Deck 16: Accounting for Income Taxes

ملء الشاشة (f)

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

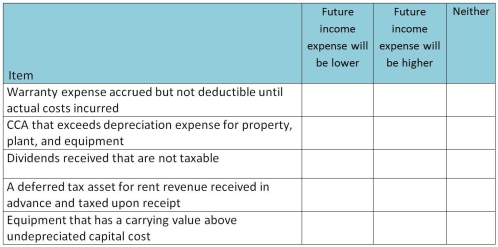

Indicate whether the item would result in future income taxes being higher,future income taxes being lower or neither:

سؤال

سؤال

For each of the following differences between the amount of taxable income and income recorded for financial reporting purposes,compute the effect of each difference on deferred taxes balances on the balance sheet.Treat each item independently of the others.Assume a tax rate of 25%.

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

For each of the following differences between the amount of taxable income and income recorded for financial reporting purposes,compute the effect of each difference on deferred taxes balances on the balance sheet.Treat each item independently of the others.Assume a tax rate of 30%.

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

فتح الحزمة

قم بالتسجيل لفتح البطاقات في هذه المجموعة!

Unlock Deck

Unlock Deck

1/85

العب

ملء الشاشة (f)

Deck 16: Accounting for Income Taxes

1

What is the deferred tax liability under the deferral method for F2014?

A)$3,750

B)$23,750

C)$27,500

D)$36,000

A)$3,750

B)$23,750

C)$27,500

D)$36,000

$3,750

2

Which statement is not correct?

A)The accrual method focuses on the balance sheet.

B)The deferral method focuses on the income statement.

C)The deferral methods matches tax expense to the balance sheet.

D)The accrual and deferral methods are both tax allocation methods.

A)The accrual method focuses on the balance sheet.

B)The deferral method focuses on the income statement.

C)The deferral methods matches tax expense to the balance sheet.

D)The accrual and deferral methods are both tax allocation methods.

C

3

What is the tax expense under the deferral method for F2015?

A)$27,500

B)$36,000

C)$36,750

D)$52,500

A)$27,500

B)$36,000

C)$36,750

D)$52,500

$52,500

4

Which method does not use "temporary differences" to account for income tax expense?

A)The taxes payable method.

B)The deferral method.

C)The accrual method.

D)The tax allocation method.

A)The taxes payable method.

B)The deferral method.

C)The accrual method.

D)The tax allocation method.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 85 في هذه المجموعة.

فتح الحزمة

k this deck

5

What is one reason to use the taxes payable method?

A)It is a complicated method,but results in the least tax expense.

B)A company only pays tax once a year under this method.

C)It results in the best matching for the balance sheet.

D)It is the least costly method for tax accounting.

A)It is a complicated method,but results in the least tax expense.

B)A company only pays tax once a year under this method.

C)It results in the best matching for the balance sheet.

D)It is the least costly method for tax accounting.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 85 في هذه المجموعة.

فتح الحزمة

k this deck

6

What is the income tax payable under the deferral method for F2013?

A)$25,500

B)$30,000

C)$30,750

D)$36,000

A)$25,500

B)$30,000

C)$30,750

D)$36,000

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 85 في هذه المجموعة.

فتح الحزمة

k this deck

7

How much tax would be reported under the taxes payable method for F2015?

A)25,500

B)31,500

C)33,750

D)36,000

A)25,500

B)31,500

C)33,750

D)36,000

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 85 في هذه المجموعة.

فتح الحزمة

k this deck

8

What is the income tax payable under the deferral method for F2014?

A)$23,750

B)$25,500

C)$27,500

D)$36,000

A)$23,750

B)$25,500

C)$27,500

D)$36,000

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 85 في هذه المجموعة.

فتح الحزمة

k this deck

9

Which statement is accurate?

A)Accounting income is generally higher than taxable income.

B)Accounting income is determined by financial reporting.

C)The balance sheet is unaffected by the tax accounting method.

D)The taxes payable method is a "tax allocation" approach.

A)Accounting income is generally higher than taxable income.

B)Accounting income is determined by financial reporting.

C)The balance sheet is unaffected by the tax accounting method.

D)The taxes payable method is a "tax allocation" approach.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 85 في هذه المجموعة.

فتح الحزمة

k this deck

10

What is the income tax payable under the deferral method for F2015?

A)$27,500

B)$36,000

C)$36,750

D)$52,500

A)$27,500

B)$36,000

C)$36,750

D)$52,500

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 85 في هذه المجموعة.

فتح الحزمة

k this deck

11

Which accurately describes the purpose of the taxes payable method?

A)It represents the amount of income recognized for accounting purposes.

B)It represents the amount of income recognized for tax purposes.

