Deck 9: Multifactor Models of Risk and Return

ملء الشاشة (f)

سؤال

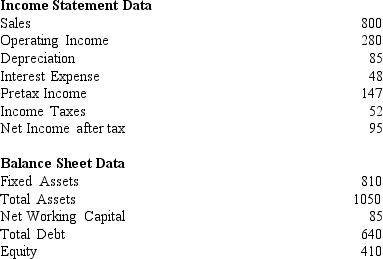

Exhibit 10.9

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

You are provided with the following year end information for All Systems Corporation.

Studies indicate that neither firm size nor the time interval used are important when computing beta.

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

You are provided with the following year end information for All Systems Corporation.

Studies indicate that neither firm size nor the time interval used are important when computing beta.

سؤال

Exhibit 10.9

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

You are provided with the following year end information for All Systems Corporation.

The January Effect is an anomaly where returns in January are significantly smaller than in any other month.

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

You are provided with the following year end information for All Systems Corporation.

The January Effect is an anomaly where returns in January are significantly smaller than in any other month.

سؤال

Exhibit 10.9

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

You are provided with the following year end information for All Systems Corporation.

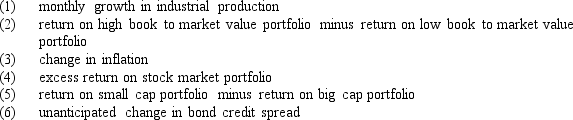

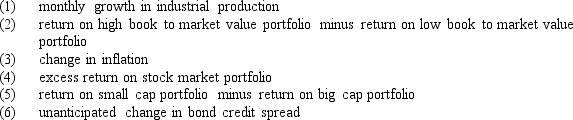

Two approaches to defining factors for multifactor models are to use macroeconomic variables or individual characteristics of the securities.

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

You are provided with the following year end information for All Systems Corporation.

Two approaches to defining factors for multifactor models are to use macroeconomic variables or individual characteristics of the securities.

سؤال

Exhibit 10.9

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

You are provided with the following year end information for All Systems Corporation.

Studies strongly suggest that the CAPM be abandoned and replaced with the APT.

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

You are provided with the following year end information for All Systems Corporation.

Studies strongly suggest that the CAPM be abandoned and replaced with the APT.

سؤال

Exhibit 10.9

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

You are provided with the following year end information for All Systems Corporation.

In the APT model, the identity of all the factors is known.

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

You are provided with the following year end information for All Systems Corporation.

In the APT model, the identity of all the factors is known.

سؤال

Exhibit 9.1

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

To date, the results of empirical tests of the Arbitrage Pricing Model have been

A)Clearly favorable.

B)Clearly unfavorable.

C)Mixed.

D)Unavailable.

E)Biased.

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

To date, the results of empirical tests of the Arbitrage Pricing Model have been

A)Clearly favorable.

B)Clearly unfavorable.

C)Mixed.

D)Unavailable.

E)Biased.

سؤال

Exhibit 10.9

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

You are provided with the following year end information for All Systems Corporation.

A major advantage of the Arbitrage Pricing Theory is the risk factors are clearly universally identifiable.

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

You are provided with the following year end information for All Systems Corporation.

A major advantage of the Arbitrage Pricing Theory is the risk factors are clearly universally identifiable.

سؤال

Exhibit 10.9

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

You are provided with the following year end information for All Systems Corporation.

The APT does not require a market portfolio.

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

You are provided with the following year end information for All Systems Corporation.

The APT does not require a market portfolio.

سؤال

Exhibit 10.9

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

You are provided with the following year end information for All Systems Corporation.

According to the APT model all securities should be priced such that riskless arbitrage is possible.

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

You are provided with the following year end information for All Systems Corporation.

According to the APT model all securities should be priced such that riskless arbitrage is possible.

سؤال

Exhibit 10.9

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

You are provided with the following year end information for All Systems Corporation.

Findings by Basu that stocks with high P/E ratios tended to outperform stocks with low P/E ratios challenge the efficacy of the CAPM.

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

You are provided with the following year end information for All Systems Corporation.

Findings by Basu that stocks with high P/E ratios tended to outperform stocks with low P/E ratios challenge the efficacy of the CAPM.

سؤال

Exhibit 9.1

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

Refer to Exhibit 9.1. In the list above, which are not assumptions of the Arbitrage Pricing model?

A)(1) and (3)

B)(1), (2), and (3)

C)(1), (2), and (5)

D)(2), (4), and (6)

E)All six are assumptions

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

Refer to Exhibit 9.1. In the list above, which are not assumptions of the Arbitrage Pricing model?

A)(1) and (3)

B)(1), (2), and (3)

C)(1), (2), and (5)

D)(2), (4), and (6)

E)All six are assumptions

سؤال

Exhibit 10.9

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

You are provided with the following year end information for All Systems Corporation.

The APT assumes that security returns are normally distributed.

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

You are provided with the following year end information for All Systems Corporation.

The APT assumes that security returns are normally distributed.

سؤال

Exhibit 10.9

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

You are provided with the following year end information for All Systems Corporation.

Fama and French suggest a four factor model approach that explains many prior market anomalies.

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

You are provided with the following year end information for All Systems Corporation.

Fama and French suggest a four factor model approach that explains many prior market anomalies.

سؤال

Exhibit 10.9

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

You are provided with the following year end information for All Systems Corporation.

The APT assumes that capital markets are perfectly competitive.

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

You are provided with the following year end information for All Systems Corporation.

The APT assumes that capital markets are perfectly competitive.

سؤال

Exhibit 9.1

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

Refer to Exhibit 9.1. In the list above which are assumptions of the Arbitrage Pricing Model?

A)(1) and (4)

B)(1), (2), and (3)

C)(1), (3), and (5)

D)(2), (3), (4), and (6)

E)All six are assumptions

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

Refer to Exhibit 9.1. In the list above which are assumptions of the Arbitrage Pricing Model?

A)(1) and (4)

B)(1), (2), and (3)

C)(1), (3), and (5)

D)(2), (3), (4), and (6)

E)All six are assumptions

سؤال

Exhibit 10.9

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

You are provided with the following year end information for All Systems Corporation.

Arbitrage Pricing Theory (APT) specifies the exact number of risk factors and their identity

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

You are provided with the following year end information for All Systems Corporation.

Arbitrage Pricing Theory (APT) specifies the exact number of risk factors and their identity

سؤال

Exhibit 10.9

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

You are provided with the following year end information for All Systems Corporation.

Findings by Fama and French that stocks with high Book Value to Market Price ratios tended to produce larger risk adjusted returns than stocks with low Book Value to Market Price ratios challenge the efficacy of the CAPM.

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

You are provided with the following year end information for All Systems Corporation.

Findings by Fama and French that stocks with high Book Value to Market Price ratios tended to produce larger risk adjusted returns than stocks with low Book Value to Market Price ratios challenge the efficacy of the CAPM.

سؤال

Exhibit 10.9

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

You are provided with the following year end information for All Systems Corporation.

One method for estimating the parameters for the Capital Asset Pricing Model is to estimate a portfolio's characteristic line via regression techniques using the single-index market model.

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

You are provided with the following year end information for All Systems Corporation.

One method for estimating the parameters for the Capital Asset Pricing Model is to estimate a portfolio's characteristic line via regression techniques using the single-index market model.

سؤال

Exhibit 10.9

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

You are provided with the following year end information for All Systems Corporation.

Multifactor models of risk and return can be broadly grouped into models that use macroeconomic factors and models that use microeconomic factors.

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

You are provided with the following year end information for All Systems Corporation.

Multifactor models of risk and return can be broadly grouped into models that use macroeconomic factors and models that use microeconomic factors.

سؤال

Exhibit 10.9

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

You are provided with the following year end information for All Systems Corporation.

