Deck 9: Other Assurance Services, Internal and Governmental Financial Auditing and Operations Auditing

ملء الشاشة (f)

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

For reviews, an accountant does which of the following?

سؤال

سؤال

سؤال

سؤال

سؤال

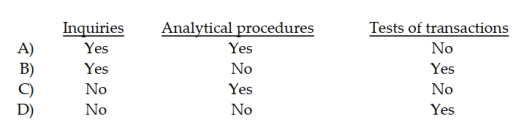

Evidence for a review engagement consists primarily of:

سؤال

Which of the following services is performed under AICPA attestation standards?

سؤال

سؤال

سؤال

سؤال

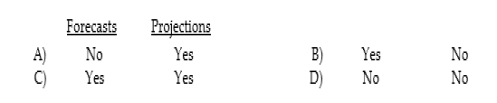

Which are prospective financial statements that present an entity's expected financial position, results of operations, and cash flows, to the best of the responsible party's knowledge and belief

سؤال

Which are prospective financial statements that present an entity's financial position, results of operations, and cash flows, to the best of the responsible party's knowledge and belief, given one or more hypothetical assumptions?

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

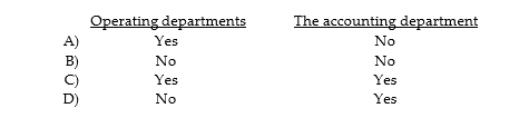

To be effective, an internal audit department must report to:

سؤال

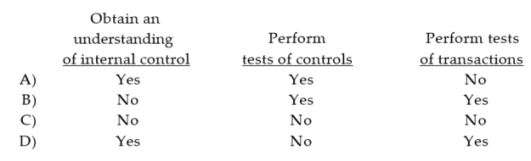

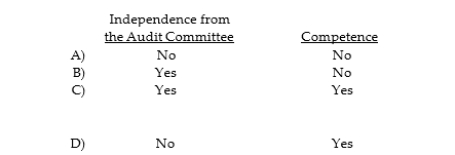

External financial statement auditors must obtain evidence regarding what attributes of an internal audit department if the external auditors intend to rely on the internal auditor's work?

A)

B)

C)

D)

A)

B)

C)

D)

سؤال

سؤال

سؤال

سؤال

سؤال

فتح الحزمة

قم بالتسجيل لفتح البطاقات في هذه المجموعة!

Unlock Deck

Unlock Deck

1/53

العب

ملء الشاشة (f)

Deck 9: Other Assurance Services, Internal and Governmental Financial Auditing and Operations Auditing

1

The two types of services provided in connection with ISRE 2410 and ISRS 4410:

A) examination and review services.

B) compilation and review services.

C) management advisory services and compilations.

D) audit and examination services.

A) examination and review services.

B) compilation and review services.

C) management advisory services and compilations.

D) audit and examination services.

compilation and review services.

2

Practitioners who perform compilation services are referred to in ISRS 4410 as:

A) auditors.

B) bookkeepers.

C) CPAs.

D) accountants.

A) auditors.

B) bookkeepers.

C) CPAs.

D) accountants.

accountants.

3

Which of these is a compilation report under IFRS 4410?

A) Compilation without independence.

B) Compilation with limited independence.

C) Compilation with a departure from the applicable financial reporting framework.

D) Compilation that omits substantially all disclosures.

A) Compilation without independence.

B) Compilation with limited independence.

C) Compilation with a departure from the applicable financial reporting framework.

D) Compilation that omits substantially all disclosures.

Compilation with a departure from the applicable financial reporting framework.

4

An examination results in a _______ conclusion.

A) equivocal

B) negative

C) positive

D) limited assurance

A) equivocal

B) negative

C) positive

D) limited assurance

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 53 في هذه المجموعة.

فتح الحزمة

k this deck

5

An auditing firm can issue a compilation report:

A) only if all the partners and the staff in the office performing the engagement are independent.

B) only if the partners are independent.

C) even if it is not independent.

D) if the partners have no material or direct immaterial interest in client.

A) only if all the partners and the staff in the office performing the engagement are independent.

B) only if the partners are independent.

C) even if it is not independent.

D) if the partners have no material or direct immaterial interest in client.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 53 في هذه المجموعة.

فتح الحزمة

k this deck

6

The distribution of which of the following types of reports is unrestricte?

