Deck 17: Activity Resource Usage Model and Tactical Decision Making

ملء الشاشة (f)

سؤال

سؤال

Make-or-Buy, Traditional Analysis

Wehner Company is currently manufacturing Part ABS-43, producing 55,000 units annually. The part is used in the production of several products made by Wehner. The cost per unit for ABS-43 is as follows:

Of the total fixed overhead assigned to ABS-43, $15,400 is direct fixed overhead (the annual lease cost of machinery used to manufacture Part ABS-43), and the remainder is common fixed overhead. An outside supplier has offered to sell the part to Wehner for $58. There is no alternative use for the facilities currently used to produce the part. No significant non-unit-based overhead costs are incurred.

Required:

1. Should Wehner Company make or buy Part ABS-43?

2. What is the maximum amount per unit that Wehner would be willing to pay to an outside supplier?

Wehner Company is currently manufacturing Part ABS-43, producing 55,000 units annually. The part is used in the production of several products made by Wehner. The cost per unit for ABS-43 is as follows:

Of the total fixed overhead assigned to ABS-43, $15,400 is direct fixed overhead (the annual lease cost of machinery used to manufacture Part ABS-43), and the remainder is common fixed overhead. An outside supplier has offered to sell the part to Wehner for $58. There is no alternative use for the facilities currently used to produce the part. No significant non-unit-based overhead costs are incurred.

Required:

1. Should Wehner Company make or buy Part ABS-43?

2. What is the maximum amount per unit that Wehner would be willing to pay to an outside supplier?

سؤال

سؤال

Keep-Or-Drop Decision, Alternatives, Relevant Costs

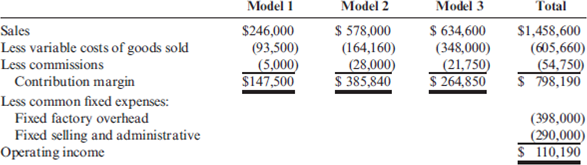

Reshier Company makes three types of rug shampooers. Model 1 is the basic model rented through hardware stores and supermarkets. Model 2 is a more advanced model with both dryand wet-vacuuming capabilities. Model 3 is the heavy-duty riding shampooer sold to hotels and convention centers. A segmented income statement is shown below.

While all models have positive contribution margins, Reshier Company is concerned because operating income is less than 10 percent of sales and is low for this type of company. The company's controller gathered additional information on fixed costs to see why they were so high. The following information on activities and drivers was gathered:

In addition, Model 1 requires the rental of specialized equipment costing $20,000 per year.

Required:

1. Reformulate the segmented income statement using the additional information on activities.

2. Using your answer to Requirement 1, assume that Reshier Company is considering dropping any model with a negative product margin. What are the alternatives? Which alternative is more cost effective and by how much? (Assume that any traceable fixed costs can be avoided.)

3. What if Reshier Company can only avoid 175 hours of engineering time and 5,000 hours of setup time that are attributable to Model 1? How does that affect the alternatives presented in Requirement 2? Which alternative is more cost effective and by how much?

Reshier Company makes three types of rug shampooers. Model 1 is the basic model rented through hardware stores and supermarkets. Model 2 is a more advanced model with both dryand wet-vacuuming capabilities. Model 3 is the heavy-duty riding shampooer sold to hotels and convention centers. A segmented income statement is shown below.

While all models have positive contribution margins, Reshier Company is concerned because operating income is less than 10 percent of sales and is low for this type of company. The company's controller gathered additional information on fixed costs to see why they were so high. The following information on activities and drivers was gathered:

In addition, Model 1 requires the rental of specialized equipment costing $20,000 per year.

Required:

1. Reformulate the segmented income statement using the additional information on activities.

2. Using your answer to Requirement 1, assume that Reshier Company is considering dropping any model with a negative product margin. What are the alternatives? Which alternative is more cost effective and by how much? (Assume that any traceable fixed costs can be avoided.)

3. What if Reshier Company can only avoid 175 hours of engineering time and 5,000 hours of setup time that are attributable to Model 1? How does that affect the alternatives presented in Requirement 2? Which alternative is more cost effective and by how much?

سؤال

سؤال

سؤال

سؤال

Make-or-Buy, Traditional and ABC Analysis

Brees, Inc., a manufacturer of golf carts, has just received an offer from a supplier to provide 2,600 units of a component used in its main product. The component is a track assembly that is currently produced internally. The supplier has offered to sell the track assembly for $66 per unit. Brees is currently using a traditional, unit-based costing system that assigns overhead to jobs on the basis of direct labor hours. The estimated traditional full cost of producing the track assembly is as follows:

Prior to making a decision, the company's CEO commissioned a special study to see whether there would be any decrease in the fixed overhead costs. The results of the study revealed the following:

3 setups-$1,160 each (The setups would be avoided, and total spending could be reduced by $1,160 per setup.)

One half-time inspector is needed. The company already uses part-time inspectors hired through a temporary employment agency. The yearly cost of the part-time inspectors for the track assembly operation is $12,300 and could be totally avoided if the part were purchased.

Engineering work: 470 hours, $45/hour. (Although the work decreases by 470 hours, the engineer assigned to the track assembly line also spends time on other products, and there would be no reduction in his salary.)

75 fewer material moves at $30 per move.

Required:

1. Ignore the special study, and determine whether the track assembly should be produced internally or purchased from the supplier.

2. Now, using the special study data, repeat the analysis.

3. Discuss the qualitative factors that would affect the decision, including strategic implications.

4. After reviewing the special study, the controller made the following remark: "This study ignores the additional activity demands that purchasing would cause. For example, although the demand for inspecting the part on the production floor decreases, we may need to inspect the incoming parts in the receiving area. Will we actually save any inspection costs?" Is the controller right?

Brees, Inc., a manufacturer of golf carts, has just received an offer from a supplier to provide 2,600 units of a component used in its main product. The component is a track assembly that is currently produced internally. The supplier has offered to sell the track assembly for $66 per unit. Brees is currently using a traditional, unit-based costing system that assigns overhead to jobs on the basis of direct labor hours. The estimated traditional full cost of producing the track assembly is as follows:

Prior to making a decision, the company's CEO commissioned a special study to see whether there would be any decrease in the fixed overhead costs. The results of the study revealed the following:

3 setups-$1,160 each (The setups would be avoided, and total spending could be reduced by $1,160 per setup.)

One half-time inspector is needed. The company already uses part-time inspectors hired through a temporary employment agency. The yearly cost of the part-time inspectors for the track assembly operation is $12,300 and could be totally avoided if the part were purchased.

Engineering work: 470 hours, $45/hour. (Although the work decreases by 470 hours, the engineer assigned to the track assembly line also spends time on other products, and there would be no reduction in his salary.)

75 fewer material moves at $30 per move.

Required:

1. Ignore the special study, and determine whether the track assembly should be produced internally or purchased from the supplier.

2. Now, using the special study data, repeat the analysis.

3. Discuss the qualitative factors that would affect the decision, including strategic implications.

4. After reviewing the special study, the controller made the following remark: "This study ignores the additional activity demands that purchasing would cause. For example, although the demand for inspecting the part on the production floor decreases, we may need to inspect the incoming parts in the receiving area. Will we actually save any inspection costs?" Is the controller right?

سؤال

سؤال

Special-Order Decision, Alternatives, Relevant Costs

Sequoia Paper Products, Inc., manufactures boxed stationery for sale to specialty shops. Currently, the company is operating at 90 percent of capacity. A chain of drugstores has offered to buy 30,000 boxes of Sequoia's blue-bordered thank-you notes as long as the box can be customized with the drugstore chain's logo. While the normal selling price is $6.00 per box, the chain has offered just $3.10 per box. Sequoia can accommodate the special order without affecting current sales. Unit cost information for a box of thank-you notes follows:

Fixed overhead is $420,000 per year and will not be affected by the special order. Normally, there is a commission of 5 percent of price; this will not be paid on the special order since the drugstore chain is dealing directly with the company. The special order will require additional fixed costs of $14,300 for the design and setup of the machinery to stamp the drugstore chain's logo on each box.

Required:

1. List the alternatives being considered. List the relevant benefits and costs for each alternative.

2. Which alternative is more cost effective and by how much?

3. What if Sequoia Paper Products was operating at capacity and accepting the special order would require rejecting an equivalent number of boxes sold to existing customers? Which alternative would be better?

