Deck 14: Audit of the Inventory and Distribution Cycle

ملء الشاشة (f)

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

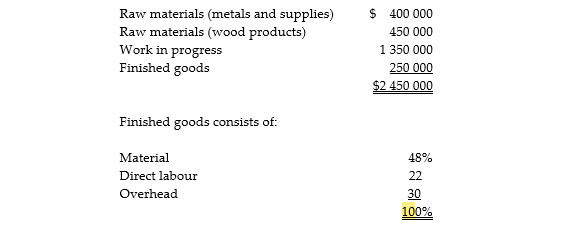

You are conducting the audit of Files R Us Inc.(FRI),a family-owned business that manufactures a variety of different wooden and metal file cabinets.In business for over twenty years,FRI has a reputation for providing high-quality products on time or even ahead of schedule.FRI does not sell to the public,but only to fine furniture stores and to a variety of office supply chains.

As of the current year-end,the company has a total of $6.3 million in assets.Inventory information is as follows:

File cabinet production is intensely competitive,primarily due to imports from Asia and Mexico.To help manage costs,FRI uses a job-order,standard cost system.Standard costs are assessed quarterly.Each job is costed and compared to standard.Inventory is counted only at the end of the year.There is no perpetual inventory system.

Due to problems with raw material quality and new staff,losses have been incurred in the last six months of the year.Your review of last year's audit file indicated that there were numerous inventory adjustments required last year.

Required:

Using the audit risk model,assess the risks associated with the audit of inventory.

As of the current year-end,the company has a total of $6.3 million in assets.Inventory information is as follows:

File cabinet production is intensely competitive,primarily due to imports from Asia and Mexico.To help manage costs,FRI uses a job-order,standard cost system.Standard costs are assessed quarterly.Each job is costed and compared to standard.Inventory is counted only at the end of the year.There is no perpetual inventory system.

Due to problems with raw material quality and new staff,losses have been incurred in the last six months of the year.Your review of last year's audit file indicated that there were numerous inventory adjustments required last year.

Required:

Using the audit risk model,assess the risks associated with the audit of inventory.

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

فتح الحزمة

قم بالتسجيل لفتح البطاقات في هذه المجموعة!

Unlock Deck

Unlock Deck

1/75

العب

ملء الشاشة (f)

Deck 14: Audit of the Inventory and Distribution Cycle

1

What are the factors that increase inherent risks for the accounts within the inventory cycle?

Factors that increase inherent risks for the accounts within the inventory cycle are:1)Inventory is often stored in different locations,which makes physical control and counting difficult.

2)Inventory is easily transportable,is easy to steal,and may be hard to access.

3)Inventory that consists of items such as jewels,chemicals,and electronic parts is often difficult for the auditor to observe and value.In these circumstances,the auditor may need specialist assistance for both counting and valuation.

4)The industry is categorized by rapid and significant technological innovation,which increases the risk of obsolescence.

5)Customer returns are frequent,which causes accuracy,timing,and cutoff issues with recording of the physical return and the corresponding credit in sales.Poor quality client return processes will result in the need for increased audit tests.

6)There are several acceptable inventory valuation methods under ASPE and IFRS,which the auditor must determine have been applied consistently from year to year.

2)Inventory is easily transportable,is easy to steal,and may be hard to access.

3)Inventory that consists of items such as jewels,chemicals,and electronic parts is often difficult for the auditor to observe and value.In these circumstances,the auditor may need specialist assistance for both counting and valuation.

4)The industry is categorized by rapid and significant technological innovation,which increases the risk of obsolescence.

5)Customer returns are frequent,which causes accuracy,timing,and cutoff issues with recording of the physical return and the corresponding credit in sales.Poor quality client return processes will result in the need for increased audit tests.

6)There are several acceptable inventory valuation methods under ASPE and IFRS,which the auditor must determine have been applied consistently from year to year.

2

The controls over purchase requisitions and the related purchase orders are evaluated and tested as part of the

A)inventory and distribution cycle.

B)acquisitions and payments cycle.

C)human resources and payroll cycle.

D)capital acquisitions cycle.

A)inventory and distribution cycle.

B)acquisitions and payments cycle.

C)human resources and payroll cycle.

D)capital acquisitions cycle.

B

3

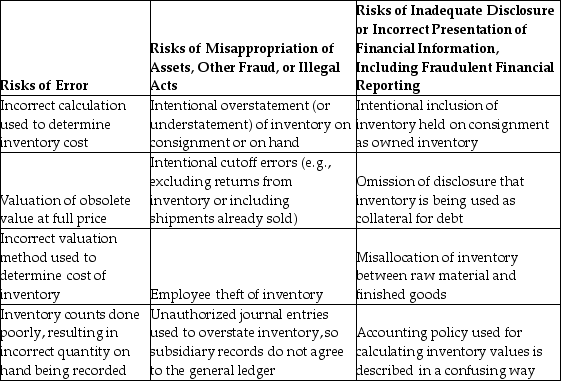

Describe the major risks of error or fraud in the inventory and distribution cycle using the headings of i)risks of error,ii)risks of misappropriation of assets,other fraud,or illegal acts,and iii)risks of inadequate disclosure or incorrect presentation of financial information,including fraudulent financial reporting.

