Deck 12: Evaluating and Improving Entity Performance

ملء الشاشة (f)

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

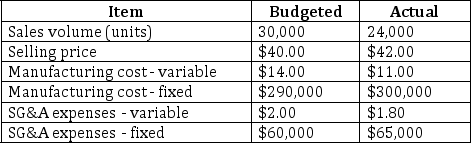

Custom Care, Inc., produces a wide variety of personal accessory products for men and women. One of the company's most popular items is a leather-covered cushioned carrying case for smartphones. The division that produces this case wants to better understand its performance over the last year and has assembled the information below to support its analysis.

Required:

Required:

a. Compute the sales volume variance for last year.

b. Compute the sales price variance for last year.

c. Compute the variable manufacturing cost variance for last year.

Required: a. Compute the sales volume variance for last year.

b. Compute the sales price variance for last year.

c. Compute the variable manufacturing cost variance for last year.

سؤال

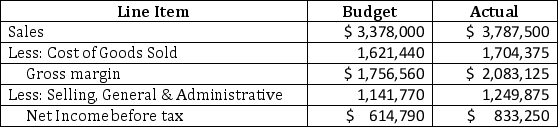

Thomas Enterprises reported the following actual vs. budgeted performance for its recently concluded year:

Required:

Required:

Compute the variances by line item for Thomas Enterprises.

Required:Compute the variances by line item for Thomas Enterprises.

سؤال

Volponi Limited produces and distributes high-quality feed products for thoroughbred racehorses. The business is highly competitive with narrow margins, and must be managed carefully to remain profitable. The company reports the following budgeted and actual results for the last year:

In order to analyze its performance, the company annually prepares a variance analysis. Using the data above:

In order to analyze its performance, the company annually prepares a variance analysis. Using the data above:

Required:

a. Compute the industry volume variance.

b. Compute the market share variance.

c. Compute the selling price variance.

In order to analyze its performance, the company annually prepares a variance analysis. Using the data above:Required:

a. Compute the industry volume variance.

b. Compute the market share variance.

c. Compute the selling price variance.

سؤال

Wolfe & Goodwin, LLC, manufactures a variety of security devices for residential and commercial use. The company is decentralized into Residential Products and Commercial Applications divisions. For their recently concluded year, the divisions reported the following budgeted and actual amounts for a motion detector and alarm that is produced in both residential and commercial models.

Required:

Required:

a. Compute the sales volume and sales price variances for the Residential Products and Commercial Applications divisions with respect to the motion detector.

b. Which division recorded the better performance? Why?

Required: a. Compute the sales volume and sales price variances for the Residential Products and Commercial Applications divisions with respect to the motion detector.

b. Which division recorded the better performance? Why?

فتح الحزمة

قم بالتسجيل لفتح البطاقات في هذه المجموعة!

Unlock Deck

Unlock Deck

1/44

العب

ملء الشاشة (f)

Deck 12: Evaluating and Improving Entity Performance

1

When assessing responsibility centers and their managers, performance measures are of no value unless some type of performance target or standard is available for comparison.

True

2

For performance evaluation purposes, any difference between a budgeted and actual result is classified as an unfavorable variance.

False

3

In order to fix responsibility for their occurrence, and analyze their underlying causes, variances must be disaggregated.

True

4

Disaggregating variances by income statement line item is a common and effective method for isolating the underlying causes of those variances.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 44 في هذه المجموعة.

فتح الحزمة

k this deck

5

A variance analysis prepared by Morton, Inc., indicated that two of the corporation's five divisions performed quite well in the past quarter, despite poor performance by the corporation as a whole. The variances used to reach this conclusion must have been disaggregated by responsibility center.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 44 في هذه المجموعة.

فتح الحزمة

k this deck

6

When preparing a static budget, all budgeted line item amounts are adjusted for the actual level of sales volume achieved.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 44 في هذه المجموعة.

فتح الحزمة

k this deck

7

A sales volume variance reflects the difference in the bottom line income number due to differences between the actual number of units sold and the number of units forecast in the flexible budget.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 44 في هذه المجموعة.

