Deck 11: Standard Costs and Variance Analysis

ملء الشاشة (f)

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

Baldwin, Inc uses a standard job cost system and purchased 25,000 kg of material at $6 per kg, and used it all. The standard amount allowed for the output achieved is 22,500 kg, and the standard price is $6.50 per kg. The company also incurred 37,500 direct labour hours for $450,000. The standard hourly price was $11 per hour, and 39,000 hours were allowed at standard. Assuming all variances are immaterial, answer the following questions:

The entry to record the direct material price variance will include a:

The entry to record the direct material price variance will include a:

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

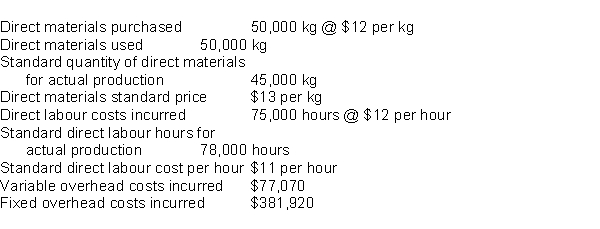

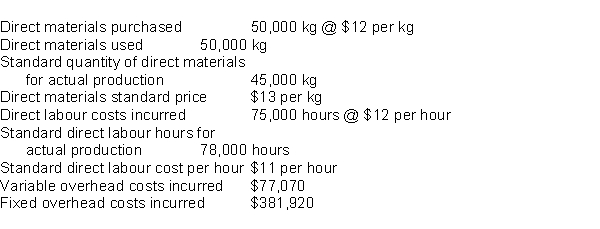

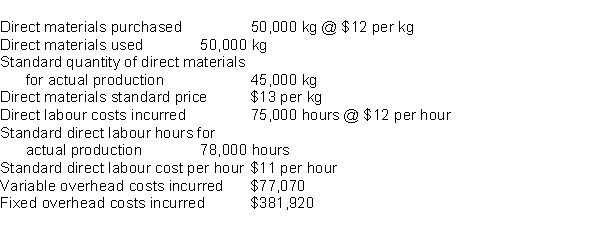

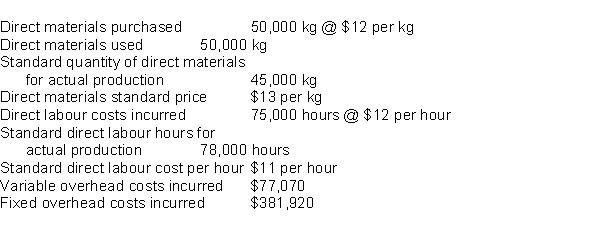

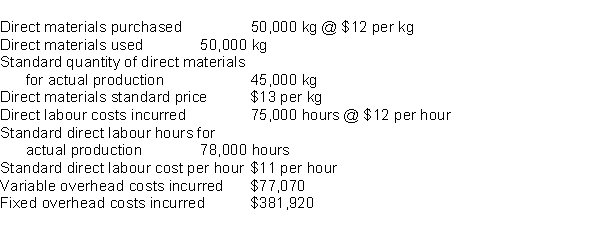

Mason, Inc. uses a standard costing system. Overhead costs are allocated based on direct labour hours. The standard variable overhead and fixed overhead rates are $1 and $5 per direct labour hour, respectively. Data relevant for the current period include:  The cost of direct materials added to work in process would be:

The cost of direct materials added to work in process would be:

A) $540,000

B) $585,000

C) $600,000

D) $650,000

The cost of direct materials added to work in process would be:A) $540,000

B) $585,000

C) $600,000

D) $650,000

سؤال

سؤال

سؤال

سؤال

Mason, Inc. uses a standard costing system. Overhead costs are allocated based on direct labour hours. The standard variable overhead and fixed overhead rates are $1 and $5 per direct labour hour, respectively. Data relevant for the current period include:  The direct materials efficiency variance is:

The direct materials efficiency variance is:

A) $60,000 Favourable

B) $60,000 Unfavourable

C) $65,000 Favourable

D) $65,000 Unfavourable

The direct materials efficiency variance is:A) $60,000 Favourable

B) $60,000 Unfavourable

C) $65,000 Favourable

D) $65,000 Unfavourable

سؤال

Mason, Inc. uses a standard costing system. Overhead costs are allocated based on direct labour hours. The standard variable overhead and fixed overhead rates are $1 and $5 per direct labour hour, respectively. Data relevant for the current period include:  The variable overhead spending variance is:

The variable overhead spending variance is:

A) $930 Favourable

B) $2,070 Unfavourable

C) $33,000 Unfavourable

D) $3,300 Unfavourable

The variable overhead spending variance is:A) $930 Favourable

B) $2,070 Unfavourable

C) $33,000 Unfavourable

D) $3,300 Unfavourable

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

Mason, Inc. uses a standard costing system. Overhead costs are allocated based on direct labour hours. The standard variable overhead and fixed overhead rates are $1 and $5 per direct labour hour, respectively. Data relevant for the current period include:  The direct labour price variance is:

The direct labour price variance is:

