Deck 10: Liabilities

ملء الشاشة (f)

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

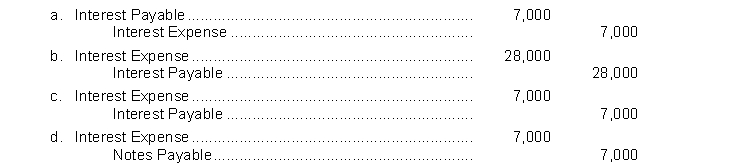

Admire County Bank agrees to lend Givens Brick Company $600,000 on January 1. Givens Brick Company signs a $600,000, 8%, 9-month note. What is the adjusting entry required if Givens Brick Company prepares financial statements on June 30?

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

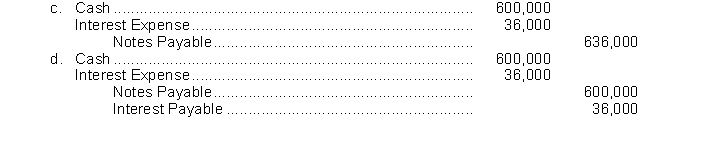

Admire County Bank agrees to lend Givens Brick Company $600,000 on January 1. Givens Brick Company signs a $600,000, 8%, 9-month note. The entry made by Givens Brick Company on January 1 to record the proceeds and issuance of the note is

سؤال

سؤال

سؤال

سؤال

On October 1, Steve's Carpet Service borrows $350,000 from First National Bank on a 3-month, $350,000, 8% note. What entry must Steve's Carpet Service make on December 31 before financial statements are prepared?

سؤال

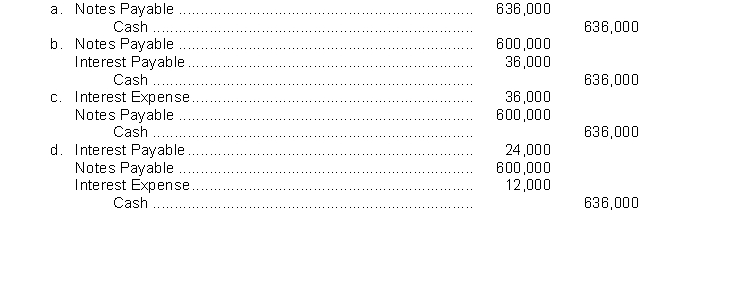

Admire County Bank agrees to lend Givens Brick Company $600,000 on January 1. Givens Brick Company signs a $600,000, 8%, 9-month note. What entry will Givens Brick Company make to pay off the note and interest at maturity assuming that interest has been accrued to September 30?

سؤال

سؤال

سؤال

سؤال

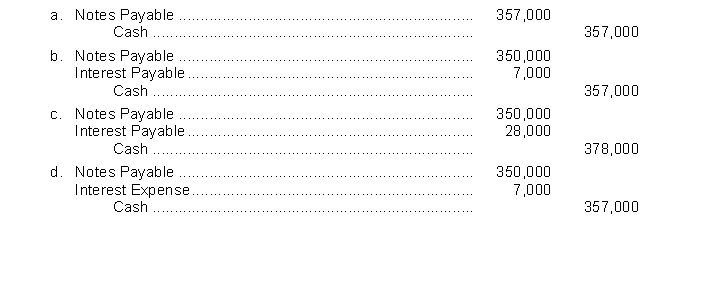

On October 1, Steve's Carpet Service borrows $350,000 from First National Bank on a 3-month, $350,000, 8% note. The entry by Steve's Carpet Service to record payment of the note and accrued interest on January 1 is

فتح الحزمة

قم بالتسجيل لفتح البطاقات في هذه المجموعة!

Unlock Deck

Unlock Deck

1/309

العب

ملء الشاشة (f)

Deck 10: Liabilities

1

Metropolitan Symphony sells 200 season tickets for $50,000 that represents a five concert season. The amount of Unearned Ticket Revenue after the second concert is $20,000.

False

2

The relationship between current liabilities and current assets is important in evaluating a company's ability to pay off its long-term debt.

False

3

Current liabilities are expected to be paid within one year or the operating cycle, whichever is longer.

True

4

A company whose current liabilities exceed its current assets may have a liquidity problem.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 309 في هذه المجموعة.