Empirical tests of the APT model have found that as the size of a portfolio increased so did the number of factors.

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

You are provided with the following year end information for All Systems Corporation.

Empirical tests of the APT model have found that as the size of a portfolio increased so did the number of factors.

سؤال

Exhibit 9.1

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

-Consider the following two factor APT model E(R) = 0 + 1b1 + 2b2

A). 1 is the expected return on the asset with zero systematic risk.

B). 1 is the expected return on asset 1.

C). 1 is the pricing relationship between the risk premium and the asset.

D). 1 is the risk premium.

E). 1 is the factor loading.

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

-Consider the following two factor APT model E(R) = 0 + 1b1 + 2b2

A). 1 is the expected return on the asset with zero systematic risk.

B). 1 is the expected return on asset 1.

C). 1 is the pricing relationship between the risk premium and the asset.

D). 1 is the risk premium.

E). 1 is the factor loading.

سؤال

Exhibit 9.1

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

-The equation for the single-index market model is

A)RFRit = ai + bRmt + et

B)Rit = ai + bRmt + et

C)Rit = ai + bRFRt + et

D)Rmt = ai + bRit + et

E)Rit = ai + b(Rmt - RFRt) + et

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

-The equation for the single-index market model is

A)RFRit = ai + bRmt + et

B)Rit = ai + bRmt + et

C)Rit = ai + bRFRt + et

D)Rmt = ai + bRit + et

E)Rit = ai + b(Rmt - RFRt) + et

سؤال

Exhibit 9.1

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

In the APT model the idea of riskless arbitrage is to assemble a portfolio that

A)requires some initial wealth, will bear no risk, and still earn a profit.

B)requires no initial wealth, will bear no risk, and still earn a profit.

C)requires no initial wealth, will bear no systematic risk, and still earn a profit.

D)requires no initial wealth, will bear no unsystematic risk, and still earn a profit.

E)requires some initial wealth, will bear no systematic risk, and still earn a profit.

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

In the APT model the idea of riskless arbitrage is to assemble a portfolio that

A)requires some initial wealth, will bear no risk, and still earn a profit.

B)requires no initial wealth, will bear no risk, and still earn a profit.

C)requires no initial wealth, will bear no systematic risk, and still earn a profit.

D)requires no initial wealth, will bear no unsystematic risk, and still earn a profit.

E)requires some initial wealth, will bear no systematic risk, and still earn a profit.

سؤال

سؤال

Exhibit 9.1

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

Assume that you are embarking on a test of the small-firm effect using APT. You form 10 size-based portfolios. The following finding would suggest there is evidence supporting APT:

A)The top five size based portfolios should have excess returns that exceed the bottom five size based portfolios.

B)The bottom five size based portfolios should have excess returns that exceed the top five size based portfolios.

C)The ten portfolios must have excess returns not significantly different from zero.

D)The ten portfolios must have excess returns significantly different from zero.

E)None of the above.

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

Assume that you are embarking on a test of the small-firm effect using APT. You form 10 size-based portfolios. The following finding would suggest there is evidence supporting APT:

A)The top five size based portfolios should have excess returns that exceed the bottom five size based portfolios.

B)The bottom five size based portfolios should have excess returns that exceed the top five size based portfolios.

C)The ten portfolios must have excess returns not significantly different from zero.

D)The ten portfolios must have excess returns significantly different from zero.

E)None of the above.

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

Consider the following list of risk factors:  Which of the following factors would you use to develop a microeconomic-based risk factor model?

Which of the following factors would you use to develop a microeconomic-based risk factor model?

A)(1), (2), and (3).

B)(1), (3), and (5).

C)(2), (4), and (5).

D)(1), (3), and (6).

E)(4), (5), and (6).

Which of the following factors would you use to develop a microeconomic-based risk factor model?A)(1), (2), and (3).

B)(1), (3), and (5).

C)(2), (4), and (5).

D)(1), (3), and (6).

E)(4), (5), and (6).

سؤال

سؤال

Exhibit 9.1

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

In one of their empirical tests of the APT, Roll and Ross examined the relationship between a security's returns and its own standard deviation. A finding of a statistically significant relationship would indicate that

A)APT is valid because a security's unsystematic component would be eliminated by diversification.

B)APT is valid because non-diversifiable components should explained by factor sensitivities.

C)APT is invalid because a security's unsystematic component would be eliminated by diversification.

D)APT is invalid because standard deviation is not an appropriate factor.

E)None of the above.

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

In one of their empirical tests of the APT, Roll and Ross examined the relationship between a security's returns and its own standard deviation. A finding of a statistically significant relationship would indicate that

A)APT is valid because a security's unsystematic component would be eliminated by diversification.

B)APT is valid because non-diversifiable components should explained by factor sensitivities.

C)APT is invalid because a security's unsystematic component would be eliminated by diversification.

D)APT is invalid because standard deviation is not an appropriate factor.

E)None of the above.

سؤال

Exhibit 9.1

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

Cho, Elton, and Gruber tested the APT by examining the number of factors in the return generating process and found that

A)Five factors were required using Roll-Ross procedures.

B)Six factors were present when using historical beta.

C)Fundamental betas indicated a need for three factors.

D)All of the above.

E)None of the above.

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

Cho, Elton, and Gruber tested the APT by examining the number of factors in the return generating process and found that

A)Five factors were required using Roll-Ross procedures.

B)Six factors were present when using historical beta.

C)Fundamental betas indicated a need for three factors.

D)All of the above.

E)None of the above.

سؤال

Exhibit 9.1

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

-The excess return form of the single-index market model is

A)Rit = + b(Rmt -Rit) + eit

B)RFRt = + b(Rmt -RFRt) + eit

C)Rit - RFRt = + b(Rmt) + eit

D)Rit = + b(Rmt - RFRt) + eit

E)Rit =RFRt = + b(Rmt - RFRt) + eit

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

-The excess return form of the single-index market model is

A)Rit = + b(Rmt -Rit) + eit

B)RFRt = + b(Rmt -RFRt) + eit

C)Rit - RFRt = + b(Rmt) + eit

D)Rit = + b(Rmt - RFRt) + eit

E)Rit =RFRt = + b(Rmt - RFRt) + eit

سؤال

Consider the following list of risk factors:  Which of the following factors would you use to develop a macroeconomic-based risk factor model?

Which of the following factors would you use to develop a macroeconomic-based risk factor model?

A)(1), (2), and (3).

B)(1), (3), and (5).

C)(2), (4), and (5).

D)(1), (3), and (6).

E)(4), (5), and (6).

Which of the following factors would you use to develop a macroeconomic-based risk factor model?A)(1), (2), and (3).

B)(1), (3), and (5).

C)(2), (4), and (5).

D)(1), (3), and (6).

E)(4), (5), and (6).

سؤال

Exhibit 9.1

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

Unlike the capital asset pricing model, the arbitrage pricing theory requires only the following assumption(s):

A)A quadratric utility function.

B)Normally distributed returns.

C)The stochastic process generating asset returns can be represented by a factor model.

D)A mean-variance efficient market portfolio consisting of all risky assets.

E)All of the above

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

Unlike the capital asset pricing model, the arbitrage pricing theory requires only the following assumption(s):

A)A quadratric utility function.

B)Normally distributed returns.

C)The stochastic process generating asset returns can be represented by a factor model.

D)A mean-variance efficient market portfolio consisting of all risky assets.

E)All of the above

سؤال

سؤال

Exhibit 9.1

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

Dhrymes, Friend, and Gultekin, in their study of the APT, found that

A)As the number of securities used to form portfolios increased the number of factors that characterized the return generating process decreased.

B)As the number of securities used to form portfolios increased the number of factors that characterized the return generating process increased.

C)As the number of securities used to form portfolios decreased the number of factors that characterized the return generating process increased.