A) $30,000 Favourable

B) $30,000 Unfavourable

C) $75,000 Unfavourable

D) $78,000 Unfavourable

The direct labour price variance is:A) $30,000 Favourable

B) $30,000 Unfavourable

C) $75,000 Unfavourable

D) $78,000 Unfavourable

سؤال

سؤال

Mason, Inc. uses a standard costing system. Overhead costs are allocated based on direct labour hours. The standard variable overhead and fixed overhead rates are $1 and $5 per direct labour hour, respectively. Data relevant for the current period include:  The purchase of direct materials would be recorded in direct materials inventory at:

The purchase of direct materials would be recorded in direct materials inventory at:

A) $540,000

B) $585,000

C) $600,000

D) $650,000

The purchase of direct materials would be recorded in direct materials inventory at:A) $540,000

B) $585,000

C) $600,000

D) $650,000

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

فتح الحزمة

قم بالتسجيل لفتح البطاقات في هذه المجموعة!

Unlock Deck

Unlock Deck

1/128

العب

ملء الشاشة (f)

Deck 11: Standard Costs and Variance Analysis

1

Normal fluctuations in labour hours may cause a favourable direct labour efficiency variance.

True

2

A standard cost variance is a difference between a standard cost and an actual cost.

True

3

A contract with a new supplier may cause an unfavourable materials price variance.

True

4

The direct materials efficiency variance tells managers about the efficiency of the purchasing process.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 128 في هذه المجموعة.

فتح الحزمة

k this deck

5

If a variance is considered material, it should be allocated to work in process inventory, finished goods inventory, and cost of goods sold.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 128 في هذه المجموعة.

فتح الحزمة

k this deck

6

The cost categories that are measured and monitored in a given organization depend, in part, on the costs that managers consider important.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 128 في هذه المجموعة.

فتح الحزمة

k this deck

7

Unreasonable standards may be the cause of direct materials variances, but not of direct labour variances.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 128 في هذه المجموعة.

فتح الحزمة

k this deck

8

If a variance is unfavourable, it should be closed directly to cost of goods sold.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 128 في هذه المجموعة.

فتح الحزمة

k this deck

9

The total direct labour variance can be broken down into two components: the efficiency variance and the price variance.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 128 في هذه المجموعة.

فتح الحزمة

k this deck

10

Calculating variances is a necessary, but not sufficient, step for completing a variance analysis.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 128 في هذه المجموعة.

فتح الحزمة

k this deck

11

The standard cost of direct materials is computed as the standard price per unit of input times the standard quantity per unit of input.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 128 في هذه المجموعة.

فتح الحزمة

k this deck

12

Identifying the reasons for variances is usually a quick and easy process.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 128 في هذه المجموعة.

فتح الحزمة

k this deck

13

The fixed overhead spending variance is normally zero because fixed costs are constant within a relevant range of activity.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 128 في هذه المجموعة.

فتح الحزمة

k this deck

14

The variable overhead budget variance is the difference between allocated variable overhead cost and actual variable overhead cost.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 128 في هذه المجموعة.

فتح الحزمة

k this deck

15

The fixed overhead budget variance can be broken down into two parts: the spending variance and the production volume variance.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 128 في هذه المجموعة.

فتح الحزمة

k this deck

16

If the total variances in the accounting information system are favourable, accountants must adjust some accounts by decreasing costs during the closing process.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 128 في هذه المجموعة.

فتح الحزمة

k this deck

17

Errors in the accounting records related to actual production output could lead to a fixed overhead production volume variance.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 128 في هذه المجموعة.

فتح الحزمة

k this deck

18

Variance analysis is used for monitoring and performance evaluation.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 128 في هذه المجموعة.

فتح الحزمة

k this deck

19

The total standard cost for a unit of output is the sum of the standard costs for the resources used in production.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 128 في هذه المجموعة.

فتح الحزمة

k this deck

20

The direct materials price variance is often based on materials purchased, rather than on materials used.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 128 في هذه المجموعة.

فتح الحزمة

k this deck

21

Burkett Company uses a standard cost system. Indirect costs were budgeted at $200,000 plus $15 per direct labour hour. The overhead rate is based on 10,000 hours. Actual results were: The over- or underapplied overhead was:

A) $50,000 under

B) $10,000 over

C) $60,000 under

D) $20,000 over

A) $50,000 under

B) $10,000 over

C) $60,000 under

D) $20,000 over

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 128 في هذه المجموعة.

فتح الحزمة

k this deck

22

Hogle Mfg. Co. uses a standard costing system. The standard time to produce one unit is 4 hours, and normal production is 3,000 units monthly. Overhead costs were estimated to be $135,000. The standard variable overhead rate is $5 per machine hour. During April the following results were recorded: The total overhead allocated was:

A) $135,000

B) $139,500

C) $141,500

D) $137,000

A) $135,000

B) $139,500

C) $141,500

D) $137,000

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 128 في هذه المجموعة.

