($420,000 ÷ 30,000). An alternative way to solve the problem and get the same answer is:

b. $12.875 + $12.875Q + $60,000 = $11Q + $150,000$1.875Q = $90,000

Q = 48,000 units

2

Choosing Performance Measures

Jen and Barry opened an ice cream shop in Eugene. It was a big success, so they decide to open a ice cream shops in many cities including Portland. They hire Dante to manage the shop in Portland. Jen and Barry are considering two different sets of performance measures for Dante. The first set would grade Dante based on the cleanliness of the restaurant and customer service. The second set would use accounting numbers including the profit of the shop in Portland.

What are the advantages and disadvantages of each set of performance measures?

Jen and Barry opened an ice cream shop in Eugene. It was a big success, so they decide to open a ice cream shops in many cities including Portland. They hire Dante to manage the shop in Portland. Jen and Barry are considering two different sets of performance measures for Dante. The first set would grade Dante based on the cleanliness of the restaurant and customer service. The second set would use accounting numbers including the profit of the shop in Portland.

What are the advantages and disadvantages of each set of performance measures?

Choosing Performance Measures

Cleanliness and customer service are important to the success of the ice cream shop. The advantage of using cleanliness and customer service as performance measures is to motivate managers to make the business appealing to customers. Customers will be more likely to return and frequent other outlets of the company. Another advantage of using cleanliness and customer service as performance measures is their controllability by the manager. The disadvantage of using cleanliness and customer service as performance measures is that managers may ignore the costs of providing customer service. Without some measure of cost or profit as part of the manager's performance measure, a manager will be less likely to make the appropriate cost/benefit trade-off.

The benefit of using profit as a performance measure is that profit tends to include all aspects of operating the business. To improve profit, the manager should also be motivated to improve customer service because profit will increase with satisfied customers. If revenues and costs are accurately measured, then managers will make the appropriate cost/benefit trade-offs if evaluated on profit. One disadvantage of using profit as a performance measure is that profit is not completely controllable by the manager. There are uncontrollable environmental factors, such as the economy of Portland, that affect profit. Also, revenues and costs may not be appropriately measured in the short-run. If costs used to calculate profit don't reflect the opportunity cost, the manager may be motivated to make inappropriate decisions, such as postponing maintenance.

Cleanliness and customer service are important to the success of the ice cream shop. The advantage of using cleanliness and customer service as performance measures is to motivate managers to make the business appealing to customers. Customers will be more likely to return and frequent other outlets of the company. Another advantage of using cleanliness and customer service as performance measures is their controllability by the manager. The disadvantage of using cleanliness and customer service as performance measures is that managers may ignore the costs of providing customer service. Without some measure of cost or profit as part of the manager's performance measure, a manager will be less likely to make the appropriate cost/benefit trade-off.

The benefit of using profit as a performance measure is that profit tends to include all aspects of operating the business. To improve profit, the manager should also be motivated to improve customer service because profit will increase with satisfied customers. If revenues and costs are accurately measured, then managers will make the appropriate cost/benefit trade-offs if evaluated on profit. One disadvantage of using profit as a performance measure is that profit is not completely controllable by the manager. There are uncontrollable environmental factors, such as the economy of Portland, that affect profit. Also, revenues and costs may not be appropriately measured in the short-run. If costs used to calculate profit don't reflect the opportunity cost, the manager may be motivated to make inappropriate decisions, such as postponing maintenance.

3

Cost, Volume, Profit Analysis

With the possibility of the US Congress relaxing restrictions on cutting old growth, a local lumber company is considering an expansion of its facilities. The company believes it can sell lumber for $0.18/board foot. A board foot is a measure of lumber. The tax rate for the company is 30 percent. The company has the following two opportunities:

• Build Factory A with annual fixed costs of $20 million and variable costs of $0.10/board foot. This factory has an annual capacity of 500 million board feet.

• Build Factory B with annual fixed costs of $10 million and variable costs of $0.12/board foot. This factory has an annual capacity of 300 million board feet.

Required:

a. What is the break-even point in board feet for Factory A?

b. If the company wants to generate an after tax profit of $2 million with Factory B, how many board feet would the company have to process and sell?

c. If demand for lumber is uncertain, which factory is riskier?

d. At what level of board feet would the after-tax profit of the two factories be the same?

With the possibility of the US Congress relaxing restrictions on cutting old growth, a local lumber company is considering an expansion of its facilities. The company believes it can sell lumber for $0.18/board foot. A board foot is a measure of lumber. The tax rate for the company is 30 percent. The company has the following two opportunities:

• Build Factory A with annual fixed costs of $20 million and variable costs of $0.10/board foot. This factory has an annual capacity of 500 million board feet.

