Deck 6: Completing the Tests in the Sales and Collection Cycle: Accounts Receivable, Audit Sampling for Tests of Details of Balances, and Audit of the Acquisition and Payment Cycle

ملء الشاشة (f)

سؤال

سؤال

سؤال

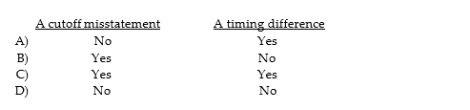

Cutoff misstatements occur when:

سؤال

سؤال

سؤال

A customer mails and records a check to a client for payment of an unpaid account on December 30. The client receives and records the amount on January 2. The records of the two organizations will be different on December 31. This represents:

سؤال

Cutoff misstatements can occur for:

سؤال

سؤال

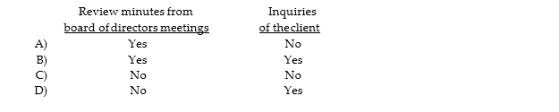

How might the auditor determine whether a client has limited rights to accounts receivable?

سؤال

سؤال

سؤال

سؤال

سؤال

Tests for rates of occurrence are appropriately used in all but which of the following situations?

سؤال

سؤال

سؤال

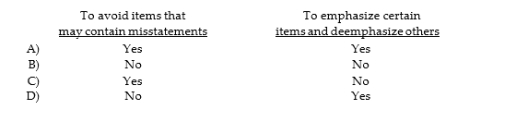

What is the purpose of applying stratified sampling to a population?

سؤال

سؤال

Tolerable misstatement is used to:

سؤال

سؤال

سؤال

سؤال

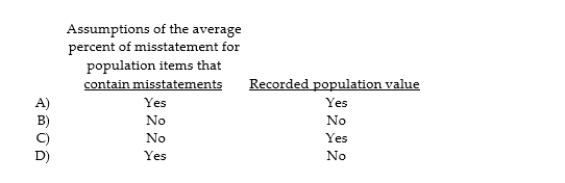

An auditor using nonstatistical sampling cannot formally measure sampling error and therefore must subjectively consider the possibility that the True population misstatement exceeds a tolerable amount. Which of the following factors should be considered by the auditor in making this assessment?

سؤال

سؤال

سؤال

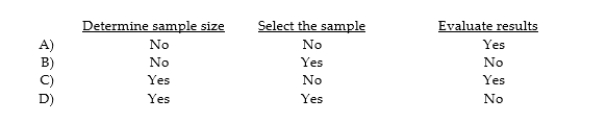

Which of the following does not need to be considered when the auditor generalizes from the sample to the population?

سؤال

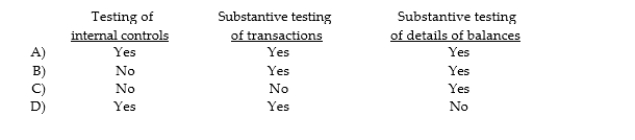

Which of the following items is not needed to apply MUS?

سؤال

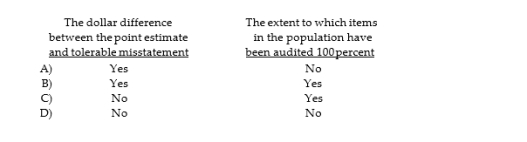

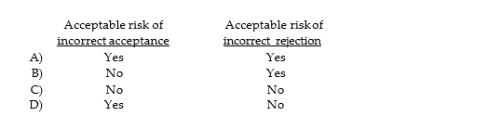

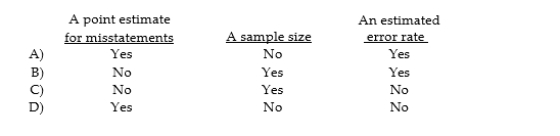

Calculating the sample size using monetary unit sampling depends on which of the following factors?

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

فتح الحزمة

قم بالتسجيل لفتح البطاقات في هذه المجموعة!