فتح الحزمة

k this deck

23

Hogle Mfg. Co. uses a standard costing system. The standard time to produce one unit is 4 hours, and normal production is 3,000 units monthly. Overhead costs were estimated to be $135,000. The standard variable overhead rate is $5 per machine hour. During April the following results were recorded: The variable overhead efficiency variance was:

A) $8,000 U

B) $4,000U

C) $2,000 U

D) $4,000 F

A) $8,000 U

B) $4,000U

C) $2,000 U

D) $4,000 F

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 128 في هذه المجموعة.

فتح الحزمة

k this deck

24

Hogle Mfg. Co. uses a standard costing system. The standard time to produce one unit is 4 hours, and normal production is 3,000 units monthly. Overhead costs were estimated to be $135,000. The standard variable overhead rate is $5 per machine hour. During April the following results were recorded: The combined fixed and variable overhead spending variance was:

A) $1,000 U

B) $2,000 F

C) $7,000 U

D) $3,000 F

A) $1,000 U

B) $2,000 F

C) $7,000 U

D) $3,000 F

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 128 في هذه المجموعة.

فتح الحزمة

k this deck

25

Hyteck, Inc. is a capital intensive firm. Indirect costs make up nearly 70% of the product costs. The company has no direct material costs because customers provide the direct materials used for each job. To plan and control such costs, the firm employs flexible budgets and standard costs. Overhead rates, based on direct labour hours, are derived from the master budget. The direct labour price variance was:

A) $2,000 F

B) $2,800 U

C) $1,000 U

D) $1,000 F

A) $2,000 F

B) $2,800 U

C) $1,000 U

D) $1,000 F

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 128 في هذه المجموعة.

فتح الحزمة

k this deck

26

Hyteck, Inc. is a capital intensive firm. Indirect costs make up nearly 70% of the product costs. The company has no direct material costs because customers provide the direct materials used for each job. To plan and control such costs, the firm employs flexible budgets and standard costs. Overhead rates, based on direct labour hours, are derived from the master budget. The fixed overhead production volume variance was:

A) $9,000 U

B) $2,000 F

C) $7,000 U

D) $2,800 U

A) $9,000 U

B) $2,000 F

C) $7,000 U

D) $2,800 U

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 128 في هذه المجموعة.

فتح الحزمة

k this deck

27

Welch Company budgeted the following cost standards for the current year: Direct materials kilograms per unit per kilogram

Direct labour hours per unit per hour

Actual production and costs were as follows:

Units produced

Direct materials used

Direct materials purchased a cost of

Direct labour incurred hours at a cost of

The labour price variance was:

A) $600 F

B) $400 U

C) $4,800 F

D) $1,000 U

Direct labour hours per unit per hour

Actual production and costs were as follows:

Units produced

Direct materials used

Direct materials purchased a cost of

Direct labour incurred hours at a cost of

The labour price variance was:

A) $600 F

B) $400 U

C) $4,800 F

D) $1,000 U

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 128 في هذه المجموعة.

فتح الحزمة

k this deck

28

Hyteck, Inc. is a capital intensive firm. Indirect costs make up nearly 70% of the product costs. The company has no direct material costs because customers provide the direct materials used for each job. To plan and control such costs, the firm employs flexible budgets and standard costs. Overhead rates, based on direct labour hours, are derived from the master budget. The budget variance for variable overhead was:

A) $2,800 U

B) $7,000 U

C) $4,400 U

D) $9,000 U

A) $2,800 U

B) $7,000 U

C) $4,400 U

D) $9,000 U

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 128 في هذه المجموعة.

فتح الحزمة

k this deck

29

Hogle Mfg. Co. uses a standard costing system. The standard time to produce one unit is 4 hours, and normal production is 3,000 units monthly. Overhead costs were estimated to be $135,000. The standard variable overhead rate is $5 per machine hour. During April the following results were recorded: The fixed overhead production volume variance was:

A) $1,000 U

B) $2,500 F

C) $1,500 F

D) $5,000 U

A) $1,000 U

B) $2,500 F

C) $1,500 F

D) $5,000 U

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 128 في هذه المجموعة.

فتح الحزمة

k this deck

30

Baldwin, Inc uses a standard job cost system and purchased 25,000 kg of material at $6 per kg, and used it all. The standard amount allowed for the output achieved is 22,500 kg, and the standard price is $6.50 per kg. The company also incurred 37,500 direct labour hours for $450,000. The standard hourly price was $11 per hour, and 39,000 hours were allowed at standard. Assuming all variances are immaterial, answer the following questions:

The entry to record the direct material price variance will include a:

The entry to record the direct material price variance will include a:

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 128 في هذه المجموعة.

فتح الحزمة

k this deck

31

Burkett Company uses a standard cost system. Indirect costs were budgeted at $200,000 plus $15 per direct labour hour. The overhead rate is based on 10,000 hours. Actual results were: The variable overhead efficiency variance was:

A) $10,000 F

B) $50,000 U

C) $35,000 U

D) $15,000 U

A) $10,000 F

B) $50,000 U

C) $35,000 U

D) $15,000 U

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 128 في هذه المجموعة.

فتح الحزمة

k this deck

32

Variance analysis can be used for both costs and revenues.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 128 في هذه المجموعة.

