Deck 6: Analyzing and Journalizing Payroll

ملء الشاشة (f)

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

Exhibit 6-1

The totals from the first payroll of the year are shown below. Refer to Exhibit 6-1 . Journalize the entry to deposit the FICA and FIT taxes.

Refer to Exhibit 6-1 . Journalize the entry to deposit the FICA and FIT taxes.

The totals from the first payroll of the year are shown below.

Refer to Exhibit 6-1 . Journalize the entry to deposit the FICA and FIT taxes. سؤال

سؤال

سؤال

Exhibit 6-1

The totals from the first payroll of the year are shown below.

Refer to Exhibit 6-1 . Journalize the adjustment for accrued wages for the following Monday, which is the end of the accounting period. The gross payroll for that day is $7,475.

The totals from the first payroll of the year are shown below.

Refer to Exhibit 6-1 . Journalize the adjustment for accrued wages for the following Monday, which is the end of the accounting period. The gross payroll for that day is $7,475.

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

Exhibit 6-1

The totals from the first payroll of the year are shown below. Refer to Exhibit 6-1 . Journalize the entry to record the employer's payroll taxes (assume a SUTA rate of 3.7%).

Refer to Exhibit 6-1 . Journalize the entry to record the employer's payroll taxes (assume a SUTA rate of 3.7%).

The totals from the first payroll of the year are shown below.

Refer to Exhibit 6-1 . Journalize the entry to record the employer's payroll taxes (assume a SUTA rate of 3.7%). سؤال

سؤال

سؤال

Exhibit 6-1  Refer to Exhibit 6-1 . Journalize the entry to record the payroll.

Refer to Exhibit 6-1 . Journalize the entry to record the payroll.

Refer to Exhibit 6-1 . Journalize the entry to record the payroll. سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