Unlock Deck

Unlock Deck

1/51

العب

ملء الشاشة (f)

Deck 6: Completing the Tests in the Sales and Collection Cycle: Accounts Receivable, Audit Sampling for Tests of Details of Balances, and Audit of the Acquisition and Payment Cycle

1

Which of the following is not a balance- related audit objective evaluated in the audit of accounts receivable?

A) Timing.

B) Completeness.

C) Accuracy.

D) Realizable value.

A) Timing.

B) Completeness.

C) Accuracy.

D) Realizable value.

Timing.

2

Which of the following is not a balance- related audit objective evaluated in the audit of accounts receivable?

A) Accuracy.

B) Completeness.

C) Occurrence.

D) Rights.

A) Accuracy.

B) Completeness.

C) Occurrence.

D) Rights.

Occurrence.

3

Cutoff misstatements occur when:

D

4

Accounting standards require that material sales returns and allowances be:

A) recorded in the period when the credit memo is issued.

B) recorded as a debit to the sales account.

C) matched with related sales.

D) recorded in the period when the merchandise is returned.

A) recorded in the period when the credit memo is issued.

B) recorded as a debit to the sales account.

C) matched with related sales.

D) recorded in the period when the merchandise is returned.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 51 في هذه المجموعة.

فتح الحزمة

k this deck

5

The most effective test of details of accounts receivable is the:

A) examination of sales invoices.

B) detail tie- in of the records.

C) confirmation of accounts receivable.

D) analysis of the allowance for doubtful accounts.

A) examination of sales invoices.

B) detail tie- in of the records.

C) confirmation of accounts receivable.

D) analysis of the allowance for doubtful accounts.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 51 في هذه المجموعة.

فتح الحزمة

k this deck

6

A customer mails and records a check to a client for payment of an unpaid account on December 30. The client receives and records the amount on January 2. The records of the two organizations will be different on December 31. This represents:

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 51 في هذه المجموعة.

فتح الحزمة

k this deck

7

Cutoff misstatements can occur for:

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 51 في هذه المجموعة.

فتح الحزمة

k this deck

8

Accounting standards require that sales returns and allowances be matched with related sales:

A) if required by industry practice.

B) if the amounts are material.

C) if practical.

D) any of the above.

A) if required by industry practice.

B) if the amounts are material.

C) if practical.

D) any of the above.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 51 في هذه المجموعة.

فتح الحزمة

k this deck

9

How might the auditor determine whether a client has limited rights to accounts receivable?

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 51 في هذه المجموعة.

فتح الحزمة

k this deck

10

Which of the following is the least important consideration in determining the sample size of confirmations?

A) Total annual credit sales.

B) The results of related analytical procedures.

C) The auditor's assessment of detection risk.

D) The types of confirmations being sent; that is, positive or negative

A) Total annual credit sales.

B) The results of related analytical procedures.

C) The auditor's assessment of detection risk.

D) The types of confirmations being sent; that is, positive or negative

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 51 في هذه المجموعة.

فتح الحزمة

k this deck

11

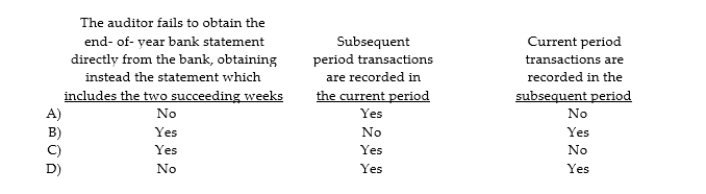

A threefold approach is typically followed when determining the reasonableness of cutoff. Briefly describe the threefold approach.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 51 في هذه المجموعة.

فتح الحزمة

k this deck

12

Sampling used for tests of details provides results in terms of:

A) percentages.

B) expectation rates.

C) dollars.

D) exception rates.

A) percentages.

B) expectation rates.

C) dollars.