فتح الحزمة

k this deck

5

Interest expense on a note payable is only recorded at maturity.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 309 في هذه المجموعة.

فتح الحزمة

k this deck

6

The current ratio permits analysts to compare the liquidity of different sized companies.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 309 في هذه المجموعة.

فتح الحزمة

k this deck

7

The higher the sales tax rate, the more profit a retailer can earn.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 309 في هذه المجموعة.

فتح الحزمة

k this deck

8

Most notes are not interest bearing.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 309 في هذه المجموعة.

فتح الحزمة

k this deck

9

Current maturities of long-term debt refers to the amount of interest on a note payable that must be paid in the current year.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 309 في هذه المجموعة.

فتح الحزمة

k this deck

10

A note payable must always be paid before an account payable.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 309 في هذه المجموعة.

فتح الحزمة

k this deck

11

During the month, a company sells goods for a total of $108,000, which includes sales taxes of $8,000; therefore, the company should recognize $100,000 in Sales Revenues and $8,000 in Sales Tax Expense.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 309 في هذه المجموعة.

فتح الحزمة

k this deck

12

A current liability must be paid out of current earnings.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 309 في هذه المجموعة.

فتح الحزمة

k this deck

13

Unearned revenues should be classified as Other Revenues and Gains on the Income Statement.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 309 في هذه المجموعة.

فتح الحزمة

k this deck

14

Working capital is current assets divided by current liabilities.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 309 في هذه المجموعة.

فتح الحزمة

k this deck

15

With an interest-bearing note, the amount of cash received upon issuance of the note generally exceeds the note's face value.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 309 في هذه المجموعة.

فتح الحزمة

k this deck

16

Notes payable usually require the borrower to pay interest.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 309 في هذه المجموعة.

فتح الحزمة

k this deck

17

Interest expense is reported under Other Expenses and Losses in the income statement.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 309 في هذه المجموعة.

فتح الحزمة

k this deck

18

FICA taxes withheld and federal income taxes withheld are mandatory payroll deductions.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 309 في هذه المجموعة.

فتح الحزمة

k this deck

19

A $30,000, 8%, 9-month note payable requires an interest payment of $1,800 at maturity.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 309 في هذه المجموعة.

فتح الحزمة

k this deck

20

Notes payable are often used instead of accounts payable.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 309 في هذه المجموعة.

فتح الحزمة

k this deck

21

The times interest earned ratio is computed by dividing net income by interest expense.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 309 في هذه المجموعة.

فتح الحزمة

k this deck

22

Bonds that the issuing company can redeem at a stated dollar amount prior to maturity are convertible bonds.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 309 في هذه المجموعة.

فتح الحزمة

k this deck

23

If bonds are issued at a discount, the issuing corporation will pay a principal amount less than the face amount of the bonds on the maturity date.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 309 في هذه المجموعة.

فتح الحزمة

k this deck

24

The carrying value of bonds is calculated by adding the balance of the Discount on Bonds Payable account to the balance in the Bonds Payable account.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 309 في هذه المجموعة.

فتح الحزمة

k this deck

25

A corporation that issues bonds at a discount will recognize interest expense at a rate which is greater than the market interest rate.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 309 في هذه المجموعة.

فتح الحزمة

k this deck

26

Gains and losses are not recognized when convertible bonds are converted into common stock.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 309 في هذه المجموعة.

فتح الحزمة

k this deck

27

If $500,000 par value bonds with a carrying value of $476,000 are redeemed at 97, a loss on redemption will be recorded.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 309 في هذه المجموعة.

فتح الحزمة

k this deck

28

Bond interest paid by a corporation is an expense, whereas dividends paid are not an expense of the corporation.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 309 في هذه المجموعة.

فتح الحزمة

k this deck

29

If bonds sell at a premium, the interest expense recognized each year will be greater than the contractual interest rate.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 309 في هذه المجموعة.

فتح الحزمة

k this deck

30

If the market interest rate is greater than the contractual interest rate, bonds will sell at a discount.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 309 في هذه المجموعة.

فتح الحزمة

k this deck

31

If a corporation issued bonds at an amount less than face value, it indicates that the corporation has a weak credit rating.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 309 في هذه المجموعة.

