Deck 5: Markup As a Merchandising Tool

ملء الشاشة (f)

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

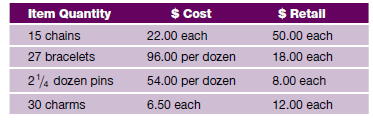

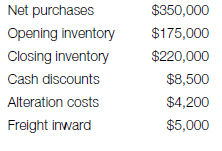

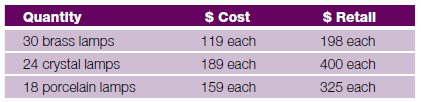

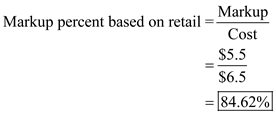

Determine the markup percent for the following group of merchandise:

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

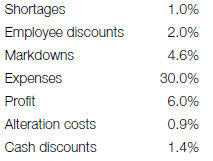

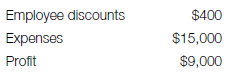

The following figures have been planned for a department:

Calculate the initial markup percent that should be used in order to arrive at the planned figures.

Calculate the initial markup percent that should be used in order to arrive at the planned figures.

سؤال

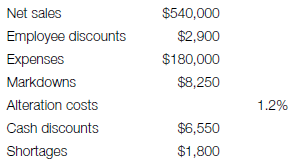

Calculate the initial markup percent that will be required to achieve a 6% profit, using the following figures:

سؤال

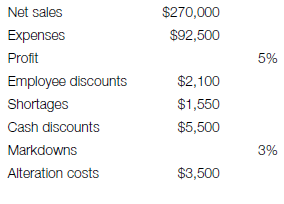

Determine the initial markup percent for a children's department with these figures:

سؤال

سؤال

سؤال

The net sales for a shoe department were $650,000. Calculate the maintained markup percent if the department has the following figures:

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

Operating a Successful Bridal Business

Wanda K. Cheek, Ph.D., Mississippi State University

You are the owner of a soon-to-open bridal store in a college town, with a population of 45,000. You began work on the business plan over a year ago, but are now within six months of the grand opening. It is time to make serious decisions concerning the financial aspects of merchandising a fashion-oriented business. Understanding markup and competitive retail pricing is an important part of the successful operation of this business.

Many merchandising and retailing students do not understand the unique structure of the retail bridal business and how it is different from most fashion businesses. The following background information is presented to clarify the differences.

First, to get into the retail bridal business, a bridal business owner carefully researches specialized bridal markets for dresses and accessories, such as the National Bridal Show at The Merchandise Mart in Chicago. There are two specialized bridal markets per year: (1) fall market in September or October for upcoming spring/summer weddings [merchandise arrives in stores in January and February] and (2) spring market in March or April for upcoming fall/winter weddings [merchandise arrives in stores in August and September]. Most bridal businesses make most purchases at fall market, since the upcoming spring and summer wedding season is by far the largest selling season of all. Business profits hinge on the success of sales during this season.

Another major difference in the bridal business, compared to other fashion retailing business structures, is that the owner only purchases sample dresses at the market. Therefore, inventory expenditures are greatly reduced, because a small store such as yours will only have about 80-90 dresses hanging in stock. Since all will be sample dresses that any bride may choose, it is important to specify sizes that can be pinned up or expanded as needed. Therefore, sizes 10, 12, 14, and 16 are popular sample sizes, with a few styles for larger sizes (up to 26). Small sample sizes such as 2 and 4 would most likely be the least useful. Therefore, sales persons need to be experienced and proficient in measuring and determining actual sizes to order.

Because the dresses will then need to be sewn by the manufacturer, bridal gown orders should ideally be placed at least six months in advance of the wedding to allow for arrival and alterations. At a minimum, gowns take three to four months for completion and delivery, depending on the designer. Rush orders are available for an extra fee, but six to eight weeks is usually required. Thus, order completion time is slow. To discourage brides who change their minds, a 60% nonrefundable deposit is generally required at the time the order is placed. Thus, return on investment in sample size stock is slow. However, since most orders will be custom, the trade-off is that markdowns on bridal gowns will be almost limited to the markdowns on sample gowns that are sold at the end of the order season (generally January and July sales).

In the trade (wholesale and retail), markup on bridal gowns is often discussed in terms of markup based on cost, rather than markup based on retail. Earlier in this chapter, keystone markup was defined as a markup that doubles the cost of the merchandise. Thus, for keystone markup, a 2.0 factor is used since the retail price is twice the cost. Bridal owners often use a markup that is more than a 2.0 factor, such as a 2.5 factor or even greater (3.0). This means that the wholesale cost is multiplied by 2.5 or 3.0, etc., to determine the $ Retail. In effect this is the same as doubling (or tripling with a factor of 3.0) the wholesale cost and adding an additional amount to ensure profitability. It is important to remember that the retail markup percent can be calculated from this information. In the bridal business, an ideal $ Retail is based on an Initial Markup (retail) % of 60% or a 2.5 factor.

Other issues in the bridal business that impact profitability and markup are transportation and alterations. In the bridal business, these expenses are pricey, compared to expenses in other types of fashion retailers. The current cost for shipping for each dress is about $20. Simple alterations begin at $40 for hemming and a bust adjustment for strapless gowns, depending on the area of the country, and prices go from that point. As the owner of the business, you must decide whether you will build these expenses into markup. In some bridal stores, each of these is added as an extra expense to be paid by the bride above the quoted $ Retail. The pricing philosophy is that treating these separately keeps the $ Retail price competitive.

Determine the Retail Markup% for a famous brand gown with a wholesale cost of $650 and a manufacturer's suggested retail price of $1,600. Then calculate the markup factor based on cost.

![Operating a Successful Bridal Business Wanda K. Cheek, Ph.D., Mississippi State University You are the owner of a soon-to-open bridal store in a college town, with a population of 45,000. You began work on the business plan over a year ago, but are now within six months of the grand opening. It is time to make serious decisions concerning the financial aspects of merchandising a fashion-oriented business. Understanding markup and competitive retail pricing is an important part of the successful operation of this business. Many merchandising and retailing students do not understand the unique structure of the retail bridal business and how it is different from most fashion businesses. The following background information is presented to clarify the differences. First, to get into the retail bridal business, a bridal business owner carefully researches specialized bridal markets for dresses and accessories, such as the National Bridal Show at The Merchandise Mart in Chicago. There are two specialized bridal markets per year: (1) fall market in September or October for upcoming spring/summer weddings [merchandise arrives in stores in January and February] and (2) spring market in March or April for upcoming fall/winter weddings [merchandise arrives in stores in August and September]. Most bridal businesses make most purchases at fall market, since the upcoming spring and summer wedding season is by far the largest selling season of all. Business profits hinge on the success of sales during this season. Another major difference in the bridal business, compared to other fashion retailing business structures, is that the owner only purchases sample dresses at the market. Therefore, inventory expenditures are greatly reduced, because a small store such as yours will only have about 80-90 dresses hanging in stock. Since all will be sample dresses that any bride may choose, it is important to specify sizes that can be pinned up or expanded as needed. Therefore, sizes 10, 12, 14, and 16 are popular sample sizes, with a few styles for larger sizes (up to 26). Small sample sizes such as 2 and 4 would most likely be the least useful. Therefore, sales persons need to be experienced and proficient in measuring and determining actual sizes to order. Because the dresses will then need to be sewn by the manufacturer, bridal gown orders should ideally be placed at least six months in advance of the wedding to allow for arrival and alterations. At a minimum, gowns take three to four months for completion and delivery, depending on the designer. Rush orders are available for an extra fee, but six to eight weeks is usually required. Thus, order completion time is slow. To discourage brides who change their minds, a 60% nonrefundable deposit is generally required at the time the order is placed. Thus, return on investment in sample size stock is slow. However, since most orders will be custom, the trade-off is that markdowns on bridal gowns will be almost limited to the markdowns on sample gowns that are sold at the end of the order season (generally January and July sales). In the trade (wholesale and retail), markup on bridal gowns is often discussed in terms of markup based on cost, rather than markup based on retail. Earlier in this chapter, keystone markup was defined as a markup that doubles the cost of the merchandise. Thus, for keystone markup, a 2.0 factor is used since the retail price is twice the cost. Bridal owners often use a markup that is more than a 2.0 factor, such as a 2.5 factor or even greater (3.0). This means that the wholesale cost is multiplied by 2.5 or 3.0, etc., to determine the $ Retail. In effect this is the same as doubling (or tripling with a factor of 3.0) the wholesale cost and adding an additional amount to ensure profitability. It is important to remember that the retail markup percent can be calculated from this information. In the bridal business, an ideal $ Retail is based on an Initial Markup (retail) % of 60% or a 2.5 factor. Other issues in the bridal business that impact profitability and markup are transportation and alterations. In the bridal business, these expenses are pricey, compared to expenses in other types of fashion retailers. The current cost for shipping for each dress is about $20. Simple alterations begin at $40 for hemming and a bust adjustment for strapless gowns, depending on the area of the country, and prices go from that point. As the owner of the business, you must decide whether you will build these expenses into markup. In some bridal stores, each of these is added as an extra expense to be paid by the bride above the quoted $ Retail. The pricing philosophy is that treating these separately keeps the $ Retail price competitive. Determine the Retail Markup% for a famous brand gown with a wholesale cost of $650 and a manufacturer's suggested retail price of $1,600. Then calculate the markup factor based on cost. <div style=padding-top: 35px>](https://d2lvgg3v3hfg70.cloudfront.net/SM3014/11eb66c1_87b6_af86_953c_f502463445cd_SM3014_00.jpg)

Wanda K. Cheek, Ph.D., Mississippi State University

You are the owner of a soon-to-open bridal store in a college town, with a population of 45,000. You began work on the business plan over a year ago, but are now within six months of the grand opening. It is time to make serious decisions concerning the financial aspects of merchandising a fashion-oriented business. Understanding markup and competitive retail pricing is an important part of the successful operation of this business.

Many merchandising and retailing students do not understand the unique structure of the retail bridal business and how it is different from most fashion businesses. The following background information is presented to clarify the differences.

First, to get into the retail bridal business, a bridal business owner carefully researches specialized bridal markets for dresses and accessories, such as the National Bridal Show at The Merchandise Mart in Chicago. There are two specialized bridal markets per year: (1) fall market in September or October for upcoming spring/summer weddings [merchandise arrives in stores in January and February] and (2) spring market in March or April for upcoming fall/winter weddings [merchandise arrives in stores in August and September]. Most bridal businesses make most purchases at fall market, since the upcoming spring and summer wedding season is by far the largest selling season of all. Business profits hinge on the success of sales during this season.

Another major difference in the bridal business, compared to other fashion retailing business structures, is that the owner only purchases sample dresses at the market. Therefore, inventory expenditures are greatly reduced, because a small store such as yours will only have about 80-90 dresses hanging in stock. Since all will be sample dresses that any bride may choose, it is important to specify sizes that can be pinned up or expanded as needed. Therefore, sizes 10, 12, 14, and 16 are popular sample sizes, with a few styles for larger sizes (up to 26). Small sample sizes such as 2 and 4 would most likely be the least useful. Therefore, sales persons need to be experienced and proficient in measuring and determining actual sizes to order.

Because the dresses will then need to be sewn by the manufacturer, bridal gown orders should ideally be placed at least six months in advance of the wedding to allow for arrival and alterations. At a minimum, gowns take three to four months for completion and delivery, depending on the designer. Rush orders are available for an extra fee, but six to eight weeks is usually required. Thus, order completion time is slow. To discourage brides who change their minds, a 60% nonrefundable deposit is generally required at the time the order is placed. Thus, return on investment in sample size stock is slow. However, since most orders will be custom, the trade-off is that markdowns on bridal gowns will be almost limited to the markdowns on sample gowns that are sold at the end of the order season (generally January and July sales).

In the trade (wholesale and retail), markup on bridal gowns is often discussed in terms of markup based on cost, rather than markup based on retail. Earlier in this chapter, keystone markup was defined as a markup that doubles the cost of the merchandise. Thus, for keystone markup, a 2.0 factor is used since the retail price is twice the cost. Bridal owners often use a markup that is more than a 2.0 factor, such as a 2.5 factor or even greater (3.0). This means that the wholesale cost is multiplied by 2.5 or 3.0, etc., to determine the $ Retail. In effect this is the same as doubling (or tripling with a factor of 3.0) the wholesale cost and adding an additional amount to ensure profitability. It is important to remember that the retail markup percent can be calculated from this information. In the bridal business, an ideal $ Retail is based on an Initial Markup (retail) % of 60% or a 2.5 factor.

Other issues in the bridal business that impact profitability and markup are transportation and alterations. In the bridal business, these expenses are pricey, compared to expenses in other types of fashion retailers. The current cost for shipping for each dress is about $20. Simple alterations begin at $40 for hemming and a bust adjustment for strapless gowns, depending on the area of the country, and prices go from that point. As the owner of the business, you must decide whether you will build these expenses into markup. In some bridal stores, each of these is added as an extra expense to be paid by the bride above the quoted $ Retail. The pricing philosophy is that treating these separately keeps the $ Retail price competitive.

Determine the Retail Markup% for a famous brand gown with a wholesale cost of $650 and a manufacturer's suggested retail price of $1,600. Then calculate the markup factor based on cost.

سؤال

Operating a Successful Bridal Business

Wanda K. Cheek, Ph.D., Mississippi State University

You are the owner of a soon-to-open bridal store in a college town, with a population of 45,000. You began work on the business plan over a year ago, but are now within six months of the grand opening. It is time to make serious decisions concerning the financial aspects of merchandising a fashion-oriented business. Understanding markup and competitive retail pricing is an important part of the successful operation of this business.

Many merchandising and retailing students do not understand the unique structure of the retail bridal business and how it is different from most fashion businesses. The following background information is presented to clarify the differences.

First, to get into the retail bridal business, a bridal business owner carefully researches specialized bridal markets for dresses and accessories, such as the National Bridal Show at The Merchandise Mart in Chicago. There are two specialized bridal markets per year: (1) fall market in September or October for upcoming spring/summer weddings [merchandise arrives in stores in January and February] and (2) spring market in March or April for upcoming fall/winter weddings [merchandise arrives in stores in August and September]. Most bridal businesses make most purchases at fall market, since the upcoming spring and summer wedding season is by far the largest selling season of all. Business profits hinge on the success of sales during this season.

Another major difference in the bridal business, compared to other fashion retailing business structures, is that the owner only purchases sample dresses at the market. Therefore, inventory expenditures are greatly reduced, because a small store such as yours will only have about 80-90 dresses hanging in stock. Since all will be sample dresses that any bride may choose, it is important to specify sizes that can be pinned up or expanded as needed. Therefore, sizes 10, 12, 14, and 16 are popular sample sizes, with a few styles for larger sizes (up to 26). Small sample sizes such as 2 and 4 would most likely be the least useful. Therefore, sales persons need to be experienced and proficient in measuring and determining actual sizes to order.

Because the dresses will then need to be sewn by the manufacturer, bridal gown orders should ideally be placed at least six months in advance of the wedding to allow for arrival and alterations. At a minimum, gowns take three to four months for completion and delivery, depending on the designer. Rush orders are available for an extra fee, but six to eight weeks is usually required. Thus, order completion time is slow. To discourage brides who change their minds, a 60% nonrefundable deposit is generally required at the time the order is placed. Thus, return on investment in sample size stock is slow. However, since most orders will be custom, the trade-off is that markdowns on bridal gowns will be almost limited to the markdowns on sample gowns that are sold at the end of the order season (generally January and July sales).

In the trade (wholesale and retail), markup on bridal gowns is often discussed in terms of markup based on cost, rather than markup based on retail. Earlier in this chapter, keystone markup was defined as a markup that doubles the cost of the merchandise. Thus, for keystone markup, a 2.0 factor is used since the retail price is twice the cost. Bridal owners often use a markup that is more than a 2.0 factor, such as a 2.5 factor or even greater (3.0). This means that the wholesale cost is multiplied by 2.5 or 3.0, etc., to determine the $ Retail. In effect this is the same as doubling (or tripling with a factor of 3.0) the wholesale cost and adding an additional amount to ensure profitability. It is important to remember that the retail markup percent can be calculated from this information. In the bridal business, an ideal $ Retail is based on an Initial Markup (retail) % of 60% or a 2.5 factor.

Other issues in the bridal business that impact profitability and markup are transportation and alterations. In the bridal business, these expenses are pricey, compared to expenses in other types of fashion retailers. The current cost for shipping for each dress is about $20. Simple alterations begin at $40 for hemming and a bust adjustment for strapless gowns, depending on the area of the country, and prices go from that point. As the owner of the business, you must decide whether you will build these expenses into markup. In some bridal stores, each of these is added as an extra expense to be paid by the bride above the quoted $ Retail. The pricing philosophy is that treating these separately keeps the $ Retail price competitive.

Using the figures below, determine the $ Retail based on cost and the Retail Markup % Equivalent for dress style # 1001. Calculate the answers manually and then by spreadsheet.

![Operating a Successful Bridal Business Wanda K. Cheek, Ph.D., Mississippi State University You are the owner of a soon-to-open bridal store in a college town, with a population of 45,000. You began work on the business plan over a year ago, but are now within six months of the grand opening. It is time to make serious decisions concerning the financial aspects of merchandising a fashion-oriented business. Understanding markup and competitive retail pricing is an important part of the successful operation of this business. Many merchandising and retailing students do not understand the unique structure of the retail bridal business and how it is different from most fashion businesses. The following background information is presented to clarify the differences. First, to get into the retail bridal business, a bridal business owner carefully researches specialized bridal markets for dresses and accessories, such as the National Bridal Show at The Merchandise Mart in Chicago. There are two specialized bridal markets per year: (1) fall market in September or October for upcoming spring/summer weddings [merchandise arrives in stores in January and February] and (2) spring market in March or April for upcoming fall/winter weddings [merchandise arrives in stores in August and September]. Most bridal businesses make most purchases at fall market, since the upcoming spring and summer wedding season is by far the largest selling season of all. Business profits hinge on the success of sales during this season. Another major difference in the bridal business, compared to other fashion retailing business structures, is that the owner only purchases sample dresses at the market. Therefore, inventory expenditures are greatly reduced, because a small store such as yours will only have about 80-90 dresses hanging in stock. Since all will be sample dresses that any bride may choose, it is important to specify sizes that can be pinned up or expanded as needed. Therefore, sizes 10, 12, 14, and 16 are popular sample sizes, with a few styles for larger sizes (up to 26). Small sample sizes such as 2 and 4 would most likely be the least useful. Therefore, sales persons need to be experienced and proficient in measuring and determining actual sizes to order. Because the dresses will then need to be sewn by the manufacturer, bridal gown orders should ideally be placed at least six months in advance of the wedding to allow for arrival and alterations. At a minimum, gowns take three to four months for completion and delivery, depending on the designer. Rush orders are available for an extra fee, but six to eight weeks is usually required. Thus, order completion time is slow. To discourage brides who change their minds, a 60% nonrefundable deposit is generally required at the time the order is placed. Thus, return on investment in sample size stock is slow. However, since most orders will be custom, the trade-off is that markdowns on bridal gowns will be almost limited to the markdowns on sample gowns that are sold at the end of the order season (generally January and July sales). In the trade (wholesale and retail), markup on bridal gowns is often discussed in terms of markup based on cost, rather than markup based on retail. Earlier in this chapter, keystone markup was defined as a markup that doubles the cost of the merchandise. Thus, for keystone markup, a 2.0 factor is used since the retail price is twice the cost. Bridal owners often use a markup that is more than a 2.0 factor, such as a 2.5 factor or even greater (3.0). This means that the wholesale cost is multiplied by 2.5 or 3.0, etc., to determine the $ Retail. In effect this is the same as doubling (or tripling with a factor of 3.0) the wholesale cost and adding an additional amount to ensure profitability. It is important to remember that the retail markup percent can be calculated from this information. In the bridal business, an ideal $ Retail is based on an Initial Markup (retail) % of 60% or a 2.5 factor. Other issues in the bridal business that impact profitability and markup are transportation and alterations. In the bridal business, these expenses are pricey, compared to expenses in other types of fashion retailers. The current cost for shipping for each dress is about $20. Simple alterations begin at $40 for hemming and a bust adjustment for strapless gowns, depending on the area of the country, and prices go from that point. As the owner of the business, you must decide whether you will build these expenses into markup. In some bridal stores, each of these is added as an extra expense to be paid by the bride above the quoted $ Retail. The pricing philosophy is that treating these separately keeps the $ Retail price competitive. Using the figures below, determine the $ Retail based on cost and the Retail Markup % Equivalent for dress style # 1001. Calculate the answers manually and then by spreadsheet. <div style=padding-top: 35px>](https://d2lvgg3v3hfg70.cloudfront.net/SM3014/11eb66c1_87b8_f97c_953c_a7c5deac8c38_SM3014_00.jpg)

Wanda K. Cheek, Ph.D., Mississippi State University

You are the owner of a soon-to-open bridal store in a college town, with a population of 45,000. You began work on the business plan over a year ago, but are now within six months of the grand opening. It is time to make serious decisions concerning the financial aspects of merchandising a fashion-oriented business. Understanding markup and competitive retail pricing is an important part of the successful operation of this business.

Many merchandising and retailing students do not understand the unique structure of the retail bridal business and how it is different from most fashion businesses. The following background information is presented to clarify the differences.

First, to get into the retail bridal business, a bridal business owner carefully researches specialized bridal markets for dresses and accessories, such as the National Bridal Show at The Merchandise Mart in Chicago. There are two specialized bridal markets per year: (1) fall market in September or October for upcoming spring/summer weddings [merchandise arrives in stores in January and February] and (2) spring market in March or April for upcoming fall/winter weddings [merchandise arrives in stores in August and September]. Most bridal businesses make most purchases at fall market, since the upcoming spring and summer wedding season is by far the largest selling season of all. Business profits hinge on the success of sales during this season.

Another major difference in the bridal business, compared to other fashion retailing business structures, is that the owner only purchases sample dresses at the market. Therefore, inventory expenditures are greatly reduced, because a small store such as yours will only have about 80-90 dresses hanging in stock. Since all will be sample dresses that any bride may choose, it is important to specify sizes that can be pinned up or expanded as needed. Therefore, sizes 10, 12, 14, and 16 are popular sample sizes, with a few styles for larger sizes (up to 26). Small sample sizes such as 2 and 4 would most likely be the least useful. Therefore, sales persons need to be experienced and proficient in measuring and determining actual sizes to order.

Because the dresses will then need to be sewn by the manufacturer, bridal gown orders should ideally be placed at least six months in advance of the wedding to allow for arrival and alterations. At a minimum, gowns take three to four months for completion and delivery, depending on the designer. Rush orders are available for an extra fee, but six to eight weeks is usually required. Thus, order completion time is slow. To discourage brides who change their minds, a 60% nonrefundable deposit is generally required at the time the order is placed. Thus, return on investment in sample size stock is slow. However, since most orders will be custom, the trade-off is that markdowns on bridal gowns will be almost limited to the markdowns on sample gowns that are sold at the end of the order season (generally January and July sales).

In the trade (wholesale and retail), markup on bridal gowns is often discussed in terms of markup based on cost, rather than markup based on retail. Earlier in this chapter, keystone markup was defined as a markup that doubles the cost of the merchandise. Thus, for keystone markup, a 2.0 factor is used since the retail price is twice the cost. Bridal owners often use a markup that is more than a 2.0 factor, such as a 2.5 factor or even greater (3.0). This means that the wholesale cost is multiplied by 2.5 or 3.0, etc., to determine the $ Retail. In effect this is the same as doubling (or tripling with a factor of 3.0) the wholesale cost and adding an additional amount to ensure profitability. It is important to remember that the retail markup percent can be calculated from this information. In the bridal business, an ideal $ Retail is based on an Initial Markup (retail) % of 60% or a 2.5 factor.

Other issues in the bridal business that impact profitability and markup are transportation and alterations. In the bridal business, these expenses are pricey, compared to expenses in other types of fashion retailers. The current cost for shipping for each dress is about $20. Simple alterations begin at $40 for hemming and a bust adjustment for strapless gowns, depending on the area of the country, and prices go from that point. As the owner of the business, you must decide whether you will build these expenses into markup. In some bridal stores, each of these is added as an extra expense to be paid by the bride above the quoted $ Retail. The pricing philosophy is that treating these separately keeps the $ Retail price competitive.

Using the figures below, determine the $ Retail based on cost and the Retail Markup % Equivalent for dress style # 1001. Calculate the answers manually and then by spreadsheet.

سؤال

Operating a Successful Bridal Business

Wanda K. Cheek, Ph.D., Mississippi State University

You are the owner of a soon-to-open bridal store in a college town, with a population of 45,000. You began work on the business plan over a year ago, but are now within six months of the grand opening. It is time to make serious decisions concerning the financial aspects of merchandising a fashion-oriented business. Understanding markup and competitive retail pricing is an important part of the successful operation of this business.

Many merchandising and retailing students do not understand the unique structure of the retail bridal business and how it is different from most fashion businesses. The following background information is presented to clarify the differences.

First, to get into the retail bridal business, a bridal business owner carefully researches specialized bridal markets for dresses and accessories, such as the National Bridal Show at The Merchandise Mart in Chicago. There are two specialized bridal markets per year: (1) fall market in September or October for upcoming spring/summer weddings [merchandise arrives in stores in January and February] and (2) spring market in March or April for upcoming fall/winter weddings [merchandise arrives in stores in August and September]. Most bridal businesses make most purchases at fall market, since the upcoming spring and summer wedding season is by far the largest selling season of all. Business profits hinge on the success of sales during this season.

Another major difference in the bridal business, compared to other fashion retailing business structures, is that the owner only purchases sample dresses at the market. Therefore, inventory expenditures are greatly reduced, because a small store such as yours will only have about 80-90 dresses hanging in stock. Since all will be sample dresses that any bride may choose, it is important to specify sizes that can be pinned up or expanded as needed. Therefore, sizes 10, 12, 14, and 16 are popular sample sizes, with a few styles for larger sizes (up to 26). Small sample sizes such as 2 and 4 would most likely be the least useful. Therefore, sales persons need to be experienced and proficient in measuring and determining actual sizes to order.

Because the dresses will then need to be sewn by the manufacturer, bridal gown orders should ideally be placed at least six months in advance of the wedding to allow for arrival and alterations. At a minimum, gowns take three to four months for completion and delivery, depending on the designer. Rush orders are available for an extra fee, but six to eight weeks is usually required. Thus, order completion time is slow. To discourage brides who change their minds, a 60% nonrefundable deposit is generally required at the time the order is placed. Thus, return on investment in sample size stock is slow. However, since most orders will be custom, the trade-off is that markdowns on bridal gowns will be almost limited to the markdowns on sample gowns that are sold at the end of the order season (generally January and July sales).

In the trade (wholesale and retail), markup on bridal gowns is often discussed in terms of markup based on cost, rather than markup based on retail. Earlier in this chapter, keystone markup was defined as a markup that doubles the cost of the merchandise. Thus, for keystone markup, a 2.0 factor is used since the retail price is twice the cost. Bridal owners often use a markup that is more than a 2.0 factor, such as a 2.5 factor or even greater (3.0). This means that the wholesale cost is multiplied by 2.5 or 3.0, etc., to determine the $ Retail. In effect this is the same as doubling (or tripling with a factor of 3.0) the wholesale cost and adding an additional amount to ensure profitability. It is important to remember that the retail markup percent can be calculated from this information. In the bridal business, an ideal $ Retail is based on an Initial Markup (retail) % of 60% or a 2.5 factor.

Other issues in the bridal business that impact profitability and markup are transportation and alterations. In the bridal business, these expenses are pricey, compared to expenses in other types of fashion retailers. The current cost for shipping for each dress is about $20. Simple alterations begin at $40 for hemming and a bust adjustment for strapless gowns, depending on the area of the country, and prices go from that point. As the owner of the business, you must decide whether you will build these expenses into markup. In some bridal stores, each of these is added as an extra expense to be paid by the bride above the quoted $ Retail. The pricing philosophy is that treating these separately keeps the $ Retail price competitive.

For the same dress style# 1001, calculate the $ Retail assuming a 60% retail markup. Then add a transportation charge of $20 and an alteration charge of $40 to determine the final cost to the bride.

![Operating a Successful Bridal Business Wanda K. Cheek, Ph.D., Mississippi State University You are the owner of a soon-to-open bridal store in a college town, with a population of 45,000. You began work on the business plan over a year ago, but are now within six months of the grand opening. It is time to make serious decisions concerning the financial aspects of merchandising a fashion-oriented business. Understanding markup and competitive retail pricing is an important part of the successful operation of this business. Many merchandising and retailing students do not understand the unique structure of the retail bridal business and how it is different from most fashion businesses. The following background information is presented to clarify the differences. First, to get into the retail bridal business, a bridal business owner carefully researches specialized bridal markets for dresses and accessories, such as the National Bridal Show at The Merchandise Mart in Chicago. There are two specialized bridal markets per year: (1) fall market in September or October for upcoming spring/summer weddings [merchandise arrives in stores in January and February] and (2) spring market in March or April for upcoming fall/winter weddings [merchandise arrives in stores in August and September]. Most bridal businesses make most purchases at fall market, since the upcoming spring and summer wedding season is by far the largest selling season of all. Business profits hinge on the success of sales during this season. Another major difference in the bridal business, compared to other fashion retailing business structures, is that the owner only purchases sample dresses at the market. Therefore, inventory expenditures are greatly reduced, because a small store such as yours will only have about 80-90 dresses hanging in stock. Since all will be sample dresses that any bride may choose, it is important to specify sizes that can be pinned up or expanded as needed. Therefore, sizes 10, 12, 14, and 16 are popular sample sizes, with a few styles for larger sizes (up to 26). Small sample sizes such as 2 and 4 would most likely be the least useful. Therefore, sales persons need to be experienced and proficient in measuring and determining actual sizes to order. Because the dresses will then need to be sewn by the manufacturer, bridal gown orders should ideally be placed at least six months in advance of the wedding to allow for arrival and alterations. At a minimum, gowns take three to four months for completion and delivery, depending on the designer. Rush orders are available for an extra fee, but six to eight weeks is usually required. Thus, order completion time is slow. To discourage brides who change their minds, a 60% nonrefundable deposit is generally required at the time the order is placed. Thus, return on investment in sample size stock is slow. However, since most orders will be custom, the trade-off is that markdowns on bridal gowns will be almost limited to the markdowns on sample gowns that are sold at the end of the order season (generally January and July sales). In the trade (wholesale and retail), markup on bridal gowns is often discussed in terms of markup based on cost, rather than markup based on retail. Earlier in this chapter, keystone markup was defined as a markup that doubles the cost of the merchandise. Thus, for keystone markup, a 2.0 factor is used since the retail price is twice the cost. Bridal owners often use a markup that is more than a 2.0 factor, such as a 2.5 factor or even greater (3.0). This means that the wholesale cost is multiplied by 2.5 or 3.0, etc., to determine the $ Retail. In effect this is the same as doubling (or tripling with a factor of 3.0) the wholesale cost and adding an additional amount to ensure profitability. It is important to remember that the retail markup percent can be calculated from this information. In the bridal business, an ideal $ Retail is based on an Initial Markup (retail) % of 60% or a 2.5 factor. Other issues in the bridal business that impact profitability and markup are transportation and alterations. In the bridal business, these expenses are pricey, compared to expenses in other types of fashion retailers. The current cost for shipping for each dress is about $20. Simple alterations begin at $40 for hemming and a bust adjustment for strapless gowns, depending on the area of the country, and prices go from that point. As the owner of the business, you must decide whether you will build these expenses into markup. In some bridal stores, each of these is added as an extra expense to be paid by the bride above the quoted $ Retail. The pricing philosophy is that treating these separately keeps the $ Retail price competitive. For the same dress style# 1001, calculate the $ Retail assuming a 60% retail markup. Then add a transportation charge of $20 and an alteration charge of $40 to determine the final cost to the bride. <div style=padding-top: 35px>](https://d2lvgg3v3hfg70.cloudfront.net/SM3014/11eb66c1_87bc_ca15_953c_9362acd55672_SM3014_00.jpg)

Wanda K. Cheek, Ph.D., Mississippi State University

You are the owner of a soon-to-open bridal store in a college town, with a population of 45,000. You began work on the business plan over a year ago, but are now within six months of the grand opening. It is time to make serious decisions concerning the financial aspects of merchandising a fashion-oriented business. Understanding markup and competitive retail pricing is an important part of the successful operation of this business.

Many merchandising and retailing students do not understand the unique structure of the retail bridal business and how it is different from most fashion businesses. The following background information is presented to clarify the differences.

First, to get into the retail bridal business, a bridal business owner carefully researches specialized bridal markets for dresses and accessories, such as the National Bridal Show at The Merchandise Mart in Chicago. There are two specialized bridal markets per year: (1) fall market in September or October for upcoming spring/summer weddings [merchandise arrives in stores in January and February] and (2) spring market in March or April for upcoming fall/winter weddings [merchandise arrives in stores in August and September]. Most bridal businesses make most purchases at fall market, since the upcoming spring and summer wedding season is by far the largest selling season of all. Business profits hinge on the success of sales during this season.

Another major difference in the bridal business, compared to other fashion retailing business structures, is that the owner only purchases sample dresses at the market. Therefore, inventory expenditures are greatly reduced, because a small store such as yours will only have about 80-90 dresses hanging in stock. Since all will be sample dresses that any bride may choose, it is important to specify sizes that can be pinned up or expanded as needed. Therefore, sizes 10, 12, 14, and 16 are popular sample sizes, with a few styles for larger sizes (up to 26). Small sample sizes such as 2 and 4 would most likely be the least useful. Therefore, sales persons need to be experienced and proficient in measuring and determining actual sizes to order.

Because the dresses will then need to be sewn by the manufacturer, bridal gown orders should ideally be placed at least six months in advance of the wedding to allow for arrival and alterations. At a minimum, gowns take three to four months for completion and delivery, depending on the designer. Rush orders are available for an extra fee, but six to eight weeks is usually required. Thus, order completion time is slow. To discourage brides who change their minds, a 60% nonrefundable deposit is generally required at the time the order is placed. Thus, return on investment in sample size stock is slow. However, since most orders will be custom, the trade-off is that markdowns on bridal gowns will be almost limited to the markdowns on sample gowns that are sold at the end of the order season (generally January and July sales).

In the trade (wholesale and retail), markup on bridal gowns is often discussed in terms of markup based on cost, rather than markup based on retail. Earlier in this chapter, keystone markup was defined as a markup that doubles the cost of the merchandise. Thus, for keystone markup, a 2.0 factor is used since the retail price is twice the cost. Bridal owners often use a markup that is more than a 2.0 factor, such as a 2.5 factor or even greater (3.0). This means that the wholesale cost is multiplied by 2.5 or 3.0, etc., to determine the $ Retail. In effect this is the same as doubling (or tripling with a factor of 3.0) the wholesale cost and adding an additional amount to ensure profitability. It is important to remember that the retail markup percent can be calculated from this information. In the bridal business, an ideal $ Retail is based on an Initial Markup (retail) % of 60% or a 2.5 factor.

Other issues in the bridal business that impact profitability and markup are transportation and alterations. In the bridal business, these expenses are pricey, compared to expenses in other types of fashion retailers. The current cost for shipping for each dress is about $20. Simple alterations begin at $40 for hemming and a bust adjustment for strapless gowns, depending on the area of the country, and prices go from that point. As the owner of the business, you must decide whether you will build these expenses into markup. In some bridal stores, each of these is added as an extra expense to be paid by the bride above the quoted $ Retail. The pricing philosophy is that treating these separately keeps the $ Retail price competitive.

For the same dress style# 1001, calculate the $ Retail assuming a 60% retail markup. Then add a transportation charge of $20 and an alteration charge of $40 to determine the final cost to the bride.

سؤال

Operating a Successful Bridal Business

Wanda K. Cheek, Ph.D., Mississippi State University

You are the owner of a soon-to-open bridal store in a college town, with a population of 45,000. You began work on the business plan over a year ago, but are now within six months of the grand opening. It is time to make serious decisions concerning the financial aspects of merchandising a fashion-oriented business. Understanding markup and competitive retail pricing is an important part of the successful operation of this business.

Many merchandising and retailing students do not understand the unique structure of the retail bridal business and how it is different from most fashion businesses. The following background information is presented to clarify the differences.

First, to get into the retail bridal business, a bridal business owner carefully researches specialized bridal markets for dresses and accessories, such as the National Bridal Show at The Merchandise Mart in Chicago. There are two specialized bridal markets per year: (1) fall market in September or October for upcoming spring/summer weddings [merchandise arrives in stores in January and February] and (2) spring market in March or April for upcoming fall/winter weddings [merchandise arrives in stores in August and September]. Most bridal businesses make most purchases at fall market, since the upcoming spring and summer wedding season is by far the largest selling season of all. Business profits hinge on the success of sales during this season.

Another major difference in the bridal business, compared to other fashion retailing business structures, is that the owner only purchases sample dresses at the market. Therefore, inventory expenditures are greatly reduced, because a small store such as yours will only have about 80-90 dresses hanging in stock. Since all will be sample dresses that any bride may choose, it is important to specify sizes that can be pinned up or expanded as needed. Therefore, sizes 10, 12, 14, and 16 are popular sample sizes, with a few styles for larger sizes (up to 26). Small sample sizes such as 2 and 4 would most likely be the least useful. Therefore, sales persons need to be experienced and proficient in measuring and determining actual sizes to order.

Because the dresses will then need to be sewn by the manufacturer, bridal gown orders should ideally be placed at least six months in advance of the wedding to allow for arrival and alterations. At a minimum, gowns take three to four months for completion and delivery, depending on the designer. Rush orders are available for an extra fee, but six to eight weeks is usually required. Thus, order completion time is slow. To discourage brides who change their minds, a 60% nonrefundable deposit is generally required at the time the order is placed. Thus, return on investment in sample size stock is slow. However, since most orders will be custom, the trade-off is that markdowns on bridal gowns will be almost limited to the markdowns on sample gowns that are sold at the end of the order season (generally January and July sales).

In the trade (wholesale and retail), markup on bridal gowns is often discussed in terms of markup based on cost, rather than markup based on retail. Earlier in this chapter, keystone markup was defined as a markup that doubles the cost of the merchandise. Thus, for keystone markup, a 2.0 factor is used since the retail price is twice the cost. Bridal owners often use a markup that is more than a 2.0 factor, such as a 2.5 factor or even greater (3.0). This means that the wholesale cost is multiplied by 2.5 or 3.0, etc., to determine the $ Retail. In effect this is the same as doubling (or tripling with a factor of 3.0) the wholesale cost and adding an additional amount to ensure profitability. It is important to remember that the retail markup percent can be calculated from this information. In the bridal business, an ideal $ Retail is based on an Initial Markup (retail) % of 60% or a 2.5 factor.

Other issues in the bridal business that impact profitability and markup are transportation and alterations. In the bridal business, these expenses are pricey, compared to expenses in other types of fashion retailers. The current cost for shipping for each dress is about $20. Simple alterations begin at $40 for hemming and a bust adjustment for strapless gowns, depending on the area of the country, and prices go from that point. As the owner of the business, you must decide whether you will build these expenses into markup. In some bridal stores, each of these is added as an extra expense to be paid by the bride above the quoted $ Retail. The pricing philosophy is that treating these separately keeps the $ Retail price competitive.

In reference to question #3, what do you think is the best method for a final $ Retail for the bridal gown? (a) Continue to mark the $ Retail at $625 and collect a separate charge of $20 for transportation and arrange a final fitting session with an alterations person in your store but let the bride pay that person's charge directly to him/her OR (b) Increase the $ Retail to include both a standard alteration charge and a standard delivery charge. Discuss the pros and cons of each.

![Operating a Successful Bridal Business Wanda K. Cheek, Ph.D., Mississippi State University You are the owner of a soon-to-open bridal store in a college town, with a population of 45,000. You began work on the business plan over a year ago, but are now within six months of the grand opening. It is time to make serious decisions concerning the financial aspects of merchandising a fashion-oriented business. Understanding markup and competitive retail pricing is an important part of the successful operation of this business. Many merchandising and retailing students do not understand the unique structure of the retail bridal business and how it is different from most fashion businesses. The following background information is presented to clarify the differences. First, to get into the retail bridal business, a bridal business owner carefully researches specialized bridal markets for dresses and accessories, such as the National Bridal Show at The Merchandise Mart in Chicago. There are two specialized bridal markets per year: (1) fall market in September or October for upcoming spring/summer weddings [merchandise arrives in stores in January and February] and (2) spring market in March or April for upcoming fall/winter weddings [merchandise arrives in stores in August and September]. Most bridal businesses make most purchases at fall market, since the upcoming spring and summer wedding season is by far the largest selling season of all. Business profits hinge on the success of sales during this season. Another major difference in the bridal business, compared to other fashion retailing business structures, is that the owner only purchases sample dresses at the market. Therefore, inventory expenditures are greatly reduced, because a small store such as yours will only have about 80-90 dresses hanging in stock. Since all will be sample dresses that any bride may choose, it is important to specify sizes that can be pinned up or expanded as needed. Therefore, sizes 10, 12, 14, and 16 are popular sample sizes, with a few styles for larger sizes (up to 26). Small sample sizes such as 2 and 4 would most likely be the least useful. Therefore, sales persons need to be experienced and proficient in measuring and determining actual sizes to order. Because the dresses will then need to be sewn by the manufacturer, bridal gown orders should ideally be placed at least six months in advance of the wedding to allow for arrival and alterations. At a minimum, gowns take three to four months for completion and delivery, depending on the designer. Rush orders are available for an extra fee, but six to eight weeks is usually required. Thus, order completion time is slow. To discourage brides who change their minds, a 60% nonrefundable deposit is generally required at the time the order is placed. Thus, return on investment in sample size stock is slow. However, since most orders will be custom, the trade-off is that markdowns on bridal gowns will be almost limited to the markdowns on sample gowns that are sold at the end of the order season (generally January and July sales). In the trade (wholesale and retail), markup on bridal gowns is often discussed in terms of markup based on cost, rather than markup based on retail. Earlier in this chapter, keystone markup was defined as a markup that doubles the cost of the merchandise. Thus, for keystone markup, a 2.0 factor is used since the retail price is twice the cost. Bridal owners often use a markup that is more than a 2.0 factor, such as a 2.5 factor or even greater (3.0). This means that the wholesale cost is multiplied by 2.5 or 3.0, etc., to determine the $ Retail. In effect this is the same as doubling (or tripling with a factor of 3.0) the wholesale cost and adding an additional amount to ensure profitability. It is important to remember that the retail markup percent can be calculated from this information. In the bridal business, an ideal $ Retail is based on an Initial Markup (retail) % of 60% or a 2.5 factor. Other issues in the bridal business that impact profitability and markup are transportation and alterations. In the bridal business, these expenses are pricey, compared to expenses in other types of fashion retailers. The current cost for shipping for each dress is about $20. Simple alterations begin at $40 for hemming and a bust adjustment for strapless gowns, depending on the area of the country, and prices go from that point. As the owner of the business, you must decide whether you will build these expenses into markup. In some bridal stores, each of these is added as an extra expense to be paid by the bride above the quoted $ Retail. The pricing philosophy is that treating these separately keeps the $ Retail price competitive. In reference to question #3, what do you think is the best method for a final $ Retail for the bridal gown? (a) Continue to mark the $ Retail at $625 and collect a separate charge of $20 for transportation and arrange a final fitting session with an alterations person in your store but let the bride pay that person's charge directly to him/her OR (b) Increase the $ Retail to include both a standard alteration charge and a standard delivery charge. Discuss the pros and cons of each. <div style=padding-top: 35px>](https://d2lvgg3v3hfg70.cloudfront.net/SM3014/11eb66c1_87c0_257a_953c_fb0403477161_SM3014_00.jpg)

Wanda K. Cheek, Ph.D., Mississippi State University

You are the owner of a soon-to-open bridal store in a college town, with a population of 45,000. You began work on the business plan over a year ago, but are now within six months of the grand opening. It is time to make serious decisions concerning the financial aspects of merchandising a fashion-oriented business. Understanding markup and competitive retail pricing is an important part of the successful operation of this business.

Many merchandising and retailing students do not understand the unique structure of the retail bridal business and how it is different from most fashion businesses. The following background information is presented to clarify the differences.

First, to get into the retail bridal business, a bridal business owner carefully researches specialized bridal markets for dresses and accessories, such as the National Bridal Show at The Merchandise Mart in Chicago. There are two specialized bridal markets per year: (1) fall market in September or October for upcoming spring/summer weddings [merchandise arrives in stores in January and February] and (2) spring market in March or April for upcoming fall/winter weddings [merchandise arrives in stores in August and September]. Most bridal businesses make most purchases at fall market, since the upcoming spring and summer wedding season is by far the largest selling season of all. Business profits hinge on the success of sales during this season.

Another major difference in the bridal business, compared to other fashion retailing business structures, is that the owner only purchases sample dresses at the market. Therefore, inventory expenditures are greatly reduced, because a small store such as yours will only have about 80-90 dresses hanging in stock. Since all will be sample dresses that any bride may choose, it is important to specify sizes that can be pinned up or expanded as needed. Therefore, sizes 10, 12, 14, and 16 are popular sample sizes, with a few styles for larger sizes (up to 26). Small sample sizes such as 2 and 4 would most likely be the least useful. Therefore, sales persons need to be experienced and proficient in measuring and determining actual sizes to order.

