Deck 21: Accounting for Leases

ملء الشاشة (f)

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

Based solely upon the following sets of circumstances indicated below, which set gives rise to a sales-type or direct-financing lease of a lessor?Transfers Ownership Contains Bargain Collectibility of Lease Any Important

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

If the lease in a sale-leaseback transaction meets one of the four leasing criteria and is therefore accounted for as a capital lease, who records the asset on its books and which party records interest expense during the lease period?

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

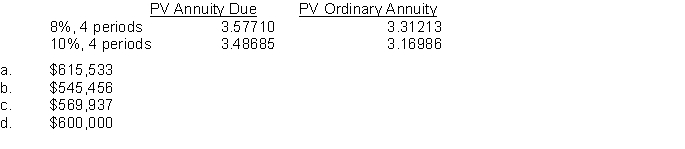

Pisa, Inc. leased equipment from Tower Company under a four-year lease requiring equal annual payments of $172,076, with the first payment due at lease inception. The lease does not transfer ownership, nor is there a bargain purchase option. The equipment has a 4-year useful life and no salvage value. If Pisa, Inc.'s incremental borrowing rate is 10% and the rate implicit in the lease (which is known by Pisa, Inc.) is 8%, what is the amount recorded for the leased asset at the lease inception?

سؤال

سؤال

Pisa, Inc. leased equipment from Tower Company under a four-year lease requiring equal annual payments of $172,076, with the first payment due at lease inception. The lease does not transfer ownership, nor is there a bargain purchase option. The equipment has a 4-year useful life and no salvage value. Pisa, Inc.'s incremental borrowing rate is 10% and the rate implicit in the lease (which is known by Pisa, Inc.) is 8%. Pisa, Inc. uses the straight-line method to depreciate similar assets. What is the amount of depreciation expense recorded by Pisa, Inc. in the first year of the asset's life?

A) $0 because the asset is depreciated by Tower Company.

B) $142,484

C) $153,883

D) $150,000

A) $0 because the asset is depreciated by Tower Company.

B) $142,484

C) $153,883

D) $150,000

سؤال

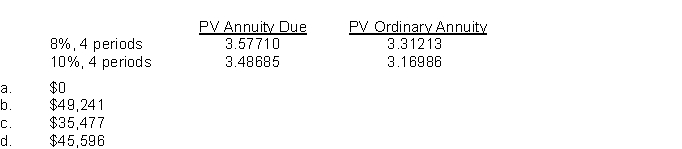

Pisa, Inc. leased equipment from Tower Company under a four-year lease requiring equal annual payments of $172,076, with the first payment due at lease inception. The lease does not transfer ownership, nor is there a bargain purchase option. The equipment has a 4-year useful life and no salvage value. Pisa, Inc.'s incremental borrowing rate is 10% and the rate implicit in the lease (which is known by Pisa, Inc.) is 8%. Assuming that this lease is properly classified as a capital lease, what is the amount of interest expense recorded by Pisa, Inc. in the first year of the asset's life?

سؤال

سؤال

سؤال

سؤال

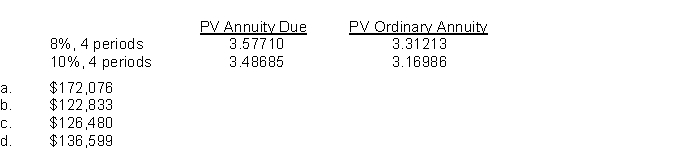

Haystack, Inc. manufactures machinery used in the mining industry. On January 2, 2015 it leased equipment with a cost of $320,000 to Silver Point Co. The 5-year lease calls for a 10% down payment and equal annual payments at the end of each year. The equipment has an expected useful life of 5 years. If the selling price of the equipment is $520,000, and the rate implicit in the lease is 8%, what are the equal annual payments?

A) $117,214

B) $108,530

C) $121,315

D) $130,237

A) $117,214

B) $108,530

C) $121,315

D) $130,237

سؤال

سؤال

سؤال

Pisa, Inc. leased equipment from Tower Company under a four-year lease requiring equal annual payments of $172,076, with the first payment due at lease inception. The lease does not transfer ownership, nor is there a bargain purchase option. The equipment has a 4 year useful life and no salvage value. Pisa, Inc.'s incremental borrowing rate is 10% and the rate implicit in the lease (which is known by Pisa, Inc.) is 8%. Assuming that this lease is properly classified as a capital lease, what is the amount of principal reduction recorded when the second lease payment is made in Year 2?

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

Haystack, Inc. manufactures machinery used in the mining industry. On January 2, 2015 it leased equipment with a cost of $320,000 to Silver Point Co. The 5-year lease calls for a 10% down payment and equal annual payments at the end of each year. The equipment has an expected useful life of 5 years. Silver Point's incremental borrowing rate is 10%, and it depreciates similar equipment using the double-declining balance method. The selling price of the equipment is $520,000, and the rate implicit in the lease is 8%, which is known to Silver Point Co. What is the amount of interest expense recorded by Silver Point Co. for the year ended December 31, 2015?

A) $46,800

B) $37,440

C) $41,600

D) $52,000

A) $46,800

B) $37,440

C) $41,600

D) $52,000

فتح الحزمة

قم بالتسجيل لفتح البطاقات في هذه المجموعة!

Unlock Deck

Unlock Deck

1/128

العب

ملء الشاشة (f)

Deck 21: Accounting for Leases

1

Leasing equipment reduces the risk of obsolescence to the lessee and in many cases passes the risk of residual value to the lessor.

True

2

Direct-financing leases are in substance the financing of an asset purchase by the lessee.

True

3

Both a guaranteed and an unguaranteed residual value affect the lessee's computation of amounts capitalized as a leased asset.

False

4

Under the operating method, the lessor records each rental receipt as part interest revenue and part rental revenue.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 128 في هذه المجموعة.

فتح الحزمة

k this deck

5

In computing the annual lease payments, the lessor deducts only a guaranteed residual value from the fair value of a leased asset.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 128 في هذه المجموعة.

فتح الحزمة

k this deck

6

The FASB agrees with the capitalization approach and requires companies to capitalize all long-term leases.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 128 في هذه المجموعة.

فتح الحزمة

k this deck

7

The gross profit amount in a sales-type lease is greater when a guaranteed residual value exists.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 128 في هذه المجموعة.

فتح الحزمة

k this deck

8

When the lessee agrees to make up any deficiency below a stated amount that the lessor realizes in residual value, that stated amount is the guaranteed residual value.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 128 في هذه المجموعة.

فتح الحزمة

k this deck

9

The primary difference between a direct-financing lease and a sales-type lease is the manufacturer's or dealer's gross profit (or loss).

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 128 في هذه المجموعة.

فتح الحزمة

k this deck

10

From the lessee's viewpoint, an unguaranteed residual value is the same as no residual value in terms of computing the minimum lease payments.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 128 في هذه المجموعة.

فتح الحزمة

k this deck

11

Executory costs should be excluded by the lessee in computing the present value of the minimum lease payments.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 128 في هذه المجموعة.

فتح الحزمة

k this deck

12

Minimum rental payments are the same as minimum lease payments.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 128 في هذه المجموعة.

فتح الحزمة

k this deck

13

The FASB requires lessees and lessors to disclose certain information about leases in their financial statements or in the notes.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 128 في هذه المجموعة.

فتح الحزمة

k this deck

14

Companies must periodically review the estimated unguaranteed residual value in a sales-type lease.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 128 في هذه المجموعة.

فتح الحزمة

k this deck

15

Lessors classify and account for all leases that don't qualify as sales-type leases as operating leases.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 128 في هذه المجموعة.

فتح الحزمة

k this deck

16

The lessor will recover a greater net investment if the residual value is guaranteed instead of unguaranteed.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 128 في هذه المجموعة.

