Deck 14: Management Accounting in a Changing Environment

ملء الشاشة (f)

سؤال

سؤال

سؤال

سؤال

Software Development Inc.

Software Development Inc. (SDI) produces and markets software for personal computers, including spreadsheet, word processing, desktop publishing, and database management programs. SDI has annual sales of $800 million.

Producing software is a time-consuming, labor-intensive process. Software quality is an extremely important aspect of success in computer software markets. One aspect of quality is program reliability. Does the software perform as expected? Does it work with other software in terms of data transfers and interfaces? Does it terminate abnormally? In spite of extensive testing of the software, programs always contain some bugs. Once the software is released, SDI stands behind the product with phone-in customer service consultants who answer questions and help the customer work around problems in the software. SDI's software maintenance group fixes bugs and sends out revised versions of the programs to customers.

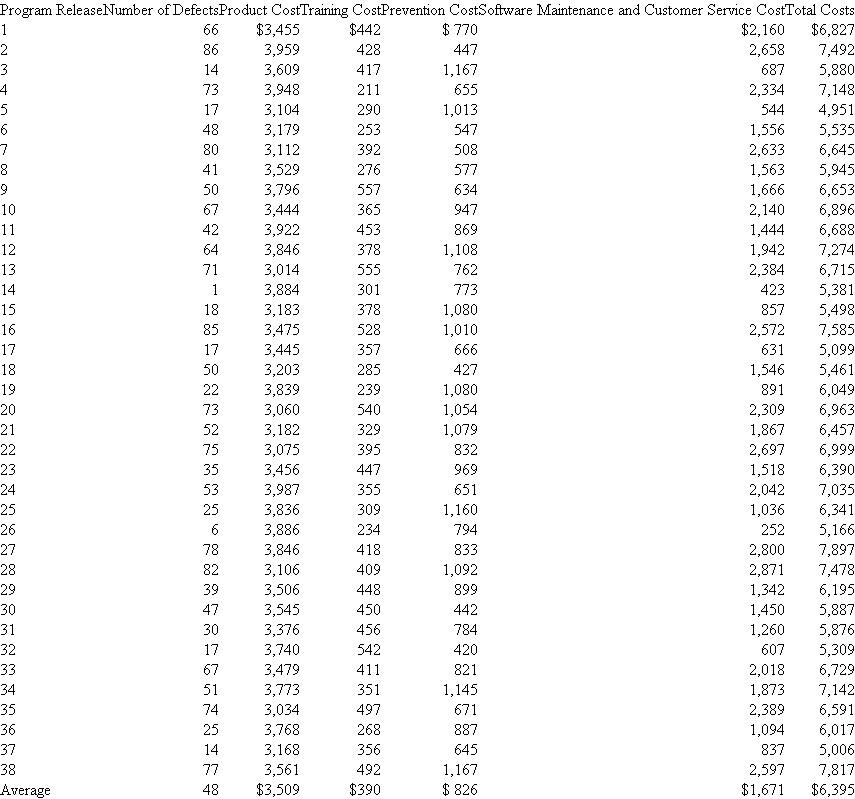

SDI tracks the relation between quality costs and quality. The quality measure it uses is the number of documented bugs in a software package. These bugs are counted when a customer calls in with a complaint and the SDI customer service representative determines that this is a new problem. The software maintenance programmers then attempt to fix the program and eliminate the bug. To manage quality, SDI tracks quality costs. It has released 38 new packages or major revisions in existing packages in the last three years. The accompanying table reports the number of defects (bugs) documented in the first six months following release. Also listed in the table are total product cost and quality cost per software package release.

Product costs include all the costs incurred to produce and market the software, excluding the quality costs in the table. Quality costs consist of three components: training, prevention, and software maintenance and customer service costs. Training costs are expenditures for educating the programmers and updating their training. Better-educated programmers produce fewer bugs. Prevention costs include expenditures for testing the software before it is released. Maintenance and customer service costs include (1) the programmers charged with fixing the bugs and reissuing the revised software and (2) the customer service representatives answering phone questions. The training and prevention costs are measured over the period the software was being developed. The number of defects and maintenance and service costs are measured in the first six months following release.

SDI Defects and Quality Costs by Program Release* * Per 100,000 lines of computer code.

* Per 100,000 lines of computer code.

All the numbers in the table have been divided by lines of computer code in the particular program release. Programs with more lines of code cost more and also have more bugs. Prior studies find that using lines of code is an acceptable way to control for program complexity. Thus, the numbers in the table are stated in terms of defects and cost per 100,000 lines of code.

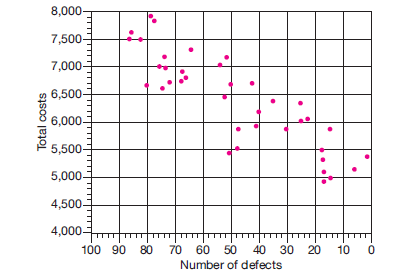

The figure below plots the relation between total cost and number of defects. The vice president of quality of SDI likes to use it to emphasize that costs and quality are inversely related. She is fond of saying, "Quality pays! Our total costs fall as the number of defects declines. The more we spend on quality, the lower our costs."

SDI total costs by defects

Required:

Critically evaluate the vice president's analysis.

Software Development Inc. (SDI) produces and markets software for personal computers, including spreadsheet, word processing, desktop publishing, and database management programs. SDI has annual sales of $800 million.

Producing software is a time-consuming, labor-intensive process. Software quality is an extremely important aspect of success in computer software markets. One aspect of quality is program reliability. Does the software perform as expected? Does it work with other software in terms of data transfers and interfaces? Does it terminate abnormally? In spite of extensive testing of the software, programs always contain some bugs. Once the software is released, SDI stands behind the product with phone-in customer service consultants who answer questions and help the customer work around problems in the software. SDI's software maintenance group fixes bugs and sends out revised versions of the programs to customers.

SDI tracks the relation between quality costs and quality. The quality measure it uses is the number of documented bugs in a software package. These bugs are counted when a customer calls in with a complaint and the SDI customer service representative determines that this is a new problem. The software maintenance programmers then attempt to fix the program and eliminate the bug. To manage quality, SDI tracks quality costs. It has released 38 new packages or major revisions in existing packages in the last three years. The accompanying table reports the number of defects (bugs) documented in the first six months following release. Also listed in the table are total product cost and quality cost per software package release.

Product costs include all the costs incurred to produce and market the software, excluding the quality costs in the table. Quality costs consist of three components: training, prevention, and software maintenance and customer service costs. Training costs are expenditures for educating the programmers and updating their training. Better-educated programmers produce fewer bugs. Prevention costs include expenditures for testing the software before it is released. Maintenance and customer service costs include (1) the programmers charged with fixing the bugs and reissuing the revised software and (2) the customer service representatives answering phone questions. The training and prevention costs are measured over the period the software was being developed. The number of defects and maintenance and service costs are measured in the first six months following release.

SDI Defects and Quality Costs by Program Release*

* Per 100,000 lines of computer code.All the numbers in the table have been divided by lines of computer code in the particular program release. Programs with more lines of code cost more and also have more bugs. Prior studies find that using lines of code is an acceptable way to control for program complexity. Thus, the numbers in the table are stated in terms of defects and cost per 100,000 lines of code.

The figure below plots the relation between total cost and number of defects. The vice president of quality of SDI likes to use it to emphasize that costs and quality are inversely related. She is fond of saying, "Quality pays! Our total costs fall as the number of defects declines. The more we spend on quality, the lower our costs."

SDI total costs by defects

Required:

Critically evaluate the vice president's analysis.

سؤال

سؤال

TQM at the Stowbridge Division

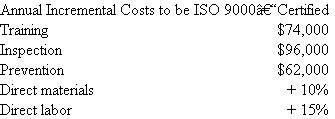

The Stowbridge Division is analyzing expanding its Total Quality Management program. It already has a TQM program in place. However, one of its customers, Amlan Equipment, is asking all suppliers to become ISO 9000-qualified, a process that certifies that the firm meets various standards. Once suppliers are ISO 9000-qualified, Amlan can reduce its inspection costs. Not all of the suppliers will be certified, and those that are will receive more business from Amlan.

