Deck 7: Income Effects of Alternative Cost Accumulation Systems

ملء الشاشة (f)

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

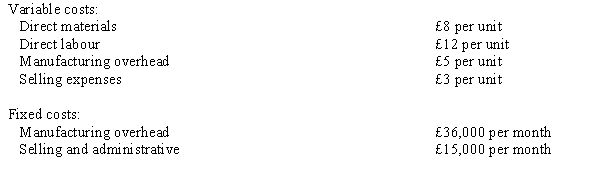

Ivy, SA., produces a single product that sells for £60 per unit. There were no inventories of work in process or finished goods. Costs for the year were as follows:  During the first three months of the year, production and sales in units were as follows:

During the first three months of the year, production and sales in units were as follows:  The company uses an actual cost system. There were no work-in-process inventories at the end of any month, and the company uses FIFO costing.

The company uses an actual cost system. There were no work-in-process inventories at the end of any month, and the company uses FIFO costing.

a.Determine the unit cost of production under variable costing for each of the three months.

b.Determine the unit cost of production under absorption costing for each of the three months.

c.Determine income under variable costing for each of the three months.

d.Determine income under absorption costing for each of the three months.

During the first three months of the year, production and sales in units were as follows: The company uses an actual cost system. There were no work-in-process inventories at the end of any month, and the company uses FIFO costing. a.Determine the unit cost of production under variable costing for each of the three months.

b.Determine the unit cost of production under absorption costing for each of the three months.

c.Determine income under variable costing for each of the three months.

d.Determine income under absorption costing for each of the three months.

فتح الحزمة

قم بالتسجيل لفتح البطاقات في هذه المجموعة!

Unlock Deck

Unlock Deck

1/42

العب

ملء الشاشة (f)

Deck 7: Income Effects of Alternative Cost Accumulation Systems

1

The method of accounting for inventory that assigns all manufacturing costs to inventory is sometimes referred to as:

A)absorption costing.

B)FIFO.

C)the weighted average cost method.

D)conversion costing.

A)absorption costing.

B)FIFO.

C)the weighted average cost method.

D)conversion costing.

A

2

Eastwood Company has the following information for 2011: There were no beginning inventories. What is the net income for Eastwood using the absorption costing method?

A)£452,000

B)£480,000

C)£1,200,000

D)£600,000

A)£452,000

B)£480,000

C)£1,200,000

D)£600,000

£452,000

3

Assuming sales prices and cost behaviour remain unchanged, when variable costing is used, when does net income change in response to changes in unit sales?

A)only when number of units sold exceeds number of units produced

B)only when number of units produced exceeds number of units sold

C)only when number of units sold exactly equals number of units produced

D)under all the above conditions

A)only when number of units sold exceeds number of units produced

B)only when number of units produced exceeds number of units sold

C)only when number of units sold exactly equals number of units produced

D)under all the above conditions

D

4

Which of the following costs would NOT be included in calculating inventory values under the absorption-costing basis?

A)direct materials

B)fixed overhead

C)selling and administrative expenses

D)direct labour

A)direct materials

B)fixed overhead

C)selling and administrative expenses

D)direct labour

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 42 في هذه المجموعة.

فتح الحزمة

k this deck

5

All of the following costs are included in inventory under absorption costing EXCEPT

A)direct materials.

B)direct labour.

C)fixed selling expenses.

D)fixed factory overhead.

A)direct materials.

B)direct labour.

C)fixed selling expenses.

D)fixed factory overhead.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 42 في هذه المجموعة.

فتح الحزمة

k this deck

6

Inventory values calculated using variable costing as opposed to absorption costing will generally be

A)equal.

B)less.

C)greater.

D)twice as much.

A)equal.

B)less.

C)greater.

D)twice as much.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 42 في هذه المجموعة.

فتح الحزمة

k this deck

7

When production is less than sales volume, net income under absorption costing will be ____ profits using variable costing procedures.

A)greater than

B)less than

C)equal to

D)randomly different than

A)greater than

B)less than

C)equal to

D)randomly different than

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 42 في هذه المجموعة.

فتح الحزمة

k this deck

8

What is the primary difference between variable and absorption costing?