فتح الحزمة

k this deck

8

If a company falls short of the level of sales volume specified in a static budget, then the variable manufacturing cost will be adjusted upward in the flexible budget.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 44 في هذه المجموعة.

فتح الحزمة

k this deck

9

For a recently concluded period, Davis Company reported a favorable sales volume variance. This variance implies that the cost of goods sold in Davis' flexible budget will be larger than the amount included in its static budget.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 44 في هذه المجموعة.

فتح الحزمة

k this deck

10

The sales price variance is computed based on the actual number of units sold, not the number of units forecast in the static budget.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 44 في هذه المجموعة.

فتح الحزمة

k this deck

11

The industry volume variance is useful if management lacks the authority to reallocate resources from one industry to another.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 44 في هذه المجموعة.

فتح الحزمة

k this deck

12

Calculation of the market share variance is based on the budgeted volume for the industry in which the firm operates.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 44 في هذه المجموعة.

فتح الحزمة

k this deck

13

In an organization that values cooperation and synergies among divisional managers, relative performance evaluations may prove to be harmful.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 44 في هذه المجموعة.

فتح الحزمة

k this deck

14

The potential for favoritism bias is a serious limitation of relative performance evaluations.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 44 في هذه المجموعة.

فتح الحزمة

k this deck

15

Performance/reward functions that feature upper and lower limits often encourage gamesmanship on the part of managers.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 44 في هذه المجموعة.

فتح الحزمة

k this deck

16

K-Lane Industries, Inc., reported an unfavorable profit variance for its most recently concluded quarter. This implies that the company's:

A) Actual sales volume exceeded its static budgeted sales volume for the quarter.

B) Static budgeted sales volume exceeded its actual sales volume for the quarter.

C) Actual sales volume exceeded its flexible budget sales volume for the quarter.

D) Actual sales volume and static budgeted sales volume were equal for the quarter.

A) Actual sales volume exceeded its static budgeted sales volume for the quarter.

B) Static budgeted sales volume exceeded its actual sales volume for the quarter.

C) Actual sales volume exceeded its flexible budget sales volume for the quarter.

D) Actual sales volume and static budgeted sales volume were equal for the quarter.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 44 في هذه المجموعة.

فتح الحزمة

k this deck

17

A difference between a static budget amount for income and flexible budget amount is termed:

A) A profit variance.

B) An accounting return variance.

C) A sales volume variance.

D) A line item variance.

A) A profit variance.

B) An accounting return variance.

C) A sales volume variance.

D) A line item variance.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 44 في هذه المجموعة.

فتح الحزمة

k this deck

18

In the "check" and "adjust" phases of the business planning and analysis process, managers must evaluate measured performance and decide on what changes need to be made. The evaluation process cannot begin until:

A) Useful performance standards are established.

B) A SWOT analysis has been completed.

C) Best-in-practice external benchmarks are available.

D) The nature of responsibility centers is understood.

A) Useful performance standards are established.

B) A SWOT analysis has been completed.

C) Best-in-practice external benchmarks are available.

D) The nature of responsibility centers is understood.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 44 في هذه المجموعة.

فتح الحزمة

k this deck

19

"Management by exception" is an approach to the "check" and "adjust" phases of the business planning analysis process that is most often focused on:

A) Profit variances.

B) Unfavorable variances.

C) Both favorable and unfavorable variances.

D) Sales volume variances.

A) Profit variances.

B) Unfavorable variances.

C) Both favorable and unfavorable variances.

D) Sales volume variances.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 44 في هذه المجموعة.

فتح الحزمة

k this deck

20

A profit variance disaggregated by income statement line item is of limited value in a responsibility accounting system because:

A) The resulting variances lack detail.

B) The resulting variances are not available in a timely fashion.

C) The resulting variances are based on external benchmarks.

D) The resulting variances are based on inadequate financial accounting measures.

A) The resulting variances lack detail.

B) The resulting variances are not available in a timely fashion.

C) The resulting variances are based on external benchmarks.

D) The resulting variances are based on inadequate financial accounting measures.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 44 في هذه المجموعة.