C)It calculates tax expense based on the accounting income before tax.

D)It calculates tax expense based on the amount payable to tax authorities.

A)It represents the amount of income recognized for accounting purposes.

B)It represents the amount of income recognized for tax purposes.

C)It calculates tax expense based on the accounting income before tax.

D)It calculates tax expense based on the amount payable to tax authorities.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 85 في هذه المجموعة.

فتح الحزمة

k this deck

12

How much tax would be reported under the taxes payable method for F2014?

A)23,750

B)25,500

C)27,500

D)36,000

A)23,750

B)25,500

C)27,500

D)36,000

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 85 في هذه المجموعة.

فتح الحزمة

k this deck

13

Which statement best describes the "deferral method"?

A)This method focuses on the balance sheet.

B)This method is an example of a "tax allocation" approach.

C)This is the same as the "accrual method" of tax accounting.

D)This method is used by companies reporting using IFRS.

A)This method focuses on the balance sheet.

B)This method is an example of a "tax allocation" approach.

C)This is the same as the "accrual method" of tax accounting.

D)This method is used by companies reporting using IFRS.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 85 في هذه المجموعة.

فتح الحزمة

k this deck

14

Which statement is correct?

A)Financial reporting rules are generally consistent with tax reporting rules.

B)Tax rules are generally consistent the principles used in accrual accounting.

C)Tax rules generally require a higher degree of reliability than financial reporting.

D)Accounting income is generally similar to taxable income.

A)Financial reporting rules are generally consistent with tax reporting rules.

B)Tax rules are generally consistent the principles used in accrual accounting.

C)Tax rules generally require a higher degree of reliability than financial reporting.

D)Accounting income is generally similar to taxable income.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 85 في هذه المجموعة.

فتح الحزمة

k this deck

15

What is the tax expense under the deferral method for F2014?

A)$23,750

B)$25,500

C)$27,500

D)$36,000

A)$23,750

B)$25,500

C)$27,500

D)$36,000

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 85 في هذه المجموعة.

فتح الحزمة

k this deck

16

Which statement is accurate?

A)The taxes payable method is also known as the "deferral method."

B)The deferral method and the accrual method are "tax allocation" approaches.

C)The income statement approach is also known as the "accrual method."

D)The balance sheet approach is also known as the "deferral method."

A)The taxes payable method is also known as the "deferral method."

B)The deferral method and the accrual method are "tax allocation" approaches.

C)The income statement approach is also known as the "accrual method."

D)The balance sheet approach is also known as the "deferral method."

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 85 في هذه المجموعة.

فتح الحزمة

k this deck

17

Which statement is correct about the "taxes payable method"?

A)It is the accounting method used under both ASPE and IFRS.

B)It records an amount for income tax equal to the tax payments required.

C)It matches income with the associated income tax expense.

D)It records an amount for income tax equal to the net income before tax.

A)It is the accounting method used under both ASPE and IFRS.

B)It records an amount for income tax equal to the tax payments required.

C)It matches income with the associated income tax expense.

D)It records an amount for income tax equal to the net income before tax.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 85 في هذه المجموعة.

فتح الحزمة

k this deck

18

What is the tax expense under the deferral method for F2013?

A)$25,500

B)$30,000

C)$30,750

D)$36,000

A)$25,500

B)$30,000

C)$30,750

D)$36,000

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 85 في هذه المجموعة.

فتح الحزمة

k this deck

19

Which method reflects the tax effect in the period that tax is payable?

A)Accrual method.

B)Taxes payable method.

C)Deferral method.

D)Tax allocation method.

A)Accrual method.

B)Taxes payable method.

C)Deferral method.

D)Tax allocation method.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 85 في هذه المجموعة.

فتح الحزمة

k this deck

20

What is the deferred tax liability under the deferral method for F2013?

A)$10,500

B)$25,500

C)$30,750

D)$36,000

A)$10,500

B)$25,500

C)$30,750

D)$36,000

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 85 في هذه المجموعة.

فتح الحزمة

k this deck

21

A company earns $390,000 in pre-tax income,while its tax return shows taxable income of $280,000.At a tax rate of 35%,how much is the income tax expense under the taxes payable method permitted under ASPE?

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 85 في هذه المجموعة.

فتح الحزمة

k this deck

22

A company earns $490,000 in pre-tax income,while its tax return shows taxable income of $380,000.At a tax rate of 35%,how much is the income tax expense under the taxes payable method permitted under ASPE?

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 85 في هذه المجموعة.

فتح الحزمة

k this deck

23

Under the accrual method,what is the effect of the tax rate change in F2015?

A)Increase of 11,000.

B)Decrease of 11,000.

C)Decrease of 62,500.