فتح الحزمة

k this deck

32

Generally, convertible bonds do not pay interest.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 309 في هذه المجموعة.

فتح الحزمة

k this deck

33

Each payment on a mortgage note payable consists of interest on the original balance of the loan and a reduction of the loan principal.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 309 في هذه المجموعة.

فتح الحزمة

k this deck

34

Each bondholder may vote for the board of directors in proportion to the number of bonds held.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 309 في هذه المجموعة.

فتح الحزمة

k this deck

35

A debenture bond is an unsecured bond which is issued against the general credit of the borrower.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 309 في هذه المجموعة.

فتح الحزمة

k this deck

36

If bonds are issued at a premium, the carrying value of the bonds will be greater than the face value of the bonds for all periods prior to the bond maturity date.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 309 في هذه المجموعة.

فتح الحزمة

k this deck

37

Discount on bonds is an additional cost of borrowing and should be recorded as interest expense over the life of the bonds.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 309 في هذه المجموعة.

فتح الحزمة

k this deck

38

If $800,000, 6% bonds are issued on January 1, and pay interest annually, the amount of interest paid on the following January 1 will be $48,000.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 309 في هذه المجموعة.

فتح الحزمة

k this deck

39

The loss on bond redemption is the difference between the cash paid and the carrying value of the bonds.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 309 في هذه المجموعة.

فتح الحزمة

k this deck

40

A long-term note that pledges title to specific property as security for a loan is known as a mortgage payable.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 309 في هذه المجموعة.

فتح الحزمة

k this deck

41

If $150,000 face value bonds are issued at 103, the proceeds received will be $103,000.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 309 في هذه المجموعة.

فتح الحزمة

k this deck

42

Current maturities of long-term debt are often identified as long-term debt due within one year on the balance sheet.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 309 في هذه المجموعة.

فتح الحزمة

k this deck

43

The contractual interest rate is always equal to the market interest rate on the date that bonds are issued.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 309 في هذه المجموعة.

فتح الحزمة

k this deck

44

Long-term liabilities are reported in a separate section of the balance sheet immediately following current liabilities.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 309 في هذه المجموعة.

فتح الحزمة

k this deck

45

48. The straight-line method of amortization allocates an increasing amount to interest expense each interest period.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 309 في هذه المجموعة.

فتح الحزمة

k this deck

46

Neither corporate bond interest nor dividends are deductible for tax purposes.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 309 في هذه المجموعة.

فتح الحزمة

k this deck

47

When bonds are converted into common stock, the carrying value of the bonds is transferred to paid-in capital accounts.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 309 في هذه المجموعة.

فتح الحزمة

k this deck

48

A debt that is expected to be paid within one year through the creation of long-term debt is a current liability.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 309 في هذه المجموعة.

فتح الحزمة

k this deck

49

Bonds that permit bondholders to convert them into common stock at their option are known as callable bonds.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 309 في هذه المجموعة.

فتح الحزمة

k this deck

50

Notes payable usually are issued to meet long-term financing needs.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 309 في هذه المجموعة.

فتح الحزمة

k this deck

51

Bonds are a form of interest-bearing notes payable.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 309 في هذه المجموعة.

فتح الحزمة

k this deck

52

49. The effective-interest method of amortization results in varying amounts of amortization and interest expense per period but a constant interest rate.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 309 في هذه المجموعة.

فتح الحزمة

k this deck

53

The holder of a convertible bond can convert an interest payment received into a cash dividend paid on common stock if the dividend is greater than the interest payment.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 309 في هذه المجموعة.

فتح الحزمة

k this deck

54

A 10% stock dividend is the equivalent of a $1,000 par value bond paying annual interest of 10%.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 309 في هذه المجموعة.

فتح الحزمة

k this deck

55

The relationship between current liabilities and current assets is

A) useful in determining income.

B) useful in evaluating a company's liquidity.

C) called the matching principle.

D) useful in determining the amount of a company's long-term debt.

A) useful in determining income.

B) useful in evaluating a company's liquidity.

C) called the matching principle.

D) useful in determining the amount of a company's long-term debt.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 309 في هذه المجموعة.

فتح الحزمة

k this deck

56

All of the following are reported as current liabilities except

A) accounts payable.