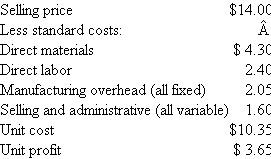

Amlan purchases a stainless steel rotor from Stowbridge. After earning ISO 9000 certification, Stowbridge estimates that it will have to incur the following annual incremental costs as long as it wants to maintain its certification: To manufacture the current quality of the rotors (before ISO 9000 certification), the budgeted selling price and standard cost data per rotor follow.

To manufacture the current quality of the rotors (before ISO 9000 certification), the budgeted selling price and standard cost data per rotor follow.  Unless Stowbridge receives ISO 9000 certification, it will lose Amlan's business of 120,000 units per year. Management estimates that the higher quality of the rotor that meets quality criteria will allow Stowbridge to add 14,000 rotors to its existing sales from new and continuing customers. Stowbridge is currently selling 480,000 rotors per year, including the Amlan sales. The 480,000 current sales amount to 63 percent of plant capacity. The additional 14,000 units sold can be manufactured without exceeding plant capacity. The higher-quality process after ISO 9000 certification is received would apply to all the rotors produced.

Unless Stowbridge receives ISO 9000 certification, it will lose Amlan's business of 120,000 units per year. Management estimates that the higher quality of the rotor that meets quality criteria will allow Stowbridge to add 14,000 rotors to its existing sales from new and continuing customers. Stowbridge is currently selling 480,000 rotors per year, including the Amlan sales. The 480,000 current sales amount to 63 percent of plant capacity. The additional 14,000 units sold can be manufactured without exceeding plant capacity. The higher-quality process after ISO 9000 certification is received would apply to all the rotors produced.

Required:

Should Stowbridge seek ISO 9000 certification? Support your recommendation with an analysis of the costs and benefits of certification.

The Stowbridge Division is analyzing expanding its Total Quality Management program. It already has a TQM program in place. However, one of its customers, Amlan Equipment, is asking all suppliers to become ISO 9000-qualified, a process that certifies that the firm meets various standards. Once suppliers are ISO 9000-qualified, Amlan can reduce its inspection costs. Not all of the suppliers will be certified, and those that are will receive more business from Amlan.

Amlan purchases a stainless steel rotor from Stowbridge. After earning ISO 9000 certification, Stowbridge estimates that it will have to incur the following annual incremental costs as long as it wants to maintain its certification:

To manufacture the current quality of the rotors (before ISO 9000 certification), the budgeted selling price and standard cost data per rotor follow. Unless Stowbridge receives ISO 9000 certification, it will lose Amlan's business of 120,000 units per year. Management estimates that the higher quality of the rotor that meets quality criteria will allow Stowbridge to add 14,000 rotors to its existing sales from new and continuing customers. Stowbridge is currently selling 480,000 rotors per year, including the Amlan sales. The 480,000 current sales amount to 63 percent of plant capacity. The additional 14,000 units sold can be manufactured without exceeding plant capacity. The higher-quality process after ISO 9000 certification is received would apply to all the rotors produced.Required:

Should Stowbridge seek ISO 9000 certification? Support your recommendation with an analysis of the costs and benefits of certification.

سؤال

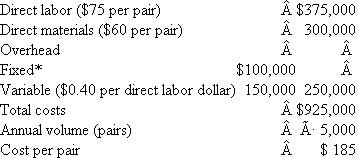

Winter Games

Winter Games manufactures a competitive line of skis and sells its skis to retailers at a price of $225 per pair. Based on an annual volume of 5,000 pairs, the cost per pair is $185: "Composed of depreciation, property taxes, charitable contributions, insurance, and so on.

"Composed of depreciation, property taxes, charitable contributions, insurance, and so on.

Sports Palace, a discount sporting goods store, currently purchases 500 pairs of skis from Winter Games. Sports Palace has asked to purchase 1,000 pairs of skis under a private brand label, at a price of $200 per pair. The skis would be identical to those normally sold for $225.

Winter Games believes that if it accepts the order, Sports Palace will cancel its usual order of 500 pairs. These sales cannot be recouped elsewhere. If this special order is accepted, the direct labor hours for the additional 500 skis would have to be compensated at overtime rates (at 1 1 / 2 times the base rate). Analysis shows that variable overhead varies with total direct labor dollars at the rate of $0.40 per direct labor dollar.

Should Winter Games accept the special order from Sports Palace?

Winter Games manufactures a competitive line of skis and sells its skis to retailers at a price of $225 per pair. Based on an annual volume of 5,000 pairs, the cost per pair is $185:

"Composed of depreciation, property taxes, charitable contributions, insurance, and so on.Sports Palace, a discount sporting goods store, currently purchases 500 pairs of skis from Winter Games. Sports Palace has asked to purchase 1,000 pairs of skis under a private brand label, at a price of $200 per pair. The skis would be identical to those normally sold for $225.

Winter Games believes that if it accepts the order, Sports Palace will cancel its usual order of 500 pairs. These sales cannot be recouped elsewhere. If this special order is accepted, the direct labor hours for the additional 500 skis would have to be compensated at overtime rates (at 1 1 / 2 times the base rate). Analysis shows that variable overhead varies with total direct labor dollars at the rate of $0.40 per direct labor dollar.

Should Winter Games accept the special order from Sports Palace?

سؤال

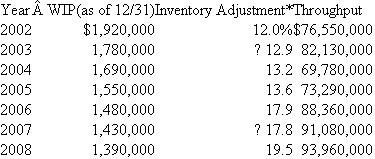

Warren City Parts Manufacturing

Warren City, with sales of $2 billion, produces and sells farm equipment. The manufacturing division produces some parts internally and purchases other parts from external suppliers and assembles farm equipment including tractors, combines, and plows. Within the manufacturing division is parts manufacturing, which fabricates a large variety of parts. Parts manufacturing is further subdivided into 12 departments, including screw products, metal stamping and fabrication, plastic injection molding, and steel castings. Each of these parts departments is headed by a department manager whose performance is evaluated along several dimensions: meeting budgeted costs, meeting delivery schedules, improving quality, achieving affirmative action and employee satisfaction goals, and minimizing inventory adjustments.

Inventory adjustments occur twice a year after internal auditors conduct a physical inventory of the parts department's work in process and compare it with the amount of inventory as reported in the work-in-process (WIP) account. For example, if on June 30 the auditors take a physical inventory count and find $130,000 of physical WIP inventory in the steel castings department but the WIP account reports an inventory balance of $143,000, then a negative inventory adjustment of -9.1 percent (-$13,000 ÷ $143,000) is made. Any inventory adjustment, positive or negative, reflects unfavorably on the parts department manager's performance and results in a reduction in the manager's bonus. The parts department manager is expected to maintain a tight control of WIP inventories, including ensuring the integrity of his or her department's accounting reports of WIP. Large inventory adjustments indicate that the manager does not have good control of WIP.

Four years ago Warren City adopted JIT production procedures. The result has been a drastic reduction of WIP inventories. For example, the following data illustrate the steel castings department's WIP account balance before adjustments, inventory adjustment, and throughput for the last seven years.

Warren City Steel Castings Department * Deflated by 12/31 WIP.

* Deflated by 12/31 WIP.

Throughput is the total dollar cost of parts manufactured in the year. It is the sum of the beginning inventory plus direct labor and materials and overhead, less ending inventory. Warren City uses a standard cost system and all inventories are valued at standard cost. When a batch of parts completes production, the WIP inventory is reduced by the standard cost of the part times the standard number of parts in the batch. Each part is manufactured in standard lot sizes.

Inventory adjustments can result for a number of reasons:

1. Different batch sizes. The department manager decides to deviate from standard batch sizes. Unless a special entry is recorded, the accounting system assumes that the number of units in the batch is the standard number. Sometimes the manager has some excess production capacity and decides to increase the standard batch size. In some cases, the manager produces fewer parts than called for by the standard lot size because of machine breakdowns or bottlenecks. For example, suppose a certain part calls for a standard batch size of 150 but the manager decides to produce 200 parts, keeps 50 as spares, but fails to update the WIP account for the additional 50 units. The WIP account contains only 150 at standard cost but the auditors count 200, causing a positive inventory adjustment.