4

The inventory and distribution cycle can be thought of as comprising two separate but closely related systems,one involving the actual physical flow of goods,and the other the

A)internal control over those goods.

B)related costs.

C)storing of the goods.

D)prevention of waste,obsolescence,and theft.

A)internal control over those goods.

B)related costs.

C)storing of the goods.

D)prevention of waste,obsolescence,and theft.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 75 في هذه المجموعة.

فتح الحزمة

k this deck

5

Receipt of ordered materials by the receiving department will generate the completion of a form called the

A)receiving report.

B)materials requisition.

C)bill of lading.

D)inventory acquisition summary.

A)receiving report.

B)materials requisition.

C)bill of lading.

D)inventory acquisition summary.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 75 في هذه المجموعة.

فتح الحزمة

k this deck

6

An auditor has determined that there is a high risk that her client has overvalued inventory.Which audit assertions would require additional testing?

A)accuracy and existence

B)allocation and accuracy

C)accuracy and valuation

D)valuation and classification

A)accuracy and existence

B)allocation and accuracy

C)accuracy and valuation

D)valuation and classification

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 75 في هذه المجموعة.

فتح الحزمة

k this deck

7

Discuss the methodology for designing tests of details of balances for inventory.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 75 في هذه المجموعة.

فتح الحزمة

k this deck

8

Master files,worksheets,and reports that accumulate material,labour,and overhead as the costs are incurred are

A)accounting system controls.

B)storeroom documents.

C)finished goods inventory records.

D)cost accounting records.

A)accounting system controls.

B)storeroom documents.

C)finished goods inventory records.

D)cost accounting records.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 75 في هذه المجموعة.

فتح الحزمة

k this deck

9

The form used to request the purchasing department to place orders for inventory items is the

A)purchase order.

B)purchase requisition.

C)materials requisition.

D)bill of lading.

A)purchase order.

B)purchase requisition.

C)materials requisition.

D)bill of lading.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 75 في هذه المجموعة.

فتح الحزمة

k this deck

10

Shipping of finished goods is an integral part of the

A)acquisitions and payments cycle.

B)inventory and distribution cycle.

C)sales and collections cycle.

D)human resources and payroll cycle.

A)acquisitions and payments cycle.

B)inventory and distribution cycle.

C)sales and collections cycle.

D)human resources and payroll cycle.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 75 في هذه المجموعة.

فتح الحزمة

k this deck

11

When labour is a significant part of inventory,verifying the proper accounting of these costs should be tested in the

A)inventory and distribution cycle.

B)human resources and payroll cycle.

C)acquisitions and payments cycle.

D)cash cycle.

A)inventory and distribution cycle.

B)human resources and payroll cycle.

C)acquisitions and payments cycle.

D)cash cycle.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 75 في هذه المجموعة.

فتح الحزمة

k this deck

12

Obtaining an adequate understanding of the client's business is important in physical observation of inventory because

A)it is required by GAAP.

B)it will help the auditor in assessing the risk of theft of inventory.

C)inventory is normally a significant item.

D)inventory varies significantly for different companies.

A)it is required by GAAP.

B)it will help the auditor in assessing the risk of theft of inventory.

C)inventory is normally a significant item.

D)inventory varies significantly for different companies.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 75 في هذه المجموعة.

فتح الحزمة

k this deck

13

The bias in recording inventory would be toward

A)overstatement.

B)understatement.

C)increasing share price.

D)income smoothing.

A)overstatement.

B)understatement.

C)increasing share price.

D)income smoothing.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 75 في هذه المجموعة.

فتح الحزمة

k this deck

14

Which three cycles is the inventory cycle interconnected with in a manufacturing company?

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 75 في هذه المجموعة.

فتح الحزمة

k this deck

15

State the six functions that make up the inventory and distribution cycle and,for each function,identify the related documents and/or records that would be used by a manufacturing company.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 75 في هذه المجموعة.

فتح الحزمة

k this deck

16

The auditor evaluates the internal transfer of assets and related costs during the

A)acquisition and payments cycle.

B)human resources and payroll cycle.

C)sales and collection cycle.

D)inventory and distribution cycle.

A)acquisition and payments cycle.

B)human resources and payroll cycle.

C)sales and collection cycle.

D)inventory and distribution cycle.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 75 في هذه المجموعة.

فتح الحزمة

k this deck

17

The auditor would like to test the existence and accuracy of the transfer of goods from the raw materials storeroom to the manufacturing assembly lines.Which of the following audit procedures should be used?

A)Conduct a variance analysis of the costs associated with manufacturing,looking for gross profit fluctuations.

B)Account for a sequence of raw material requisitions,examining details and looking for proper approvals.

C)Look at overtime records to determine the amount and timing of overtime hours used in the manufacturing process.

D)Inquire with the inventory custodian regarding procedures used to transfer raw materials to the production line.

A)Conduct a variance analysis of the costs associated with manufacturing,looking for gross profit fluctuations.