D)Increase of 63,500.

A)Increase of 11,000.

B)Decrease of 11,000.

C)Decrease of 62,500.

D)Increase of 63,500.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 85 في هذه المجموعة.

فتح الحزمة

k this deck

24

Under the accrual method,what is the effect of the tax rate change in F2014?

A)Increase of 5,000.

B)Decrease of 5,000.

C)Increase of 32,500.

D)Decrease of 32,500.

A)Increase of 5,000.

B)Decrease of 5,000.

C)Increase of 32,500.

D)Decrease of 32,500.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 85 في هذه المجموعة.

فتح الحزمة

k this deck

25

How much tax expense would be recorded under the accrual method for F2014?

A)5,000

B)27,500

C)32,500

D)37,500

A)5,000

B)27,500

C)32,500

D)37,500

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 85 في هذه المجموعة.

فتح الحزمة

k this deck

26

Under the accrual method,what is the effect of the current year temporary difference in F2014?

A)4,500

B)30,500

C)35,000

D)39,500

A)4,500

B)30,500

C)35,000

D)39,500

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 85 في هذه المجموعة.

فتح الحزمة

k this deck

27

Which of the following is not an example of a "temporary difference"?

A)Membership fees that are not deductible.

B)Advances received on rent revenue.

C)Percentage of completion method.

D)Fair value decrease on biological assets.

A)Membership fees that are not deductible.

B)Advances received on rent revenue.

C)Percentage of completion method.

D)Fair value decrease on biological assets.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 85 في هذه المجموعة.

فتح الحزمة

k this deck

28

Under the accrual method,what is the effect of the current year temporary difference in F2014?

A)5,000

B)27,500

C)32,500

D)37,500

A)5,000

B)27,500

C)32,500

D)37,500

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 85 في هذه المجموعة.

فتح الحزمة

k this deck

29

Which statement is correct?

A)The deferral and accrual methods produce the same tax expense when tax rates are constant.

B)The deferral method applies new tax rates to accumulated tax balances.

C)The accrual method applies new tax rates to only to current year's income.

D)The deferral and accrual methods produce the same tax expense when tax rates are falling.

A)The deferral and accrual methods produce the same tax expense when tax rates are constant.

B)The deferral method applies new tax rates to accumulated tax balances.

C)The accrual method applies new tax rates to only to current year's income.

D)The deferral and accrual methods produce the same tax expense when tax rates are falling.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 85 في هذه المجموعة.

فتح الحزمة

k this deck

30

How much tax expense would be recorded under the accrual method for F2014?

A)5,000

B)27,500

C)32,500

D)37,500

A)5,000

B)27,500

C)32,500

D)37,500

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 85 في هذه المجموعة.

فتح الحزمة

k this deck

31

How much tax expense would be recorded under the accrual method for F2015?

A)11,000

B)42,500

C)52,500

D)63,500

A)11,000

B)42,500

C)52,500

D)63,500

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 85 في هذه المجموعة.

فتح الحزمة

k this deck

32

Under the accrual method,what is the tax expense in F2014?

A)4,500

B)30,500

C)35,000

D)39,500

A)4,500

B)30,500

C)35,000

D)39,500

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 85 في هذه المجموعة.

فتح الحزمة

k this deck

33

SEG Company reported $490,000 in income tax expense for the year under the accrual method.Its balance sheet reported an overall increase in deferred income tax liability of $20,000 and a decrease in income tax payable of $25,000.How much would SEG report as income tax expense had it used the taxes payable method?

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 85 في هذه المجموعة.

فتح الحزمة

k this deck

34

Under the accrual method,what is the effect of the tax rate change in F2014?

A)Increase of 5,000.

B)Decrease of 5,000.

C)Increase of 27,500.

D)Decrease of 27,500.

A)Increase of 5,000.

B)Decrease of 5,000.

C)Increase of 27,500.

D)Decrease of 27,500.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 85 في هذه المجموعة.

فتح الحزمة

k this deck

35

What is the deferred tax liability under the deferral method for F2015?

A)$52,500

B)$36,750

C)$27,500

D)$15,750

A)$52,500

B)$36,750

C)$27,500

D)$15,750

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 85 في هذه المجموعة.

فتح الحزمة

k this deck

36

Under the accrual method,what is the effect of the current year temporary difference in F2015?

A)11,000

B)42,500

C)52,500

D)63,500

A)11,000

B)42,500

C)52,500

D)63,500

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 85 في هذه المجموعة.

فتح الحزمة

k this deck

37

Which of the following is an example of a "permanent difference"?

A)Warranty provisions.

B)Dividends on corporations.

C)Depreciation on capital assets.

D)Completed contract method.

A)Warranty provisions.