فتح الحزمة

k this deck

33

Welch Company budgeted the following cost standards for the current year: Direct materials kilograms per unit per kilogram

Direct labour hours per unit per hour

Actual production and costs were as follows:

Units produced

Direct materials used

Direct materials purchased a cost of

Direct labour incurred hours at a cost of

The labour efficiency variance was:

A) $600 F

B) $400 U

C) $4,800 F

D) $1,000 U

Direct labour hours per unit per hour

Actual production and costs were as follows:

Units produced

Direct materials used

Direct materials purchased a cost of

Direct labour incurred hours at a cost of

The labour efficiency variance was:

A) $600 F

B) $400 U

C) $4,800 F

D) $1,000 U

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 128 في هذه المجموعة.

فتح الحزمة

k this deck

34

Welch Company budgeted the following cost standards for the current year: Direct materials kilograms per unit per kilogram

Direct labour hours per unit per hour

Actual production and costs were as follows:

Units produced

Direct materials used

Direct materials purchased a cost of

Direct labour incurred hours at a cost of The material price variance for materials purchased was:

A) $1,650 F

B) $870 U

C) $2,520 U

D) $780 F

Direct labour hours per unit per hour

Actual production and costs were as follows:

Units produced

Direct materials used

Direct materials purchased a cost of

Direct labour incurred hours at a cost of The material price variance for materials purchased was:

A) $1,650 F

B) $870 U

C) $2,520 U

D) $780 F

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 128 في هذه المجموعة.

فتح الحزمة

k this deck

35

Hyteck, Inc. is a capital intensive firm. Indirect costs make up nearly 70% of the product costs. The company has no direct material costs because customers provide the direct materials used for each job. To plan and control such costs, the firm employs flexible budgets and standard costs. Overhead rates, based on direct labour hours, are derived from the master budget. The variable overhead spending variance was:

A) $1,200 F

B) $2,000 F

C) $2,800 U

D) $1,600 U

A) $1,200 F

B) $2,000 F

C) $2,800 U

D) $1,600 U

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 128 في هذه المجموعة.

فتح الحزمة

k this deck

36

Burkett Company uses a standard cost system. Indirect costs were budgeted at $200,000 plus $15 per direct labour hour. The overhead rate is based on 10,000 hours. Actual results were: The fixed overhead production volume variance was:

A) $15,000 F

B) $20,000 U

C) $10,000 F

D) $10,000 U

A) $15,000 F

B) $20,000 U

C) $10,000 F

D) $10,000 U

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 128 في هذه المجموعة.

فتح الحزمة

k this deck

37

Hyteck, Inc. is a capital intensive firm. Indirect costs make up nearly 70% of the product costs. The company has no direct material costs because customers provide the direct materials used for each job. To plan and control such costs, the firm employs flexible budgets and standard costs. Overhead rates, based on direct labour hours, are derived from the master budget.

The direct labour efficiency variance was:

A) $2,000 F

B) $2,800 U

C) $1,000 U

D) $1,000 F

The direct labour efficiency variance was:

A) $2,000 F

B) $2,800 U

C) $1,000 U

D) $1,000 F

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 128 في هذه المجموعة.

فتح الحزمة

k this deck

38

Hyteck, Inc. is a capital intensive firm. Indirect costs make up nearly 70% of the product costs. The company has no direct material costs because customers provide the direct materials used for each job. To plan and control such costs, the firm employs flexible budgets and standard costs. Overhead rates, based on direct labour hours, are derived from the master budget. The fixed overhead spending variance was:

A) $9,000 U

B) $2,000 F

C) $7,000 U

D) $2,800 U

A) $9,000 U

B) $2,000 F

C) $7,000 U

D) $2,800 U

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 128 في هذه المجموعة.

فتح الحزمة

k this deck

39

Welch Company budgeted the following cost standards for the current year: Direct materials kilograms per unit per kilogram

Direct labour hours per unit per hour

Actual production and costs were as follows:

Units produced

Direct materials used

Direct materials purchased a cost of

Direct labour incurred hours at a cost of

The material efficiency variance was:

A) $1,650 F

B) $870 U

C) $2,520 U

D) $780 F

Direct labour hours per unit per hour

Actual production and costs were as follows:

Units produced

Direct materials used

Direct materials purchased a cost of

Direct labour incurred hours at a cost of

The material efficiency variance was:

A) $1,650 F

B) $870 U

C) $2,520 U

D) $780 F

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 128 في هذه المجموعة.

فتح الحزمة

k this deck

40

Burkett Company uses a standard cost system. Indirect costs were budgeted at $200,000 plus $15 per direct labour hour. The overhead rate is based on 10,000 hours. Actual results were: The variable overhead spending variance was:

A) $10,000 F

B) $50,000 U

C) $35,000 U

D) $15,000 U

A) $10,000 F

B) $50,000 U

C) $35,000 U

D) $15,000 U

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 128 في هذه المجموعة.

فتح الحزمة

k this deck

41

Standard costing allows management to:

I) Measure performance

II) Identify inefficiencies

III) Control costs

A) I and II only

B) I and III only

C) II and III only

D) I, II, and III

I) Measure performance

II) Identify inefficiencies

III) Control costs

A) I and II only

B) I and III only

C) II and III only

D) I, II, and III

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 128 في هذه المجموعة.