D)As the number of securities used to form portfolios increased the number of factors that characterized the return generating process remained unchanged.

E)None of the above.

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

Dhrymes, Friend, and Gultekin, in their study of the APT, found that

A)As the number of securities used to form portfolios increased the number of factors that characterized the return generating process decreased.

B)As the number of securities used to form portfolios increased the number of factors that characterized the return generating process increased.

C)As the number of securities used to form portfolios decreased the number of factors that characterized the return generating process increased.

D)As the number of securities used to form portfolios increased the number of factors that characterized the return generating process remained unchanged.

E)None of the above.

سؤال

Exhibit 9.2

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

Consider the three stocks, stock X, stock Y and stock Z, that have the following factor loadings (or factor betas).

The zero-beta return ( 0) = 3%, and the risk premia are 1 = 10%, 2 = 8%. Assume that all three stocks are currently priced at $50.

The zero-beta return ( 0) = 3%, and the risk premia are 1 = 10%, 2 = 8%. Assume that all three stocks are currently priced at $50.

-Refer to Exhibit 9.2. If you know that the actual prices one year from now are stock X $55, stock Y $52, and stock Z $57, then

A)stock X is undervalued, stock Y is undervalued, stock Z is undervalued.

B)stock X is undervalued, stock Y is overvalued, stock Z is overvalued.

C)stock X is overvalued, stock Y is undervalued, stock Z is undervalued.

D)stock X is undervalued, stock Y is overvalued, stock Z is undervalued.

E)stock X is overvalued, stock Y is overvalued, stock Z is undervalued.

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

Consider the three stocks, stock X, stock Y and stock Z, that have the following factor loadings (or factor betas).

The zero-beta return ( 0) = 3%, and the risk premia are 1 = 10%, 2 = 8%. Assume that all three stocks are currently priced at $50.-Refer to Exhibit 9.2. If you know that the actual prices one year from now are stock X $55, stock Y $52, and stock Z $57, then

A)stock X is undervalued, stock Y is undervalued, stock Z is undervalued.

B)stock X is undervalued, stock Y is overvalued, stock Z is overvalued.

C)stock X is overvalued, stock Y is undervalued, stock Z is undervalued.

D)stock X is undervalued, stock Y is overvalued, stock Z is undervalued.

E)stock X is overvalued, stock Y is overvalued, stock Z is undervalued.

سؤال

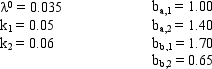

The table below provides factor risk sensitivities and factor risk premia for a three factor model for a particular asset where factor 1 is MP the growth rate in U.S. industrial production, factor 2 is UI the difference between actual and expected inflation, and factor 3 is UPR the unanticipated change in bond credit spread.  Calculate the expected excess return for the asset.

Calculate the expected excess return for the asset.

A)12.32%

B)9.32%

C)4.56%

D)6.32%

E)8.02%

Calculate the expected excess return for the asset.A)12.32%

B)9.32%

C)4.56%

D)6.32%

E)8.02%

سؤال

Exhibit 9.2

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

Consider the three stocks, stock X, stock Y and stock Z, that have the following factor loadings (or factor betas).

The zero-beta return ( 0) = 3%, and the risk premia are 1 = 10%, 2 = 8%. Assume that all three stocks are currently priced at $50.

-Refer to Exhibit 9.2. The new prices now for stocks X, Y, and Z that will not allow for arbitrage profits are

A)$53.55, $54.4, $55.25

B)$45.35, $54.4, $55.25

C)$55.55, $56.35, $57.15

D)$50, $50, $50

E)$51.35, $47.79, $51.58.

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

Consider the three stocks, stock X, stock Y and stock Z, that have the following factor loadings (or factor betas).

The zero-beta return ( 0) = 3%, and the risk premia are 1 = 10%, 2 = 8%. Assume that all three stocks are currently priced at $50.-Refer to Exhibit 9.2. The new prices now for stocks X, Y, and Z that will not allow for arbitrage profits are

A)$53.55, $54.4, $55.25

B)$45.35, $54.4, $55.25

C)$55.55, $56.35, $57.15

D)$50, $50, $50

E)$51.35, $47.79, $51.58.

سؤال

Exhibit 9.3

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

Stocks A, B, and C have two risk factors with the following beta coefficients. The zero-beta return ( 0) = .025 and the risk premiums for the two factors are ( 1) = .12 and ( 0) = .10.

-Refer to Exhibit 9.3. Suppose that you know that the prices of stocks A, B, and C will be $10.95, 22.18, and $30.89, respectively. Based on this information

A)All three stocks are overvalued.

B)All three stocks are undervalued.

C)Stock a is undervalued, stock b is properly valued, stock c is undervalued.

D)Stock a is undervalued, stock b is properly valued, stock c is overvalued.

E)Stock a is overvalued, stock b is overvalued, stock c is undervalued.

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

Stocks A, B, and C have two risk factors with the following beta coefficients. The zero-beta return ( 0) = .025 and the risk premiums for the two factors are ( 1) = .12 and ( 0) = .10.

-Refer to Exhibit 9.3. Suppose that you know that the prices of stocks A, B, and C will be $10.95, 22.18, and $30.89, respectively. Based on this information

A)All three stocks are overvalued.

B)All three stocks are undervalued.

C)Stock a is undervalued, stock b is properly valued, stock c is undervalued.

D)Stock a is undervalued, stock b is properly valued, stock c is overvalued.

E)Stock a is overvalued, stock b is overvalued, stock c is undervalued.

سؤال

Exhibit 9.2

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

Consider the three stocks, stock X, stock Y and stock Z, that have the following factor loadings (or factor betas).

The zero-beta return ( 0) = 3%, and the risk premia are 1 = 10%, 2 = 8%. Assume that all three stocks are currently priced at $50.

-Refer to Exhibit 9.2. Assume that you wish to create a portfolio with no net wealth invested and the portfolio that achieves this has 50% in stock X, -100% in stock Y, and 50% in stock Z. The net arbitrage profit is

A)$8

B)$5

C)$7

D)$12

E)$15

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

Consider the three stocks, stock X, stock Y and stock Z, that have the following factor loadings (or factor betas).

The zero-beta return ( 0) = 3%, and the risk premia are 1 = 10%, 2 = 8%. Assume that all three stocks are currently priced at $50.-Refer to Exhibit 9.2. Assume that you wish to create a portfolio with no net wealth invested and the portfolio that achieves this has 50% in stock X, -100% in stock Y, and 50% in stock Z. The net arbitrage profit is

A)$8

B)$5

C)$7

D)$12

E)$15

سؤال

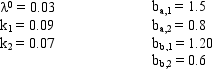

Under the following conditions, what are the expected returns for stocks A and B?

A)14.8% and 13.8%

B)19.8% and 29.5%

C)16.0% and 19.8%

D)16.9% and 15.9%

E)None of the above

A)14.8% and 13.8%

B)19.8% and 29.5%

C)16.0% and 19.8%

D)16.9% and 15.9%

E)None of the above

سؤال

Exhibit 9.3

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

Stocks A, B, and C have two risk factors with the following beta coefficients. The zero-beta return ( 0) = .025 and the risk premiums for the two factors are ( 1) = .12 and ( 0) = .10.

-Refer to Exhibit 9.3. Calculate the expected returns for stocks A, B, C. A B C

A)0.082 0.091 0.033

B)0.105 0.109 0.032

C)0.132 0.128 0.033

D)0.165 0.121 0.032

E)0.850 0.850 0.610

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

Stocks A, B, and C have two risk factors with the following beta coefficients. The zero-beta return ( 0) = .025 and the risk premiums for the two factors are ( 1) = .12 and ( 0) = .10.