فتح الحزمة

k this deck

17

The distinction between a direct-financing lease and a sales-type lease is the presence or absence of a transfer of title.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 128 في هذه المجموعة.

فتح الحزمة

k this deck

18

A benefit of leasing to the lessor is the return of the leased property at the end of the lease term.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 128 في هذه المجموعة.

فتح الحزمة

k this deck

19

A capitalized leased asset is always depreciated over the term of the lease by the lessee.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 128 في هذه المجموعة.

فتح الحزمة

k this deck

20

A lessee records interest expense in both a capital lease and an operating lease.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 128 في هذه المجموعة.

فتح الحزمة

k this deck

21

In order to properly record a direct-financing lease, the lessor needs to know how to calculate the lease receivable. The lease receivable in a direct-financing lease is best defined as

A) the amount of funds the lessor has tied up in the asset which is the subject of the direct-financing lease.

B) the difference between the lease payments receivable and the fair value of the leased property.

C) the present value of minimum lease payments.

D) the total book value of the asset less any accumulated depreciation recorded by the lessor prior to the lease agreement.

A) the amount of funds the lessor has tied up in the asset which is the subject of the direct-financing lease.

B) the difference between the lease payments receivable and the fair value of the leased property.

C) the present value of minimum lease payments.

D) the total book value of the asset less any accumulated depreciation recorded by the lessor prior to the lease agreement.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 128 في هذه المجموعة.

فتح الحزمة

k this deck

22

Minimum lease payments may include a

A) penalty for failure to renew.

B) bargain purchase option.

C) guaranteed residual value.

D) any of these.

A) penalty for failure to renew.

B) bargain purchase option.

C) guaranteed residual value.

D) any of these.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 128 في هذه المجموعة.

فتح الحزمة

k this deck

23

In a lease that is appropriately recorded as a direct-financing lease by the lessor, the unearned income

A) should be amortized over the period of the lease using the effective interest method.

B) should be amortized over the period of the lease using the straight-line method.

C) does not arise.

D) should be recognized at the lease's expiration.

A) should be amortized over the period of the lease using the effective interest method.

B) should be amortized over the period of the lease using the straight-line method.

C) does not arise.

D) should be recognized at the lease's expiration.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 128 في هذه المجموعة.

فتح الحزمة

k this deck

24

The methods of accounting for a lease by the lessee are

A) operating and capital lease methods.

B) operating, sales, and capital lease methods.

C) operating and leveraged lease methods.

D) None of these answers are correct.

A) operating and capital lease methods.

B) operating, sales, and capital lease methods.

C) operating and leveraged lease methods.

D) None of these answers are correct.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 128 في هذه المجموعة.

فتح الحزمة

k this deck

25

An essential element of a lease is that the

A) lessor conveys less than his or her total interest in the property.

B) lessee provides a sinking fund equal to one year's lease payments.

C) property that is the subject of the lease agreement must be held for sale by the lessor prior to the drafting of the lease agreement.

D) term of the lease is substantially equal to the economic life of the leased property.

A) lessor conveys less than his or her total interest in the property.

B) lessee provides a sinking fund equal to one year's lease payments.

C) property that is the subject of the lease agreement must be held for sale by the lessor prior to the drafting of the lease agreement.

D) term of the lease is substantially equal to the economic life of the leased property.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 128 في هذه المجموعة.

فتح الحزمة

k this deck

26

Major reasons why a company may become involved in leasing to other companies is (are)

A) interest revenue.

B) high residual values.

C) tax incentives.

D) All of these answers are correct.

A) interest revenue.

B) high residual values.

C) tax incentives.

D) All of these answers are correct.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 128 في هذه المجموعة.

فتح الحزمة

k this deck

27

Which of the following would not be included in the Lease Receivable account?

A) Guaranteed residual value

B) Unguaranteed residual value

C) A bargain purchase option

D) All would be included

A) Guaranteed residual value

B) Unguaranteed residual value

C) A bargain purchase option

D) All would be included

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 128 في هذه المجموعة.

فتح الحزمة

k this deck

28

While only certain leases are currently accounted for as a sale or purchase, there is theoretic justification for considering all leases to be sales or purchases. The principal reason that supports this idea is that

A) all leases are generally for the economic life of the property and the residual value of the property at the end of the lease is minimal.

B) at the end of the lease the property usually can be purchased by the lessee.

C) a lease reflects the purchase or sale of a quantifiable right to the use of property.

D) during the life of the lease the lessee can effectively treat the property as if it were owned.

A) all leases are generally for the economic life of the property and the residual value of the property at the end of the lease is minimal.

B) at the end of the lease the property usually can be purchased by the lessee.

C) a lease reflects the purchase or sale of a quantifiable right to the use of property.

D) during the life of the lease the lessee can effectively treat the property as if it were owned.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 128 في هذه المجموعة.

فتح الحزمة

k this deck

29

Which of the following is a correct statement of one of the capitalization criteria?

A) The lease transfers ownership of the property to the lessor.

B) The lease contains a purchase option.

C) The lease term is equal to or more than 75% of the estimated economic life of the leased property.

D) The minimum lease payments (excluding executory costs) equal or exceed 90% of the fair value of the leased property.

A) The lease transfers ownership of the property to the lessor.

B) The lease contains a purchase option.

C) The lease term is equal to or more than 75% of the estimated economic life of the leased property.

D) The minimum lease payments (excluding executory costs) equal or exceed 90% of the fair value of the leased property.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 128 في هذه المجموعة.

فتح الحزمة

k this deck

30

The amount to be recorded as the cost of an asset under capital lease is equal to the

A) present value of the minimum lease payments.

B) present value of the minimum lease payments or the fair value of the asset, whichever is lower.

C) present value of the minimum lease payments plus the present value of any unguaranteed residual value.

D) carrying value of the asset on the lessor's books.

A) present value of the minimum lease payments.

B) present value of the minimum lease payments or the fair value of the asset, whichever is lower.

C) present value of the minimum lease payments plus the present value of any unguaranteed residual value.

D) carrying value of the asset on the lessor's books.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 128 في هذه المجموعة.

فتح الحزمة

k this deck

31

A lessee with a capital lease containing a bargain purchase option should depreciate the leased asset over the

A) asset's remaining economic life.

B) term of the lease.

C) life of the asset or the term of the lease, whichever is shorter.

D) life of the asset or the term of the lease, whichever is longer.

A) asset's remaining economic life.

B) term of the lease.

C) life of the asset or the term of the lease, whichever is shorter.

D) life of the asset or the term of the lease, whichever is longer.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 128 في هذه المجموعة.

فتح الحزمة

k this deck

32

From the lessee's perspective, in the earlier years of a lease, the use of the

A) capital method will enable the lessee to report higher income, compared to the operating method.

B) capital method will cause debt to increase, compared to the operating method.

C) operating method will cause income to decrease, compared to the capital method.

D) operating method will cause debt to increase, compared to the capital method.

A) capital method will enable the lessee to report higher income, compared to the operating method.

B) capital method will cause debt to increase, compared to the operating method.

C) operating method will cause income to decrease, compared to the capital method.

D) operating method will cause debt to increase, compared to the capital method.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 128 في هذه المجموعة.

فتح الحزمة

k this deck

33

If the residual value of a leased asset is guaranteed by a third party

A) it is treated by the lessee as no residual value.

B) the third party is also liable for any lease payments not paid by the lessee.

C) the net investment to be recovered by the lessor is reduced.

D) it is treated by the lessee as an additional payment and by the lessor as realized at the end of the lease term.

A) it is treated by the lessee as no residual value.

B) the third party is also liable for any lease payments not paid by the lessee.

C) the net investment to be recovered by the lessor is reduced.

D) it is treated by the lessee as an additional payment and by the lessor as realized at the end of the lease term.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 128 في هذه المجموعة.