B) bonds payable.

C) notes payable.

D) unearned revenues.

A) accounts payable.

B) bonds payable.

C) notes payable.

D) unearned revenues.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 309 في هذه المجموعة.

فتح الحزمة

k this deck

57

The board of directors may authorize more bonds than are issued.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 309 في هذه المجموعة.

فتح الحزمة

k this deck

58

The terms of the bond issue are set forth in a formal legal document called a bond indenture.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 309 في هذه المجموعة.

فتح الحزمة

k this deck

59

Premium on Bonds Payable is a contra account to Bonds Payable.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 309 في هذه المجموعة.

فتح الحزمة

k this deck

60

The carrying value of bonds at maturity should be equal to the face value of the bonds.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 309 في هذه المجموعة.

فتح الحزمة

k this deck

61

With an interest-bearing note, the amount of assets received upon issuance of the note is generally

A) equal to the note's face value.

B) greater than the note's face value.

C) less than the note's face value.

D) equal to the note's maturity value.

A) equal to the note's face value.

B) greater than the note's face value.

C) less than the note's face value.

D) equal to the note's maturity value.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 309 في هذه المجموعة.

فتح الحزمة

k this deck

62

The relationship of current assets to current liabilities is used in evaluating a company's

A) operating cycle.

B) revenue-producing ability.

C) short-term debt paying ability.

D) long-range solvency.

A) operating cycle.

B) revenue-producing ability.

C) short-term debt paying ability.

D) long-range solvency.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 309 في هذه المجموعة.

فتح الحزمة

k this deck

63

A current liability is a debt that can reasonably be expected to be paid

A) within one year or the operating cycle, whichever is longer.

B) between 6 months and 18 months.

C) out of currently recognized revenues.

D) out of cash currently on hand.

A) within one year or the operating cycle, whichever is longer.

B) between 6 months and 18 months.

C) out of currently recognized revenues.

D) out of cash currently on hand.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 309 في هذه المجموعة.

فتح الحزمة

k this deck

64

Admire County Bank agrees to lend Givens Brick Company $600,000 on January 1. Givens Brick Company signs a $600,000, 8%, 9-month note. What is the adjusting entry required if Givens Brick Company prepares financial statements on June 30?

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 309 في هذه المجموعة.

فتح الحزمة

k this deck

65

From a liquidity standpoint, it is more desirable for a company to have current

A) assets equal current liabilities.

B) liabilities exceed current assets.

C) assets exceed current liabilities.

D) liabilities exceed long-term liabilities.

A) assets equal current liabilities.

B) liabilities exceed current assets.

C) assets exceed current liabilities.

D) liabilities exceed long-term liabilities.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 309 في هذه المجموعة.

فتح الحزمة

k this deck

66

Liabilities are classified on the balance sheet as current or

A) deferred.

B) unearned.

C) long-term.

D) accrued.

A) deferred.

B) unearned.

C) long-term.

D) accrued.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 309 في هذه المجموعة.

فتح الحزمة

k this deck

67

Most companies pay current liabilities

A) out of current assets.

B) by issuing interest-bearing notes payable.

C) by issuing stock.

D) by creating long-term liabilities.

A) out of current assets.

B) by issuing interest-bearing notes payable.

C) by issuing stock.

D) by creating long-term liabilities.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 309 في هذه المجموعة.

فتح الحزمة

k this deck

68

Which of the following is usually not an accrued liability?

A) Interest payable

B) Wages payable

C) Taxes payable

D) Notes payable

A) Interest payable

B) Wages payable

C) Taxes payable

D) Notes payable

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 309 في هذه المجموعة.

فتح الحزمة

k this deck

69

When an interest-bearing note matures, the balance in the Notes Payable account is

A) less than the total amount repaid by the borrower.

B) the difference between the maturity value of the note and the face value of the note.

C) equal to the total amount repaid by the borrower.

D) greater than the total amount repaid by the borrower.

A) less than the total amount repaid by the borrower.

B) the difference between the maturity value of the note and the face value of the note.

C) equal to the total amount repaid by the borrower.

D) greater than the total amount repaid by the borrower.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 309 في هذه المجموعة.