-Refer to Exhibit 9.3. Calculate the expected returns for stocks A, B, C. A B C

A)0.082 0.091 0.033

B)0.105 0.109 0.032

C)0.132 0.128 0.033

D)0.165 0.121 0.032

E)0.850 0.850 0.610

سؤال

Exhibit 9.3

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

Stocks A, B, and C have two risk factors with the following beta coefficients. The zero-beta return ( 0) = .025 and the risk premiums for the two factors are ( 1) = .12 and ( 0) = .10.

-Refer to Exhibit 9.3. Assume that stocks A, B, and C never pay dividends and stocks A, B, and C are currently trading at $10, $20, and $30, respectively. What is the expected price next year for each stock? A B C

A)$10.82 $21.82 $30.99

B)$11.05 $22.18 $30.96

C)$11.32 $22.56 $30.99

D)$11.65 $22.42 $30.96

E)$18.50 $37.00 $48.30

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

Stocks A, B, and C have two risk factors with the following beta coefficients. The zero-beta return ( 0) = .025 and the risk premiums for the two factors are ( 1) = .12 and ( 0) = .10.

-Refer to Exhibit 9.3. Assume that stocks A, B, and C never pay dividends and stocks A, B, and C are currently trading at $10, $20, and $30, respectively. What is the expected price next year for each stock? A B C

A)$10.82 $21.82 $30.99

B)$11.05 $22.18 $30.96

C)$11.32 $22.56 $30.99

D)$11.65 $22.42 $30.96

E)$18.50 $37.00 $48.30

سؤال

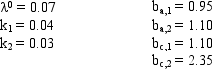

Under the following conditions, what are the expected returns for stocks A and B?

A)24.8% and 19.7%

B)22.1% and 18.0%

C)20.3% and 17.8%

D)19.9% and 16.9%

E)18.7% and 15.3%

A)24.8% and 19.7%

B)22.1% and 18.0%

C)20.3% and 17.8%

D)19.9% and 16.9%

E)18.7% and 15.3%

سؤال

Under the following conditions, what are the expected returns for stocks A and C?

A)14.1% and 17.65%

B)14.1% and 18.45%

C)17.65% and 18.45%

D)18.45% and 17.52%

E)None of the above

A)14.1% and 17.65%

B)14.1% and 18.45%

C)17.65% and 18.45%

D)18.45% and 17.52%

E)None of the above

سؤال

Exhibit 9.2

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

Consider the three stocks, stock X, stock Y and stock Z, that have the following factor loadings (or factor betas).

The zero-beta return ( 0) = 3%, and the risk premia are 1 = 10%, 2 = 8%. Assume that all three stocks are currently priced at $50.

-Refer to Exhibit 9.2. The expected prices one year from now for stocks X, Y, and Z are

A)$53.55, $54.4, $55.25

B)$45.35, $54.4, $55.25

C)$55.55, $56.35, $57.15

D)$50, $50, $50

E)$51.35, $47.79, $51.58.

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

Consider the three stocks, stock X, stock Y and stock Z, that have the following factor loadings (or factor betas).

The zero-beta return ( 0) = 3%, and the risk premia are 1 = 10%, 2 = 8%. Assume that all three stocks are currently priced at $50.-Refer to Exhibit 9.2. The expected prices one year from now for stocks X, Y, and Z are

A)$53.55, $54.4, $55.25

B)$45.35, $54.4, $55.25

C)$55.55, $56.35, $57.15

D)$50, $50, $50

E)$51.35, $47.79, $51.58.

سؤال

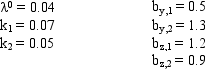

Under the following conditions, what are the expected returns for stocks Y and Z?

A)12.0% and 13.3%

B)13.5% and 14.2%

C)13.9% and 15.6%

D)14.0% and 16.9%

E)15.8% and 17.3%

A)12.0% and 13.3%

B)13.5% and 14.2%

C)13.9% and 15.6%

D)14.0% and 16.9%

E)15.8% and 17.3%

سؤال

سؤال

Exhibit 9.2

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

Consider the three stocks, stock X, stock Y and stock Z, that have the following factor loadings (or factor betas).

The zero-beta return ( 0) = 3%, and the risk premia are 1 = 10%, 2 = 8%. Assume that all three stocks are currently priced at $50.

-Refer to Exhibit 9.2. The expected returns for stock X, stock Y, and stock Z are

A)3%, 8%, 10%

B)7.1%, 10.5%, 8.8%

C)7.1%, 8.8%, 10.5%

D)10%, 5.5%, 14%

E)None of the above.

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

Consider the three stocks, stock X, stock Y and stock Z, that have the following factor loadings (or factor betas).

The zero-beta return ( 0) = 3%, and the risk premia are 1 = 10%, 2 = 8%. Assume that all three stocks are currently priced at $50.-Refer to Exhibit 9.2. The expected returns for stock X, stock Y, and stock Z are

A)3%, 8%, 10%

B)7.1%, 10.5%, 8.8%

C)7.1%, 8.8%, 10.5%

D)10%, 5.5%, 14%

E)None of the above.

سؤال

Exhibit 9.2

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

Consider the three stocks, stock X, stock Y and stock Z, that have the following factor loadings (or factor betas).

The zero-beta return ( 0) = 3%, and the risk premia are 1 = 10%, 2 = 8%. Assume that all three stocks are currently priced at $50.

-Refer to Exhibit 9.2. Assume that you wish to create a portfolio with no net wealth invested. The portfolio that achieves this has 50% in stock X, -100% in stock Y, and 50% in stock Z. The weighted exposure to risk factor 2 for stocks X, Y, and Z are

A)0.50, -1.0, 0.50

B)-0.50, 1.0, -0.50

C)0.60, -0.85, 0.25

D)-0.275, 0.10, 0.175

E)None of the above.

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

Consider the three stocks, stock X, stock Y and stock Z, that have the following factor loadings (or factor betas).

The zero-beta return ( 0) = 3%, and the risk premia are 1 = 10%, 2 = 8%. Assume that all three stocks are currently priced at $50.-Refer to Exhibit 9.2. Assume that you wish to create a portfolio with no net wealth invested. The portfolio that achieves this has 50% in stock X, -100% in stock Y, and 50% in stock Z. The weighted exposure to risk factor 2 for stocks X, Y, and Z are

A)0.50, -1.0, 0.50

B)-0.50, 1.0, -0.50

C)0.60, -0.85, 0.25

D)-0.275, 0.10, 0.175

E)None of the above.

سؤال

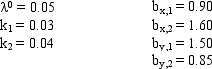

Under the following conditions, what are the expected returns for stocks X and Y?

A)14.1% and 12.9%

B)12.5% and 19.5%

C)19.5% and 18.5%

D)21.2% and 18.5%

E)None of the above

A)14.1% and 12.9%

B)12.5% and 19.5%

C)19.5% and 18.5%

D)21.2% and 18.5%

E)None of the above

سؤال

Under the following conditions, what are the expected returns for stocks Y and Z?

A)17.61% and 13.23%

B)16.25% and 18.25%

C)13.24% and 28.46%

D)14.83% and 17.69%

E)None of the above

A)17.61% and 13.23%

B)16.25% and 18.25%

C)13.24% and 28.46%

D)14.83% and 17.69%

E)None of the above

سؤال

Exhibit 9.2

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

Consider the three stocks, stock X, stock Y and stock Z, that have the following factor loadings (or factor betas).

The zero-beta return ( 0) = 3%, and the risk premia are 1 = 10%, 2 = 8%. Assume that all three stocks are currently priced at $50.

-Refer to Exhibit 9.2. Assume that you wish to create a portfolio with no net wealth invested. The portfolio that achieves this has 50% in stock X, -100% in stock Y, and 50% in stock Z. The weighted exposure to risk factor 1 for stocks X, Y, and Z are

A)0.50, -1.0, 0.50

B)-0.50, 1.0, -00.50

C)0.60, -0.85, 0.25

D)-0.275, 0.10, 0.175

E)None of the above.