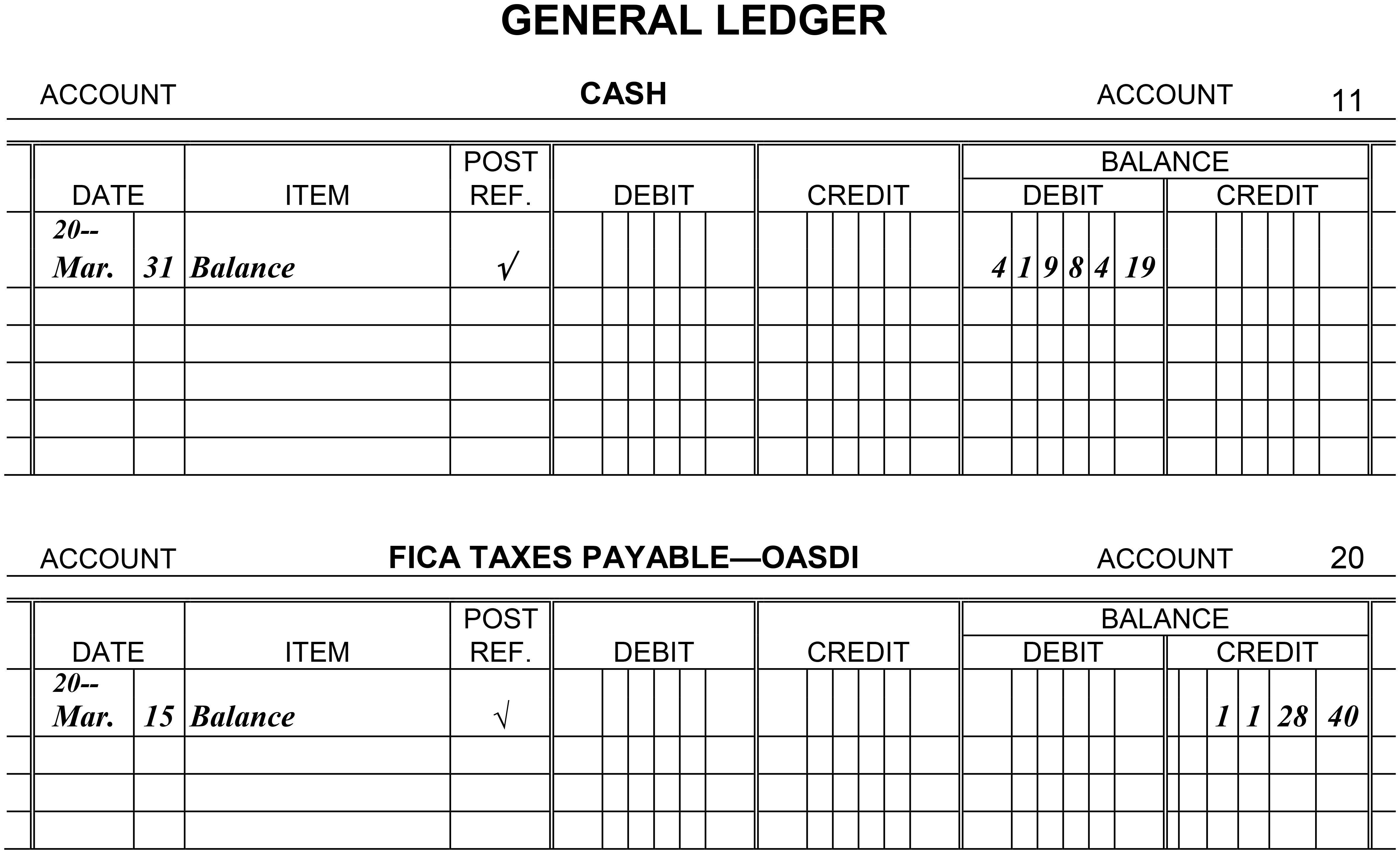

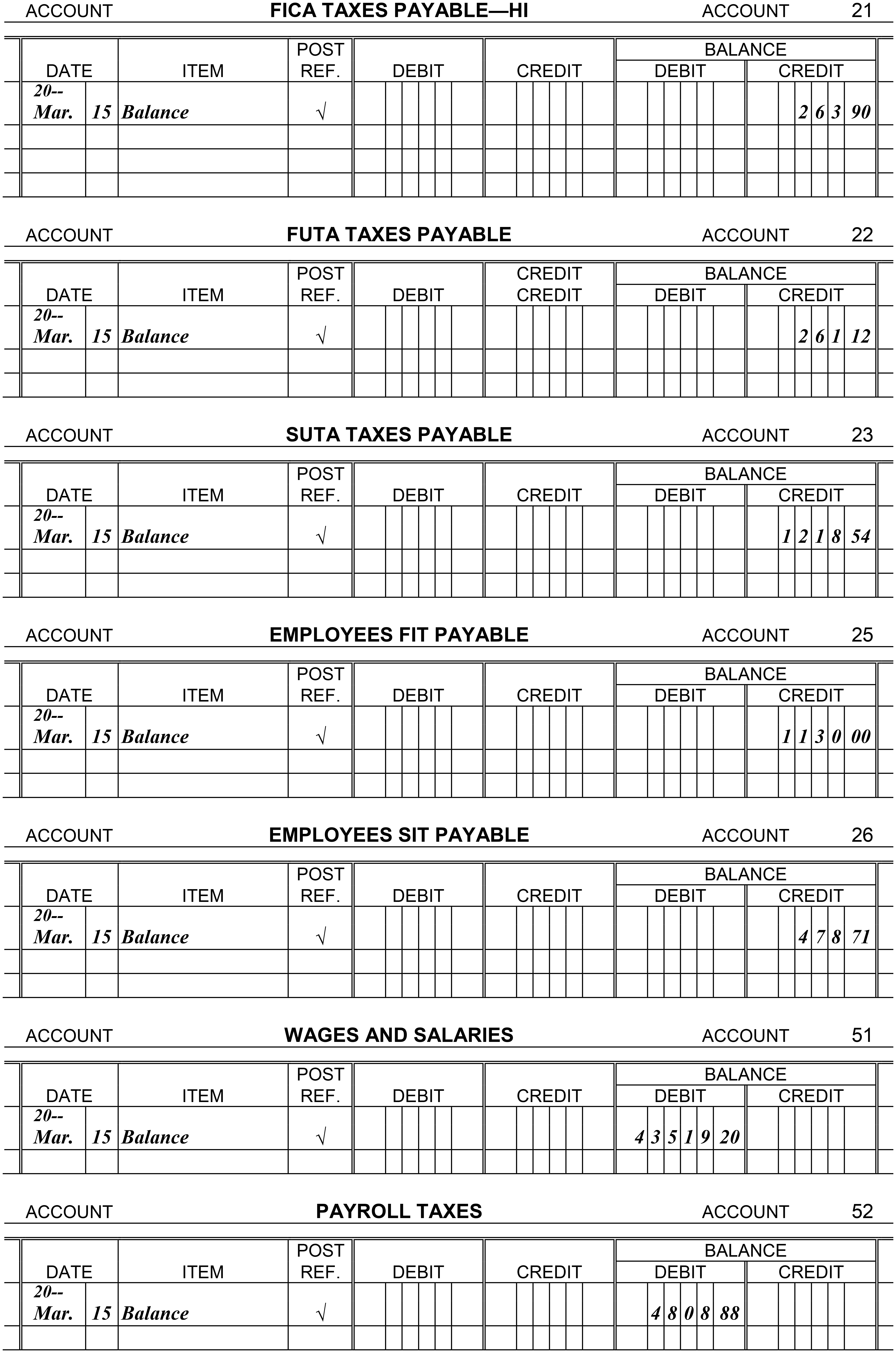

Journalize each of the payroll transactions listed below. Omit the writing of a description or explanation for each journal entry, and do not skip a line between each entry . Then post all entries except the last two to the appropriate general ledger accounts.

The balances listed in the general ledger accounts for Cash, FUTA Taxes Payable, SUTA Taxes Payable, Employees SIT Payable, Wages and Salaries, and Payroll Taxes are the results of all payroll transactions for the first quarter, not including the last pay of the quarter. The balances in FICA Taxes Payable-OASDI, FICA Taxes Payable-HI, and Employees FIT Payable are the amounts due from

the March 15 payroll.

March 31, 20--: Paid total wages of $9,350.00. These are the wages for the last semimonthly pay of March. All of this amount is taxable under FICA (OASDI and HI). In addition, withhold $1,175 for federal income taxes and $102.03 for state income taxes. These are the only deductions made from the employees' wages.

March 31, 20--: Record the employer's payroll taxes for the last pay in March. All of the earnings are taxable under FICA (OASDI and HI), FUTA (0.6%), and SUTA (2.8%).

April 15, 20--: Made a deposit to remove the liability for the FICA taxes and the employees' federal income taxes withheld on the two March payrolls.

May 2, 20--: Made the deposit to remove the liability for FUTA taxes for the first quarter of 20--.

May 2, 20--: Filed the state unemployment contributions return for the first quarter of 20-- and paid the total amount owed for the quarter to the state unemployment compensation fund.

May 2, 20--: Filed the state income tax return for the first quarter of 20-- and paid the total amount owed for the quarter to the state income tax bureau.