B)Account for a sequence of raw material requisitions,examining details and looking for proper approvals.

C)Look at overtime records to determine the amount and timing of overtime hours used in the manufacturing process.

D)Inquire with the inventory custodian regarding procedures used to transfer raw materials to the production line.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 75 في هذه المجموعة.

فتح الحزمة

k this deck

18

The audit of the inventory and distribution cycle consists of five parts.State the five parts and,for each part,identify the cycle in which that part is tested by the auditor.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 75 في هذه المجموعة.

فتح الحزمة

k this deck

19

What are the significant risks relating to the inventory cycle?

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 75 في هذه المجموعة.

فتح الحزمة

k this deck

20

The overall objective in the audit of the inventory and distribution cycle is to determine that

A)costs of goods sold and gross profit are correctly stated on the income statement.

B)inventory items on the balance sheet are neither fraudulent nor materially in error.

C)gross profit and inventory are fairly presented on the financial statements.

D)inventory and cost of goods sold are fairly stated on the financial statements.

A)costs of goods sold and gross profit are correctly stated on the income statement.

B)inventory items on the balance sheet are neither fraudulent nor materially in error.

C)gross profit and inventory are fairly presented on the financial statements.

D)inventory and cost of goods sold are fairly stated on the financial statements.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 75 في هذه المجموعة.

فتح الحزمة

k this deck

21

What are the five distinct activities used during the audit of the inventory cycle?

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 75 في هذه المجموعة.

فتح الحزمة

k this deck

22

Reconciling the open production cost reports to the work-in-process inventory control account is a procedure designed to test the control objective of

A)completeness.

B)accounting.

C)validity.

D)authorization.

A)completeness.

B)accounting.

C)validity.

D)authorization.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 75 في هذه المجموعة.

فتح الحزمة

k this deck

23

You are conducting the audit of Files R Us Inc.(FRI),a family-owned business that manufactures a variety of different wooden and metal file cabinets.In business for over twenty years,FRI has a reputation for providing high-quality products on time or even ahead of schedule.FRI does not sell to the public,but only to fine furniture stores and to a variety of office supply chains.

As of the current year-end,the company has a total of $6.3 million in assets.Inventory information is as follows:

File cabinet production is intensely competitive,primarily due to imports from Asia and Mexico.To help manage costs,FRI uses a job-order,standard cost system.Standard costs are assessed quarterly.Each job is costed and compared to standard.Inventory is counted only at the end of the year.There is no perpetual inventory system.

Due to problems with raw material quality and new staff,losses have been incurred in the last six months of the year.Your review of last year's audit file indicated that there were numerous inventory adjustments required last year.

Required:

Using the audit risk model,assess the risks associated with the audit of inventory.

As of the current year-end,the company has a total of $6.3 million in assets.Inventory information is as follows:

File cabinet production is intensely competitive,primarily due to imports from Asia and Mexico.To help manage costs,FRI uses a job-order,standard cost system.Standard costs are assessed quarterly.Each job is costed and compared to standard.Inventory is counted only at the end of the year.There is no perpetual inventory system.

Due to problems with raw material quality and new staff,losses have been incurred in the last six months of the year.Your review of last year's audit file indicated that there were numerous inventory adjustments required last year.

Required:

Using the audit risk model,assess the risks associated with the audit of inventory.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 75 في هذه المجموعة.

فتح الحزمة

k this deck

24

A well-designed computerized system of perpetual inventory data files includes information about the

A)units of inventory purchased,sold,and on hand.

B)unit costs of inventory purchased,sold,and on hand.

C)units and unit costs of inventory purchased,sold,and on hand.

D)units of raw materials,work-in-process,and finished goods.

A)units of inventory purchased,sold,and on hand.

B)unit costs of inventory purchased,sold,and on hand.

C)units and unit costs of inventory purchased,sold,and on hand.

D)units of raw materials,work-in-process,and finished goods.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 75 في هذه المجموعة.

فتح الحزمة

k this deck

25

XYZ Company uses standard costs for allocating costs to work-in-process and finished goods inventory.What internal control is required with respect to these costs to ensure proper valuation of inventory?

A)Procedures must be designed to keep the standards updated for changes in production processes and costs.

B)Computer software should be used to make sure that the standard costs are properly updated into the inventory item master file.

C)Input edit routines should be used to help detect input data entry errors for the entry of the standard costs.

D)Standard costs should be used to provide a value for inventory every month by calculating cost times quantity on hand.

A)Procedures must be designed to keep the standards updated for changes in production processes and costs.

B)Computer software should be used to make sure that the standard costs are properly updated into the inventory item master file.

C)Input edit routines should be used to help detect input data entry errors for the entry of the standard costs.

D)Standard costs should be used to provide a value for inventory every month by calculating cost times quantity on hand.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 75 في هذه المجموعة.

فتح الحزمة

k this deck

26

If the auditor concludes that the physical controls over inventory are so inadequate that inventory will be difficult to count,the auditor should

A)inquire of management the additional controls that can be put in place to enable a better count to be carried out.