A) Examinations and agreed- upon procedures.

B) Examinations and reviews.

C) Reviews and agreed- upon procedures.

D) Examinations, reviews, and agreed- upon procedures.

A) Examinations and agreed- upon procedures.

B) Examinations and reviews.

C) Reviews and agreed- upon procedures.

D) Examinations, reviews, and agreed- upon procedures.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 53 في هذه المجموعة.

فتح الحزمة

k this deck

7

For reviews, an accountant does which of the following?

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 53 في هذه المجموعة.

فتح الحزمة

k this deck

8

In the U.S., the AICPA has developed specific standards for assurance engagements in all but which of the following areas?

A) Prospective financial statements.

B) Compliance with laws and regulations.

C) Pro forma financial information.

D) Standards have been developed for all of the above.

A) Prospective financial statements.

B) Compliance with laws and regulations.

C) Pro forma financial information.

D) Standards have been developed for all of the above.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 53 في هذه المجموعة.

فتح الحزمة

k this deck

9

Which of the following is not an area of emphasis in a review conducted under ISRE 2410?

A) Make inquiries of management.

B) Obtain knowledge of the client.

C) Obtain knowledge of the accounting principles and practices of the client's industry.

D) Tests of internal controls.

A) Make inquiries of management.

B) Obtain knowledge of the client.

C) Obtain knowledge of the accounting principles and practices of the client's industry.

D) Tests of internal controls.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 53 في هذه المجموعة.

فتح الحزمة

k this deck

10

Distribution of which of the following types of reports is limited?

A) Audit.

B) Agreed- upon procedures.

C) Examination.

D) Review.

A) Audit.

B) Agreed- upon procedures.

C) Examination.

D) Review.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 53 في هذه المجموعة.

فتح الحزمة

k this deck

11

Which of the following forms of review are permissible under ISRE 2410

A) Reviews without auditor independence.

B) Review on financial statements that omit substantially all disclosures.

C) Review without limited procedures.

D) Review with limited assurance.

A) Reviews without auditor independence.

B) Review on financial statements that omit substantially all disclosures.

C) Review without limited procedures.

D) Review with limited assurance.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 53 في هذه المجموعة.

فتح الحزمة

k this deck

12

Evidence for a review engagement consists primarily of:

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 53 في هذه المجموعة.

فتح الحزمة

k this deck

13

Which of the following services is performed under AICPA attestation standards?

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 53 في هذه المجموعة.

فتح الحزمة

k this deck

14

Reports on debt compliance and similar engagements may be issued as a separate report or as part of a report that expresses the auditor's opinion on the financial statements. When they are issued as a part of the report on the financial statements, it is done by:

A) adding a middle paragraph before the opinion paragraph.

B) adding a paragraph between the introductory and scope paragraphs.

C) adding a paragraph after the opinion paragraph.

D) adding an additional phrase or sentence within the opinion paragraph.

A) adding a middle paragraph before the opinion paragraph.

B) adding a paragraph between the introductory and scope paragraphs.

C) adding a paragraph after the opinion paragraph.

D) adding an additional phrase or sentence within the opinion paragraph.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 53 في هذه المجموعة.

فتح الحزمة

k this deck

15

Which of the following is not required under ISAE 3000 for an assurance engagemet?

A) The engagement must serve as the basis for a positive conclusion.

B) The practitioner must have adequate knowledge of the subject matter sufficient understanding of the client's internal control.

C) The subject matter must be evaluated against suitable criteria.

D) An attitude of professional skepticism must be maintained.

A) The engagement must serve as the basis for a positive conclusion.

B) The practitioner must have adequate knowledge of the subject matter sufficient understanding of the client's internal control.

C) The subject matter must be evaluated against suitable criteria.

D) An attitude of professional skepticism must be maintained.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 53 في هذه المجموعة.

فتح الحزمة

k this deck

16

A report on an examination is _________ as to the distribution by the client after it is issued.

A) restricted

B) unrestricted

C) directed

D) limited

A) restricted

B) unrestricted

C) directed

D) limited

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 53 في هذه المجموعة.

فتح الحزمة

k this deck

17

Which are prospective financial statements that present an entity's expected financial position, results of operations, and cash flows, to the best of the responsible party's knowledge and belief

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 53 في هذه المجموعة.