2. Timing differences. The accounting system charges some expenses in a different time period than the department manager expects. This causes the dollar amount of the WIP balance to differ from standard cost.

3. Standard cost revisions. The standard cost of a part is revised and the auditors use a different standard cost in valuing the ending WIP inventory than was used in the WIP account.

4. Audit mistakes. The internal auditors make mistakes in counting the final physical WIP inventory.

The first two reasons are by far the most prevalent causes of inventory adjustments.

Required:

a. Management is concerned that the magnitude of the inventory adjustment has increased over time. What are some likely reasons that the absolute value of the inventory adjustment has grown?

b. Evaluate the use of the inventory adjustment described above to measure a parts department manager's performance.

Warren City, with sales of $2 billion, produces and sells farm equipment. The manufacturing division produces some parts internally and purchases other parts from external suppliers and assembles farm equipment including tractors, combines, and plows. Within the manufacturing division is parts manufacturing, which fabricates a large variety of parts. Parts manufacturing is further subdivided into 12 departments, including screw products, metal stamping and fabrication, plastic injection molding, and steel castings. Each of these parts departments is headed by a department manager whose performance is evaluated along several dimensions: meeting budgeted costs, meeting delivery schedules, improving quality, achieving affirmative action and employee satisfaction goals, and minimizing inventory adjustments.

Inventory adjustments occur twice a year after internal auditors conduct a physical inventory of the parts department's work in process and compare it with the amount of inventory as reported in the work-in-process (WIP) account. For example, if on June 30 the auditors take a physical inventory count and find $130,000 of physical WIP inventory in the steel castings department but the WIP account reports an inventory balance of $143,000, then a negative inventory adjustment of -9.1 percent (-$13,000 ÷ $143,000) is made. Any inventory adjustment, positive or negative, reflects unfavorably on the parts department manager's performance and results in a reduction in the manager's bonus. The parts department manager is expected to maintain a tight control of WIP inventories, including ensuring the integrity of his or her department's accounting reports of WIP. Large inventory adjustments indicate that the manager does not have good control of WIP.

Four years ago Warren City adopted JIT production procedures. The result has been a drastic reduction of WIP inventories. For example, the following data illustrate the steel castings department's WIP account balance before adjustments, inventory adjustment, and throughput for the last seven years.

Warren City Steel Castings Department

* Deflated by 12/31 WIP.Throughput is the total dollar cost of parts manufactured in the year. It is the sum of the beginning inventory plus direct labor and materials and overhead, less ending inventory. Warren City uses a standard cost system and all inventories are valued at standard cost. When a batch of parts completes production, the WIP inventory is reduced by the standard cost of the part times the standard number of parts in the batch. Each part is manufactured in standard lot sizes.

Inventory adjustments can result for a number of reasons:

1. Different batch sizes. The department manager decides to deviate from standard batch sizes. Unless a special entry is recorded, the accounting system assumes that the number of units in the batch is the standard number. Sometimes the manager has some excess production capacity and decides to increase the standard batch size. In some cases, the manager produces fewer parts than called for by the standard lot size because of machine breakdowns or bottlenecks. For example, suppose a certain part calls for a standard batch size of 150 but the manager decides to produce 200 parts, keeps 50 as spares, but fails to update the WIP account for the additional 50 units. The WIP account contains only 150 at standard cost but the auditors count 200, causing a positive inventory adjustment.

2. Timing differences. The accounting system charges some expenses in a different time period than the department manager expects. This causes the dollar amount of the WIP balance to differ from standard cost.

3. Standard cost revisions. The standard cost of a part is revised and the auditors use a different standard cost in valuing the ending WIP inventory than was used in the WIP account.

4. Audit mistakes. The internal auditors make mistakes in counting the final physical WIP inventory.

The first two reasons are by far the most prevalent causes of inventory adjustments.

Required:

a. Management is concerned that the magnitude of the inventory adjustment has increased over time. What are some likely reasons that the absolute value of the inventory adjustment has grown?

b. Evaluate the use of the inventory adjustment described above to measure a parts department manager's performance.

سؤال

Secure Servers Inc.

Secure Servers Inc. (SSI) is one of the largest software and service providers directed at providing high levels of backup and security for computer servers to the financial community, military, and other clients requiring off-site backup and security systems. SSI's software packages include encryption, downloading, and data warehousing of large amounts of data to various SSI sites in dedicated locations. SSI backup locations are designed to survive virtually all natural disasters and terrorist attacks.

SSI employs 6,000 people in Dayton, Ohio. Being one of Dayton's largest employers, it has a deep commitment to the community and supports local educational, cultural, and philanthropic activities. SSI also believes strongly in both customer and employee satisfaction. To achieve these objectives, SSI employs a balanced scorecard to evaluate and reward senior managers. One-fourth of each senior executive's bonus is tied to the following objectively determined performance measures:

Community engagement (independent survey of local leaders).

Customer satisfaction (independent survey of customers).

Employee satisfaction (independent survey of employees).

Corporate profit (audited net income before taxes).

The annual surveys of local leaders, customers, and employees are conducted by an independent opinion survey firm that reports directly to the board of directors. Corporate profit is the firm's reported net income before taxes as audited by an international public accounting firm. SSI's senior management team believes strongly in the concept of the balanced scorecard and accepts it as a valid and productive performance measurement and incentive tool.

Senior management is tasked with determining how much to spend on further improvements in community engagement, customer satisfaction, and employee satisfaction. The following table captures the relations among additional spending in each area and the expected improvements from such expenditures (in millions).![Secure Servers Inc. Secure Servers Inc. (SSI) is one of the largest software and service providers directed at providing high levels of backup and security for computer servers to the financial community, military, and other clients requiring off-site backup and security systems. SSI's software packages include encryption, downloading, and data warehousing of large amounts of data to various SSI sites in dedicated locations. SSI backup locations are designed to survive virtually all natural disasters and terrorist attacks. SSI employs 6,000 people in Dayton, Ohio. Being one of Dayton's largest employers, it has a deep commitment to the community and supports local educational, cultural, and philanthropic activities. SSI also believes strongly in both customer and employee satisfaction. To achieve these objectives, SSI employs a balanced scorecard to evaluate and reward senior managers. One-fourth of each senior executive's bonus is tied to the following objectively determined performance measures: Community engagement (independent survey of local leaders). Customer satisfaction (independent survey of customers). Employee satisfaction (independent survey of employees). Corporate profit (audited net income before taxes). The annual surveys of local leaders, customers, and employees are conducted by an independent opinion survey firm that reports directly to the board of directors. Corporate profit is the firm's reported net income before taxes as audited by an international public accounting firm. SSI's senior management team believes strongly in the concept of the balanced scorecard and accepts it as a valid and productive performance measurement and incentive tool. Senior management is tasked with determining how much to spend on further improvements in community engagement, customer satisfaction, and employee satisfaction. The following table captures the relations among additional spending in each area and the expected improvements from such expenditures (in millions). For example, by spending an additional $3 million on customer service (improved call centers, training, etc.), a 95 percent customer satisfaction can be achieved. Or, by spending an additional $2 million on employee-related activities (improved child care, athletic facilities, fringe benefits), a 90 percent employee satisfaction can be achieved. Or spending $1 million on additional community projects can raise SSI's community rating survey to 50 percent. Besides raising the satisfaction scores as detailed above, making additional expenditures on these three areas also generates additional net cash flows to the firm. The following table estimates the additional cash flows SSI receives from making the additional expenditures. For example, spending $3 million for community projects yields a community rating index of 90 percent and additional cash flows of $4.0 million, which increases net income before taxes by $1.0 million ($4.0 ? $3.0). To convert audited net income into a percentage index that can be averaged with the other three survey metrics, SSI uses the following formula: Profit index = ?3 + 0.05 × Net income So, if net income is $74 million, the profit index for use in the balanced scorecard is 70 percent [?3 + (0.05 × 74)]. The four indexes are averaged to get an overall index for determining the bonus for each senior executive of SSI. For example, the following four indexes yield a balanced scorecard of 79.75 percent: SSI expects audited net income before taxes for the year before making any additional expenditures on customer satisfaction, employee satisfaction, and community engagement to be $72 million. Required: a. What levels of additional spending do you expect the senior management team of SSI will select for: (1) Customer satisfaction. (2) Community engagement. (3) Employee satisfaction. Be sure to justify your answers with appropriate analysis. b. Given the levels of additional spending on the three items you recommended in ( a ), what is the expected balanced scorecard index? That is, calculate the average balanced scorecard management expects to generate if they make the expenditure decisions you predict in ( a ). Show calculations. c. What level of spending would you expect a profit-maximizing owner of SSI to select for: (1) Customer satisfaction. (2) Community engagement. (3) Employee satisfaction. What is the expected balanced scorecard resulting from these spending levels?<div style=padding-top: 35px>](https://d2lvgg3v3hfg70.cloudfront.net/SM1503/11eb559c_84e6_32eb_a8c8_37eddf32638f_SM1503_00.jpg) For example, by spending an additional $3 million on customer service (improved call centers, training, etc.), a 95 percent customer satisfaction can be achieved. Or, by spending an additional $2 million on employee-related activities (improved child care, athletic facilities, fringe benefits), a 90 percent employee satisfaction can be achieved. Or spending $1 million on additional community projects can raise SSI's community rating survey to 50 percent.