فتح الحزمة

k this deck

21

Abrasive Brothers, Inc., manufactures brake pads for automobiles. For April 2017, the company's static budget projected 5,000 units would be produced and sold at a variable cost of $6 per unit and total fixed costs of $12,000. The budgeted selling price was $18 per unit. Actual results for April were somewhat disappointing in that the company produced and sold only 4,200 units at an actual price of $17.50 per unit.

-What sale volume variance would the company report for April?

A) 800 units Unfavorable.

B) $14,400 Unfavorable.

C) $14,000 Unfavorable.

D) $2,100 Unfavorable.

-What sale volume variance would the company report for April?

A) 800 units Unfavorable.

B) $14,400 Unfavorable.

C) $14,000 Unfavorable.

D) $2,100 Unfavorable.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 44 في هذه المجموعة.

فتح الحزمة

k this deck

22

Abrasive Brothers, Inc., manufactures brake pads for automobiles. For April 2017, the company's static budget projected 5,000 units would be produced and sold at a variable cost of $6 per unit and total fixed costs of $12,000. The budgeted selling price was $18 per unit. Actual results for April were somewhat disappointing in that the company produced and sold only 4,200 units at an actual price of $17.50 per unit.

-What sale price variance would the company report for April?

A) $0.50 Unfavorable.

B) $14,400 Unfavorable.

C) $14,000 Unfavorable.

D) $2,100 Unfavorable.

-What sale price variance would the company report for April?

A) $0.50 Unfavorable.

B) $14,400 Unfavorable.

C) $14,000 Unfavorable.

D) $2,100 Unfavorable.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 44 في هذه المجموعة.

فتح الحزمة

k this deck

23

Abrasive Brothers, Inc., manufactures brake pads for automobiles. For April 2017, the company's static budget projected 5,000 units would be produced and sold at a variable cost of $6 per unit and total fixed costs of $12,000. The budgeted selling price was $18 per unit. Actual results for April were somewhat disappointing in that the company produced and sold only 4,200 units at an actual price of $17.50 per unit.

-What would be the amount of cost of goods sold that would be included in a flexible budget for April 2017?

A) $30,000

B) $42,000

C) $25,200

D) $37,200

-What would be the amount of cost of goods sold that would be included in a flexible budget for April 2017?

A) $30,000

B) $42,000

C) $25,200

D) $37,200

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 44 في هذه المجموعة.

فتح الحزمة

k this deck

24

Abrasive Brothers, Inc., manufactures brake pads for automobiles. For April 2017, the company's static budget projected 5,000 units would be produced and sold at a variable cost of $6 per unit and total fixed costs of $12,000. The budgeted selling price was $18 per unit. Actual results for April were somewhat disappointing in that the company produced and sold only 4,200 units at an actual price of $17.50 per unit.

-The actual cost of goods sold for April amounted to $39,800. What would be the most meaningful variance to report for cost of goods sold for April?

A) $2,000 Favorable.

B) $2,600 Unfavorable.

C) $2,700 Favorable.

D) $2,100 Unfavorable.

-The actual cost of goods sold for April amounted to $39,800. What would be the most meaningful variance to report for cost of goods sold for April?

A) $2,000 Favorable.

B) $2,600 Unfavorable.

C) $2,700 Favorable.

D) $2,100 Unfavorable.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 44 في هذه المجموعة.

فتح الحزمة

k this deck

25

If the data is available regarding actual variable and fixed manufacturing costs, the difference between the actual cost of goods sold and its amount in the flexible budget, or the manufacturing cost variance, can be further disaggregated into:

A) The variable manufacturing cost variance and the fixed manufacturing cost variance.

B) The cost of goods sold price variance and efficiency variance.

C) The direct material price and efficiency variances.

D) The static budget variance and flexible budget variance.

A) The variable manufacturing cost variance and the fixed manufacturing cost variance.

B) The cost of goods sold price variance and efficiency variance.

C) The direct material price and efficiency variances.

D) The static budget variance and flexible budget variance.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 44 في هذه المجموعة.

فتح الحزمة

k this deck

26

Management in a key investment center of VR Industries achieved a return on investment of 18% in a recently concluded year. This fell short of the investment center's targeted ROI of 20%. The difference illustrates a(n):

A) Profit variance.