فتح الحزمة

k this deck

18

Which are prospective financial statements that present an entity's financial position, results of operations, and cash flows, to the best of the responsible party's knowledge and belief, given one or more hypothetical assumptions?

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 53 في هذه المجموعة.

فتح الحزمة

k this deck

19

General use statements are prepared for use by:

A) known contractual parties.

B) regulators.

C) any third party.

D) internal auditor.

A) known contractual parties.

B) regulators.

C) any third party.

D) internal auditor.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 53 في هذه المجموعة.

فتح الحزمة

k this deck

20

Which of the following procedures is not included in a review service engagement?

A) Procedures designed to identify relationships among data that appear to be unusual.

B) A study and evaluation of internal control.

C) Inquiries of management.

D) Looking at the results of any internal audit and any subsequent actions taken by management.

A) Procedures designed to identify relationships among data that appear to be unusual.

B) A study and evaluation of internal control.

C) Inquiries of management.

D) Looking at the results of any internal audit and any subsequent actions taken by management.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 53 في هذه المجموعة.

فتح الحزمة

k this deck

21

Why do standards prohibit accepting an engagement on a projection for general use?

A) The auditor is not qualified to report on the use of accounting standards in the projected financial statement.

B) Underlying hypothetical assumptions are difficult to interpret without obtaining additional information.

C) Reports on projections are not well understood by the general public.

D) The auditor's procedures would violate auditing standards.

A) The auditor is not qualified to report on the use of accounting standards in the projected financial statement.

B) Underlying hypothetical assumptions are difficult to interpret without obtaining additional information.

C) Reports on projections are not well understood by the general public.

D) The auditor's procedures would violate auditing standards.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 53 في هذه المجموعة.

فتح الحزمة

k this deck

22

SysTrust engagements should be performed following guidance provided by the:

A) AICPA attestation standards.

B) AICPA accounting standards.

C) AICPA auditing standards.

D) AICPA review standards.

A) AICPA attestation standards.

B) AICPA accounting standards.

C) AICPA auditing standards.

D) AICPA review standards.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 53 في هذه المجموعة.

فتح الحزمة

k this deck

23

An auditor's standard report on the examination of a forecast should not include a:

A) statement that the prospective results may not be achieved.

B) an opinion on the reasonableness of management's assumptions.

C) statement that the auditor expresses only limited assurance that the results may be achieved.

D) disclaimer of responsibility to update the report for events occurring after the report's date.

A) statement that the prospective results may not be achieved.

B) an opinion on the reasonableness of management's assumptions.

C) statement that the auditor expresses only limited assurance that the results may be achieved.

D) disclaimer of responsibility to update the report for events occurring after the report's date.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 53 في هذه المجموعة.

فتح الحزمة

k this deck

24

ISRE 2410 recommends five main activities are performed during a financial statement review engagement, one of which is to 'perform analytical procedures.' State the other four.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 53 في هذه المجموعة.

فتح الحزمة

k this deck

25

Auditors frequently audit statements prepared on bases other than IFRS. Discuss four commonly used bases other than IFRS.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 53 في هذه المجموعة.

فتح الحزمة

k this deck

26

Draft a report that would be appropriate when an auditor has performed a compilation of financial statements in accordance with IFRS.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 53 في هذه المجموعة.

فتح الحزمة

k this deck

27

Draft a report that would be appropriate when an auditor has made a proper review of the financial statements of a nonpublic entity and has concluded they appear reasonable.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 53 في هذه المجموعة.

فتح الحزمة

k this deck

28

Discuss the main difference between an audit of specified elements, accounts, or items to a standard audit of financial statements in accordance with IFRS.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 53 في هذه المجموعة.

فتح الحزمة

k this deck

29

Match each the source of authoritative support for that engagement with the type of engagement

-Compilation of financial statements prepared in accordance with IFRS for a nonpublic company.

A) International Standards on Auditing

B) International Standard on Related Services (ISRS) 4410

C) International Standard on Assurance Engagements (ISAE) 3000

D) International Standard on Assurance Engagements (ISAE) 3400

E) International Standard on Review Engagements (ISRE) 2410

F) No standards have been set for these engagements

-Compilation of financial statements prepared in accordance with IFRS for a nonpublic company.