For example, by spending an additional $3 million on customer service (improved call centers, training, etc.), a 95 percent customer satisfaction can be achieved. Or, by spending an additional $2 million on employee-related activities (improved child care, athletic facilities, fringe benefits), a 90 percent employee satisfaction can be achieved. Or spending $1 million on additional community projects can raise SSI's community rating survey to 50 percent.

Besides raising the satisfaction scores as detailed above, making additional expenditures on these three areas also generates additional net cash flows to the firm. The following table estimates the additional cash flows SSI receives from making the additional expenditures.![Secure Servers Inc. Secure Servers Inc. (SSI) is one of the largest software and service providers directed at providing high levels of backup and security for computer servers to the financial community, military, and other clients requiring off-site backup and security systems. SSI's software packages include encryption, downloading, and data warehousing of large amounts of data to various SSI sites in dedicated locations. SSI backup locations are designed to survive virtually all natural disasters and terrorist attacks. SSI employs 6,000 people in Dayton, Ohio. Being one of Dayton's largest employers, it has a deep commitment to the community and supports local educational, cultural, and philanthropic activities. SSI also believes strongly in both customer and employee satisfaction. To achieve these objectives, SSI employs a balanced scorecard to evaluate and reward senior managers. One-fourth of each senior executive's bonus is tied to the following objectively determined performance measures: Community engagement (independent survey of local leaders). Customer satisfaction (independent survey of customers). Employee satisfaction (independent survey of employees). Corporate profit (audited net income before taxes). The annual surveys of local leaders, customers, and employees are conducted by an independent opinion survey firm that reports directly to the board of directors. Corporate profit is the firm's reported net income before taxes as audited by an international public accounting firm. SSI's senior management team believes strongly in the concept of the balanced scorecard and accepts it as a valid and productive performance measurement and incentive tool. Senior management is tasked with determining how much to spend on further improvements in community engagement, customer satisfaction, and employee satisfaction. The following table captures the relations among additional spending in each area and the expected improvements from such expenditures (in millions). For example, by spending an additional $3 million on customer service (improved call centers, training, etc.), a 95 percent customer satisfaction can be achieved. Or, by spending an additional $2 million on employee-related activities (improved child care, athletic facilities, fringe benefits), a 90 percent employee satisfaction can be achieved. Or spending $1 million on additional community projects can raise SSI's community rating survey to 50 percent. Besides raising the satisfaction scores as detailed above, making additional expenditures on these three areas also generates additional net cash flows to the firm. The following table estimates the additional cash flows SSI receives from making the additional expenditures. For example, spending $3 million for community projects yields a community rating index of 90 percent and additional cash flows of $4.0 million, which increases net income before taxes by $1.0 million ($4.0 ? $3.0). To convert audited net income into a percentage index that can be averaged with the other three survey metrics, SSI uses the following formula: Profit index = ?3 + 0.05 × Net income So, if net income is $74 million, the profit index for use in the balanced scorecard is 70 percent [?3 + (0.05 × 74)]. The four indexes are averaged to get an overall index for determining the bonus for each senior executive of SSI. For example, the following four indexes yield a balanced scorecard of 79.75 percent: SSI expects audited net income before taxes for the year before making any additional expenditures on customer satisfaction, employee satisfaction, and community engagement to be $72 million. Required: a. What levels of additional spending do you expect the senior management team of SSI will select for: (1) Customer satisfaction. (2) Community engagement. (3) Employee satisfaction. Be sure to justify your answers with appropriate analysis. b. Given the levels of additional spending on the three items you recommended in ( a ), what is the expected balanced scorecard index? That is, calculate the average balanced scorecard management expects to generate if they make the expenditure decisions you predict in ( a ). Show calculations. c. What level of spending would you expect a profit-maximizing owner of SSI to select for: (1) Customer satisfaction. (2) Community engagement. (3) Employee satisfaction. What is the expected balanced scorecard resulting from these spending levels?<div style=padding-top: 35px>](https://d2lvgg3v3hfg70.cloudfront.net/SM1503/11eb559c_84e6_32ec_a8c8_ebd250aa3031_SM1503_00.jpg) For example, spending $3 million for community projects yields a community rating index of 90 percent and additional cash flows of $4.0 million, which increases net income before taxes by $1.0 million ($4.0 ? $3.0).

For example, spending $3 million for community projects yields a community rating index of 90 percent and additional cash flows of $4.0 million, which increases net income before taxes by $1.0 million ($4.0 ? $3.0).

To convert audited net income into a percentage index that can be averaged with the other three survey metrics, SSI uses the following formula:

Profit index = ?3 + 0.05 × Net income

So, if net income is $74 million, the profit index for use in the balanced scorecard is 70 percent [?3 + (0.05 × 74)].

The four indexes are averaged to get an overall index for determining the bonus for each senior executive of SSI. For example, the following four indexes yield a balanced scorecard of 79.75 percent:![Secure Servers Inc. Secure Servers Inc. (SSI) is one of the largest software and service providers directed at providing high levels of backup and security for computer servers to the financial community, military, and other clients requiring off-site backup and security systems. SSI's software packages include encryption, downloading, and data warehousing of large amounts of data to various SSI sites in dedicated locations. SSI backup locations are designed to survive virtually all natural disasters and terrorist attacks. SSI employs 6,000 people in Dayton, Ohio. Being one of Dayton's largest employers, it has a deep commitment to the community and supports local educational, cultural, and philanthropic activities. SSI also believes strongly in both customer and employee satisfaction. To achieve these objectives, SSI employs a balanced scorecard to evaluate and reward senior managers. One-fourth of each senior executive's bonus is tied to the following objectively determined performance measures: Community engagement (independent survey of local leaders). Customer satisfaction (independent survey of customers). Employee satisfaction (independent survey of employees). Corporate profit (audited net income before taxes). The annual surveys of local leaders, customers, and employees are conducted by an independent opinion survey firm that reports directly to the board of directors. Corporate profit is the firm's reported net income before taxes as audited by an international public accounting firm. SSI's senior management team believes strongly in the concept of the balanced scorecard and accepts it as a valid and productive performance measurement and incentive tool. Senior management is tasked with determining how much to spend on further improvements in community engagement, customer satisfaction, and employee satisfaction. The following table captures the relations among additional spending in each area and the expected improvements from such expenditures (in millions). For example, by spending an additional $3 million on customer service (improved call centers, training, etc.), a 95 percent customer satisfaction can be achieved. Or, by spending an additional $2 million on employee-related activities (improved child care, athletic facilities, fringe benefits), a 90 percent employee satisfaction can be achieved. Or spending $1 million on additional community projects can raise SSI's community rating survey to 50 percent. Besides raising the satisfaction scores as detailed above, making additional expenditures on these three areas also generates additional net cash flows to the firm. The following table estimates the additional cash flows SSI receives from making the additional expenditures. For example, spending $3 million for community projects yields a community rating index of 90 percent and additional cash flows of $4.0 million, which increases net income before taxes by $1.0 million ($4.0 ? $3.0). To convert audited net income into a percentage index that can be averaged with the other three survey metrics, SSI uses the following formula: Profit index = ?3 + 0.05 × Net income So, if net income is $74 million, the profit index for use in the balanced scorecard is 70 percent [?3 + (0.05 × 74)]. The four indexes are averaged to get an overall index for determining the bonus for each senior executive of SSI. For example, the following four indexes yield a balanced scorecard of 79.75 percent: SSI expects audited net income before taxes for the year before making any additional expenditures on customer satisfaction, employee satisfaction, and community engagement to be $72 million. Required: a. What levels of additional spending do you expect the senior management team of SSI will select for: (1) Customer satisfaction. (2) Community engagement. (3) Employee satisfaction. Be sure to justify your answers with appropriate analysis. b. Given the levels of additional spending on the three items you recommended in ( a ), what is the expected balanced scorecard index? That is, calculate the average balanced scorecard management expects to generate if they make the expenditure decisions you predict in ( a ). Show calculations. c. What level of spending would you expect a profit-maximizing owner of SSI to select for: (1) Customer satisfaction. (2) Community engagement. (3) Employee satisfaction. What is the expected balanced scorecard resulting from these spending levels?<div style=padding-top: 35px>](https://d2lvgg3v3hfg70.cloudfront.net/SM1503/11eb559c_84e6_32ed_a8c8_9141453d16c7_SM1503_00.jpg) SSI expects audited net income before taxes for the year before making any additional expenditures on customer satisfaction, employee satisfaction, and community engagement to be $72 million.