A)inclusion of fixed selling expenses in product costs

B)inclusion of variable factory overhead in period costs

C)inclusion of fixed selling expenses in period costs

D)inclusion of fixed factory overhead in product costs

A)inclusion of fixed selling expenses in product costs

B)inclusion of variable factory overhead in period costs

C)inclusion of fixed selling expenses in period costs

D)inclusion of fixed factory overhead in product costs

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 42 في هذه المجموعة.

فتح الحزمة

k this deck

9

Toshi Company incurred the following costs in manufacturing desk calculators: During the period, the company produced and sold 1,000 units. What is the inventory cost per unit using absorption costing?

A)£104

B)£70

C)£84

D)£32

A)£104

B)£70

C)£84

D)£32

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 42 في هذه المجموعة.

فتح الحزمة

k this deck

10

Which of the following statements is TRUE?

A)Absorption costing net income exceeds variable costing net income when units produced and sold are equal.

B)Variable costing net income exceeds absorption costing net income when units produced exceed units sold.

C)Absorption costing net income exceeds variable costing net income when units produced are less than units sold.

D)Absorption costing net income exceeds variable costing net income when units produced are greater than units sold.

A)Absorption costing net income exceeds variable costing net income when units produced and sold are equal.

B)Variable costing net income exceeds absorption costing net income when units produced exceed units sold.

C)Absorption costing net income exceeds variable costing net income when units produced are less than units sold.

D)Absorption costing net income exceeds variable costing net income when units produced are greater than units sold.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 42 في هذه المجموعة.

فتح الحزمة

k this deck

11

Which costing approach assumes fixed overhead costs only expire when product is sold?

A)product costing

B)backflush accounting

C)absorption costing

D)cash basis accounting

A)product costing

B)backflush accounting

C)absorption costing

D)cash basis accounting

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 42 في هذه المجموعة.

فتح الحزمة

k this deck

12

Steele Ltd. has the following information for January, February, and March 2011:

There were no beginning inventories for January 2011, and all units were sold for £50. Costs are stable over the three months. What is the February ending inventory for Steele Ltd. using the absorption costing method?

A)£39,000

B)£45,000

C)£135,000

D)£300,000

There were no beginning inventories for January 2011, and all units were sold for £50. Costs are stable over the three months. What is the February ending inventory for Steele Ltd. using the absorption costing method?

A)£39,000

B)£45,000

C)£135,000

D)£300,000

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 42 في هذه المجموعة.

فتح الحزمة

k this deck

13

Figure 7-2

Steele Ltd. has the following information for January, February, and March 2011: Production costs per unit (based on 10,000 units) are as follows: There were no beginning inventories for January 2011, and all units were sold for £50. Costs are stable over the three months.

-Refer to Figure 7-2. What is the January ending inventory for Steele Ltd. using the variable costing method?

A)£260,000

B)£78,000

C)£108,000

D)£90,000

Steele Ltd. has the following information for January, February, and March 2011: Production costs per unit (based on 10,000 units) are as follows: There were no beginning inventories for January 2011, and all units were sold for £50. Costs are stable over the three months.

-Refer to Figure 7-2. What is the January ending inventory for Steele Ltd. using the variable costing method?

A)£260,000

B)£78,000

C)£108,000

D)£90,000

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 42 في هذه المجموعة.

فتح الحزمة

k this deck

14

Figure 7-1

The following information pertains to Mayberry Ltd.:

-Refer to Figure 7-1. What is the value of the ending inventory using the absorption costing method?

A)£240,000

B)£360,000

C)£600,000

D)£420,000

The following information pertains to Mayberry Ltd.:

-Refer to Figure 7-1. What is the value of the ending inventory using the absorption costing method?

A)£240,000

B)£360,000

C)£600,000

D)£420,000

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 42 في هذه المجموعة.

فتح الحزمة

k this deck

15

Under which of the following conditions is net income higher under absorption costing (relative to variable costing)?

A)Current period production exceeds sales.

B)Inventory is reduced during the current period.

C)Sales prices are rising.

D)Net income is higher under absorption costing under all conditions.

A)Current period production exceeds sales.

B)Inventory is reduced during the current period.

C)Sales prices are rising.

D)Net income is higher under absorption costing under all conditions.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 42 في هذه المجموعة.

فتح الحزمة

k this deck

16

Figure 7-1

The following information pertains to Mayberry Ltd.:

-Refer to Figure 7-1. Absorption costing net income would be ____ variable costing net income.