A) International Standards on Auditing

B) International Standard on Related Services (ISRS) 4410

C) International Standard on Assurance Engagements (ISAE) 3000

D) International Standard on Assurance Engagements (ISAE) 3400

E) International Standard on Review Engagements (ISRE) 2410

F) No standards have been set for these engagements

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 53 في هذه المجموعة.

فتح الحزمة

k this deck

30

Match each the source of authoritative support for that engagement with the type of engagement

-Examination of forecasted financial statements.

A) International Standards on Auditing

B) International Standard on Related Services (ISRS) 4411

C) International Standard on Assurance Engagements (ISAE) 3001

D) International Standard on Assurance Engagements (ISAE) 3401

E) International Standard on Review Engagements (ISRE) 2410

F) No standards have been set for these engagements

-Examination of forecasted financial statements.

A) International Standards on Auditing

B) International Standard on Related Services (ISRS) 4411

C) International Standard on Assurance Engagements (ISAE) 3001

D) International Standard on Assurance Engagements (ISAE) 3401

E) International Standard on Review Engagements (ISRE) 2410

F) No standards have been set for these engagements

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 53 في هذه المجموعة.

فتح الحزمة

k this deck

31

Match each the source of authoritative support for that engagement with the type of engagement

-Operational auditing.

A) International Standards on Auditing

B) International Standard on Related Services (ISRS) 4412

C) International Standard on Assurance Engagements (ISAE) 3002

D) International Standard on Assurance Engagements (ISAE) 3402

E) International Standard on Review Engagements (ISRE) 2410

F) No standards have been set for these engagements

-Operational auditing.

A) International Standards on Auditing

B) International Standard on Related Services (ISRS) 4412

C) International Standard on Assurance Engagements (ISAE) 3002

D) International Standard on Assurance Engagements (ISAE) 3402

E) International Standard on Review Engagements (ISRE) 2410

F) No standards have been set for these engagements

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 53 في هذه المجموعة.

فتح الحزمة

k this deck

32

Match each the source of authoritative support for that engagement with the type of engagement

-Audits of financial statements for a nonpublic entity prepared in accordance with IFRS.

A) International Standards on Auditing

B) International Standard on Related Services (ISRS) 4413

C) International Standard on Assurance Engagements (ISAE) 3003

D) International Standard on Assurance Engagements (ISAE) 3403

E) International Standard on Review Engagements (ISRE) 2410

F) No standards have been set for these engagements

-Audits of financial statements for a nonpublic entity prepared in accordance with IFRS.

A) International Standards on Auditing

B) International Standard on Related Services (ISRS) 4413

C) International Standard on Assurance Engagements (ISAE) 3003

D) International Standard on Assurance Engagements (ISAE) 3403

E) International Standard on Review Engagements (ISRE) 2410

F) No standards have been set for these engagements

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 53 في هذه المجموعة.

فتح الحزمة

k this deck

33

Match each the source of authoritative support for that engagement with the type of engagement

-Limited assurance engagements other than audits, reviews, or compilations of historical financial statements prepared in accordance with IFRS.

A) International Standards on Auditing

B) International Standard on Related Services (ISRS) 4414

C) International Standard on Assurance Engagements (ISAE) 3004

D) International Standard on Assurance Engagements (ISAE) 3404

E) International Standard on Review Engagements (ISRE) 2410

F) No standards have been set for these engagements

-Limited assurance engagements other than audits, reviews, or compilations of historical financial statements prepared in accordance with IFRS.

A) International Standards on Auditing

B) International Standard on Related Services (ISRS) 4414

C) International Standard on Assurance Engagements (ISAE) 3004

D) International Standard on Assurance Engagements (ISAE) 3404

E) International Standard on Review Engagements (ISRE) 2410

F) No standards have been set for these engagements

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 53 في هذه المجموعة.

فتح الحزمة

k this deck

34

Match each the source of authoritative support for that engagement with the type of engagement

-A review of unaudited financial statements designed to provide limited assurance that no material modifications need be made to the statements in order for them to be in conformity with IFRS.

A) International Standards on Auditing

B) International Standard on Related Services (ISRS) 4415

C) International Standard on Assurance Engagements (ISAE) 3005

D) International Standard on Assurance Engagements (ISAE) 3405

E) International Standard on Review Engagements (ISRE) 2410

F) No standards have been set for these engagements

-A review of unaudited financial statements designed to provide limited assurance that no material modifications need be made to the statements in order for them to be in conformity with IFRS.