SSI expects audited net income before taxes for the year before making any additional expenditures on customer satisfaction, employee satisfaction, and community engagement to be $72 million.

Required:

a. What levels of additional spending do you expect the senior management team of SSI will select for:

(1) Customer satisfaction.

(2) Community engagement.

(3) Employee satisfaction.

Be sure to justify your answers with appropriate analysis.

b. Given the levels of additional spending on the three items you recommended in ( a ), what is the expected balanced scorecard index? That is, calculate the average balanced scorecard management expects to generate if they make the expenditure decisions you predict in ( a ). Show calculations.

c. What level of spending would you expect a profit-maximizing owner of SSI to select for:

(1) Customer satisfaction.

(2) Community engagement.

(3) Employee satisfaction.

What is the expected balanced scorecard resulting from these spending levels?

Secure Servers Inc. (SSI) is one of the largest software and service providers directed at providing high levels of backup and security for computer servers to the financial community, military, and other clients requiring off-site backup and security systems. SSI's software packages include encryption, downloading, and data warehousing of large amounts of data to various SSI sites in dedicated locations. SSI backup locations are designed to survive virtually all natural disasters and terrorist attacks.

SSI employs 6,000 people in Dayton, Ohio. Being one of Dayton's largest employers, it has a deep commitment to the community and supports local educational, cultural, and philanthropic activities. SSI also believes strongly in both customer and employee satisfaction. To achieve these objectives, SSI employs a balanced scorecard to evaluate and reward senior managers. One-fourth of each senior executive's bonus is tied to the following objectively determined performance measures:

Community engagement (independent survey of local leaders).

Customer satisfaction (independent survey of customers).

Employee satisfaction (independent survey of employees).

Corporate profit (audited net income before taxes).

The annual surveys of local leaders, customers, and employees are conducted by an independent opinion survey firm that reports directly to the board of directors. Corporate profit is the firm's reported net income before taxes as audited by an international public accounting firm. SSI's senior management team believes strongly in the concept of the balanced scorecard and accepts it as a valid and productive performance measurement and incentive tool.

Senior management is tasked with determining how much to spend on further improvements in community engagement, customer satisfaction, and employee satisfaction. The following table captures the relations among additional spending in each area and the expected improvements from such expenditures (in millions).

For example, by spending an additional $3 million on customer service (improved call centers, training, etc.), a 95 percent customer satisfaction can be achieved. Or, by spending an additional $2 million on employee-related activities (improved child care, athletic facilities, fringe benefits), a 90 percent employee satisfaction can be achieved. Or spending $1 million on additional community projects can raise SSI's community rating survey to 50 percent.Besides raising the satisfaction scores as detailed above, making additional expenditures on these three areas also generates additional net cash flows to the firm. The following table estimates the additional cash flows SSI receives from making the additional expenditures.

For example, spending $3 million for community projects yields a community rating index of 90 percent and additional cash flows of $4.0 million, which increases net income before taxes by $1.0 million ($4.0 ? $3.0).To convert audited net income into a percentage index that can be averaged with the other three survey metrics, SSI uses the following formula:

Profit index = ?3 + 0.05 × Net income

So, if net income is $74 million, the profit index for use in the balanced scorecard is 70 percent [?3 + (0.05 × 74)].

The four indexes are averaged to get an overall index for determining the bonus for each senior executive of SSI. For example, the following four indexes yield a balanced scorecard of 79.75 percent:

SSI expects audited net income before taxes for the year before making any additional expenditures on customer satisfaction, employee satisfaction, and community engagement to be $72 million.Required:

a. What levels of additional spending do you expect the senior management team of SSI will select for:

(1) Customer satisfaction.

(2) Community engagement.

(3) Employee satisfaction.

Be sure to justify your answers with appropriate analysis.

b. Given the levels of additional spending on the three items you recommended in ( a ), what is the expected balanced scorecard index? That is, calculate the average balanced scorecard management expects to generate if they make the expenditure decisions you predict in ( a ). Show calculations.

c. What level of spending would you expect a profit-maximizing owner of SSI to select for:

(1) Customer satisfaction.

(2) Community engagement.

(3) Employee satisfaction.

What is the expected balanced scorecard resulting from these spending levels?

سؤال

British Airways

British Airways (BA) has implemented the balanced scorecard. Match the following performance indicators: to these four balanced scorecard perspectives:

to these four balanced scorecard perspectives:  Note: Performance indicators may be used for more than one perspective.

Note: Performance indicators may be used for more than one perspective.

British Airways (BA) has implemented the balanced scorecard. Match the following performance indicators:

to these four balanced scorecard perspectives: Note: Performance indicators may be used for more than one perspective. سؤال

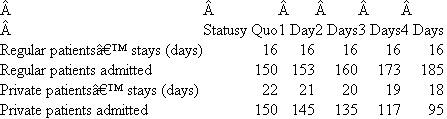

Kollel Hospital

Kollel is a private hospital that operates in a large metropolitan area. The hospital admits "regular" patients and "private" patients. Regular patients are admitted and treated by staff doctors who are fulltime employees of Kollel Hospital. Private patients are admitted and treated by private physicians (physicians in private practice who have admitting privileges to Kollel). To maintain its leadership role in the community, Kollel is deeply committed to its Total Quality Management program. Management and staff form multidisciplinary teams to study various hospital functions. This year, one team reviewed a hospital unit that exclusively treated a particular type of medical admittance. (All patients of this type of admittance were treated in this unit.) The team found that patients preferred to be discharged sooner rather than later and that, overall, the patients felt that they were kept in the hospital too long.

The specific unit under review consists of 16 beds. Last year the unit treated 300 patients. The patients were heterogeneous with respect to their level of illness. Properly diagnosed and treated, patients should have been discharged in an average of 16 days. Nevertheless, the TQM study showed that patients remain in the hospital an average of 19 days. Furthermore, research showed that the average stay of regular patients was shorter than the average stay of private patients, even though the private physicians did not handle more difficult cases at the time of admission. The study found that private doctors took longer to diagnose their patients and spent less time with them during treatment. As a result, these doctors did not promptly recognize whether a treatment was working or whether the patient was ready to be discharged.

In order to increase the quality of care, hospital management is studying plans to lower the average stay of these patients. One alternative being considered is preventing the private doctors, who are keeping their patients in the unit the longest, from admitting patients into the unit. Some, but not all, of these patients can be replaced by patients admitted by staff doctors. The trade-off between the number of patients admitted and the length of a patient's stay is shown in the following table. Last year 150 regular and 150 private patients were admitted. The average stay was 16 days for regular patients and 22 days for private patients, making an overall average of 19 days per patient.