A)£150,000 greater than

B)£150,000 less than

C)£240,000 less than

D)£240,000 greater than

The following information pertains to Mayberry Ltd.:

-Refer to Figure 7-1. Absorption costing net income would be ____ variable costing net income.

A)£150,000 greater than

B)£150,000 less than

C)£240,000 less than

D)£240,000 greater than

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 42 في هذه المجموعة.

فتح الحزمة

k this deck

17

Figure 7-2

Steele Ltd. has the following information for January, February, and March 2011: Production costs per unit (based on 10,000 units) are as follows: There were no beginning inventories for January 2011, and all units were sold for £50. Costs are stable over the three months.

-Refer to Figure 7-2. What is the March ending inventory for Steele Ltd. using the variable costing method?

A)£120,000

B)£104,000

C)£260,000

D)£15,000

Steele Ltd. has the following information for January, February, and March 2011: Production costs per unit (based on 10,000 units) are as follows: There were no beginning inventories for January 2011, and all units were sold for £50. Costs are stable over the three months.

-Refer to Figure 7-2. What is the March ending inventory for Steele Ltd. using the variable costing method?

A)£120,000

B)£104,000

C)£260,000

D)£15,000

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 42 في هذه المجموعة.

فتح الحزمة

k this deck

18

The efficient level of activity performance is called

A)activity capacity.

B)practical capacity.

C)unused capacity.

D)acquired capacity.

A)activity capacity.

B)practical capacity.

C)unused capacity.

D)acquired capacity.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 42 في هذه المجموعة.

فتح الحزمة

k this deck

19

Ramon Company reported the following units of production and sales for June and July 2011: Net income under absorption costing for June was £40,000; net income under variable costing for July was £50,000. Fixed manufacturing costs were £600,000 for each month. How much was net income for July using absorption costing?

A)£50,000

B)£20,000

C)£80,000

D)£40,000

A)£50,000

B)£20,000

C)£80,000

D)£40,000

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 42 في هذه المجموعة.

فتح الحزمة

k this deck

20

Assuming sales prices and cost behaviour remain unchanged, when absorption costing is used, overproducing creates which of the following situations?

A)a buildup of inventory levels

B)higher net income

C)less fixed costs on the income statement

D)all of the above

A)a buildup of inventory levels

B)higher net income

C)less fixed costs on the income statement

D)all of the above

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 42 في هذه المجموعة.

فتح الحزمة

k this deck

21

Using absorption costing, a company can ____ net operating income by simply producing more than it sells.

A)decrease

B)increase

C)maintain

D)none of the above

A)decrease

B)increase

C)maintain

D)none of the above

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 42 في هذه المجموعة.

فتح الحزمة

k this deck

22

Figure 7-3

Eastwood Company has the following information for 2011: There were no beginning inventories.

-Refer to Figure 7-3. What is the ending inventory for Eastwood using the variable costing method?

A)£300,000

B)£180,000

C)£120,000

D)£80,000

Eastwood Company has the following information for 2011: There were no beginning inventories.

-Refer to Figure 7-3. What is the ending inventory for Eastwood using the variable costing method?

A)£300,000

B)£180,000

C)£120,000

D)£80,000

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 42 في هذه المجموعة.

فتح الحزمة

k this deck

23

Proponents of ____ costing believe that fixed costs are incurred to provide the capacity to produce during a given period, and these costs expire with the passage of time.

A)variable

B)absorption

C)activity-based

D)all of the above

A)variable

B)absorption

C)activity-based

D)all of the above

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 42 في هذه المجموعة.

فتح الحزمة

k this deck

24

During this past year, Bouncy Company experienced no change in inventory. Sales were 40,000 units at a selling price of £3 per unit. Variable manufacturing costs were £1.25 per unit, and total manufacturing costs were £55,000. Under absorption costing, net income was calculated at £53,000. What was net income under variable costing?

A)£65,000

B)£55,000

C)£53,000

D)£2,000

A)£65,000

B)£55,000

C)£53,000

D)£2,000

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 42 في هذه المجموعة.

فتح الحزمة

k this deck

25

The following information pertains to Stark Ltd.: What is the value of ending inventory using the variable costing method?

A)£310,000

B)£250,000

C)£200,000

D)£390,000

A)£310,000

B)£250,000

C)£200,000

D)£390,000

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 42 في هذه المجموعة.