B) Sales volume variance.

C) Accounting return variance.

D) Line-item variance.

A) Profit variance.

B) Sales volume variance.

C) Accounting return variance.

D) Line-item variance.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 44 في هذه المجموعة.

فتح الحزمة

k this deck

27

The primary difference between a static and flexible budget is:

A) The level of output used to derive the budgeted amounts.

B) That static budgets are only prepared at the level of the investment center.

C) That static budgets are prepared for publication in external annual reports while flexible budgets are only internal documents.

D) That the flexible budget is always prepared on a rolling basis.

A) The level of output used to derive the budgeted amounts.

B) That static budgets are only prepared at the level of the investment center.

C) That static budgets are prepared for publication in external annual reports while flexible budgets are only internal documents.

D) That the flexible budget is always prepared on a rolling basis.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 44 في هذه المجموعة.

فتح الحزمة

k this deck

28

For a given year, the static budget of Norton and Cramden Company was developed based on forecasted sales of 12,000 units. Actual sales for the year totaled 14,000 units. The preparation of a flexible budget to evaluate performance by responsibility center should be based on:

A) 12,000 units.

B) 14,000 units.

C) The 13,000 units average of 12,000 and 14,000 units.

D) Some other amount.

A) 12,000 units.

B) 14,000 units.

C) The 13,000 units average of 12,000 and 14,000 units.

D) Some other amount.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 44 في هذه المجموعة.

فتح الحزمة

k this deck

29

A company contains several profit centers, all of which face the same numerous environmental and economic circumstances. In view of this, the company assesses the performance of it profit centers against one another rather than against budget targets. This style of performance assessment is called:

A) Variance analysis.

B) Management by exception.

C) Activity-based management.

D) Relative performance evaluation.

A) Variance analysis.

B) Management by exception.

C) Activity-based management.

D) Relative performance evaluation.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 44 في هذه المجموعة.

فتح الحزمة

k this deck

30

A drawback of relative performance evaluation systems is:

A) They do not require setting static budget targets.

B) They filter out uncontrollable effects in the environment.

C) They rely on benchmarks derived from the performance of similar units.

D) They provide no incentive for managers of different units to cooperate.

A) They do not require setting static budget targets.

B) They filter out uncontrollable effects in the environment.

C) They rely on benchmarks derived from the performance of similar units.

D) They provide no incentive for managers of different units to cooperate.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 44 في هذه المجموعة.

فتح الحزمة

k this deck

31

In recent years, Diageo plc has made a significant strategic commitment to reducing the company's carbon footprint. An unusual opportunity arose to make progress against this corporate goal by having a Canadian subsidiary substitute methane pumped from a local landfill for natural gas to power its manufacturing facility. Doing so, however, would negatively impact the income of the subsidiary and the performance evaluation of this investment center's management. The managers were assured by the corporation that adjustments would be made to their performance evaluations if they went ahead with the methane project. This incident illustrates the use of:

A) Subjective performance evaluation.

B) The industry volume variance.

C) The market share variance.

D) Expectancy theory.

A) Subjective performance evaluation.

B) The industry volume variance.

C) The market share variance.

D) Expectancy theory.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 44 في هذه المجموعة.

فتح الحزمة

k this deck

32

Subjective performance evaluation can be useful when:

A) Important aspects of performance are difficult to measure.

B) Evaluating start-up businesses that show large accounting losses in early years.

C) A responsibility center experiences a large and unforeseen event.

D) All of the above would argue for subjective evaluations.

A) Important aspects of performance are difficult to measure.

B) Evaluating start-up businesses that show large accounting losses in early years.

C) A responsibility center experiences a large and unforeseen event.

D) All of the above would argue for subjective evaluations.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 44 في هذه المجموعة.

فتح الحزمة

k this deck

33

Favoritism bias and hindsight bias are two of the significant disadvantages of:

A) Relative performance evaluation.

B) Line-item variance analysis.

C) Subjective performance evaluation.

D) Profit-driver profit variance analysis.

A) Relative performance evaluation.

B) Line-item variance analysis.