Admissions as a Function of Reducing Length of Stay For this specific type of admittance, the hospital collects $10,000 per stay from the insurance companies, regardless of whether the patient is admitted regularly or privately. This amount is used to cover the unit's fixed cost of $1,752,000 per year (365 days) and a variable cost of $150 per patient per day. Note that the charges for the doctor's services are handled separately and are not considered for purposes of this analysis.

For this specific type of admittance, the hospital collects $10,000 per stay from the insurance companies, regardless of whether the patient is admitted regularly or privately. This amount is used to cover the unit's fixed cost of $1,752,000 per year (365 days) and a variable cost of $150 per patient per day. Note that the charges for the doctor's services are handled separately and are not considered for purposes of this analysis.

Required:

a. Calculate the average hospital stay for all patients under each scenario listed in the table. Also, for each case calculate the occupancy rate (percentage of beds filled on average). Discuss the relation between the average length of stay and the occupancy rate.

b. Prepare an income statement showing the net income for each scenario, separating the margin earned on regular and private patients. Where is profit maximized? What are the components of the change in net income?

Kollel is a private hospital that operates in a large metropolitan area. The hospital admits "regular" patients and "private" patients. Regular patients are admitted and treated by staff doctors who are fulltime employees of Kollel Hospital. Private patients are admitted and treated by private physicians (physicians in private practice who have admitting privileges to Kollel). To maintain its leadership role in the community, Kollel is deeply committed to its Total Quality Management program. Management and staff form multidisciplinary teams to study various hospital functions. This year, one team reviewed a hospital unit that exclusively treated a particular type of medical admittance. (All patients of this type of admittance were treated in this unit.) The team found that patients preferred to be discharged sooner rather than later and that, overall, the patients felt that they were kept in the hospital too long.

The specific unit under review consists of 16 beds. Last year the unit treated 300 patients. The patients were heterogeneous with respect to their level of illness. Properly diagnosed and treated, patients should have been discharged in an average of 16 days. Nevertheless, the TQM study showed that patients remain in the hospital an average of 19 days. Furthermore, research showed that the average stay of regular patients was shorter than the average stay of private patients, even though the private physicians did not handle more difficult cases at the time of admission. The study found that private doctors took longer to diagnose their patients and spent less time with them during treatment. As a result, these doctors did not promptly recognize whether a treatment was working or whether the patient was ready to be discharged.

In order to increase the quality of care, hospital management is studying plans to lower the average stay of these patients. One alternative being considered is preventing the private doctors, who are keeping their patients in the unit the longest, from admitting patients into the unit. Some, but not all, of these patients can be replaced by patients admitted by staff doctors. The trade-off between the number of patients admitted and the length of a patient's stay is shown in the following table. Last year 150 regular and 150 private patients were admitted. The average stay was 16 days for regular patients and 22 days for private patients, making an overall average of 19 days per patient.

Admissions as a Function of Reducing Length of Stay

For this specific type of admittance, the hospital collects $10,000 per stay from the insurance companies, regardless of whether the patient is admitted regularly or privately. This amount is used to cover the unit's fixed cost of $1,752,000 per year (365 days) and a variable cost of $150 per patient per day. Note that the charges for the doctor's services are handled separately and are not considered for purposes of this analysis.Required:

a. Calculate the average hospital stay for all patients under each scenario listed in the table. Also, for each case calculate the occupancy rate (percentage of beds filled on average). Discuss the relation between the average length of stay and the occupancy rate.

b. Prepare an income statement showing the net income for each scenario, separating the margin earned on regular and private patients. Where is profit maximized? What are the components of the change in net income?

سؤال

سؤال

سؤال

Chateau Napa

Chateau Napa purchased a small vineyard and is now producing magnum bottles (1.5 liters) of Redwood Cabernet Sauvignon. This wine is much sought after, and bottling the wine in larger bottles enhances its quality, prestige, and demand. Because of the limited size of the vineyard, the quantity of wine produced is fixed. The only decision variable is the quality of the wine produced. Quality is a function of a host of factors: the quality of oak barrels used to age the wine, the ability of the oenologist (winemaker), the length of time it is aged, and so forth. In general, the more money spent on quality, the higher the price of the wine. Several experts rate wines, and the Wine Spectator ' s rating has become the industry standard. The following table summarizes how quality (as measured in expected Wine Spectator points with a scale of 0-100) varies with the amount of spending on quality and how various quality levels translate into price:![Chateau Napa Chateau Napa purchased a small vineyard and is now producing magnum bottles (1.5 liters) of Redwood Cabernet Sauvignon. This wine is much sought after, and bottling the wine in larger bottles enhances its quality, prestige, and demand. Because of the limited size of the vineyard, the quantity of wine produced is fixed. The only decision variable is the quality of the wine produced. Quality is a function of a host of factors: the quality of oak barrels used to age the wine, the ability of the oenologist (winemaker), the length of time it is aged, and so forth. In general, the more money spent on quality, the higher the price of the wine. Several experts rate wines, and the Wine Spectator ' s rating has become the industry standard. The following table summarizes how quality (as measured in expected Wine Spectator points with a scale of 0-100) varies with the amount of spending on quality and how various quality levels translate into price: Note: Magnums are produced in two-bottle sets. So if $115 is spent on enhancing the quality of a two-bottle set, a quality rating of 94.90 is expected and a final wholesale price Chateau Napa expects to receive is $598.52 per two-bottle set. The managers producing and marketing the Redwood Cabernet Sauvignon are evaluated and compensated based on the balanced scorecard. Just two metrics are used in their scorecard: actual quality achieved and profits per two-bottle set. Half the bonus is based on quality achieved using the following formula: Quality bonus = Maximum (0, quality achieved - 90) × 5% In other words, the managers must receive a quality rating of at least 90 points before any bonus is paid. If they achieve a perfect rating of 100 points, they receive 50 percent of their bonus [5% × (100 - 90)]. The other 50 percent of their bonus is tied to profits achieved from selling the two-bottle sets. Profits consist of the wholesale selling price less quality costs less all other operating costs ($450 per two-bottle set 12 ). The profit bonus is based on the following formula: Profit bonus = Maximum (0, profit - $30) × 10% Managers are expected to achieve profits between $30 and $35. For every dollar of profit they generate above $30, they receive 10 percent of their bonus. So if they have profits of $33.15 per set, they receive 31.5 percent [10% × ($33.15 - $30)] of their bonus. (All bonus computations are rounded to three significant digits, i.e., 46.7 percent.) Required: a. Given the balanced scorecard incentive scheme being used to reward the Redwood Cabernet Sauvignon managers, how much do you expect them to spend on quality? What quality level do they expect to achieve? How much profit per two-bottle set do they expect to earn, and what is their expected total bonus (in percent)? b. To maximize firm value, how much would Chateau Napa want the managers of Redwood Cabernet Sauvignon to spend on quality; what quality level would this spending likely yield; and how much profit does this quality level produce? c. Explain why your answers in parts ( a ) and ( b ) are either the same or different. d. Using the setting in the problem, explain what is meant by the saying You can only maximize in one dimension at a time.<div style=padding-top: 35px>](https://d2lvgg3v3hfg70.cloudfront.net/SM1503/11eb559c_84c7_fc5d_a8c8_6544d8d2e86b_SM1503_00.jpg) Note: Magnums are produced in two-bottle sets. So if $115 is spent on enhancing the quality of a two-bottle set, a quality rating of 94.90 is expected and a final wholesale price Chateau Napa expects to receive is $598.52 per two-bottle set.

Note: Magnums are produced in two-bottle sets. So if $115 is spent on enhancing the quality of a two-bottle set, a quality rating of 94.90 is expected and a final wholesale price Chateau Napa expects to receive is $598.52 per two-bottle set.