فتح الحزمة

k this deck

34

Based solely upon the following sets of circumstances indicated below, which set gives rise to a sales-type or direct-financing lease of a lessor?Transfers Ownership Contains Bargain Collectibility of Lease Any Important

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 128 في هذه المجموعة.

فتح الحزمة

k this deck

35

Lessees prefer to account for their leases as operating lease because:

A) it increases their debt to total equity ratio.

B) it decreases the income tax expense.

C) it increases the amount of total assets.

D) it decreases the amount of liability reported.

A) it increases their debt to total equity ratio.

B) it decreases the income tax expense.

C) it increases the amount of total assets.

D) it decreases the amount of liability reported.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 128 في هذه المجموعة.

فتح الحزمة

k this deck

36

In computing depreciation of a leased asset, the lessee should subtract

A) a guaranteed residual value and depreciate over the term of the lease.

B) an unguaranteed residual value and depreciate over the term of the lease.

C) a guaranteed residual value and depreciate over the life of the asset.

D) an unguaranteed residual value and depreciate over the life of the asset.

A) a guaranteed residual value and depreciate over the term of the lease.

B) an unguaranteed residual value and depreciate over the term of the lease.

C) a guaranteed residual value and depreciate over the life of the asset.

D) an unguaranteed residual value and depreciate over the life of the asset.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 128 في هذه المجموعة.

فتح الحزمة

k this deck

37

What impact does a bargain purchase option have on the present value of the minimum lease payments computed by the lessee?

A) There is no impact as the option does not enter into the transaction until the end of the lease term.

B) The lessee must increase the present value of the minimum lease payments by the present value of the option price.

C) The lessee must decrease the present value of the minimum lease payments by the present value of the option price.

D) The minimum lease payments would be increased by the present value of the option price if, at the time of the lease agreement, it appeared certain that the lessee would exercise the option at the end of the lease and purchase the asset at the option price.

A) There is no impact as the option does not enter into the transaction until the end of the lease term.

B) The lessee must increase the present value of the minimum lease payments by the present value of the option price.

C) The lessee must decrease the present value of the minimum lease payments by the present value of the option price.

D) The minimum lease payments would be increased by the present value of the option price if, at the time of the lease agreement, it appeared certain that the lessee would exercise the option at the end of the lease and purchase the asset at the option price.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 128 في هذه المجموعة.

فتح الحزمة

k this deck

38

Which of the following best describes current practice in accounting for leases?

A) Leases are not capitalized.

B) Leases similar to installment purchases are capitalized.

C) All long-term leases are capitalized.

D) All leases are capitalized.

A) Leases are not capitalized.

B) Leases similar to installment purchases are capitalized.

C) All long-term leases are capitalized.

D) All leases are capitalized.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 128 في هذه المجموعة.

فتح الحزمة

k this deck

39

Which of the following is an advantage of captive leasing companies over the other players in the leasing market?

A) They have access to low-cost funds allowing them to purchase assets at lower cost.

B) They are good at developing innovative contracts that help avoid accounting .

C) They provide leasing arrangements for a wider range of products than the parent company's product line.

D) They have the paint-of-sale advantage in finding leasing customers.

A) They have access to low-cost funds allowing them to purchase assets at lower cost.

B) They are good at developing innovative contracts that help avoid accounting .

C) They provide leasing arrangements for a wider range of products than the parent company's product line.

D) They have the paint-of-sale advantage in finding leasing customers.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 128 في هذه المجموعة.

فتح الحزمة

k this deck

40

In computing the present value of the minimum lease payments, the lessee should

A) use its incremental borrowing rate in all cases.

B) use either its incremental borrowing rate or the implicit rate of the lessor, whichever is higher, assuming that the implicit rate is known to the lessee.

C) use either its incremental borrowing rate or the implicit rate of the lessor, whichever is lower, assuming that the implicit rate is known to the lessee.

D) None of these answers are correct.

A) use its incremental borrowing rate in all cases.

B) use either its incremental borrowing rate or the implicit rate of the lessor, whichever is higher, assuming that the implicit rate is known to the lessee.

C) use either its incremental borrowing rate or the implicit rate of the lessor, whichever is lower, assuming that the implicit rate is known to the lessee.

D) None of these answers are correct.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 128 في هذه المجموعة.

فتح الحزمة

k this deck

41

In a sale-leaseback transaction where none of the four leasing criteria are satisfied, which of the following is false?

A) The seller-lessee removes the asset from its books.

B) The purchaser-lessor records a gain.

C) The seller-lessee records the lease as an operating lease.

D) All of the answers are false statements.

A) The seller-lessee removes the asset from its books.

B) The purchaser-lessor records a gain.

C) The seller-lessee records the lease as an operating lease.

D) All of the answers are false statements.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 128 في هذه المجموعة.

فتح الحزمة

k this deck

42

Which of the following statements is correct?

A) For direct-financing leases, initial direct costs are added to the net investment in the lease.

B) For sales-type leases, initial direct costs are expensed in the year of incurrence.

C) For operating leases, initial direct costs are deferred and allocated over the lease term.

D) All of these answers are correct.

A) For direct-financing leases, initial direct costs are added to the net investment in the lease.

B) For sales-type leases, initial direct costs are expensed in the year of incurrence.

C) For operating leases, initial direct costs are deferred and allocated over the lease term.

D) All of these answers are correct.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 128 في هذه المجموعة.

فتح الحزمة

k this deck

43

Use the following information for questions 54 through 59. (Annuity tables on page 21-25.)

On January 1, 2015, Yancey, Inc. signs a 10-year noncancelable lease agreement to lease a storage building from Holt Warehouse Company. Collectibility of lease payments is reasonably predictable and no important uncertainties surround the amount of costs yet to be incurred by the lessor. The following information pertains to this lease agreement.

(a) The agreement requires equal rental payments at the beginning each year.

(b) The fair value of the building on January 1, 2015 is $4,000,000; however, the book value to Holt is $3,300,000.

(c) The building has an estimated economic life of 10 years, with no residual value. Yancey depreciates similar buildings on the straight-line method.

(d) At the termination of the lease, the title to the building will be transferred to the lessee.

(e) Yancey's incremental borrowing rate is 11% per year. Holt Warehouse Co. set the annual rental to insure a 10% rate of return. The implicit rate of the lessor is known by Yancey, Inc.

(f) The yearly rental payment includes $10,000 of executory costs related to taxes on the property.

If the lease were nonrenewable, there was no purchase option, title to the building does not pass to the lessee at termination of the lease and the lease were only for eight years, what type of lease would this be for the lessee?

A) Sales-type lease

B) Direct-financing lease

C) Operating lease

D) Capital lease

On January 1, 2015, Yancey, Inc. signs a 10-year noncancelable lease agreement to lease a storage building from Holt Warehouse Company. Collectibility of lease payments is reasonably predictable and no important uncertainties surround the amount of costs yet to be incurred by the lessor. The following information pertains to this lease agreement.

(a) The agreement requires equal rental payments at the beginning each year.

(b) The fair value of the building on January 1, 2015 is $4,000,000; however, the book value to Holt is $3,300,000.

(c) The building has an estimated economic life of 10 years, with no residual value. Yancey depreciates similar buildings on the straight-line method.

(d) At the termination of the lease, the title to the building will be transferred to the lessee.

(e) Yancey's incremental borrowing rate is 11% per year. Holt Warehouse Co. set the annual rental to insure a 10% rate of return. The implicit rate of the lessor is known by Yancey, Inc.

(f) The yearly rental payment includes $10,000 of executory costs related to taxes on the property.

If the lease were nonrenewable, there was no purchase option, title to the building does not pass to the lessee at termination of the lease and the lease were only for eight years, what type of lease would this be for the lessee?

A) Sales-type lease

B) Direct-financing lease

C) Operating lease

D) Capital lease

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 128 في هذه المجموعة.