B)Dividends on corporations.

C)Depreciation on capital assets.

D)Completed contract method.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 85 في هذه المجموعة.

فتح الحزمة

k this deck

38

Withering Inc.began operations in 2011.Due to the untimely death of its founder,Edwin Delaney,the company was wound up in 2013.The following table provides information on Withering's income over the three years.

The statutory income tax rate remained at 45% throughout the three years.

Requirement:

a.For each year and for the three years combined,compute the following:

- income tax expense under the taxes payable method;

- the effective tax rate (= tax expense -;- pre-tax income)under the taxes payable method;

- income tax expense under the accrual method;

- effective tax rate under the accrual method.

b.Briefly comment on any differences between the effective tax rates and the statutory rate of 45%.

The statutory income tax rate remained at 45% throughout the three years.

Requirement:

a.For each year and for the three years combined,compute the following:

- income tax expense under the taxes payable method;

- the effective tax rate (= tax expense -;- pre-tax income)under the taxes payable method;

- income tax expense under the accrual method;

- effective tax rate under the accrual method.

b.Briefly comment on any differences between the effective tax rates and the statutory rate of 45%.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 85 في هذه المجموعة.

فتح الحزمة

k this deck

39

What is a "taxable" temporary difference?

A)Results in future taxable income being higher than accounting income.

B)Results in future taxable income being less than accounting income.

C)The amount of income tax payable in the current and future periods.

D)Result of an event affecting accounting and taxable income in different periods.

A)Results in future taxable income being higher than accounting income.

B)Results in future taxable income being less than accounting income.

C)The amount of income tax payable in the current and future periods.

D)Result of an event affecting accounting and taxable income in different periods.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 85 في هذه المجموعة.

فتح الحزمة

k this deck

40

A company facing a 45% tax rate has calculated its taxable income for the year to be $2,100,000.It made installment payments during the year totalling $995,000; this amount has been recorded in an asset account as "income tax installments"

Requirement:

Prepare the journal entry to record the adjusting entry for income taxes at the end of the year under the taxes payable method.

Requirement:

Prepare the journal entry to record the adjusting entry for income taxes at the end of the year under the taxes payable method.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 85 في هذه المجموعة.

فتح الحزمة

k this deck

41

At the beginning of the current fiscal year,Withering Corporation had a deferred income tax liability balance of $20,000,which relates to depreciable assets.During the year,Withering reported the following information:

• Income before income taxes for the year was $300,000 and the tax rate was 45%.

• Depreciation expense was $150,000 and CCA was $130,000.

• Unearned rent revenue was reported at $120,000.Rent revenue is taxable when the cash is received.There was no opening balance in the unearned rent revenue account at the beginning of the year.

• No other items affected deferred tax amounts other than these transactions.

Requirement:

Prepare the journal entry or entries to record income taxes for the year.

• Income before income taxes for the year was $300,000 and the tax rate was 45%.

• Depreciation expense was $150,000 and CCA was $130,000.

• Unearned rent revenue was reported at $120,000.Rent revenue is taxable when the cash is received.There was no opening balance in the unearned rent revenue account at the beginning of the year.

• No other items affected deferred tax amounts other than these transactions.

Requirement:

Prepare the journal entry or entries to record income taxes for the year.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 85 في هذه المجموعة.

فتح الحزمة

k this deck

42

The following information relates to the accounting income for Saskatchewan Real Estate Company (SREC)for the current year ended December 31.

During the year,the company sold one of its buildings with carrying value of $780,000 for proceeds of $1,000,000,resulting in an accounting gain of $220,000.This gain has been included in the pre-tax income figure of $670,000 shown above.For tax purposes,the acquisition cost of the building was $870,000.For purposes of CCA,it is a Class 1 Asset,which treats each building as a separate class.The undepreciated capital cost (VCC)on the building at the time of disposal was $660,000.

Requirement:

Prepare the journal entries to record income taxes for SREC.

During the year,the company sold one of its buildings with carrying value of $780,000 for proceeds of $1,000,000,resulting in an accounting gain of $220,000.This gain has been included in the pre-tax income figure of $670,000 shown above.For tax purposes,the acquisition cost of the building was $870,000.For purposes of CCA,it is a Class 1 Asset,which treats each building as a separate class.The undepreciated capital cost (VCC)on the building at the time of disposal was $660,000.

Requirement:

Prepare the journal entries to record income taxes for SREC.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 85 في هذه المجموعة.

فتح الحزمة

k this deck

43

When will a terminal loss occur?

A)When proceeds of disposal are less than undepreciated capital cost.

B)When proceeds of disposal are between undepreciated capital cost and original cost.

C)When proceeds of disposal are more than undepreciated capital cost.