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

Consider the three stocks, stock X, stock Y and stock Z, that have the following factor loadings (or factor betas).

The zero-beta return ( 0) = 3%, and the risk premia are 1 = 10%, 2 = 8%. Assume that all three stocks are currently priced at $50.-Refer to Exhibit 9.2. Assume that you wish to create a portfolio with no net wealth invested. The portfolio that achieves this has 50% in stock X, -100% in stock Y, and 50% in stock Z. The weighted exposure to risk factor 1 for stocks X, Y, and Z are

A)0.50, -1.0, 0.50

B)-0.50, 1.0, -00.50

C)0.60, -0.85, 0.25

D)-0.275, 0.10, 0.175

E)None of the above.

سؤال

Under the following conditions, what are the expected returns for stocks X and Y?

A)11.58% and 12.8%

B)15.65% and 18.23%

C)13.27% and 15.6%

D)18.2% and 16.45%

E)None of the above

A)11.58% and 12.8%

B)15.65% and 18.23%

C)13.27% and 15.6%

D)18.2% and 16.45%

E)None of the above

فتح الحزمة

قم بالتسجيل لفتح البطاقات في هذه المجموعة!

Unlock Deck

Unlock Deck

1/59

العب

ملء الشاشة (f)

Deck 9: Multifactor Models of Risk and Return

1

Exhibit 10.9

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

You are provided with the following year end information for All Systems Corporation.

Studies indicate that neither firm size nor the time interval used are important when computing beta.

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

You are provided with the following year end information for All Systems Corporation.

Studies indicate that neither firm size nor the time interval used are important when computing beta.

False

2

Exhibit 10.9

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

You are provided with the following year end information for All Systems Corporation.

The January Effect is an anomaly where returns in January are significantly smaller than in any other month.

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

You are provided with the following year end information for All Systems Corporation.

The January Effect is an anomaly where returns in January are significantly smaller than in any other month.

False

3

Exhibit 10.9

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

You are provided with the following year end information for All Systems Corporation.

Two approaches to defining factors for multifactor models are to use macroeconomic variables or individual characteristics of the securities.

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

You are provided with the following year end information for All Systems Corporation.

Two approaches to defining factors for multifactor models are to use macroeconomic variables or individual characteristics of the securities.

True

4

Exhibit 10.9

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

You are provided with the following year end information for All Systems Corporation.

Studies strongly suggest that the CAPM be abandoned and replaced with the APT.

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

You are provided with the following year end information for All Systems Corporation.

Studies strongly suggest that the CAPM be abandoned and replaced with the APT.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 59 في هذه المجموعة.

فتح الحزمة

k this deck

5

Exhibit 10.9

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

You are provided with the following year end information for All Systems Corporation.

In the APT model, the identity of all the factors is known.

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

You are provided with the following year end information for All Systems Corporation.

In the APT model, the identity of all the factors is known.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 59 في هذه المجموعة.

فتح الحزمة

k this deck

6

Exhibit 9.1

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

To date, the results of empirical tests of the Arbitrage Pricing Model have been

A)Clearly favorable.

B)Clearly unfavorable.

C)Mixed.

D)Unavailable.

E)Biased.

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

To date, the results of empirical tests of the Arbitrage Pricing Model have been

A)Clearly favorable.

B)Clearly unfavorable.

C)Mixed.

D)Unavailable.

E)Biased.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 59 في هذه المجموعة.

فتح الحزمة

k this deck

7

Exhibit 10.9

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

You are provided with the following year end information for All Systems Corporation.

A major advantage of the Arbitrage Pricing Theory is the risk factors are clearly universally identifiable.

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

You are provided with the following year end information for All Systems Corporation.

A major advantage of the Arbitrage Pricing Theory is the risk factors are clearly universally identifiable.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 59 في هذه المجموعة.

فتح الحزمة

k this deck

8

Exhibit 10.9

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

You are provided with the following year end information for All Systems Corporation.

The APT does not require a market portfolio.

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

You are provided with the following year end information for All Systems Corporation.

The APT does not require a market portfolio.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 59 في هذه المجموعة.

فتح الحزمة

k this deck

9

Exhibit 10.9

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

You are provided with the following year end information for All Systems Corporation.

According to the APT model all securities should be priced such that riskless arbitrage is possible.

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

You are provided with the following year end information for All Systems Corporation.

According to the APT model all securities should be priced such that riskless arbitrage is possible.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 59 في هذه المجموعة.

فتح الحزمة

k this deck

10

Exhibit 10.9

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

You are provided with the following year end information for All Systems Corporation.

Findings by Basu that stocks with high P/E ratios tended to outperform stocks with low P/E ratios challenge the efficacy of the CAPM.

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

You are provided with the following year end information for All Systems Corporation.

Findings by Basu that stocks with high P/E ratios tended to outperform stocks with low P/E ratios challenge the efficacy of the CAPM.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 59 في هذه المجموعة.

فتح الحزمة

k this deck

11

Exhibit 9.1

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

Refer to Exhibit 9.1. In the list above, which are not assumptions of the Arbitrage Pricing model?

A)(1) and (3)

B)(1), (2), and (3)

C)(1), (2), and (5)

D)(2), (4), and (6)

E)All six are assumptions

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

Refer to Exhibit 9.1. In the list above, which are not assumptions of the Arbitrage Pricing model?

A)(1) and (3)

B)(1), (2), and (3)

C)(1), (2), and (5)

D)(2), (4), and (6)

E)All six are assumptions

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 59 في هذه المجموعة.

فتح الحزمة

k this deck

12

Exhibit 10.9

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

You are provided with the following year end information for All Systems Corporation.

The APT assumes that security returns are normally distributed.

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

You are provided with the following year end information for All Systems Corporation.

The APT assumes that security returns are normally distributed.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 59 في هذه المجموعة.

فتح الحزمة

k this deck

13

Exhibit 10.9

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

You are provided with the following year end information for All Systems Corporation.

Fama and French suggest a four factor model approach that explains many prior market anomalies.

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

You are provided with the following year end information for All Systems Corporation.

Fama and French suggest a four factor model approach that explains many prior market anomalies.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 59 في هذه المجموعة.

فتح الحزمة

k this deck

14

Exhibit 10.9

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

You are provided with the following year end information for All Systems Corporation.

The APT assumes that capital markets are perfectly competitive.

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

You are provided with the following year end information for All Systems Corporation.

The APT assumes that capital markets are perfectly competitive.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 59 في هذه المجموعة.

فتح الحزمة

k this deck

15

Exhibit 9.1

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

Refer to Exhibit 9.1. In the list above which are assumptions of the Arbitrage Pricing Model?

A)(1) and (4)

B)(1), (2), and (3)

C)(1), (3), and (5)

D)(2), (3), (4), and (6)

E)All six are assumptions

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

Refer to Exhibit 9.1. In the list above which are assumptions of the Arbitrage Pricing Model?

A)(1) and (4)

B)(1), (2), and (3)

C)(1), (3), and (5)

D)(2), (3), (4), and (6)

E)All six are assumptions

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 59 في هذه المجموعة.

فتح الحزمة

k this deck

16

Exhibit 10.9

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

You are provided with the following year end information for All Systems Corporation.

Arbitrage Pricing Theory (APT) specifies the exact number of risk factors and their identity

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

You are provided with the following year end information for All Systems Corporation.

Arbitrage Pricing Theory (APT) specifies the exact number of risk factors and their identity

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 59 في هذه المجموعة.

فتح الحزمة

k this deck

17

Exhibit 10.9

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

You are provided with the following year end information for All Systems Corporation.