فتح الحزمة

k this deck

44

If the lease in a sale-leaseback transaction meets one of the four leasing criteria and is therefore accounted for as a capital lease, who records the asset on its books and which party records interest expense during the lease period?

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 128 في هذه المجموعة.

فتح الحزمة

k this deck

45

When lessors account for residual values related to leased assets, they

A) include the residual value because they always assume the residual value will be realized.

B) include the unguaranteed residual value in sales revenue.

C) recognize more gross profit on a sales-type lease with a guaranteed residual value than on a sales-type lease with an unguaranteed residual value.

D) All of the answers are true with regard to lessors and residual values.

A) include the residual value because they always assume the residual value will be realized.

B) include the unguaranteed residual value in sales revenue.

C) recognize more gross profit on a sales-type lease with a guaranteed residual value than on a sales-type lease with an unguaranteed residual value.

D) All of the answers are true with regard to lessors and residual values.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 128 في هذه المجموعة.

فتح الحزمة

k this deck

46

For a sales-type lease,

A) the sales price includes the present value of the unguaranteed residual value.

B) the present value of the guaranteed residual value is deducted to determine the cost of goods sold.

C) the gross profit will be the same whether the residual value is guaranteed or unguaranteed.

D) None of these answers are correct.

A) the sales price includes the present value of the unguaranteed residual value.

B) the present value of the guaranteed residual value is deducted to determine the cost of goods sold.

C) the gross profit will be the same whether the residual value is guaranteed or unguaranteed.

D) None of these answers are correct.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 128 في هذه المجموعة.

فتح الحزمة

k this deck

47

On December 1, 2015, Goetz Corporation leased office space for 10 years at a monthly rental of $90,000. On that date Goetz paid the landlord the following amounts: The entire amount of $990,000 was charged to rent expense in 2015. What amount should Goetz have charged to expense for the year ended December 31, 2015?

A) $90,000

B) $96,000

C) $186,000

D) $720,000

A) $90,000

B) $96,000

C) $186,000

D) $720,000

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 128 في هذه المجموعة.

فتح الحزمة

k this deck

48

The initial direct costs of leasing

A) are generally borne by the lessee.

B) include incremental costs related to internal activities of leasing, and internal costs related to costs paid to external third parties for originating a lease arrangement.

C) are expensed in the period of the sale under a sales-type lease.

D) All of the answers are true with regard to the initial direct costs of leasing.

A) are generally borne by the lessee.

B) include incremental costs related to internal activities of leasing, and internal costs related to costs paid to external third parties for originating a lease arrangement.

C) are expensed in the period of the sale under a sales-type lease.

D) All of the answers are true with regard to the initial direct costs of leasing.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 128 في هذه المجموعة.

فتح الحزمة

k this deck

49

Use the following information for questions 54 through 59. (Annuity tables on page 21-25.)

On January 1, 2015, Yancey, Inc. signs a 10-year noncancelable lease agreement to lease a storage building from Holt Warehouse Company. Collectibility of lease payments is reasonably predictable and no important uncertainties surround the amount of costs yet to be incurred by the lessor. The following information pertains to this lease agreement.

(a) The agreement requires equal rental payments at the beginning each year.

(b) The fair value of the building on January 1, 2015 is $4,000,000; however, the book value to Holt is $3,300,000.

(c) The building has an estimated economic life of 10 years, with no residual value. Yancey depreciates similar buildings on the straight-line method.

(d) At the termination of the lease, the title to the building will be transferred to the lessee.

(e) Yancey's incremental borrowing rate is 11% per year. Holt Warehouse Co. set the annual rental to insure a 10% rate of return. The implicit rate of the lessor is known by Yancey, Inc.

(f) The yearly rental payment includes $10,000 of executory costs related to taxes on the property.

From the lessee's viewpoint, what type of lease exists in this case?

A) Sales-type lease

B) Sale-leaseback

C) Capital lease

D) Operating lease

On January 1, 2015, Yancey, Inc. signs a 10-year noncancelable lease agreement to lease a storage building from Holt Warehouse Company. Collectibility of lease payments is reasonably predictable and no important uncertainties surround the amount of costs yet to be incurred by the lessor. The following information pertains to this lease agreement.

(a) The agreement requires equal rental payments at the beginning each year.

(b) The fair value of the building on January 1, 2015 is $4,000,000; however, the book value to Holt is $3,300,000.

(c) The building has an estimated economic life of 10 years, with no residual value. Yancey depreciates similar buildings on the straight-line method.

(d) At the termination of the lease, the title to the building will be transferred to the lessee.

(e) Yancey's incremental borrowing rate is 11% per year. Holt Warehouse Co. set the annual rental to insure a 10% rate of return. The implicit rate of the lessor is known by Yancey, Inc.

(f) The yearly rental payment includes $10,000 of executory costs related to taxes on the property.

From the lessee's viewpoint, what type of lease exists in this case?

A) Sales-type lease

B) Sale-leaseback

C) Capital lease

D) Operating lease

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 128 في هذه المجموعة.

فتح الحزمة

k this deck

50

The Lease Liability account should be disclosed as

A) all current liabilities.

B) all noncurrent liabilities.

C) current portions in current liabilities and the remainder in noncurrent liabilities.

D) deferred credits.

A) all current liabilities.

B) all noncurrent liabilities.

C) current portions in current liabilities and the remainder in noncurrent liabilities.

D) deferred credits.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 128 في هذه المجموعة.

فتح الحزمة

k this deck

51

The primary difference between a direct-financing lease and a sales-type lease is the

A) manner in which rental receipts are recorded as rental income.

B) amount of the depreciation recorded each year by the lessor.

C) recognition of the manufacturer's or dealer's profit at (or loss) the inception of the lease.

D) allocation of initial direct costs by the lessor to periods benefited by the lease arrangements.

A) manner in which rental receipts are recorded as rental income.

B) amount of the depreciation recorded each year by the lessor.

C) recognition of the manufacturer's or dealer's profit at (or loss) the inception of the lease.

D) allocation of initial direct costs by the lessor to periods benefited by the lease arrangements.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 128 في هذه المجموعة.

فتح الحزمة

k this deck

52

Use the following information for questions 54 through 59. (Annuity tables on page 21-25.)

On January 1, 2015, Yancey, Inc. signs a 10-year noncancelable lease agreement to lease a storage building from Holt Warehouse Company. Collectibility of lease payments is reasonably predictable and no important uncertainties surround the amount of costs yet to be incurred by the lessor. The following information pertains to this lease agreement.

(a) The agreement requires equal rental payments at the beginning each year.

(b) The fair value of the building on January 1, 2015 is $4,000,000; however, the book value to Holt is $3,300,000.

(c) The building has an estimated economic life of 10 years, with no residual value. Yancey depreciates similar buildings on the straight-line method.

(d) At the termination of the lease, the title to the building will be transferred to the lessee.

(e) Yancey's incremental borrowing rate is 11% per year. Holt Warehouse Co. set the annual rental to insure a 10% rate of return. The implicit rate of the lessor is known by Yancey, Inc.

(f) The yearly rental payment includes $10,000 of executory costs related to taxes on the property.

What is the amount of the minimum annual lease payment? (Rounded to the nearest dollar.)

A) $181,801

B) $581,801

C) $591,801

D) $601,801

On January 1, 2015, Yancey, Inc. signs a 10-year noncancelable lease agreement to lease a storage building from Holt Warehouse Company. Collectibility of lease payments is reasonably predictable and no important uncertainties surround the amount of costs yet to be incurred by the lessor. The following information pertains to this lease agreement.

(a) The agreement requires equal rental payments at the beginning each year.

(b) The fair value of the building on January 1, 2015 is $4,000,000; however, the book value to Holt is $3,300,000.

(c) The building has an estimated economic life of 10 years, with no residual value. Yancey depreciates similar buildings on the straight-line method.

(d) At the termination of the lease, the title to the building will be transferred to the lessee.

