Deck 9: Consolidation: Controlled Entities

ملء الشاشة (f)

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

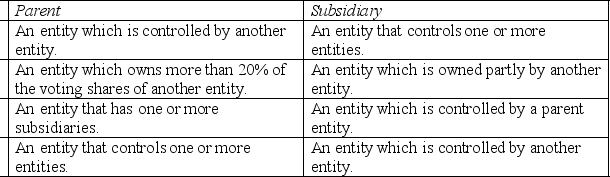

AASB 10/IFRS 10 Consolidated Financial Statements defines a 'parent' and a 'subsidiary' as which of the following?

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

فتح الحزمة

قم بالتسجيل لفتح البطاقات في هذه المجموعة!

Unlock Deck

Unlock Deck

1/50

العب

ملء الشاشة (f)

Deck 9: Consolidation: Controlled Entities

1

According to AASB 10/IFRS 10 Consolidated Financial Statements, which of the following factors indicate the existence of control? I. Possessing existing rights that give the current ability to direct the relevant activities.

II) Shared power in the governance of financial and operating policies of another entity so as to obtain benefits.

III) The power to have significant influence over the operating policies of an entity so as to obtain benefits.

IV) Ownership of more than 50% of the voting rights in the subsidiary.

A) I, II and III only

B) I and IV only

C) II and IV only

D) IV only

II) Shared power in the governance of financial and operating policies of another entity so as to obtain benefits.

III) The power to have significant influence over the operating policies of an entity so as to obtain benefits.

IV) Ownership of more than 50% of the voting rights in the subsidiary.

A) I, II and III only

B) I and IV only

C) II and IV only

D) IV only

B

2

The entity that is represented by a single set of consolidated financial statements is:

A) an economic entity.

B) a parent entity.

C) a subsidiary entity.

D) a consolidated entity.

A) an economic entity.

B) a parent entity.

C) a subsidiary entity.

D) a consolidated entity.

A

3

A group of entities comprised of Kerri Limited (parent entity), Georgia Limited (subsidiary entity) and Emily Limited (subsidiary entity) have the following inventory balances. - Kerri Limited $41 000

- Georgia Limited $14 000

- Emily Limited $12 000

Which of the following amounts is shown as the consolidated inventory balance in the consolidated financial statements?

A) $12 000

B) $14 000

C) $26 000

D) $67 000

- Georgia Limited $14 000

- Emily Limited $12 000

Which of the following amounts is shown as the consolidated inventory balance in the consolidated financial statements?

A) $12 000

B) $14 000

C) $26 000

D) $67 000

D

4

Which of the following is not one of the three elements of control according to AASB 10/IFRS 10 Consolidated Financial Statements?

A) The ability to use power over the investee to affect the amount of the investor's returns.

B) Dominating the decision making of the investee.

C) Power over the investee.

D) Exposure, or rights, to variable returns from involvement with the investee.

A) The ability to use power over the investee to affect the amount of the investor's returns.

B) Dominating the decision making of the investee.

C) Power over the investee.

D) Exposure, or rights, to variable returns from involvement with the investee.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 50 في هذه المجموعة.

فتح الحزمة

k this deck

5

At balance date, Company A has 40% of the voting rights in Company B. In addition Company A holds potential voting rights in Company B amounting to 6% that are currently exercisable, and a further 9% of voting rights in Company B that can be exercised in two years' time. Which of the following statements is correct?

A) Consolidated financial statements must be prepared for Company A and B in the current year.

B) Consolidated financial statements need not be prepared for Company A and B for the current year.

C) Consolidated financial statements must be prepared as Company A controls Company B at balance date.

D) Consolidated financial statements must be prepared as Company A has more than half of the voting rights in Company B at balance date.

A) Consolidated financial statements must be prepared for Company A and B in the current year.

B) Consolidated financial statements need not be prepared for Company A and B for the current year.

C) Consolidated financial statements must be prepared as Company A controls Company B at balance date.

D) Consolidated financial statements must be prepared as Company A has more than half of the voting rights in Company B at balance date.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 50 في هذه المجموعة.

فتح الحزمة

k this deck

6

When one entity controls another entity, the business combination results in which of the following types of relationship?

A) Parent-subsidiary

B) Investor-investee

C) Investor-associate

D) Parent-child

A) Parent-subsidiary

B) Investor-investee

C) Investor-associate

D) Parent-child

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 50 في هذه المجموعة.

فتح الحزمة

k this deck

7

For the purposes of consolidated financial reporting, a group is:

A) an investor and its investees.

B) a parent entity and all its subsidiaries.

C) an entity that has one or more subsidiaries.