The managers producing and marketing the Redwood Cabernet Sauvignon are evaluated and compensated based on the balanced scorecard. Just two metrics are used in their scorecard: actual quality achieved and profits per two-bottle set. Half the bonus is based on quality achieved using the following formula:

Quality bonus = Maximum (0, quality achieved - 90) × 5%

In other words, the managers must receive a quality rating of at least 90 points before any bonus is paid. If they achieve a perfect rating of 100 points, they receive 50 percent of their bonus [5% × (100 - 90)]. The other 50 percent of their bonus is tied to profits achieved from selling the two-bottle sets. Profits consist of the wholesale selling price less quality costs less all other operating costs ($450 per two-bottle set 12 ). The profit bonus is based on the following formula:

Profit bonus = Maximum (0, profit - $30) × 10%

Managers are expected to achieve profits between $30 and $35. For every dollar of profit they generate above $30, they receive 10 percent of their bonus. So if they have profits of $33.15 per set, they receive 31.5 percent [10% × ($33.15 - $30)] of their bonus. (All bonus computations are rounded to three significant digits, i.e., 46.7 percent.)

Required:

a. Given the balanced scorecard incentive scheme being used to reward the Redwood Cabernet Sauvignon managers, how much do you expect them to spend on quality? What quality level do they expect to achieve? How much profit per two-bottle set do they expect to earn, and what is their expected total bonus (in percent)?

b. To maximize firm value, how much would Chateau Napa want the managers of Redwood Cabernet Sauvignon to spend on quality; what quality level would this spending likely yield; and how much profit does this quality level produce?

c. Explain why your answers in parts ( a ) and ( b ) are either the same or different.

d. Using the setting in the problem, explain what is meant by the saying "You can only maximize in one dimension at a time."

Chateau Napa purchased a small vineyard and is now producing magnum bottles (1.5 liters) of Redwood Cabernet Sauvignon. This wine is much sought after, and bottling the wine in larger bottles enhances its quality, prestige, and demand. Because of the limited size of the vineyard, the quantity of wine produced is fixed. The only decision variable is the quality of the wine produced. Quality is a function of a host of factors: the quality of oak barrels used to age the wine, the ability of the oenologist (winemaker), the length of time it is aged, and so forth. In general, the more money spent on quality, the higher the price of the wine. Several experts rate wines, and the Wine Spectator ' s rating has become the industry standard. The following table summarizes how quality (as measured in expected Wine Spectator points with a scale of 0-100) varies with the amount of spending on quality and how various quality levels translate into price:

Note: Magnums are produced in two-bottle sets. So if $115 is spent on enhancing the quality of a two-bottle set, a quality rating of 94.90 is expected and a final wholesale price Chateau Napa expects to receive is $598.52 per two-bottle set.The managers producing and marketing the Redwood Cabernet Sauvignon are evaluated and compensated based on the balanced scorecard. Just two metrics are used in their scorecard: actual quality achieved and profits per two-bottle set. Half the bonus is based on quality achieved using the following formula:

Quality bonus = Maximum (0, quality achieved - 90) × 5%

In other words, the managers must receive a quality rating of at least 90 points before any bonus is paid. If they achieve a perfect rating of 100 points, they receive 50 percent of their bonus [5% × (100 - 90)]. The other 50 percent of their bonus is tied to profits achieved from selling the two-bottle sets. Profits consist of the wholesale selling price less quality costs less all other operating costs ($450 per two-bottle set 12 ). The profit bonus is based on the following formula:

Profit bonus = Maximum (0, profit - $30) × 10%

Managers are expected to achieve profits between $30 and $35. For every dollar of profit they generate above $30, they receive 10 percent of their bonus. So if they have profits of $33.15 per set, they receive 31.5 percent [10% × ($33.15 - $30)] of their bonus. (All bonus computations are rounded to three significant digits, i.e., 46.7 percent.)

Required:

a. Given the balanced scorecard incentive scheme being used to reward the Redwood Cabernet Sauvignon managers, how much do you expect them to spend on quality? What quality level do they expect to achieve? How much profit per two-bottle set do they expect to earn, and what is their expected total bonus (in percent)?

b. To maximize firm value, how much would Chateau Napa want the managers of Redwood Cabernet Sauvignon to spend on quality; what quality level would this spending likely yield; and how much profit does this quality level produce?

c. Explain why your answers in parts ( a ) and ( b ) are either the same or different.

d. Using the setting in the problem, explain what is meant by the saying "You can only maximize in one dimension at a time."

سؤال

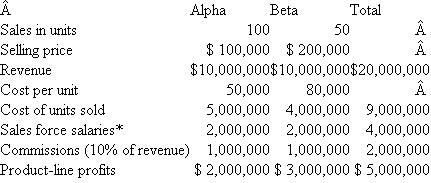

Telephone Computer Corporation (TCC)

Telephone Computer Corporation (TCC) manufactures and sells two computerized directory assistance computers to telephone companies. The firm has its own sales force that sells directly to the phone companies. TCC currently sells two computer systems: the Alpha and the Beta. TCC has 90 percent of the high-end market (Beta) and 50 percent of the low-end market (Alpha). The Alpha sells for $100,000. The Beta sells for $200,000 but has three times the capacity of the Alpha.

TCC has developed a new high-volume machine, Zeta, that has four times the capacity of the Beta and lower operating costs, but a price of $300,000. The unit manufacturing cost is $170,000. Users can connect the Zeta directly to mainframe computers for customer billing as well as to future expected telecommunications advancements. If the Zeta is introduced, management expects that its closest competition will be from the Beta, so most initial sales of the Zeta will come at the expense of Beta sales.

Senior management has invested considerable resources in Zeta. It believes that the future of the company is tied closely to the success of this project. Next year's operations of TCC (if the Zeta is not introduced) are:

Next Year's Projected Profits by Product without Zet a * Assigned based on commissions.

* Assigned based on commissions.

The existing sales force will sell all three types of machines. Salespeople are paid a salary plus 10 percent of sales. To sell the Zeta, salespeople with more knowledge of telecommunications and computer systems will be hired. The additional salary cost of these new employees will be $500,000. The existing sales force will still sell the Zeta but will call in these system experts to assist with the sale. The Zeta system experts are paid a flat salary, and the existing sales force's 10 percent commission incentive will not change with the introduction of the Zeta.

If the Zeta is not introduced, Alpha unit sales are projected to grow at 5 percent per year and Beta unit sales are projected to grow at 10 percent per year. Selling prices will remain constant in real terms. (Prices and salaries will grow at the inflation rate. To keep the analysis simple, all numbers should be projected in real, not nominal, terms. That is, do not adjust the numbers for inflation.)

If the Zeta is introduced, Alpha unit sales will not be affected. But Beta unit sales will be affected: All the Zeta sales will come from the Beta sales in the first year and then Beta unit sales will grow only 2 percent per year. Zeta sales will grow at 9 percent per year from an initial base of 25 machines.

Required:

Management wants to see how the preceding table on product-line profitability will appear when the Zeta model is added. In particular, management asks you to project profits for the Alpha, Beta, and Zeta for the next five years and to make a recommendation on this project. Discuss how the five-year product-line profitability projections should be presented to senior management.

Telephone Computer Corporation (TCC) manufactures and sells two computerized directory assistance computers to telephone companies. The firm has its own sales force that sells directly to the phone companies. TCC currently sells two computer systems: the Alpha and the Beta. TCC has 90 percent of the high-end market (Beta) and 50 percent of the low-end market (Alpha). The Alpha sells for $100,000. The Beta sells for $200,000 but has three times the capacity of the Alpha.

TCC has developed a new high-volume machine, Zeta, that has four times the capacity of the Beta and lower operating costs, but a price of $300,000. The unit manufacturing cost is $170,000. Users can connect the Zeta directly to mainframe computers for customer billing as well as to future expected telecommunications advancements. If the Zeta is introduced, management expects that its closest competition will be from the Beta, so most initial sales of the Zeta will come at the expense of Beta sales.

Senior management has invested considerable resources in Zeta. It believes that the future of the company is tied closely to the success of this project. Next year's operations of TCC (if the Zeta is not introduced) are:

Next Year's Projected Profits by Product without Zet a

* Assigned based on commissions.The existing sales force will sell all three types of machines. Salespeople are paid a salary plus 10 percent of sales. To sell the Zeta, salespeople with more knowledge of telecommunications and computer systems will be hired. The additional salary cost of these new employees will be $500,000. The existing sales force will still sell the Zeta but will call in these system experts to assist with the sale. The Zeta system experts are paid a flat salary, and the existing sales force's 10 percent commission incentive will not change with the introduction of the Zeta.