B)conduct additional control tests over the pricing and compilation of inventory to obtain a higher degree of accuracy.

C)rely on the perpetual inventory master files rather than the physical count.

D)expand the observation of physical inventory tests to ensure that an adequate count is carried out.

A)inquire of management the additional controls that can be put in place to enable a better count to be carried out.

B)conduct additional control tests over the pricing and compilation of inventory to obtain a higher degree of accuracy.

C)rely on the perpetual inventory master files rather than the physical count.

D)expand the observation of physical inventory tests to ensure that an adequate count is carried out.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 75 في هذه المجموعة.

فتح الحزمة

k this deck

27

The existence of an adequate storeroom with a competent custodian in charge results in the orderly storage of inventory and can protect inventory from theft and misuse.How would an auditor assess these controls?

A)observation during the audit and inquiry of the accounting staff

B)inquiry of the accounting staff and inspection of theft statistics

C)observation during the inventory count and inquiry of inventory personnel

D)inspection of inventory damage statistics and inquiry of inventory personnel

A)observation during the audit and inquiry of the accounting staff

B)inquiry of the accounting staff and inspection of theft statistics

C)observation during the inventory count and inquiry of inventory personnel

D)inspection of inventory damage statistics and inquiry of inventory personnel

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 75 في هذه المجموعة.

فتح الحزمة

k this deck

28

Which one of the following analytical procedures would be most helpful in alerting the auditor to the possibility of obsolete inventory?

A)comparing gross margin percentage with previous years

B)comparing unit costs of inventory with previous years

C)comparing inventory turnover with previous years

D)comparing current year manufacturing costs with previous years

A)comparing gross margin percentage with previous years

B)comparing unit costs of inventory with previous years

C)comparing inventory turnover with previous years

D)comparing current year manufacturing costs with previous years

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 75 في هذه المجموعة.

فتح الحزمة

k this deck

29

The auditor's tests of the adequacy of the physical controls over raw materials,work-in-process,and finished goods are usually limited to

A)observation and inquiry.

B)inspection and observation.

C)inspection and confirmation.

D)inspection and inquiry.

A)observation and inquiry.

B)inspection and observation.

C)inspection and confirmation.

D)inspection and inquiry.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 75 في هذه المجموعة.

فتح الحزمة

k this deck

30

What are inventory price tests and inventory compilation tests? Provide an example of each.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 75 في هذه المجموعة.

فتح الحزمة

k this deck

31

Segregation of duties between production,inventory control,and accounting are important controls in the inventory and distribution cycle.How would the auditor test these controls?

A)using inquiry and reperformance

B)using observation and inquiry

C)using observation and reperformance

D)using discussion with management

A)using inquiry and reperformance

B)using observation and inquiry

C)using observation and reperformance

D)using discussion with management

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 75 في هذه المجموعة.

فتح الحزمة

k this deck

32

It is frequently possible to test the physical inventory prior to the balance sheet date when

A)there are accurate perpetual inventory master files.

B)year-end sales are small.

C)the internal control system is no better at year-end than at an earlier point in time.

D)client counts inventory at interim dates.

A)there are accurate perpetual inventory master files.

B)year-end sales are small.

C)the internal control system is no better at year-end than at an earlier point in time.

D)client counts inventory at interim dates.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 75 في هذه المجموعة.

فتح الحزمة

k this deck

33

The auditor must verify whether the physical counts were correctly summarized,the inventory quantities and prices were correctly extended,and the extended inventory was correctly footed.These tests are called

A)price tests.

B)compilation tests.

C)cost tests.

D)mechanical tests.

A)price tests.

B)compilation tests.

C)cost tests.

D)mechanical tests.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 75 في هذه المجموعة.

فتح الحزمة

k this deck

34

To protect the inventory,Globus Corp wants to assign the custody of inventory to a specific responsible individual.Globus can accomplish this by

A)having a designated employee to authorize movement of inventory.

B)requiring employees to have photo id cards.

C)having restricted access to the production facility.

D)performing frequent inventory counts.

A)having a designated employee to authorize movement of inventory.

B)requiring employees to have photo id cards.

C)having restricted access to the production facility.

D)performing frequent inventory counts.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 75 في هذه المجموعة.

فتح الحزمة

k this deck

35

Selecting a sample of job orders from the job cost summary and matching them to bills of material and the schedule of production labour requirements is a procedure designed to test the control objective of

A)validity.

B)accounting.

C)accuracy.

D)completeness.

A)validity.

B)accounting.

C)accuracy.

D)completeness.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 75 في هذه المجموعة.

فتح الحزمة

k this deck

36

Outline the key controls relating to compilation and pricing in the inventory cycle.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 75 في هذه المجموعة.

فتح الحزمة

k this deck

37

The costs used to value the physical inventory must be tested to determine whether the client has correctly followed an inventory method that is in accordance with an acceptable financial reporting framework and is consistent with previous years.The audit procedures used to verify these costs are referred to as inventory

A)price tests.

B)compilation tests.

C)cost allocation tests.

D)consistency tests.

A)price tests.

B)compilation tests.