Findings by Fama and French that stocks with high Book Value to Market Price ratios tended to produce larger risk adjusted returns than stocks with low Book Value to Market Price ratios challenge the efficacy of the CAPM.

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

You are provided with the following year end information for All Systems Corporation.

Findings by Fama and French that stocks with high Book Value to Market Price ratios tended to produce larger risk adjusted returns than stocks with low Book Value to Market Price ratios challenge the efficacy of the CAPM.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 59 في هذه المجموعة.

فتح الحزمة

k this deck

18

Exhibit 10.9

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

You are provided with the following year end information for All Systems Corporation.

One method for estimating the parameters for the Capital Asset Pricing Model is to estimate a portfolio's characteristic line via regression techniques using the single-index market model.

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

You are provided with the following year end information for All Systems Corporation.

One method for estimating the parameters for the Capital Asset Pricing Model is to estimate a portfolio's characteristic line via regression techniques using the single-index market model.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 59 في هذه المجموعة.

فتح الحزمة

k this deck

19

Exhibit 10.9

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

You are provided with the following year end information for All Systems Corporation.

Multifactor models of risk and return can be broadly grouped into models that use macroeconomic factors and models that use microeconomic factors.

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

You are provided with the following year end information for All Systems Corporation.

Multifactor models of risk and return can be broadly grouped into models that use macroeconomic factors and models that use microeconomic factors.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 59 في هذه المجموعة.

فتح الحزمة

k this deck

20

Exhibit 10.9

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

You are provided with the following year end information for All Systems Corporation.

Empirical tests of the APT model have found that as the size of a portfolio increased so did the number of factors.

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

You are provided with the following year end information for All Systems Corporation.

Empirical tests of the APT model have found that as the size of a portfolio increased so did the number of factors.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 59 في هذه المجموعة.

فتح الحزمة

k this deck

21

Exhibit 9.1

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

-Consider the following two factor APT model E(R) = 0 + 1b1 + 2b2

A). 1 is the expected return on the asset with zero systematic risk.

B). 1 is the expected return on asset 1.

C). 1 is the pricing relationship between the risk premium and the asset.

D). 1 is the risk premium.

E). 1 is the factor loading.

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

-Consider the following two factor APT model E(R) = 0 + 1b1 + 2b2

A). 1 is the expected return on the asset with zero systematic risk.

B). 1 is the expected return on asset 1.

C). 1 is the pricing relationship between the risk premium and the asset.

D). 1 is the risk premium.

E). 1 is the factor loading.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 59 في هذه المجموعة.

فتح الحزمة

k this deck

22

Exhibit 9.1

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

-The equation for the single-index market model is

A)RFRit = ai + bRmt + et

B)Rit = ai + bRmt + et

C)Rit = ai + bRFRt + et

D)Rmt = ai + bRit + et

E)Rit = ai + b(Rmt - RFRt) + et

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

-The equation for the single-index market model is

A)RFRit = ai + bRmt + et

B)Rit = ai + bRmt + et

C)Rit = ai + bRFRt + et

D)Rmt = ai + bRit + et

E)Rit = ai + b(Rmt - RFRt) + et

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 59 في هذه المجموعة.

فتح الحزمة

k this deck

23

Exhibit 9.1

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

In the APT model the idea of riskless arbitrage is to assemble a portfolio that

A)requires some initial wealth, will bear no risk, and still earn a profit.

B)requires no initial wealth, will bear no risk, and still earn a profit.

C)requires no initial wealth, will bear no systematic risk, and still earn a profit.

D)requires no initial wealth, will bear no unsystematic risk, and still earn a profit.

E)requires some initial wealth, will bear no systematic risk, and still earn a profit.

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

In the APT model the idea of riskless arbitrage is to assemble a portfolio that

A)requires some initial wealth, will bear no risk, and still earn a profit.

B)requires no initial wealth, will bear no risk, and still earn a profit.

C)requires no initial wealth, will bear no systematic risk, and still earn a profit.

D)requires no initial wealth, will bear no unsystematic risk, and still earn a profit.

E)requires some initial wealth, will bear no systematic risk, and still earn a profit.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 59 في هذه المجموعة.

فتح الحزمة

k this deck

24

A study by Chen, Roll, and Ross in 1986 examined all of the following factors in applying the Arbitrage Pricing Theory (APT) except the

A)Return on a market value-weighted return.

B)Monthly growth rate in U.S.industrial production.

C)Change in the consumer price index (CPI).

D)Expected change in the bond credit spread.

E)All of the above factors were used in their 1986 study.

A)Return on a market value-weighted return.

B)Monthly growth rate in U.S.industrial production.

C)Change in the consumer price index (CPI).

D)Expected change in the bond credit spread.

E)All of the above factors were used in their 1986 study.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 59 في هذه المجموعة.

فتح الحزمة

k this deck

25

Exhibit 9.1

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

Assume that you are embarking on a test of the small-firm effect using APT. You form 10 size-based portfolios. The following finding would suggest there is evidence supporting APT:

A)The top five size based portfolios should have excess returns that exceed the bottom five size based portfolios.

B)The bottom five size based portfolios should have excess returns that exceed the top five size based portfolios.

C)The ten portfolios must have excess returns not significantly different from zero.

D)The ten portfolios must have excess returns significantly different from zero.

E)None of the above.

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

Assume that you are embarking on a test of the small-firm effect using APT. You form 10 size-based portfolios. The following finding would suggest there is evidence supporting APT:

A)The top five size based portfolios should have excess returns that exceed the bottom five size based portfolios.

B)The bottom five size based portfolios should have excess returns that exceed the top five size based portfolios.

C)The ten portfolios must have excess returns not significantly different from zero.

D)The ten portfolios must have excess returns significantly different from zero.

E)None of the above.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 59 في هذه المجموعة.

فتح الحزمة

k this deck

26

Which of the following is not a step required for a multifactor risk model to estimate expected return for an individual stock position?

A)Identify a set of K common risk factors.

B)Estimate the risk premia for the factors.

C)Estimate the sensitivities of the each stock to these K factors.

D)Calculate the expected returns using linear programming analysis.

E)All of the above are necessary steps for a multifactor risk model.

A)Identify a set of K common risk factors.

B)Estimate the risk premia for the factors.

C)Estimate the sensitivities of the each stock to these K factors.

D)Calculate the expected returns using linear programming analysis.

E)All of the above are necessary steps for a multifactor risk model.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 59 في هذه المجموعة.

فتح الحزمة

k this deck

27

In a multifactor model, confidence risk represents

A)Unanticipated changes in the level of overall business activity.

B)Unanticipated changes in investors' desired time to receive payouts.

C)Unanticipated changes in short term and long term inflation rates.

D)Unanticipated changes in the willingness of investors to take on investment risk.

E)None of the above.

A)Unanticipated changes in the level of overall business activity.

B)Unanticipated changes in investors' desired time to receive payouts.

C)Unanticipated changes in short term and long term inflation rates.

D)Unanticipated changes in the willingness of investors to take on investment risk.

E)None of the above.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 59 في هذه المجموعة.

فتح الحزمة

k this deck

28

Fama and French suggest a three factor model approach. Which of the following is not included in their approach?

A)Excess returns to a broad market index

B)Return differences between small-cap and large-cap portfolios

C)Return differences between industry characteristics

D)Return differences between value and growth stocks

E)Both c and d

A)Excess returns to a broad market index

B)Return differences between small-cap and large-cap portfolios

C)Return differences between industry characteristics

D)Return differences between value and growth stocks

E)Both c and d

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 59 في هذه المجموعة.

فتح الحزمة

k this deck

29

In a micro-economic (or characteristic) based risk factor model the following factor would be one of many appropriate factors:

A)Confidence risk.

B)Maturity risk.

C)Expected inflation risk.

D)Call risk.

E)Return difference between small capitalization and large capitalization stocks.