Sequoia Paper Products, Inc., manufactures boxed stationery for sale to specialty shops. Currently, the company is operating at 90 percent of capacity. A chain of drugstores has offered to buy 30,000 boxes of Sequoia's blue-bordered thank-you notes as long as the box can be customized with the drugstore chain's logo. While the normal selling price is $6.00 per box, the chain has offered just $3.10 per box. Sequoia can accommodate the special order without affecting current sales. Unit cost information for a box of thank-you notes follows:

Fixed overhead is $420,000 per year and will not be affected by the special order. Normally, there is a commission of 5 percent of price; this will not be paid on the special order since the drugstore chain is dealing directly with the company. The special order will require additional fixed costs of $14,300 for the design and setup of the machinery to stamp the drugstore chain's logo on each box.

Required:

1. List the alternatives being considered. List the relevant benefits and costs for each alternative.

2. Which alternative is more cost effective and by how much?

3. What if Sequoia Paper Products was operating at capacity and accepting the special order would require rejecting an equivalent number of boxes sold to existing customers? Which alternative would be better?

سؤال

سؤال

سؤال

سؤال

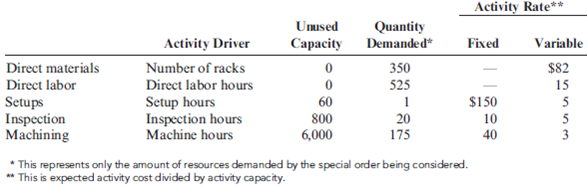

Resource Usage Model, Special Order

Ehrling, Inc., manufactures metal racks for hanging clothing in retail stores. Ehrling was approached by the CEO of Carly's Corner, a regional nonprofit food bank, with an offer to buy 350 heavy-duty metal racks for storing canned goods and dry food products. While racks normally sell for $245 each, Carly's Corner offered $75 per rack. The CEO explained that the number of families they served had grown significantly over the past two years, and that the charity needed additional storage for the donated food items. Since Ehrling is operating at 80 percent of capacity, and Ehrling employees have "adopted" Carly's Corner as their annual charity, the company wants to make the special order work. Ehrling's controller looked into the cost of the storage racks using the following information from the activity-based accounting system:

Expansion of activity capacity for setups, inspection, and machining must be done in steps. For setups, each step provides an additional 20 hours of setup activity and costs $3,000. For inspection, activity capacity is expanded by 2,000 hours per year, and the cost is $20,000 per year (the salary for an additional inspector). Machine capacity can be leased for a year at a rate of $40 per machine hour. Machine capacity must be acquired, however, in steps of 1,500 machine hours.

Required:

1. Compute the change in income for Ehrling, Inc., if the order is accepted.

2. Does the order require any change in capacity for setups, packing, or machining?

3. Suppose that the packing activity can be eliminated for this order since the customer is in town and does not need to have the racks boxed and shipped. Because of this, direct materials can be reduced by $13 per unit, and direct labor can be reduced by 0.5 hour per unit. How is the analysis affected?

4. Ehrling can find no other cost-saving measures for this special order. Why might the company decide to accept it even if it shows a loss?

Ehrling, Inc., manufactures metal racks for hanging clothing in retail stores. Ehrling was approached by the CEO of Carly's Corner, a regional nonprofit food bank, with an offer to buy 350 heavy-duty metal racks for storing canned goods and dry food products. While racks normally sell for $245 each, Carly's Corner offered $75 per rack. The CEO explained that the number of families they served had grown significantly over the past two years, and that the charity needed additional storage for the donated food items. Since Ehrling is operating at 80 percent of capacity, and Ehrling employees have "adopted" Carly's Corner as their annual charity, the company wants to make the special order work. Ehrling's controller looked into the cost of the storage racks using the following information from the activity-based accounting system:

Expansion of activity capacity for setups, inspection, and machining must be done in steps. For setups, each step provides an additional 20 hours of setup activity and costs $3,000. For inspection, activity capacity is expanded by 2,000 hours per year, and the cost is $20,000 per year (the salary for an additional inspector). Machine capacity can be leased for a year at a rate of $40 per machine hour. Machine capacity must be acquired, however, in steps of 1,500 machine hours.

Required:

1. Compute the change in income for Ehrling, Inc., if the order is accepted.

2. Does the order require any change in capacity for setups, packing, or machining?

3. Suppose that the packing activity can be eliminated for this order since the customer is in town and does not need to have the racks boxed and shipped. Because of this, direct materials can be reduced by $13 per unit, and direct labor can be reduced by 0.5 hour per unit. How is the analysis affected?

4. Ehrling can find no other cost-saving measures for this special order. Why might the company decide to accept it even if it shows a loss?

سؤال

سؤال

سؤال

سؤال

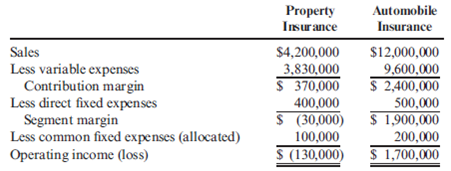

Keep-or-Drop for Service Firm, Complementary Effects, Traditional Analysis

Devern Assurance Company provides both property and automobile insurance. The projected income statements for the two products are as follows:

The president of the company is considering dropping the property insurance. However, some policyholders prefer having their property and automobile insurance with the same company, so if property insurance is dropped, sales of automobile insurance will drop by 12 percent. No significant non-unit-level activity costs are incurred.

Required:

1. If Devern Assurance Company drops property insurance, by how much will income increase or decrease? Provide supporting computations.

2. Assume that dropping all advertising for the property insurance line and increasing the corporate advertising budget by $450,000 will increase sales of property insurance by 10 percent and automobile insurance by 8 percent. Prepare a segmented income statement that reflects the effect of increased advertising. Should advertising be increased?

Devern Assurance Company provides both property and automobile insurance. The projected income statements for the two products are as follows:

The president of the company is considering dropping the property insurance. However, some policyholders prefer having their property and automobile insurance with the same company, so if property insurance is dropped, sales of automobile insurance will drop by 12 percent. No significant non-unit-level activity costs are incurred.

Required:

1. If Devern Assurance Company drops property insurance, by how much will income increase or decrease? Provide supporting computations.

2. Assume that dropping all advertising for the property insurance line and increasing the corporate advertising budget by $450,000 will increase sales of property insurance by 10 percent and automobile insurance by 8 percent. Prepare a segmented income statement that reflects the effect of increased advertising. Should advertising be increased?

سؤال

سؤال

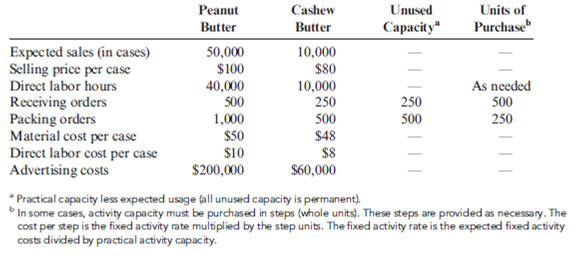

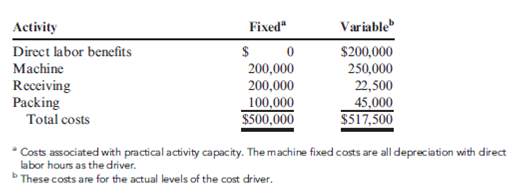

Keep-or-Drop: Traditional Versus Activity-Based Analysis

Nutterco, Inc., produces two types of nut butter: peanut butter and cashew butter. Of the two, peanut butter is the more popular. Cashew butter is a specialty line using smaller jars and fewer jars per case. Data concerning the two products follow:

Annual overhead costs are listed below. These costs are classified as fixed or variable with respect to the appropriate activity driver.

Required:

1. Prepare a traditional segmented income statement, using a unit-level overhead rate based on direct labor hours. Using this approach, determine whether the cashew butter product line should be kept or dropped.

2. Prepare an activity-based segmented income statement. Repeat the keep-or-drop analysis using an ABC approach.

Nutterco, Inc., produces two types of nut butter: peanut butter and cashew butter. Of the two, peanut butter is the more popular. Cashew butter is a specialty line using smaller jars and fewer jars per case. Data concerning the two products follow:

Annual overhead costs are listed below. These costs are classified as fixed or variable with respect to the appropriate activity driver.