(e) Yancey's incremental borrowing rate is 11% per year. Holt Warehouse Co. set the annual rental to insure a 10% rate of return. The implicit rate of the lessor is known by Yancey, Inc.

(f) The yearly rental payment includes $10,000 of executory costs related to taxes on the property.

What is the amount of the minimum annual lease payment? (Rounded to the nearest dollar.)

A) $181,801

B) $581,801

C) $591,801

D) $601,801

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 128 في هذه المجموعة.

فتح الحزمة

k this deck

53

On January 1, 2015, Dean Corporation signed a ten-year noncancelable lease for certain machinery. The terms of the lease called for Dean to make annual payments of $150,000 at the end of each year for ten years with the title passing to Dean at the end of this period. The machinery has an estimated useful life of 15 years and no salvage value. Dean uses the straight-line method of depreciation for all of its fixed assets. Dean accordingly accounted for this lease transaction as a capital lease. The lease payments were determined to have a present value of $1,006,512 at an effective interest rate of 8%. With respect to this capitalized lease, Dean should record for 2015

A) lease expense of $150,000.

B) interest expense of $67,101 and depreciation expense of $57,102.

C) interest expense of $80,521 and depreciation expense of $67,101.

D) interest expense of $68,522 and depreciation expense of $100,652.

A) lease expense of $150,000.

B) interest expense of $67,101 and depreciation expense of $57,102.

C) interest expense of $80,521 and depreciation expense of $67,101.

D) interest expense of $68,522 and depreciation expense of $100,652.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 128 في هذه المجموعة.

فتح الحزمة

k this deck

54

When a company sells property and then leases it back, any gain on the sale should usually be

A) recognized in the current year.

B) recognized as a prior period adjustment.

C) recognized at the end of the lease.

D) deferred and recognized as income over the term of the lease.

A) recognized in the current year.

B) recognized as a prior period adjustment.

C) recognized at the end of the lease.

D) deferred and recognized as income over the term of the lease.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 128 في هذه المجموعة.

فتح الحزمة

k this deck

55

A lessor with a sales-type lease involving an unguaranteed residual value available to the lessor at the end of the lease term will report sales revenue in the period of inception of the lease at which of the following amounts?

A) The minimum lease payments plus the unguaranteed residual value.

B) The present value of the minimum lease payments.

C) The cost of the asset to the lessor, less the present value of any unguaranteed residual value.

D) The present value of the minimum lease payments plus the present value of the unguaranteed residual value.

A) The minimum lease payments plus the unguaranteed residual value.

B) The present value of the minimum lease payments.

C) The cost of the asset to the lessor, less the present value of any unguaranteed residual value.

D) The present value of the minimum lease payments plus the present value of the unguaranteed residual value.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 128 في هذه المجموعة.

فتح الحزمة

k this deck

56

To avoid leased asset capitalization, companies can devise lease agreements that fail to satisfy any of the four leasing criteria. Which of the following is not one of the ways to accomplish this goal?

A) Lessee uses a higher interest rate than that used by lessor.

B) Set the lease term at something less than 75% of the estimated useful life of the property.

C) Write in a bargain purchase option.

D) Use a third party to guarantee the asset's residual value.

A) Lessee uses a higher interest rate than that used by lessor.

B) Set the lease term at something less than 75% of the estimated useful life of the property.

C) Write in a bargain purchase option.

D) Use a third party to guarantee the asset's residual value.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 128 في هذه المجموعة.

فتح الحزمة

k this deck

57

Metcalf Company leases a machine from Vollmer Corp. under an agreement which meets the criteria to be a capital lease for Metcalf. The six-year lease requires payment of $136,000 at the beginning of each year, including $20,000 per year for maintenance, insurance, and taxes. The incremental borrowing rate for the lessee is 10%; the lessor's implicit rate is 8% and is known by the lessee. The present value of an annuity due of 1 for six years at 10% is 4.79079. The present value of an annuity due of 1 for six years at 8% is 4.99271. Metcalf should record the leased asset at

A) $679,008.

B) $651,548.

C) $579,154.

D) $555,732.

A) $679,008.

B) $651,548.

C) $579,154.

D) $555,732.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 128 في هذه المجموعة.

فتح الحزمة

k this deck

58

Use the following information for questions 54 through 59. (Annuity tables on page 21-25.)

On January 1, 2015, Yancey, Inc. signs a 10-year noncancelable lease agreement to lease a storage building from Holt Warehouse Company. Collectibility of lease payments is reasonably predictable and no important uncertainties surround the amount of costs yet to be incurred by the lessor. The following information pertains to this lease agreement.

(a) The agreement requires equal rental payments at the beginning each year.

(b) The fair value of the building on January 1, 2015 is $4,000,000; however, the book value to Holt is $3,300,000.

(c) The building has an estimated economic life of 10 years, with no residual value. Yancey depreciates similar buildings on the straight-line method.

(d) At the termination of the lease, the title to the building will be transferred to the lessee.

(e) Yancey's incremental borrowing rate is 11% per year. Holt Warehouse Co. set the annual rental to insure a 10% rate of return. The implicit rate of the lessor is known by Yancey, Inc.

(f) The yearly rental payment includes $10,000 of executory costs related to taxes on the property.

What is the amount of the total annual lease payment?

A) $181,801

B) $581,801

C) $591,801

D) $601,801

On January 1, 2015, Yancey, Inc. signs a 10-year noncancelable lease agreement to lease a storage building from Holt Warehouse Company. Collectibility of lease payments is reasonably predictable and no important uncertainties surround the amount of costs yet to be incurred by the lessor. The following information pertains to this lease agreement.

(a) The agreement requires equal rental payments at the beginning each year.

(b) The fair value of the building on January 1, 2015 is $4,000,000; however, the book value to Holt is $3,300,000.

(c) The building has an estimated economic life of 10 years, with no residual value. Yancey depreciates similar buildings on the straight-line method.

(d) At the termination of the lease, the title to the building will be transferred to the lessee.

(e) Yancey's incremental borrowing rate is 11% per year. Holt Warehouse Co. set the annual rental to insure a 10% rate of return. The implicit rate of the lessor is known by Yancey, Inc.

(f) The yearly rental payment includes $10,000 of executory costs related to taxes on the property.

What is the amount of the total annual lease payment?

A) $181,801

B) $581,801

C) $591,801

D) $601,801

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 128 في هذه المجموعة.

فتح الحزمة

k this deck

59

Use the following information for questions 54 through 59. (Annuity tables on page 21-25.)

On January 1, 2015, Yancey, Inc. signs a 10-year noncancelable lease agreement to lease a storage building from Holt Warehouse Company. Collectibility of lease payments is reasonably predictable and no important uncertainties surround the amount of costs yet to be incurred by the lessor. The following information pertains to this lease agreement.

(a) The agreement requires equal rental payments at the beginning each year.

(b) The fair value of the building on January 1, 2015 is $4,000,000; however, the book value to Holt is $3,300,000.

(c) The building has an estimated economic life of 10 years, with no residual value. Yancey depreciates similar buildings on the straight-line method.

(d) At the termination of the lease, the title to the building will be transferred to the lessee.

(e) Yancey's incremental borrowing rate is 11% per year. Holt Warehouse Co. set the annual rental to insure a 10% rate of return. The implicit rate of the lessor is known by Yancey, Inc.

(f) The yearly rental payment includes $10,000 of executory costs related to taxes on the property.

Yancey, Inc. would record depreciation expense on this storage building in 2015 of (Rounded to the nearest dollar.)

A) $0.

B) $330,000.

C) $400,000.

D) $650,981.

On January 1, 2015, Yancey, Inc. signs a 10-year noncancelable lease agreement to lease a storage building from Holt Warehouse Company. Collectibility of lease payments is reasonably predictable and no important uncertainties surround the amount of costs yet to be incurred by the lessor. The following information pertains to this lease agreement.