D)When proceeds of disposal are less than original cost.

A)When proceeds of disposal are less than undepreciated capital cost.

B)When proceeds of disposal are between undepreciated capital cost and original cost.

C)When proceeds of disposal are more than undepreciated capital cost.

D)When proceeds of disposal are less than original cost.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 85 في هذه المجموعة.

فتح الحزمة

k this deck

44

The following summarizes information relating to Gonzalez Corporation's operations for the current year.

Requirement:

Compute the amount of taxes payable and income tax expense for Gonzalez Corporation.

Requirement:

Compute the amount of taxes payable and income tax expense for Gonzalez Corporation.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 85 في هذه المجموعة.

فتح الحزمة

k this deck

45

The following summarizes information relating to Gonzalez Corporation's operations for the current year.

Requirement:

Compute the amount of taxes payable and income tax expense for Gonzalez Corporation.

Requirement:

Compute the amount of taxes payable and income tax expense for Gonzalez Corporation.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 85 في هذه المجموعة.

فتح الحزمة

k this deck

46

Which statement is correct?

A)A deductible temporary difference results in future taxable income being higher than accounting income.

B)A deductible temporary difference results in future taxable income being less than accounting income.

C)A deductible temporary difference refers to the amount of income tax payable in the current

D)A deductible temporary difference results from an event affecting accounting and taxable income in the same periods.

A)A deductible temporary difference results in future taxable income being higher than accounting income.

B)A deductible temporary difference results in future taxable income being less than accounting income.

C)A deductible temporary difference refers to the amount of income tax payable in the current

D)A deductible temporary difference results from an event affecting accounting and taxable income in the same periods.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 85 في هذه المجموعة.

فتح الحزمة

k this deck

47

When will there be a recapture of depreciation?

A)When proceeds of disposal are less than undepreciated capital cost.

B)When proceeds of disposal are between undepreciated capital cost and original cost.

C)When proceeds of disposal are more than undepreciated capital cost.

D)When proceeds of disposal are less than original cost.

A)When proceeds of disposal are less than undepreciated capital cost.

B)When proceeds of disposal are between undepreciated capital cost and original cost.

C)When proceeds of disposal are more than undepreciated capital cost.

D)When proceeds of disposal are less than original cost.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 85 في هذه المجموعة.

فتح الحزمة

k this deck

48

The following information relates to the accounting income for Ontario Uranium Enterprises (QUE)for the current year ended December 31.

During the year,the company sold one of its machines with carrying value of $85,000 for proceeds of $10,000,resulting in an accounting loss of $75,000.This loss has been included in the pre-tax income figure of $850,000 shown above.For tax purposes,the proceeds from the disposal were removed from the undepreciated capital cost (VCC)of Class 8 assets.

The deferred income tax liability account on January 1 had a credit balance of $230,000.This balance is entirely related to property,plant,and equipment (PPE).

Requirement:

Prepare the journal entries to record income taxes for QUE.

During the year,the company sold one of its machines with carrying value of $85,000 for proceeds of $10,000,resulting in an accounting loss of $75,000.This loss has been included in the pre-tax income figure of $850,000 shown above.For tax purposes,the proceeds from the disposal were removed from the undepreciated capital cost (VCC)of Class 8 assets.

The deferred income tax liability account on January 1 had a credit balance of $230,000.This balance is entirely related to property,plant,and equipment (PPE).

Requirement:

Prepare the journal entries to record income taxes for QUE.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 85 في هذه المجموعة.

فتح الحزمة

k this deck

49

A company has income before tax of $200,000.The company also has a temporary difference of $80,000 relating to capital cost allowance (CCA)in excess of depreciation expense recorded for the year.There are no other permanent or temporary differences.The income tax rate is 40%.

Requirement:

Compute the amount of taxes payable and income tax expense.

Requirement:

Compute the amount of taxes payable and income tax expense.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 85 في هذه المجموعة.

فتح الحزمة

k this deck

50

Indicate whether the item would result in future income taxes being higher,future income taxes being lower or neither:

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 85 في هذه المجموعة.

فتح الحزمة

k this deck

51

What is a deferred tax asset?

A)A deductible temporary difference that results in future taxable income being less than accounting income.

B)The amount of income tax recoverable in future periods as a result of deductible temporary differences.

C)A deductible temporary difference that results in future taxable income being higher than accounting income.

D)The amount of income tax payable in future periods as a result of taxable temporary differences.

A)A deductible temporary difference that results in future taxable income being less than accounting income.

B)The amount of income tax recoverable in future periods as a result of deductible temporary differences.

C)A deductible temporary difference that results in future taxable income being higher than accounting income.

