Deck 21: Variable Costing for Management Analysis

ملء الشاشة (f)

سؤال

سؤال

سؤال

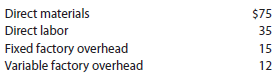

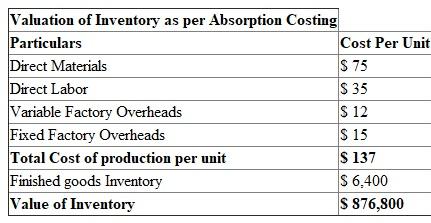

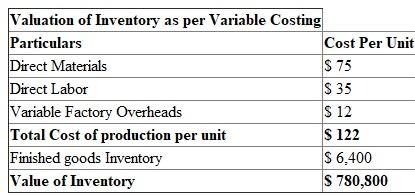

Inventory valuation under absorption costing and variable costing

At the end of the first year of operations, 6,400 units remained in the finished goods inventory. The unit manufacturing costs during the year were as follows:

Determine the cost of the finished goods inventory reported on the balance sheet under (a) the absorption costing concept and (b) the variable costing concept.

At the end of the first year of operations, 6,400 units remained in the finished goods inventory. The unit manufacturing costs during the year were as follows:

Determine the cost of the finished goods inventory reported on the balance sheet under (a) the absorption costing concept and (b) the variable costing concept.

سؤال

Variable costing

Light Company has the following information for January:

Determine (a) the manufacturing margin, (b) the contribution margin, and (c) income from operations for Light Company for the month of January.

Marley Company has the following information for March:

Determine (a) the manufacturing margin, (b) the contribution margin, and (c) income from operations for Marley Company for the month of March.

Light Company has the following information for January:

Determine (a) the manufacturing margin, (b) the contribution margin, and (c) income from operations for Light Company for the month of January.

Marley Company has the following information for March:

Determine (a) the manufacturing margin, (b) the contribution margin, and (c) income from operations for Marley Company for the month of March.

سؤال

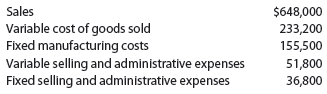

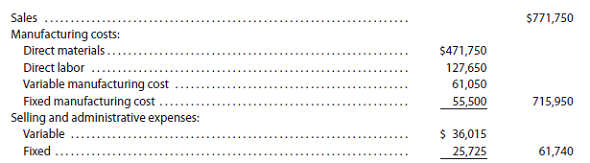

Absorption and variable costing income statements

During the first month of operations ended May 31016, Frost Point Fridge Company manufactured 40,000 mini refrigerators, of which 36,000 were sold. Operating data for the month are summarized as follows:

Instructions

1. Prepare an income statement based on the absorption costing concept.

2. Prepare an income statement based on the variable costing concept.

3. Explain the reason for the difference in the amount of income from operations reported in (1) and (2).

During the first month of operations ended May 31016, Frost Point Fridge Company manufactured 40,000 mini refrigerators, of which 36,000 were sold. Operating data for the month are summarized as follows:

Instructions

1. Prepare an income statement based on the absorption costing concept.

2. Prepare an income statement based on the variable costing concept.

3. Explain the reason for the difference in the amount of income from operations reported in (1) and (2).

سؤال

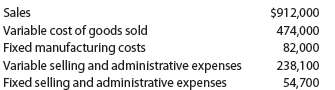

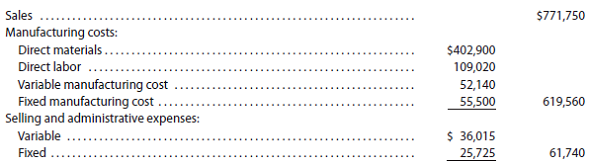

Absorption and variable costing income statements

During the first month of operations ended July 31, 2016, YoSan Inc. manufactured 2,400 flat panel televisions, of which 2,000 were sold. Operating data for the month are summarized as follows:

Instructions

1. Prepare an income statement based on the absorption costing concept.

2. Prepare an income statement based on the variable costing concept.

3. Explain the reason for the difference in the amount of income from operations reported in (1) and (2).

During the first month of operations ended July 31, 2016, YoSan Inc. manufactured 2,400 flat panel televisions, of which 2,000 were sold. Operating data for the month are summarized as follows:

Instructions

1. Prepare an income statement based on the absorption costing concept.

2. Prepare an income statement based on the variable costing concept.

3. Explain the reason for the difference in the amount of income from operations reported in (1) and (2).

سؤال

سؤال

سؤال

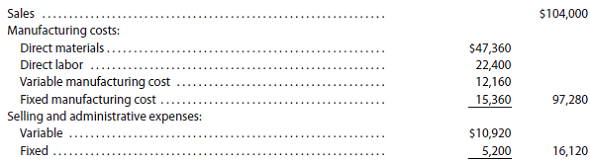

Income statements under absorption costing and variable costing

Frigid Motors Inc. assembles and sells snowmobile engines. The company began operations on July 1, 2016, and operated at 100% of capacity during the first month. The following data summarize the results for July:

a. Prepare an income statement according to the absorption costing concept.

b. Prepare an income statement according to the variable costing concept.

c. What is the reason for the difference in the amount of income from operations reported in (a) and (b)?

Frigid Motors Inc. assembles and sells snowmobile engines. The company began operations on July 1, 2016, and operated at 100% of capacity during the first month. The following data summarize the results for July:

a. Prepare an income statement according to the absorption costing concept.

b. Prepare an income statement according to the variable costing concept.

c. What is the reason for the difference in the amount of income from operations reported in (a) and (b)?

سؤال

سؤال

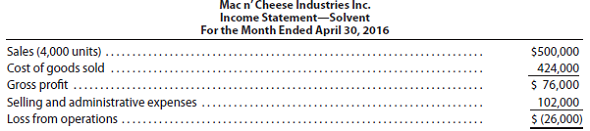

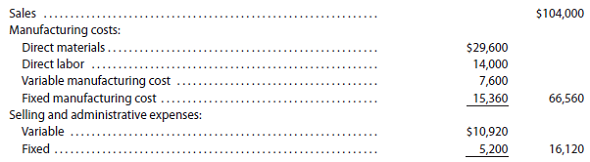

Income statements under absorption costing and variable costing

The demand for solvent, one of numerous products manufactured by Mac n' Cheese Industries Inc., has dropped sharply because of recent competition from a similar product. The company's chemists are currently completing tests of various new formulas, and it is anticipated that the manufacture of a superior product can be started on June 1, one month in the future. No changes will be needed in the present production facilities to manufacture the new product because only the mixture of the various materials will be changed.

The controller has been asked by the president of the company for advice on whether to continue production during May or to suspend the manufacture of solvent until June 1. The controller has assembled the following pertinent data:

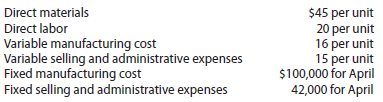

The production costs and selling and administrative expenses, based on production of 4,000 units in April, are as follows:

Sales for May are expected to drop about 20% below those of the preceding month. No significant changes are anticipated in the fixed costs or variable costs per unit. No extra costs will be incurred in discontinuing operations in the portion of the plant associated with solvent. The inventory of solvent at the beginning and end of May is expected to be inconsequential.

Instructions

1. Prepare an estimated income statement in absorption costing form for May for solvent, assuming that production continues during the month. Round amounts to two decimals.

2. Prepare an estimated income statement in variable costing form for May for solvent, assuming that production continues during the month. Round amounts to two decimals.

3. What would be the estimated loss in income from operations if the solvent production were temporarily suspended for May?

4. What advice should the controller give to management?

The demand for solvent, one of numerous products manufactured by Mac n' Cheese Industries Inc., has dropped sharply because of recent competition from a similar product. The company's chemists are currently completing tests of various new formulas, and it is anticipated that the manufacture of a superior product can be started on June 1, one month in the future. No changes will be needed in the present production facilities to manufacture the new product because only the mixture of the various materials will be changed.

The controller has been asked by the president of the company for advice on whether to continue production during May or to suspend the manufacture of solvent until June 1. The controller has assembled the following pertinent data:

The production costs and selling and administrative expenses, based on production of 4,000 units in April, are as follows:

Sales for May are expected to drop about 20% below those of the preceding month. No significant changes are anticipated in the fixed costs or variable costs per unit. No extra costs will be incurred in discontinuing operations in the portion of the plant associated with solvent. The inventory of solvent at the beginning and end of May is expected to be inconsequential.

Instructions

1. Prepare an estimated income statement in absorption costing form for May for solvent, assuming that production continues during the month. Round amounts to two decimals.

2. Prepare an estimated income statement in variable costing form for May for solvent, assuming that production continues during the month. Round amounts to two decimals.

3. What would be the estimated loss in income from operations if the solvent production were temporarily suspended for May?