• Build Factory B with annual fixed costs of $10 million and variable costs of $0.12/board foot. This factory has an annual capacity of 300 million board feet.

Required:

a. What is the break-even point in board feet for Factory A?

b. If the company wants to generate an after tax profit of $2 million with Factory B, how many board feet would the company have to process and sell?

c. If demand for lumber is uncertain, which factory is riskier?

d. At what level of board feet would the after-tax profit of the two factories be the same?

Cost, Volume, Profit Analysis

a. Break-even point of Factory A = $20,000,000/($0.18 - $0.10) = 250,000,000 board-feet

b. To achieve an after-tax profit of $2,000,000:

[$10,000,000 + ($2,000,000/(1 - .3))]/($0.18 - $0.12) = 14,285,717 board-feet

c. Factory A has higher fixed costs, but lower variable costs per unit because of its larger capacity. If the demand for lumber is lower than expected, Factory A will have a more difficult time recovering its fixed costs. The break-even point for factory B is lower than the break-even point for factory

RRR

a. Break-even point of Factory A = $20,000,000/($0.18 - $0.10) = 250,000,000 board-feet

b. To achieve an after-tax profit of $2,000,000:

[$10,000,000 + ($2,000,000/(1 - .3))]/($0.18 - $0.12) = 14,285,717 board-feet

c. Factory A has higher fixed costs, but lower variable costs per unit because of its larger capacity. If the demand for lumber is lower than expected, Factory A will have a more difficult time recovering its fixed costs. The break-even point for factory B is lower than the break-even point for factory

RRR

4

Financing Charges and Net Present Value

The president of the company is not convinced that the interest expense should be excluded from the calculation of the net present value. He points out that, "Interest is a cash flow. You are supposed to discount cash flows. We borrowed money to completely finance this project. Why not discount interest expenditures?" The president is so convinced that he asks you, the controller, to calculate the net present value including the interest expense.

How can you adjust the net present value analysis to compensate for the inclusion of the interest expense?

The president of the company is not convinced that the interest expense should be excluded from the calculation of the net present value. He points out that, "Interest is a cash flow. You are supposed to discount cash flows. We borrowed money to completely finance this project. Why not discount interest expenditures?" The president is so convinced that he asks you, the controller, to calculate the net present value including the interest expense.

How can you adjust the net present value analysis to compensate for the inclusion of the interest expense?

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 66 في هذه المجموعة.

فتح الحزمة

k this deck

5

Fixed and Variable Costs

The university athletic department has been asked to host a professional basketball game at the campus sports center. The athletic director must estimate the opportunity cost of holding the event at the sports center. The only other event scheduled for the sports center that evening is a fencing match that would not have generated any additional costs or revenues. The fencing match can be held at the local high school, but the rental cost of the high school gym would be $200. The athletic director estimates that the professional basketball game will require 20 hours of labor to prepare the building. Clean-up depends on the number of spectators. The athletic director estimates the time of clean-up to be equal to 2 minutes per spectator. The labor would be hired especially for the basketball game and would cost $8 per hour. Utilities will be $500 greater if the basketball game is held at the sports center. All other costs would be covered by the professional basketball team.

Required:

a. What is the variable cost of having one more spectator?

b. What is the opportunity cost of allowing the professional basketball team to use the sports center if 10,000 spectators are expected?

c. What is the opportunity cost of allowing the professional basketball team to use the sports center if 12,000 spectators are expected?

The university athletic department has been asked to host a professional basketball game at the campus sports center. The athletic director must estimate the opportunity cost of holding the event at the sports center. The only other event scheduled for the sports center that evening is a fencing match that would not have generated any additional costs or revenues. The fencing match can be held at the local high school, but the rental cost of the high school gym would be $200. The athletic director estimates that the professional basketball game will require 20 hours of labor to prepare the building. Clean-up depends on the number of spectators. The athletic director estimates the time of clean-up to be equal to 2 minutes per spectator. The labor would be hired especially for the basketball game and would cost $8 per hour. Utilities will be $500 greater if the basketball game is held at the sports center. All other costs would be covered by the professional basketball team.

Required:

a. What is the variable cost of having one more spectator?

b. What is the opportunity cost of allowing the professional basketball team to use the sports center if 10,000 spectators are expected?

c. What is the opportunity cost of allowing the professional basketball team to use the sports center if 12,000 spectators are expected?

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 66 في هذه المجموعة.