D) an entity that is controlled by a parent.

A) an investor and its investees.

B) a parent entity and all its subsidiaries.

C) an entity that has one or more subsidiaries.

D) an entity that is controlled by a parent.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 50 في هذه المجموعة.

فتح الحزمة

k this deck

8

The process of preparing consolidated financial statements requires that:

A) no adjustments be made to the individual financial statements or ledger accounts of the entities in the group.

B) adjusting journal entries are recorded in the ledger accounts of the subsidiaries only.

C) accruals of expenses and revenues are recorded directly into the retained earnings account of the parent entity.

D) adjusting journal entries are recorded in the ledger accounts of the parent only.

A) no adjustments be made to the individual financial statements or ledger accounts of the entities in the group.

B) adjusting journal entries are recorded in the ledger accounts of the subsidiaries only.

C) accruals of expenses and revenues are recorded directly into the retained earnings account of the parent entity.

D) adjusting journal entries are recorded in the ledger accounts of the parent only.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 50 في هذه المجموعة.

فتح الحزمة

k this deck

9

A subsidiary is an entity that:

A) has significant influence over a parent entity.

B) exercises control over a parent entity.

C) has the power to control a parent entity.

D) is controlled by another entity.

A) has significant influence over a parent entity.

B) exercises control over a parent entity.

C) has the power to control a parent entity.

D) is controlled by another entity.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 50 في هذه المجموعة.

فتح الحزمة

k this deck

10

The equity in a subsidiary not attributable to a parent is known as a/an:

A) non-controlling interest.

B) attributable interest.

C) non-parent interest.

D) external interest.

A) non-controlling interest.

B) attributable interest.

C) non-parent interest.

D) external interest.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 50 في هذه المجموعة.

فتح الحزمة

k this deck

11

The key characteristic that determines when consolidated financial statements should be prepared is:

A) the existence of transactions between the entities.

B) control.

C) substance over form.

D) significant influence.

A) the existence of transactions between the entities.

B) control.

C) substance over form.

D) significant influence.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 50 في هذه المجموعة.

فتح الحزمة

k this deck

12

AASB 10/IFRS 10 Consolidated Financial Statements defines a 'parent' and a 'subsidiary' as which of the following?

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 50 في هذه المجموعة.

فتح الحزمة

k this deck

13

Eastpac Bank has lent Alexandra Ltd $500 000. Part of the loan contract prevents Alexandra from borrowing money in the future from other banks without the permission of Eastpac. As a result of this relationship:

A) Eastpac Bank is regarded as a parent entity of Alexandra Limited.

B) Alexandra Limited is regarded as a subsidiary of Eastpac Bank.

C) a parent-subsidiary relationship does not exist between these two parties.

D) a parent-subsidiary relationship is regarded as existing between these two parties as Eastpac Bank is able to direct the relevant activities of Alexandra Limited.

A) Eastpac Bank is regarded as a parent entity of Alexandra Limited.

B) Alexandra Limited is regarded as a subsidiary of Eastpac Bank.

C) a parent-subsidiary relationship does not exist between these two parties.

D) a parent-subsidiary relationship is regarded as existing between these two parties as Eastpac Bank is able to direct the relevant activities of Alexandra Limited.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 50 في هذه المجموعة.

فتح الحزمة

k this deck

14

In a consolidated group of entities, control over the subsidiaries in the group:

A) may not be shared control.

B) can be shared with other entities.

C) requires 100% ownership of the subsidiaries' shares.

D) can exist where the rights are purely protective rights.

A) may not be shared control.

B) can be shared with other entities.

C) requires 100% ownership of the subsidiaries' shares.

D) can exist where the rights are purely protective rights.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 50 في هذه المجموعة.

فتح الحزمة

k this deck

15

The process of preparing the combined financial statements of a group of entities is known as:

A) aggregation.

B) combination.

C) accumulation.

D) consolidation.

A) aggregation.

B) combination.

C) accumulation.

D) consolidation.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 50 في هذه المجموعة.

فتح الحزمة

k this deck

16

When deciding whether or not one entity controls another entity:

A) the controlling entity must have exercised its power to control.

B) it is sufficient that the controlling entity has the capacity to control.

C) the controlling entity must be actively involved in the decision making of the other entity.

D) the controlling entity must have exerted its control over the financing policies of the other entity.

A) the controlling entity must have exercised its power to control.

B) it is sufficient that the controlling entity has the capacity to control.

C) the controlling entity must be actively involved in the decision making of the other entity.

D) the controlling entity must have exerted its control over the financing policies of the other entity.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 50 في هذه المجموعة.