فتح الحزمة

k this deck

42

Baldwin, Inc uses a standard job cost system and purchased 25,000 kg of material at $6 per kg, and used it all. The standard amount allowed for the output achieved is 22,500 kg, and the standard price is $6.50 per kg. The company also incurred 37,500 direct labour hours for $450,000. The standard hourly price was $11 per hour, and 39,000 hours were allowed at standard. Assuming all variances are immaterial, answer the following questions:

The entry to record the direct labour variances will include a:

A) Credit to wages payable for $429,000

B) Debit to wages expense for $450,000

C) Debit to work in process inventory for $412,500

D) Credit to direct labour efficiency variance for $16,500

The entry to record the direct labour variances will include a:

A) Credit to wages payable for $429,000

B) Debit to wages expense for $450,000

C) Debit to work in process inventory for $412,500

D) Credit to direct labour efficiency variance for $16,500

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 128 في هذه المجموعة.

فتح الحزمة

k this deck

43

For overhead variances, the difference between the flexible budget amounts and actual costs incurred is called the:

A) Efficiency variance

B) Budget variance

C) Favourable variance

D) Quantity variance

A) Efficiency variance

B) Budget variance

C) Favourable variance

D) Quantity variance

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 128 في هذه المجموعة.

فتح الحزمة

k this deck

44

Which department is customarily responsible for an unfavourable material price variance?

A) Sales

B) Purchasing

C) Engineering

D) Production

A) Sales

B) Purchasing

C) Engineering

D) Production

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 128 في هذه المجموعة.

فتح الحزمة

k this deck

45

Brodie Co. uses a standard job cost system and a denominator volume of 25,000 direct labour hours for allocating overhead. The actual output was 12,000 units, which cost $185,700 for direct labour (23,000 hours), $27,525 for variable overhead, and $136,400 for fixed overhead. The standard variable overhead per unit is $2 (2 hours @ $1 per hour), and the standard fixed overhead per unit is $10 (2 hours @ $5 per hour). All variances are immaterial and are closed to Cost of Goods Sold at the end of the period.

The entry to close the fixed overhead variances includes a:

A) Credit to work in process for $120,000

B) Debit to fixed overhead control for $125,000

C) Debit to Cost of Goods Sold for $16,400

D) Debit to the fixed overhead production volume variance for $5,000

The entry to close the fixed overhead variances includes a:

A) Credit to work in process for $120,000

B) Debit to fixed overhead control for $125,000

C) Debit to Cost of Goods Sold for $16,400

D) Debit to the fixed overhead production volume variance for $5,000

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 128 في هذه المجموعة.

فتح الحزمة

k this deck

46

Mason, Inc. uses a standard costing system. Overhead costs are allocated based on direct labour hours. The standard variable overhead and fixed overhead rates are $1 and $5 per direct labour hour, respectively. Data relevant for the current period include: The cost of direct materials added to work in process would be:

A) $540,000

B) $585,000

C) $600,000

D) $650,000

The cost of direct materials added to work in process would be:A) $540,000

B) $585,000

C) $600,000

D) $650,000

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 128 في هذه المجموعة.

فتح الحزمة

k this deck

47

In a traditional manufacturing accounting system, the standard cost of a unit of output is the sum of the standard costs of:

A) Direct material, direct labour, and variable overhead

B) Direct material, direct labour ,and fixed overhead

C) Direct material, direct labour, and period costs

D) Direct material, direct labour, variable overhead, and fixed overhead

A) Direct material, direct labour, and variable overhead

B) Direct material, direct labour ,and fixed overhead

C) Direct material, direct labour, and period costs

D) Direct material, direct labour, variable overhead, and fixed overhead

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 128 في هذه المجموعة.

فتح الحزمة

k this deck

48

Given the following account balances at the end of the first year of operations: Assuming that variances are considered material, the entry and amount of the direct material efficiency variance allocated to work in process inventory is:

A) Credit $26,000

B) Credit $24,375

C) Debit $17,333

D) Debit $8,125

A) Credit $26,000

B) Credit $24,375

C) Debit $17,333

D) Debit $8,125

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 128 في هذه المجموعة.

فتح الحزمة

k this deck

49

Expected costs per unit of input are called:

A) Standard prices

B) Standard costs

C) Standard quantities

D) Standard ideals

A) Standard prices

B) Standard costs

C) Standard quantities

D) Standard ideals

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 128 في هذه المجموعة.

فتح الحزمة

k this deck

50

Mason, Inc. uses a standard costing system. Overhead costs are allocated based on direct labour hours. The standard variable overhead and fixed overhead rates are $1 and $5 per direct labour hour, respectively. Data relevant for the current period include: The direct materials efficiency variance is:

A) $60,000 Favourable

B) $60,000 Unfavourable

C) $65,000 Favourable

D) $65,000 Unfavourable

The direct materials efficiency variance is:A) $60,000 Favourable

B) $60,000 Unfavourable

C) $65,000 Favourable

D) $65,000 Unfavourable

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 128 في هذه المجموعة.