December 31, 20--: In July 20--, the company changed from a semimonthly pay system to a weekly pay system. The employees were paid every Friday through the rest of 20--. Record the adjusting entry for wages accrued at the end of December ($770) but not paid until the first Friday in January. Do not post this entry.

December 31, 20--: The company has determined that employees have earned $19,300 in unused vacation time. Record the adjusting entry to put this expense on the books. Do not post this entry.

The balances listed in the general ledger accounts for Cash, FUTA Taxes Payable, SUTA Taxes Payable, Employees SIT Payable, Wages and Salaries, and Payroll Taxes are the results of all payroll transactions for the first quarter, not including the last pay of the quarter. The balances in FICA Taxes Payable-OASDI, FICA Taxes Payable-HI, and Employees FIT Payable are the amounts due from

the March 15 payroll.

March 31, 20--: Paid total wages of $9,350.00. These are the wages for the last semimonthly pay of March. All of this amount is taxable under FICA (OASDI and HI). In addition, withhold $1,175 for federal income taxes and $102.03 for state income taxes. These are the only deductions made from the employees' wages.

March 31, 20--: Record the employer's payroll taxes for the last pay in March. All of the earnings are taxable under FICA (OASDI and HI), FUTA (0.6%), and SUTA (2.8%).

April 15, 20--: Made a deposit to remove the liability for the FICA taxes and the employees' federal income taxes withheld on the two March payrolls.

May 2, 20--: Made the deposit to remove the liability for FUTA taxes for the first quarter of 20--.

May 2, 20--: Filed the state unemployment contributions return for the first quarter of 20-- and paid the total amount owed for the quarter to the state unemployment compensation fund.

May 2, 20--: Filed the state income tax return for the first quarter of 20-- and paid the total amount owed for the quarter to the state income tax bureau.