فتح الحزمة

k this deck

6

Monitoring Computer Use

Samson Company is an engineering firm. Many of the employees are engineers who are working individually on different projects. Most of the design work takes place on computers. The computers are connected by a network and employees can also "surf" the internet through their desk top computers.

The president is concerned about productivity among his engineers. He has acquired software that allows him to monitor each engineer's computer work. At anytime during the day, the president can observe on her screen exactly what the different engineers are working on. The engineers are quite unhappy with this monitoring process. They feel it is unethical for the president to be able to access what they are working on without their knowledge.

Describe the pros and cons of monitoring through observing the computer work of the engineers.

Samson Company is an engineering firm. Many of the employees are engineers who are working individually on different projects. Most of the design work takes place on computers. The computers are connected by a network and employees can also "surf" the internet through their desk top computers.

The president is concerned about productivity among his engineers. He has acquired software that allows him to monitor each engineer's computer work. At anytime during the day, the president can observe on her screen exactly what the different engineers are working on. The engineers are quite unhappy with this monitoring process. They feel it is unethical for the president to be able to access what they are working on without their knowledge.

Describe the pros and cons of monitoring through observing the computer work of the engineers.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 66 في هذه المجموعة.

فتح الحزمة

k this deck

7

Opportunity Costs

The First Church has been asked to operate a homeless shelter in part of the church. To operate a homeless shelter the church would have to hire a full time employee for $1,200/month to manage the shelter. In addition, the church would have to purchase $400 of supplies/month for the people using the shelter. The space that would be used by the shelter is rented for wedding parties. The church averages about 5 wedding parties a month that pay rent of $200 per party. Utilities are normally $1,000 per month. With the homeless shelter, the utilities will increase to $1,300 per month.

What is the opportunity cost to the church of operating a homeless shelter in the church?

The First Church has been asked to operate a homeless shelter in part of the church. To operate a homeless shelter the church would have to hire a full time employee for $1,200/month to manage the shelter. In addition, the church would have to purchase $400 of supplies/month for the people using the shelter. The space that would be used by the shelter is rented for wedding parties. The church averages about 5 wedding parties a month that pay rent of $200 per party. Utilities are normally $1,000 per month. With the homeless shelter, the utilities will increase to $1,300 per month.

What is the opportunity cost to the church of operating a homeless shelter in the church?

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 66 في هذه المجموعة.

فتح الحزمة

k this deck

8

Cost, Volume, Profit Analysis

Kalifo Company manufactures a line of electric garden tools that are sold in general hardware stores. The company's controller, Sylvia Harlow, has just received the sales forecast for the coming year for Kalifo's three products: weeders, hedge clippers, and leaf blowers. Kalifo has experienced considerable variations in sales volumes and variable costs over the past two years, and Harlow believes the forecast should be carefully evaluated from a cost-volume-profit viewpoint. The preliminary budget information for 1996 is presented below. For 1996, Kalifo's fixed factory overhead is budgeted at $2 million, and the company's fixed selling and administrative expenses are forecast to be $600,000. Kalifo has a tax rate of 40 percent.

Required:

a. Determine Kalifo Co.'s budgeted net income for 1996.

b. Assuming that the sales mix remains as budgeted, determine how many units of each product Kalifo must sell in order to break even in 1996.

c. Determine the total dollar sales Kalifo must sell in 1996 in order to earn an after-tax net income of $450,000.

d. After preparing the original estimates, Kalifo determines that its variable manufacturing cost of leaf blowers will increase 20 percent and the variable selling cost of hedge clippers can be expected to increase $1 per unit. However, Kalifo has decided not to change the selling price of either product. In addition, Kalifo learns that its leaf blower is perceived as the best value on the market, and it can expect to sell three times as many leaf blowers as any other product. Under these circumstances, determine how many units of each product Kalifo will have to sell to break even in 1996.

e. Explain the limitations of cost-volume-profit analysis that Sylvia Harlow should consider when evaluating Kalifo's 1996 budget.

Kalifo Company manufactures a line of electric garden tools that are sold in general hardware stores. The company's controller, Sylvia Harlow, has just received the sales forecast for the coming year for Kalifo's three products: weeders, hedge clippers, and leaf blowers. Kalifo has experienced considerable variations in sales volumes and variable costs over the past two years, and Harlow believes the forecast should be carefully evaluated from a cost-volume-profit viewpoint. The preliminary budget information for 1996 is presented below.