A)Confidence risk.

B)Maturity risk.

C)Expected inflation risk.

D)Call risk.

E)Return difference between small capitalization and large capitalization stocks.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 59 في هذه المجموعة.

فتح الحزمة

k this deck

30

In a macro-economic based risk factor model the following factor would be one of many appropriate factors:

A)Confidence risk.

B)Maturity risk.

C)Expected inflation risk.

D)Call risk.

E)Return difference between small capitalization and large capitalization stocks.

A)Confidence risk.

B)Maturity risk.

C)Expected inflation risk.

D)Call risk.

E)Return difference between small capitalization and large capitalization stocks.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 59 في هذه المجموعة.

فتح الحزمة

k this deck

31

In a multifactor model, time horizon risk represents

A)Unanticipated changes in the level of overall business activity.

B)Unanticipated changes in investors' desired time to receive payouts.

C)Unanticipated changes in short term and long term inflation rates.

D)Unanticipated changes in the willingness of investors to take on investment risk.

E)None of the above.

A)Unanticipated changes in the level of overall business activity.

B)Unanticipated changes in investors' desired time to receive payouts.

C)Unanticipated changes in short term and long term inflation rates.

D)Unanticipated changes in the willingness of investors to take on investment risk.

E)None of the above.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 59 في هذه المجموعة.

فتح الحزمة

k this deck

32

Consider the following list of risk factors: Which of the following factors would you use to develop a microeconomic-based risk factor model?

A)(1), (2), and (3).

B)(1), (3), and (5).

C)(2), (4), and (5).

D)(1), (3), and (6).

E)(4), (5), and (6).

Which of the following factors would you use to develop a microeconomic-based risk factor model?A)(1), (2), and (3).

B)(1), (3), and (5).

C)(2), (4), and (5).

D)(1), (3), and (6).

E)(4), (5), and (6).

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 59 في هذه المجموعة.

فتح الحزمة

k this deck

33

A 1994 study by Burmeister, Roll, and Ross defined all of the following risk factors except

A)Confidence risk

B)Market risk

C)Inflation risk

D)Market-timing risk

E)Business cycle risk

A)Confidence risk

B)Market risk

C)Inflation risk

D)Market-timing risk

E)Business cycle risk

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 59 في هذه المجموعة.

فتح الحزمة

k this deck

34

Exhibit 9.1

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

In one of their empirical tests of the APT, Roll and Ross examined the relationship between a security's returns and its own standard deviation. A finding of a statistically significant relationship would indicate that

A)APT is valid because a security's unsystematic component would be eliminated by diversification.

B)APT is valid because non-diversifiable components should explained by factor sensitivities.

C)APT is invalid because a security's unsystematic component would be eliminated by diversification.

D)APT is invalid because standard deviation is not an appropriate factor.

E)None of the above.

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

In one of their empirical tests of the APT, Roll and Ross examined the relationship between a security's returns and its own standard deviation. A finding of a statistically significant relationship would indicate that

A)APT is valid because a security's unsystematic component would be eliminated by diversification.

B)APT is valid because non-diversifiable components should explained by factor sensitivities.

C)APT is invalid because a security's unsystematic component would be eliminated by diversification.

D)APT is invalid because standard deviation is not an appropriate factor.

E)None of the above.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 59 في هذه المجموعة.

فتح الحزمة

k this deck

35

Exhibit 9.1

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

Cho, Elton, and Gruber tested the APT by examining the number of factors in the return generating process and found that

A)Five factors were required using Roll-Ross procedures.

B)Six factors were present when using historical beta.

C)Fundamental betas indicated a need for three factors.

D)All of the above.

E)None of the above.

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

Cho, Elton, and Gruber tested the APT by examining the number of factors in the return generating process and found that

A)Five factors were required using Roll-Ross procedures.

B)Six factors were present when using historical beta.

C)Fundamental betas indicated a need for three factors.

D)All of the above.

E)None of the above.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 59 في هذه المجموعة.

فتح الحزمة

k this deck

36

Exhibit 9.1

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

-The excess return form of the single-index market model is

A)Rit = + b(Rmt -Rit) + eit

B)RFRt = + b(Rmt -RFRt) + eit

C)Rit - RFRt = + b(Rmt) + eit

D)Rit = + b(Rmt - RFRt) + eit

E)Rit =RFRt = + b(Rmt - RFRt) + eit

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

-The excess return form of the single-index market model is

A)Rit = + b(Rmt -Rit) + eit

B)RFRt = + b(Rmt -RFRt) + eit

C)Rit - RFRt = + b(Rmt) + eit

D)Rit = + b(Rmt - RFRt) + eit

E)Rit =RFRt = + b(Rmt - RFRt) + eit

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 59 في هذه المجموعة.

فتح الحزمة

k this deck

37

Consider the following list of risk factors: Which of the following factors would you use to develop a macroeconomic-based risk factor model?

A)(1), (2), and (3).

B)(1), (3), and (5).

C)(2), (4), and (5).

D)(1), (3), and (6).

E)(4), (5), and (6).

Which of the following factors would you use to develop a macroeconomic-based risk factor model?A)(1), (2), and (3).

B)(1), (3), and (5).

C)(2), (4), and (5).

D)(1), (3), and (6).

E)(4), (5), and (6).

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 59 في هذه المجموعة.

فتح الحزمة

k this deck

38

Exhibit 9.1

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

Unlike the capital asset pricing model, the arbitrage pricing theory requires only the following assumption(s):

A)A quadratric utility function.

B)Normally distributed returns.

C)The stochastic process generating asset returns can be represented by a factor model.

D)A mean-variance efficient market portfolio consisting of all risky assets.

E)All of the above

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

Unlike the capital asset pricing model, the arbitrage pricing theory requires only the following assumption(s):

A)A quadratric utility function.

B)Normally distributed returns.

C)The stochastic process generating asset returns can be represented by a factor model.

D)A mean-variance efficient market portfolio consisting of all risky assets.

E)All of the above

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 59 في هذه المجموعة.

فتح الحزمة

k this deck

39

One approach for using multifactor models is to use factors that capture systematic risk. Which of the following is not a common factor used in this approach?

A)Unexpected changes in inflation

B)Consumer confidence

C)Yield curve shifts

D)Unexpected changes in real GDP

E)All of the above are common factors used to measure systematic risk

A)Unexpected changes in inflation

B)Consumer confidence

C)Yield curve shifts

D)Unexpected changes in real GDP

E)All of the above are common factors used to measure systematic risk

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 59 في هذه المجموعة.

فتح الحزمة

k this deck

40

Exhibit 9.1

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

Dhrymes, Friend, and Gultekin, in their study of the APT, found that

A)As the number of securities used to form portfolios increased the number of factors that characterized the return generating process decreased.

B)As the number of securities used to form portfolios increased the number of factors that characterized the return generating process increased.

C)As the number of securities used to form portfolios decreased the number of factors that characterized the return generating process increased.

D)As the number of securities used to form portfolios increased the number of factors that characterized the return generating process remained unchanged.

E)None of the above.

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

Dhrymes, Friend, and Gultekin, in their study of the APT, found that

A)As the number of securities used to form portfolios increased the number of factors that characterized the return generating process decreased.

B)As the number of securities used to form portfolios increased the number of factors that characterized the return generating process increased.

C)As the number of securities used to form portfolios decreased the number of factors that characterized the return generating process increased.

D)As the number of securities used to form portfolios increased the number of factors that characterized the return generating process remained unchanged.

E)None of the above.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 59 في هذه المجموعة.

فتح الحزمة

k this deck

41

Exhibit 9.2

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

Consider the three stocks, stock X, stock Y and stock Z, that have the following factor loadings (or factor betas).

The zero-beta return ( 0) = 3%, and the risk premia are 1 = 10%, 2 = 8%. Assume that all three stocks are currently priced at $50.