December 31, 20--: In July 20--, the company changed from a semimonthly pay system to a weekly pay system. The employees were paid every Friday through the rest of 20--. Record the adjusting entry for wages accrued at the end of December ($770) but not paid until the first Friday in January. Do not post this entry.

December 31, 20--: The company has determined that employees have earned $19,300 in unused vacation time. Record the adjusting entry to put this expense on the books. Do not post this entry.

سؤال

سؤال

سؤال

سؤال

سؤال

فتح الحزمة

قم بالتسجيل لفتح البطاقات في هذه المجموعة!

Unlock Deck

Unlock Deck

1/75

العب

ملء الشاشة (f)

Deck 6: Analyzing and Journalizing Payroll

1

Every state allows employers to make e-payment options as a condition of employment.

False

2

Service charges that are passed on to the employee by the employer are not part of the disposable earnings subject to garnishment.

False

3

An employer will use the payroll register to keep track of an employee's accumulated wages.

False

4

A debit to the employees FIT payable account removes the liability for the amount of federal income taxes withheld from employees' wages.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 75 في هذه المجموعة.

فتح الحزمة

k this deck

5

FIT Payable is a liability account used to record employees' withheld federal income tax and also the employer's match of that tax.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 75 في هذه المجموعة.

فتح الحزمة

k this deck

6

An employee's marital status and number of withholding allowances never appear on the payroll register.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 75 في هذه المجموعة.

فتح الحزمة

k this deck

7

The total of the net amount paid to employees each payday is credited to either the cash account or the salaries payable account.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 75 في هذه المجموعة.

فتح الحزمة

k this deck

8

The wage and salaries expense account is an operating expense account debited for total net pay each payroll period.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 75 في هذه المجموعة.

فتح الحزمة

k this deck

9

If wages are paid weekly, postings to the employee's earnings record would be done once a month.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 75 في هذه المجموعة.

فتح الحزمة

k this deck

10

Each payday, the total of net pays that the employer incurs is the wage expense that must be debited.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 75 في هذه المجموعة.

فتح الحزمة

k this deck

11

Under the provisions of the Consumer Credit Protection Act, an employer can discharge an employee simply because the employee's wage is subject to garnishment for a single indebtedness.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 75 في هذه المجموعة.

فتح الحزمة

k this deck

12

Deductions from gross pay in the payroll register are reflected on the credit side of the journal entry to record the payroll.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 75 في هذه المجموعة.

فتح الحزمة

k this deck

13

When withheld union dues are turned over to the union by the employer, a journal entry is made debiting the liability account and crediting the cash account.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 75 في هذه المجموعة.

فتح الحزمة

k this deck

14

In order to prepare Forms W-2, an employer would utilize the employee's earnings record.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 75 في هذه المجموعة.

فتح الحزمة

k this deck

15

Under the Consumer Credit Protection Act, disposable earnings are the earnings remaining after any deductions for health insurance.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 75 في هذه المجموعة.

فتح الحزمة

k this deck

16

Amounts withheld from employees' wages for health insurance are credited to a liability account.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 75 في هذه المجموعة.

فتح الحزمة

k this deck

17

Companies usually provide a separate column in the payroll register to record the employer's payroll taxes.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 75 في هذه المجموعة.

فتح الحزمة

k this deck

18

Tips received by employees in excess of tip credit amount are not included as disposable earnings subject to garnishment

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 75 في هذه المجموعة.

فتح الحزمة

k this deck

19

Tax withholdings from employees' pays reduce the amount of the debit to Salary Expense in the payroll entry.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 75 في هذه المجموعة.

فتح الحزمة

k this deck

20

Once the journal entry for the payroll is complete, the information is posted to the appropriate general ledger accounts.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 75 في هذه المجموعة.

فتح الحزمة

k this deck

21

If employees must contribute to the state unemployment fund, this deduction should be shown in the payroll tax entry.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 75 في هذه المجموعة.

فتح الحزمة

k this deck

22

FICA Taxes Payable-OASDI is a liability account debited for the employer's portion of the FICA tax.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 75 في هذه المجموعة.

فتح الحزمة

k this deck

23

Since the credit against the FUTA tax (for SUTA contributions) is made on Form 940, the employer's payroll tax entries should include the FUTA tax at the gross amount (6.0%).