If the Zeta is not introduced, Alpha unit sales are projected to grow at 5 percent per year and Beta unit sales are projected to grow at 10 percent per year. Selling prices will remain constant in real terms. (Prices and salaries will grow at the inflation rate. To keep the analysis simple, all numbers should be projected in real, not nominal, terms. That is, do not adjust the numbers for inflation.)

If the Zeta is introduced, Alpha unit sales will not be affected. But Beta unit sales will be affected: All the Zeta sales will come from the Beta sales in the first year and then Beta unit sales will grow only 2 percent per year. Zeta sales will grow at 9 percent per year from an initial base of 25 machines.

Required:

Management wants to see how the preceding table on product-line profitability will appear when the Zeta model is added. In particular, management asks you to project profits for the Alpha, Beta, and Zeta for the next five years and to make a recommendation on this project. Discuss how the five-year product-line profitability projections should be presented to senior management.

سؤال

Fiedler International

You work on a team that reports to the chief financial officer of Fiedler International, a consumer products company that manages a variety of consumer beauty brands (shampoos, facial soaps, deodorants). Your team evaluates possible acquisitions. You are currently analyzing the possible purchase of Lush, a manufacturer of face moisturizers with UV sun blockers. Lush is a small publicly traded company that has no single large shareholder. Most of the stock is held by institutional investors and Lush managers hold a small percentage of the stock.

The materials you have received from Lush include information about its senior management performance evaluation and incentive compensation plans. Lush uses a balanced scorecard to evaluate and reward senior managers. Managers can earn up to 50 percent of their salary as a bonus depending on four balanced scorecard metrics: customer service, human resources and innovation, operational efficiency, and financial performance. Each of the four metrics is scaled between 0 and 1. Senior managers receive up to 25 percent of their bonus for each metric. If the customer service metric is 0.67, and a particular manager's salary is $400,000, then for customer service, that manager receives $33,500 (50% × $400,000 × 0.67 × 25%). The compensation committee of Lush's board of directors sets the scale for each of the four metrics. For example, the financial performance metric is economic value added, or EVA. Last year's EVA was $13 million. The compensation committee sets the lower and upper bound of EVA as $12 million and $16 million. Hence, if the current year's EVA is $12 million, the financial performance metric is 0. If EVA is $15 million, the metric is 0.75 [($15 - $12)/($16 - 12)], and the manager earning the $400,000 salary would receive a bonus of $37,500 (50% × $400,000 × 0.75 × 25%).

Fourteen separate metrics are used to compute the four metrics. The following metrics are computed and then aggregated to form the four metrics:![Fiedler International You work on a team that reports to the chief financial officer of Fiedler International, a consumer products company that manages a variety of consumer beauty brands (shampoos, facial soaps, deodorants). Your team evaluates possible acquisitions. You are currently analyzing the possible purchase of Lush, a manufacturer of face moisturizers with UV sun blockers. Lush is a small publicly traded company that has no single large shareholder. Most of the stock is held by institutional investors and Lush managers hold a small percentage of the stock. The materials you have received from Lush include information about its senior management performance evaluation and incentive compensation plans. Lush uses a balanced scorecard to evaluate and reward senior managers. Managers can earn up to 50 percent of their salary as a bonus depending on four balanced scorecard metrics: customer service, human resources and innovation, operational efficiency, and financial performance. Each of the four metrics is scaled between 0 and 1. Senior managers receive up to 25 percent of their bonus for each metric. If the customer service metric is 0.67, and a particular manager's salary is $400,000, then for customer service, that manager receives $33,500 (50% × $400,000 × 0.67 × 25%). The compensation committee of Lush's board of directors sets the scale for each of the four metrics. For example, the financial performance metric is economic value added, or EVA. Last year's EVA was $13 million. The compensation committee sets the lower and upper bound of EVA as $12 million and $16 million. Hence, if the current year's EVA is $12 million, the financial performance metric is 0. If EVA is $15 million, the metric is 0.75 [($15 - $12)/($16 - 12)], and the manager earning the $400,000 salary would receive a bonus of $37,500 (50% × $400,000 × 0.75 × 25%). Fourteen separate metrics are used to compute the four metrics. The following metrics are computed and then aggregated to form the four metrics: Lush has been using the balanced scorecard for three years and the achieved levels of each metric for the last three years are: Required: Write a memo to your acquisition team describing balanced scorecards and the primary reasons they are used, and the likely affect of Lush's use of the balanced scorecard in terms of how Fiedler should be evaluating Lush. Specifically: ( a ) briefly describe balanced scorecards and why firms use them and ( b ) analyze Lush's use of the balanced scorecard and how this might affect Fiedler's evaluation of Lush as a possible takeover target.<div style=padding-top: 35px>](https://d2lvgg3v3hfg70.cloudfront.net/SM1503/11eb559c_84cc_9046_a8c8_95c910fd1e89_SM1503_00.jpg) Lush has been using the balanced scorecard for three years and the achieved levels of each metric for the last three years are:

Lush has been using the balanced scorecard for three years and the achieved levels of each metric for the last three years are: ![Fiedler International You work on a team that reports to the chief financial officer of Fiedler International, a consumer products company that manages a variety of consumer beauty brands (shampoos, facial soaps, deodorants). Your team evaluates possible acquisitions. You are currently analyzing the possible purchase of Lush, a manufacturer of face moisturizers with UV sun blockers. Lush is a small publicly traded company that has no single large shareholder. Most of the stock is held by institutional investors and Lush managers hold a small percentage of the stock. The materials you have received from Lush include information about its senior management performance evaluation and incentive compensation plans. Lush uses a balanced scorecard to evaluate and reward senior managers. Managers can earn up to 50 percent of their salary as a bonus depending on four balanced scorecard metrics: customer service, human resources and innovation, operational efficiency, and financial performance. Each of the four metrics is scaled between 0 and 1. Senior managers receive up to 25 percent of their bonus for each metric. If the customer service metric is 0.67, and a particular manager's salary is $400,000, then for customer service, that manager receives $33,500 (50% × $400,000 × 0.67 × 25%). The compensation committee of Lush's board of directors sets the scale for each of the four metrics. For example, the financial performance metric is economic value added, or EVA. Last year's EVA was $13 million. The compensation committee sets the lower and upper bound of EVA as $12 million and $16 million. Hence, if the current year's EVA is $12 million, the financial performance metric is 0. If EVA is $15 million, the metric is 0.75 [($15 - $12)/($16 - 12)], and the manager earning the $400,000 salary would receive a bonus of $37,500 (50% × $400,000 × 0.75 × 25%). Fourteen separate metrics are used to compute the four metrics. The following metrics are computed and then aggregated to form the four metrics: Lush has been using the balanced scorecard for three years and the achieved levels of each metric for the last three years are: Required: Write a memo to your acquisition team describing balanced scorecards and the primary reasons they are used, and the likely affect of Lush's use of the balanced scorecard in terms of how Fiedler should be evaluating Lush. Specifically: ( a ) briefly describe balanced scorecards and why firms use them and ( b ) analyze Lush's use of the balanced scorecard and how this might affect Fiedler's evaluation of Lush as a possible takeover target.<div style=padding-top: 35px>](https://d2lvgg3v3hfg70.cloudfront.net/SM1503/11eb559c_84cc_9047_a8c8_5b51a7500ff0_SM1503_00.jpg) Required:

Required:

Write a memo to your acquisition team describing balanced scorecards and the primary reasons they are used, and the likely affect of Lush's use of the balanced scorecard in terms of how Fiedler should be evaluating Lush. Specifically: ( a ) briefly describe balanced scorecards and why firms use them and ( b ) analyze Lush's use of the balanced scorecard and how this might affect Fiedler's evaluation of Lush as a possible takeover target.

You work on a team that reports to the chief financial officer of Fiedler International, a consumer products company that manages a variety of consumer beauty brands (shampoos, facial soaps, deodorants). Your team evaluates possible acquisitions. You are currently analyzing the possible purchase of Lush, a manufacturer of face moisturizers with UV sun blockers. Lush is a small publicly traded company that has no single large shareholder. Most of the stock is held by institutional investors and Lush managers hold a small percentage of the stock.