فتح الحزمة

k this deck

51

Mason, Inc. uses a standard costing system. Overhead costs are allocated based on direct labour hours. The standard variable overhead and fixed overhead rates are $1 and $5 per direct labour hour, respectively. Data relevant for the current period include: The variable overhead spending variance is:

A) $930 Favourable

B) $2,070 Unfavourable

C) $33,000 Unfavourable

D) $3,300 Unfavourable

The variable overhead spending variance is:A) $930 Favourable

B) $2,070 Unfavourable

C) $33,000 Unfavourable

D) $3,300 Unfavourable

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 128 في هذه المجموعة.

فتح الحزمة

k this deck

52

Favourable price variances occur because of:

A) Rising prices of finished goods

B) Increases in raw materials efficiency

C) Price decreases in raw materials

D) Efficiency in the production department

A) Rising prices of finished goods

B) Increases in raw materials efficiency

C) Price decreases in raw materials

D) Efficiency in the production department

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 128 في هذه المجموعة.

فتح الحزمة

k this deck

53

Which of the following is a possible cause of an unfavourable materials efficiency variance?

A) Using materials that do not meet specifications

B) Using a higher class of labour than called for

C) Using a higher quality of material than called for

D) Using fewer hours of labour than labour specifications call for

A) Using materials that do not meet specifications

B) Using a higher class of labour than called for

C) Using a higher quality of material than called for

D) Using fewer hours of labour than labour specifications call for

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 128 في هذه المجموعة.

فتح الحزمة

k this deck

54

Brodie Co. uses a standard job cost system and a denominator volume of 25,000 direct labour hours for allocating overhead. The actual output was 12,000 units, which cost $185,700 for direct labour (23,000 hours), $27,525 for variable overhead, and $136,400 for fixed overhead. The standard variable overhead per unit is $2 (2 hours @ $1 per hour), and the standard fixed overhead per unit is $10 (2 hours @ $5 per hour). All variances are immaterial and are closed to Cost of Goods Sold at the end of the period.

The entry to close the variable overhead variances includes a:

A) Credit to the variable overhead spending variance for $4,525

B) Credit to work in process for $24,000

C) Credit to the variable overhead efficiency variance for $1,000

D) Debit to Cost of Goods Sold for $5,525

The entry to close the variable overhead variances includes a:

A) Credit to the variable overhead spending variance for $4,525

B) Credit to work in process for $24,000

C) Credit to the variable overhead efficiency variance for $1,000

D) Debit to Cost of Goods Sold for $5,525

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 128 في هذه المجموعة.

فتح الحزمة

k this deck

55

Given the following account balances at the end of the first year of operations: Assuming that variances are considered material, the entry and amount of the direct material price variance allocated to Cost of Goods Sold is:

A) Debit $40,625

B) Debit $41,082

C) Credit $43,333

D) Debit $39,935

A) Debit $40,625

B) Debit $41,082

C) Credit $43,333

D) Debit $39,935

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 128 في هذه المجموعة.

فتح الحزمة

k this deck

56

The budget that reflects the level of activity management expects to attain is the:

A) Flexible budget

B) Standard budget

C) Master budget

D) Expected budget

A) Flexible budget

B) Standard budget

C) Master budget

D) Expected budget

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 128 في هذه المجموعة.

فتح الحزمة

k this deck

57

Given the following account balances at the end of the first year of operations: Assuming that variances are considered material, the entry and amount of direct labour variances allocated to the Finished Goods Inventory is:

A) Credit $3,740

B) Debit $2,160

C) Credit $770

D) Debit $3,960

A) Credit $3,740

B) Debit $2,160

C) Credit $770

D) Debit $3,960

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 128 في هذه المجموعة.

فتح الحزمة

k this deck

58

Mason, Inc. uses a standard costing system. Overhead costs are allocated based on direct labour hours. The standard variable overhead and fixed overhead rates are $1 and $5 per direct labour hour, respectively. Data relevant for the current period include: The direct labour price variance is:

A) $30,000 Favourable

B) $30,000 Unfavourable

C) $75,000 Unfavourable

D) $78,000 Unfavourable

The direct labour price variance is:A) $30,000 Favourable

B) $30,000 Unfavourable

C) $75,000 Unfavourable

D) $78,000 Unfavourable

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 128 في هذه المجموعة.

فتح الحزمة

k this deck

59

Baldwin, Inc uses a standard job cost system and purchased 25,000 kg of material at $6 per kg, and used it all. The standard amount allowed for the output achieved is 22,500 kg, and the standard price is $6.50 per kg. The company also incurred 37,500 direct labour hours for $450,000. The standard hourly price was $11 per hour, and 39,000 hours were allowed at standard. Assuming all variances are immaterial, answer the following questions:

The entry to record the direct material efficiency variance will include a;

A) Debit to work in process inventory for $146,250

B) Credit to the efficiency variance for $16,250

C) Credit to the efficiency variance for $12,500

D) Credit to materials inventory for $150,000

The entry to record the direct material efficiency variance will include a;

A) Debit to work in process inventory for $146,250

B) Credit to the efficiency variance for $16,250

C) Credit to the efficiency variance for $12,500

D) Credit to materials inventory for $150,000

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 128 في هذه المجموعة.