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 75 في هذه المجموعة.

فتح الحزمة

k this deck

24

The payroll taxes account is an expense account that is debited for the FICA, FUTA, and SUTA taxes on the employer.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 75 في هذه المجموعة.

فتح الحزمة

k this deck

25

The entry to record the employer's payroll taxes usually includes credits to the liability accounts for FICA (OASDI and HI), FUTA, and SUTA taxes.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 75 في هذه المجموعة.

فتح الحزمة

k this deck

26

At the time that the entry is made to record the employer's payroll taxes, the SUTA tax is recorded at the net amount (0.6%).

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 75 في هذه المجموعة.

فتح الحزمة

k this deck

27

The adjusting entry to record the accrued vacation pay at the end of an accounting period includes credits to the tax withholding liability accounts.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 75 في هذه المجموعة.

فتح الحزمة

k this deck

28

Under the Uniform Unclaimed Property Act, any unclaimed paychecks must be turned over to the state after the next payday.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 75 في هذه المجموعة.

فتح الحزمة

k this deck

29

When the federal tax deposit is made, the employees' and employer's shares of FICA taxes are paid along with the employees' FIT taxes withheld.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 75 في هذه المجموعة.

فتح الحزمة

k this deck

30

The FICA taxes on the employer represent both business expenses and liabilities of the employer.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 75 في هذه المجموعة.

فتح الحزمة

k this deck

31

Since vacation time is paid when used, there is no need to accrue this time in a liability account at the end of each accounting period.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 75 في هذه المجموعة.

فتح الحزمة

k this deck

32

Posting to the general ledger for payroll entries is done only at the end of each calendar year.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 75 في هذه المجموعة.

فتح الحزمة

k this deck

33

The FUTA tax part of the payroll tax entry is recorded at the net amount (0.6%) of the taxable payroll.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 75 في هذه المجموعة.

فتح الحزمة

k this deck

34

FUTA Taxes Payable is an expense account in which are recorded the employer's federal unemployment taxes.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 75 في هذه المجموعة.

فتح الحزمة

k this deck

35

The payroll taxes incurred by an employer are FICA, FUTA, and SUTA.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 75 في هذه المجموعة.

فتح الحزمة

k this deck

36

Union Dues Payable is a liability account credited with the deductions made from union members' wages for their union dues.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 75 في هذه المجموعة.

فتح الحزمة

k this deck

37

The employer's payroll tax expenses are recorded by all employers at the time these taxes are actually paid.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 75 في هذه المجموعة.

فتح الحزمة

k this deck

38

In the adjusting entry to accrue wages at the end of the accounting period, there is no need to credit any tax withholding accounts.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 75 في هذه المجموعة.

فتح الحزمة

k this deck

39

Since FUTA tax is paid only once a quarter, the FUTA tax expense is recorded only at the time of payment.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 75 في هذه المجموعة.

فتح الحزمة

k this deck

40

Since the FUTA tax is a social security tax, it can be charged to the same expense account as the other payroll taxes on the employer, the payroll taxes account.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 75 في هذه المجموعة.

فتح الحزمة

k this deck

41

Exhibit 6-1

The totals from the first payroll of the year are shown below. Refer to Exhibit 6-1 . Journalize the entry to deposit the FICA and FIT taxes.

The totals from the first payroll of the year are shown below.

Refer to Exhibit 6-1 . Journalize the entry to deposit the FICA and FIT taxes. فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 75 في هذه المجموعة.

فتح الحزمة

k this deck

42

Which of these accounts shows the total gross earnings that the employer incurs as an expense each payday?

A) Payroll Taxes

B) Federal Income Taxes Payable

C) Wages Expense

D) Salaries Payable

E) None of the above

A) Payroll Taxes

B) Federal Income Taxes Payable

C) Wages Expense

D) Salaries Payable

E) None of the above

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 75 في هذه المجموعة.

فتح الحزمة

k this deck

43

In calculating overtime premium earnings at one and a half times the regular hourly rate, the overtime hours are multiplied by one-half the hourly rate of pay.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 75 في هذه المجموعة.

فتح الحزمة

k this deck

44

Exhibit 6-1

The totals from the first payroll of the year are shown below.

Refer to Exhibit 6-1 . Journalize the adjustment for accrued wages for the following Monday, which is the end of the accounting period. The gross payroll for that day is $7,475.