Required:

1. Prepare a traditional segmented income statement, using a unit-level overhead rate based on direct labor hours. Using this approach, determine whether the cashew butter product line should be kept or dropped.

2. Prepare an activity-based segmented income statement. Repeat the keep-or-drop analysis using an ABC approach.

سؤال

سؤال

سؤال

سؤال

سؤال

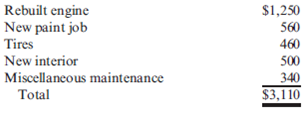

Determining Relevant Costs

Six months ago, Lee Anna Carver purchased a fire-engine red, used LeBaron convertible for $10,000. Lee Anna was looking forward to the feel of the sun on her shoulders and the wind whipping through her hair as she zipped along the highways of life. Unfortunately, the wind turned her hair into straw, and she didn't do much zipping along since the car spent so much of its time in the shop. So far, she has spent $1,200 on repairs, and she's afraid there is no end in sight. In fact, Lee Anna anticipates the following costs of restoration:

On a visit to a used car dealer, Lee Anna found a five-year-old Honda CR-V in excellent condition for $9,100-Lee Anna thinks she might really be more the sport-utility type anyway. Lee Anna checked the Blue Book values and found that she can sell the LeBaron for only $3,600. If she buys the CR-V, she will pay cash but would need to sell the LeBaron.

Required:

1. In trying to decide whether to restore the LeBaron or buy the CR-V, Lee Anna is distressed because she has already spent $11,200 on the LeBaron. The investment seems too much to give up. How would you react to her concern?

2. List all costs that are relevant to Lee Anna's decision. What advice would you give her?

Six months ago, Lee Anna Carver purchased a fire-engine red, used LeBaron convertible for $10,000. Lee Anna was looking forward to the feel of the sun on her shoulders and the wind whipping through her hair as she zipped along the highways of life. Unfortunately, the wind turned her hair into straw, and she didn't do much zipping along since the car spent so much of its time in the shop. So far, she has spent $1,200 on repairs, and she's afraid there is no end in sight. In fact, Lee Anna anticipates the following costs of restoration:

On a visit to a used car dealer, Lee Anna found a five-year-old Honda CR-V in excellent condition for $9,100-Lee Anna thinks she might really be more the sport-utility type anyway. Lee Anna checked the Blue Book values and found that she can sell the LeBaron for only $3,600. If she buys the CR-V, she will pay cash but would need to sell the LeBaron.

Required:

1. In trying to decide whether to restore the LeBaron or buy the CR-V, Lee Anna is distressed because she has already spent $11,200 on the LeBaron. The investment seems too much to give up. How would you react to her concern?

2. List all costs that are relevant to Lee Anna's decision. What advice would you give her?

سؤال

Sell or Process Further, Basic Analysis

Carleigh, Inc., is a pork processor. Its plants, located in the Midwest, produce several products from a common process: sirloin roasts, chops, spare ribs, and the residual. The roasts, chops, and spare ribs are packaged, branded, and sold to supermarkets. The residual consists of organ meats and leftover pieces that are sold to sausage and hot dog processors. The joint costs for a typical week are as follows:

The revenues from each product are as follows: sirloin roasts, $68,000; chops, $71,000; spare ribs, $33,000; and residual, $9,800.

Carleigh's management has learned that certain organ meats are a prized delicacy in Asia. They are considering separating those from the residual and selling them abroad for $52,000. This would bring the value of the residual down to $2,650. In addition, the organ meats would need to be packaged and then air freighted to Asia. Further processing cost per week is estimated to be $27,500 (the cost of renting additional packaging equipment, purchasing materials, and hiring additional direct labor). Transportation cost would be $12,100 per week. Finally, resource spending would need to be expanded for other activities as well (purchasing, receiving, and internal shipping). The increase in resource spending for these activities is estimated to be $3,120 per week.

Required:

1. What is the gross profit earned by the original mix of products for one week?

2. Should the company separate the organ meats for shipment overseas or continue to sell them at split-off? What is the effect of the decision on weekly gross profit?

Carleigh, Inc., is a pork processor. Its plants, located in the Midwest, produce several products from a common process: sirloin roasts, chops, spare ribs, and the residual. The roasts, chops, and spare ribs are packaged, branded, and sold to supermarkets. The residual consists of organ meats and leftover pieces that are sold to sausage and hot dog processors. The joint costs for a typical week are as follows:

The revenues from each product are as follows: sirloin roasts, $68,000; chops, $71,000; spare ribs, $33,000; and residual, $9,800.

Carleigh's management has learned that certain organ meats are a prized delicacy in Asia. They are considering separating those from the residual and selling them abroad for $52,000. This would bring the value of the residual down to $2,650. In addition, the organ meats would need to be packaged and then air freighted to Asia. Further processing cost per week is estimated to be $27,500 (the cost of renting additional packaging equipment, purchasing materials, and hiring additional direct labor). Transportation cost would be $12,100 per week. Finally, resource spending would need to be expanded for other activities as well (purchasing, receiving, and internal shipping). The increase in resource spending for these activities is estimated to be $3,120 per week.

Required:

1. What is the gross profit earned by the original mix of products for one week?

2. Should the company separate the organ meats for shipment overseas or continue to sell them at split-off? What is the effect of the decision on weekly gross profit?

سؤال

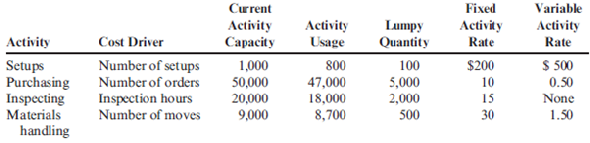

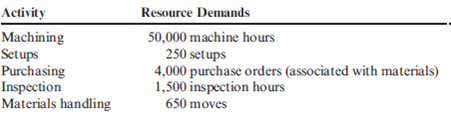

Activity-Based Resource Usage Model, Make-or-Buy

Brandy Dees recently bought Nievo Enterprises, a company that manufactures ice skates. Brandy decided to assume management responsibilities for the company and appointed herself president shortly after the purchase was completed. When she bought the company, Brandy's investigation revealed that with the exception of the blades, all parts of the skates are produced internally. The investigation also revealed that Nievo once produced the blades internally and still owned the equipment. The equipment was in good condition and was stored in a local warehouse. Nievo's former owner had decided three years earlier to purchase the blades from external suppliers.

Brandy Dees is seriously considering making the blades instead of buying them from external suppliers. The blades are purchased in sets of two and cost $8 per set. Currently, 100,000 sets of blades are purchased annually.

Skates are produced in batches, according to shoe size. Production equipment must be reconfigured for each batch. The blades could be produced using an available area within the plant. Prime costs will average $5.00 per set. There is enough equipment to set up three lines of production, each capable of producing 80,000 sets of blades. A supervisor would need to be hired for each line. Each supervisor would be paid a salary of $40,000. Additionally, it would cost $1.50 per machine hour for power, oil, and other operating expenses. Since three types of blades would be produced, additional demands would be made on the setup activity. Other overhead activities affected include purchasing, inspection, and materials handling. The company's ABC system provides the following information about the current status of the overhead activities that would be affected. (The lumpy quantity indicates how much capacity must be purchased should any expansion of activity supply be needed-the units of purchase. The purchase cost per unit is the fixed activity rate. The variable rate is the cost per unit of resources acquired as needed for each activity.)

The demands that the production of blades places on the overhead activities are as follows:

If the blades are made, the purchase of the blades from outside suppliers will cease. Therefore, purchase orders will decrease by 6,500 (the number associated with their purchase). Similarly, the moves for the handling of incoming blades will decrease by 400. Any unused activity capacity is viewed as permanent.

Required:

1. Should Nievo make or buy the blades?

2. Explain how the ABC resource usage model helped in the analysis. Also, comment on how a conventional approach would have differed.