فتح الحزمة

k this deck

60

Mason, Inc. uses a standard costing system. Overhead costs are allocated based on direct labour hours. The standard variable overhead and fixed overhead rates are $1 and $5 per direct labour hour, respectively. Data relevant for the current period include: The purchase of direct materials would be recorded in direct materials inventory at:

A) $540,000

B) $585,000

C) $600,000

D) $650,000

The purchase of direct materials would be recorded in direct materials inventory at:A) $540,000

B) $585,000

C) $600,000

D) $650,000

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 128 في هذه المجموعة.

فتح الحزمة

k this deck

61

Unattainable standards are likely to lead to:

I) Errors in the accounting information system

II) Favourable variances

III) Unfavourable variances

A) I only

B) II only

C) III only

D) I and III only

I) Errors in the accounting information system

II) Favourable variances

III) Unfavourable variances

A) I only

B) II only

C) III only

D) I and III only

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 128 في هذه المجموعة.

فتح الحزمة

k this deck

62

Which of the following is not a typical step in variance analysis?

A) Calculate variances

B) Identify reasons for variances

C) Report variances in financial statements

D) Draw conclusions and take action

A) Calculate variances

B) Identify reasons for variances

C) Report variances in financial statements

D) Draw conclusions and take action

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 128 في هذه المجموعة.

فتح الحزمة

k this deck

63

Theft of raw materials is most likely to lead to:

A) Direct materials price variance

B) Favourable direct materials price variance

C) Unfavourable direct materials efficiency variance

D) Favourable direct materials efficiency variance

A) Direct materials price variance

B) Favourable direct materials price variance

C) Unfavourable direct materials efficiency variance

D) Favourable direct materials efficiency variance

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 128 في هذه المجموعة.

فتح الحزمة

k this deck

64

Variance analysis involves the steps listed below. In which order should the steps be performed?

1) Calculate variances

2) Choose variances for further investigation

3) Draw conclusions and take action

4) Identify reasons for variances

A) 1, 2, 3, 4

B) 2, 1, 3, 4

C) 2, 1, 4, 3

D) 1, 2, 4, 3

1) Calculate variances

2) Choose variances for further investigation

3) Draw conclusions and take action

4) Identify reasons for variances

A) 1, 2, 3, 4

B) 2, 1, 3, 4

C) 2, 1, 4, 3

D) 1, 2, 4, 3

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 128 في هذه المجموعة.

فتح الحزمة

k this deck

65

Which of the following statements regarding tradeoffs among variances is true?

A) Managers generally do not need to consider tradeoffs in variance analysis

B) Managers may sometimes make tradeoffs between favourable and unfavourable variances

C) Unfavourable direct material price variances often lead to unfavourable direct labour efficiency variances

D) Favourable direct material price variances often lead to favourable direct material efficiency variances

A) Managers generally do not need to consider tradeoffs in variance analysis

B) Managers may sometimes make tradeoffs between favourable and unfavourable variances

C) Unfavourable direct material price variances often lead to unfavourable direct labour efficiency variances

D) Favourable direct material price variances often lead to favourable direct material efficiency variances

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 128 في هذه المجموعة.

فتح الحزمة

k this deck

66

Variance analysis includes which of the following processes?

I) Calculating variances

II) Analyzing the reasons variances occurred

III) Predicting variances in future periods

A) I and II only

B) I and III only

C) II and III only

D) I, II, and III

I) Calculating variances

II) Analyzing the reasons variances occurred

III) Predicting variances in future periods

A) I and II only

B) I and III only

C) II and III only

D) I, II, and III

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 128 في هذه المجموعة.

فتح الحزمة

k this deck

67

At the end of 20x5, ELM Corporation's production manager estimated direct labour overtime hours at 200 for the first quarter of 20x6. At the end of the first quarter, actual overtime hours totalled 180. This difference is most likely to lead to:

A) Favourable variable overhead spending variance

B) Unfavourable production volume variance

C) Favourable labour efficiency variance

D) Unfavourable labour efficiency variance

A) Favourable variable overhead spending variance

B) Unfavourable production volume variance

C) Favourable labour efficiency variance

D) Unfavourable labour efficiency variance

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 128 في هذه المجموعة.

فتح الحزمة

k this deck

68

ELM Corporation introduced a new automated production process that has reduced the amount of labour needed, but not affected the use of materials. The standard cost system has not been changed yet to reflect this new process. Assuming the machinery is functioning properly and that workers were properly trained in its use, which of the following variances is most likely to result?

A) Favourable variable overhead spending variance

B) Favourable direct labour efficiency variance

C) Unfavourable direct labour efficiency variance

D) Favourable direct materials price variance

A) Favourable variable overhead spending variance

B) Favourable direct labour efficiency variance

C) Unfavourable direct labour efficiency variance

D) Favourable direct materials price variance

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 128 في هذه المجموعة.

فتح الحزمة

k this deck

69

Standard costs should be reviewed:

A) Daily

B) Monthly

C) Annually

D) As often as managers and accountants deem necessary

A) Daily

B) Monthly

C) Annually

D) As often as managers and accountants deem necessary

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 128 في هذه المجموعة.