D)The amount of income tax payable in future periods as a result of taxable temporary differences.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 85 في هذه المجموعة.

فتح الحزمة

k this deck

52

For each of the following differences between the amount of taxable income and income recorded for financial reporting purposes,compute the effect of each difference on deferred taxes balances on the balance sheet.Treat each item independently of the others.Assume a tax rate of 25%.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 85 في هذه المجموعة.

فتح الحزمة

k this deck

53

What is an "originating difference"?

A)The net carrying amount of a capital asset or capital asset class for tax purposes in Canada.

B)A temporary item that narrows that gap between accounting and tax values of an asset or liability.

C)A temporary item that widens the gap between accounting and tax values of an asset or liability.

D)The terminology used for depreciation of capital assets under for tax purposes in Canada.

A)The net carrying amount of a capital asset or capital asset class for tax purposes in Canada.

B)A temporary item that narrows that gap between accounting and tax values of an asset or liability.

C)A temporary item that widens the gap between accounting and tax values of an asset or liability.

D)The terminology used for depreciation of capital assets under for tax purposes in Canada.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 85 في هذه المجموعة.

فتح الحزمة

k this deck

54

The following data represent the differences between accounting and tax income for Seafood Imports Inc.,whose pre-tax accounting income is $650,000 for the year ended December 31.The company's income tax rate is 45%.Additional information relevant to income taxes includes the following.

a.Capital cost allowance of $270,000 exceeded accounting depreciation expense of $160,000 in the current year.

b.Rents of $25,000,applicable to next year,had been collected in December and deferred for financial statement purposes but are taxable in the year received.

c.In a previous year,the company established a provision for product warranty expense.A summary of the current year's transactions appears below:

For tax purposes,only actual amounts paid for warranties are deductible.

d.Insurance expense to cover the company's executive officers was $6,800 for the year,and you have determined that this expense is not deductible for tax purposes.

Requirement:

Prepare the journal entries to record income taxes for Seafood Imports.

a.Capital cost allowance of $270,000 exceeded accounting depreciation expense of $160,000 in the current year.

b.Rents of $25,000,applicable to next year,had been collected in December and deferred for financial statement purposes but are taxable in the year received.

c.In a previous year,the company established a provision for product warranty expense.A summary of the current year's transactions appears below:

For tax purposes,only actual amounts paid for warranties are deductible.

d.Insurance expense to cover the company's executive officers was $6,800 for the year,and you have determined that this expense is not deductible for tax purposes.

Requirement:

Prepare the journal entries to record income taxes for Seafood Imports.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 85 في هذه المجموعة.

فتح الحزمة

k this deck

55

What is the balance of the deferred tax liability due to the rate change?

A)100,000 debit

B)100,000 credit

C)120,000 debit

D)120,000 credit

A)100,000 debit

B)100,000 credit

C)120,000 debit

D)120,000 credit

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 85 في هذه المجموعة.

فتح الحزمة

k this deck

56

A company has income before tax of $350,000,which includes a permanent difference of $65,000 relating to non-taxable dividend income.There are no other permanent or temporary differences.The income tax rate is 45%.

Requirement:

Compute the amount of taxes payable and income tax expense.

Requirement:

Compute the amount of taxes payable and income tax expense.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 85 في هذه المجموعة.

فتح الحزمة

k this deck

57

Indicate whether the item will result in a deductible temporary difference,taxable temporary difference or neither.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 85 في هذه المجموعة.

فتح الحزمة

k this deck

58

The following information relates to the accounting income for Withering Press Company (WPC)for the current year ended December 31.

The company had purchased land some years ago for $600,000.Recently,it was discovered that this land is contaminated by industrial pollution.Because of the soil remediation costs required,the value of the land has decreased.For tax purposes,the impairment loss is not currently deductible.In the future when the land is sold,half of any losses is deductible against taxable capital gains (ie.,the other half that is not taxable or deductible is a permanent difference).

The deferred income tax liability account on January 1 had a credit balance of $45,000.This balance is entirely related to property,plant,and equipment (PPE).

Requirement:

Prepare the journal entries to record income taxes for WPC.

The company had purchased land some years ago for $600,000.Recently,it was discovered that this land is contaminated by industrial pollution.Because of the soil remediation costs required,the value of the land has decreased.For tax purposes,the impairment loss is not currently deductible.In the future when the land is sold,half of any losses is deductible against taxable capital gains (ie.,the other half that is not taxable or deductible is a permanent difference).

The deferred income tax liability account on January 1 had a credit balance of $45,000.This balance is entirely related to property,plant,and equipment (PPE).

Requirement:

Prepare the journal entries to record income taxes for WPC.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 85 في هذه المجموعة.