Brandy Dees recently bought Nievo Enterprises, a company that manufactures ice skates. Brandy decided to assume management responsibilities for the company and appointed herself president shortly after the purchase was completed. When she bought the company, Brandy's investigation revealed that with the exception of the blades, all parts of the skates are produced internally. The investigation also revealed that Nievo once produced the blades internally and still owned the equipment. The equipment was in good condition and was stored in a local warehouse. Nievo's former owner had decided three years earlier to purchase the blades from external suppliers.

Brandy Dees is seriously considering making the blades instead of buying them from external suppliers. The blades are purchased in sets of two and cost $8 per set. Currently, 100,000 sets of blades are purchased annually.

Skates are produced in batches, according to shoe size. Production equipment must be reconfigured for each batch. The blades could be produced using an available area within the plant. Prime costs will average $5.00 per set. There is enough equipment to set up three lines of production, each capable of producing 80,000 sets of blades. A supervisor would need to be hired for each line. Each supervisor would be paid a salary of $40,000. Additionally, it would cost $1.50 per machine hour for power, oil, and other operating expenses. Since three types of blades would be produced, additional demands would be made on the setup activity. Other overhead activities affected include purchasing, inspection, and materials handling. The company's ABC system provides the following information about the current status of the overhead activities that would be affected. (The lumpy quantity indicates how much capacity must be purchased should any expansion of activity supply be needed-the units of purchase. The purchase cost per unit is the fixed activity rate. The variable rate is the cost per unit of resources acquired as needed for each activity.)

The demands that the production of blades places on the overhead activities are as follows:

If the blades are made, the purchase of the blades from outside suppliers will cease. Therefore, purchase orders will decrease by 6,500 (the number associated with their purchase). Similarly, the moves for the handling of incoming blades will decrease by 400. Any unused activity capacity is viewed as permanent.

Required:

1. Should Nievo make or buy the blades?

2. Explain how the ABC resource usage model helped in the analysis. Also, comment on how a conventional approach would have differed.

سؤال

سؤال

سؤال

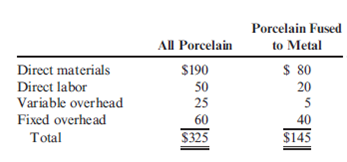

Make-or-Buy, Traditional Analysis, Qualitative Considerations

Apollonia Dental Services is part of an HMO that operates in a large metropolitan area. Currently, Apollonia has its own dental laboratory to produce two varieties of porcelain crowns-all porcelain and porcelain fused to metal. The unit costs to produce the crowns are as follows:

Fixed overhead is detailed as follows:

Overhead is applied on the basis of direct labor hours. The rates above were computed using 8,000 direct labor hours. No significant non-unit-level overhead costs are incurred.

A local dental laboratory has offered to supply Apollonia all the crowns it needs. Its price is $265 for all-porcelain crowns and $145 for porcelain-fused-to-metal crowns; however, the offer is conditional on supplying both types of crowns-it will not supply just one type for the price indicated. If the offer is accepted, the equipment used by Apollonia's laboratory would be scrapped (it is old and has no market value), and the lab facility would be closed. Apollonia uses 2,500 all-porcelain crowns and 1,000 porcelain-fused-to-metal crowns per year.

Required:

1. Should Apollonia continue to make its own crowns, or should they be purchased from the external supplier? What is the dollar effect of purchasing?

2. What qualitative factors should Apollonia consider in making this decision?

3. Suppose that the lab facility is owned rather than rented and that the $22,000 is depreciation rather than rent. What effect does this have on the analysis in Requirement 1?

4. Refer to the original data. Assume that the volume of crowns is 5,000 all porcelain and 2,000 porcelain fused to metal. Should Apollonia make or buy the crowns? Explain the outcome.

Apollonia Dental Services is part of an HMO that operates in a large metropolitan area. Currently, Apollonia has its own dental laboratory to produce two varieties of porcelain crowns-all porcelain and porcelain fused to metal. The unit costs to produce the crowns are as follows:

Fixed overhead is detailed as follows:

Overhead is applied on the basis of direct labor hours. The rates above were computed using 8,000 direct labor hours. No significant non-unit-level overhead costs are incurred.

A local dental laboratory has offered to supply Apollonia all the crowns it needs. Its price is $265 for all-porcelain crowns and $145 for porcelain-fused-to-metal crowns; however, the offer is conditional on supplying both types of crowns-it will not supply just one type for the price indicated. If the offer is accepted, the equipment used by Apollonia's laboratory would be scrapped (it is old and has no market value), and the lab facility would be closed. Apollonia uses 2,500 all-porcelain crowns and 1,000 porcelain-fused-to-metal crowns per year.

Required:

1. Should Apollonia continue to make its own crowns, or should they be purchased from the external supplier? What is the dollar effect of purchasing?

2. What qualitative factors should Apollonia consider in making this decision?

3. Suppose that the lab facility is owned rather than rented and that the $22,000 is depreciation rather than rent. What effect does this have on the analysis in Requirement 1?

4. Refer to the original data. Assume that the volume of crowns is 5,000 all porcelain and 2,000 porcelain fused to metal. Should Apollonia make or buy the crowns? Explain the outcome.

سؤال

سؤال

سؤال

Sell or Process Further

Pharmaco Corporation buys three chemicals that are processed to produce two popular ingredients for liquid pain relievers. The three chemicals are in liquid form. The purchased chemicals are blended for two to three hours and then heated for 15 minutes. The results of the process are two separate ingredients, PR1 and PR2. For every 4,300 gallons of chemicals used, 2,000 gallons of each pain reliever are produced. The pain relievers are sold to companies that process them into their final form. The selling prices are $34 per gallon for PR1 and $45 per gallon for PR2. The costs to produce one batch (containing 2,000 gallons of each chemical) are as follows:

The pain relievers are bottled in five-gallon plastic containers and shipped. The cost of each container is $2.10. The costs of shipping are $0.50 per container.

Pharmaco Corporation could process PR1 further by mixing it with inert powders and flavoring to form tablets. The tablets can be sold directly to retail drug stores as a generic brand. If this route is taken, the revenue received per case of tablets would be $13.50, with eight cases produced by every gallon of PR1. The costs of processing into tablets total $11.00 per gallon of PR1. Packaging costs $5.16 per case. Shipping costs are $1.68 per case.

Required:

1. Should Pharmaco sell PR1 at split-off, or should PR1 be processed and sold as tablets?

2. If Pharmaco normally sells 26,000 gallons of PR1 per year, what will be the difference in profits if PR1 is processed further?

Pharmaco Corporation buys three chemicals that are processed to produce two popular ingredients for liquid pain relievers. The three chemicals are in liquid form. The purchased chemicals are blended for two to three hours and then heated for 15 minutes. The results of the process are two separate ingredients, PR1 and PR2. For every 4,300 gallons of chemicals used, 2,000 gallons of each pain reliever are produced. The pain relievers are sold to companies that process them into their final form. The selling prices are $34 per gallon for PR1 and $45 per gallon for PR2. The costs to produce one batch (containing 2,000 gallons of each chemical) are as follows:

The pain relievers are bottled in five-gallon plastic containers and shipped. The cost of each container is $2.10. The costs of shipping are $0.50 per container.

Pharmaco Corporation could process PR1 further by mixing it with inert powders and flavoring to form tablets. The tablets can be sold directly to retail drug stores as a generic brand. If this route is taken, the revenue received per case of tablets would be $13.50, with eight cases produced by every gallon of PR1. The costs of processing into tablets total $11.00 per gallon of PR1. Packaging costs $5.16 per case. Shipping costs are $1.68 per case.

Required:

1. Should Pharmaco sell PR1 at split-off, or should PR1 be processed and sold as tablets?

2. If Pharmaco normally sells 26,000 gallons of PR1 per year, what will be the difference in profits if PR1 is processed further?

سؤال

سؤال

سؤال

Plant Shutdown or Continue Operations, Qualitative Considerations, Traditional Analysis

KarlAuto Corporation manufactures automobiles, vans, and trucks. Among the various Karl- Auto plants around the United States is the Bloomington plant, where vinyl covers and upholstery fabric are sewn. These are used to cover interior seating and other surfaces of KarlAuto products.

Pam Teegin is the plant manager for the Bloomington cover plant-the first KarlAuto plant in the region. As other area plants were opened, Teegin, in recognition of her management ability, was given the responsibility to manage them. Teegin functions as a regional manager, although the budget for her and her staff is charged to the Bloomington plant.

