Deck 16: Additional Topics in Time Series Regression

ملء الشاشة (f)

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

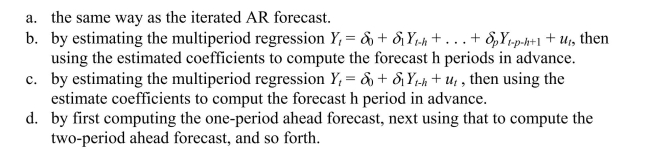

A multiperiod regression forecast h periods into the future based on an AR(p)is computed

سؤال

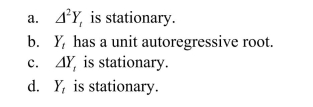

If Yt is I(2), then

سؤال

سؤال

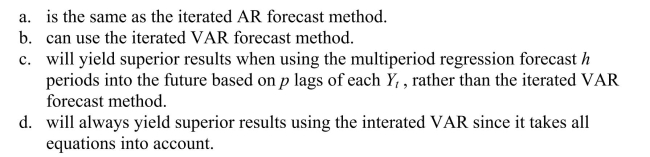

Multiperiod forecasting with multiple predictors

سؤال

In a VECM,

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

A vector autoregression

سؤال

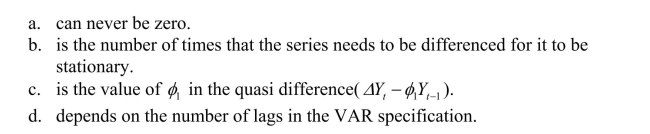

The order of integration

سؤال

سؤال

سؤال

Consider the GARCH (1,1) model  Show that this model can be

Show that this model can be

rewritten as (Hint: use the GARCH(1,1) model but specify it for

(Hint: use the GARCH(1,1) model but specify it for  ; substitute this expression into the original specification, and so on.) Explain intuitively the meaning of the resulting formulation.

; substitute this expression into the original specification, and so on.) Explain intuitively the meaning of the resulting formulation.

Show that this model can berewritten as

(Hint: use the GARCH(1,1) model but specify it for ; substitute this expression into the original specification, and so on.) Explain intuitively the meaning of the resulting formulation. سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

Your textbook states that there "are three ways to decide if two variables can plausibly be

modeled as cointegrated: use expert knowledge and economic theory, graph the series

and see whether they appear to have a common stochastic trend, and perform statistical

tests for cointegration.All three ways should be used in practice." Accordingly you set

out to check whether (the log of)consumption and (the log of)personal disposable

income are cointegrated.You collect data for the sample period 1962:I to 1995:IV and

plot the two variables. (a)Using the first two methods to examine the series for cointegration, what do you think the

(a)Using the first two methods to examine the series for cointegration, what do you think the

likely answer is?

modeled as cointegrated: use expert knowledge and economic theory, graph the series

and see whether they appear to have a common stochastic trend, and perform statistical

tests for cointegration.All three ways should be used in practice." Accordingly you set

out to check whether (the log of)consumption and (the log of)personal disposable

income are cointegrated.You collect data for the sample period 1962:I to 1995:IV and

plot the two variables.

(a)Using the first two methods to examine the series for cointegration, what do you think thelikely answer is?

سؤال

سؤال

سؤال

سؤال

There has been much talk recently about the convergence of inflation rates between many

of the OECD economies.You want to see if there is evidence of this closer to home by

checking whether or not Canada's inflation rate and the United States' inflation rate are

cointegrated.

(a)You begin your numerical analysis by testing for a stochastic trend in the variables, using

an Augmented Dickey-Fuller test.The t-statistic for the coefficient of interest is as

follows: where InfCan is the Canadian inflation rate, and InfUS is the United States inflation rate.

where InfCan is the Canadian inflation rate, and InfUS is the United States inflation rate.

The estimated equation included an intercept.For each case make a decision about the

stationarity of the variables based on the critical value of the Augmented Dickey-Fuller

test statistic.

of the OECD economies.You want to see if there is evidence of this closer to home by

checking whether or not Canada's inflation rate and the United States' inflation rate are

cointegrated.