فتح الحزمة

k this deck

26

Figure 7-3

Eastwood Company has the following information for 2011: There were no beginning inventories.

-Refer to Figure 7-3. What is the net income for Eastwood using the variable costing method?

A)£412,000

B)£480,000

C)£1,200,000

D)£600,000

Eastwood Company has the following information for 2011: There were no beginning inventories.

-Refer to Figure 7-3. What is the net income for Eastwood using the variable costing method?

A)£412,000

B)£480,000

C)£1,200,000

D)£600,000

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 42 في هذه المجموعة.

فتح الحزمة

k this deck

27

The following information pertains to Mayberry Ltd.: What is the value of the ending inventory using the variable costing method?

A)£240,000

B)£360,000

C)£350,000

D)£420,000

A)£240,000

B)£360,000

C)£350,000

D)£420,000

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 42 في هذه المجموعة.

فتح الحزمة

k this deck

28

Ramon Company reported the following units of production and sales for June and July 2011: Net income under absorption costing for June was £40,000; net income under variable costing for July was £50,000. Fixed manufacturing costs were £600,000 for each month. How much was net income for June using variable costing?

A)£40,000

B)£20,000

C)£(40,000)

D)£(20,000)

A)£40,000

B)£20,000

C)£(40,000)

D)£(20,000)

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 42 في هذه المجموعة.

فتح الحزمة

k this deck

29

Figure 7-2

Steele Ltd. has the following information for January, February, and March 2011: Production costs per unit (based on 10,000 units) are as follows: There were no beginning inventories for January 2011, and all units were sold for £50. Costs are stable over the three months.

-Refer to Figure 7-2. What is the February contribution margin for Steele Ltd. using the variable costing method?

A)£240,000

B)£170,000

C)£119,000

D)£204,000

Steele Ltd. has the following information for January, February, and March 2011: Production costs per unit (based on 10,000 units) are as follows: There were no beginning inventories for January 2011, and all units were sold for £50. Costs are stable over the three months.

-Refer to Figure 7-2. What is the February contribution margin for Steele Ltd. using the variable costing method?

A)£240,000

B)£170,000

C)£119,000

D)£204,000

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 42 في هذه المجموعة.

فتح الحزمة

k this deck

30

Toshi Company incurred the following costs in manufacturing desk calculators: During the period, the company produced and sold 1,000 units. What is the inventory cost per unit using variable costing?

A)£52

B)£62

C)£42

D)£70

A)£52

B)£62

C)£42

D)£70

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 42 في هذه المجموعة.

فتح الحزمة

k this deck

31

The variable costing income statement for Jackson Company for 2011 is as follows:

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 42 في هذه المجموعة.

فتح الحزمة

k this deck

32

In the month just ended, Aldebraun Industries produced 40,000 units and sold 37,000 units. There were 2,000 units in finished goods inventory at the start of the month. Manufacturing costs are stable from month to month. The fixed overhead rate was £8 per unit. Aldebraun uses absorption costing. If Aldebraun used variable costing, the difference in net income would have been

A)£24,000.

B)£16,000.

C)£40,000.

D)£8,000.

A)£24,000.

B)£16,000.

C)£40,000.

D)£8,000.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 42 في هذه المجموعة.

فتح الحزمة

k this deck

33

Stannel Company had 5,200 units in its ending inventory last year. The fixed manufacturing overhead was £1.75 per unit in beginning inventory, and variable manufacturing cost is £5 per unit. Stannel's net income was £4,725 higher than variable costing. How many units did the company have in beginning inventory?

A)2,500

B)7,900

C)5,200

D)5,000

A)2,500

B)7,900

C)5,200

D)5,000

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 42 في هذه المجموعة.

فتح الحزمة

k this deck

34

Figure 7-4

The following information pertains to Stark Ltd.:

-Refer to Figure 7-4. Absorption costing net income would be ____ the variable costing net income.

A)£50,000 greater than

B)£70,000 greater than

C)£70,000 less than

D)£50,000 less than

The following information pertains to Stark Ltd.:

-Refer to Figure 7-4. Absorption costing net income would be ____ the variable costing net income.

A)£50,000 greater than

B)£70,000 greater than

C)£70,000 less than

D)£50,000 less than

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 42 في هذه المجموعة.