C)cost allocation tests.

D)consistency tests.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 75 في هذه المجموعة.

فتح الحزمة

k this deck

38

The auditor has determined that the perpetual inventory master files are high quality,assessing control risk related to physical observation of inventory as low.How does this affect audit testing? The auditor may

A)reduce the extent of control tests over data entry to the master file.

B)reduce the extent of the tests of physical inventory.

C)reduce the extent of control tests with respect to program change controls.

D)increase assessed inherent risks over the tests of physical inventory.

A)reduce the extent of control tests over data entry to the master file.

B)reduce the extent of the tests of physical inventory.

C)reduce the extent of control tests with respect to program change controls.

D)increase assessed inherent risks over the tests of physical inventory.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 75 في هذه المجموعة.

فتح الحزمة

k this deck

39

XYZ Company uses standard costs for allocating costs to work-in-process and finished goods inventory.For the last few months,there have been high variances between total standard costs and actual costs.What is one of the likely reasons for this variance?

A)The accounting department has been developing the costs.

B)Production quantities are different than expected.

C)There is an increase in inventory quantities on hand.

D)The receiving department has been stockpiling raw materials.

A)The accounting department has been developing the costs.

B)Production quantities are different than expected.

C)There is an increase in inventory quantities on hand.

D)The receiving department has been stockpiling raw materials.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 75 في هذه المجموعة.

فتح الحزمة

k this deck

40

Cost accounting controls are those related to the physical inventory and the consequent costs from the point at which

A)materials are ordered for purchase until the finished product is sold.

B)raw materials are requisitioned until the finished product is sent to storage.

C)raw materials are requisitioned until the finished product is completely manufactured.

D)the customer's order is received until the finished product is shipped.

A)materials are ordered for purchase until the finished product is sold.

B)raw materials are requisitioned until the finished product is sent to storage.

C)raw materials are requisitioned until the finished product is completely manufactured.

D)the customer's order is received until the finished product is shipped.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 75 في هذه المجموعة.

فتح الحزمة

k this deck

41

A public accountant observes his client's physical inventory count on December 31.There are eight inventory-taking teams and a tag system is used.The public accountant's observation normally may be expected to result in detection of which of the following inventory errors?

A)The inventory takers forgot to count all the items in one room of the warehouse.

B)An error is made in the count of one inventory item.

C)Some of the items included in the inventory had been received on consignment.

D)The inventory omits items on consignment to wholesalers.

A)The inventory takers forgot to count all the items in one room of the warehouse.

B)An error is made in the count of one inventory item.

C)Some of the items included in the inventory had been received on consignment.

D)The inventory omits items on consignment to wholesalers.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 75 في هذه المجموعة.

فتح الحزمة

k this deck

42

If the auditor is appointed after the year-end of the client,the auditor

A)should qualify the audit opinion for the inventory balance and cost of sales.

B)could attend a current perpetual inventory count and roll backward with the records.

C)should do an inventory count as soon as he is appointed.

D)will inquire with management about the inventory count performed at year-end.

A)should qualify the audit opinion for the inventory balance and cost of sales.

B)could attend a current perpetual inventory count and roll backward with the records.

C)should do an inventory count as soon as he is appointed.

D)will inquire with management about the inventory count performed at year-end.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 75 في هذه المجموعة.

فتح الحزمة

k this deck

43

Which analytical procedures will help an auditor identify possible misstatements in compilation,unit costs,or extensions that affect inventory and cost of goods sold?

A)comparing gross margin percentage with previous years

B)comparing unit costs of inventory with previous years

C)comparing inventory turnover with previous years

D)comparing extended inventory value with previous years

A)comparing gross margin percentage with previous years

B)comparing unit costs of inventory with previous years

C)comparing inventory turnover with previous years

D)comparing extended inventory value with previous years

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 75 في هذه المجموعة.

فتح الحزمة

k this deck

44

The test of details of balance procedure that requires the auditor to account for unused inventory tag numbers to make sure none have been omitted is an attempt to satisfy the objective of

A)allocation.

B)existence.

C)completeness.

D)accuracy.

A)allocation.

B)existence.

C)completeness.

D)accuracy.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 75 في هذه المجموعة.

فتح الحزمة

k this deck

45

To detect an overstatement or understatement of inventory and cost of goods sold,the auditor may perform an analytical procedure such as comparing

A)gross margin percentage with previous years.

B)inventory turnover with previous years.

C)current year manufacturing costs with previous years.

D)extended inventory value with previous years.

A)gross margin percentage with previous years.

B)inventory turnover with previous years.

C)current year manufacturing costs with previous years.

D)extended inventory value with previous years.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 75 في هذه المجموعة.

فتح الحزمة

k this deck

46

Identify three analytical procedures commonly used when auditing accounts in the inventory and distribution cycle.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 75 في هذه المجموعة.

فتح الحزمة

k this deck

47

A common inventory observation procedure is to record in the working papers for subsequent follow-up the last shipping document number used at year-end.The audit objective being achieved by this procedure is

A)inventory as recorded exists.

B)existing inventory is counted and tagged.