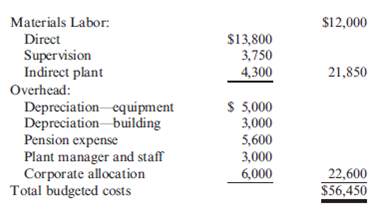

Teegin has just received a report indicating that KarlAuto could purchase the entire annual output of the Bloomington cover plant from outside suppliers for $32 million. Teegin was astonished at the low outside price, because the budget for the Bloomington plant's operating costs was set at $56.45 million. Teegin believes that the Bloomington plant will have to close down operations in order to realize the $24.45 million in annual cost savings.

The budget (in thousands) for the Bloomington plant's operating costs for the coming year follows:

Additional facts regarding the plant's operations are as follows:

Due to the Bloomington plant's commitment to use high-quality fabrics in all of its products, the Purchasing Department was instructed to place blanket orders with major suppliers to ensure the receipt of sufficient materials for the coming year. If these orders are canceled as a consequence of the plant closing, termination charges would amount to 18 percent of the cost of direct materials.

Approximately 600 plant employees will lose their jobs if the plant is closed. This includes all direct laborers and supervisors as well as the plumbers, electricians, and other skilled workers classified as indirect plant workers. Some would be able to find new jobs, but many others would have difficulty. All employees would have difficulty matching the Bloomington plant's base pay of $29.40 per hour, the highest in the area. A clause in the Bloomington plant's contract with the union may help some employees; the company must provide employment assistance to its former employees for 12 months after a plant closing. The estimated cost to administer this service would be $1 million for the year.

Some employees would probably elect early retirement because the company has an excellent pension plan. In fact, $4.6 million of next year's pension expense would continue whether or not the plant is open.

Teegin and her staff would not be affected by the closing of the Bloomington plant. They would still be responsible for administering three other area plants.

Equipment depreciation for the plant is considered to be a variable cost and the units-of-pro- duction method is used to depreciate equipment; the Bloomington plant is the only KarlAuto plant to use this depreciation method. However, it uses the customary straight-line method to depreciate its building.

Required:

1. Prepare a quantitative analysis to help in deciding whether or not to close the Bloomington plant. Explain how you treated the nonrecurring relevant costs.

2. Consider the analysis in Requirement 1, and add to it the qualitative factors that you believe are important to the decision. What is your decision? Would you close the plant? Explain.

(CMA adapted)

KarlAuto Corporation manufactures automobiles, vans, and trucks. Among the various Karl- Auto plants around the United States is the Bloomington plant, where vinyl covers and upholstery fabric are sewn. These are used to cover interior seating and other surfaces of KarlAuto products.

Pam Teegin is the plant manager for the Bloomington cover plant-the first KarlAuto plant in the region. As other area plants were opened, Teegin, in recognition of her management ability, was given the responsibility to manage them. Teegin functions as a regional manager, although the budget for her and her staff is charged to the Bloomington plant.

Teegin has just received a report indicating that KarlAuto could purchase the entire annual output of the Bloomington cover plant from outside suppliers for $32 million. Teegin was astonished at the low outside price, because the budget for the Bloomington plant's operating costs was set at $56.45 million. Teegin believes that the Bloomington plant will have to close down operations in order to realize the $24.45 million in annual cost savings.

The budget (in thousands) for the Bloomington plant's operating costs for the coming year follows:

Additional facts regarding the plant's operations are as follows:

Due to the Bloomington plant's commitment to use high-quality fabrics in all of its products, the Purchasing Department was instructed to place blanket orders with major suppliers to ensure the receipt of sufficient materials for the coming year. If these orders are canceled as a consequence of the plant closing, termination charges would amount to 18 percent of the cost of direct materials.

Approximately 600 plant employees will lose their jobs if the plant is closed. This includes all direct laborers and supervisors as well as the plumbers, electricians, and other skilled workers classified as indirect plant workers. Some would be able to find new jobs, but many others would have difficulty. All employees would have difficulty matching the Bloomington plant's base pay of $29.40 per hour, the highest in the area. A clause in the Bloomington plant's contract with the union may help some employees; the company must provide employment assistance to its former employees for 12 months after a plant closing. The estimated cost to administer this service would be $1 million for the year.

Some employees would probably elect early retirement because the company has an excellent pension plan. In fact, $4.6 million of next year's pension expense would continue whether or not the plant is open.

Teegin and her staff would not be affected by the closing of the Bloomington plant. They would still be responsible for administering three other area plants.

Equipment depreciation for the plant is considered to be a variable cost and the units-of-pro- duction method is used to depreciate equipment; the Bloomington plant is the only KarlAuto plant to use this depreciation method. However, it uses the customary straight-line method to depreciate its building.

Required:

1. Prepare a quantitative analysis to help in deciding whether or not to close the Bloomington plant. Explain how you treated the nonrecurring relevant costs.

2. Consider the analysis in Requirement 1, and add to it the qualitative factors that you believe are important to the decision. What is your decision? Would you close the plant? Explain.

(CMA adapted)

سؤال

سؤال

سؤال

Make-or-Buy, Traditional Analysis

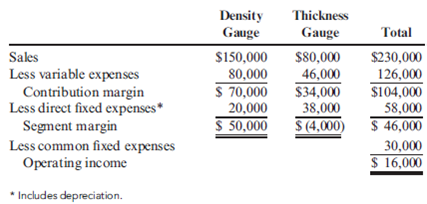

Morrill Company produces two different types of gauges: a density gauge and a thickness gauge. The segmented income statement for a typical quarter follows.

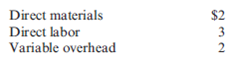

The density gauge uses a subassembly that is purchased from an external supplier for $25 per unit. Each quarter, 2,000 subassemblies are purchased. All units produced are sold, and there are no ending inventories of subassemblies. Morrill is considering making the subassembly rather than buying it. Unit-level variable manufacturing costs are as follows:

No significant non-unit-level costs are incurred.

Morrill is considering two alternatives to supply the productive capacity for the subassembly.

1. Lease the needed space and equipment at a cost of $27,000 per quarter for the space and $10,000 per quarter for a supervisor. There are no other fixed expenses.

2. Drop the thickness gauge. The equipment could be adapted with virtually no cost and the existing space utilized to produce the subassembly. The direct fixed expenses, including supervision, would be $38,000, $8,000 of which is depreciation on equipment. If the thickness gauge is dropped, sales of the density gauge will not be affected.

Required:

1. Should Morrill Company make or buy the subassembly? If it makes the subassembly, which alternative should be chosen? Explain and provide supporting computations.

2. Suppose that dropping the thickness gauge will decrease sales of the density gauge by 10 percent. What effect does this have on the decision?

3. Assume that dropping the thickness gauge decreases sales of the density gauge by 10 percent and that 2,800 subassemblies are required per quarter. As before, assume that there are no ending inventories of subassemblies and that all units produced are sold. Assume also that the per-unit sales price and variable costs are the same as in Requirement 1. Include the leasing alternative in your consideration. Now, what is the correct decision?

Morrill Company produces two different types of gauges: a density gauge and a thickness gauge. The segmented income statement for a typical quarter follows.

The density gauge uses a subassembly that is purchased from an external supplier for $25 per unit. Each quarter, 2,000 subassemblies are purchased. All units produced are sold, and there are no ending inventories of subassemblies. Morrill is considering making the subassembly rather than buying it. Unit-level variable manufacturing costs are as follows:

No significant non-unit-level costs are incurred.

Morrill is considering two alternatives to supply the productive capacity for the subassembly.

1. Lease the needed space and equipment at a cost of $27,000 per quarter for the space and $10,000 per quarter for a supervisor. There are no other fixed expenses.

2. Drop the thickness gauge. The equipment could be adapted with virtually no cost and the existing space utilized to produce the subassembly. The direct fixed expenses, including supervision, would be $38,000, $8,000 of which is depreciation on equipment. If the thickness gauge is dropped, sales of the density gauge will not be affected.

Required:

1. Should Morrill Company make or buy the subassembly? If it makes the subassembly, which alternative should be chosen? Explain and provide supporting computations.

2. Suppose that dropping the thickness gauge will decrease sales of the density gauge by 10 percent. What effect does this have on the decision?