(a)You begin your numerical analysis by testing for a stochastic trend in the variables, using

an Augmented Dickey-Fuller test.The t-statistic for the coefficient of interest is as

follows:

where InfCan is the Canadian inflation rate, and InfUS is the United States inflation rate.The estimated equation included an intercept.For each case make a decision about the

stationarity of the variables based on the critical value of the Augmented Dickey-Fuller

test statistic.

سؤال

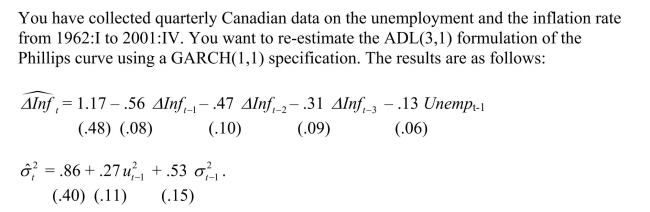

You have collected quarterly data on inflation and unemployment rates for Canada from

1961:III to 1995:IV to estimate a VAR(4)model of the change in the rate of inflation and

the unemployment rate.The results are (a)Explain how you would use the above regressions to conduct one period ahead forecasts.

(a)Explain how you would use the above regressions to conduct one period ahead forecasts.

1961:III to 1995:IV to estimate a VAR(4)model of the change in the rate of inflation and

the unemployment rate.The results are

(a)Explain how you would use the above regressions to conduct one period ahead forecasts. سؤال

(a)

(a)

سؤال

سؤال

Consider the following model  is strictly

is strictly

exogenous. Show that by imposing the restriction you can derive the following so-called Error Correction Mechanism (ECM) model

you can derive the following so-called Error Correction Mechanism (ECM) model

where

What is the short-run (impact) response of a unit increase in X ? What is the long-run solution? Why do you think the term in parenthesis in the above expression is called ECM?

is strictlyexogenous. Show that by imposing the restriction

you can derive the following so-called Error Correction Mechanism (ECM) modelwhere

What is the short-run (impact) response of a unit increase in X ? What is the long-run solution? Why do you think the term in parenthesis in the above expression is called ECM?

سؤال

سؤال

سؤال

سؤال

(a)

(a)

فتح الحزمة

قم بالتسجيل لفتح البطاقات في هذه المجموعة!

Unlock Deck

Unlock Deck

1/40

العب

ملء الشاشة (f)

Deck 16: Additional Topics in Time Series Regression

1

Unit root tests

A)use the standard normal distribution since they are based on the t-statistic.

B)cannot use the standard normal distribution for statistical inference.As a result the ADF statistic has its own special table of critical values.

C)can use the standard normal distribution only when testing that the level variable is stationary, but not the difference variable.

D)can use the standard normal distribution but only if HAC standard errors were computed.

A)use the standard normal distribution since they are based on the t-statistic.

B)cannot use the standard normal distribution for statistical inference.As a result the ADF statistic has its own special table of critical values.

C)can use the standard normal distribution only when testing that the level variable is stationary, but not the difference variable.

D)can use the standard normal distribution but only if HAC standard errors were computed.

B

2

The coefficients of the VAR are estimated by

A)using a simultaneous estimation method such as TSLS.

B)maximum likelihood.

C)panel methods.

D)estimating each of the equations by OLS.

A)using a simultaneous estimation method such as TSLS.

B)maximum likelihood.

C)panel methods.

D)estimating each of the equations by OLS.

D

3

A VAR with five variables, 4 lags and constant terms for each equation will have a total of

A)21 coefficients.

B)100 coefficients.

C)105 coefficients.

D)84 coefficients.

A)21 coefficients.

B)100 coefficients.

C)105 coefficients.

D)84 coefficients.

C

4

One advantage of forecasts based on a VAR rather than separately forecasting the variables involved is

A)that VAR forecasts are easier to calculate.

B)you typically have knowledge of future values of at least one of the variables involved.

C)it can help to make the forecasts mutually consistent.

D)that VAR involves panel data.

A)that VAR forecasts are easier to calculate.

B)you typically have knowledge of future values of at least one of the variables involved.

C)it can help to make the forecasts mutually consistent.

D)that VAR involves panel data.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 40 في هذه المجموعة.