-Refer to Exhibit 9.2. If you know that the actual prices one year from now are stock X $55, stock Y $52, and stock Z $57, then

A)stock X is undervalued, stock Y is undervalued, stock Z is undervalued.

B)stock X is undervalued, stock Y is overvalued, stock Z is overvalued.

C)stock X is overvalued, stock Y is undervalued, stock Z is undervalued.

D)stock X is undervalued, stock Y is overvalued, stock Z is undervalued.

E)stock X is overvalued, stock Y is overvalued, stock Z is undervalued.

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

Consider the three stocks, stock X, stock Y and stock Z, that have the following factor loadings (or factor betas).

The zero-beta return ( 0) = 3%, and the risk premia are 1 = 10%, 2 = 8%. Assume that all three stocks are currently priced at $50.-Refer to Exhibit 9.2. If you know that the actual prices one year from now are stock X $55, stock Y $52, and stock Z $57, then

A)stock X is undervalued, stock Y is undervalued, stock Z is undervalued.

B)stock X is undervalued, stock Y is overvalued, stock Z is overvalued.

C)stock X is overvalued, stock Y is undervalued, stock Z is undervalued.

D)stock X is undervalued, stock Y is overvalued, stock Z is undervalued.

E)stock X is overvalued, stock Y is overvalued, stock Z is undervalued.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 59 في هذه المجموعة.

فتح الحزمة

k this deck

42

The table below provides factor risk sensitivities and factor risk premia for a three factor model for a particular asset where factor 1 is MP the growth rate in U.S. industrial production, factor 2 is UI the difference between actual and expected inflation, and factor 3 is UPR the unanticipated change in bond credit spread. Calculate the expected excess return for the asset.

A)12.32%

B)9.32%

C)4.56%

D)6.32%

E)8.02%

Calculate the expected excess return for the asset.A)12.32%

B)9.32%

C)4.56%

D)6.32%

E)8.02%

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 59 في هذه المجموعة.

فتح الحزمة

k this deck

43

Exhibit 9.2

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

Consider the three stocks, stock X, stock Y and stock Z, that have the following factor loadings (or factor betas).

The zero-beta return ( 0) = 3%, and the risk premia are 1 = 10%, 2 = 8%. Assume that all three stocks are currently priced at $50.

-Refer to Exhibit 9.2. The new prices now for stocks X, Y, and Z that will not allow for arbitrage profits are

A)$53.55, $54.4, $55.25

B)$45.35, $54.4, $55.25

C)$55.55, $56.35, $57.15

D)$50, $50, $50

E)$51.35, $47.79, $51.58.

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

Consider the three stocks, stock X, stock Y and stock Z, that have the following factor loadings (or factor betas).

The zero-beta return ( 0) = 3%, and the risk premia are 1 = 10%, 2 = 8%. Assume that all three stocks are currently priced at $50.-Refer to Exhibit 9.2. The new prices now for stocks X, Y, and Z that will not allow for arbitrage profits are

A)$53.55, $54.4, $55.25

B)$45.35, $54.4, $55.25

C)$55.55, $56.35, $57.15

D)$50, $50, $50

E)$51.35, $47.79, $51.58.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 59 في هذه المجموعة.

فتح الحزمة

k this deck

44

Exhibit 9.3

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

Stocks A, B, and C have two risk factors with the following beta coefficients. The zero-beta return ( 0) = .025 and the risk premiums for the two factors are ( 1) = .12 and ( 0) = .10.

-Refer to Exhibit 9.3. Suppose that you know that the prices of stocks A, B, and C will be $10.95, 22.18, and $30.89, respectively. Based on this information

A)All three stocks are overvalued.

B)All three stocks are undervalued.

C)Stock a is undervalued, stock b is properly valued, stock c is undervalued.

D)Stock a is undervalued, stock b is properly valued, stock c is overvalued.

E)Stock a is overvalued, stock b is overvalued, stock c is undervalued.

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

Stocks A, B, and C have two risk factors with the following beta coefficients. The zero-beta return ( 0) = .025 and the risk premiums for the two factors are ( 1) = .12 and ( 0) = .10.

-Refer to Exhibit 9.3. Suppose that you know that the prices of stocks A, B, and C will be $10.95, 22.18, and $30.89, respectively. Based on this information

A)All three stocks are overvalued.

B)All three stocks are undervalued.

C)Stock a is undervalued, stock b is properly valued, stock c is undervalued.

D)Stock a is undervalued, stock b is properly valued, stock c is overvalued.

E)Stock a is overvalued, stock b is overvalued, stock c is undervalued.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 59 في هذه المجموعة.

فتح الحزمة

k this deck

45

Exhibit 9.2

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

Consider the three stocks, stock X, stock Y and stock Z, that have the following factor loadings (or factor betas).

The zero-beta return ( 0) = 3%, and the risk premia are 1 = 10%, 2 = 8%. Assume that all three stocks are currently priced at $50.

-Refer to Exhibit 9.2. Assume that you wish to create a portfolio with no net wealth invested and the portfolio that achieves this has 50% in stock X, -100% in stock Y, and 50% in stock Z. The net arbitrage profit is

A)$8

B)$5

C)$7

D)$12

E)$15

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

Consider the three stocks, stock X, stock Y and stock Z, that have the following factor loadings (or factor betas).

The zero-beta return ( 0) = 3%, and the risk premia are 1 = 10%, 2 = 8%. Assume that all three stocks are currently priced at $50.-Refer to Exhibit 9.2. Assume that you wish to create a portfolio with no net wealth invested and the portfolio that achieves this has 50% in stock X, -100% in stock Y, and 50% in stock Z. The net arbitrage profit is

A)$8

B)$5

C)$7

D)$12

E)$15

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 59 في هذه المجموعة.

فتح الحزمة

k this deck

46

Under the following conditions, what are the expected returns for stocks A and B?

A)14.8% and 13.8%

B)19.8% and 29.5%

C)16.0% and 19.8%

D)16.9% and 15.9%

E)None of the above

A)14.8% and 13.8%

B)19.8% and 29.5%

C)16.0% and 19.8%

D)16.9% and 15.9%

E)None of the above

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 59 في هذه المجموعة.

فتح الحزمة

k this deck

47

Exhibit 9.3

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

Stocks A, B, and C have two risk factors with the following beta coefficients. The zero-beta return ( 0) = .025 and the risk premiums for the two factors are ( 1) = .12 and ( 0) = .10.

-Refer to Exhibit 9.3. Calculate the expected returns for stocks A, B, C. A B C

A)0.082 0.091 0.033

B)0.105 0.109 0.032

C)0.132 0.128 0.033

D)0.165 0.121 0.032

E)0.850 0.850 0.610

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

Stocks A, B, and C have two risk factors with the following beta coefficients. The zero-beta return ( 0) = .025 and the risk premiums for the two factors are ( 1) = .12 and ( 0) = .10.

-Refer to Exhibit 9.3. Calculate the expected returns for stocks A, B, C. A B C

A)0.082 0.091 0.033

B)0.105 0.109 0.032

C)0.132 0.128 0.033

D)0.165 0.121 0.032

E)0.850 0.850 0.610

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 59 في هذه المجموعة.

فتح الحزمة

k this deck

48

Exhibit 9.3

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

Stocks A, B, and C have two risk factors with the following beta coefficients. The zero-beta return ( 0) = .025 and the risk premiums for the two factors are ( 1) = .12 and ( 0) = .10.

-Refer to Exhibit 9.3. Assume that stocks A, B, and C never pay dividends and stocks A, B, and C are currently trading at $10, $20, and $30, respectively. What is the expected price next year for each stock? A B C

A)$10.82 $21.82 $30.99

B)$11.05 $22.18 $30.96