C)information is obtained to make sure sales and inventory purchases are recorded in the proper period.

D)tags are accounted for to make sure none are missing.

A)inventory as recorded exists.

B)existing inventory is counted and tagged.

C)information is obtained to make sure sales and inventory purchases are recorded in the proper period.

D)tags are accounted for to make sure none are missing.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 75 في هذه المجموعة.

فتح الحزمة

k this deck

48

When auditing merchandise inventory at year-end,the auditor performs a purchase cutoff test to obtain evidence that

A)all goods purchased before year-end are received before the physical inventory count.

B)no goods held on consignment for customers are included in the inventory balance.

C)no goods observed during the physical count are pledged or sold.

D)all goods owned at year-end are included in the current period inventory balance.

A)all goods purchased before year-end are received before the physical inventory count.

B)no goods held on consignment for customers are included in the inventory balance.

C)no goods observed during the physical count are pledged or sold.

D)all goods owned at year-end are included in the current period inventory balance.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 75 في هذه المجموعة.

فتح الحزمة

k this deck

49

When a physical count of inventory is permitted at an interim date,the auditor observes it at that time,and also tests the perpetual inventory for transactions

A)throughout the year.

B)which are a representative sample of the period under audit.

C)from the date of the count to year-end.

D)from the date of the count to the end of the audit field work.

A)throughout the year.

B)which are a representative sample of the period under audit.

C)from the date of the count to year-end.

D)from the date of the count to the end of the audit field work.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 75 في هذه المجموعة.

فتح الحزمة

k this deck

50

A common inventory observation procedure is to be alert for items that are damaged,rust- or dust-covered,or located in inappropriate places.The balance-related audit objective achieved by this procedure is

A)classification.

B)cutoff.

C)valuation.

D)rights.

A)classification.

B)cutoff.

C)valuation.

D)rights.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 75 في هذه المجموعة.

فتح الحزمة

k this deck

51

Analytical procedures applied to management's production cost reports provide evidence for which assertion(s)?

A)existence,valuation,and completeness

B)ownership

C)physical inspection

D)auditor's recomputation of inventory extensions

A)existence,valuation,and completeness

B)ownership

C)physical inspection

D)auditor's recomputation of inventory extensions

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 75 في هذه المجموعة.

فتح الحزمة

k this deck

52

An inventory observation procedure that compares physical counts with the perpetual inventory master file is an attempt to satisfy the audit objective of

A)existence.

B)completeness.

C)accuracy.

D)classification.

A)existence.

B)completeness.

C)accuracy.

D)classification.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 75 في هذه المجموعة.

فتح الحزمة

k this deck

53

From which of the following evidence-gathering audit procedures would an auditor obtain most assurance concerning the existence of inventories?

A)observation of physical inventory counts

B)written inventory representations from management

C)confirmation of inventories in a public warehouse

D)auditor's recomputation of inventory extensions

A)observation of physical inventory counts

B)written inventory representations from management

C)confirmation of inventories in a public warehouse

D)auditor's recomputation of inventory extensions

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 75 في هذه المجموعة.

فتح الحزمة

k this deck

54

CAS for audit procedures for inventory indicate that the auditor

A)must count the inventory.

B)must be present at the inventory count and must receive adequate documentation from the client regarding the effectiveness of inventory-taking.

C)must be present at the inventory count and evaluate the methods followed in the determination of quantities and values.

D)need not be present at the count but must review the methods followed in the determination of quantities and values.

A)must count the inventory.

B)must be present at the inventory count and must receive adequate documentation from the client regarding the effectiveness of inventory-taking.

C)must be present at the inventory count and evaluate the methods followed in the determination of quantities and values.

D)need not be present at the count but must review the methods followed in the determination of quantities and values.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 75 في هذه المجموعة.

فتح الحزمة

k this deck

55

Sample size in physical observation of inventory is

A)determined using attributes sampling.

B)determined using variables sampling.

C)determined using dollar-unit sampling.

D)difficult to specify because the emphasis is on observing the client's procedures.

A)determined using attributes sampling.

B)determined using variables sampling.

C)determined using dollar-unit sampling.

D)difficult to specify because the emphasis is on observing the client's procedures.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 75 في هذه المجموعة.

فتح الحزمة

k this deck

56

Dishware Distribution Limited uses average costing to cost its inventory.It keeps a perpetual inventory file that is linked to its sales systems.It orders inventory in for specific customers as needed,and traditionally has a slow time just before its year-end.Accordingly,inventory at the year-end is about $2000,while materiality is about $30 000.How should the auditor approach the audit of physical inventory?

A)Exclude testing of physical inventory from the audit program.

B)Use attribute sampling to select a sample of items to count.

C)Use dollar-unit sampling to select a sample of items to count.

D)Count only those items that have a dollar value in excess of $100.

A)Exclude testing of physical inventory from the audit program.

B)Use attribute sampling to select a sample of items to count.

C)Use dollar-unit sampling to select a sample of items to count.

D)Count only those items that have a dollar value in excess of $100.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 75 في هذه المجموعة.