3. Assume that dropping the thickness gauge decreases sales of the density gauge by 10 percent and that 2,800 subassemblies are required per quarter. As before, assume that there are no ending inventories of subassemblies and that all units produced are sold. Assume also that the per-unit sales price and variable costs are the same as in Requirement 1. Include the leasing alternative in your consideration. Now, what is the correct decision?

سؤال

سؤال

سؤال

سؤال

Special-Order Decision, Traditional Analysis, Qualitative Aspects

Feinan Sports, Inc., manufactures sporting equipment, including weight-lifting gloves. A national sporting goods chain recently submitted a special order for 4,600 pairs of weight-lifting gloves. Feinan Sports was not operating at capacity and could use the extra business. Unfortunately, the order's offering price of $12.80 per pair was below the cost to produce them. The controller was opposed to taking a loss on the deal. However, the personnel manager argued in favor of accepting the order even though a loss would be incurred; it would avoid the problem of layoffs and would help maintain the community image of the company. The full cost to produce a pair of weight-lifting gloves is presented below.

No variable selling or administrative expenses would be associated with the order. Non-unitlevel activity costs are a small percentage of total costs and are therefore not considered.

Required:

1. Assume that the company would accept the order only if it increased total profits. Should the company accept or reject the order? Provide supporting computations.

2. Suppose that Feinan Sports has negotiated with the potential customer, and has determined that it can substitute cheaper materials, reducing direct materials cost by $0.95 per unit. In addition, the company's engineers have found a way to reduce direct labor cost by $0.50 per unit. Should the company accept or reject the order? Provide supporting computations. 3. Consider the personnel manager's concerns. Discuss the merits of accepting the order even if it decreases total profits.

Feinan Sports, Inc., manufactures sporting equipment, including weight-lifting gloves. A national sporting goods chain recently submitted a special order for 4,600 pairs of weight-lifting gloves. Feinan Sports was not operating at capacity and could use the extra business. Unfortunately, the order's offering price of $12.80 per pair was below the cost to produce them. The controller was opposed to taking a loss on the deal. However, the personnel manager argued in favor of accepting the order even though a loss would be incurred; it would avoid the problem of layoffs and would help maintain the community image of the company. The full cost to produce a pair of weight-lifting gloves is presented below.

No variable selling or administrative expenses would be associated with the order. Non-unitlevel activity costs are a small percentage of total costs and are therefore not considered.

Required:

1. Assume that the company would accept the order only if it increased total profits. Should the company accept or reject the order? Provide supporting computations.

2. Suppose that Feinan Sports has negotiated with the potential customer, and has determined that it can substitute cheaper materials, reducing direct materials cost by $0.95 per unit. In addition, the company's engineers have found a way to reduce direct labor cost by $0.50 per unit. Should the company accept or reject the order? Provide supporting computations. 3. Consider the personnel manager's concerns. Discuss the merits of accepting the order even if it decreases total profits.

سؤال

Keep-or-Drop, Services, Qualitative Aspects

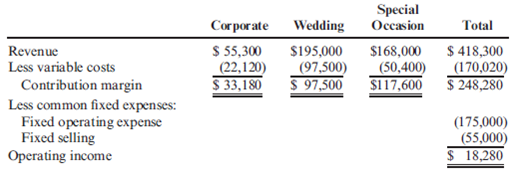

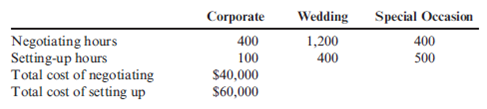

Jem Dawson owns Jem's Special Event Planning Service, a full-service event planner. Jem does much of the work herself and hires additional help as needed. She plans corporate events, weddings, and special occasion parties. Each of these is considered a separate line of business due to the specialized aspects of each type of event. Last year, Jem's accountant provided the following segmented income statement:

Jem was not pleased with last year's results; corporate events were down considerably from the previous few years. In addition, she thinks that dealing with the corporate party-throwers may be more work than it is worth. Two important aspects of event planning are negotiating with vendors (e.g., caterers, florists, bands and orchestras, and venues) on price and setting up for and being present at the event itself. The corporate negotiating seemed to consume extra time, and their restrictions on the price they would pay made the negotiations particularly difficult. She decided to gather some data on the negotiation and setting-up activities:

Required:

1. Prepare a segmented income statement using the activity data for negotiating and setting up. The total cost of these two activities can be subtracted from the fixed operating expense. The remaining fixed operating expense will be the common fixed operating expense. What does this income statement suggest about the relative profitability of the three product lines?

2. Jem believes that next year will be even worse. Her hunch is that corporate business will be down and that these clients will be especially intent on saving money by reducing the rate paid to Jem. She believes total corporate revenue may decrease by 25 percent overall, while the variable costs associated with those events will only decrease by 20 percent. On the other hand, Jem expects weddings to increase. Her reputation is growing and she thinks she can raise her revenues in this area by 15 percent even if the number of weddings does not increase. As a result, she expects variable costs of weddings to remain static. The special occasions (wedding anniversary parties, bar and bat mitzvahs, and so on) line is also expected to increase-with revenue and variable costs expected to increase by 10 percent. Jem does not know quite what to expect with respect to the negotiating and setting-up activities, so she thinks she'll just keep those constant for planning purposes. Prepare a segmented income statement using the activity data and these assumptions. What does this income statement suggest about dropping the corporate segment?

Jem Dawson owns Jem's Special Event Planning Service, a full-service event planner. Jem does much of the work herself and hires additional help as needed. She plans corporate events, weddings, and special occasion parties. Each of these is considered a separate line of business due to the specialized aspects of each type of event. Last year, Jem's accountant provided the following segmented income statement:

Jem was not pleased with last year's results; corporate events were down considerably from the previous few years. In addition, she thinks that dealing with the corporate party-throwers may be more work than it is worth. Two important aspects of event planning are negotiating with vendors (e.g., caterers, florists, bands and orchestras, and venues) on price and setting up for and being present at the event itself. The corporate negotiating seemed to consume extra time, and their restrictions on the price they would pay made the negotiations particularly difficult. She decided to gather some data on the negotiation and setting-up activities:

Required:

1. Prepare a segmented income statement using the activity data for negotiating and setting up. The total cost of these two activities can be subtracted from the fixed operating expense. The remaining fixed operating expense will be the common fixed operating expense. What does this income statement suggest about the relative profitability of the three product lines?

2. Jem believes that next year will be even worse. Her hunch is that corporate business will be down and that these clients will be especially intent on saving money by reducing the rate paid to Jem. She believes total corporate revenue may decrease by 25 percent overall, while the variable costs associated with those events will only decrease by 20 percent. On the other hand, Jem expects weddings to increase. Her reputation is growing and she thinks she can raise her revenues in this area by 15 percent even if the number of weddings does not increase. As a result, she expects variable costs of weddings to remain static. The special occasions (wedding anniversary parties, bar and bat mitzvahs, and so on) line is also expected to increase-with revenue and variable costs expected to increase by 10 percent. Jem does not know quite what to expect with respect to the negotiating and setting-up activities, so she thinks she'll just keep those constant for planning purposes. Prepare a segmented income statement using the activity data and these assumptions. What does this income statement suggest about dropping the corporate segment?

سؤال

Make-or-Buy Decision, Alternatives, Relevant Costs

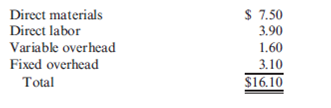

Each year, Basu Company produces 18,000 units of a component used in microwave ovens. An outside supplier has offered to supply the part for $1.38. The unit cost is:

Required:

1. What are the alternatives for Basu Company?

2. Assume that none of the fixed cost is avoidable. List the relevant cost(s) of internal production and of external purchase.

3. Which alternative is more cost effective and by how much?

4. What if $18,540 of fixed overhead is rental of equipment used only in production of the component that can be avoided if the component is purchased? Which alternative is more cost effective and by how much?

Each year, Basu Company produces 18,000 units of a component used in microwave ovens. An outside supplier has offered to supply the part for $1.38. The unit cost is:

Required:

1. What are the alternatives for Basu Company?

2. Assume that none of the fixed cost is avoidable. List the relevant cost(s) of internal production and of external purchase.

