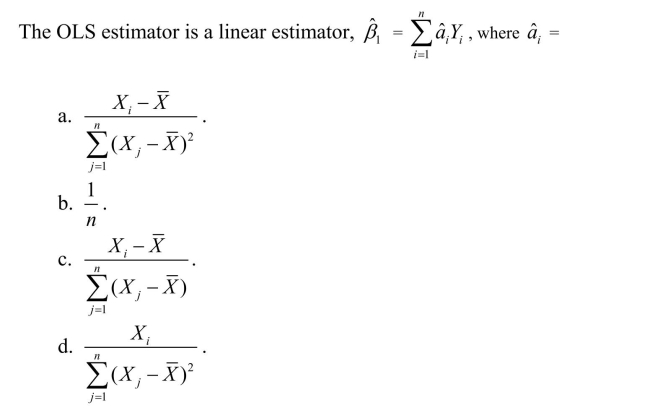

Deck 17: The Theory of Linear Regression With One Regressor

ملء الشاشة (f)

سؤال

سؤال

سؤال

سؤال

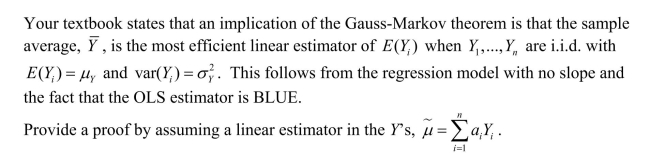

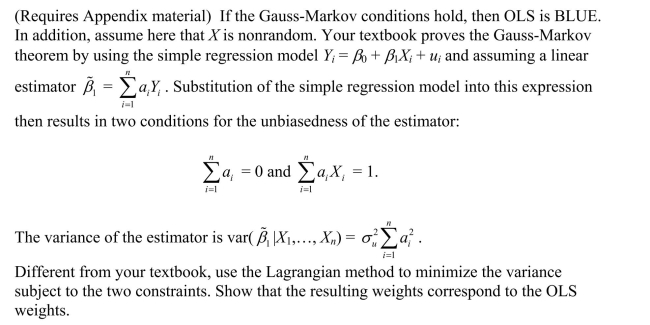

The Gauss-Markov Theorem proves that

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

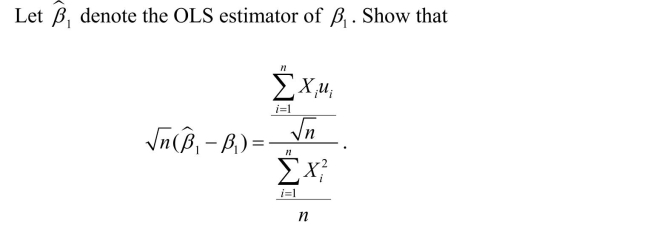

Finite-sample distributions of the OLS estimator and t-statistics are complicated, unless

سؤال

سؤال

.

. سؤال

سؤال

سؤال

سؤال

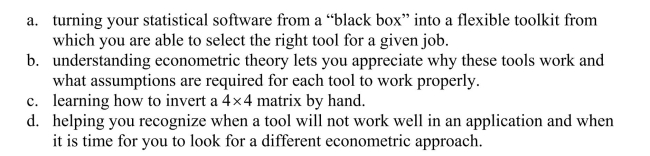

All of the following are good reasons for an applied econometrician to learn some econometric theory, with the exception of

سؤال

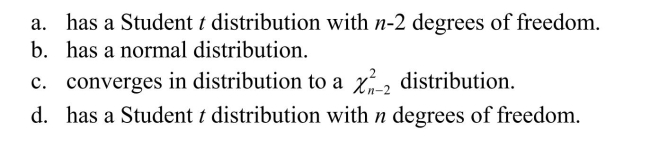

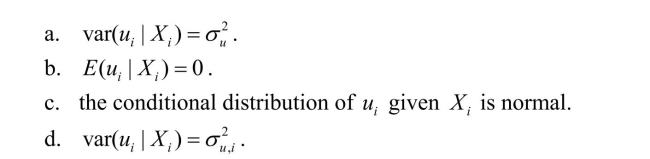

Under the five extended least squares assumptions, the homoskedasticity-only t- distribution in this chapter