فتح الحزمة

k this deck

57

The test of details of balance procedure that requires the auditor to review contracts with suppliers and customers and inquire of management for the possibility of the inclusion of consigned or other non-owned inventory is an attempt to satisfy the objective of

A)existence.

B)completeness.

C)realizable value.

D)rights and obligations.

A)existence.

B)completeness.

C)realizable value.

D)rights and obligations.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 75 في هذه المجموعة.

فتح الحزمة

k this deck

58

The client has a perpetual inventory system,and takes an inventory count of 100 items every two weeks for comparison to the perpetual records.There are no plans to have a complete year-end physical count of inventory.How will the auditor conduct the audit of physical inventory?

A)Select an attribute sample of items to count at the year end for comparison to the perpetual records.

B)Select a dollar unit sample of items to count at the year end for comparison to the perpetual records.

C)Use roll-forwards to carry forward the inventory records from the cyclical counts for an attribute sample of inventory items.

D)Conduct test counts and compare the perpetual records with a cyclical count during the interim audit.

A)Select an attribute sample of items to count at the year end for comparison to the perpetual records.

B)Select a dollar unit sample of items to count at the year end for comparison to the perpetual records.

C)Use roll-forwards to carry forward the inventory records from the cyclical counts for an attribute sample of inventory items.

D)Conduct test counts and compare the perpetual records with a cyclical count during the interim audit.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 75 في هذه المجموعة.

فتح الحزمة

k this deck

59

The auditor has evaluated the effectiveness of the client's procedures to count inventory,and has provided constructive suggestions for improvement.However,the client has not implemented the suggestions,so the auditor has concluded that the inventory instructions do not provide adequate controls.This means that the auditor

A)must send a management letter informing management of the impact of these weaknesses.

B)must spend more time ensuring that the physical count is accurate.

C)should use attribute sampling to select a smaller sample for testing the physical inventory.

D)should increase the level of price and compilation tests to ensure better quality inventory pricing data.

A)must send a management letter informing management of the impact of these weaknesses.

B)must spend more time ensuring that the physical count is accurate.

C)should use attribute sampling to select a smaller sample for testing the physical inventory.

D)should increase the level of price and compilation tests to ensure better quality inventory pricing data.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 75 في هذه المجموعة.

فتح الحزمة

k this deck

60

The auditor has determined that the inventory procedures are highly automated with limited use of a paper or physical trail.Rather than having people count inventory (since all inventory has RFID tags attached),inventory is being read using the wireless mesh network.To provide assurance with respect to ending inventory,the auditor should

A)bring in additional audit staff and conduct a high level of test counts,matching these counts to the automated systems.

B)use dollar-unit sampling to identify all high-dollar inventory items and ask the client to physically count these items using count teams.

C)test the quality of the controls over the programs in use and over tagging inventory items.

D)request that the client implement manual rotating counts to test the quality of the automated systems.

A)bring in additional audit staff and conduct a high level of test counts,matching these counts to the automated systems.

B)use dollar-unit sampling to identify all high-dollar inventory items and ask the client to physically count these items using count teams.

C)test the quality of the controls over the programs in use and over tagging inventory items.

D)request that the client implement manual rotating counts to test the quality of the automated systems.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 75 في هذه المجموعة.

فتح الحزمة

k this deck

61

Which of the following is correct relating to "fraud risk factor"?

A)it may affect the auditors assessment of risks relating to fraud

B)if it involves senior management,it will result in resignation of the auditor

C)it is also a material weakness in internal control

D)the planned audit procedures would require modifications

A)it may affect the auditors assessment of risks relating to fraud

B)if it involves senior management,it will result in resignation of the auditor

C)it is also a material weakness in internal control

D)the planned audit procedures would require modifications

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 75 في هذه المجموعة.

فتح الحزمة

k this deck

62

What is the first step that the auditor takes when auditing the valuation of inventory?

A)Conduct analytical review,comparing gross margin for the current year to the prior year.

B)Do an industry analysis to determine whether there is a potential for technology-induced obsolescence.

C)Ask the client about the level of obsolete inventory that was on hand and counted during the inventory count.

D)Clearly establish the valuation method used and how the calculations are being performed.

A)Conduct analytical review,comparing gross margin for the current year to the prior year.

B)Do an industry analysis to determine whether there is a potential for technology-induced obsolescence.

C)Ask the client about the level of obsolete inventory that was on hand and counted during the inventory count.

D)Clearly establish the valuation method used and how the calculations are being performed.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 75 في هذه المجموعة.

فتح الحزمة

k this deck

63

The test of details of balance procedure that requires the auditor to perform tests of lower-of-cost-or-market,selling price,and obsolescence is an attempt to satisfy the objective of

A)existence.

B)completeness.

C)accuracy.

D)valuation.

A)existence.

B)completeness.

C)accuracy.

D)valuation.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 75 في هذه المجموعة.

فتح الحزمة

k this deck

64

Outline some examples of fraud-related procedures that could be performed for the inventory and distribution cycle.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 75 في هذه المجموعة.