4. What advice should the controller give to management?

سؤال

Income statements under absorption costing and variable costing

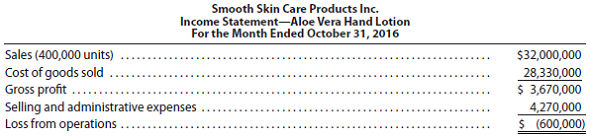

The demand for aloe vera hand lotion, one of numerous products manufactured by Smooth Skin Care Products Inc., has dropped sharply because of recent competition from a similar product. The company's chemists are currently completing tests of various new formulas, and it is anticipated that the manufacture of a superior product can be started on December 1, one month in the future. No changes will be needed in the present production facilities to manufacture the new product because only the mixture of the various materials will be changed.

The controller has been asked by the president of the company for advice on whether to continue production during November or to suspend the manufacture of aloe vera hand lotion until December 1. The controller has assembled the following pertinent data:

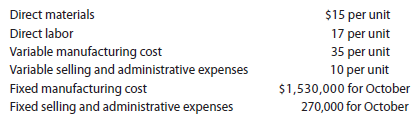

The production costs and selling and administrative expenses, based on production of 400,000 units in October, are as follows:

Sales for November are expected to drop about 20% below those of the preceding month. No significant changes are anticipated in the fixed costs or variable costs per unit. No extra costs will be incurred in discontinuing operations in the portion of the plant associated with aloe vera hand lotion. The inventory of aloe vera hand lotion at the beginning and end of November is expected to be inconsequential.

Instructions

1. Prepare an estimated income statement in absorption costing form for November for aloe vera hand lotion, assuming that production continues during the month.

2. Prepare an estimated income statement in variable costing form for November for aloe vera hand lotion, assuming that production continues during the month.

3. What would be the estimated loss in income from operations if the aloe vera hand lotion production were temporarily suspended for November?

4. What advice should the controller give to management?

The demand for aloe vera hand lotion, one of numerous products manufactured by Smooth Skin Care Products Inc., has dropped sharply because of recent competition from a similar product. The company's chemists are currently completing tests of various new formulas, and it is anticipated that the manufacture of a superior product can be started on December 1, one month in the future. No changes will be needed in the present production facilities to manufacture the new product because only the mixture of the various materials will be changed.

The controller has been asked by the president of the company for advice on whether to continue production during November or to suspend the manufacture of aloe vera hand lotion until December 1. The controller has assembled the following pertinent data:

The production costs and selling and administrative expenses, based on production of 400,000 units in October, are as follows:

Sales for November are expected to drop about 20% below those of the preceding month. No significant changes are anticipated in the fixed costs or variable costs per unit. No extra costs will be incurred in discontinuing operations in the portion of the plant associated with aloe vera hand lotion. The inventory of aloe vera hand lotion at the beginning and end of November is expected to be inconsequential.

Instructions

1. Prepare an estimated income statement in absorption costing form for November for aloe vera hand lotion, assuming that production continues during the month.

2. Prepare an estimated income statement in variable costing form for November for aloe vera hand lotion, assuming that production continues during the month.

3. What would be the estimated loss in income from operations if the aloe vera hand lotion production were temporarily suspended for November?

4. What advice should the controller give to management?

سؤال

Segmented contribution margin analysis

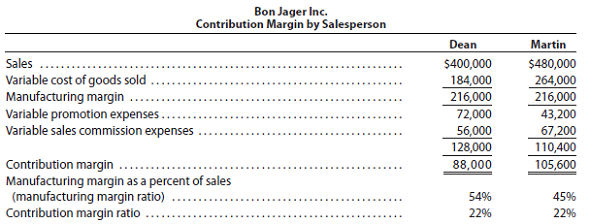

Bon Jager Inc. manufactures and sells devices used in cardiovascular surgery. The company has two salespersons, Dean and Martin.

A contribution margin by salesperson report was prepared as follows:

Interpret the report, and provide recommendations to the two salespersons for improving profitability.

Bon Jager Inc. manufactures and sells devices used in cardiovascular surgery. The company has two salespersons, Dean and Martin.

A contribution margin by salesperson report was prepared as follows:

Interpret the report, and provide recommendations to the two salespersons for improving profitability.

سؤال

سؤال

Income statements under absorption costing and variable costing

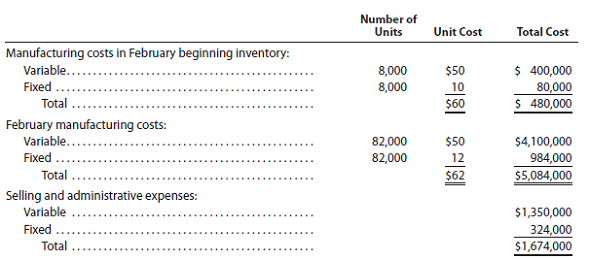

Bionic Cotton Inc. manufactures and sells high-quality sporting goods equipment under its highly recognizable Cool Cat logo. The company began operations on January 1, 2016, and operated at 100% of capacity (90,000 units) during the first month, creating an ending inventory of 8,000 units. During February, the company produced 82,000 garments during the month but sold 90,000 units at $100 per unit. The February manufacturing costs and selling and administrative expenses were as follows:

a. Prepare an income statement according to the absorption costing concept for February.

b. Prepare an income statement according to the variable costing concept for February.

c. What is the reason for the difference in the amount of income from operations reported in (a) and (b)?

Bionic Cotton Inc. manufactures and sells high-quality sporting goods equipment under its highly recognizable Cool Cat logo. The company began operations on January 1, 2016, and operated at 100% of capacity (90,000 units) during the first month, creating an ending inventory of 8,000 units. During February, the company produced 82,000 garments during the month but sold 90,000 units at $100 per unit. The February manufacturing costs and selling and administrative expenses were as follows:

a. Prepare an income statement according to the absorption costing concept for February.

b. Prepare an income statement according to the variable costing concept for February.

c. What is the reason for the difference in the amount of income from operations reported in (a) and (b)?

سؤال

سؤال

Absorption and variable costing income statements for two months and analysis

During the first month of operations ended March 31, 2016, Hip and Conscious Clothing Company produced 55,500 designer cowboy hats, of which 51,450 were sold. Operating data for the month are summarized as follows:

During April, Hip and Conscious Clothing produced 47,400 designer cowboy hats and sold 51,450 cowboy hats. Operating data for April are summarized as follows:

Instructions

1. Using the absorption costing concept, prepare income statements for (a) March and (b) April.

2. Using the variable costing concept, prepare income statements for (a) March and (b) April.

3. a. Explain the reason for the differences in the amount of income from operations in (1) and (2) for March.

?b. Explain the reason for the differences in the amount of income from operations in (1) and (2) for April.

4. Based on your answers to (1) and (2), did Hip and Conscious Clothing Company operate more profitably in March or in April? Explain.

During the first month of operations ended March 31, 2016, Hip and Conscious Clothing Company produced 55,500 designer cowboy hats, of which 51,450 were sold. Operating data for the month are summarized as follows:

During April, Hip and Conscious Clothing produced 47,400 designer cowboy hats and sold 51,450 cowboy hats. Operating data for April are summarized as follows:

Instructions

1. Using the absorption costing concept, prepare income statements for (a) March and (b) April.

2. Using the variable costing concept, prepare income statements for (a) March and (b) April.

3. a. Explain the reason for the differences in the amount of income from operations in (1) and (2) for March.

?b. Explain the reason for the differences in the amount of income from operations in (1) and (2) for April.

4. Based on your answers to (1) and (2), did Hip and Conscious Clothing Company operate more profitably in March or in April? Explain.

سؤال

Absorption and variable costing income statements for two months and analysis

During the first month of operations ended July 31, 2016, Head Gear Inc. manufactured 6,400 hats, of which 5,200 were sold. Operating data for the month are summarized as follows:

During August Head Gear Inc. manufactured 4,000 hats and sold 5,200 hats. Operating data for August are summarized as follows:

Instructions

1. Using the absorption costing concept, prepare income statements for (a) July and (b) August.

2. Using the variable costing concept, prepare income statements for (a) July and (b) August.

3. a. Explain the reason for the differences in the amount of income from operations in (1) and (2) for July.

b. Explain the reason for the differences in the amount of income from operations in (1) and (2) for August.

4. Based on your answers to (1) and (2), did Head Gear Inc. operate more profitably in July or in August? Explain.

During the first month of operations ended July 31, 2016, Head Gear Inc. manufactured 6,400 hats, of which 5,200 were sold. Operating data for the month are summarized as follows:

During August Head Gear Inc. manufactured 4,000 hats and sold 5,200 hats. Operating data for August are summarized as follows:

Instructions

1. Using the absorption costing concept, prepare income statements for (a) July and (b) August.

2. Using the variable costing concept, prepare income statements for (a) July and (b) August.

3. a. Explain the reason for the differences in the amount of income from operations in (1) and (2) for July.

b. Explain the reason for the differences in the amount of income from operations in (1) and (2) for August.

4. Based on your answers to (1) and (2), did Head Gear Inc. operate more profitably in July or in August? Explain.

سؤال

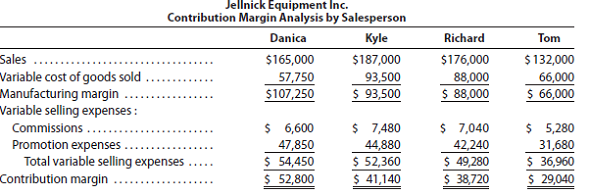

Margin analysis

Jellnick Equipment Inc. manufactures and sells kitchen cooking products throughout the state. The company employs four salespersons. The following contribution margin by salesperson analysis was prepared:

1. Calculate the manufacturing margin as a percent of sales and the contribution margin ratio for each salesperson.

2. Explain the results of the analysis.

Jellnick Equipment Inc. manufactures and sells kitchen cooking products throughout the state. The company employs four salespersons. The following contribution margin by salesperson analysis was prepared:

1. Calculate the manufacturing margin as a percent of sales and the contribution margin ratio for each salesperson.

2. Explain the results of the analysis.

سؤال

سؤال

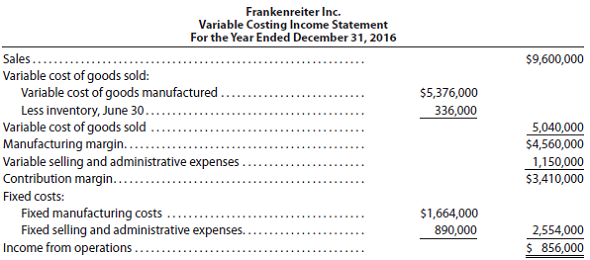

Cost of goods manufactured, using variable costing and absorption costing

On December 31, the end of the first year of operations, Frankenreiter Inc. manufactured 25,600 units and sold 24,000 units. The following income statement was prepared, based on the variable costing concept:

Determine the unit cost of goods manufactured, based on (a) the variable costing concept and (b) the absorption costing concept.

On December 31, the end of the first year of operations, Frankenreiter Inc. manufactured 25,600 units and sold 24,000 units. The following income statement was prepared, based on the variable costing concept:

Determine the unit cost of goods manufactured, based on (a) the variable costing concept and (b) the absorption costing concept.

سؤال

سؤال

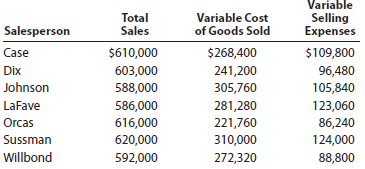

Salespersons' report and analysis

Walthman Industries Inc. employs seven salespersons to sell and distribute its product throughout the state. Data taken from reports received from the salespersons during the year ended December 31 are as follows:

Instructions

1. Prepare a table indicating contribution margin, variable cost of goods sold as a percent of sales, variable selling expenses as a percent of sales, and contribution margin ratio by salesperson. Round whole percents to a single digit.

2. Which salesperson generated the highest contribution margin ratio for the year and why?

3. Briefly list factors other than contribution margin that should be considered in evaluating the performance of salespersons.

Walthman Industries Inc. employs seven salespersons to sell and distribute its product throughout the state. Data taken from reports received from the salespersons during the year ended December 31 are as follows:

Instructions

1. Prepare a table indicating contribution margin, variable cost of goods sold as a percent of sales, variable selling expenses as a percent of sales, and contribution margin ratio by salesperson. Round whole percents to a single digit.

2. Which salesperson generated the highest contribution margin ratio for the year and why?

3. Briefly list factors other than contribution margin that should be considered in evaluating the performance of salespersons.

سؤال

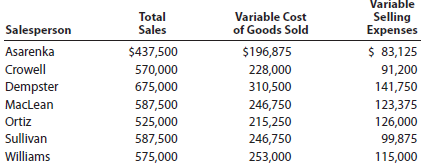

Salespersons' report and analysis

Pachec Inc. employs seven salespersons to sell and distribute its product throughout the state. Data taken from reports received from the salespersons during the year ended June 30 are as follows:

Instructions

1. Prepare a table indicating contribution margin, variable cost of goods sold as a percent of sales, variable selling expenses as a percent of sales, and contribution margin ratio by salesperson. (Round whole percent to one digit after decimal point.)

2. Which salesperson generated the highest contribution margin ratio for the year and why?

3. Briefly list factors other than contribution margin that should be considered in evaluating the performance of salespersons.

Pachec Inc. employs seven salespersons to sell and distribute its product throughout the state. Data taken from reports received from the salespersons during the year ended June 30 are as follows:

Instructions

1. Prepare a table indicating contribution margin, variable cost of goods sold as a percent of sales, variable selling expenses as a percent of sales, and contribution margin ratio by salesperson. (Round whole percent to one digit after decimal point.)

2. Which salesperson generated the highest contribution margin ratio for the year and why?

3. Briefly list factors other than contribution margin that should be considered in evaluating the performance of salespersons.

سؤال

Contribution margin analysis

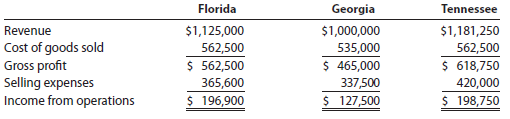

Trans Sport Company sells sporting goods to retailers in three different states-Florida, Georgia, and Tennessee. The following profit analysis by state was prepared by the company:

The following fixed costs have also been provided:

In addition, assume that inventories have been negligible.

Management believes it could increase state sales by 20%, without increasing any of the fixed costs, by spending an additional $42,200 per state on advertising.

1. Prepare a contribution margin by state report for Trans Sport Company.

2. Determine how much state operating profit will be generated for an additional $42,200 per state on advertising.

3. Which state will provide the greatest profit return for a $42,200 increase in advertising? Why?

Trans Sport Company sells sporting goods to retailers in three different states-Florida, Georgia, and Tennessee. The following profit analysis by state was prepared by the company:

The following fixed costs have also been provided:

In addition, assume that inventories have been negligible.

Management believes it could increase state sales by 20%, without increasing any of the fixed costs, by spending an additional $42,200 per state on advertising.

1. Prepare a contribution margin by state report for Trans Sport Company.

2. Determine how much state operating profit will be generated for an additional $42,200 per state on advertising.

3. Which state will provide the greatest profit return for a $42,200 increase in advertising? Why?

سؤال

سؤال

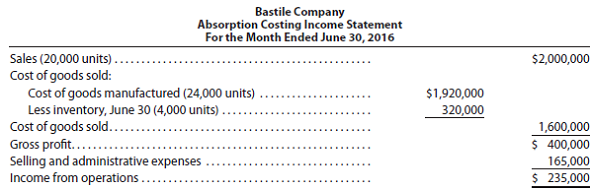

Variable costing income statement

On June 30, the end of the first month of operations, Bastile Company prepared the following income statement, based on the absorption costing concept:

If the fixed manufacturing costs were $192,000 and the variable selling and administrative expenses were $92,400 prepare an income statement according to the variable costing concept.

On June 30, the end of the first month of operations, Bastile Company prepared the following income statement, based on the absorption costing concept:

If the fixed manufacturing costs were $192,000 and the variable selling and administrative expenses were $92,400 prepare an income statement according to the variable costing concept.

سؤال

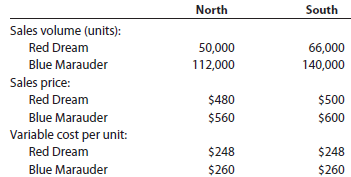

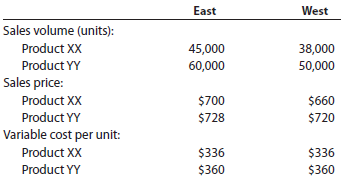

Contribution margin by segment

The following information is for Olivio Coaster Bikes Inc.:

Determine the contribution margin for (a) Red Dream and (b) North Region.

The following information is for LaPlanche Industries Inc.:

Determine the contribution margin for (a) Product YY and (b) West Region.

The following information is for Olivio Coaster Bikes Inc.:

Determine the contribution margin for (a) Red Dream and (b) North Region.

The following information is for LaPlanche Industries Inc.:

Determine the contribution margin for (a) Product YY and (b) West Region.

سؤال

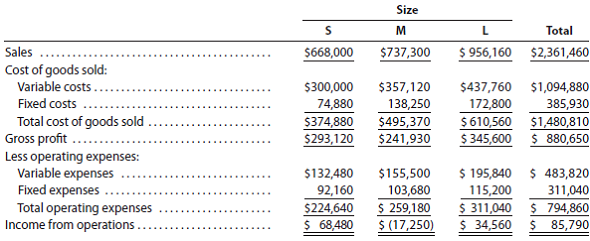

Segment variable costing income statement and effect on income of change in operations

Valdespin Company manufactures three sizes of camping tents-small (S), medium (M), and large (L). The income statement has consistently indicated a net loss for the M size, and management is considering three proposals: (1) continue Size M, (2) discontinue Size M and reduce total output accordingly, or (3) discontinue Size M and conduct an advertising campaign to expand the sales of Size S so that the entire plant capacity can continue to be used.

If Proposal 2 is selected and Size M is discontinued and production curtailed, the annual fixed production costs and fixed operating expenses could be reduced by $46,080 and $32,240 respectively. If Proposal 3 is selected, it is anticipated that an additional annual expenditure of $34,560 for the rental of additional warehouse space would yield an additional 130% in Size S sales volume. It is also assumed that the increased production of Size S would utilize the plant facilities released by the discontinuance of Size M.

The sales and costs have been relatively stable over the past few years, and they are expected to remain so for the foreseeable future. The income statement for the past year ended June 30, 2016, is as follows:

Instructions

1. Prepare an income statement for the past year in the variable costing format. Use the following headings:

Data for each style should be reported through contribution margin. The fixed costs should be deducted from the total contribution margin, as reported in the "Total" column, to determine income from operations.

2. Based on the income statement prepared in (1) and the other data presented, determine the amount by which total annual income from operations would be reduced below its present level if Proposal 2 is accepted.

3. Prepare an income statement in the variable costing format, indicating the projected annual income from operations if Proposal 3 is accepted. Use the following headings:

Data for each style should be reported through contribution margin. The fixed costs should be deducted from the total contribution margin as reported in the "Total" column. For purposes of this problem, the expenditure of $34,560 for the rental of additional warehouse space can be added to the fixed operating expenses.

4. By how much would total annual income increase above its present level if Proposal 3 is accepted? Explain.

Valdespin Company manufactures three sizes of camping tents-small (S), medium (M), and large (L). The income statement has consistently indicated a net loss for the M size, and management is considering three proposals: (1) continue Size M, (2) discontinue Size M and reduce total output accordingly, or (3) discontinue Size M and conduct an advertising campaign to expand the sales of Size S so that the entire plant capacity can continue to be used.

If Proposal 2 is selected and Size M is discontinued and production curtailed, the annual fixed production costs and fixed operating expenses could be reduced by $46,080 and $32,240 respectively. If Proposal 3 is selected, it is anticipated that an additional annual expenditure of $34,560 for the rental of additional warehouse space would yield an additional 130% in Size S sales volume. It is also assumed that the increased production of Size S would utilize the plant facilities released by the discontinuance of Size M.

The sales and costs have been relatively stable over the past few years, and they are expected to remain so for the foreseeable future. The income statement for the past year ended June 30, 2016, is as follows:

Instructions

1. Prepare an income statement for the past year in the variable costing format. Use the following headings:

Data for each style should be reported through contribution margin. The fixed costs should be deducted from the total contribution margin, as reported in the "Total" column, to determine income from operations.

2. Based on the income statement prepared in (1) and the other data presented, determine the amount by which total annual income from operations would be reduced below its present level if Proposal 2 is accepted.

3. Prepare an income statement in the variable costing format, indicating the projected annual income from operations if Proposal 3 is accepted. Use the following headings:

Data for each style should be reported through contribution margin. The fixed costs should be deducted from the total contribution margin as reported in the "Total" column. For purposes of this problem, the expenditure of $34,560 for the rental of additional warehouse space can be added to the fixed operating expenses.

4. By how much would total annual income increase above its present level if Proposal 3 is accepted? Explain.

سؤال

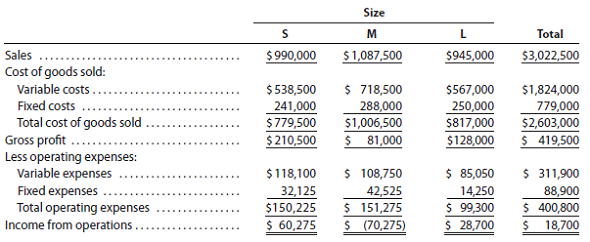

Variable costing income statement and effect on income of change in operations

Kimbrell Inc. manufactures three sizes of utility tables-small (S), medium (M), and large (L). The income statement has consistently indicated a net loss for the M size, and management is considering three proposals: (1) continue Size M, (2) discontinue Size M and reduce total output accordingly, or (3) discontinue Size M and conduct an advertising campaign to expand the sales of Size S so that the entire plant capacity can continue to be used.

If Proposal 2 is selected and Size M is discontinued and production curtailed, the annual fixed production costs and fixed operating expenses could be reduced by $142,500 and $28,350, respectively. If Proposal 3 is selected, it is anticipated that an additional annual expenditure of $85,050 for the salary of an assistant brand manager (classified as a fixed operating expense) would yield an additional 130% in Size S sales volume. It is also assumed that the increased production of Size S would utilize the plant facilities released by the discontinuance of Size M.

The sales and costs have been relatively stable over the past few years, and they are expected to remain so for the foreseeable future. The income statement for the past year ended December 31, 2016, is as follows:

Instructions

1. Prepare an income statement for the past year in the variable costing format. Use the following headings:

Data for each style should be reported through contribution margin. The fixed costs should be deducted from the total contribution margin, as reported in the "Total" column, to determine income from operations.

2. Based on the income statement prepared in (1) and the other data presented above, determine the amount by which total annual income from operations would be reduced below its present level if Proposal 2 is accepted.

3. Prepare an income statement in the variable costing format, indicating the projected annual income from operations if Proposal 3 is accepted. Use the following headings:

Data for each style should be reported through contribution margin. The fixed costs should be deducted from the total contribution margin as reported in the "Total" column. For purposes of this problem, the additional expenditure of $85,050 for the assistant brand manager's salary can be added to the fixed operating expenses.

4. By how much would total annual income increase above its present level if Proposal 3 is accepted? Explain.

Kimbrell Inc. manufactures three sizes of utility tables-small (S), medium (M), and large (L). The income statement has consistently indicated a net loss for the M size, and management is considering three proposals: (1) continue Size M, (2) discontinue Size M and reduce total output accordingly, or (3) discontinue Size M and conduct an advertising campaign to expand the sales of Size S so that the entire plant capacity can continue to be used.

If Proposal 2 is selected and Size M is discontinued and production curtailed, the annual fixed production costs and fixed operating expenses could be reduced by $142,500 and $28,350, respectively. If Proposal 3 is selected, it is anticipated that an additional annual expenditure of $85,050 for the salary of an assistant brand manager (classified as a fixed operating expense) would yield an additional 130% in Size S sales volume. It is also assumed that the increased production of Size S would utilize the plant facilities released by the discontinuance of Size M.

The sales and costs have been relatively stable over the past few years, and they are expected to remain so for the foreseeable future. The income statement for the past year ended December 31, 2016, is as follows:

Instructions

1. Prepare an income statement for the past year in the variable costing format. Use the following headings:

Data for each style should be reported through contribution margin. The fixed costs should be deducted from the total contribution margin, as reported in the "Total" column, to determine income from operations.

2. Based on the income statement prepared in (1) and the other data presented above, determine the amount by which total annual income from operations would be reduced below its present level if Proposal 2 is accepted.

3. Prepare an income statement in the variable costing format, indicating the projected annual income from operations if Proposal 3 is accepted. Use the following headings:

Data for each style should be reported through contribution margin. The fixed costs should be deducted from the total contribution margin as reported in the "Total" column. For purposes of this problem, the additional expenditure of $85,050 for the assistant brand manager's salary can be added to the fixed operating expenses.

4. By how much would total annual income increase above its present level if Proposal 3 is accepted? Explain.

سؤال

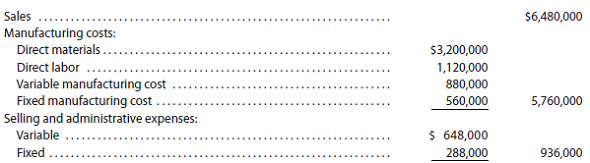

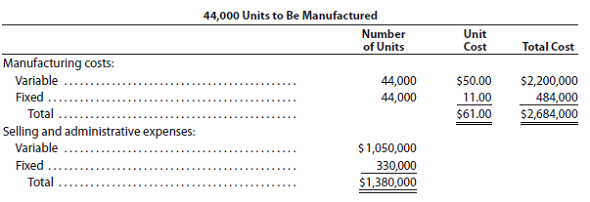

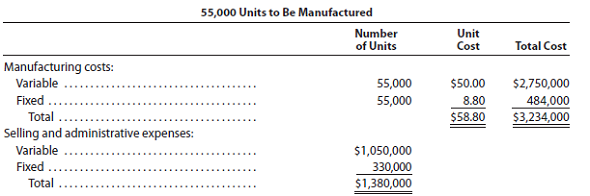

Absorption costing Group Project

Craig Company is a family-owned business in which you own 20% of the common stock and your brothers and sisters own the remaining shares. The employment contract of Craig's new president, Ajay Pinder, stipulates a base salary of $140,000 per year plus 10% of income from operations in excess of $670,000. Craig uses the absorption costing method of reporting income from operations, which has averaged approximately $670,000 for the past several years.

Sales for 2016, Pinder's first year as president of Craig Company, are estimated at 44,000 units at a selling price of $106 per unit. To maximize the use of Craig's productive capacity, Pinder has decided to manufacture 55,000 units, rather than the 44,000 units of estimated sales. The beginning inventory at January 1, 2016, is insignificant in amount, and the manufacturing costs and selling and administrative expenses for the production of 44,000 and 55,000 units are as follows:

1. In one group, prepare an absorption costing income statement for the year ending December 31, 2016, based on sales of 44,000 units and the manufacture of 44,000 units. In the other group, conduct the same analysis, assuming production of 55,000 units.

2. Explain the difference in the income from operations reported in (1).

3. Compute Pinder's total salary for the year 2016, based on sales of 44,000 units and the manufacture of 44,000 units (Group 1) and 55,000 units (Group 2). Compare your answers.

4. In addition to maximizing the use of Craig Company's productive capacity, why might Pinder wish to manufacture 55,000 units rather than 44,000 units?

5. Can you suggest an alternative way in which Pinder's salary could be determined, using a base salary of $140,000 and 10% of income from operations in excess of $670,000, so that the salary could not be increased by simply manufacturing more units?

Craig Company is a family-owned business in which you own 20% of the common stock and your brothers and sisters own the remaining shares. The employment contract of Craig's new president, Ajay Pinder, stipulates a base salary of $140,000 per year plus 10% of income from operations in excess of $670,000. Craig uses the absorption costing method of reporting income from operations, which has averaged approximately $670,000 for the past several years.

Sales for 2016, Pinder's first year as president of Craig Company, are estimated at 44,000 units at a selling price of $106 per unit. To maximize the use of Craig's productive capacity, Pinder has decided to manufacture 55,000 units, rather than the 44,000 units of estimated sales. The beginning inventory at January 1, 2016, is insignificant in amount, and the manufacturing costs and selling and administrative expenses for the production of 44,000 and 55,000 units are as follows:

1. In one group, prepare an absorption costing income statement for the year ending December 31, 2016, based on sales of 44,000 units and the manufacture of 44,000 units. In the other group, conduct the same analysis, assuming production of 55,000 units.

2. Explain the difference in the income from operations reported in (1).

3. Compute Pinder's total salary for the year 2016, based on sales of 44,000 units and the manufacture of 44,000 units (Group 1) and 55,000 units (Group 2). Compare your answers.

4. In addition to maximizing the use of Craig Company's productive capacity, why might Pinder wish to manufacture 55,000 units rather than 44,000 units?

5. Can you suggest an alternative way in which Pinder's salary could be determined, using a base salary of $140,000 and 10% of income from operations in excess of $670,000, so that the salary could not be increased by simply manufacturing more units?

سؤال

سؤال

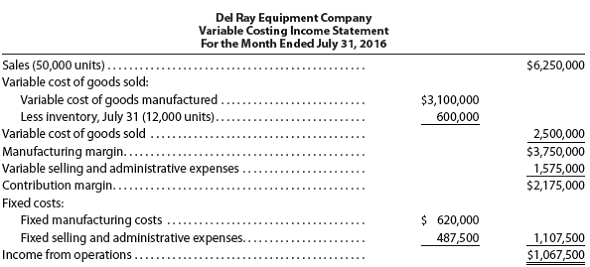

Absorption costing income statement

On July 31, the end of the first month of operations, Del Ray Equipment Company prepared the following income statement, based on the variable costing concept:

Prepare an income statement under absorption costing.

On July 31, the end of the first month of operations, Del Ray Equipment Company prepared the following income statement, based on the variable costing concept:

Prepare an income statement under absorption costing.

سؤال

سؤال

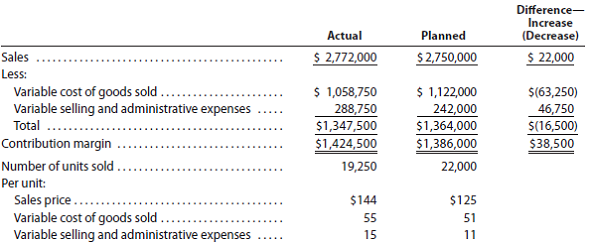

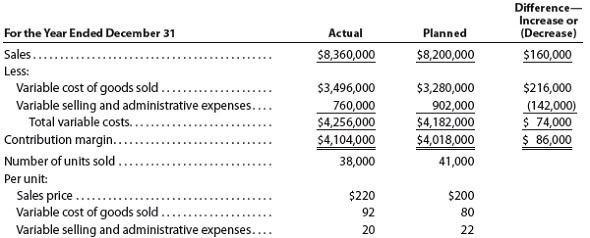

Contribution margin analysis

Dozier Industries Inc. manufactures only one product. For the year ended December 31, the contribution margin increased by $38,500 from the planned level of $1,386,000 The president of Dozier Industries Inc. has expressed some concern about such a small increase and has requested a follow-up report.

The following data have been gathered from the accounting records for the year ended December 31:

Instructions

1. Prepare a contribution margin analysis report for the year ended December 31.

2. At a meeting of the board of directors on January 30, the president, after reviewing the contribution margin analysis report, made the following comment:

It looks as if the price increase of $19 had the effect of decreasing sales volume. However, this was a favorable tradeoff. The variable cost of goods sold was less than planned. Apparently, we are efficiently managing our variable cost of goods sold. However, the variable selling and administrative expenses appear out of control. Let's look into these expenses and get them under control! Also, let's consider increasing the sales price to $160 and continue this favorable tradeoff between higher price and lower volume.

Do you agree with the president's comment? Explain.

Dozier Industries Inc. manufactures only one product. For the year ended December 31, the contribution margin increased by $38,500 from the planned level of $1,386,000 The president of Dozier Industries Inc. has expressed some concern about such a small increase and has requested a follow-up report.

The following data have been gathered from the accounting records for the year ended December 31:

Instructions

1. Prepare a contribution margin analysis report for the year ended December 31.

2. At a meeting of the board of directors on January 30, the president, after reviewing the contribution margin analysis report, made the following comment:

It looks as if the price increase of $19 had the effect of decreasing sales volume. However, this was a favorable tradeoff. The variable cost of goods sold was less than planned. Apparently, we are efficiently managing our variable cost of goods sold. However, the variable selling and administrative expenses appear out of control. Let's look into these expenses and get them under control! Also, let's consider increasing the sales price to $160 and continue this favorable tradeoff between higher price and lower volume.

Do you agree with the president's comment? Explain.

سؤال

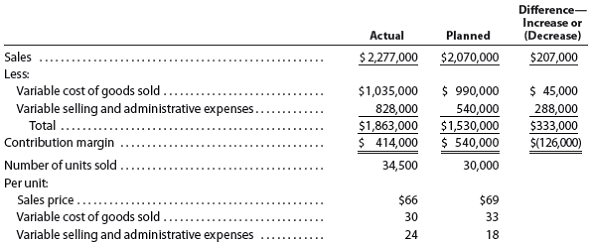

Contribution margin analysis

Mathews Company manufactures only one product. For the year ended December 31, the contribution margin decreased by $126,000 from the planned level of $540,000. The president of Mathews Company has expressed some concern about this decrease and has requested a follow-up report.

The following data have been gathered from the accounting records for the year ended December 31:

Instructions

1. Prepare a contribution margin analysis report for the year ended December 31.

2. At a meeting of the board of directors on January 30, the president, after reviewing the contribution margin analysis report, made the following comment:

It looks as if the price decrease of $3.00 had the effect of increasing sales. However, we lost control over the variable cost of goods sold and variable selling and administrative expenses. Let's look into these expenses and get them under control! Also, let's consider decreasing the sales price to $60 to increase sales further.

Do you agree with the president's comment? Explain.

Mathews Company manufactures only one product. For the year ended December 31, the contribution margin decreased by $126,000 from the planned level of $540,000. The president of Mathews Company has expressed some concern about this decrease and has requested a follow-up report.

The following data have been gathered from the accounting records for the year ended December 31:

Instructions

1. Prepare a contribution margin analysis report for the year ended December 31.

2. At a meeting of the board of directors on January 30, the president, after reviewing the contribution margin analysis report, made the following comment:

It looks as if the price decrease of $3.00 had the effect of increasing sales. However, we lost control over the variable cost of goods sold and variable selling and administrative expenses. Let's look into these expenses and get them under control! Also, let's consider decreasing the sales price to $60 to increase sales further.

Do you agree with the president's comment? Explain.

سؤال

سؤال

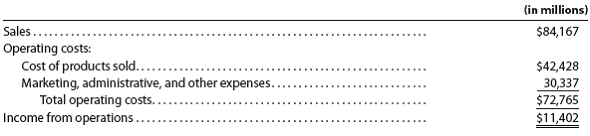

Variable costing income statement

The following data were adapted from a recent income statement of Procter Gamble Company:

Assume that the variable amount of each category of operating costs is as follows:

a. Based on the data given, prepare a variable costing income statement for Procter Gamble Company, assuming that the company maintained constant inventory levels during the period.

b. If Procter Gamble reduced its inventories during the period, what impact would that have on the income from operations determined under absorption costing?

The following data were adapted from a recent income statement of Procter Gamble Company:

Assume that the variable amount of each category of operating costs is as follows:

a. Based on the data given, prepare a variable costing income statement for Procter Gamble Company, assuming that the company maintained constant inventory levels during the period.

b. If Procter Gamble reduced its inventories during the period, what impact would that have on the income from operations determined under absorption costing?

سؤال

سؤال

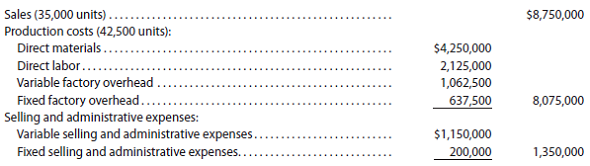

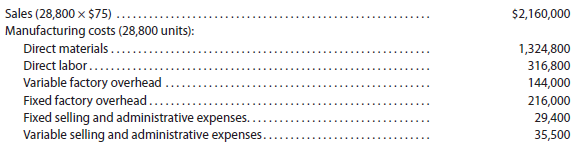

Estimated income statements, using absorption and variable costing

Prior to the first month of operations ending July 31, 2016, Muzenski Industries Inc. estimated the following operating results:

The company is evaluating a proposal to manufacture 36,000 units instead of 28,800 units, thus creating an ending inventory of 7,200 units. Manufacturing the additional units will not change sales, unit variable factory overhead costs, total fixed factory overhead cost, or total selling and administrative expenses.

a. Prepare an estimated income statement, comparing operating results if 28,800 and 36,000 units are manufactured in (1) the absorption costing format and (2) the variable costing format.

b. What is the reason for the difference in income from operations reported for the two levels of production by the absorption costing income statement?

Prior to the first month of operations ending July 31, 2016, Muzenski Industries Inc. estimated the following operating results:

The company is evaluating a proposal to manufacture 36,000 units instead of 28,800 units, thus creating an ending inventory of 7,200 units. Manufacturing the additional units will not change sales, unit variable factory overhead costs, total fixed factory overhead cost, or total selling and administrative expenses.

a. Prepare an estimated income statement, comparing operating results if 28,800 and 36,000 units are manufactured in (1) the absorption costing format and (2) the variable costing format.

b. What is the reason for the difference in income from operations reported for the two levels of production by the absorption costing income statement?

سؤال

سؤال

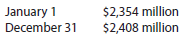

Variable and absorption costing

Ansara Company had the following abbreviated income statement for the year ended December 31, 2016:

Assume that there were $3,860 million fixed manufacturing costs and $1,170 million fixed selling, administrative, and other costs for the year.

The finished goods inventories at the beginning and end of the year from the balance sheet were as follows:

Assume that 30% of the beginning and ending inventory consists of fixed costs. Assume work in process and materials inventory were unchanged during the period.

a. Prepare an income statement according to the variable costing concept for Ansara Company for 2016.

b. Explain the difference between the amount of income from operations reported under the absorption costing and variable costing concepts.

Ansara Company had the following abbreviated income statement for the year ended December 31, 2016:

Assume that there were $3,860 million fixed manufacturing costs and $1,170 million fixed selling, administrative, and other costs for the year.

The finished goods inventories at the beginning and end of the year from the balance sheet were as follows:

Assume that 30% of the beginning and ending inventory consists of fixed costs. Assume work in process and materials inventory were unchanged during the period.

a. Prepare an income statement according to the variable costing concept for Ansara Company for 2016.

b. Explain the difference between the amount of income from operations reported under the absorption costing and variable costing concepts.

سؤال

سؤال

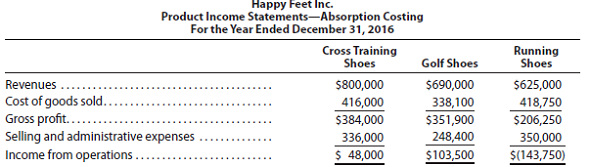

Variable and absorption costing-three products

Happy Feet Inc. manufactures and sells three types of shoes. The income statements prepared under the absorption costing method for the three shoes are as follows:

In addition, you have determined the following information with respect to allocated fixed costs:

These fixed costs are used to support all three product lines. In addition, you have determined that the inventory is negligible.

The management of the company has deemed the profit performance of the running shoe line as unacceptable. As a result, it has decided to eliminate the running shoe line. Management does not expect to be able to increase sales in the other two lines. However, as a result of eliminating the running shoe line, management expects the profits of the company to increase by $143,750.

a. Do you agree with management's decision and conclusions?

b. Prepare a variable costing income statement for the three products.

c. Use the report in (b) to determine the profit impact of eliminating the running shoe line, assuming no other changes.

Happy Feet Inc. manufactures and sells three types of shoes. The income statements prepared under the absorption costing method for the three shoes are as follows:

In addition, you have determined the following information with respect to allocated fixed costs:

These fixed costs are used to support all three product lines. In addition, you have determined that the inventory is negligible.

The management of the company has deemed the profit performance of the running shoe line as unacceptable. As a result, it has decided to eliminate the running shoe line. Management does not expect to be able to increase sales in the other two lines. However, as a result of eliminating the running shoe line, management expects the profits of the company to increase by $143,750.

a. Do you agree with management's decision and conclusions?

b. Prepare a variable costing income statement for the three products.

c. Use the report in (b) to determine the profit impact of eliminating the running shoe line, assuming no other changes.

سؤال

سؤال

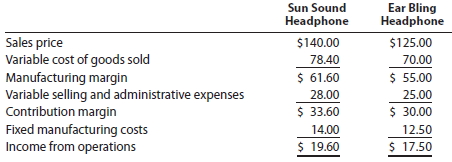

Change in sales mix and contribution margin

Head Pops Inc. manufactures two models of solar powered noise-canceling headphones: Sun Sound and Ear Bling models. The company is operating at less than full capacity. Market research indicates that 28,000 additional Sun Sound and 30,000 additional Ear Bling headphones could be sold. The income from operations by unit of product is as follows:

Prepare an analysis indicating the increase or decrease in total profitability if 28,000 additional Sun Sound and 30,000 additional Ear Bling headphones are produced and sold, assuming that there is sufficient capacity for the additional production.

Head Pops Inc. manufactures two models of solar powered noise-canceling headphones: Sun Sound and Ear Bling models. The company is operating at less than full capacity. Market research indicates that 28,000 additional Sun Sound and 30,000 additional Ear Bling headphones could be sold. The income from operations by unit of product is as follows:

Prepare an analysis indicating the increase or decrease in total profitability if 28,000 additional Sun Sound and 30,000 additional Ear Bling headphones are produced and sold, assuming that there is sufficient capacity for the additional production.

سؤال

Product profitability analysis

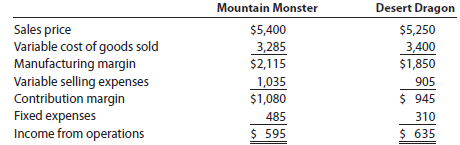

PowerTrain Sports Inc. manufactures and sells two styles of All Terrain Vehicles (ATVs), the Mountain Monster, and Desert Dragon from a single manufacturing facility. The manufacturing facility operates at 100% of capacity. The following per unit information is available for the two products:

In addition, the following sales unit volume information for the period is as follows:

a. Prepare a contribution margin by product report. Calculate the contribution margin ratio for each product as a whole percent, rounded to two decimal places.

b. What advice would you give to the management of PowerTrain Sports Inc.regarding the relative profitability of the two products?

PowerTrain Sports Inc. manufactures and sells two styles of All Terrain Vehicles (ATVs), the Mountain Monster, and Desert Dragon from a single manufacturing facility. The manufacturing facility operates at 100% of capacity. The following per unit information is available for the two products:

In addition, the following sales unit volume information for the period is as follows:

a. Prepare a contribution margin by product report. Calculate the contribution margin ratio for each product as a whole percent, rounded to two decimal places.

b. What advice would you give to the management of PowerTrain Sports Inc.regarding the relative profitability of the two products?

سؤال

Territory and product profitability analysis

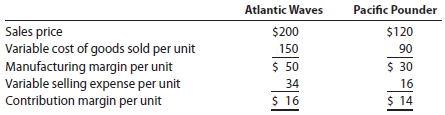

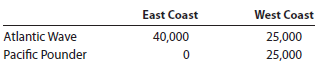

Coast to Coast Surfboards Inc. manufactures and sells two styles of surfboards, Atlantic Wave and Pacific Pounder. These surfboards are sold in two regions, East Coast and West Coast. Information about the two surfboards is as follows:

The sales unit volume for the sales territories and products for the period is as follows:

a. Prepare a contribution margin by sales territory report. Calculate the contribution margin ratio for each territory as a whole percent, rounded to two decimal places.

b. What advice would you give to the management of Coast to Coast Surfboards regarding the relative profitability of the two territories?

Coast to Coast Surfboards Inc. manufactures and sells two styles of surfboards, Atlantic Wave and Pacific Pounder. These surfboards are sold in two regions, East Coast and West Coast. Information about the two surfboards is as follows:

The sales unit volume for the sales territories and products for the period is as follows:

a. Prepare a contribution margin by sales territory report. Calculate the contribution margin ratio for each territory as a whole percent, rounded to two decimal places.

b. What advice would you give to the management of Coast to Coast Surfboards regarding the relative profitability of the two territories?

سؤال

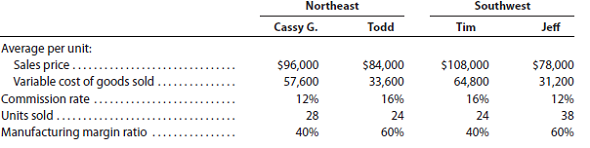

Sales territory and salesperson profitability analysis

Reyes Industries Inc. manufactures and sells a variety of commercial vehicles in the North east and South west regions. There are two salespersons assigned to each territory. Higher commission rates go to the most experienced salespersons. The following sales statistics are available for each salesperson:

a. 1. Prepare a contribution margin by salesperson report. Calculate the contribution margin ratio for each salesperson.

2. Interpret the report.

b. 1. Prepare a contribution margin by territory report. Calculate the contribution margin for each territory as a percent, rounded to one decimal place.

2. Interpret the report.

Reyes Industries Inc. manufactures and sells a variety of commercial vehicles in the North east and South west regions. There are two salespersons assigned to each territory. Higher commission rates go to the most experienced salespersons. The following sales statistics are available for each salesperson:

a. 1. Prepare a contribution margin by salesperson report. Calculate the contribution margin ratio for each salesperson.

2. Interpret the report.

b. 1. Prepare a contribution margin by territory report. Calculate the contribution margin for each territory as a percent, rounded to one decimal place.

2. Interpret the report.

سؤال

Segment profitability analysis

The marketing segment sales for Caterpillar, Inc. , for a recent year follow:

In addition, assume the following information:

a. Use the sales information and the additional assumed information to prepare a contribution margin by segment report. Round to two decimal places. In addition, calculate the contribution margin ratio for each segment as a percentage, rounded to one decimal place.

b. Prepare a table showing the manufacturing margin, dealer commissions, and variable promotion expenses as a percent of sales for each segment. Round whole percents to one decimal place.

c. Use the information in (a) and (b) to interpret the segment performance.

The marketing segment sales for Caterpillar, Inc. , for a recent year follow:

In addition, assume the following information:

a. Use the sales information and the additional assumed information to prepare a contribution margin by segment report. Round to two decimal places. In addition, calculate the contribution margin ratio for each segment as a percentage, rounded to one decimal place.

b. Prepare a table showing the manufacturing margin, dealer commissions, and variable promotion expenses as a percent of sales for each segment. Round whole percents to one decimal place.

c. Use the information in (a) and (b) to interpret the segment performance.

سؤال

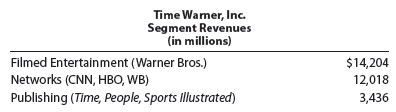

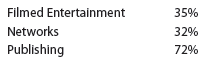

Segment contribution margin analysis

The operating revenues of the three largest business segments for Time Warner, Inc. , for a recent year follow. Each segment includes a number of businesses, examples of which are indicated in parentheses.

Assume that the variable costs as a percent of sales for each segment are as follows:

a. Determine the contribution margin (round to whole millions) and contribution margin ratio (round to whole percents) for each segment from the information given.

b. Why is the contribution margin ratio for the Publishing segment smaller than for the other segments?

c. Does your answer to (b) mean that the other segments are more profitable businesses than the Publishing segment?

The operating revenues of the three largest business segments for Time Warner, Inc. , for a recent year follow. Each segment includes a number of businesses, examples of which are indicated in parentheses.

Assume that the variable costs as a percent of sales for each segment are as follows:

a. Determine the contribution margin (round to whole millions) and contribution margin ratio (round to whole percents) for each segment from the information given.

b. Why is the contribution margin ratio for the Publishing segment smaller than for the other segments?

c. Does your answer to (b) mean that the other segments are more profitable businesses than the Publishing segment?

سؤال

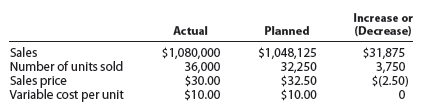

Contribution margin analysis-sales

Buy Best Inc. sells electronic equipment. Management decided early in the year to reduce the price of the speakers in order to increase sales volume. As a result, for the year ended December 31, the sales increased by $31,875 from the planned level of $1,048,125. The following information is available from the accounting records for the year ended December 31.

a. Prepare an analysis of the sales quantity and unit price factors.

b. Did the price decrease generate sufficient volume to result in a net increase in contribution margin if the actual variable cost per unit was $10, as planned?

Buy Best Inc. sells electronic equipment. Management decided early in the year to reduce the price of the speakers in order to increase sales volume. As a result, for the year ended December 31, the sales increased by $31,875 from the planned level of $1,048,125. The following information is available from the accounting records for the year ended December 31.

a. Prepare an analysis of the sales quantity and unit price factors.

b. Did the price decrease generate sufficient volume to result in a net increase in contribution margin if the actual variable cost per unit was $10, as planned?

سؤال

Contribution margin analysis-sales

The following data for Romero Products Inc. are available:

Prepare an analysis of the sales quantity and unit price factors.

The following data for Romero Products Inc. are available:

Prepare an analysis of the sales quantity and unit price factors.

سؤال

سؤال

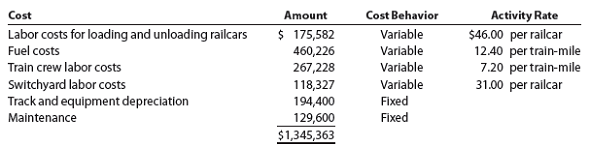

Variable costing income statement for a service company

East Coast Railroad Company transports commodities among three routes (city-pairs): Atlanta/Baltimore, Baltimore/Pittsburgh, and Pittsburgh/Atlanta. Significant costs, their cost behavior, and activity rates for April are as follows:

Operating statistics from the management information system reveal the following for April:

a. Prepare a contribution margin by route report for East Coast Railroad Company for the month of April. Calculate the contribution margin ratio in whole percents, rounded to one decimal place.

b. Evaluate the route performance of the railroad using the report in (a).

East Coast Railroad Company transports commodities among three routes (city-pairs): Atlanta/Baltimore, Baltimore/Pittsburgh, and Pittsburgh/Atlanta. Significant costs, their cost behavior, and activity rates for April are as follows:

Operating statistics from the management information system reveal the following for April:

a. Prepare a contribution margin by route report for East Coast Railroad Company for the month of April. Calculate the contribution margin ratio in whole percents, rounded to one decimal place.

b. Evaluate the route performance of the railroad using the report in (a).

سؤال

سؤال

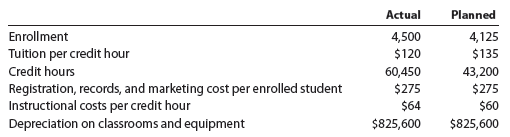

Variable costing income statement and contribution margin analysis for a service company

The actual and planned data for Underwater University for the Fall term 2016 were as follows:

Registration, records, and marketing costs vary by the number of enrolled students, while instructional costs vary by the number of credit hours. Depreciation is a fixed cost.

a. Prepare a variable costing income statement showing the contribution margin and income from operations for the Fall 2016 term.

b. Prepare a contribution margin analysis report comparing planned with actual performance for the Fall 2016 term.

The actual and planned data for Underwater University for the Fall term 2016 were as follows:

Registration, records, and marketing costs vary by the number of enrolled students, while instructional costs vary by the number of credit hours. Depreciation is a fixed cost.

a. Prepare a variable costing income statement showing the contribution margin and income from operations for the Fall 2016 term.

b. Prepare a contribution margin analysis report comparing planned with actual performance for the Fall 2016 term.

فتح الحزمة

قم بالتسجيل لفتح البطاقات في هذه المجموعة!

Unlock Deck

Unlock Deck

1/57

العب

ملء الشاشة (f)

Deck 21: Variable Costing for Management Analysis

1

Ethics and professional conduct in business

The Southwest Division of Texcaliber Inc. uses absorption costing for profit reporting. The general manager of the Southwest Division is concerned about meeting the income objectives of the division. At the beginning of the reporting period, the division had an adequate supply of inventory. The general manager has decided to increase production of goods in the plant in order to allocate fixed manufacturing cost over a greater number of units. Unfortunately, the increased production cannot be sold and will increase the inventory. However, the impact on earnings will be positive because the lower cost per unit will be matched against sales. The general manager has come to Aston Melon, the controller, to determine exactly how much additional production is required in order to increase net income enough to meet the division's profit objectives. Aston analyzes the data and determines that the inventory will need to be increased by 30% in order to absorb enough fixed costs and meet the income objective. Aston reports this information to the division manager.

Discuss whether Aston is acting in an ethical manner.

The Southwest Division of Texcaliber Inc. uses absorption costing for profit reporting. The general manager of the Southwest Division is concerned about meeting the income objectives of the division. At the beginning of the reporting period, the division had an adequate supply of inventory. The general manager has decided to increase production of goods in the plant in order to allocate fixed manufacturing cost over a greater number of units. Unfortunately, the increased production cannot be sold and will increase the inventory. However, the impact on earnings will be positive because the lower cost per unit will be matched against sales. The general manager has come to Aston Melon, the controller, to determine exactly how much additional production is required in order to increase net income enough to meet the division's profit objectives. Aston analyzes the data and determines that the inventory will need to be increased by 30% in order to absorb enough fixed costs and meet the income objective. Aston reports this information to the division manager.

Discuss whether Aston is acting in an ethical manner.

Comment the Ethical manner of Aston:

S Division of TI uses absorption costing for reporting income statement figures. The general manager of the division is under pressure to meet income targets. He is planning to increase production even though there are no corresponding customer orders.

Aston, the controller of production, is acting with integrity by reporting the information to the division manager. As a controller, he has overall jurisdiction over the operations.

However, he may not have the powers to question the general manager's actions of increasing production solely for meeting the division's profit targets.

By reporting the matter to the division manager, Aston is indirectly questioning the decision of the general manager.

It is the responsibility of the divisional manager to present a true picture of the division's performance. Condoning the general manager's actions would show a lack of integrity for the following reasons:

• The division is resorting to a deliberate increase in production without corresponding customer demand in order to show increased earnings. The result is that fixed costs are allocated over a larger inventory base. This effectively decreases the unit cost of production decreases for the same sales level and artificially boosts net income for the period. The fixed costs become part of unsold inventory and thus get transferred to the balance sheet.

• The true state of profitability and net income is glossed over and hidden behind artificial reporting. The income information in such financial reports can be misleading to senior management.

• Since there is an avenue available to cover up lackluster performance, there is no incentive to improve performance and profitability. Senior management, believing that the division's performance is good, will not intervene to improve things.

• Increasing production without corresponding sales (production exceeds sales) provides short-term benefits. When inventory gets used later, the costs must be allocated to the period's sales, reducing profits for the subsequent reporting period. Therefore the general manager's action will adversely affect future period net income.

• The objective of financial reporting is to present a true picture of the company's affairs to users. The general manager has utilized a loophole in absorption costing under GAAP, which permits transfer of fixed costs to inventory. This is tantamount to misrepresentation.

S Division of TI uses absorption costing for reporting income statement figures. The general manager of the division is under pressure to meet income targets. He is planning to increase production even though there are no corresponding customer orders.

Aston, the controller of production, is acting with integrity by reporting the information to the division manager. As a controller, he has overall jurisdiction over the operations.

However, he may not have the powers to question the general manager's actions of increasing production solely for meeting the division's profit targets.

By reporting the matter to the division manager, Aston is indirectly questioning the decision of the general manager.

It is the responsibility of the divisional manager to present a true picture of the division's performance. Condoning the general manager's actions would show a lack of integrity for the following reasons:

• The division is resorting to a deliberate increase in production without corresponding customer demand in order to show increased earnings. The result is that fixed costs are allocated over a larger inventory base. This effectively decreases the unit cost of production decreases for the same sales level and artificially boosts net income for the period. The fixed costs become part of unsold inventory and thus get transferred to the balance sheet.

• The true state of profitability and net income is glossed over and hidden behind artificial reporting. The income information in such financial reports can be misleading to senior management.

• Since there is an avenue available to cover up lackluster performance, there is no incentive to improve performance and profitability. Senior management, believing that the division's performance is good, will not intervene to improve things.

• Increasing production without corresponding sales (production exceeds sales) provides short-term benefits. When inventory gets used later, the costs must be allocated to the period's sales, reducing profits for the subsequent reporting period. Therefore the general manager's action will adversely affect future period net income.

• The objective of financial reporting is to present a true picture of the company's affairs to users. The general manager has utilized a loophole in absorption costing under GAAP, which permits transfer of fixed costs to inventory. This is tantamount to misrepresentation.

2

What types of costs are customarily included in the cost of manufactured products under (a) the absorption costing concept and (b) the variable costing concept?

a. Absorption Costing:

Under Absorption Costing, the cost of manufactured goods includes:

1. Direct materials costs

2. Direct labor costs

3. Factory overhead costs consisting of (i) variable and (ii) fixed factory overheads.

b. Variable Costing:

Under Variable Costing, only variable costs are included for determining the cost of goods manufactured. Fixed costs relating to factory overheads are treated as a period expense. The costs included are:

1. Direct materials costs

2. Direct labor costs

3. Variable factory overheads

The cost of goods manufactured will be higher when Absorption Costing is adopted, as it includes fixed factory overheads also.

Under Absorption Costing, the cost of manufactured goods includes:

1. Direct materials costs

2. Direct labor costs

3. Factory overhead costs consisting of (i) variable and (ii) fixed factory overheads.

b. Variable Costing:

Under Variable Costing, only variable costs are included for determining the cost of goods manufactured. Fixed costs relating to factory overheads are treated as a period expense. The costs included are:

1. Direct materials costs

2. Direct labor costs

3. Variable factory overheads

The cost of goods manufactured will be higher when Absorption Costing is adopted, as it includes fixed factory overheads also.

3

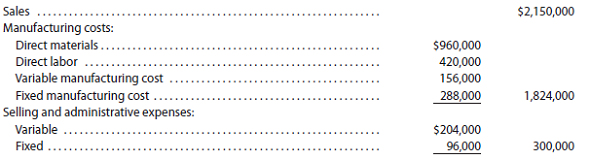

Inventory valuation under absorption costing and variable costing

At the end of the first year of operations, 6,400 units remained in the finished goods inventory. The unit manufacturing costs during the year were as follows:

Determine the cost of the finished goods inventory reported on the balance sheet under (a) the absorption costing concept and (b) the variable costing concept.

At the end of the first year of operations, 6,400 units remained in the finished goods inventory. The unit manufacturing costs during the year were as follows:

Determine the cost of the finished goods inventory reported on the balance sheet under (a) the absorption costing concept and (b) the variable costing concept.

a. Absorption costing:

Under the absorption costing approach all the costs incurred for manufacturing a product will be allocated to the costs. The cost incurred for manufacturing will consist of direct material, direct labor, variable overhead and fixed overheads. The absorption costing includes both fixed and variable overheads.

Calculate Valuation of Closing Inventory as per Absorption Costing:

Under absorption costing the fixed manufacturing costs are treated as manufacturing costs and are added to direct material, direct labor and other direct expenses to arrive at costs of goods sold.

Consider the below table:

Therefore from the above calculations, it is clear that the value of Inventory calculated using absorption costing is $876,800

Therefore from the above calculations, it is clear that the value of Inventory calculated using absorption costing is $876,800

b. Variable costing:

• Under variable costing, all the variable costs are treated as product costs. All the fixed costs are treated as period costs. Therefore, all the costs related to the manufacturing of products, that will vary will the production such as direct material, direct labor and variable manufacturing overhead are treated as product costs.

• Further, costs such as selling and administration expenses which are fixed in nature, are treated as period costs, as these expenses are incurred throughout the period irrespective of production.

Calculate Valuation of Closing Inventory as per Variable Costing:

Under variable costing concept, fixed manufacturing costs are not included while calculating the cost of goods sold. Hence to calculate the contribution margin, variable costing uses the below formula:

Consider Below Table:

Consider Below Table:

Therefore from the above calculations, it is clear that the value of Inventory calculated using Variable costing is $780,800.

Therefore from the above calculations, it is clear that the value of Inventory calculated using Variable costing is $780,800.

Under the absorption costing approach all the costs incurred for manufacturing a product will be allocated to the costs. The cost incurred for manufacturing will consist of direct material, direct labor, variable overhead and fixed overheads. The absorption costing includes both fixed and variable overheads.

Calculate Valuation of Closing Inventory as per Absorption Costing:

Under absorption costing the fixed manufacturing costs are treated as manufacturing costs and are added to direct material, direct labor and other direct expenses to arrive at costs of goods sold.

Consider the below table:

Therefore from the above calculations, it is clear that the value of Inventory calculated using absorption costing is $876,800 b. Variable costing:

• Under variable costing, all the variable costs are treated as product costs. All the fixed costs are treated as period costs. Therefore, all the costs related to the manufacturing of products, that will vary will the production such as direct material, direct labor and variable manufacturing overhead are treated as product costs.

• Further, costs such as selling and administration expenses which are fixed in nature, are treated as period costs, as these expenses are incurred throughout the period irrespective of production.

Calculate Valuation of Closing Inventory as per Variable Costing:

Under variable costing concept, fixed manufacturing costs are not included while calculating the cost of goods sold. Hence to calculate the contribution margin, variable costing uses the below formula:

Consider Below Table: Therefore from the above calculations, it is clear that the value of Inventory calculated using Variable costing is $780,800. 4

Variable costing

Light Company has the following information for January:

Determine (a) the manufacturing margin, (b) the contribution margin, and (c) income from operations for Light Company for the month of January.

Marley Company has the following information for March:

Determine (a) the manufacturing margin, (b) the contribution margin, and (c) income from operations for Marley Company for the month of March.

Light Company has the following information for January:

Determine (a) the manufacturing margin, (b) the contribution margin, and (c) income from operations for Light Company for the month of January.

Marley Company has the following information for March:

Determine (a) the manufacturing margin, (b) the contribution margin, and (c) income from operations for Marley Company for the month of March.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 57 في هذه المجموعة.

فتح الحزمة

k this deck

5

Absorption and variable costing income statements

During the first month of operations ended May 31016, Frost Point Fridge Company manufactured 40,000 mini refrigerators, of which 36,000 were sold. Operating data for the month are summarized as follows:

Instructions

1. Prepare an income statement based on the absorption costing concept.

2. Prepare an income statement based on the variable costing concept.

3. Explain the reason for the difference in the amount of income from operations reported in (1) and (2).