سؤال

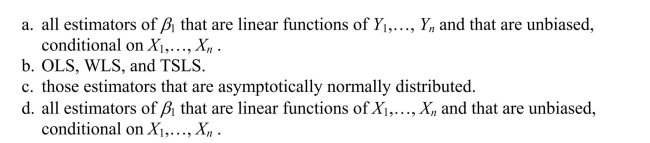

The class of linear conditionally unbiased estimators consists of

سؤال

سؤال

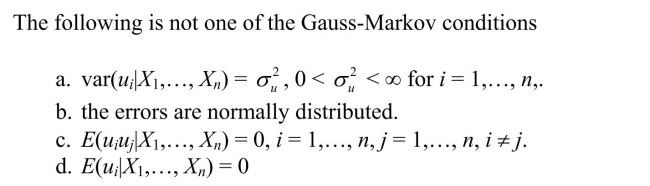

The following is not part of the extended least squares assumptions for regression with a single regressor:

سؤال

For this question you may assume that linear combinations of normal variates are

themselves normally distributed.Let a, b, and c be non-zero constants.

(a)

themselves normally distributed.Let a, b, and c be non-zero constants.

(a)

سؤال

(a)

(a)

سؤال

سؤال

سؤال

(a)Which of the Extended Least Squares Assumptions are satisfied here? Prove your

(a)Which of the Extended Least Squares Assumptions are satisfied here? Prove yourassertions.

سؤال

(a)State the condition under which this estimator is unbiased.

(a)State the condition under which this estimator is unbiased. سؤال

سؤال

سؤال

سؤال

سؤال

(a)

(a)

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

.

. سؤال

فتح الحزمة

قم بالتسجيل لفتح البطاقات في هذه المجموعة!

Unlock Deck

Unlock Deck

1/39

العب

ملء الشاشة (f)

Deck 17: The Theory of Linear Regression With One Regressor

1

It is possible for an estimator of to be inconsistent while

A) converging in probability to

B)

C) unbiased.

D)

A) converging in probability to

B)

C) unbiased.

D)

unbiased.

2

When the errors are heteroskedastic, then

A)WLS is efficient in large samples, if the functional form of the heteroskedasticity is known.

B)OLS is biased.

C)OLS is still efficient as along as there is no serial correlation in the error terms.

D)weighted least squares is efficient.

A)WLS is efficient in large samples, if the functional form of the heteroskedasticity is known.

B)OLS is biased.

C)OLS is still efficient as along as there is no serial correlation in the error terms.

D)weighted least squares is efficient.

A

3

If the errors are heteroskedastic, then

A)the OLS estimator is still BLUE as long as the regressors are nonrandom.

B)the usual formula cannot be used for the OLS estimator.

C)your model becomes overidentified.

D)the OLS estimator is not BLUE.

A)the OLS estimator is still BLUE as long as the regressors are nonrandom.

B)the usual formula cannot be used for the OLS estimator.

C)your model becomes overidentified.

D)the OLS estimator is not BLUE.

D

4

The Gauss-Markov Theorem proves that

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 39 في هذه المجموعة.

فتح الحزمة

k this deck

5

Asymptotic distribution theory is

A)not practically relevant, because we never have an infinite number of observations.

B)only of theoretical interest.

C)of interest because it tells you what the distribution approximately looks like in small samples.

D)the distribution of statistics when the sample size is very large.

A)not practically relevant, because we never have an infinite number of observations.

B)only of theoretical interest.

C)of interest because it tells you what the distribution approximately looks like in small samples.

D)the distribution of statistics when the sample size is very large.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 39 في هذه المجموعة.

فتح الحزمة

k this deck

6

Besides the Central Limit Theorem, the other cornerstone of asymptotic distribution theory is the

A)normal distribution.

B)OLS estimator.

C)Law of Large Numbers.

D)Slutsky's theorem.

A)normal distribution.

B)OLS estimator.

C)Law of Large Numbers.

D)Slutsky's theorem.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 39 في هذه المجموعة.

فتح الحزمة

k this deck

7

A) is the expected value of the homoskedasticity only standard errors.

B)

C) exists only asymptotically.

D)

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 39 في هذه المجموعة.

فتح الحزمة

k this deck

8

If, in addition to the least squares assumptions made in the previous chapter on the simple regression model, the errors are homoskedastic, then the OLS estimator is

A)identical to the TSLS estimator.

B)BLUE.

C)inconsistent.

D)different from the OLS estimator in the presence of heteroskedasticity.

A)identical to the TSLS estimator.

B)BLUE.

C)inconsistent.

D)different from the OLS estimator in the presence of heteroskedasticity.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 39 في هذه المجموعة.

فتح الحزمة

k this deck

9

The extended least squares assumptions are of interest, because

A)they will often hold in practice.

B)if they hold, then OLS is consistent.

C)they allow you to study additional theoretical properties of OLS.

D)if they hold, we can no longer calculate confidence intervals.

A)they will often hold in practice.

B)if they hold, then OLS is consistent.