فتح الحزمة

k this deck

65

Controls that provide a means of ensuring that the physical counts are properly summarized,priced at the same amount as the unit records,correctly extended and totalled,and included in the general ledger at the proper amount are known as

A)standard cost records.

B)pricing internal controls.

C)compilation internal controls.

D)count quantity internal controls.

A)standard cost records.

B)pricing internal controls.

C)compilation internal controls.

D)count quantity internal controls.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 75 في هذه المجموعة.

فتح الحزمة

k this deck

66

When considering pricing of inventory,three things are important.The first two are that the method must be in accordance with an acceptable financial accounting framework,and the application of the method must be consistent from year to year.What is the third?

A)The input edits over the data entry of prices must be robust.

B)The cutoff testing for the use of supplier invoices should be carefully done.

C)The cost versus market value must be considered.

D)The freight should always be included in the cost of the inventory.

A)The input edits over the data entry of prices must be robust.

B)The cutoff testing for the use of supplier invoices should be carefully done.

C)The cost versus market value must be considered.

D)The freight should always be included in the cost of the inventory.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 75 في هذه المجموعة.

فتح الحزمة

k this deck

67

State six specific balance-related audit objectives for physical inventory observation and,for each objective,describe one common test of details of balances related to that objective.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 75 في هذه المجموعة.

فتح الحزمة

k this deck

68

The auditor is determining which specific inventory items should be selected for pricing tests.The auditor has selected a representative sample,and those items that have a large dollar amount.In addition,the auditor should select those items that

A)are prone to breakage or theft.

B)have wide fluctuations in price.

C)are stored in multiple locations.

D)are likely to have been miscounted during the inventory count.

A)are prone to breakage or theft.

B)have wide fluctuations in price.

C)are stored in multiple locations.

D)are likely to have been miscounted during the inventory count.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 75 في هذه المجموعة.

فتح الحزمة

k this deck

69

A)State seven specific balance-related audit objectives for inventory pricing and compilation and,for each objective,describe one common test of details of balances related to that objective.B)Explain why the audit of work-in-process and finished goods inventory is generally more complex than the audit of purchased inventory.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 75 في هذه المجموعة.

فتح الحزمة

k this deck

70

When performing a financial statement audit,auditors are required to explicitly assess the risk of material misstatement due to

A)fraud.

B)audit risk.

C)illegal acts.

D)business risks.

A)fraud.

B)audit risk.

C)illegal acts.

D)business risks.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 75 في هذه المجموعة.

فتح الحزمة

k this deck

71

A common inventory observation procedure is to select a random sample of tag numbers and identify the tag with that number attached to the actual inventory.The audit objective being achieved by this procedure is

A)inventory as recorded on tags exists (existence).

B)existing inventory is counted and tagged (completeness).

C)inventory is counted accurately (accuracy).

D)inventory is classified correctly (classification).

A)inventory as recorded on tags exists (existence).

B)existing inventory is counted and tagged (completeness).

C)inventory is counted accurately (accuracy).

D)inventory is classified correctly (classification).

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 75 في هذه المجموعة.

فتح الحزمة

k this deck

72

As part of the audit of valuation,the auditor is conducting pricing tests by comparing to supplier invoices.The auditor is making sure that,for each item tested,sufficient supplier invoices are examined to cover the quantity of inventory that was on hand during the physical inventory count.What type of pricing error could this detect?

A)The client valued their inventory on the basis of the most recent invoice only.

B)The client has used the incorrect accounting method to value its inventory.

C)Extension errors could occur with numerous different inventory items.

D)The wrong inventory count quantity could have been recorded on the count sheets.

A)The client valued their inventory on the basis of the most recent invoice only.

B)The client has used the incorrect accounting method to value its inventory.

C)Extension errors could occur with numerous different inventory items.

D)The wrong inventory count quantity could have been recorded on the count sheets.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 75 في هذه المجموعة.

فتح الحزمة

k this deck

73

The most important part of the observation of inventory is determining whether

A)the inventory-takers are qualified.

B)the physical count is being taken in accordance with the client's instructions.

C)the counts are accurate.

D)obsolete inventory has been identified.

A)the inventory-takers are qualified.

B)the physical count is being taken in accordance with the client's instructions.

C)the counts are accurate.

D)obsolete inventory has been identified.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 75 في هذه المجموعة.

فتح الحزمة

k this deck

74

A useful starting point for becoming familiar with the client's inventory is for the auditor to

A)obtain and review industry ratios.

B)review accounting theory covering special problems,such as gas and oil accounting,or lease-purchase agreements.

C)read the client's Accounting Manual.

D)tour the client's facility.

A)obtain and review industry ratios.

B)review accounting theory covering special problems,such as gas and oil accounting,or lease-purchase agreements.

C)read the client's Accounting Manual.

D)tour the client's facility.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 75 في هذه المجموعة.

فتح الحزمة

k this deck

75

A)Discuss the key control procedures relating to the client's physical count of inventory.B)State the primary determinants of the amount of time needed to perform the physical observation of inventory.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 75 في هذه المجموعة.

فتح الحزمة

k this deck

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 75 في هذه المجموعة.