فتح الحزمة

k this deck

70

Interest expense on an interest-bearing note is

A) always equal to zero.

B) accrued over the life of the note.

C) only recorded at the time the note is issued.

D) only recorded at maturity when the note is paid.

A) always equal to zero.

B) accrued over the life of the note.

C) only recorded at the time the note is issued.

D) only recorded at maturity when the note is paid.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 309 في هذه المجموعة.

فتح الحزمة

k this deck

71

Admire County Bank agrees to lend Givens Brick Company $600,000 on January 1. Givens Brick Company signs a $600,000, 8%, 9-month note. The entry made by Givens Brick Company on January 1 to record the proceeds and issuance of the note is

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 309 في هذه المجموعة.

فتح الحزمة

k this deck

72

The entry to record the payment of an interest-bearing note at maturity after all interest expense has been recognized is

A) Notes Payable Interest Payable

Cash

B) Notes Payable Interest Expense

Cash

C) Notes Payable Cash

D) Notes Payable Cash

Interest Payable

A) Notes Payable Interest Payable

Cash

B) Notes Payable Interest Expense

Cash

C) Notes Payable Cash

D) Notes Payable Cash

Interest Payable

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 309 في هذه المجموعة.

فتح الحزمة

k this deck

73

The entry to record the issuance of an interest-bearing note credits Notes Payable for the note's

A) maturity value.

B) market value.

C) face value.

D) cash realizable value.

A) maturity value.

B) market value.

C) face value.

D) cash realizable value.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 309 في هذه المجموعة.

فتح الحزمة

k this deck

74

In most companies, current liabilities are paid within

A) one year through the creation of other current liabilities.

B) the operating cycle through the creation of other current liabilities.

C) one year or the operating cycle out of current assets.

D) the operating cycle out of current assets.

A) one year through the creation of other current liabilities.

B) the operating cycle through the creation of other current liabilities.

C) one year or the operating cycle out of current assets.

D) the operating cycle out of current assets.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 309 في هذه المجموعة.

فتح الحزمة

k this deck

75

On October 1, Steve's Carpet Service borrows $350,000 from First National Bank on a 3-month, $350,000, 8% note. What entry must Steve's Carpet Service make on December 31 before financial statements are prepared?

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 309 في هذه المجموعة.

فتح الحزمة

k this deck

76

Admire County Bank agrees to lend Givens Brick Company $600,000 on January 1. Givens Brick Company signs a $600,000, 8%, 9-month note. What entry will Givens Brick Company make to pay off the note and interest at maturity assuming that interest has been accrued to September 30?

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 309 في هذه المجموعة.

فتح الحزمة

k this deck

77

A note payable is in the form of

A) a contingency that is reasonably likely to occur.

B) a written promissory note.

C) an oral agreement.

D) a standing agreement.

A) a contingency that is reasonably likely to occur.

B) a written promissory note.

C) an oral agreement.

D) a standing agreement.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 309 في هذه المجموعة.

فتح الحزمة

k this deck

78

The entry to record the proceeds upon issuing an interest-bearing note is

A) Interest Expense Cash

Notes Payable

B) Cash Notes Payable

C) Notes Payable Cash

D) Cash Notes Payable

Interest Payable

A) Interest Expense Cash

Notes Payable

B) Cash Notes Payable

C) Notes Payable Cash

D) Cash Notes Payable

Interest Payable

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 309 في هذه المجموعة.

فتح الحزمة

k this deck

79

As interest is recorded on an interest-bearing note, the Interest Expense account is

A) increased; the Notes Payable account is increased.

B) increased; the Notes Payable account is decreased.

C) increased; the Interest Payable account is increased.

D) decreased; the Interest Payable account is increased.

A) increased; the Notes Payable account is increased.

B) increased; the Notes Payable account is decreased.

C) increased; the Interest Payable account is increased.

D) decreased; the Interest Payable account is increased.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 309 في هذه المجموعة.

فتح الحزمة

k this deck

80

On October 1, Steve's Carpet Service borrows $350,000 from First National Bank on a 3-month, $350,000, 8% note. The entry by Steve's Carpet Service to record payment of the note and accrued interest on January 1 is

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 309 في هذه المجموعة.

فتح الحزمة

k this deck

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 309 في هذه المجموعة.