فتح الحزمة

k this deck

17

In the context of control, which of the following is correct regarding rights?

A) They must be protective rights.

B) They must arise from a legal contract.

C) They must arise as a result of future events.

D) They must be substantive rights.

A) They must be protective rights.

B) They must arise from a legal contract.

C) They must arise as a result of future events.

D) They must be substantive rights.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 50 في هذه المجموعة.

فتح الحزمة

k this deck

18

The reasons for the preparation of consolidated financial statements include which of the following?

A) Reporting of risks and benefits

B) Comparable information

C) Supply of relevant information

D) All of the above

A) Reporting of risks and benefits

B) Comparable information

C) Supply of relevant information

D) All of the above

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 50 في هذه المجموعة.

فتح الحزمة

k this deck

19

Rights to variable returns from an investee include:

A) returns from economies of scale.

B) remuneration from provision of services.

C) returns from denying or regulating access to a subsidiary's assets.

D) all of the above.

A) returns from economies of scale.

B) remuneration from provision of services.

C) returns from denying or regulating access to a subsidiary's assets.

D) all of the above.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 50 في هذه المجموعة.

فتح الحزمة

k this deck

20

A single set of financial statements that combines the separate sets of financial statements for all entities within an economic entity, is known as:

A) a concise financial report.

B) a condensed financial report.

C) combined financial statements.

D) consolidated financial statements.

A) a concise financial report.

B) a condensed financial report.

C) combined financial statements.

D) consolidated financial statements.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 50 في هذه المجموعة.

فتح الحزمة

k this deck

21

Which of the following is not one of the factors in AASB 3/IFRS 3 Business Combinations that guide the identification of the acquirer where 2 companies combine to form a new company?

A) The entity that has the smaller fair value.

B) The entity that has a significantly greater fair value.

C) The entity whose management is able to dominate the business combination.

D) The entity that gives up the cash or other assets where equity instruments are exchanged for cash or other assets.

A) The entity that has the smaller fair value.

B) The entity that has a significantly greater fair value.

C) The entity whose management is able to dominate the business combination.

D) The entity that gives up the cash or other assets where equity instruments are exchanged for cash or other assets.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 50 في هذه المجموعة.

فتح الحزمة

k this deck

22

One of the major problems with control where an investor owns less than a majority of the investee's voting shares is the issue of temporary control.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 50 في هذه المجموعة.

فتح الحزمة

k this deck

23

According to AASB 12/IFRS 12 Disclosure of Interests in Other Entities, an entity that has been designed so that voting or similar rights are not the dominant factor in deciding who controls the entity is known as a:

A) controlling entity.

B) structured entity.

C) dominant entity.

D) rights entity.

A) controlling entity.

B) structured entity.

C) dominant entity.

D) rights entity.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 50 في هذه المجموعة.

فتح الحزمة

k this deck

24

Entities can only classify investments in other entities as subsidiaries if they actually exercise control over the financial and operating policies of an entity.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 50 في هذه المجموعة.

فتح الحزمة

k this deck

25

Where a non-controlling interest exists in a subsidiary, AASB 12 /IFRS 12 Disclosure of Interests in Other Parties requires parent entities to disclose which of the following for each such subsidiary? I Summarised financial information about each subsidiary.

II The proportion of ownership interests held by non-controlling interests.

III If the subsidiary is not wholly owned, the names of all other members.

IV The country of incorporation of subsidiaries.

A) I, II and IV only

B) II, III and IV only

C) I and IV only

D) I, II, III and IV

II The proportion of ownership interests held by non-controlling interests.

III If the subsidiary is not wholly owned, the names of all other members.

IV The country of incorporation of subsidiaries.

A) I, II and IV only

B) II, III and IV only

C) I and IV only

D) I, II, III and IV

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 50 في هذه المجموعة.

فتح الحزمة

k this deck

26

Control is the criterion for determining whether a parent-subsidiary relationship exists.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 50 في هذه المجموعة.

فتح الحزمة

k this deck

27

Where an entity directly holds more than 50% of the voting rights of another entity, they are presumed to have power in accordance with AASB 10/IFRS 10 Consolidated Financial Statements.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 50 في هذه المجموعة.

فتح الحزمة

k this deck

28

An entity can control another entity with an ownership interest of less than 50%, but only if there is a legally-binding contract in place between all investors that passes control to the entity.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 50 في هذه المجموعة.

فتح الحزمة

k this deck

29

Control is defined within AASB 10/IFRS 10 Consolidated Financial Statements as the ability to govern the financial and operating policies of an entity so as to obtain benefits from its activities.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 50 في هذه المجموعة.