فتح الحزمة

k this deck

35

Focus Picture Company sold 5,600 units and produced 6,000 units this past year. Unit variable costs were £15 (including variable selling costs of £3), and total fixed manufacturing costs totaled £16,500. Which costing system (variable or absorption) will show a higher net income and by how much?

A)absorption costing, £1,100

B)variable costing, £1,100

C)absorption costing £17,600

D)This cannot be determined from the information given.

A)absorption costing, £1,100

B)variable costing, £1,100

C)absorption costing £17,600

D)This cannot be determined from the information given.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 42 في هذه المجموعة.

فتح الحزمة

k this deck

36

Proponents of variable costing argue that inventories have value only to the extent that they:

A)avoid the necessity for incurring costs in the future.

B)eliminate depreciation charges.

C)can be sold for enough to cover costs and a reasonable profit.

D)turn over in less than one year.

A)avoid the necessity for incurring costs in the future.

B)eliminate depreciation charges.

C)can be sold for enough to cover costs and a reasonable profit.

D)turn over in less than one year.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 42 في هذه المجموعة.

فتح الحزمة

k this deck

37

What is the central theoretical issue in the variable costing debate?

A)the issue of how to differentiate between manufacturing and non-manufacturing costs

B)the issue of whether or not fixed manufacturing costs add value to products.

C)the issue of identifying which units were sold out of inventory.

D)the issue of identifying which costs vary with activities.

A)the issue of how to differentiate between manufacturing and non-manufacturing costs

B)the issue of whether or not fixed manufacturing costs add value to products.

C)the issue of identifying which units were sold out of inventory.

D)the issue of identifying which costs vary with activities.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 42 في هذه المجموعة.

فتح الحزمة

k this deck

38

Laguna Company had a net income of £25,000 using variable costing and a net income of £34,600 using absorption costing. The product cost using variable costing was £10.20 and using absorption costing was £15. If 10,000 units were sold, how many units were produced during?

A)2,000

B)8,000

C)12,000

D)4,800

A)2,000

B)8,000

C)12,000

D)4,800

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 42 في هذه المجموعة.

فتح الحزمة

k this deck

39

Figure 7-4

The following information pertains to Stark Ltd.:

-Refer to Figure 7-4. What is the value of ending inventory using the absorption costing method?

A)£310,000

B)£250,000

C)£200,000

D)£390,000

The following information pertains to Stark Ltd.:

-Refer to Figure 7-4. What is the value of ending inventory using the absorption costing method?

A)£310,000

B)£250,000

C)£200,000

D)£390,000

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 42 في هذه المجموعة.

فتح الحزمة

k this deck

40

Baker Company produced 30,000 units and sold 28,000 units in 2011. Beginning inventory was zero. During the period, the following costs were incurred:

a.Absorption costing

b.Variable costing

a.Absorption costing

b.Variable costing

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 42 في هذه المجموعة.

فتح الحزمة

k this deck

41

Jensen Company produced 10,000 cases of cookies this year. It sold 9,500 cases for £10 each. There were no beginning inventories. Variable manufacturing costs were £30,000, and fixed manufacturing expenses were £50,000. Selling and administrative expenses were £10,000, all fixed.

a.Prepare income statements using the variable costing and absorption costing.

b.Reconcile the net income under absorption and variable costing.

a.Prepare income statements using the variable costing and absorption costing.

b.Reconcile the net income under absorption and variable costing.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 42 في هذه المجموعة.

فتح الحزمة

k this deck

42

Ivy, SA., produces a single product that sells for £60 per unit. There were no inventories of work in process or finished goods. Costs for the year were as follows: During the first three months of the year, production and sales in units were as follows: The company uses an actual cost system. There were no work-in-process inventories at the end of any month, and the company uses FIFO costing.

a.Determine the unit cost of production under variable costing for each of the three months.

b.Determine the unit cost of production under absorption costing for each of the three months.

c.Determine income under variable costing for each of the three months.

d.Determine income under absorption costing for each of the three months.

During the first three months of the year, production and sales in units were as follows: The company uses an actual cost system. There were no work-in-process inventories at the end of any month, and the company uses FIFO costing. a.Determine the unit cost of production under variable costing for each of the three months.

b.Determine the unit cost of production under absorption costing for each of the three months.

c.Determine income under variable costing for each of the three months.

d.Determine income under absorption costing for each of the three months.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 42 في هذه المجموعة.

فتح الحزمة

k this deck

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 42 في هذه المجموعة.