D) exception rates.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 51 في هذه المجموعة.

فتح الحزمة

k this deck

13

Tolerable misstatements for overstatements and understatements:

A) must be expressed in percentages.

B) must be set at the same amount.

C) must be different amounts.

D) may be different amounts.

A) must be expressed in percentages.

B) must be set at the same amount.

C) must be different amounts.

D) may be different amounts.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 51 في هذه المجموعة.

فتح الحزمة

k this deck

14

Tests for rates of occurrence are appropriately used in all but which of the following situations?

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 51 في هذه المجموعة.

فتح الحزمة

k this deck

15

Which of the following is not a term relevant to sampling for tests of details?

A) Analysis of misstatements.

B) Define the exception conditions.

C) Estimate misstatements in the population.

D) Acceptable risk of incorrect acceptance.

A) Analysis of misstatements.

B) Define the exception conditions.

C) Estimate misstatements in the population.

D) Acceptable risk of incorrect acceptance.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 51 في هذه المجموعة.

فتح الحزمة

k this deck

16

When auditors sample for tests of details of balances, the objective is to determine whether the:

A) account balance being audited is fairly stated.

B) transactions being audited are free of misstatements.

C) controls being tested are operating effectively.

D) transactions and account balances being audited are fairly stated.

A) account balance being audited is fairly stated.

B) transactions being audited are free of misstatements.

C) controls being tested are operating effectively.

D) transactions and account balances being audited are fairly stated.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 51 في هذه المجموعة.

فتح الحزمة

k this deck

17

What is the purpose of applying stratified sampling to a population?

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 51 في هذه المجموعة.

فتح الحزمة

k this deck

18

Which of the following is not a likely item on which to apply stratification techniques?

A) Dollar value of accounts receivable.

B) Number of sales per customer in a period.

C) Customer names of account receivables.

D) Aging of accounts receivable.

A) Dollar value of accounts receivable.

B) Number of sales per customer in a period.

C) Customer names of account receivables.

D) Aging of accounts receivable.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 51 في هذه المجموعة.

فتح الحزمة

k this deck

19

Tolerable misstatement is used to:

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 51 في هذه المجموعة.

فتح الحزمة

k this deck

20

If acceptable audit risk is increased, ARIA should be:

A) unaffected.

B) reduced.

C) increased.

D) modified.

A) unaffected.

B) reduced.

C) increased.

D) modified.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 51 في هذه المجموعة.

فتح الحزمة

k this deck

21

As the acceptable risk of incorrect acceptance is reduced, the required sample size:

A) increases.

B) is unaffected.

C) decreases.

D) increases or decreases.

A) increases.

B) is unaffected.

C) decreases.

D) increases or decreases.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 51 في هذه المجموعة.

فتح الحزمة

k this deck

22

Which of the following is the auditor least likely to consider when estimating misstatements in the population?

A) Prior experience with the client.

B) Results of current year tests of controls.

C) Results of analytical procedures already performed.

D) Acceptable audit risk.

A) Prior experience with the client.

B) Results of current year tests of controls.

C) Results of analytical procedures already performed.

D) Acceptable audit risk.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 51 في هذه المجموعة.

فتح الحزمة

k this deck

23

An auditor using nonstatistical sampling cannot formally measure sampling error and therefore must subjectively consider the possibility that the True population misstatement exceeds a tolerable amount. Which of the following factors should be considered by the auditor in making this assessment?

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 51 في هذه المجموعة.

فتح الحزمة

k this deck

24

In a probability proportional to size (PPS) sample, all population physical audit units with an amount equal to or greater than the amount of the interval will automatically be included in the sample if the auditor uses:

A) stratified selection.

B) block selection.

C) systematic selection.

D) random selection.

A) stratified selection.

B) block selection.

C) systematic selection.

D) random selection.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 51 في هذه المجموعة.