فتح الحزمة

k this deck

30

The consolidation process involves making adjustments to the individual financial statements and ledger accounts of the entities within the group.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 50 في هذه المجموعة.

فتح الحزمة

k this deck

31

Kowloon Limited is an entity listed in Hong Kong. Kowloon Limited holds a 100% investment in Aussie Pty Ltd, an Australian based company, who in turn holds a 90% interest in Skippy Pty Ltd. Aussie Pty Ltd and the Aussie group (comprising Aussie and Skippy) are both non-reporting entities. Which of the following statements is correct?

A) Aussie Pty Ltd will be required to prepare consolidated financial statements as the ultimate Australian parent.

B) Aussie Pty Ltd will not be required to prepare consolidated financial statements as they are a non-reporting entity.

C) Aussie Pty Ltd will be required to prepare consolidated financial statements only if directed to do so by ASIC.

D) Aussie Pty Ltd will not be required to prepare consolidated financial statements as Kowloon is a listed foreign entity.

A) Aussie Pty Ltd will be required to prepare consolidated financial statements as the ultimate Australian parent.

B) Aussie Pty Ltd will not be required to prepare consolidated financial statements as they are a non-reporting entity.

C) Aussie Pty Ltd will be required to prepare consolidated financial statements only if directed to do so by ASIC.

D) Aussie Pty Ltd will not be required to prepare consolidated financial statements as Kowloon is a listed foreign entity.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 50 في هذه المجموعة.

فتح الحزمة

k this deck

32

Juliet Ltd is a listed public company and has a 60% controlling interest in Marley Pty Ltd. Marley Pty Ltd is the parent of Butterscotch Pty Ltd. In which of the following situations will Marley Pty Ltd not be required to prepare consolidated financial statements?

A) If Marley Pty Ltd prepares separate financial statements that comply with IFRS.

B) If the other owners of Marley Pty Ltd have consented to the non-preparation of consolidated financial statements.

C) Where it is likely that there are external users dependant on the information.

D) Marley Pty Ltd would never be required to prepare consolidated financial statements.

A) If Marley Pty Ltd prepares separate financial statements that comply with IFRS.

B) If the other owners of Marley Pty Ltd have consented to the non-preparation of consolidated financial statements.

C) Where it is likely that there are external users dependant on the information.

D) Marley Pty Ltd would never be required to prepare consolidated financial statements.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 50 في هذه المجموعة.

فتح الحزمة

k this deck

33

Which of the following is not included in the definition of an investment entity as per IFRS 10 Consolidated Financial Statements?

A) Measures and evaluates the performance of substantially all of its investments on a cost basis.

B) Measures and evaluates the performance of substantially all of its investments on a fair value basis.

C) Commits to its investors that its business purpose is to invest funds solely for returns from capital appreciation or investment income.

D) Obtains funds from one or more investors for the purpose of providing those investors with investment management services.

A) Measures and evaluates the performance of substantially all of its investments on a cost basis.

B) Measures and evaluates the performance of substantially all of its investments on a fair value basis.

C) Commits to its investors that its business purpose is to invest funds solely for returns from capital appreciation or investment income.

D) Obtains funds from one or more investors for the purpose of providing those investors with investment management services.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 50 في هذه المجموعة.

فتح الحزمة

k this deck

34

A subsidiary is defined in AASB 10/IFRS 10 Consolidated Financial Statements as a company that is controlled by another entity.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 50 في هذه المجموعة.

فتح الحزمة

k this deck

35

Which of the following statements is correct?

A) The legal acquirer under AASB 3/IFRS 3 and the accounting acquirer under AASB 10/IFRS 10 do not have to be the same entity.

B) The entity identified under AASB 10/IFRS 10 as the parent will be the acquirer under AASB 3/IFRS 3.

C) The legal acquirer is determined under AASB 3/IFRS 3 as the entity that issues the equity instruments.

D) The accounting acquirer is the entity that becomes the controlling entity.

A) The legal acquirer under AASB 3/IFRS 3 and the accounting acquirer under AASB 10/IFRS 10 do not have to be the same entity.

B) The entity identified under AASB 10/IFRS 10 as the parent will be the acquirer under AASB 3/IFRS 3.

C) The legal acquirer is determined under AASB 3/IFRS 3 as the entity that issues the equity instruments.

D) The accounting acquirer is the entity that becomes the controlling entity.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 50 في هذه المجموعة.

فتح الحزمة

k this deck

36

According to AASB 10/IFRS 10 Consolidated Financial Statements, all parent entities are required to present consolidated statements unless which of the following conditions apply to them? I The parent is a wholly owned subsidiary.