3. Which alternative is more cost effective and by how much?

4. What if $18,540 of fixed overhead is rental of equipment used only in production of the component that can be avoided if the component is purchased? Which alternative is more cost effective and by how much?

سؤال

سؤال

فتح الحزمة

قم بالتسجيل لفتح البطاقات في هذه المجموعة!

Unlock Deck

Unlock Deck

1/47

العب

ملء الشاشة (f)

Deck 17: Activity Resource Usage Model and Tactical Decision Making

1

What is tactical decision making?

Tactical decision making consists of choosing among the alternatives with an immediate or limited end in view.

Tactical decision may belongs to short run that an "accepting of special order which is less than the normal selling price" or may belongs to long run that "the company considering making component rather the buying it from outside".

However the tactical decision should support overall objective even if immediate objective is short run or long run. A sound tactical decision achieves not only the limited objective but also serve a larger purpose.

The tactical decision process would be generally as:

1. Recognize and define the problem

2. Identify alternatives as possible solutions to the problem, and eliminate any un feasible alternatives

3. Identify the cost and benefits which associated with each feasible alternative. Eliminate the costs and benefits that are not relevant to the decision.

4. Compare the relevant costs and benefits for each alternative.

5. Asses qualitative factors

6. Select the alternative with the greatest overall benefit.

Tactical decision may belongs to short run that an "accepting of special order which is less than the normal selling price" or may belongs to long run that "the company considering making component rather the buying it from outside".

However the tactical decision should support overall objective even if immediate objective is short run or long run. A sound tactical decision achieves not only the limited objective but also serve a larger purpose.

The tactical decision process would be generally as:

1. Recognize and define the problem

2. Identify alternatives as possible solutions to the problem, and eliminate any un feasible alternatives

3. Identify the cost and benefits which associated with each feasible alternative. Eliminate the costs and benefits that are not relevant to the decision.

4. Compare the relevant costs and benefits for each alternative.

5. Asses qualitative factors

6. Select the alternative with the greatest overall benefit.

2

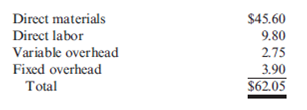

Make-or-Buy, Traditional Analysis

Wehner Company is currently manufacturing Part ABS-43, producing 55,000 units annually. The part is used in the production of several products made by Wehner. The cost per unit for ABS-43 is as follows:

Of the total fixed overhead assigned to ABS-43, $15,400 is direct fixed overhead (the annual lease cost of machinery used to manufacture Part ABS-43), and the remainder is common fixed overhead. An outside supplier has offered to sell the part to Wehner for $58. There is no alternative use for the facilities currently used to produce the part. No significant non-unit-based overhead costs are incurred.

Required:

1. Should Wehner Company make or buy Part ABS-43?

2. What is the maximum amount per unit that Wehner would be willing to pay to an outside supplier?

Wehner Company is currently manufacturing Part ABS-43, producing 55,000 units annually. The part is used in the production of several products made by Wehner. The cost per unit for ABS-43 is as follows:

Of the total fixed overhead assigned to ABS-43, $15,400 is direct fixed overhead (the annual lease cost of machinery used to manufacture Part ABS-43), and the remainder is common fixed overhead. An outside supplier has offered to sell the part to Wehner for $58. There is no alternative use for the facilities currently used to produce the part. No significant non-unit-based overhead costs are incurred.

Required:

1. Should Wehner Company make or buy Part ABS-43?

2. What is the maximum amount per unit that Wehner would be willing to pay to an outside supplier?

Generally when a company needs any item for use it has two options either he can make the same or he can buy the same. This decision is knows as make or buy decision. A company has to decide that which option will be useful for him and which will be not.

Sometime we take a decision and do work according to the same. But option of review is always available with us. So here we are reviewing this decision for Wehner Company who has the option to buy a part which he is currently manufacturing.

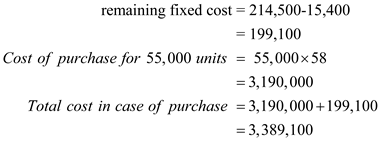

Part 1:

First of all we will calculate total production cost which is as follows:

$15,400 is the only fixed cost which will be saved as that is especially for production of this particular component.

$15,400 is the only fixed cost which will be saved as that is especially for production of this particular component.

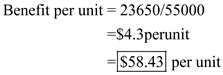

So it is $23,650 beneficial if we buy the product and stop manufacturing.

So it is $23,650 beneficial if we buy the product and stop manufacturing.

Part 2:

As it is $23,650 beneficial so we can pay this amount extra to buyer.

`

Sometime we take a decision and do work according to the same. But option of review is always available with us. So here we are reviewing this decision for Wehner Company who has the option to buy a part which he is currently manufacturing.

Part 1:

First of all we will calculate total production cost which is as follows:

$15,400 is the only fixed cost which will be saved as that is especially for production of this particular component. So it is $23,650 beneficial if we buy the product and stop manufacturing.Part 2:

As it is $23,650 beneficial so we can pay this amount extra to buyer.

`

3

(2010 CPA Exam) Egan Company owns land that could be developed in the future. Egan estimates it can sell the land for $1,200,000, net of all selling costs. If it is not sold, Egan will continue with its plans to develop the land. As Egan evaluates its options for development or sale of the property, what type of cost would the potential selling price represent in Egan's decision?

A) Sunk

B) Opportunity

C) Future

D) Variable

A) Sunk

B) Opportunity

C) Future

D) Variable

In business operations we have to take decisions which are good and profitable for company. For that we always compare costs and revenue from available options so that we can identify the best decision for us. Some costs are direct costs but some are not.

As Egan company is having an option to sale the land and another option to develop the land. In both cases company will earn profit. If company will opt any option then he will lose other option to earn money which is known as Opportunity Cost.

So correct answer is

- Opportunity Cost

- Opportunity Cost

As Egan company is having an option to sale the land and another option to develop the land. In both cases company will earn profit. If company will opt any option then he will lose other option to earn money which is known as Opportunity Cost.

So correct answer is

- Opportunity Cost 4

Keep-Or-Drop Decision, Alternatives, Relevant Costs

Reshier Company makes three types of rug shampooers. Model 1 is the basic model rented through hardware stores and supermarkets. Model 2 is a more advanced model with both dryand wet-vacuuming capabilities. Model 3 is the heavy-duty riding shampooer sold to hotels and convention centers. A segmented income statement is shown below.

While all models have positive contribution margins, Reshier Company is concerned because operating income is less than 10 percent of sales and is low for this type of company. The company's controller gathered additional information on fixed costs to see why they were so high. The following information on activities and drivers was gathered:

In addition, Model 1 requires the rental of specialized equipment costing $20,000 per year.

Required:

1. Reformulate the segmented income statement using the additional information on activities.

2. Using your answer to Requirement 1, assume that Reshier Company is considering dropping any model with a negative product margin. What are the alternatives? Which alternative is more cost effective and by how much? (Assume that any traceable fixed costs can be avoided.)

3. What if Reshier Company can only avoid 175 hours of engineering time and 5,000 hours of setup time that are attributable to Model 1? How does that affect the alternatives presented in Requirement 2? Which alternative is more cost effective and by how much?

Reshier Company makes three types of rug shampooers. Model 1 is the basic model rented through hardware stores and supermarkets. Model 2 is a more advanced model with both dryand wet-vacuuming capabilities. Model 3 is the heavy-duty riding shampooer sold to hotels and convention centers. A segmented income statement is shown below.

While all models have positive contribution margins, Reshier Company is concerned because operating income is less than 10 percent of sales and is low for this type of company. The company's controller gathered additional information on fixed costs to see why they were so high. The following information on activities and drivers was gathered:

In addition, Model 1 requires the rental of specialized equipment costing $20,000 per year.

Required:

1. Reformulate the segmented income statement using the additional information on activities.

2. Using your answer to Requirement 1, assume that Reshier Company is considering dropping any model with a negative product margin. What are the alternatives? Which alternative is more cost effective and by how much? (Assume that any traceable fixed costs can be avoided.)

3. What if Reshier Company can only avoid 175 hours of engineering time and 5,000 hours of setup time that are attributable to Model 1? How does that affect the alternatives presented in Requirement 2? Which alternative is more cost effective and by how much?