The totals from the first payroll of the year are shown below.

Refer to Exhibit 6-1 . Journalize the adjustment for accrued wages for the following Monday, which is the end of the accounting period. The gross payroll for that day is $7,475.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 75 في هذه المجموعة.

فتح الحزمة

k this deck

45

In recording the monthly adjusting entry for accrued wages at the end of the accounting period, the amount of the adjustment would usually be determined by:

A) collecting the timesheets for the days accrued.

B) using the same amount as the prior month's adjustment.

C) using the wages of the salaried workers only.

D) a percentage of the previous week's gross payroll.

E) a percentage of the previous week's net payroll.

A) collecting the timesheets for the days accrued.

B) using the same amount as the prior month's adjustment.

C) using the wages of the salaried workers only.

D) a percentage of the previous week's gross payroll.

E) a percentage of the previous week's net payroll.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 75 في هذه المجموعة.

فتح الحزمة

k this deck

46

The garnishment that takes priority over all others is :

A) a federal tax levy

B) a government student loan

C) a creditor garnishment

D) an administrative wage garnishment

E) a child support order

A) a federal tax levy

B) a government student loan

C) a creditor garnishment

D) an administrative wage garnishment

E) a child support order

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 75 في هذه المجموعة.

فتح الحزمة

k this deck

47

Which of the following accounts is an expense account in which an employer records the FICA, FUTA, and SUTA taxes?

A) Wages Expense

B) Payroll Taxes

C) SUTA Taxes Payable

D) Salaries Payable

E) None of the above

A) Wages Expense

B) Payroll Taxes

C) SUTA Taxes Payable

D) Salaries Payable

E) None of the above

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 75 في هذه المجموعة.

فتح الحزمة

k this deck

48

The entry made at the end of the accounting period to record wages incurred but unpaid is:

A) Wages Expense Wages Payable

B) Wages Expense FICA Taxes Payable-OASDI

FICA Taxes Payable-HI

FIT Payable

Wages Payable

C) Wages Payable Cash

D) Wages Expense Cash

E) Wages Expense Payroll Taxes

Wages Payroll

A) Wages Expense Wages Payable

B) Wages Expense FICA Taxes Payable-OASDI

FICA Taxes Payable-HI

FIT Payable

Wages Payable

C) Wages Payable Cash

D) Wages Expense Cash

E) Wages Expense Payroll Taxes

Wages Payroll

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 75 في هذه المجموعة.

فتح الحزمة

k this deck

49

Which of the following items would require an adjusting entry at the end of each accounting period?

A) Garnishment for child support payments

B) Withholdings for a 401(k) plan

C) Vacation pay earned by employees

D) Union dues withheld

E) None of the above

A) Garnishment for child support payments

B) Withholdings for a 401(k) plan

C) Vacation pay earned by employees

D) Union dues withheld

E) None of the above

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 75 في هذه المجموعة.

فتح الحزمة

k this deck

50

The payroll register is used by employers in completing Forms W-2.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 75 في هذه المجموعة.

فتح الحزمة

k this deck

51

Which of the following is not an expense of the employer?

A) FUTA tax

B) FICA tax-HI

C) FICA tax-OASDI

D) SUTA tax

E) Union dues withheld

A) FUTA tax

B) FICA tax-HI

C) FICA tax-OASDI

D) SUTA tax

E) Union dues withheld

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 75 في هذه المجموعة.

فتح الحزمة

k this deck

52

Carmen Gaetano worked 46 hours during this payweek. He is paid time-and-a-half for hours over 40 and his pay rate is $17.90/hour. What was his overtime premium pay for this workweek?

A) $107.40

B) $161.10

C) $50.70

D) $53.70

E) $26.85

A) $107.40

B) $161.10

C) $50.70

D) $53.70

E) $26.85

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 75 في هذه المجموعة.

فتح الحزمة

k this deck

53

Exhibit 6-1

The totals from the first payroll of the year are shown below. Refer to Exhibit 6-1 . Journalize the entry to record the employer's payroll taxes (assume a SUTA rate of 3.7%).

The totals from the first payroll of the year are shown below.

Refer to Exhibit 6-1 . Journalize the entry to record the employer's payroll taxes (assume a SUTA rate of 3.7%). فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 75 في هذه المجموعة.