(a) The agreement requires equal rental payments at the beginning each year.

(b) The fair value of the building on January 1, 2015 is $4,000,000; however, the book value to Holt is $3,300,000.

(c) The building has an estimated economic life of 10 years, with no residual value. Yancey depreciates similar buildings on the straight-line method.

(d) At the termination of the lease, the title to the building will be transferred to the lessee.

(e) Yancey's incremental borrowing rate is 11% per year. Holt Warehouse Co. set the annual rental to insure a 10% rate of return. The implicit rate of the lessor is known by Yancey, Inc.

(f) The yearly rental payment includes $10,000 of executory costs related to taxes on the property.

Yancey, Inc. would record depreciation expense on this storage building in 2015 of (Rounded to the nearest dollar.)

A) $0.

B) $330,000.

C) $400,000.

D) $650,981.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 128 في هذه المجموعة.

فتح الحزمة

k this deck

60

Use the following information for questions 54 through 59. (Annuity tables on page 21-25.)

On January 1, 2015, Yancey, Inc. signs a 10-year noncancelable lease agreement to lease a storage building from Holt Warehouse Company. Collectibility of lease payments is reasonably predictable and no important uncertainties surround the amount of costs yet to be incurred by the lessor. The following information pertains to this lease agreement.

(a) The agreement requires equal rental payments at the beginning each year.

(b) The fair value of the building on January 1, 2015 is $4,000,000; however, the book value to Holt is $3,300,000.

(c) The building has an estimated economic life of 10 years, with no residual value. Yancey depreciates similar buildings on the straight-line method.

(d) At the termination of the lease, the title to the building will be transferred to the lessee.

(e) Yancey's incremental borrowing rate is 11% per year. Holt Warehouse Co. set the annual rental to insure a 10% rate of return. The implicit rate of the lessor is known by Yancey, Inc.

(f) The yearly rental payment includes $10,000 of executory costs related to taxes on the property.

From the lessor's viewpoint, what type of lease is involved?

A) Sales-type lease

B) Sale-leaseback

C) Direct-financing lease

D) Operating lease

On January 1, 2015, Yancey, Inc. signs a 10-year noncancelable lease agreement to lease a storage building from Holt Warehouse Company. Collectibility of lease payments is reasonably predictable and no important uncertainties surround the amount of costs yet to be incurred by the lessor. The following information pertains to this lease agreement.

(a) The agreement requires equal rental payments at the beginning each year.

(b) The fair value of the building on January 1, 2015 is $4,000,000; however, the book value to Holt is $3,300,000.

(c) The building has an estimated economic life of 10 years, with no residual value. Yancey depreciates similar buildings on the straight-line method.

(d) At the termination of the lease, the title to the building will be transferred to the lessee.

(e) Yancey's incremental borrowing rate is 11% per year. Holt Warehouse Co. set the annual rental to insure a 10% rate of return. The implicit rate of the lessor is known by Yancey, Inc.

(f) The yearly rental payment includes $10,000 of executory costs related to taxes on the property.

From the lessor's viewpoint, what type of lease is involved?

A) Sales-type lease

B) Sale-leaseback

C) Direct-financing lease

D) Operating lease

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 128 في هذه المجموعة.

فتح الحزمة

k this deck

61

Pisa, Inc. leased equipment from Tower Company under a four-year lease requiring equal annual payments of $172,076, with the first payment due at lease inception. The lease does not transfer ownership, nor is there a bargain purchase option. The equipment has a 4-year useful life and no salvage value. If Pisa, Inc.'s incremental borrowing rate is 10% and the rate implicit in the lease (which is known by Pisa, Inc.) is 8%, what is the amount recorded for the leased asset at the lease inception?

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 128 في هذه المجموعة.

فتح الحزمة

k this deck

62

Haystack, Inc. manufactures machinery used in the mining industry. On January 2, 2015 it leased equipment with a cost of $320,000 to Silver Point Co. The 5-year lease calls for a 10% down payment and equal annual payments of $146,518 at the end of each year. The equipment has an expected useful life of 5 years. Silver Point's incremental borrowing rate is 10%, and it depreciates similar equipment using the double-declining balance method. The selling price of the equipment is $520,000, and the rate implicit in the lease is 8%, which is known to Silver Point Co. What is the book value of the leased asset at December 31, 2015?

A) $520,000

B) $416,000

C) $312,000

D) $332,800

A) $520,000

B) $416,000

C) $312,000

D) $332,800

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 128 في هذه المجموعة.

فتح الحزمة

k this deck

63

Pisa, Inc. leased equipment from Tower Company under a four-year lease requiring equal annual payments of $172,076, with the first payment due at lease inception. The lease does not transfer ownership, nor is there a bargain purchase option. The equipment has a 4-year useful life and no salvage value. Pisa, Inc.'s incremental borrowing rate is 10% and the rate implicit in the lease (which is known by Pisa, Inc.) is 8%. Pisa, Inc. uses the straight-line method to depreciate similar assets. What is the amount of depreciation expense recorded by Pisa, Inc. in the first year of the asset's life?

A) $0 because the asset is depreciated by Tower Company.

B) $142,484

C) $153,883

D) $150,000

A) $0 because the asset is depreciated by Tower Company.

B) $142,484

C) $153,883

D) $150,000

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 128 في هذه المجموعة.

فتح الحزمة

k this deck

64

Pisa, Inc. leased equipment from Tower Company under a four-year lease requiring equal annual payments of $172,076, with the first payment due at lease inception. The lease does not transfer ownership, nor is there a bargain purchase option. The equipment has a 4-year useful life and no salvage value. Pisa, Inc.'s incremental borrowing rate is 10% and the rate implicit in the lease (which is known by Pisa, Inc.) is 8%. Assuming that this lease is properly classified as a capital lease, what is the amount of interest expense recorded by Pisa, Inc. in the first year of the asset's life?

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 128 في هذه المجموعة.

فتح الحزمة

k this deck

65

Use the following information for questions 62 and 63.

On January 1, 2014, Sauder Corporation signed a five-year noncancelable lease for equipment. The terms of the lease called for Sauder to make annual payments of $150,000 at the beginning of each year for five years with the title passing to Sauder at the end of this period. The equipment has an estimated useful life of 7 years and no salvage value. Sauder uses the straight-line method of depreciation for all of its fixed assets. Sauder accordingly accounts for this lease transaction as a capital lease. The minimum lease payments were determined to have a present value of $625,479 at an effective interest rate of 10%.

In 2015, Sauder should record interest expense of

A) $32,547.

B) $52,303.

C) $47,548.

D) $52,302.

On January 1, 2014, Sauder Corporation signed a five-year noncancelable lease for equipment. The terms of the lease called for Sauder to make annual payments of $150,000 at the beginning of each year for five years with the title passing to Sauder at the end of this period. The equipment has an estimated useful life of 7 years and no salvage value. Sauder uses the straight-line method of depreciation for all of its fixed assets. Sauder accordingly accounts for this lease transaction as a capital lease. The minimum lease payments were determined to have a present value of $625,479 at an effective interest rate of 10%.

In 2015, Sauder should record interest expense of

A) $32,547.

B) $52,303.

C) $47,548.

D) $52,302.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 128 في هذه المجموعة.

فتح الحزمة

k this deck

66

Use the following information for questions 75 through 80. (Annuity tables on page 21-25.)

Alt Corporation enters into an agreement with Yates Rentals Co. on January 1, 2015 for the purpose of leasing a machine to be used in its manufacturing operations. The following data pertain to the agreement:

(a) The term of the noncancelable lease is 3 years with no renewal option. Payments of $287,432 are due on January 1 of each year.

(b) The fair value of the machine on January 1, 2015, is $800,000. The machine has a remaining economic life of 10 years, with no salvage value. The machine reverts to the lessor upon the termination of the lease.