C) Subjective performance evaluation.

D) Profit-driver profit variance analysis.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 44 في هذه المجموعة.

فتح الحزمة

k this deck

34

Incentives are motivational tools intended to:

A) Induce employees to change their poor performances.

B) Enhance employee performance.

C) Prevent gamesmanship on the part of employees.

D) Avoid biases in performance evaluations.

A) Induce employees to change their poor performances.

B) Enhance employee performance.

C) Prevent gamesmanship on the part of employees.

D) Avoid biases in performance evaluations.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 44 في هذه المجموعة.

فتح الحزمة

k this deck

35

A motivational tool used not to enhance performance, but to discourage poor performance is termed:

A) A disincentive.

B) An incentive or reward.

C) The expectancy that an individual's behavior will accomplish a goal.

D) An unfavorable variance.

A) A disincentive.

B) An incentive or reward.

C) The expectancy that an individual's behavior will accomplish a goal.

D) An unfavorable variance.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 44 في هذه المجموعة.

فتح الحزمة

k this deck

36

Expectancy theory suggests that group incentive awards that are based on company performance:

A) Will be highly effective when the size of the group is large.

B) Will be highly effective because they place a high value on successful performance by the individual.

C) Will be relatively ineffective due to their effect on organization culture.

D) Will be relatively ineffective because individual managers may exert little influence on performance at the corporate level.

A) Will be highly effective when the size of the group is large.

B) Will be highly effective because they place a high value on successful performance by the individual.

C) Will be relatively ineffective due to their effect on organization culture.

D) Will be relatively ineffective because individual managers may exert little influence on performance at the corporate level.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 44 في هذه المجموعة.

فتح الحزمة

k this deck

37

One of the reasons that group incentive awards based on improved corporate performance are popular is:

A) The lack of correlation between corporate performance and the performance of individual responsibility center managers.

B) That the individual managers' motivation is largely independent of corporate performance.

C) That the group awards will result in reduced compensation expense and cash outflows when actual profits and cash inflows are below expectations.

D) That group awards function best in large organizations with numerous responsibility centers.

A) The lack of correlation between corporate performance and the performance of individual responsibility center managers.

B) That the individual managers' motivation is largely independent of corporate performance.

C) That the group awards will result in reduced compensation expense and cash outflows when actual profits and cash inflows are below expectations.

D) That group awards function best in large organizations with numerous responsibility centers.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 44 في هذه المجموعة.

فتح الحزمة

k this deck

38

Williams Corporation features a compensation system that offers a bonus above base salary for exceptional performance. Managers of all responsibility centers receive bonus payments if earnings per share is at least 10% larger than the previous year. If the increase in earnings per share is less than 10%, no bonus is paid. As the current year nears its close, it is apparent that the company's poor performance will make it impossible for management to reach the threshold for bonus payments. Under these circumstances, management will have an incentive:

A) To accelerate recognition of revenues from sales that will not be closed until the following year.

B) To further reduce earnings per share by accelerating the recognition of losses and expenses, thereby increasing the likelihood of exceeding the threshold next year.

C) Monitor each other's behaviors in an effort to find ways to improve earnings.

D) To implement new accounting principles such as a change from LIFO to FIFO in order to reduce expenses.

A) To accelerate recognition of revenues from sales that will not be closed until the following year.

B) To further reduce earnings per share by accelerating the recognition of losses and expenses, thereby increasing the likelihood of exceeding the threshold next year.

C) Monitor each other's behaviors in an effort to find ways to improve earnings.

D) To implement new accounting principles such as a change from LIFO to FIFO in order to reduce expenses.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 44 في هذه المجموعة.

فتح الحزمة

k this deck

39

TPC Company is considering a new incentive system under which bonuses will be awarded to divisional managers employing the following weights:

Division performance 15%

Corporate performance 70%

Individual performance 15%

Todd Brown, a divisional manager, believes he has minimal impact on overall corporate performance and only a 10% impact on group performance in his division. How motivating does expectancy theory suggest the new system will be for Brown?

A) Brown will have little motivation because of his limited ability to influence group and corporate performance.