A) International Standards on Auditing

B) International Standard on Related Services (ISRS) 4415

C) International Standard on Assurance Engagements (ISAE) 3005

D) International Standard on Assurance Engagements (ISAE) 3405

E) International Standard on Review Engagements (ISRE) 2410

F) No standards have been set for these engagements

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 53 في هذه المجموعة.

فتح الحزمة

k this deck

35

An accountant must be independent to issue a compilation report.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 53 في هذه المجموعة.

فتح الحزمة

k this deck

36

An auditor must be independent to undertake a review service engagement.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 53 في هذه المجموعة.

فتح الحزمة

k this deck

37

WebTrust services are performed under the direction of the IAASB.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 53 في هذه المجموعة.

فتح الحزمة

k this deck

38

When performing a review of financial statements, an auditor is required to obtain a letter of representation from management.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 53 في هذه المجموعة.

فتح الحزمة

k this deck

39

An auditing firm can issue a compilation report even if it is not independent with respect to the client.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 53 في هذه المجموعة.

فتح الحزمة

k this deck

40

The IIA Code of Ethics is based on all but which of the following ethical principles?

A) Competency.

B) Confidentiality.

C) Independence.

D) Integrity.

A) Competency.

B) Confidentiality.

C) Independence.

D) Integrity.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 53 في هذه المجموعة.

فتح الحزمة

k this deck

41

Statements on Internal Auditing Standards are issued by the:

A) FASB.

B) IAASB

C) AICPA.

D) IIA.

A) FASB.

B) IAASB

C) AICPA.

D) IIA.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 53 في هذه المجموعة.

فتح الحزمة

k this deck

42

Auditing standards ________ external auditors to use the internal auditors for direct assistance on the audit.

A) permit

B) prohibit

C) discourage

D) encourage

A) permit

B) prohibit

C) discourage

D) encourage

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 53 في هذه المجموعة.

فتح الحزمة

k this deck

43

Which of the following is not one of the broad categories of operational audits?

A) Special assignment audits.

B) Internal audits.

C) Organizational audits.

D) Functional audits.

A) Special assignment audits.

B) Internal audits.

C) Organizational audits.

D) Functional audits.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 53 في هذه المجموعة.

فتح الحزمة

k this deck

44

The IIA's professional practice framework (including its code of ethics and International Standards for the Professional Practice of Internal Auditing) is commonly referred to as the:

A) Red Book.

B) Green Book.

C) Blue Book.

D) Yellow Book.

A) Red Book.

B) Green Book.

C) Blue Book.

D) Yellow Book.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 53 في هذه المجموعة.

فتح الحزمة

k this deck

45

Which of the following can affect the independence of operational auditors?

A)

B)

C)

D)

A)

B)

C)

D)

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 53 في هذه المجموعة.

فتح الحزمة

k this deck

46

A(n)) ________audit emphasizes how efficiently and effectively functions interact.

A) financial

B) operational

C) organizational

D) compliance

A) financial

B) operational

C) organizational

D) compliance

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 53 في هذه المجموعة.

فتح الحزمة

k this deck

47

To be effective, an internal audit department must report to:

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 53 في هذه المجموعة.

فتح الحزمة

k this deck

48

External financial statement auditors must obtain evidence regarding what attributes of an internal audit department if the external auditors intend to rely on the internal auditor's work?

A)

B)

C)

D)

A)

B)

C)

D)

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 53 في هذه المجموعة.

فتح الحزمة

k this deck

49

What organization establishes auditing standards for internal auditors and what are those standards commonly called?

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 53 في هذه المجموعة.

فتح الحزمة

k this deck

50

Define internal auditing.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 53 في هذه المجموعة.

فتح الحزمة

k this deck

51

Discuss the main sources of criteria that an operational auditor can use to evaluate efficiency and effectiveness.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 53 في هذه المجموعة.

فتح الحزمة

k this deck

52

Operational audits are primarily geared toward compliance.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 53 في هذه المجموعة.

فتح الحزمة

k this deck

53

Reports of internal audits are standardized just as those for external audits.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 53 في هذه المجموعة.

فتح الحزمة

k this deck

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 53 في هذه المجموعة.