(c) Alt depreciates all machinery it owns on a straight-line basis.

(d) Alt's incremental borrowing rate is 10% per year. Alt does not have knowledge of the 8% implicit rate used by Yates.

(e) Immediately after signing the lease, Yates finds out that Alt Corp. is the defendant in a suit which is sufficiently material to make collectibility of future lease payments doubtful.

If Alt accounts for the lease as an operating lease, what expenses will be recorded as a consequence of the lease during the fiscal year ended December 31, 2015?

A) Depreciation Expense

B) Rent Expense

C) Interest Expense

D) Depreciation Expense and Interest Expense

Alt Corporation enters into an agreement with Yates Rentals Co. on January 1, 2015 for the purpose of leasing a machine to be used in its manufacturing operations. The following data pertain to the agreement:

(a) The term of the noncancelable lease is 3 years with no renewal option. Payments of $287,432 are due on January 1 of each year.

(b) The fair value of the machine on January 1, 2015, is $800,000. The machine has a remaining economic life of 10 years, with no salvage value. The machine reverts to the lessor upon the termination of the lease.

(c) Alt depreciates all machinery it owns on a straight-line basis.

(d) Alt's incremental borrowing rate is 10% per year. Alt does not have knowledge of the 8% implicit rate used by Yates.

(e) Immediately after signing the lease, Yates finds out that Alt Corp. is the defendant in a suit which is sufficiently material to make collectibility of future lease payments doubtful.

If Alt accounts for the lease as an operating lease, what expenses will be recorded as a consequence of the lease during the fiscal year ended December 31, 2015?

A) Depreciation Expense

B) Rent Expense

C) Interest Expense

D) Depreciation Expense and Interest Expense

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 128 في هذه المجموعة.

فتح الحزمة

k this deck

67

Use the following information for questions 75 through 80. (Annuity tables on page 21-25.)

Alt Corporation enters into an agreement with Yates Rentals Co. on January 1, 2015 for the purpose of leasing a machine to be used in its manufacturing operations. The following data pertain to the agreement:

(a) The term of the noncancelable lease is 3 years with no renewal option. Payments of $287,432 are due on January 1 of each year.

(b) The fair value of the machine on January 1, 2015, is $800,000. The machine has a remaining economic life of 10 years, with no salvage value. The machine reverts to the lessor upon the termination of the lease.

(c) Alt depreciates all machinery it owns on a straight-line basis.

(d) Alt's incremental borrowing rate is 10% per year. Alt does not have knowledge of the 8% implicit rate used by Yates.

(e) Immediately after signing the lease, Yates finds out that Alt Corp. is the defendant in a suit which is sufficiently material to make collectibility of future lease payments doubtful.

If Yates records this lease as a direct-financing lease, what amount would be recorded as Lease Receivable at the inception of the lease?

A) $287,432

B) $786,282

C) $800,000

D) $862,296

Alt Corporation enters into an agreement with Yates Rentals Co. on January 1, 2015 for the purpose of leasing a machine to be used in its manufacturing operations. The following data pertain to the agreement:

(a) The term of the noncancelable lease is 3 years with no renewal option. Payments of $287,432 are due on January 1 of each year.

(b) The fair value of the machine on January 1, 2015, is $800,000. The machine has a remaining economic life of 10 years, with no salvage value. The machine reverts to the lessor upon the termination of the lease.

(c) Alt depreciates all machinery it owns on a straight-line basis.

(d) Alt's incremental borrowing rate is 10% per year. Alt does not have knowledge of the 8% implicit rate used by Yates.

(e) Immediately after signing the lease, Yates finds out that Alt Corp. is the defendant in a suit which is sufficiently material to make collectibility of future lease payments doubtful.

If Yates records this lease as a direct-financing lease, what amount would be recorded as Lease Receivable at the inception of the lease?

A) $287,432

B) $786,282

C) $800,000

D) $862,296

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 128 في هذه المجموعة.

فتح الحزمة

k this deck

68

Haystack, Inc. manufactures machinery used in the mining industry. On January 2, 2015 it leased equipment with a cost of $320,000 to Silver Point Co. The 5-year lease calls for a 10% down payment and equal annual payments at the end of each year. The equipment has an expected useful life of 5 years. If the selling price of the equipment is $520,000, and the rate implicit in the lease is 8%, what are the equal annual payments?

A) $117,214

B) $108,530

C) $121,315

D) $130,237

A) $117,214

B) $108,530

C) $121,315

D) $130,237

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 128 في هذه المجموعة.

فتح الحزمة

k this deck

69

Use the following information for questions 75 through 80. (Annuity tables on page 21-25.)

Alt Corporation enters into an agreement with Yates Rentals Co. on January 1, 2015 for the purpose of leasing a machine to be used in its manufacturing operations. The following data pertain to the agreement:

(a) The term of the noncancelable lease is 3 years with no renewal option. Payments of $287,432 are due on January 1 of each year.

(b) The fair value of the machine on January 1, 2015, is $800,000. The machine has a remaining economic life of 10 years, with no salvage value. The machine reverts to the lessor upon the termination of the lease.

(c) Alt depreciates all machinery it owns on a straight-line basis.

(d) Alt's incremental borrowing rate is 10% per year. Alt does not have knowledge of the 8% implicit rate used by Yates.

(e) Immediately after signing the lease, Yates finds out that Alt Corp. is the defendant in a suit which is sufficiently material to make collectibility of future lease payments doubtful.

Which of the following lease-related revenue and expense items would be recorded by Yates if the lease is accounted for as an operating lease?

A) Rent Revenue only

B) Interest Revenue only

C) Depreciation Expense only

D) Rent Revenue and Depreciation Expense

Alt Corporation enters into an agreement with Yates Rentals Co. on January 1, 2015 for the purpose of leasing a machine to be used in its manufacturing operations. The following data pertain to the agreement:

(a) The term of the noncancelable lease is 3 years with no renewal option. Payments of $287,432 are due on January 1 of each year.

(b) The fair value of the machine on January 1, 2015, is $800,000. The machine has a remaining economic life of 10 years, with no salvage value. The machine reverts to the lessor upon the termination of the lease.

(c) Alt depreciates all machinery it owns on a straight-line basis.

(d) Alt's incremental borrowing rate is 10% per year. Alt does not have knowledge of the 8% implicit rate used by Yates.

(e) Immediately after signing the lease, Yates finds out that Alt Corp. is the defendant in a suit which is sufficiently material to make collectibility of future lease payments doubtful.

Which of the following lease-related revenue and expense items would be recorded by Yates if the lease is accounted for as an operating lease?

A) Rent Revenue only

B) Interest Revenue only

C) Depreciation Expense only

D) Rent Revenue and Depreciation Expense

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 128 في هذه المجموعة.

فتح الحزمة

k this deck

70

Use the following information for questions 75 through 80. (Annuity tables on page 21-25.)

Alt Corporation enters into an agreement with Yates Rentals Co. on January 1, 2015 for the purpose of leasing a machine to be used in its manufacturing operations. The following data pertain to the agreement:

(a) The term of the noncancelable lease is 3 years with no renewal option. Payments of $287,432 are due on January 1 of each year.

(b) The fair value of the machine on January 1, 2015, is $800,000. The machine has a remaining economic life of 10 years, with no salvage value. The machine reverts to the lessor upon the termination of the lease.

(c) Alt depreciates all machinery it owns on a straight-line basis.

(d) Alt's incremental borrowing rate is 10% per year. Alt does not have knowledge of the 8% implicit rate used by Yates.

(e) Immediately after signing the lease, Yates finds out that Alt Corp. is the defendant in a suit which is sufficiently material to make collectibility of future lease payments doubtful.

What type of lease is this from Alt Corporation's viewpoint?