B) Brown will have little motivation because his base salary is sufficiently large as to negate the influence of bonus payments.

C) Brown will be highly motivated since the bonus will reward his individual performance.

D) Brown will be highly motivated because he is personally risk-averse.

Division performance 15%

Corporate performance 70%

Individual performance 15%

Todd Brown, a divisional manager, believes he has minimal impact on overall corporate performance and only a 10% impact on group performance in his division. How motivating does expectancy theory suggest the new system will be for Brown?

A) Brown will have little motivation because of his limited ability to influence group and corporate performance.

B) Brown will have little motivation because his base salary is sufficiently large as to negate the influence of bonus payments.

C) Brown will be highly motivated since the bonus will reward his individual performance.

D) Brown will be highly motivated because he is personally risk-averse.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 44 في هذه المجموعة.

فتح الحزمة

k this deck

40

After the first three quarters of the year, Apex, Inc., was well ahead of its budgeted targets for corporate income and earnings per share. During the fourth quarter, the company found that divisional managers were holding sales open, thereby delaying revenue recognition to the following year. Several sales of assets expected to generate gains were also delayed for no apparent business reason. Given the behavior of its divisional managers during the fourth quarter, it is likely that:

A) Apex, Inc., employs a performance/reward function with a linear shape.

B) Apex, Inc., employs a performance/reward function with an upper limit or cap on bonus payments.

C) Apex, Inc., employs a performance/reward function with a floor.

D) Apex, Inc., does not provide incentive payments to divisional managers.

A) Apex, Inc., employs a performance/reward function with a linear shape.

B) Apex, Inc., employs a performance/reward function with an upper limit or cap on bonus payments.

C) Apex, Inc., employs a performance/reward function with a floor.

D) Apex, Inc., does not provide incentive payments to divisional managers.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 44 في هذه المجموعة.

فتح الحزمة

k this deck

41

Custom Care, Inc., produces a wide variety of personal accessory products for men and women. One of the company's most popular items is a leather-covered cushioned carrying case for smartphones. The division that produces this case wants to better understand its performance over the last year and has assembled the information below to support its analysis.

Required:

a. Compute the sales volume variance for last year.

b. Compute the sales price variance for last year.

c. Compute the variable manufacturing cost variance for last year.

Required: a. Compute the sales volume variance for last year.

b. Compute the sales price variance for last year.

c. Compute the variable manufacturing cost variance for last year.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 44 في هذه المجموعة.

فتح الحزمة

k this deck

42

Thomas Enterprises reported the following actual vs. budgeted performance for its recently concluded year:

Required:

Compute the variances by line item for Thomas Enterprises.

Required:Compute the variances by line item for Thomas Enterprises.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 44 في هذه المجموعة.

فتح الحزمة

k this deck

43

Volponi Limited produces and distributes high-quality feed products for thoroughbred racehorses. The business is highly competitive with narrow margins, and must be managed carefully to remain profitable. The company reports the following budgeted and actual results for the last year:

In order to analyze its performance, the company annually prepares a variance analysis. Using the data above:

Required:

a. Compute the industry volume variance.

b. Compute the market share variance.

c. Compute the selling price variance.

In order to analyze its performance, the company annually prepares a variance analysis. Using the data above:Required:

a. Compute the industry volume variance.

b. Compute the market share variance.

c. Compute the selling price variance.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 44 في هذه المجموعة.

فتح الحزمة

k this deck

44

Wolfe & Goodwin, LLC, manufactures a variety of security devices for residential and commercial use. The company is decentralized into Residential Products and Commercial Applications divisions. For their recently concluded year, the divisions reported the following budgeted and actual amounts for a motion detector and alarm that is produced in both residential and commercial models.

Required:

a. Compute the sales volume and sales price variances for the Residential Products and Commercial Applications divisions with respect to the motion detector.

b. Which division recorded the better performance? Why?

Required: a. Compute the sales volume and sales price variances for the Residential Products and Commercial Applications divisions with respect to the motion detector.

b. Which division recorded the better performance? Why?

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 44 في هذه المجموعة.

فتح الحزمة

k this deck

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 44 في هذه المجموعة.