For 1996, Kalifo's fixed factory overhead is budgeted at $2 million, and the company's fixed selling and administrative expenses are forecast to be $600,000. Kalifo has a tax rate of 40 percent.Required:

a. Determine Kalifo Co.'s budgeted net income for 1996.

b. Assuming that the sales mix remains as budgeted, determine how many units of each product Kalifo must sell in order to break even in 1996.

c. Determine the total dollar sales Kalifo must sell in 1996 in order to earn an after-tax net income of $450,000.

d. After preparing the original estimates, Kalifo determines that its variable manufacturing cost of leaf blowers will increase 20 percent and the variable selling cost of hedge clippers can be expected to increase $1 per unit. However, Kalifo has decided not to change the selling price of either product. In addition, Kalifo learns that its leaf blower is perceived as the best value on the market, and it can expect to sell three times as many leaf blowers as any other product. Under these circumstances, determine how many units of each product Kalifo will have to sell to break even in 1996.

e. Explain the limitations of cost-volume-profit analysis that Sylvia Harlow should consider when evaluating Kalifo's 1996 budget.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 66 في هذه المجموعة.

فتح الحزمة

k this deck

9

Identifying the Opportunity Cost of Capital

Don Phelps recently started a dry cleaning business. He would like to expand the business and have a coin-operated laundry also. The expansion of the building and the washing and drying machines will cost $100,000. The bank will lend the business $100,000 at 12 percent interest rate. Don could get a 10 percent interest rate loan if he uses his personal house as collateral. The lower interest rate reflects the increased security of the loan to the bank, because the bank could take Don's home if he doesn't pay back the loan. Don currently can put money in the bank and receive 6 percent interest.

Required:

Provide arguments for using 12 percent, 10 percent, and 6 percent as the opportunity cost of capital for evaluating the investment.

Don Phelps recently started a dry cleaning business. He would like to expand the business and have a coin-operated laundry also. The expansion of the building and the washing and drying machines will cost $100,000. The bank will lend the business $100,000 at 12 percent interest rate. Don could get a 10 percent interest rate loan if he uses his personal house as collateral. The lower interest rate reflects the increased security of the loan to the bank, because the bank could take Don's home if he doesn't pay back the loan. Don currently can put money in the bank and receive 6 percent interest.

Required:

Provide arguments for using 12 percent, 10 percent, and 6 percent as the opportunity cost of capital for evaluating the investment.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 66 في هذه المجموعة.

فتح الحزمة

k this deck

10

Choosing Performance Measures

The president of the Canby Insurance Company has just read an article on the balanced scorecard. A company has a balanced scorecard when there is a set of performance measures that reflect the diverse interests and goals of all the stakeholders (shareholders, customers, employees, and society) of the organization. Presently, Canby Insurance Company has only one performance measure for the top executives: profit. The board of directors claims that profit as the sole performance measure is sufficient. If customers are satisfied and employees are productive, then the company will be profitable. Any other performance measure will detract from the basic goal of making a profit.

Required:

Explain the costs and benefits of only having profit as a performance measure.

The president of the Canby Insurance Company has just read an article on the balanced scorecard. A company has a balanced scorecard when there is a set of performance measures that reflect the diverse interests and goals of all the stakeholders (shareholders, customers, employees, and society) of the organization. Presently, Canby Insurance Company has only one performance measure for the top executives: profit. The board of directors claims that profit as the sole performance measure is sufficient. If customers are satisfied and employees are productive, then the company will be profitable. Any other performance measure will detract from the basic goal of making a profit.

Required:

Explain the costs and benefits of only having profit as a performance measure.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 66 في هذه المجموعة.

فتح الحزمة

k this deck

11

Breakeven and Cost-Volume-Profit with Taxes

DisKing Company is a retailer for video disks. The projected after-tax net income for the current year is $120,000 based on a sales volume of 200,000 video disks. DisKing has been selling the disks at $16 each. The variable costs consist of the $10 unit purchase price of the disks and a handling cost of $2 per disk. DisKing's annual fixed costs are $600,000 and DisKing is subject to a 40 percent income tax rate.

Management is planning for the coming year, when it expects that the unit purchase price of the video disks will increase 30 percent.

Required:

a. Calculate DisKing Company's break-even point for the current year in number of video disks.

b. Calculate the increased after-tax income for the current year from an increase of 10 percent in projected unit sales volume.

c. If the unit selling price remains at $16, calculate the volume of sales in dollars that DisKing Company must achieve in the coming year to maintain the same after-tax net income as projected for the current year.

Source: CMA adapted

DisKing Company is a retailer for video disks. The projected after-tax net income for the current year is $120,000 based on a sales volume of 200,000 video disks. DisKing has been selling the disks at $16 each. The variable costs consist of the $10 unit purchase price of the disks and a handling cost of $2 per disk. DisKing's annual fixed costs are $600,000 and DisKing is subject to a 40 percent income tax rate.