فتح الحزمة

k this deck

5

A VAR allows you to test joint hypothesis that involve restrictions across multiple equations by

A)computing a z-statistic.

B)computing the BIC but not the AIC.

C)using a stability test.

D)computing an F-statistic.

A)computing a z-statistic.

B)computing the BIC but not the AIC.

C)using a stability test.

D)computing an F-statistic.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 40 في هذه المجموعة.

فتح الحزمة

k this deck

6

A multiperiod regression forecast h periods into the future based on an AR(p)is computed

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 40 في هذه المجموعة.

فتح الحزمة

k this deck

7

If Yt is I(2), then

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 40 في هذه المجموعة.

فتح الحزمة

k this deck

8

The following is not a consequence of Xt and Yt being cointegrated:

A) if and Yt are both I(1) , then for some

B) have the same stochastic trend.

C) in the expression is called the cointegrating coefficient.

D) if are cointegrated then integrating one of the variables gives you the same result as integrating the other.

A) if and Yt are both I(1) , then for some

B) have the same stochastic trend.

C) in the expression is called the cointegrating coefficient.

D) if are cointegrated then integrating one of the variables gives you the same result as integrating the other.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 40 في هذه المجموعة.

فتح الحزمة

k this deck

9

Multiperiod forecasting with multiple predictors

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 40 في هذه المجموعة.

فتح الحزمة

k this deck

10

In a VECM,

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 40 في هذه المجموعة.

فتح الحزمة

k this deck

11

You can determine the lag lengths in a VAR

A)by using confidence intervals.

B)by using critical values from the standard normal table.

C)by using either F-tests or information criteria.

D)with the help from economic theory and institutional knowledge.

A)by using confidence intervals.

B)by using critical values from the standard normal table.

C)by using either F-tests or information criteria.

D)with the help from economic theory and institutional knowledge.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 40 في هذه المجموعة.

فتح الحزمة

k this deck

12

The biggest conceptual difference between using VARs for forecasting and using them for structural modeling is that

A)you need to use the Granger causality test for structural modeling.

B)structural modeling requires very specific assumptions derived from economic theory and institutional knowledge, of what is exogenous and what is not.

C)you can no longer use the information criteria to decide on the lag length.

D)structural modeling only allows a maximum of three equations in the VAR.

A)you need to use the Granger causality test for structural modeling.

B)structural modeling requires very specific assumptions derived from economic theory and institutional knowledge, of what is exogenous and what is not.

C)you can no longer use the information criteria to decide on the lag length.

D)structural modeling only allows a maximum of three equations in the VAR.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 40 في هذه المجموعة.

فتح الحزمة

k this deck

13

The error term in a multiperiod regression

A)is serially correlated.

B)causes OLS to be inconsistent.

C)is serially correlated, but less so the longer the forecast horizon.

D)is serially uncorrelated.

A)is serially correlated.

B)causes OLS to be inconsistent.

C)is serially correlated, but less so the longer the forecast horizon.

D)is serially uncorrelated.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 40 في هذه المجموعة.

فتح الحزمة

k this deck

14

To test the null hypothesis of a unit root, the ADF test

A)has higher power than the so-called DF-GLS test.

B)uses complicated interative techniques.

C)cannot be calculated if the variable is integrated of order two or higher.

D)uses a t-statistic and a special critical value.

A)has higher power than the so-called DF-GLS test.

B)uses complicated interative techniques.

C)cannot be calculated if the variable is integrated of order two or higher.

D)uses a t-statistic and a special critical value.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 40 في هذه المجموعة.

فتح الحزمة

k this deck

15

The following is not an appropriate way to tell whether two variables are cointegrated

A)see if the two variables are integrated of the same order.

B)graph the series and see whether they appear to have a common stochastic trend.

C)perform statistical tests for cointegration.

D)use expert knowledge and economic theory.

A)see if the two variables are integrated of the same order.

B)graph the series and see whether they appear to have a common stochastic trend.

C)perform statistical tests for cointegration.

D)use expert knowledge and economic theory.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 40 في هذه المجموعة.