Because the dresses will then need to be sewn by the manufacturer, bridal gown orders should ideally be placed at least six months in advance of the wedding to allow for arrival and alterations. At a minimum, gowns take three to four months for completion and delivery, depending on the designer. Rush orders are available for an extra fee, but six to eight weeks is usually required. Thus, order completion time is slow. To discourage brides who change their minds, a 60% nonrefundable deposit is generally required at the time the order is placed. Thus, return on investment in sample size stock is slow. However, since most orders will be custom, the trade-off is that markdowns on bridal gowns will be almost limited to the markdowns on sample gowns that are sold at the end of the order season (generally January and July sales).

In the trade (wholesale and retail), markup on bridal gowns is often discussed in terms of markup based on cost, rather than markup based on retail. Earlier in this chapter, keystone markup was defined as a markup that doubles the cost of the merchandise. Thus, for keystone markup, a 2.0 factor is used since the retail price is twice the cost. Bridal owners often use a markup that is more than a 2.0 factor, such as a 2.5 factor or even greater (3.0). This means that the wholesale cost is multiplied by 2.5 or 3.0, etc., to determine the $ Retail. In effect this is the same as doubling (or tripling with a factor of 3.0) the wholesale cost and adding an additional amount to ensure profitability. It is important to remember that the retail markup percent can be calculated from this information. In the bridal business, an ideal $ Retail is based on an Initial Markup (retail) % of 60% or a 2.5 factor.

Other issues in the bridal business that impact profitability and markup are transportation and alterations. In the bridal business, these expenses are pricey, compared to expenses in other types of fashion retailers. The current cost for shipping for each dress is about $20. Simple alterations begin at $40 for hemming and a bust adjustment for strapless gowns, depending on the area of the country, and prices go from that point. As the owner of the business, you must decide whether you will build these expenses into markup. In some bridal stores, each of these is added as an extra expense to be paid by the bride above the quoted $ Retail. The pricing philosophy is that treating these separately keeps the $ Retail price competitive.

In reference to question #3, what do you think is the best method for a final $ Retail for the bridal gown? (a) Continue to mark the $ Retail at $625 and collect a separate charge of $20 for transportation and arrange a final fitting session with an alterations person in your store but let the bride pay that person's charge directly to him/her OR (b) Increase the $ Retail to include both a standard alteration charge and a standard delivery charge. Discuss the pros and cons of each.

سؤال

Operating a Successful Bridal Business

Wanda K. Cheek, Ph.D., Mississippi State University

You are the owner of a soon-to-open bridal store in a college town, with a population of 45,000. You began work on the business plan over a year ago, but are now within six months of the grand opening. It is time to make serious decisions concerning the financial aspects of merchandising a fashion-oriented business. Understanding markup and competitive retail pricing is an important part of the successful operation of this business.

Many merchandising and retailing students do not understand the unique structure of the retail bridal business and how it is different from most fashion businesses. The following background information is presented to clarify the differences.

First, to get into the retail bridal business, a bridal business owner carefully researches specialized bridal markets for dresses and accessories, such as the National Bridal Show at The Merchandise Mart in Chicago. There are two specialized bridal markets per year: (1) fall market in September or October for upcoming spring/summer weddings [merchandise arrives in stores in January and February] and (2) spring market in March or April for upcoming fall/winter weddings [merchandise arrives in stores in August and September]. Most bridal businesses make most purchases at fall market, since the upcoming spring and summer wedding season is by far the largest selling season of all. Business profits hinge on the success of sales during this season.

Another major difference in the bridal business, compared to other fashion retailing business structures, is that the owner only purchases sample dresses at the market. Therefore, inventory expenditures are greatly reduced, because a small store such as yours will only have about 80-90 dresses hanging in stock. Since all will be sample dresses that any bride may choose, it is important to specify sizes that can be pinned up or expanded as needed. Therefore, sizes 10, 12, 14, and 16 are popular sample sizes, with a few styles for larger sizes (up to 26). Small sample sizes such as 2 and 4 would most likely be the least useful. Therefore, sales persons need to be experienced and proficient in measuring and determining actual sizes to order.

Because the dresses will then need to be sewn by the manufacturer, bridal gown orders should ideally be placed at least six months in advance of the wedding to allow for arrival and alterations. At a minimum, gowns take three to four months for completion and delivery, depending on the designer. Rush orders are available for an extra fee, but six to eight weeks is usually required. Thus, order completion time is slow. To discourage brides who change their minds, a 60% nonrefundable deposit is generally required at the time the order is placed. Thus, return on investment in sample size stock is slow. However, since most orders will be custom, the trade-off is that markdowns on bridal gowns will be almost limited to the markdowns on sample gowns that are sold at the end of the order season (generally January and July sales).

In the trade (wholesale and retail), markup on bridal gowns is often discussed in terms of markup based on cost, rather than markup based on retail. Earlier in this chapter, keystone markup was defined as a markup that doubles the cost of the merchandise. Thus, for keystone markup, a 2.0 factor is used since the retail price is twice the cost. Bridal owners often use a markup that is more than a 2.0 factor, such as a 2.5 factor or even greater (3.0). This means that the wholesale cost is multiplied by 2.5 or 3.0, etc., to determine the $ Retail. In effect this is the same as doubling (or tripling with a factor of 3.0) the wholesale cost and adding an additional amount to ensure profitability. It is important to remember that the retail markup percent can be calculated from this information. In the bridal business, an ideal $ Retail is based on an Initial Markup (retail) % of 60% or a 2.5 factor.

Other issues in the bridal business that impact profitability and markup are transportation and alterations. In the bridal business, these expenses are pricey, compared to expenses in other types of fashion retailers. The current cost for shipping for each dress is about $20. Simple alterations begin at $40 for hemming and a bust adjustment for strapless gowns, depending on the area of the country, and prices go from that point. As the owner of the business, you must decide whether you will build these expenses into markup. In some bridal stores, each of these is added as an extra expense to be paid by the bride above the quoted $ Retail. The pricing philosophy is that treating these separately keeps the $ Retail price competitive.

Since markup percentages can be "controlled" in the bridal market through manufacturer's suggested prices and bridal is a seasonal market, what are some additional product categories (other than bridal gowns) that you could offer in your store to improve maintained markup and also offer the customer a full-service, one-stop package?