C)they allow you to study additional theoretical properties of OLS.

D)if they hold, we can no longer calculate confidence intervals.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 39 في هذه المجموعة.

فتح الحزمة

k this deck

10

Finite-sample distributions of the OLS estimator and t-statistics are complicated, unless

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 39 في هذه المجموعة.

فتح الحزمة

k this deck

11

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 39 في هذه المجموعة.

فتح الحزمة

k this deck

12

. فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 39 في هذه المجموعة.

فتح الحزمة

k this deck

13

The link between the variance of and the probability that is within is provided by

A) Slutsky's theorem.

B) the Central Limit Theorem.

C) the Law of Large Numbers.

D) Chebychev's inequality.

A) Slutsky's theorem.

B) the Central Limit Theorem.

C) the Law of Large Numbers.

D) Chebychev's inequality.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 39 في هذه المجموعة.

فتح الحزمة

k this deck

14

You need to adjust by the degrees of freedom to ensure that is

A) an unbiased estimator of

B) a consistent estimator of

C) efficient in small samples.

D) F -distributed.

A) an unbiased estimator of

B) a consistent estimator of

C) efficient in small samples.

D) F -distributed.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 39 في هذه المجموعة.

فتح الحزمة

k this deck

15

An implication of is that

A)

B)

C) OLS is BLUE.

D) there is heteroskedasticity in the errors.

A)

B)

C) OLS is BLUE.

D) there is heteroskedasticity in the errors.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 39 في هذه المجموعة.

فتح الحزمة

k this deck

16

All of the following are good reasons for an applied econometrician to learn some econometric theory, with the exception of

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 39 في هذه المجموعة.

فتح الحزمة

k this deck

17

Under the five extended least squares assumptions, the homoskedasticity-only t- distribution in this chapter

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 39 في هذه المجموعة.

فتح الحزمة

k this deck

18

The class of linear conditionally unbiased estimators consists of

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 39 في هذه المجموعة.

فتح الحزمة

k this deck

19

Slutsky's theorem combines the Law of Large Numbers

A)with continuous functions.

B)and the normal distribution.

C)and the Central Limit Theorem.

D)with conditions for the unbiasedness of an estimator.

A)with continuous functions.

B)and the normal distribution.

C)and the Central Limit Theorem.

D)with conditions for the unbiasedness of an estimator.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 39 في هذه المجموعة.

فتح الحزمة

k this deck

20

The following is not part of the extended least squares assumptions for regression with a single regressor:

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 39 في هذه المجموعة.

فتح الحزمة

k this deck

21

For this question you may assume that linear combinations of normal variates are

themselves normally distributed.Let a, b, and c be non-zero constants.

(a)

themselves normally distributed.Let a, b, and c be non-zero constants.

(a)

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 39 في هذه المجموعة.

فتح الحزمة

k this deck

22

(a) فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 39 في هذه المجموعة.

فتح الحزمة

k this deck

23

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 39 في هذه المجموعة.

فتح الحزمة

k this deck

24

Feasible WLS does not rely on the following condition:

A)the conditional variance depends on a variable which does not have to appear in the regression function.

B)estimating the conditional variance function.

C)the key assumptions for OLS estimation have to apply when estimating the conditional variance function.

D)the conditional variance depends on a variable which appears in the regression function.

A)the conditional variance depends on a variable which does not have to appear in the regression function.

B)estimating the conditional variance function.

C)the key assumptions for OLS estimation have to apply when estimating the conditional variance function.

D)the conditional variance depends on a variable which appears in the regression function.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 39 في هذه المجموعة.

فتح الحزمة

k this deck

25

(a)Which of the Extended Least Squares Assumptions are satisfied here? Prove yourassertions.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 39 في هذه المجموعة.

فتح الحزمة

k this deck

26

(a)State the condition under which this estimator is unbiased. فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 39 في هذه المجموعة.

فتح الحزمة

k this deck

27

What does the Gauss-Markov theorem prove? Without giving mathematical details,

explain how the proof proceeds.What is its importance?

explain how the proof proceeds.What is its importance?

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 39 في هذه المجموعة.

فتح الحزمة

k this deck

28

The advantage of using heteroskedasticity-robust standard errors is that

A)they are easier to compute than the homoskedasticity-only standard errors.

B)they produce asymptotically valid inferences even if you do not know the form of the conditional variance function.

C)it makes the OLS estimator BLUE, even in the presence of heteroskedasticity.

D)they do not unnecessarily complicate matters, since in real-world applications, the functional form of the conditional variance can easily be found.

A)they are easier to compute than the homoskedasticity-only standard errors.