فتح الحزمة

k this deck

16

If are cointegrated, then the OLS estimator of the coefficient in the cointegrating regression is

A) BLUE

B) unbiased when using HAC standard errors.

C) unbiased even in small samples.

D) consistent.

A) BLUE

B) unbiased when using HAC standard errors.

C) unbiased even in small samples.

D) consistent.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 40 في هذه المجموعة.

فتح الحزمة

k this deck

17

Under the VAR assumptions, the OLS estimators are

A)consistent and have a joint normal distribution even in small samples.

B)BLUE.

C)consistent and have a joint normal distribution in large samples.

D)unbiased.

A)consistent and have a joint normal distribution even in small samples.

B)BLUE.

C)consistent and have a joint normal distribution in large samples.

D)unbiased.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 40 في هذه المجموعة.

فتح الحزمة

k this deck

18

A vector autoregression

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 40 في هذه المجموعة.

فتح الحزمة

k this deck

19

The order of integration

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 40 في هذه المجموعة.

فتح الحزمة

k this deck

20

A)

B)

C)

D)

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 40 في هذه المجموعة.

فتح الحزمة

k this deck

21

Volatility clustering

A)is evident in most cross-sections.

B)implies that a series is serially correlated.

C)can mostly be found in studies of the labor market.

D)is evident in many financial time series.

A)is evident in most cross-sections.

B)implies that a series is serially correlated.

C)can mostly be found in studies of the labor market.

D)is evident in many financial time series.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 40 في هذه المجموعة.

فتح الحزمة

k this deck

22

Consider the GARCH (1,1) model Show that this model can be

rewritten as (Hint: use the GARCH(1,1) model but specify it for ; substitute this expression into the original specification, and so on.) Explain intuitively the meaning of the resulting formulation.

Show that this model can berewritten as

(Hint: use the GARCH(1,1) model but specify it for ; substitute this expression into the original specification, and so on.) Explain intuitively the meaning of the resulting formulation. فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 40 في هذه المجموعة.

فتح الحزمة

k this deck

23

"Heteroskedasticity typically occurs in cross-sections, while serial correlation is typically

observed in time-series data." Discuss and critically evaluate this statement.

observed in time-series data." Discuss and critically evaluate this statement.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 40 في هذه المجموعة.

فتح الحزمة

k this deck

24

Carefully explain the difference between forecasting variables separately versus

forecasting a vector of time series variables.Mention how you choose optimal lag lengths

in each case.Part of your essay should deal with multiperiod forecasts and different

methods that can be used in that situation.Finally address the difference between VARS

and VECM.

forecasting a vector of time series variables.Mention how you choose optimal lag lengths

in each case.Part of your essay should deal with multiperiod forecasts and different

methods that can be used in that situation.Finally address the difference between VARS

and VECM.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 40 في هذه المجموعة.

فتح الحزمة

k this deck

25

What role does the concept of cointegration and the order of integration play in modeling

the relationship between variables? Explain how tests of cointegration work.

the relationship between variables? Explain how tests of cointegration work.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 40 في هذه المجموعة.

فتح الحزمة

k this deck

26

For the United States, there is somewhat conflicting evidence whether or not the inflation

rate has a unit autoregressive root.For example, for the sample period 1962:I to 1999:IV

using the ADF statistic, you cannot reject at the 5% significance level that inflation

contains a stochastic trend.However the null hypothesis can be rejected at the 10%

significance level.The DF-GLS test rejects the null hypothesis at the five percent level.

This result turns out to be sensitive to the number of lags chosen and the sample period.

(a)Somewhat intrigued by these findings, you decide to repeat the exercise using Canadian

data.Letting the AIC choose the lag length of the ADF regression, which turns out to be

three, the ADF statistic is (-1.91).What is your decision regarding the null hypothesis?

rate has a unit autoregressive root.For example, for the sample period 1962:I to 1999:IV

using the ADF statistic, you cannot reject at the 5% significance level that inflation

contains a stochastic trend.However the null hypothesis can be rejected at the 10%

significance level.The DF-GLS test rejects the null hypothesis at the five percent level.

This result turns out to be sensitive to the number of lags chosen and the sample period.