فتح الحزمة

k this deck

54

In the garnishment process, federal tax levies take secondary priority to wages withheld for child support orders.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 75 في هذه المجموعة.

فتح الحزمة

k this deck

55

The information needed in preparing a journal entry to record the wages earned, deductions from wages, and net amount paid each payday is obtained from the payroll register.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 75 في هذه المجموعة.

فتح الحزمة

k this deck

56

Exhibit 6-1 Refer to Exhibit 6-1 . Journalize the entry to record the payroll.

Refer to Exhibit 6-1 . Journalize the entry to record the payroll. فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 75 في هذه المجموعة.

فتح الحزمة

k this deck

57

The employer keeps track of each employee's accumulated wages in the employee's earnings record.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 75 في هذه المجموعة.

فتح الحزمة

k this deck

58

The employee's earnings record provides information for each of the following except :

A) completing Forms W-2.

B) completing the journal entry to record the payroll.

C) determining when the accumulated wages of an employee reach cutoff levels.

D) preparing reports required by state unemployment compensation laws.

E) preparing the payroll register.

A) completing Forms W-2.

B) completing the journal entry to record the payroll.

C) determining when the accumulated wages of an employee reach cutoff levels.

D) preparing reports required by state unemployment compensation laws.

E) preparing the payroll register.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 75 في هذه المجموعة.

فتح الحزمة

k this deck

59

In all computerized payroll systems, there is still the need to manually post from the printed payroll journal entry to the general ledger.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 75 في هذه المجموعة.

فتح الحزمة

k this deck

60

When recording the deposit of FUTA taxes owed, the proper entry is:

A) FUTA Tax Expense Cash

B) Payroll Taxes Cash

C) Payroll Taxes FUTA Taxes Payable

D) FUTA Taxes Payable Cash

E) FUTA Tax Expense FUTA Taxes Payable

A) FUTA Tax Expense Cash

B) Payroll Taxes Cash

C) Payroll Taxes FUTA Taxes Payable

D) FUTA Taxes Payable Cash

E) FUTA Tax Expense FUTA Taxes Payable

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 75 في هذه المجموعة.

فتح الحزمة

k this deck

61

Federal tax levies are not subject to the limits imposed on garnishments under the Consumer Credit Protection Act.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 75 في هذه المجموعة.

فتح الحزمة

k this deck

62

For child support garnishments, tips are considered part of an employee's disposable earnings.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 75 في هذه المجموعة.

فتح الحزمة

k this deck

63

Direct deposit of paychecks can be forced on employees in every state.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 75 في هذه المجموعة.

فتح الحزمة

k this deck

64

The employers' OASDI portion of FICA taxes is included as part of the payroll tax entry, but the employer's HI portion of FICA taxes is not.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 75 في هذه المجموعة.

فتح الحزمة

k this deck

65

In the case of a federal tax levy, the employee will notify the employer of the amount the employee wants taken out of his or her paycheck.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 75 في هذه المجموعة.

فتح الحزمة

k this deck

66

In the case of multiple wage attachments, a garnishment for a student loan has priority over any other garnishment.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 75 في هذه المجموعة.

فتح الحزمة

k this deck

67

When recording the employer's payroll taxes, a liability account entitled Employers Payroll Taxes Payable is credited for the total taxes owed (FICA, FUTA, and SUTA).

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 75 في هذه المجموعة.

فتح الحزمة

k this deck

68

FICA Taxes Payable-HI is a liability account in which is recorded the liability of the employer for the HI tax on the employer as well as for the HI tax withheld from employees' wages.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 75 في هذه المجموعة.

فتح الحزمة

k this deck

69

Disposable earnings are the earnings remaining after withholding only federal income taxes.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 75 في هذه المجموعة.

فتح الحزمة

k this deck

70

Journalize each of the payroll transactions listed below. Omit the writing of a description or explanation for each journal entry, and do not skip a line between each entry . Then post all entries except the last two to the appropriate general ledger accounts.

The balances listed in the general ledger accounts for Cash, FUTA Taxes Payable, SUTA Taxes Payable, Employees SIT Payable, Wages and Salaries, and Payroll Taxes are the results of all payroll transactions for the first quarter, not including the last pay of the quarter. The balances in FICA Taxes Payable-OASDI, FICA Taxes Payable-HI, and Employees FIT Payable are the amounts due from

the March 15 payroll.