Management is planning for the coming year, when it expects that the unit purchase price of the video disks will increase 30 percent.

Required:

a. Calculate DisKing Company's break-even point for the current year in number of video disks.

b. Calculate the increased after-tax income for the current year from an increase of 10 percent in projected unit sales volume.

c. If the unit selling price remains at $16, calculate the volume of sales in dollars that DisKing Company must achieve in the coming year to maintain the same after-tax net income as projected for the current year.

Source: CMA adapted

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 66 في هذه المجموعة.

فتح الحزمة

k this deck

12

Opportunity Cost of Attracting Industry

The Itagi Computer Company From Japan is looking to build a factory for making CD-ROM's in the United States. The company is concerned about the safety and well-being of its employees and wants to locate in a community with good schools. The company also wants the factory to be profitable and is looking for subsidies from potential communities. Encouraging new business to create jobs for citizens is important for communities, especially communities with high unemployment.

Wellville has not been very well since the shoe factory left town. The city officials have been working on a deal with Itagi to get the company to locate in Wellville. Itagi officials have identified a 20 acre undeveloped site. The city has tentatively agreed to buy the site for $50,000 for Itagi and not require any payment of property taxes on the factory by Itagi for the first five years of operation. The property tax deal will save Itagi $3,000,000 in taxes over the five years. This deal was leaked to the local newspaper. The headlines the next day were: "Wellville Gives Away $3,000,000+ to Japanese Company".

Required:

a. Do the headlines accurately describe the deal with Itagi?

b. What are the relevant costs and benefits to the citizens of Wellville of making this deal?

The Itagi Computer Company From Japan is looking to build a factory for making CD-ROM's in the United States. The company is concerned about the safety and well-being of its employees and wants to locate in a community with good schools. The company also wants the factory to be profitable and is looking for subsidies from potential communities. Encouraging new business to create jobs for citizens is important for communities, especially communities with high unemployment.

Wellville has not been very well since the shoe factory left town. The city officials have been working on a deal with Itagi to get the company to locate in Wellville. Itagi officials have identified a 20 acre undeveloped site. The city has tentatively agreed to buy the site for $50,000 for Itagi and not require any payment of property taxes on the factory by Itagi for the first five years of operation. The property tax deal will save Itagi $3,000,000 in taxes over the five years. This deal was leaked to the local newspaper. The headlines the next day were: "Wellville Gives Away $3,000,000+ to Japanese Company".

Required:

a. Do the headlines accurately describe the deal with Itagi?

b. What are the relevant costs and benefits to the citizens of Wellville of making this deal?

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 66 في هذه المجموعة.

فتح الحزمة

k this deck

13

Annuity

Suppose the opportunity cost of capital is 10 percent and you have just won a $1 million lottery that entitles you to $100,000 at the end of each of the next ten years.

Required:

a. What is the minimum lump sum cash payment you would be willing to take now in lieu of the ten-year annuity?

b. What is the minimum lump sum you would be willing to accept at the end of the ten years in lieu of the annuity?

c. Suppose three years have passed and you have just received the third payment and you have seven left when the lottery promoters approach you with an offer to "settle-up for cash." What is the minimum you would accept (the end of year three)?

d. How would your answer to part (a) change if the first payment came immediately (at t = 0) and the remaining payments were at the beginning instead of at the end of each year?

Suppose the opportunity cost of capital is 10 percent and you have just won a $1 million lottery that entitles you to $100,000 at the end of each of the next ten years.

Required:

a. What is the minimum lump sum cash payment you would be willing to take now in lieu of the ten-year annuity?

b. What is the minimum lump sum you would be willing to accept at the end of the ten years in lieu of the annuity?

c. Suppose three years have passed and you have just received the third payment and you have seven left when the lottery promoters approach you with an offer to "settle-up for cash." What is the minimum you would accept (the end of year three)?

d. How would your answer to part (a) change if the first payment came immediately (at t = 0) and the remaining payments were at the beginning instead of at the end of each year?

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 66 في هذه المجموعة.

فتح الحزمة

k this deck

14

Linking Decision Rights and Knowledge

Professional football teams have both a coach and a general manager. The general manager is usually responsible for the general operations of the organization and maintains the decision rights for selecting personnel on the football team. The coach is responsible for the training of the football team and making decisions on game day. Many coaches have been unhappy with their relationship with the general manager and feel they should have more decision rights in choosing the players on the team. Some of the top coaches are now insisting on also being general managers.