فتح الحزمة

k this deck

25

Monetary unit sampling is also referred to as all of the following except:

A) sampling with probability proportional to size.

B) cumulative monetary amount sampling.

C) dollar unit sampling.

D) attribute sampling.

A) sampling with probability proportional to size.

B) cumulative monetary amount sampling.

C) dollar unit sampling.

D) attribute sampling.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 51 في هذه المجموعة.

فتح الحزمة

k this deck

26

Which of the following does not need to be considered when the auditor generalizes from the sample to the population?

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 51 في هذه المجموعة.

فتح الحزمة

k this deck

27

Which of the following items is not needed to apply MUS?

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 51 في هذه المجموعة.

فتح الحزمة

k this deck

28

Calculating the sample size using monetary unit sampling depends on which of the following factors?

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 51 في هذه المجموعة.

فتح الحزمة

k this deck

29

What are the three primary types of sampling methods used for calculating dollar misstatements in auditing?

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 51 في هذه المجموعة.

فتح الحزمة

k this deck

30

Explain ARIA and ARIR within the context of variables sampling.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 51 في هذه المجموعة.

فتح الحزمة

k this deck

31

Attributes sampling tables can be used to evaluate results of tests of details with ARACR being replaced with ARIA.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 51 في هذه المجموعة.

فتح الحزمة

k this deck

32

The primary factor affecting the auditor's decision about ARIA is assessed inherent risk.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 51 في هذه المجموعة.

فتح الحزمة

k this deck

33

The statistical results when MUS is used are called exception bounds.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 51 في هذه المجموعة.

فتح الحزمة

k this deck

34

The audit of the acquisition and payment cycle often takes ________ time to audit than other cycles.

A) less

B) no less

C) more

D) about the same

A) less

B) no less

C) more

D) about the same

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 51 في هذه المجموعة.

فتح الحزمة

k this deck

35

The receipt of goods and services in the normal course of business represents the date clients normally recognize:

A) income.

B) the liability.

C) expenses.

D) warranty assets.

A) income.

B) the liability.

C) expenses.

D) warranty assets.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 51 في هذه المجموعة.

فتح الحزمة

k this deck

36

The accounts payable account includes obligations for the acquisition of:

A) utilities.

B) equipment.

C) raw materials.

D) all three of the above.

A) utilities.

B) equipment.

C) raw materials.

D) all three of the above.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 51 في هذه المجموعة.

فتح الحزمة

k this deck

37

The computer- generated file that includes all acquisition transactions during a given period is the:

A) Accounts payable file.

B) Purchase approval file.

C) Acquisitions transaction file.

D) Cash disbursements file.

A) Accounts payable file.

B) Purchase approval file.

C) Acquisitions transaction file.

D) Cash disbursements file.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 51 في هذه المجموعة.

فتح الحزمة

k this deck

38

Tests of controls for the acquisition and payment cycle are usually divided into:

A) tests of acquisitions and payment.

B) tests of authorization and payment.

C) tests of authorization and acquisition.

D) tests of acquisitions and classification.

A) tests of acquisitions and payment.

B) tests of authorization and payment.

C) tests of authorization and acquisition.

D) tests of acquisitions and classification.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 51 في هذه المجموعة.

فتح الحزمة

k this deck

39

Which department should initiate a report when goods arrive from a vendor?

A) Manufacturing.

B) Receiving.

C) Treasury.

D) Accounting.

A) Manufacturing.

B) Receiving.

C) Treasury.

D) Accounting.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 51 في هذه المجموعة.

فتح الحزمة

k this deck

40

Once the auditor has decided on the specific procedures, the acquisitions tests and the cash disbursements tests are typically performed:

A) separately.

B) sequentially.

C) at the same time.

D) independently.

A) separately.

B) sequentially.

C) at the same time.

D) independently.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 51 في هذه المجموعة.

فتح الحزمة

k this deck

41

The most important controls over cash disbursements include all but which of the following?