March 31, 20--: Paid total wages of $9,350.00. These are the wages for the last semimonthly pay of March. All of this amount is taxable under FICA (OASDI and HI). In addition, withhold $1,175 for federal income taxes and $102.03 for state income taxes. These are the only deductions made from the employees' wages.

March 31, 20--: Record the employer's payroll taxes for the last pay in March. All of the earnings are taxable under FICA (OASDI and HI), FUTA (0.6%), and SUTA (2.8%).

April 15, 20--: Made a deposit to remove the liability for the FICA taxes and the employees' federal income taxes withheld on the two March payrolls.

May 2, 20--: Made the deposit to remove the liability for FUTA taxes for the first quarter of 20--.

May 2, 20--: Filed the state unemployment contributions return for the first quarter of 20-- and paid the total amount owed for the quarter to the state unemployment compensation fund.

May 2, 20--: Filed the state income tax return for the first quarter of 20-- and paid the total amount owed for the quarter to the state income tax bureau.

December 31, 20--: In July 20--, the company changed from a semimonthly pay system to a weekly pay system. The employees were paid every Friday through the rest of 20--. Record the adjusting entry for wages accrued at the end of December ($770) but not paid until the first Friday in January. Do not post this entry.

December 31, 20--: The company has determined that employees have earned $19,300 in unused vacation time. Record the adjusting entry to put this expense on the books. Do not post this entry.

The balances listed in the general ledger accounts for Cash, FUTA Taxes Payable, SUTA Taxes Payable, Employees SIT Payable, Wages and Salaries, and Payroll Taxes are the results of all payroll transactions for the first quarter, not including the last pay of the quarter. The balances in FICA Taxes Payable-OASDI, FICA Taxes Payable-HI, and Employees FIT Payable are the amounts due from

the March 15 payroll.

March 31, 20--: Paid total wages of $9,350.00. These are the wages for the last semimonthly pay of March. All of this amount is taxable under FICA (OASDI and HI). In addition, withhold $1,175 for federal income taxes and $102.03 for state income taxes. These are the only deductions made from the employees' wages.

March 31, 20--: Record the employer's payroll taxes for the last pay in March. All of the earnings are taxable under FICA (OASDI and HI), FUTA (0.6%), and SUTA (2.8%).

April 15, 20--: Made a deposit to remove the liability for the FICA taxes and the employees' federal income taxes withheld on the two March payrolls.

May 2, 20--: Made the deposit to remove the liability for FUTA taxes for the first quarter of 20--.

May 2, 20--: Filed the state unemployment contributions return for the first quarter of 20-- and paid the total amount owed for the quarter to the state unemployment compensation fund.

May 2, 20--: Filed the state income tax return for the first quarter of 20-- and paid the total amount owed for the quarter to the state income tax bureau.

December 31, 20--: In July 20--, the company changed from a semimonthly pay system to a weekly pay system. The employees were paid every Friday through the rest of 20--. Record the adjusting entry for wages accrued at the end of December ($770) but not paid until the first Friday in January. Do not post this entry.

December 31, 20--: The company has determined that employees have earned $19,300 in unused vacation time. Record the adjusting entry to put this expense on the books. Do not post this entry.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 75 في هذه المجموعة.

فتح الحزمة

k this deck

71

At the time of depositing FICA taxes and employees' federal income taxes, the account FICA Tax Expense is debited for both the employees' and the employer's portions of the FICA taxes.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 75 في هذه المجموعة.

فتح الحزمة

k this deck

72

For the purpose of a federal tax levy, the IRS defines take-home pay as the gross pay less taxes withheld and the other payroll deductions in effect before the tax levy was received.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 75 في هذه المجموعة.

فتح الحزمة

k this deck

73

The payment of the FUTA tax and the FICA taxes by the employer to the IRS is recorded in the same journal entry.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 75 في هذه المجموعة.

فتح الحزمة

k this deck

74

When union dues that have been withheld from employees' wages are turned over to the union treasurer, the account Union Dues Payable is debited.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 75 في هذه المجموعة.

فتح الحزمة

k this deck

75

In the case of an unclaimed paycheck, the employer can hold the check indefinitely until the employee or heirs claim the paycheck.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 75 في هذه المجموعة.

فتح الحزمة

k this deck

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 75 في هذه المجموعة.