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 47 في هذه المجموعة.

فتح الحزمة

k this deck

5

When will flexible resources be relevant to a decision?

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 47 في هذه المجموعة.

فتح الحزمة

k this deck

6

(2010 CPA Exam) A company is offered a one-time special order for its product and has the capacity to take this order without losing current business. Variable costs per unit and fixed costs in total will be the same. The gross profit for the special order will be 10 percent, which is 15 percent less than the usual gross profit. What impact will this order have on total fixed costs and operating income?

A) Total fixed costs increase, and operating income increases.

B) Total fixed costs do not change, and operating income does not change.

C) Total fixed costs do not change, and operating income increases.

D) Total fixed costs increase, and operating income decreases.

A) Total fixed costs increase, and operating income increases.

B) Total fixed costs do not change, and operating income does not change.

C) Total fixed costs do not change, and operating income increases.

D) Total fixed costs increase, and operating income decreases.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 47 في هذه المجموعة.

فتح الحزمة

k this deck

7

"Tactical decisions are often small-scale decisions that serve a larger purpose." Explain what this means.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 47 في هذه المجموعة.

فتح الحزمة

k this deck

8

Make-or-Buy, Traditional and ABC Analysis

Brees, Inc., a manufacturer of golf carts, has just received an offer from a supplier to provide 2,600 units of a component used in its main product. The component is a track assembly that is currently produced internally. The supplier has offered to sell the track assembly for $66 per unit. Brees is currently using a traditional, unit-based costing system that assigns overhead to jobs on the basis of direct labor hours. The estimated traditional full cost of producing the track assembly is as follows:

Prior to making a decision, the company's CEO commissioned a special study to see whether there would be any decrease in the fixed overhead costs. The results of the study revealed the following:

3 setups-$1,160 each (The setups would be avoided, and total spending could be reduced by $1,160 per setup.)

One half-time inspector is needed. The company already uses part-time inspectors hired through a temporary employment agency. The yearly cost of the part-time inspectors for the track assembly operation is $12,300 and could be totally avoided if the part were purchased.

Engineering work: 470 hours, $45/hour. (Although the work decreases by 470 hours, the engineer assigned to the track assembly line also spends time on other products, and there would be no reduction in his salary.)

75 fewer material moves at $30 per move.

Required:

1. Ignore the special study, and determine whether the track assembly should be produced internally or purchased from the supplier.

2. Now, using the special study data, repeat the analysis.

3. Discuss the qualitative factors that would affect the decision, including strategic implications.

4. After reviewing the special study, the controller made the following remark: "This study ignores the additional activity demands that purchasing would cause. For example, although the demand for inspecting the part on the production floor decreases, we may need to inspect the incoming parts in the receiving area. Will we actually save any inspection costs?" Is the controller right?

Brees, Inc., a manufacturer of golf carts, has just received an offer from a supplier to provide 2,600 units of a component used in its main product. The component is a track assembly that is currently produced internally. The supplier has offered to sell the track assembly for $66 per unit. Brees is currently using a traditional, unit-based costing system that assigns overhead to jobs on the basis of direct labor hours. The estimated traditional full cost of producing the track assembly is as follows:

Prior to making a decision, the company's CEO commissioned a special study to see whether there would be any decrease in the fixed overhead costs. The results of the study revealed the following:

3 setups-$1,160 each (The setups would be avoided, and total spending could be reduced by $1,160 per setup.)

One half-time inspector is needed. The company already uses part-time inspectors hired through a temporary employment agency. The yearly cost of the part-time inspectors for the track assembly operation is $12,300 and could be totally avoided if the part were purchased.

Engineering work: 470 hours, $45/hour. (Although the work decreases by 470 hours, the engineer assigned to the track assembly line also spends time on other products, and there would be no reduction in his salary.)

75 fewer material moves at $30 per move.

Required:

1. Ignore the special study, and determine whether the track assembly should be produced internally or purchased from the supplier.

2. Now, using the special study data, repeat the analysis.

3. Discuss the qualitative factors that would affect the decision, including strategic implications.

4. After reviewing the special study, the controller made the following remark: "This study ignores the additional activity demands that purchasing would cause. For example, although the demand for inspecting the part on the production floor decreases, we may need to inspect the incoming parts in the receiving area. Will we actually save any inspection costs?" Is the controller right?

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 47 في هذه المجموعة.

فتح الحزمة

k this deck

9

(2011 CPA Exam) Jones Corp. had an opportunity to use its capacity to produce an extra 5,000 units with a contribution margin of $5 per unit, or to rent out the space for $10,000. What was the opportuity cost of using the capacity?

A) $35,000

B) $25,000

C) $15,000

D) $10,000

A) $35,000

B) $25,000

C) $15,000

D) $10,000

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 47 في هذه المجموعة.

فتح الحزمة

k this deck

10

Special-Order Decision, Alternatives, Relevant Costs

Sequoia Paper Products, Inc., manufactures boxed stationery for sale to specialty shops. Currently, the company is operating at 90 percent of capacity. A chain of drugstores has offered to buy 30,000 boxes of Sequoia's blue-bordered thank-you notes as long as the box can be customized with the drugstore chain's logo. While the normal selling price is $6.00 per box, the chain has offered just $3.10 per box. Sequoia can accommodate the special order without affecting current sales. Unit cost information for a box of thank-you notes follows:

Fixed overhead is $420,000 per year and will not be affected by the special order. Normally, there is a commission of 5 percent of price; this will not be paid on the special order since the drugstore chain is dealing directly with the company. The special order will require additional fixed costs of $14,300 for the design and setup of the machinery to stamp the drugstore chain's logo on each box.

Required:

1. List the alternatives being considered. List the relevant benefits and costs for each alternative.

2. Which alternative is more cost effective and by how much?

3. What if Sequoia Paper Products was operating at capacity and accepting the special order would require rejecting an equivalent number of boxes sold to existing customers? Which alternative would be better?

Sequoia Paper Products, Inc., manufactures boxed stationery for sale to specialty shops. Currently, the company is operating at 90 percent of capacity. A chain of drugstores has offered to buy 30,000 boxes of Sequoia's blue-bordered thank-you notes as long as the box can be customized with the drugstore chain's logo. While the normal selling price is $6.00 per box, the chain has offered just $3.10 per box. Sequoia can accommodate the special order without affecting current sales. Unit cost information for a box of thank-you notes follows:

Fixed overhead is $420,000 per year and will not be affected by the special order. Normally, there is a commission of 5 percent of price; this will not be paid on the special order since the drugstore chain is dealing directly with the company. The special order will require additional fixed costs of $14,300 for the design and setup of the machinery to stamp the drugstore chain's logo on each box.

Required:

1. List the alternatives being considered. List the relevant benefits and costs for each alternative.

2. Which alternative is more cost effective and by how much?

3. What if Sequoia Paper Products was operating at capacity and accepting the special order would require rejecting an equivalent number of boxes sold to existing customers? Which alternative would be better?

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 47 في هذه المجموعة.

فتح الحزمة

k this deck

11

When will the cost of committed resources be relevant to a decision?

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 47 في هذه المجموعة.

فتح الحزمة

k this deck

12

(2011 CPA Exam) The ABC Company is trying to decide between keeping an existing machine and replacing it with a new machine. The old machine was purchased just two years ago for $50,000 and had an expected life of 10 years. It now costs $1,000 a month for maintenance and repairs due to a mechanical problem. A new machine is being considered to replace it at a cost of $60,000. The new machine is more efficient and it will only cost $200 a month for maintenance and repairs. The new machine has an expected life of 10 years. In deciding to replace the old machine, which of the following factors, ignoring income taxes, should ABC not consider?

A) Any estimated salvage value on the old machine

B) The original cost of the old machine

C) The estimated useful life of the new machine

D) The lower maintenance cost on the new machine

A) Any estimated salvage value on the old machine

B) The original cost of the old machine

C) The estimated useful life of the new machine

D) The lower maintenance cost on the new machine

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 47 في هذه المجموعة.

فتح الحزمة

k this deck

13

What is tactical cost analysis? What steps in the tactical decision-making model correspond to tactical cost analysis?

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 47 في هذه المجموعة.

فتح الحزمة

k this deck

14

Resource Usage Model, Special Order