![Operating a Successful Bridal Business Wanda K. Cheek, Ph.D., Mississippi State University You are the owner of a soon-to-open bridal store in a college town, with a population of 45,000. You began work on the business plan over a year ago, but are now within six months of the grand opening. It is time to make serious decisions concerning the financial aspects of merchandising a fashion-oriented business. Understanding markup and competitive retail pricing is an important part of the successful operation of this business. Many merchandising and retailing students do not understand the unique structure of the retail bridal business and how it is different from most fashion businesses. The following background information is presented to clarify the differences. First, to get into the retail bridal business, a bridal business owner carefully researches specialized bridal markets for dresses and accessories, such as the National Bridal Show at The Merchandise Mart in Chicago. There are two specialized bridal markets per year: (1) fall market in September or October for upcoming spring/summer weddings [merchandise arrives in stores in January and February] and (2) spring market in March or April for upcoming fall/winter weddings [merchandise arrives in stores in August and September]. Most bridal businesses make most purchases at fall market, since the upcoming spring and summer wedding season is by far the largest selling season of all. Business profits hinge on the success of sales during this season. Another major difference in the bridal business, compared to other fashion retailing business structures, is that the owner only purchases sample dresses at the market. Therefore, inventory expenditures are greatly reduced, because a small store such as yours will only have about 80-90 dresses hanging in stock. Since all will be sample dresses that any bride may choose, it is important to specify sizes that can be pinned up or expanded as needed. Therefore, sizes 10, 12, 14, and 16 are popular sample sizes, with a few styles for larger sizes (up to 26). Small sample sizes such as 2 and 4 would most likely be the least useful. Therefore, sales persons need to be experienced and proficient in measuring and determining actual sizes to order. Because the dresses will then need to be sewn by the manufacturer, bridal gown orders should ideally be placed at least six months in advance of the wedding to allow for arrival and alterations. At a minimum, gowns take three to four months for completion and delivery, depending on the designer. Rush orders are available for an extra fee, but six to eight weeks is usually required. Thus, order completion time is slow. To discourage brides who change their minds, a 60% nonrefundable deposit is generally required at the time the order is placed. Thus, return on investment in sample size stock is slow. However, since most orders will be custom, the trade-off is that markdowns on bridal gowns will be almost limited to the markdowns on sample gowns that are sold at the end of the order season (generally January and July sales). In the trade (wholesale and retail), markup on bridal gowns is often discussed in terms of markup based on cost, rather than markup based on retail. Earlier in this chapter, keystone markup was defined as a markup that doubles the cost of the merchandise. Thus, for keystone markup, a 2.0 factor is used since the retail price is twice the cost. Bridal owners often use a markup that is more than a 2.0 factor, such as a 2.5 factor or even greater (3.0). This means that the wholesale cost is multiplied by 2.5 or 3.0, etc., to determine the $ Retail. In effect this is the same as doubling (or tripling with a factor of 3.0) the wholesale cost and adding an additional amount to ensure profitability. It is important to remember that the retail markup percent can be calculated from this information. In the bridal business, an ideal $ Retail is based on an Initial Markup (retail) % of 60% or a 2.5 factor. Other issues in the bridal business that impact profitability and markup are transportation and alterations. In the bridal business, these expenses are pricey, compared to expenses in other types of fashion retailers. The current cost for shipping for each dress is about $20. Simple alterations begin at $40 for hemming and a bust adjustment for strapless gowns, depending on the area of the country, and prices go from that point. As the owner of the business, you must decide whether you will build these expenses into markup. In some bridal stores, each of these is added as an extra expense to be paid by the bride above the quoted $ Retail. The pricing philosophy is that treating these separately keeps the $ Retail price competitive. Since markup percentages can be controlled in the bridal market through manufacturer's suggested prices and bridal is a seasonal market, what are some additional product categories (other than bridal gowns) that you could offer in your store to improve maintained markup and also offer the customer a full-service, one-stop package? <div style=padding-top: 35px>](https://d2lvgg3v3hfg70.cloudfront.net/SM3014/11eb66c1_87c4_1d22_953c_c5cd87462c78_SM3014_00.jpg)

Wanda K. Cheek, Ph.D., Mississippi State University

You are the owner of a soon-to-open bridal store in a college town, with a population of 45,000. You began work on the business plan over a year ago, but are now within six months of the grand opening. It is time to make serious decisions concerning the financial aspects of merchandising a fashion-oriented business. Understanding markup and competitive retail pricing is an important part of the successful operation of this business.

Many merchandising and retailing students do not understand the unique structure of the retail bridal business and how it is different from most fashion businesses. The following background information is presented to clarify the differences.

First, to get into the retail bridal business, a bridal business owner carefully researches specialized bridal markets for dresses and accessories, such as the National Bridal Show at The Merchandise Mart in Chicago. There are two specialized bridal markets per year: (1) fall market in September or October for upcoming spring/summer weddings [merchandise arrives in stores in January and February] and (2) spring market in March or April for upcoming fall/winter weddings [merchandise arrives in stores in August and September]. Most bridal businesses make most purchases at fall market, since the upcoming spring and summer wedding season is by far the largest selling season of all. Business profits hinge on the success of sales during this season.

Another major difference in the bridal business, compared to other fashion retailing business structures, is that the owner only purchases sample dresses at the market. Therefore, inventory expenditures are greatly reduced, because a small store such as yours will only have about 80-90 dresses hanging in stock. Since all will be sample dresses that any bride may choose, it is important to specify sizes that can be pinned up or expanded as needed. Therefore, sizes 10, 12, 14, and 16 are popular sample sizes, with a few styles for larger sizes (up to 26). Small sample sizes such as 2 and 4 would most likely be the least useful. Therefore, sales persons need to be experienced and proficient in measuring and determining actual sizes to order.

Because the dresses will then need to be sewn by the manufacturer, bridal gown orders should ideally be placed at least six months in advance of the wedding to allow for arrival and alterations. At a minimum, gowns take three to four months for completion and delivery, depending on the designer. Rush orders are available for an extra fee, but six to eight weeks is usually required. Thus, order completion time is slow. To discourage brides who change their minds, a 60% nonrefundable deposit is generally required at the time the order is placed. Thus, return on investment in sample size stock is slow. However, since most orders will be custom, the trade-off is that markdowns on bridal gowns will be almost limited to the markdowns on sample gowns that are sold at the end of the order season (generally January and July sales).

In the trade (wholesale and retail), markup on bridal gowns is often discussed in terms of markup based on cost, rather than markup based on retail. Earlier in this chapter, keystone markup was defined as a markup that doubles the cost of the merchandise. Thus, for keystone markup, a 2.0 factor is used since the retail price is twice the cost. Bridal owners often use a markup that is more than a 2.0 factor, such as a 2.5 factor or even greater (3.0). This means that the wholesale cost is multiplied by 2.5 or 3.0, etc., to determine the $ Retail. In effect this is the same as doubling (or tripling with a factor of 3.0) the wholesale cost and adding an additional amount to ensure profitability. It is important to remember that the retail markup percent can be calculated from this information. In the bridal business, an ideal $ Retail is based on an Initial Markup (retail) % of 60% or a 2.5 factor.

Other issues in the bridal business that impact profitability and markup are transportation and alterations. In the bridal business, these expenses are pricey, compared to expenses in other types of fashion retailers. The current cost for shipping for each dress is about $20. Simple alterations begin at $40 for hemming and a bust adjustment for strapless gowns, depending on the area of the country, and prices go from that point. As the owner of the business, you must decide whether you will build these expenses into markup. In some bridal stores, each of these is added as an extra expense to be paid by the bride above the quoted $ Retail. The pricing philosophy is that treating these separately keeps the $ Retail price competitive.

Since markup percentages can be "controlled" in the bridal market through manufacturer's suggested prices and bridal is a seasonal market, what are some additional product categories (other than bridal gowns) that you could offer in your store to improve maintained markup and also offer the customer a full-service, one-stop package?

سؤال

Operating a Successful Bridal Business

Wanda K. Cheek, Ph.D., Mississippi State University

You are the owner of a soon-to-open bridal store in a college town, with a population of 45,000. You began work on the business plan over a year ago, but are now within six months of the grand opening. It is time to make serious decisions concerning the financial aspects of merchandising a fashion-oriented business. Understanding markup and competitive retail pricing is an important part of the successful operation of this business.

Many merchandising and retailing students do not understand the unique structure of the retail bridal business and how it is different from most fashion businesses. The following background information is presented to clarify the differences.

First, to get into the retail bridal business, a bridal business owner carefully researches specialized bridal markets for dresses and accessories, such as the National Bridal Show at The Merchandise Mart in Chicago. There are two specialized bridal markets per year: (1) fall market in September or October for upcoming spring/summer weddings [merchandise arrives in stores in January and February] and (2) spring market in March or April for upcoming fall/winter weddings [merchandise arrives in stores in August and September]. Most bridal businesses make most purchases at fall market, since the upcoming spring and summer wedding season is by far the largest selling season of all. Business profits hinge on the success of sales during this season.

Another major difference in the bridal business, compared to other fashion retailing business structures, is that the owner only purchases sample dresses at the market. Therefore, inventory expenditures are greatly reduced, because a small store such as yours will only have about 80-90 dresses hanging in stock. Since all will be sample dresses that any bride may choose, it is important to specify sizes that can be pinned up or expanded as needed. Therefore, sizes 10, 12, 14, and 16 are popular sample sizes, with a few styles for larger sizes (up to 26). Small sample sizes such as 2 and 4 would most likely be the least useful. Therefore, sales persons need to be experienced and proficient in measuring and determining actual sizes to order.