(a)Somewhat intrigued by these findings, you decide to repeat the exercise using Canadian

data.Letting the AIC choose the lag length of the ADF regression, which turns out to be

three, the ADF statistic is (-1.91).What is your decision regarding the null hypothesis?

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 40 في هذه المجموعة.

فتح الحزمة

k this deck

27

ARCH and GARCH models are estimated using the

A)OLS estimation method.

B)the method of maximum likelihood.

C)DOLS estimation method.

D)VAR specification.

A)OLS estimation method.

B)the method of maximum likelihood.

C)DOLS estimation method.

D)VAR specification.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 40 في هذه المجموعة.

فتح الحزمة

k this deck

28

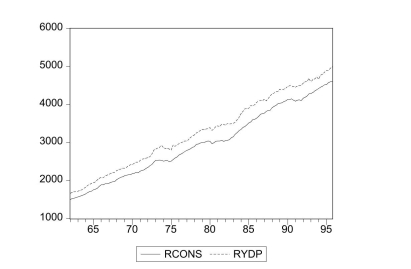

Your textbook states that there "are three ways to decide if two variables can plausibly be

modeled as cointegrated: use expert knowledge and economic theory, graph the series

and see whether they appear to have a common stochastic trend, and perform statistical

tests for cointegration.All three ways should be used in practice." Accordingly you set

out to check whether (the log of)consumption and (the log of)personal disposable

income are cointegrated.You collect data for the sample period 1962:I to 1995:IV and

plot the two variables. (a)Using the first two methods to examine the series for cointegration, what do you think the

likely answer is?

modeled as cointegrated: use expert knowledge and economic theory, graph the series

and see whether they appear to have a common stochastic trend, and perform statistical

tests for cointegration.All three ways should be used in practice." Accordingly you set

out to check whether (the log of)consumption and (the log of)personal disposable

income are cointegrated.You collect data for the sample period 1962:I to 1995:IV and

plot the two variables.

(a)Using the first two methods to examine the series for cointegration, what do you think thelikely answer is?

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 40 في هذه المجموعة.

فتح الحزمة

k this deck

29

Some macroeconomic theories suggest that there is a short-run relationship between the

inflation rate and the unemployment rate.How would you go about forecasting these two

variables? Suggest various alternatives and discuss their advantages and disadvantages.

inflation rate and the unemployment rate.How would you go about forecasting these two

variables? Suggest various alternatives and discuss their advantages and disadvantages.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 40 في هذه المجموعة.

فتح الحزمة

k this deck

30

Think of at least five examples from economics where theory suggests that the variables

involved are cointegrated.For one of these cases, explain how you would test for

cointegration between the variables involved and how you could use this information to

improve forecasting.

involved are cointegrated.For one of these cases, explain how you would test for

cointegration between the variables involved and how you could use this information to

improve forecasting.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 40 في هذه المجموعة.

فتح الحزمة

k this deck

31

You have collected time series for various macroeconomic variables to test if there is a

single cointegrating relationship among multiple variables.Formulate the null hypothesis

and compare the EG-ADF statistic to its critical value.

(a)Canadian unemployment rate, Canadian Inflation Rate, United States unemployment rate,

United States inflation rate; t = (-3.374).

single cointegrating relationship among multiple variables.Formulate the null hypothesis

and compare the EG-ADF statistic to its critical value.

(a)Canadian unemployment rate, Canadian Inflation Rate, United States unemployment rate,

United States inflation rate; t = (-3.374).

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 40 في هذه المجموعة.

فتح الحزمة

k this deck

32

There has been much talk recently about the convergence of inflation rates between many

of the OECD economies.You want to see if there is evidence of this closer to home by

checking whether or not Canada's inflation rate and the United States' inflation rate are

cointegrated.

(a)You begin your numerical analysis by testing for a stochastic trend in the variables, using

an Augmented Dickey-Fuller test.The t-statistic for the coefficient of interest is as

follows: where InfCan is the Canadian inflation rate, and InfUS is the United States inflation rate.

The estimated equation included an intercept.For each case make a decision about the

stationarity of the variables based on the critical value of the Augmented Dickey-Fuller

test statistic.

of the OECD economies.You want to see if there is evidence of this closer to home by

checking whether or not Canada's inflation rate and the United States' inflation rate are

cointegrated.