فتح الحزمة

k this deck

70

How do managers decide which variances are important enough to investigate?

I) By considering whether they are favourable or unfavourable

II) By calculating and investigating all possible variances

III) By considering whether it is large enough to justify investigation

A) I only

B) II only

C) III only

D) I and III only

I) By considering whether they are favourable or unfavourable

II) By calculating and investigating all possible variances

III) By considering whether it is large enough to justify investigation

A) I only

B) II only

C) III only

D) I and III only

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 128 في هذه المجموعة.

فتح الحزمة

k this deck

71

A favourable variance in one area might be offset by:

A) Favourable variance in another area

B) Unfavourable variance in another area

C) Increase in period costs

D) Decrease in period costs

A) Favourable variance in another area

B) Unfavourable variance in another area

C) Increase in period costs

D) Decrease in period costs

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 128 في هذه المجموعة.

فتح الحزمة

k this deck

72

If a variance analysis shows that operations are better than expected, managers should:

A) Do nothing

B) Revise standard costs to make them harder to achieve

C) Distribute extra dividends to shareholders

D) Monitor quality to ensure it was maintained

A) Do nothing

B) Revise standard costs to make them harder to achieve

C) Distribute extra dividends to shareholders

D) Monitor quality to ensure it was maintained

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 128 في هذه المجموعة.

فتح الحزمة

k this deck

73

Intentional worker damage is most likely to result in which type of variance?

A) Direct materials price variance

B) Direct materials efficiency variance

C) Direct labour price variance

D) Variable overhead spending variance

A) Direct materials price variance

B) Direct materials efficiency variance

C) Direct labour price variance

D) Variable overhead spending variance

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 128 في هذه المجموعة.

فتح الحزمة

k this deck

74

Managers investigate:

A) All variances

B) All unfavourable variances

C) Variances they consider important

D) Variances that are reported in the financial statements

A) All variances

B) All unfavourable variances

C) Variances they consider important

D) Variances that are reported in the financial statements

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 128 في هذه المجموعة.

فتح الحزمة

k this deck

75

The process of calculating variances and analyzing the reasons they occurred is called:

A) Variance analysis

B) Budget analysis

C) Historical analysis

D) Activity-based analysis

A) Variance analysis

B) Budget analysis

C) Historical analysis

D) Activity-based analysis

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 128 في هذه المجموعة.

فتح الحزمة

k this deck

76

Rewarding employees in one production department for meeting or exceeding standard cost benchmarks can create new sets of problems for organizations. Which of the following is not one of them?

A) An unfavourable efficiency variance because of rework needed on work from another department

B) Variances in another production department

C) Unmotivated employees in that production department

D) Poor quality finished goods

A) An unfavourable efficiency variance because of rework needed on work from another department

B) Variances in another production department

C) Unmotivated employees in that production department

D) Poor quality finished goods

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 128 في هذه المجموعة.

فتح الحزمة

k this deck

77

Variances can be caused by:

I) Out-of-control operations

II) Better-than-expected operations

III) Inappropriate benchmarks

A) I and III only

B) II and III only

C) I and II only

D) I, II, and III

I) Out-of-control operations

II) Better-than-expected operations

III) Inappropriate benchmarks

A) I and III only

B) II and III only

C) I and II only

D) I, II, and III

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 128 في هذه المجموعة.

فتح الحزمة

k this deck

78

If a variance is investigated and determined to be random, managers should:

A) Write off the variance against cost of goods sold

B) Do nothing

C) Identify and discipline the employee(s) responsible

D) Write off the variance against work in process

A) Write off the variance against cost of goods sold

B) Do nothing

C) Identify and discipline the employee(s) responsible

D) Write off the variance against work in process

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 128 في هذه المجموعة.

فتح الحزمة

k this deck

79

The production manager of CLR Corporation calculated a material and unfavourable variance of $4,000 with respect to the cost of direct materials. Which of the following is a likely next step for the production manager?

A) Identify and discipline the responsible employee

B) Take actions to prevent the variance from recurring

C) Ascertain the cause of the variance

D) Switch suppliers for direct materials

A) Identify and discipline the responsible employee

B) Take actions to prevent the variance from recurring

C) Ascertain the cause of the variance

D) Switch suppliers for direct materials

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 128 في هذه المجموعة.

فتح الحزمة

k this deck

80

LST Corporation entered into a new contract with one of its raw material suppliers. The new contract required the supplier to deliver raw materials with a 24-hour notice from LST. This reduces LST's material handling costs, but has increased the cost of the raw materials delivered. Which of the following variances is most likely to result?

A) Unfavourable direct material price variance

B) Favourable direct price variance

C) Unfavourable variable overhead spending variance

D) Unfavourable fixed overhead spending variance

A) Unfavourable direct material price variance

B) Favourable direct price variance

C) Unfavourable variable overhead spending variance

D) Unfavourable fixed overhead spending variance

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 128 في هذه المجموعة.

فتح الحزمة

k this deck

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 128 في هذه المجموعة.