II The parent is a partly owned subsidiary and its other owners do not object to the non-presentation of consolidated financial statements.

III The parent's debt or equity securities are traded in a public market.

IV The parent is not in the process of applying to issue any securities in a public market.

A) I and II only

B) I, II and III only

C) I, II and IV only

D) I, II, III and IV

II The parent is a partly owned subsidiary and its other owners do not object to the non-presentation of consolidated financial statements.

III The parent's debt or equity securities are traded in a public market.

IV The parent is not in the process of applying to issue any securities in a public market.

A) I and II only

B) I, II and III only

C) I, II and IV only

D) I, II, III and IV

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 50 في هذه المجموعة.

فتح الحزمة

k this deck

37

The financial statements of a group are referred to as consolidated financial statements.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 50 في هذه المجموعة.

فتح الحزمة

k this deck

38

AASB 10/IFRS 10 Consolidated Financial Statements requires that control be non-shared.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 50 في هذه المجموعة.

فتح الحزمة

k this deck

39

Where an entity controls another entity but holds less than half of the other entity's voting rights, AASB 12/IFRS 12 Disclosure of Interests in Other Entities, requires which of the following disclosures be made?

A) The reasons why the ownership of the investee does not constitute control.

B) The nature of the relationship between the investor and investee.

C) The significant judgements and assumptions it has made in determining the nature of the interest in the other entity.

D) The amount of any repayments of borrowings between the investor and investee during the period.

A) The reasons why the ownership of the investee does not constitute control.

B) The nature of the relationship between the investor and investee.

C) The significant judgements and assumptions it has made in determining the nature of the interest in the other entity.

D) The amount of any repayments of borrowings between the investor and investee during the period.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 50 في هذه المجموعة.

فتح الحزمة

k this deck

40

Two entities A Limited and B Limited together form a third entity, C Limited. C Limited acquires A Limited and B Limited. In this situation, AASB 3/IFRS 3 Business Combinations, adjudges that:

A) A Limited and B Limited cease to exist and C Limited is the acquirer.

B) the combined A Limited and B Limited, is the acquirer of C Limited.

C) C Limited is considered to be the acquirer.

D) C Limited is not to be considered to be the acquirer.

A) A Limited and B Limited cease to exist and C Limited is the acquirer.

B) the combined A Limited and B Limited, is the acquirer of C Limited.

C) C Limited is considered to be the acquirer.

D) C Limited is not to be considered to be the acquirer.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 50 في هذه المجموعة.

فتح الحزمة

k this deck

41

There are no disclosures specified by AASB 10/IFRS 10 Consolidated Financial Statements.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 50 في هذه المجموعة.

فتح الحزمة

k this deck

42

The preparation of consolidated financial statements for a group relieves subsidiaries within the group from preparing individual financial statements.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 50 في هذه المجموعة.

فتح الحزمة

k this deck

43

When a business combination is formed by the creation of a parent-subsidiary relationship, the parent will always be identified as the acquirer.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 50 في هذه المجموعة.

فتح الحزمة

k this deck

44

The formation of a new entity to acquire the shares of two (or more) other entities is an example of a business combination in accordance with AASB 3/IFRS 3 Business Combinations.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 50 في هذه المجموعة.

فتح الحزمة

k this deck

45

Potential voting rights that cannot be exercised or converted until a future date or until the occurrence of a future event are not taken into account when determining an entity's capacity to control another entity.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 50 في هذه المجموعة.

فتح الحزمة

k this deck

46

Power is defined in AASB 10/IFRS 10 Consolidated Financial Statements as the current ability to direct the relevant activities of an investee.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 50 في هذه المجموعة.

فتح الحزمة

k this deck

47

Unless the parent trades any debt or equity instruments on a securities exchange, the parent is relieved from the requirement to prepare consolidated financial statements.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 50 في هذه المجموعة.

فتح الحزمة

k this deck

48

Where there is a substantial non-controlling interest and the non-controlling shareholders do not object, AASB 10/IFRS 10 Consolidated Financial Statements allows such subsidiaries to be excluded from consolidation.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 50 في هذه المجموعة.

فتح الحزمة

k this deck

49

Where a parent is exempted from preparing consolidated financial statements under AASB 10/IFRS 10 Consolidated Financial Statements, they are still required to present separate financial statements under AASB 127/IAS 27 Separate Financial Statements.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 50 في هذه المجموعة.

فتح الحزمة

k this deck

50

Typical characteristics of an investment entity in accordance with IFRS 10 Consolidated Financial Statements include that it has more than one investment.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 50 في هذه المجموعة.

فتح الحزمة

k this deck

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 50 في هذه المجموعة.