فتح الحزمة

k this deck

59

For each of the following differences between the amount of taxable income and income recorded for financial reporting purposes,compute the effect of each difference on deferred taxes balances on the balance sheet.Treat each item independently of the others.Assume a tax rate of 30%.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 85 في هذه المجموعة.

فتح الحزمة

k this deck

60

When will there be recapture and a capital gain?

A)When proceeds of disposal are less than undepreciated capital cost.

B)When proceeds of disposal are between undepreciated capital cost and original cost.

C)When proceeds of disposal are more than undepreciated capital cost.

D)When proceeds of disposal are more than original cost.

A)When proceeds of disposal are less than undepreciated capital cost.

B)When proceeds of disposal are between undepreciated capital cost and original cost.

C)When proceeds of disposal are more than undepreciated capital cost.

D)When proceeds of disposal are more than original cost.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 85 في هذه المجموعة.

فتح الحزمة

k this deck

61

In the first two years of operations,a company reports taxable income of $125,000 and $65,000,respectively.In the first two years,the company paid $50,000 and $13,000.It is now the end of the third year,and the company has a loss of $160,000 for tax purposes.The company carries losses to the earliest year possible.The tax rate is currently 25%.

Requirement:

Compute the amount of income tax payable or receivable in the current (third)year.

Requirement:

Compute the amount of income tax payable or receivable in the current (third)year.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 85 في هذه المجموعة.

فتح الحزمة

k this deck

62

In the first two years of operations,a company reports taxable income of $115,000 and $165,000,respectively.In the first two years,the tax rates were 38% and 32% respectively.It is now the end of the third year,and the company has a loss of$160,000 for tax purposes.The company carries losses to the earliest year possible.The tax rate is currently 25%.

Requirement:

a.How much tax was paid in year 1 and year 2?

b.Compute the amount of income tax payable or receivable in the current (third)year.

Requirement:

a.How much tax was paid in year 1 and year 2?

b.Compute the amount of income tax payable or receivable in the current (third)year.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 85 في هذه المجموعة.

فتح الحزمة

k this deck

63

In the first two years of operations,a company reports taxable income of $125,000 and $65,000,respectively.In the first two years,the tax rates were 44% and 48% respectively.It is now the end of the third year,and the company has a loss of $260,000 for tax purposes.The company carries losses to the earliest year possible.The tax rate is currently 25%.

Requirement:

a.How much tax was paid in year 1 and year 2?

b.Compute the amount of income tax payable or receivable in the current (third)year.

Requirement:

a.How much tax was paid in year 1 and year 2?

b.Compute the amount of income tax payable or receivable in the current (third)year.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 85 في هذه المجموعة.

فتح الحزمة

k this deck

64

What adjustment is required to the opening deferred taxes as a result of the rate change?

A)30,000 debit

B)30,000 credit

C)130,000 credit

D)190,000 credit

A)30,000 debit

B)30,000 credit

C)130,000 credit

D)190,000 credit

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 85 في هذه المجموعة.

فتح الحزمة

k this deck

65

A company had taxable income of $2 million in fiscal 2013 and paid taxes of 0.6 million; the company incurred a loss of $7 million in fiscal 2015 when the tax rate is 50%.How much refund is the company entitled to?

A)Nil

B)$0.6 million

C)$1.0 million

D)$3.5 million

A)Nil

B)$0.6 million

C)$1.0 million

D)$3.5 million

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 85 في هذه المجموعة.

فتح الحزمة

k this deck

66

A company had taxable income of $12 million in fiscal 2013 and paid taxes of 4.8 million; the company incurred a loss of $7 million in fiscal 2015 when the tax rate is 50%.How much refund is the company entitled to?

A)Nil

B)$2.8 million

C)$3.5 million

D)$4.8 million

A)Nil

B)$2.8 million

C)$3.5 million

D)$4.8 million

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 85 في هذه المجموعة.

فتح الحزمة

k this deck

67

What adjustment is required to the opening deferred taxes as a result of the rate change?

A)30,000 credit

B)90,000 credit

C)120,000 credit

D)150,000 credit

A)30,000 credit

B)90,000 credit

C)120,000 credit

D)150,000 credit

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 85 في هذه المجموعة.

فتح الحزمة

k this deck

68

What is the ending balance of deferred taxes?

A)30,000 debit

B)30,000 credit

C)130,000 credit

D)190,000 credit

A)30,000 debit

B)30,000 credit

C)130,000 credit

D)190,000 credit

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 85 في هذه المجموعة.

فتح الحزمة

k this deck

69

A company has a deferred tax liability of $20,000 at the beginning of the fiscal year relating to a taxable temporary difference of $80,000.The current year tax rate is 30%.