(a)You begin your numerical analysis by testing for a stochastic trend in the variables, using

an Augmented Dickey-Fuller test.The t-statistic for the coefficient of interest is as

follows:

where InfCan is the Canadian inflation rate, and InfUS is the United States inflation rate.The estimated equation included an intercept.For each case make a decision about the

stationarity of the variables based on the critical value of the Augmented Dickey-Fuller

test statistic.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 40 في هذه المجموعة.

فتح الحزمة

k this deck

33

You have collected quarterly data on inflation and unemployment rates for Canada from

1961:III to 1995:IV to estimate a VAR(4)model of the change in the rate of inflation and

the unemployment rate.The results are (a)Explain how you would use the above regressions to conduct one period ahead forecasts.

1961:III to 1995:IV to estimate a VAR(4)model of the change in the rate of inflation and

the unemployment rate.The results are

(a)Explain how you would use the above regressions to conduct one period ahead forecasts. فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 40 في هذه المجموعة.

فتح الحزمة

k this deck

34

(a) فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 40 في هذه المجموعة.

فتح الحزمة

k this deck

35

Using the ADL (1,1) regression

the ARCH model for the regression error assumes that ut is normally distributed with mean zero and variance where

A)

B)

C)

D)

the ARCH model for the regression error assumes that ut is normally distributed with mean zero and variance where

A)

B)

C)

D)

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 40 في هذه المجموعة.

فتح الحزمة

k this deck

36

Consider the following model is strictly

exogenous. Show that by imposing the restriction you can derive the following so-called Error Correction Mechanism (ECM) model

where

What is the short-run (impact) response of a unit increase in X ? What is the long-run solution? Why do you think the term in parenthesis in the above expression is called ECM?

is strictlyexogenous. Show that by imposing the restriction

you can derive the following so-called Error Correction Mechanism (ECM) modelwhere

What is the short-run (impact) response of a unit increase in X ? What is the long-run solution? Why do you think the term in parenthesis in the above expression is called ECM?

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 40 في هذه المجموعة.

فتح الحزمة

k this deck

37

Your textbook so far considered variables for cointegration that are integrated of the

same order.For example, the log of consumption and personal disposable income might

both be I(1)variables, and the error correction term would be I(0), if consumption and

personal disposable income were cointegrated.

(a)Do you think that it makes sense to test for cointegration between two variables if they

are integrated of different orders? Explain.

same order.For example, the log of consumption and personal disposable income might

both be I(1)variables, and the error correction term would be I(0), if consumption and

personal disposable income were cointegrated.

(a)Do you think that it makes sense to test for cointegration between two variables if they

are integrated of different orders? Explain.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 40 في هذه المجموعة.

فتح الحزمة

k this deck

38

The DOLS estimator has the following property if

are cointegrated:

A) it is BLUE even in small samples.

B) it is efficient in large samples.

C) it has a standard normal distribution when homoskedasticity-only standard errors are used.

D) it has a non-normal distribution in large samples when HAC standard errors are used.

are cointegrated:

A) it is BLUE even in small samples.

B) it is efficient in large samples.

C) it has a standard normal distribution when homoskedasticity-only standard errors are used.

D) it has a non-normal distribution in large samples when HAC standard errors are used.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 40 في هذه المجموعة.

فتح الحزمة

k this deck

39

Assume that you have used the OLS estimator in the cointegrating regression and test the residual for a unit root using an ADF test.The resulting ADF test statistic has a

A)normal distribution in large samples.

B)non-normal distribution which require ADF critical values for inference.

C)non-normal distribution which require EG-ADF critical values for inference.

D)normal distribution when HAC standard errors are used.

A)normal distribution in large samples.

B)non-normal distribution which require ADF critical values for inference.

C)non-normal distribution which require EG-ADF critical values for inference.

D)normal distribution when HAC standard errors are used.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 40 في هذه المجموعة.

فتح الحزمة

k this deck

40

(a) فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 40 في هذه المجموعة.

فتح الحزمة

k this deck

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 40 في هذه المجموعة.