A) Signing of checks by an authorized employee.

B) Random examination of the supporting documents by the authorized check signer before signing checks.

C) Prenumbering of checks and investigations of missing checks.

D) Separation of responsibilities for signing the checks and performing the accounts payable function.

A) Signing of checks by an authorized employee.

B) Random examination of the supporting documents by the authorized check signer before signing checks.

C) Prenumbering of checks and investigations of missing checks.

D) Separation of responsibilities for signing the checks and performing the accounts payable function.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 51 في هذه المجموعة.

فتح الحزمة

k this deck

42

The test of details of balances procedure to 'trace from account payable list to vendors' invoices and statements' satisfies the objective of:

A) detail tie- in.

B) classification.

C) completeness.

D) occurrence.

A) detail tie- in.

B) classification.

C) completeness.

D) occurrence.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 51 في هذه المجموعة.

فتح الحزمة

k this deck

43

A failure to record acquisitions of goods most likely will affect all but which of the following?

A) Cash.

B) Accounts payable.

C) Net income.

D) Retained earnings.

A) Cash.

B) Accounts payable.

C) Net income.

D) Retained earnings.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 51 في هذه المجموعة.

فتح الحزمة

k this deck

44

Assume that during cutoff testing you determined that the last receiving report number for inventory was 24986. Which of the following receiving report numbers would you not expect to be included in inventory and accounts payable at year- end?

A) 24980

B) 19773

C) 23019

D) 24990

A) 24980

B) 19773

C) 23019

D) 24990

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 51 في هذه المجموعة.

فتح الحزمة

k this deck

45

Which of the following is an effective internal accounting control over cash payments?

A) A check- signing machine with two signatures should be used.

B) Checks should be prepared only by persons responsible for cash receipts and disbursements.

C) Spoiled checks that have been voided should be disposed of immediately.

D) Signed checks should be mailed under the supervision of the check signer.

A) A check- signing machine with two signatures should be used.

B) Checks should be prepared only by persons responsible for cash receipts and disbursements.

C) Spoiled checks that have been voided should be disposed of immediately.

D) Signed checks should be mailed under the supervision of the check signer.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 51 في هذه المجموعة.

فتح الحزمة

k this deck

46

Which of the following statements is False?

A) The ownership objective is an important part of verifying assets but not liabilities.

B) The success of the auditor's search for unrecorded liabilities is not dependent upon the materiality of the potential balance in the account.

C) In auditing liabilities, the emphasis is on the search for understatements rather than overstatements.

D) Because of the emphasis on understatements in liability accounts, out- of- period liability tests are important for accounts payable.

A) The ownership objective is an important part of verifying assets but not liabilities.

B) The success of the auditor's search for unrecorded liabilities is not dependent upon the materiality of the potential balance in the account.

C) In auditing liabilities, the emphasis is on the search for understatements rather than overstatements.

D) Because of the emphasis on understatements in liability accounts, out- of- period liability tests are important for accounts payable.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 51 في هذه المجموعة.

فتح الحزمة

k this deck

47

Tests of controls and tests of transactions for the acquisition and payment cycle are normally divided into two broad areas. What are these areas?

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 51 في هذه المجموعة.

فتح الحزمة

k this deck

48

Explain why the confirmation of accounts payable is less common than confirmation of accounts receivable.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 51 في هذه المجموعة.

فتح الحزمة

k this deck

49

Discuss the difference in the auditor's approach to the audit of assets and the audit of liabilities.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 51 في هذه المجموعة.

فتح الحزمة

k this deck

50

Most companies recognize a liability when the goods are received by the company.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 51 في هذه المجموعة.

فتح الحزمة

k this deck

51

A bill of lading is normally prepared at the time tangible goods are received and indicates the description of goods, the quantity received, the date received, and other relevant data.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 51 في هذه المجموعة.

فتح الحزمة

k this deck

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 51 في هذه المجموعة.