A) Operating lease

B) Capital lease

C) Sales-type lease

D) Direct-financing lease

Alt Corporation enters into an agreement with Yates Rentals Co. on January 1, 2015 for the purpose of leasing a machine to be used in its manufacturing operations. The following data pertain to the agreement:

(a) The term of the noncancelable lease is 3 years with no renewal option. Payments of $287,432 are due on January 1 of each year.

(b) The fair value of the machine on January 1, 2015, is $800,000. The machine has a remaining economic life of 10 years, with no salvage value. The machine reverts to the lessor upon the termination of the lease.

(c) Alt depreciates all machinery it owns on a straight-line basis.

(d) Alt's incremental borrowing rate is 10% per year. Alt does not have knowledge of the 8% implicit rate used by Yates.

(e) Immediately after signing the lease, Yates finds out that Alt Corp. is the defendant in a suit which is sufficiently material to make collectibility of future lease payments doubtful.

What type of lease is this from Alt Corporation's viewpoint?

A) Operating lease

B) Capital lease

C) Sales-type lease

D) Direct-financing lease

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 128 في هذه المجموعة.

فتح الحزمة

k this deck

71

Pisa, Inc. leased equipment from Tower Company under a four-year lease requiring equal annual payments of $172,076, with the first payment due at lease inception. The lease does not transfer ownership, nor is there a bargain purchase option. The equipment has a 4 year useful life and no salvage value. Pisa, Inc.'s incremental borrowing rate is 10% and the rate implicit in the lease (which is known by Pisa, Inc.) is 8%. Assuming that this lease is properly classified as a capital lease, what is the amount of principal reduction recorded when the second lease payment is made in Year 2?

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 128 في هذه المجموعة.

فتح الحزمة

k this deck

72

Use the following information for questions 62 and 63.

On January 1, 2014, Sauder Corporation signed a five-year noncancelable lease for equipment. The terms of the lease called for Sauder to make annual payments of $150,000 at the beginning of each year for five years with the title passing to Sauder at the end of this period. The equipment has an estimated useful life of 7 years and no salvage value. Sauder uses the straight-line method of depreciation for all of its fixed assets. Sauder accordingly accounts for this lease transaction as a capital lease. The minimum lease payments were determined to have a present value of $625,479 at an effective interest rate of 10%.

In 2014, Sauder should record interest expense of

A) $47,548.

B) $87,453.

C) $62,547.

D) $102,453.

On January 1, 2014, Sauder Corporation signed a five-year noncancelable lease for equipment. The terms of the lease called for Sauder to make annual payments of $150,000 at the beginning of each year for five years with the title passing to Sauder at the end of this period. The equipment has an estimated useful life of 7 years and no salvage value. Sauder uses the straight-line method of depreciation for all of its fixed assets. Sauder accordingly accounts for this lease transaction as a capital lease. The minimum lease payments were determined to have a present value of $625,479 at an effective interest rate of 10%.

In 2014, Sauder should record interest expense of

A) $47,548.

B) $87,453.

C) $62,547.

D) $102,453.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 128 في هذه المجموعة.

فتح الحزمة

k this deck

73

Use the following information for questions 65 and 66.

On January 1, 2014, Ogleby Corporation signed a five-year noncancelable lease for equipment. The terms of the lease called for Ogleby to make annual payments of $90,000 at the beginning of each year for five years with title passing to Ogleby at the end of this period. The equipment has an estimated useful life of 7 years and no salvage value. Ogleby uses the straight-line method of depreciation for all of its fixed assets. Ogleby accordingly accounts for this lease transaction as a capital lease. The minimum lease payments were determined to have a present value of $375,289 at an effective interest rate of 10%.

With respect to this capitalized lease, for 2014 Ogleby should record

A) rent expense of $90,000.

B) interest expense of $28,529 and depreciation expense of $75,058.

C) interest expense of $28,529 and depreciation expense of $53,613.

D) interest expense of $45,000 and depreciation expense of $90,978.

On January 1, 2014, Ogleby Corporation signed a five-year noncancelable lease for equipment. The terms of the lease called for Ogleby to make annual payments of $90,000 at the beginning of each year for five years with title passing to Ogleby at the end of this period. The equipment has an estimated useful life of 7 years and no salvage value. Ogleby uses the straight-line method of depreciation for all of its fixed assets. Ogleby accordingly accounts for this lease transaction as a capital lease. The minimum lease payments were determined to have a present value of $375,289 at an effective interest rate of 10%.

With respect to this capitalized lease, for 2014 Ogleby should record

A) rent expense of $90,000.

B) interest expense of $28,529 and depreciation expense of $75,058.

C) interest expense of $28,529 and depreciation expense of $53,613.

D) interest expense of $45,000 and depreciation expense of $90,978.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 128 في هذه المجموعة.

فتح الحزمة

k this deck

74

Use the following information for questions 65 and 66.

On January 1, 2014, Ogleby Corporation signed a five-year noncancelable lease for equipment. The terms of the lease called for Ogleby to make annual payments of $90,000 at the beginning of each year for five years with title passing to Ogleby at the end of this period. The equipment has an estimated useful life of 7 years and no salvage value. Ogleby uses the straight-line method of depreciation for all of its fixed assets. Ogleby accordingly accounts for this lease transaction as a capital lease. The minimum lease payments were determined to have a present value of $375,289 at an effective interest rate of 10%.

With respect to this capitalized lease, for 2015 Ogleby should record

A) interest expense of $28,529 and depreciation expense of $53,613.

B) interest expense of $37,529 and depreciation expense of $53,613.

C) interest expense of $22,382 and depreciation expense of $53,613.

D) interest expense of $31,382 and depreciation expense of $53,613.

On January 1, 2014, Ogleby Corporation signed a five-year noncancelable lease for equipment. The terms of the lease called for Ogleby to make annual payments of $90,000 at the beginning of each year for five years with title passing to Ogleby at the end of this period. The equipment has an estimated useful life of 7 years and no salvage value. Ogleby uses the straight-line method of depreciation for all of its fixed assets. Ogleby accordingly accounts for this lease transaction as a capital lease. The minimum lease payments were determined to have a present value of $375,289 at an effective interest rate of 10%.

With respect to this capitalized lease, for 2015 Ogleby should record

A) interest expense of $28,529 and depreciation expense of $53,613.

B) interest expense of $37,529 and depreciation expense of $53,613.

C) interest expense of $22,382 and depreciation expense of $53,613.

D) interest expense of $31,382 and depreciation expense of $53,613.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 128 في هذه المجموعة.

فتح الحزمة

k this deck

75

Use the following information for questions 75 through 80. (Annuity tables on page 21-25.)

Alt Corporation enters into an agreement with Yates Rentals Co. on January 1, 2015 for the purpose of leasing a machine to be used in its manufacturing operations. The following data pertain to the agreement:

(a) The term of the noncancelable lease is 3 years with no renewal option. Payments of $287,432 are due on January 1 of each year.

(b) The fair value of the machine on January 1, 2015, is $800,000. The machine has a remaining economic life of 10 years, with no salvage value. The machine reverts to the lessor upon the termination of the lease.

(c) Alt depreciates all machinery it owns on a straight-line basis.

(d) Alt's incremental borrowing rate is 10% per year. Alt does not have knowledge of the 8% implicit rate used by Yates.

(e) Immediately after signing the lease, Yates finds out that Alt Corp. is the defendant in a suit which is sufficiently material to make collectibility of future lease payments doubtful.

If the present value of the future lease payments is $800,000 at January 1, 2015, what is the amount of the reduction in the lease liability for Alt Corp. in the second full year of the lease if Alt Corp. accounts for the lease as a capital lease? (Rounded to the nearest dollar.)

A) $207,426

B) $223,426

C) $236,175

D) $228,175

Alt Corporation enters into an agreement with Yates Rentals Co. on January 1, 2015 for the purpose of leasing a machine to be used in its manufacturing operations. The following data pertain to the agreement: