Deck 21: Assurance, Attestation, and Internal Auditing Services

ملء الشاشة (f)

سؤال

سؤال

سؤال

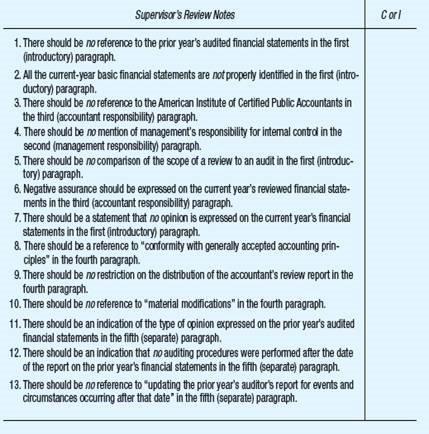

This question consists of 13 items pertaining to possible deficiencies in an accountant's review report. Select the best answer for each item. Indicate your answers in the space provided.

Jordan Stone, CPAs, audited the financial statements of Tech Company, a non-public entity, for the year ended December 31, 2012, and expressed an unmodified opinion. For the year ended December 31, 2013, Tech issued comparative financial statements. Jordan Stone reviewed Tech's 2013 financial statements, and Kent, an assistant on the engagement, drafted the following accountant's review report. Land, the engagement supervisor, decided not to reissue the prior year's auditor's report but instructed Kent to include a separate paragraph in the current year's review report describing the responsibility assumed for the prior year's audited financial statements. This is an appropriate reporting procedure.

Land reviewed Kent's draft and indicated in the supervisor's review notes (shown following the accountant's review report) that there were several deficiencies in Kent's draft.

Accountant ' s Review Report

We have reviewed the accompanying balance sheet of Tech Company as of December 31, 2013 and 2012, and the related statements of income, retained earnings, and cash flows for the year then ended. A review includes primarily applying analytical procedures to management's financial data and making inquiries of company management. A review is substantially less in scope than an audit, the objective of which is the expression of an opinion regarding the financial statements as a whole.

Management is responsible for the preparation and fair presentation of the financial statements in accordance with accounting principles generally accepted in the United States of America and for designing, implementing, and maintaining internal control relevant to the preparation and fair presentation of the financial statements.

Our responsibility is to conduct the review in accordance with Statements on Standards for Accounting and Review Services issued by the American Institute of Certified Public Accountants. Those standards require us to perform procedures to obtain limited assurance that there are no material modifications that should be made to the financial statements. We believe that the results of our procedures provide a reasonable basis for our report.

Based on our review, we are not aware of any material modifications that should be made to the accompanying financial statements. Because of the inherent limitations of a review engagement, this report is intended for the information of management and should not be used for any other purpose.

The financial statements for the year ended December 31, 2012, were audited by us, and our report was dated March 2, 2013. We have no responsibility for updating that report for events and circumstances occurring after that date.

Required:

Items 1 through 13 represent deficiencies noted by Land. For each deficiency, indicate whether Land is correct (C) or incorrect (I) in the criticism of Kent's draft.

(AICPA, adapted)

Jordan Stone, CPAs, audited the financial statements of Tech Company, a non-public entity, for the year ended December 31, 2012, and expressed an unmodified opinion. For the year ended December 31, 2013, Tech issued comparative financial statements. Jordan Stone reviewed Tech's 2013 financial statements, and Kent, an assistant on the engagement, drafted the following accountant's review report. Land, the engagement supervisor, decided not to reissue the prior year's auditor's report but instructed Kent to include a separate paragraph in the current year's review report describing the responsibility assumed for the prior year's audited financial statements. This is an appropriate reporting procedure.

Land reviewed Kent's draft and indicated in the supervisor's review notes (shown following the accountant's review report) that there were several deficiencies in Kent's draft.

Accountant ' s Review Report

We have reviewed the accompanying balance sheet of Tech Company as of December 31, 2013 and 2012, and the related statements of income, retained earnings, and cash flows for the year then ended. A review includes primarily applying analytical procedures to management's financial data and making inquiries of company management. A review is substantially less in scope than an audit, the objective of which is the expression of an opinion regarding the financial statements as a whole.

Management is responsible for the preparation and fair presentation of the financial statements in accordance with accounting principles generally accepted in the United States of America and for designing, implementing, and maintaining internal control relevant to the preparation and fair presentation of the financial statements.

Our responsibility is to conduct the review in accordance with Statements on Standards for Accounting and Review Services issued by the American Institute of Certified Public Accountants. Those standards require us to perform procedures to obtain limited assurance that there are no material modifications that should be made to the financial statements. We believe that the results of our procedures provide a reasonable basis for our report.

Based on our review, we are not aware of any material modifications that should be made to the accompanying financial statements. Because of the inherent limitations of a review engagement, this report is intended for the information of management and should not be used for any other purpose.

The financial statements for the year ended December 31, 2012, were audited by us, and our report was dated March 2, 2013. We have no responsibility for updating that report for events and circumstances occurring after that date.

Required:

Items 1 through 13 represent deficiencies noted by Land. For each deficiency, indicate whether Land is correct (C) or incorrect (I) in the criticism of Kent's draft.

(AICPA, adapted)

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

فتح الحزمة

قم بالتسجيل لفتح البطاقات في هذه المجموعة!

Unlock Deck

Unlock Deck

1/42

العب

ملء الشاشة (f)

Deck 21: Assurance, Attestation, and Internal Auditing Services

1

Define an attest engagement. List the two conditions that are necessary, according to the third general standard for attestation engagements, in order to perform an attest engagement.

Attest Engagements

Attest engagement is an engagement where a practitioner expresses his view in the form of a report over the evaluation, recognition, and presentation of a subject matter or the financial statements prepared by the management against the International Financial Reporting Standards (IFRS).

The two conditions that are necessary, according to the third general standard for attestation engagements, in order to perform an attest engagement are:

• The practitioner must identify the financial statements that are reported or the assertions made, and state the nature of the engagement in the report.

• The practitioner must state his findings in the report while evaluating the financial statements or the financial assertions against the criteria of International Financial Reporting Standards (IFRS).

Attest engagement is an engagement where a practitioner expresses his view in the form of a report over the evaluation, recognition, and presentation of a subject matter or the financial statements prepared by the management against the International Financial Reporting Standards (IFRS).

The two conditions that are necessary, according to the third general standard for attestation engagements, in order to perform an attest engagement are:

• The practitioner must identify the financial statements that are reported or the assertions made, and state the nature of the engagement in the report.

• The practitioner must state his findings in the report while evaluating the financial statements or the financial assertions against the criteria of International Financial Reporting Standards (IFRS).

2

Which of the following statements concerning prospective financial statements is correct?

A) Only a financial forecast would normally be appropriate for limited use.

B) Only a financial projection would normally be appropriate for general use.

C) Any type of prospective financial statement would normally be appropriate for limited use.

D) Any type of prospective financial statement would normally be appropriate for general use.

A) Only a financial forecast would normally be appropriate for limited use.

B) Only a financial projection would normally be appropriate for general use.

C) Any type of prospective financial statement would normally be appropriate for limited use.

D) Any type of prospective financial statement would normally be appropriate for general use.

(C) Any type of prospective financial statement would normally be appropriate for limited use.

Justification :

There are two types of prospective financial statements; they are financial forecasts and financial projections. The users of financial forecasts and financial projections cannot question the responsible party for any hypothetical assumptions based on expected results. Hence, any type of prospective financial statement would normally be appropriate for limited use.

Justification :

There are two types of prospective financial statements; they are financial forecasts and financial projections. The users of financial forecasts and financial projections cannot question the responsible party for any hypothetical assumptions based on expected results. Hence, any type of prospective financial statement would normally be appropriate for limited use.

3

This question consists of 13 items pertaining to possible deficiencies in an accountant's review report. Select the best answer for each item. Indicate your answers in the space provided.

Jordan Stone, CPAs, audited the financial statements of Tech Company, a non-public entity, for the year ended December 31, 2012, and expressed an unmodified opinion. For the year ended December 31, 2013, Tech issued comparative financial statements. Jordan Stone reviewed Tech's 2013 financial statements, and Kent, an assistant on the engagement, drafted the following accountant's review report. Land, the engagement supervisor, decided not to reissue the prior year's auditor's report but instructed Kent to include a separate paragraph in the current year's review report describing the responsibility assumed for the prior year's audited financial statements. This is an appropriate reporting procedure.

Land reviewed Kent's draft and indicated in the supervisor's review notes (shown following the accountant's review report) that there were several deficiencies in Kent's draft.

Accountant ' s Review Report

We have reviewed the accompanying balance sheet of Tech Company as of December 31, 2013 and 2012, and the related statements of income, retained earnings, and cash flows for the year then ended. A review includes primarily applying analytical procedures to management's financial data and making inquiries of company management. A review is substantially less in scope than an audit, the objective of which is the expression of an opinion regarding the financial statements as a whole.

Management is responsible for the preparation and fair presentation of the financial statements in accordance with accounting principles generally accepted in the United States of America and for designing, implementing, and maintaining internal control relevant to the preparation and fair presentation of the financial statements.

Our responsibility is to conduct the review in accordance with Statements on Standards for Accounting and Review Services issued by the American Institute of Certified Public Accountants. Those standards require us to perform procedures to obtain limited assurance that there are no material modifications that should be made to the financial statements. We believe that the results of our procedures provide a reasonable basis for our report.

Based on our review, we are not aware of any material modifications that should be made to the accompanying financial statements. Because of the inherent limitations of a review engagement, this report is intended for the information of management and should not be used for any other purpose.

The financial statements for the year ended December 31, 2012, were audited by us, and our report was dated March 2, 2013. We have no responsibility for updating that report for events and circumstances occurring after that date.

Required:

Items 1 through 13 represent deficiencies noted by Land. For each deficiency, indicate whether Land is correct (C) or incorrect (I) in the criticism of Kent's draft.

(AICPA, adapted)

Jordan Stone, CPAs, audited the financial statements of Tech Company, a non-public entity, for the year ended December 31, 2012, and expressed an unmodified opinion. For the year ended December 31, 2013, Tech issued comparative financial statements. Jordan Stone reviewed Tech's 2013 financial statements, and Kent, an assistant on the engagement, drafted the following accountant's review report. Land, the engagement supervisor, decided not to reissue the prior year's auditor's report but instructed Kent to include a separate paragraph in the current year's review report describing the responsibility assumed for the prior year's audited financial statements. This is an appropriate reporting procedure.

Land reviewed Kent's draft and indicated in the supervisor's review notes (shown following the accountant's review report) that there were several deficiencies in Kent's draft.

Accountant ' s Review Report

We have reviewed the accompanying balance sheet of Tech Company as of December 31, 2013 and 2012, and the related statements of income, retained earnings, and cash flows for the year then ended. A review includes primarily applying analytical procedures to management's financial data and making inquiries of company management. A review is substantially less in scope than an audit, the objective of which is the expression of an opinion regarding the financial statements as a whole.

Management is responsible for the preparation and fair presentation of the financial statements in accordance with accounting principles generally accepted in the United States of America and for designing, implementing, and maintaining internal control relevant to the preparation and fair presentation of the financial statements.

Our responsibility is to conduct the review in accordance with Statements on Standards for Accounting and Review Services issued by the American Institute of Certified Public Accountants. Those standards require us to perform procedures to obtain limited assurance that there are no material modifications that should be made to the financial statements. We believe that the results of our procedures provide a reasonable basis for our report.

Based on our review, we are not aware of any material modifications that should be made to the accompanying financial statements. Because of the inherent limitations of a review engagement, this report is intended for the information of management and should not be used for any other purpose.

The financial statements for the year ended December 31, 2012, were audited by us, and our report was dated March 2, 2013. We have no responsibility for updating that report for events and circumstances occurring after that date.

Required:

Items 1 through 13 represent deficiencies noted by Land. For each deficiency, indicate whether Land is correct (C) or incorrect (I) in the criticism of Kent's draft.

(AICPA, adapted)

not answer

4

What types of engagements can be provided under the attestation standards? Give two examples of attestation engagements.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 42 في هذه المجموعة.

فتح الحزمة

k this deck

5

When compiling the financial statements of a non-public entity, an accountant should

A) Review agreements with financial institutions for restrictions on cash balances.

B) Understand the accounting principles and practices of the entity's industry.

C) Inquire of key personnel concerning related parties and subsequent events.

D) Perform ratio analyses of the financial data of comparable prior periods.

A) Review agreements with financial institutions for restrictions on cash balances.

B) Understand the accounting principles and practices of the entity's industry.

C) Inquire of key personnel concerning related parties and subsequent events.

D) Perform ratio analyses of the financial data of comparable prior periods.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 42 في هذه المجموعة.

فتح الحزمة

k this deck

6

Rhett Corporation, a local sporting goods company, has asked your firm for assistance in setting up its website. Eric Rhett, the CEO, is concerned that potential customers will be reluctant to place orders over the Internet to a relatively unknown entity. He recently heard about companies finding ways to provide assurance to customers about secure websites, and Rhett has asked to meet with you about this issue.

Required:

Prepare answers to each of the following questions that may be asked by Rhett.

a. Why are customers reluctant to engage in e-commerce?

b. What type of assurance can your firm provide to his customers concerning the company's website?

c. What process will your firm follow in providing a WebTrust assurance service for Rhett's website?

Required:

Prepare answers to each of the following questions that may be asked by Rhett.

a. Why are customers reluctant to engage in e-commerce?

b. What type of assurance can your firm provide to his customers concerning the company's website?

c. What process will your firm follow in providing a WebTrust assurance service for Rhett's website?

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 42 في هذه المجموعة.

فتح الحزمة

k this deck

7

How can the practitioner satisfy the requirement that specified users take responsibility for the adequacy of procedures performed on an agreed-upon procedures engagement?

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 42 في هذه المجموعة.

فتح الحزمة

k this deck

8

Which of the following statements is correct concerning both an engagement to compile and an engagement to review a non-public entity's financial statements?

A) The accountant is not required to obtain an understanding of internal control.

B) The accountant must be independent in fact and appearance.

C) The accountant expresses no assurance on the financial statements.

D) The accountant should obtain a written management representation letter.

A) The accountant is not required to obtain an understanding of internal control.

B) The accountant must be independent in fact and appearance.

C) The accountant expresses no assurance on the financial statements.

D) The accountant should obtain a written management representation letter.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 42 في هذه المجموعة.

فتح الحزمة

k this deck

9

Beachwood Sparks Company, a non-public company that supplies apparel to retail stores, recently has implemented a new information system. However, during system development and implementation, the company experienced a great deal of turnover in personnel involved with designing and implementing the system. Consequently, the company's board of directors is concerned about whether the system is reliable. It has heard of an assurance service called SysTrust but would like to know more about it before discussing it with its CPA firm.

Required:

a. What types of assurances does a SysTrust examination provide? What are the main principles underlying a reliable system that a SysTrust examination considers?

b. What special skills does a CPA undertaking a SysTrust examination require?

c. Beachwood's board of directors is wondering whether any of its constituents would be interested in the SysTrust report. For example, the company is interested in renewing its business interruption insurance, winning business from new retailers, and making itself attractive as a takeover target. Describe how an unqualified SysTrust report would benefit Beachwood from the point of view of the insurance company, potential customers, and potential buyers of the company. ( Hint: Examine the SysTrust principles and underlying criteria perhaps by obtaining SysTrust documentation available on the CICA website, www.webtrust.org, specifically considering which principles and criteria would be of interest to each of the three constituents.)

Required:

a. What types of assurances does a SysTrust examination provide? What are the main principles underlying a reliable system that a SysTrust examination considers?

b. What special skills does a CPA undertaking a SysTrust examination require?

c. Beachwood's board of directors is wondering whether any of its constituents would be interested in the SysTrust report. For example, the company is interested in renewing its business interruption insurance, winning business from new retailers, and making itself attractive as a takeover target. Describe how an unqualified SysTrust report would benefit Beachwood from the point of view of the insurance company, potential customers, and potential buyers of the company. ( Hint: Examine the SysTrust principles and underlying criteria perhaps by obtaining SysTrust documentation available on the CICA website, www.webtrust.org, specifically considering which principles and criteria would be of interest to each of the three constituents.)

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 42 في هذه المجموعة.

فتح الحزمة

k this deck

10

What kind of entity might request an attestation report on internal control, and why?

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 42 في هذه المجموعة.

فتح الحزمة

k this deck

11

The standard report issued by an accountant after reviewing the financial statements of a non-public entity states that

A) A review includes assessing the accounting principles used and significant estimates made by management.

B) A review includes examining, on a test basis, evidence supporting the amounts and disclosures in the financial statements.

C) The accountant is not aware of any material modifications that should be made to the financial statements.

D) The accountant does not express an opinion or any other form of assurance on the financial statements.

A) A review includes assessing the accounting principles used and significant estimates made by management.

B) A review includes examining, on a test basis, evidence supporting the amounts and disclosures in the financial statements.

C) The accountant is not aware of any material modifications that should be made to the financial statements.

D) The accountant does not express an opinion or any other form of assurance on the financial statements.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 42 في هذه المجموعة.

فتح الحزمة

k this deck

12

Mr. and Mrs. Greg Jun called your firm, Hillison Reimer, in response to a brochure they received from Greg's elderly mother. The Juns reside in Ann Arbor, Michigan, while Greg's mother has retired to Tallahassee, Florida. In recent months, the Juns have become very concerned about Greg's mother and her ability to care for herself. On a number of occasions, Greg has received calls from his mother's friends expressing concern that she has not been eating properly and is not regularly taking her medicine for a heart condition.

Required:

a. Describe the PrimePlus service to the Juns, including the types of services that can be offered.

b. Because the Juns' concerns do not relate to areas of your expertise as a CPA, explain to them how you will be able to provide assurance on the care providers.

Required:

a. Describe the PrimePlus service to the Juns, including the types of services that can be offered.

b. Because the Juns' concerns do not relate to areas of your expertise as a CPA, explain to them how you will be able to provide assurance on the care providers.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 42 في هذه المجموعة.

فتح الحزمة

k this deck

13

What are the two types of prospective financial statements? How do they differ from each other?

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 42 في هذه المجموعة.

فتح الحزمة

k this deck

14

Financial statements of a non-public entity that have been reviewed by an accountant should be accompanied by a report stating that

A) The scope of the inquiry and the analytical procedures performed by the accountant have not been restricted.

B) All information included in the financial statements is the representation of the management of the entity.

C) A review includes examining, on a test basis, evidence supporting the amounts and disclosures in the financial statements.

D) A review is greater in scope than a compilation, the objective of which is to present financial statements that are free of material misstatements.

A) The scope of the inquiry and the analytical procedures performed by the accountant have not been restricted.

B) All information included in the financial statements is the representation of the management of the entity.

C) A review includes examining, on a test basis, evidence supporting the amounts and disclosures in the financial statements.

D) A review is greater in scope than a compilation, the objective of which is to present financial statements that are free of material misstatements.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 42 في هذه المجموعة.

فتح الحزمة

k this deck

15

The accounting profession is concerned about whether companies are in compliance with various federal and state environmental laws and regulations and whether they have reported environmental liabilities in their financial statements. Environmental auditing typically refers to the process of assessing compliance with environmental laws and regulations, as well as compliance with company policies and procedures. AT Section 601, "Compliance Attestation," allows a practitioner to perform agreed-upon procedures to assist users in evaluating management's written assertions about (1) the entity's compliance with specified requirements, (2) the effectiveness of the entity's internal control over compliance, or (3) both.

Required:

a. Discuss how a practitioner would conduct an agreed-upon procedures engagement to evaluate an entity's written assertion that it was in compliance with its state's environmental laws and regulations.

b. Assume that this same entity maintained an internal control system that monitored the entity's compliance with its state's environmental laws and regulations. Discuss how a practitioner would evaluate the effectiveness of the entity's internal control over compliance.

Required:

a. Discuss how a practitioner would conduct an agreed-upon procedures engagement to evaluate an entity's written assertion that it was in compliance with its state's environmental laws and regulations.

b. Assume that this same entity maintained an internal control system that monitored the entity's compliance with its state's environmental laws and regulations. Discuss how a practitioner would evaluate the effectiveness of the entity's internal control over compliance.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 42 في هذه المجموعة.

فتح الحزمة

k this deck

16

What types of services can be performed under Statements on Standards for Accounting and Review Services?

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 42 في هذه المجموعة.

فتح الحزمة

k this deck

17

The general accreditation granted by the Institute of Internal Auditors is known as the

A) CFE.

B) CGAP.

C) CFSA.

D) CIA.

A) CFE.

B) CGAP.

C) CFSA.

D) CIA.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 42 في هذه المجموعة.

فتح الحزمة

k this deck

18

The IIA maintains its own website containing useful information about the Institute and the internal auditing profession in general. Visit the IIA's home page (www.theiia.org).

Required:

a. Under the tab "Periodicals," follow the link to the official magazine of the IIA ( Internal Auditor ). What is the mission of this respected publication?

b. Although the IIA does not require that its members obtain CIA certification, it is becoming popular worldwide. What advantages are afforded to those who certify, according to the IIA's website? Who might benefit from the CIA designation?

Required:

a. Under the tab "Periodicals," follow the link to the official magazine of the IIA ( Internal Auditor ). What is the mission of this respected publication?

b. Although the IIA does not require that its members obtain CIA certification, it is becoming popular worldwide. What advantages are afforded to those who certify, according to the IIA's website? Who might benefit from the CIA designation?

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 42 في هذه المجموعة.

فتح الحزمة

k this deck

19

What type of knowledge must an accountant possess about the entity in order to perform a compilation engagement? A review engagement?

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 42 في هذه المجموعة.

فتح الحزمة

k this deck

20

Which of the following is not one of the general areas of the IIA's International Standards for the Professional Practice of Internal Auditing?

A) Performance standards.

B) Implementation standards.

C) Ethical standards.

D) Attribute standards.

A) Performance standards.

B) Implementation standards.

C) Ethical standards.

D) Attribute standards.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 42 في هذه المجموعة.

فتح الحزمة

k this deck

21

The AICPA has developed an assurance service related to electronic commerce called WebTrust. Visit the WebTrust home page (www.webtrust.org) and examine the WebTrust seal.

Required:

a. Under the overview of Trust Services section, find and list the four broad areas that the Trust Service principles are organized into.

b. On that same page, there is a heading: "Need for Trust." List two reasons given in that section for why trust in online transactions is an issue today.

Required:

a. Under the overview of Trust Services section, find and list the four broad areas that the Trust Service principles are organized into.

b. On that same page, there is a heading: "Need for Trust." List two reasons given in that section for why trust in online transactions is an issue today.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 42 في هذه المجموعة.

فتح الحزمة

k this deck

22

Define corporate governance. Why do you think an effective internal audit function is referred to as one of the cornerstones of corporate governance?

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 42 في هذه المجموعة.

فتح الحزمة

k this deck

23

The four principles of the IIA Code of Ethics are

A) Confidentiality, competency, objectivity, and integrity.

B) Objectivity, independence, compliance, and due diligence.

C) Honesty, integrity, independence, and competency.

D) Integrity, confidentiality, independence, and compliance.

A) Confidentiality, competency, objectivity, and integrity.

B) Objectivity, independence, compliance, and due diligence.

C) Honesty, integrity, independence, and competency.

D) Integrity, confidentiality, independence, and compliance.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 42 في هذه المجموعة.

فتح الحزمة

k this deck

24

EarthWear has a number of competitors that sell goods over the Internet. Visit the home page for any two of EarthWear's competitors. For example, visit the home page for Timberland (www.timberland.com), L.L. Bean (www.llbean.com), or Lands' End (www.landsend.com).

Required:

a. Determine if any of the sites provides any type of assurance on its electronic commerce. Note that you may have to prepare to order a product before any assurances are presented on the site. (You may need to go into tools, properties, or page info in your browser to look for the certificates.)

b. If any of the sites provides assurance on electronic commerce, compare the assurances provided with the Trust Services principles and criteria.

Required:

a. Determine if any of the sites provides any type of assurance on its electronic commerce. Note that you may have to prepare to order a product before any assurances are presented on the site. (You may need to go into tools, properties, or page info in your browser to look for the certificates.)

b. If any of the sites provides assurance on electronic commerce, compare the assurances provided with the Trust Services principles and criteria.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 42 في هذه المجموعة.

فتح الحزمة

k this deck

25

Explain how internal auditors play a role in helping management comply with the requirements of the Sarbanes-Oxley Act of 2002.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 42 في هذه المجموعة.

فتح الحزمة

k this deck

26

Which of the following is not a Trust Services principle?

A) Processing integrity.

B) Online privacy.

C) Digital certificate authorization.

D) Availability.

A) Processing integrity.

B) Online privacy.

C) Digital certificate authorization.

D) Availability.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 42 في هذه المجموعة.

فتح الحزمة

k this deck

27

Using an Internet search engine, find the web page on PrimePlus services created by the AICPA. On the website, find the PrimePlus/ElderCare glossary.

Required:

Describe the "funeral rule" defined in the glossary.

Required:

Describe the "funeral rule" defined in the glossary.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 42 في هذه المجموعة.

فتح الحزمة

k this deck

28

The Elliott Committee developed six assurance services with significant market potential for CPA firms. What are these six services?

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 42 في هذه المجموعة.

فتح الحزمة

k this deck

29

Which of the following assurances is not provided by an unqualified opinion on a Type 2 SysTrust report?

A) There are procedures to protect the system against unauthorized physical access.

B) The financial statements created by the system are free of material misstatements.

C) The documented system availability objectives, policies, and standards have been communicated to authorized users and controls are functioning as documented.

D) Documented system processing integrity objectives, policies, and standards have been communicated to authorized users and controls are functioning as documented.

A) There are procedures to protect the system against unauthorized physical access.

B) The financial statements created by the system are free of material misstatements.

C) The documented system availability objectives, policies, and standards have been communicated to authorized users and controls are functioning as documented.

D) Documented system processing integrity objectives, policies, and standards have been communicated to authorized users and controls are functioning as documented.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 42 في هذه المجموعة.

فتح الحزمة

k this deck

30

What are the risks of electronic commerce? What are the Trust Services Principles?

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 42 في هذه المجموعة.

فتح الحزمة

k this deck

31

PrimePlus engagements are mainly designed to

A) Provide guidance to assisted-living care facilities to enhance quality of life for the elderly.

B) Provide guidance to health care providers in giving high-quality health care.

C) Assist the elderly to maintain their financial independence and desired lifestyle as they age.

D) Assist the elderly in perfecting their shuffleboard techniques.

A) Provide guidance to assisted-living care facilities to enhance quality of life for the elderly.

B) Provide guidance to health care providers in giving high-quality health care.

C) Assist the elderly to maintain their financial independence and desired lifestyle as they age.

D) Assist the elderly in perfecting their shuffleboard techniques.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 42 في هذه المجموعة.

فتح الحزمة

k this deck

32

What is the main difference between WebTrust and SysTrust Services?

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 42 في هذه المجموعة.

فتح الحزمة

k this deck

33

Which of the following is not a type of PrimePlus service?

A) Assurance services.

B) Consulting/facilitating services.

C) Direct services.

D) Systems design services.

A) Assurance services.

B) Consulting/facilitating services.

C) Direct services.

D) Systems design services.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 42 في هذه المجموعة.

فتح الحزمة

k this deck

34

Why is PrimePlus potentially a major service for CPA firms? What types of PrimePlus services can a practitioner offer?

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 42 في هذه المجموعة.

فتح الحزمة

k this deck

35

Orange Grove Farms has approached your CPA firm with some questions. Orange Grove's management has spoken with a bank about obtaining a loan to expand its operations. The bank has informed Orange Grove that the bank will not make the requested loan unless the company submits financial statements. Further, the interest rate on the loan will depend on whether Orange Grove's financial statements are compiled, reviewed, or audited by an independent auditor. Orange Grove's management is not familiar with the differences between these three services and wonders why the interest rate charged on the loan would depend on the type of service they obtain from your CPA firm.

Required:

Describe for Orange Grove the differences between compilation, review, and audit engagements. Be sure to include the level of assurance provided by each one as part of your explanation.

Required:

Describe for Orange Grove the differences between compilation, review, and audit engagements. Be sure to include the level of assurance provided by each one as part of your explanation.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 42 في هذه المجموعة.

فتح الحزمة

k this deck

36

An assurance report on information can provide assurance about the information's

A) Reliability.

B) Relevance.

C) Timeliness.

D) All of the above.

A) Reliability.

B) Relevance.

C) Timeliness.

D) All of the above.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 42 في هذه المجموعة.

فتح الحزمة

k this deck

37

Your client, Cheaney Rental Properties, has engaged you to perform a compilation of its forecasted financial statements for a loan with the National Bank of Rockwood.

Required:

a. Describe the steps an accountant should complete when conducting a compilation of prospective financial statements.

b. Prepare a standard compilation report for Cheaney Rental Properties.

Required:

a. Describe the steps an accountant should complete when conducting a compilation of prospective financial statements.

b. Prepare a standard compilation report for Cheaney Rental Properties.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 42 في هذه المجموعة.

فتح الحزمة

k this deck

38

Which of the following professional services would be considered an attest engagement?

A) A management consulting engagement to provide IT advice to a client.

B) An engagement to report on compliance with statutory requirements.

C) An income tax engagement to prepare federal and state tax returns.

D) Compilation of financial statements from a client's accounting records.

A) A management consulting engagement to provide IT advice to a client.

B) An engagement to report on compliance with statutory requirements.

C) An income tax engagement to prepare federal and state tax returns.

D) Compilation of financial statements from a client's accounting records.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 42 في هذه المجموعة.

فتح الحزمة

k this deck

39

You are the manager of the examination engagement of the financial projection of Honey's Health Foods as of December 31, 2013, and for the year then ended. The audit senior, Currie, has prepared the following draft of the examination report:

To the Board of Directors of Honey's Health Foods:

We have examined the accompanying projected balance sheet and statements of income, retained earnings, and cash flows of Honey's Health Foods as of December 31, 2013, and for the year then ending. Our examination was made in accordance with standards for an examination of a projection and accordingly included such procedures as we considered necessary to evaluate the assumptions used by management.

In our opinion, the accompanying forecast is presented in conformity with guidelines for presentation of a forecast established by the American Institute of Certified Public Accountants, and the underlying assumptions provide a reasonable basis for management's projection. However, there will usually be differences between the projected and actual results because events and circumstances frequently do not occur as expected, and those differences may be material.

Libby Nelson, CPAs

Required:

Identify the deficiencies in Currie's draft of the examination report. Group the deficiencies by paragraph.

To the Board of Directors of Honey's Health Foods:

We have examined the accompanying projected balance sheet and statements of income, retained earnings, and cash flows of Honey's Health Foods as of December 31, 2013, and for the year then ending. Our examination was made in accordance with standards for an examination of a projection and accordingly included such procedures as we considered necessary to evaluate the assumptions used by management.

In our opinion, the accompanying forecast is presented in conformity with guidelines for presentation of a forecast established by the American Institute of Certified Public Accountants, and the underlying assumptions provide a reasonable basis for management's projection. However, there will usually be differences between the projected and actual results because events and circumstances frequently do not occur as expected, and those differences may be material.

Libby Nelson, CPAs

Required:

Identify the deficiencies in Currie's draft of the examination report. Group the deficiencies by paragraph.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 42 في هذه المجموعة.

فتح الحزمة

k this deck

40

Define assurance services. Discuss why the definition focuses on decision making and information.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 42 في هذه المجموعة.

فتح الحزمة

k this deck

41

An accountant may accept an engagement to apply agreed-upon procedures to prospective financial statements, provided that

A) The prospective financial statements are also examined.

B) Responsibility for the adequacy of the procedures performed is taken by the accountant.

C) Negative assurance is expressed on the prospective financial statements taken as a whole.

D) Distribution of the report is restricted to the specified users.

A) The prospective financial statements are also examined.

B) Responsibility for the adequacy of the procedures performed is taken by the accountant.

C) Negative assurance is expressed on the prospective financial statements taken as a whole.

D) Distribution of the report is restricted to the specified users.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 42 في هذه المجموعة.

فتح الحزمة

k this deck

42

The following report was drafted on October 25, 2013, by Major, CPA, at the completion of an engagement to compile the financial statements of Ajax Company for the year ended September 30, 2013. Ajax is a non-public entity in which Major's child has a material direct financial interest. Ajax decided to omit substantially all of the disclosures required by generally accepted accounting principles because the financial statements will be for management's use only. The statement of cash flows was also omitted because management does not believe it to be a useful financial statement.

To the Board of Directors of Ajax Company:

I have compiled the accompanying financial statements of Ajax Company as of December 31, 2013, and for the year then ended. I planned and performed the compilation to obtain limited assurance about whether the financial statements are free of material misstatements.

Management is responsible for the preparation and fair presentation of the financial statements in accordance with accounting principles generally accepted in the United States of America and for designing, implementing, and maintaining internal control relevant to the preparation and fair presentation of the financial statements.

My responsibility is to conduct the compilation in accordance with Statements on Standards for Accounting and Review Services issued by the American Institute of Certified Public Accountants. It is substantially less in scope than an audit in accordance with generally accepted auditing standards, the objective of which is the expression of an opinion regarding the financial statements taken as a whole. I have not audited the accompanying financial statements and, accordingly, do not express any opinion on them.

Management has elected to omit substantially all of the disclosures required by accounting principles generally accepted in the United States of America. If the omitted disclosures were included in the financial statements, they might influence the user's conclusions about the company's financial position, results of operations, and cash flows.

I am not independent with respect to Ajax Company. This lack of independence is due to my daughter's ownership of a material direct financial interest in Ajax Company.

This report is intended solely for the information and use of the board of directors and management of Ajax Company and should not be used for any other purpose.

Major, CPA

Required:

Identify the deficiencies contained in Major's report on the compiled financial statements. Group the deficiencies by paragraph where applicable. Do not redraft the report.

(AICPA, adapted)

To the Board of Directors of Ajax Company:

I have compiled the accompanying financial statements of Ajax Company as of December 31, 2013, and for the year then ended. I planned and performed the compilation to obtain limited assurance about whether the financial statements are free of material misstatements.

Management is responsible for the preparation and fair presentation of the financial statements in accordance with accounting principles generally accepted in the United States of America and for designing, implementing, and maintaining internal control relevant to the preparation and fair presentation of the financial statements.

My responsibility is to conduct the compilation in accordance with Statements on Standards for Accounting and Review Services issued by the American Institute of Certified Public Accountants. It is substantially less in scope than an audit in accordance with generally accepted auditing standards, the objective of which is the expression of an opinion regarding the financial statements taken as a whole. I have not audited the accompanying financial statements and, accordingly, do not express any opinion on them.

Management has elected to omit substantially all of the disclosures required by accounting principles generally accepted in the United States of America. If the omitted disclosures were included in the financial statements, they might influence the user's conclusions about the company's financial position, results of operations, and cash flows.

I am not independent with respect to Ajax Company. This lack of independence is due to my daughter's ownership of a material direct financial interest in Ajax Company.

This report is intended solely for the information and use of the board of directors and management of Ajax Company and should not be used for any other purpose.

Major, CPA

Required:

Identify the deficiencies contained in Major's report on the compiled financial statements. Group the deficiencies by paragraph where applicable. Do not redraft the report.

(AICPA, adapted)

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 42 في هذه المجموعة.

فتح الحزمة

k this deck

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 42 في هذه المجموعة.