B)they produce asymptotically valid inferences even if you do not know the form of the conditional variance function.

C)it makes the OLS estimator BLUE, even in the presence of heteroskedasticity.

D)they do not unnecessarily complicate matters, since in real-world applications, the functional form of the conditional variance can easily be found.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 39 في هذه المجموعة.

فتح الحزمة

k this deck

29

The WLS estimator is called infeasible WLS estimator when

A)the memory required to compute it on your PC is insufficient.

B)the conditional variance function is not known.

C)the numbers used to compute the estimator get too large.

D)calculating the weights requires you to take a square root of a negative number.

A)the memory required to compute it on your PC is insufficient.

B)the conditional variance function is not known.

C)the numbers used to compute the estimator get too large.

D)calculating the weights requires you to take a square root of a negative number.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 39 في هذه المجموعة.

فتح الحزمة

k this deck

30

One of the earlier textbooks in econometrics, first published in 1971, compared

"estimation of a parameter to shooting at a target with a rifle.The bull's-eye can be taken

to represent the true value of the parameter, the rifle the estimator, and each shot a

particular estimate." Use this analogy to discuss small and large sample properties of

estimators.How do you think the author approached the n → ∞ condition? (Dependent

on your view of the world, feel free to substitute guns with bow and arrow, or missile.)

"estimation of a parameter to shooting at a target with a rifle.The bull's-eye can be taken

to represent the true value of the parameter, the rifle the estimator, and each shot a

particular estimate." Use this analogy to discuss small and large sample properties of

estimators.How do you think the author approached the n → ∞ condition? (Dependent

on your view of the world, feel free to substitute guns with bow and arrow, or missile.)

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 39 في هذه المجموعة.

فتح الحزمة

k this deck

31

(a) فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 39 في هذه المجموعة.

فتح الحزمة

k this deck

32

In practice, the most difficult aspect of feasible WLS estimation is

A)knowing the functional form of the conditional variance.

B)applying the WLS rather than the OLS formula.

C)finding an econometric package that actually calculates WLS.

D)applying WLS when you have a log-log functional form.

A)knowing the functional form of the conditional variance.

B)applying the WLS rather than the OLS formula.

C)finding an econometric package that actually calculates WLS.

D)applying WLS when you have a log-log functional form.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 39 في هذه المجموعة.

فتح الحزمة

k this deck

33

(Requires Appendix material)State and prove the Cauchy-Schwarz Inequality.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 39 في هذه المجموعة.

فتح الحزمة

k this deck

34

(Requires Appendix Material)This question requires you to work with Chebychev's

Inequality.

(a)State Chebychev's Inequality.

Inequality.

(a)State Chebychev's Inequality.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 39 في هذه المجموعة.

فتح الحزمة

k this deck

35

"One should never bother with WLS.Using OLS with robust standard errors gives

correct inference, at least asymptotically." True, false, or a bit of both? Explain carefully

what the quote means and evaluate it critically.

correct inference, at least asymptotically." True, false, or a bit of both? Explain carefully

what the quote means and evaluate it critically.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 39 في هذه المجموعة.

فتح الحزمة

k this deck

36

"I am an applied econometrician and therefore should not have to deal with econometric

theory.There will be others who I leave that to.I am more interested in interpreting the

estimation results." Evaluate.

theory.There will be others who I leave that to.I am more interested in interpreting the

estimation results." Evaluate.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 39 في هذه المجموعة.

فتح الحزمة

k this deck

37

Discuss the properties of the OLS estimator when the regression errors are

homoskedastic and normally distributed.What can you say about the distribution of the

OLS estimator when these features are absent?

homoskedastic and normally distributed.What can you say about the distribution of the

OLS estimator when these features are absent?

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 39 في هذه المجموعة.

فتح الحزمة

k this deck

38

. فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 39 في هذه المجموعة.

فتح الحزمة

k this deck

39

Estimation by WLS

A)although harder than OLS, will always produce a smaller variance.

B)does not mean that you should use homoskedasticity-only standard errors on the transformed equation.

C)requires quite a bit of knowledge about the conditional variance function.

D)makes it very hard to interpret the coefficients, since the data is now weighted and not any longer in its original form.

A)although harder than OLS, will always produce a smaller variance.

B)does not mean that you should use homoskedasticity-only standard errors on the transformed equation.

C)requires quite a bit of knowledge about the conditional variance function.

D)makes it very hard to interpret the coefficients, since the data is now weighted and not any longer in its original form.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 39 في هذه المجموعة.

فتح الحزمة

k this deck

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 39 في هذه المجموعة.