Requirement:

Provide the journal entry to reflect the tax rate change.

Requirement:

Provide the journal entry to reflect the tax rate change.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 85 في هذه المجموعة.

فتح الحزمة

k this deck

70

Which statement is not correct?

A)Loss carryback result in definite cash inflow.

B)Loss carryback result in immediate cash inflow.

C)Loss carryforward result in definite cash inflow.

D)Loss carryforward result in uncertain cash inflow.

A)Loss carryback result in definite cash inflow.

B)Loss carryback result in immediate cash inflow.

C)Loss carryforward result in definite cash inflow.

D)Loss carryforward result in uncertain cash inflow.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 85 في هذه المجموعة.

فتح الحزمة

k this deck

71

A company has a deferred tax liability of $112,500 at the beginning of the fiscal year relating to a taxable temporary difference of $450,000.The tax rate for the year increased from 25% to 35%.

Requirement:

Provide the journal entry to reflect the tax rate change.

Requirement:

Provide the journal entry to reflect the tax rate change.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 85 في هذه المجموعة.

فتح الحزمة

k this deck

72

A company has a deferred tax liability of $120,000 at the beginning of the fiscal year relating to a taxable temporary difference of $300,000.The current year tax rate is 20%.

Requirement:

Provide the journal entry to reflect the tax rate change.

Requirement:

Provide the journal entry to reflect the tax rate change.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 85 في هذه المجموعة.

فتح الحزمة

k this deck

73

What is the effect on the deferred tax balance as a result of the rate change?

A)100,000 credit

B)160,000 credit

C)120,000 credit

D)200,000 credit

A)100,000 credit

B)160,000 credit

C)120,000 credit

D)200,000 credit

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 85 في هذه المجموعة.

فتح الحزمة

k this deck

74

What adjustment is required to the opening deferred taxes as a result of the rate change?

A)30,000 debit

B)90,000 debit

C)120,000 debit

D)150,000 debit

A)30,000 debit

B)90,000 debit

C)120,000 debit

D)150,000 debit

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 85 في هذه المجموعة.

فتح الحزمة

k this deck

75

Which statement is correct?

A)Income tax system treats income and losses symmetrically.

B)Income tax system treats income and losses asymmetrically.

C)When a company has a loss,a refund is received equal to the loss multiplied by the tax rate.

D)A loss carryforward has immediate cash flow benefits to a company.

A)Income tax system treats income and losses symmetrically.

B)Income tax system treats income and losses asymmetrically.

C)When a company has a loss,a refund is received equal to the loss multiplied by the tax rate.

D)A loss carryforward has immediate cash flow benefits to a company.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 85 في هذه المجموعة.

فتح الحزمة

k this deck

76

A company had taxable income of $2 million in fiscal 2013 and paid taxes of 7.7 million; the company incurred a loss of $8 million in fiscal 2015 when the tax rate is 50%.How much refund is the company entitled to?

A)Nil

B)$0.7 million

C)$3.85 million

D)$4 million

A)Nil

B)$0.7 million

C)$3.85 million

D)$4 million

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 85 في هذه المجموعة.

فتح الحزمة

k this deck

77

A company has a deferred tax liability of $60,000 at the beginning of the fiscal year relating to a taxable temporary difference of $300,000.The tax rate for the year increased from 20% to 25%.

Requirement:

Provide the journal entry to reflect the tax rate change.

Requirement:

Provide the journal entry to reflect the tax rate change.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 85 في هذه المجموعة.

فتح الحزمة

k this deck

78

A company has a deferred tax liability of $20,000 at the beginning of the fiscal year relating to a taxable temporary difference of $80,000.The current year tax rate is 20%.

Requirement:

Provide the journal entry to reflect the tax rate change.

Requirement:

Provide the journal entry to reflect the tax rate change.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 85 في هذه المجموعة.

فتح الحزمة

k this deck

79

A company had taxable income of $2 million in fiscal 2013 and paid taxes of 0.4 million; the company incurred a loss of $0.5 million in fiscal 2015 when the tax rate is 30%.How much refund is the company entitled to?

A)Nil

B)$0.2 million

C)$0.4 million

D)$0.6 million

A)Nil

B)$0.2 million

C)$0.4 million

D)$0.6 million

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 85 في هذه المجموعة.

فتح الحزمة

k this deck

80

A company has a deferred tax liability of $120,000 at the beginning of the fiscal year relating to a taxable temporary difference of $300,000.The current year tax rate is 50%.

Requirement:

Provide the journal entry to reflect the tax rate change.

Requirement:

Provide the journal entry to reflect the tax rate change.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 85 في هذه المجموعة.

فتح الحزمة

k this deck

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 85 في هذه المجموعة.