Deck 15: Cost Allocation: Joint Products and Byproducts

ملء الشاشة (f)

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

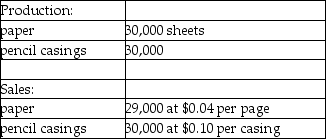

Use the information below to answer the following question(s).

Raynor Manufacturing purchases trees from Tree Nursery and processes them up to the splitoff point, where two products (paper and pencil casings) are obtained. The products are then sold to an independent company that markets and distributes them to retail outlets. The following information was collected for the month of October.

Trees processed:

50 trees (yield is 30,000 sheets of paper and 30,000 pencil casings and no scrap)

Cost of purchasing 50 trees and processing them up to the splitoff point to yield 30,000 sheets of paper and 30,000 pencil casings is $1,500.

Cost of purchasing 50 trees and processing them up to the splitoff point to yield 30,000 sheets of paper and 30,000 pencil casings is $1,500.

Raynor Manufacturing's accounting department reported no beginning inventories; however, ending inventory amounts reflected 1,000 sheets of paper in stock.

-What is the paper's sales value at the splitoff point?

A) $120

B) $1,160

C) $1,200

D) $1,950

E) $3,000

Raynor Manufacturing purchases trees from Tree Nursery and processes them up to the splitoff point, where two products (paper and pencil casings) are obtained. The products are then sold to an independent company that markets and distributes them to retail outlets. The following information was collected for the month of October.

Trees processed:

50 trees (yield is 30,000 sheets of paper and 30,000 pencil casings and no scrap)

Cost of purchasing 50 trees and processing them up to the splitoff point to yield 30,000 sheets of paper and 30,000 pencil casings is $1,500.Raynor Manufacturing's accounting department reported no beginning inventories; however, ending inventory amounts reflected 1,000 sheets of paper in stock.

-What is the paper's sales value at the splitoff point?

A) $120

B) $1,160

C) $1,200

D) $1,950

E) $3,000

سؤال

Use the information below to answer the following question(s).

Raynor Manufacturing purchases trees from Tree Nursery and processes them up to the splitoff point, where two products (paper and pencil casings) are obtained. The products are then sold to an independent company that markets and distributes them to retail outlets. The following information was collected for the month of October.

Trees processed:

50 trees (yield is 30,000 sheets of paper and 30,000 pencil casings and no scrap)

Cost of purchasing 50 trees and processing them up to the splitoff point to yield 30,000 sheets of paper and 30,000 pencil casings is $1,500.

Raynor Manufacturing's accounting department reported no beginning inventories; however, ending inventory amounts reflected 1,000 sheets of paper in stock.

-What are the paper's and the pencil's approximate weighted cost proportions using the sales value at splitoff method, respectively?

A) 28.57% and 71.43%

B) 33.33% and 66.67%

C) 40% and 60%

D) 49.00% and 51.00%

E) 50.00% and 50.00%

Raynor Manufacturing purchases trees from Tree Nursery and processes them up to the splitoff point, where two products (paper and pencil casings) are obtained. The products are then sold to an independent company that markets and distributes them to retail outlets. The following information was collected for the month of October.

Trees processed:

50 trees (yield is 30,000 sheets of paper and 30,000 pencil casings and no scrap)

Cost of purchasing 50 trees and processing them up to the splitoff point to yield 30,000 sheets of paper and 30,000 pencil casings is $1,500.Raynor Manufacturing's accounting department reported no beginning inventories; however, ending inventory amounts reflected 1,000 sheets of paper in stock.

-What are the paper's and the pencil's approximate weighted cost proportions using the sales value at splitoff method, respectively?

A) 28.57% and 71.43%

B) 33.33% and 66.67%

C) 40% and 60%

D) 49.00% and 51.00%

E) 50.00% and 50.00%

سؤال

Use the information below to answer the following question(s).

Chem Manufacturing Company processes direct materials up to the splitoff point, where two products (X and Y) are obtained and sold. The following information was collected for the month of November.

Direct materials processed:

10,000 litres (10,000 litres yield 9,500 litres of good product and 500 litres of shrinkage)

The cost of purchasing 10,000 litres of direct materials and processing it up to the splitoff point to yield a total of 9,500 litres of good products was $975,000.

The beginning inventories totalled 50 litres for X and 25 litres for Y. Ending inventory amounts reflected 300 litres of product X and 525 litres of product Y. October costs were per unit were the same as November.

-What are the respective physical volume proportions for products X and Y?

A) 55.00% and 45.00%

B) 54.00% and 46.00%

C) 52.63% and 47.37%

D) 47.37% and 53.63%

E) 36.36 % and 63.64%

Chem Manufacturing Company processes direct materials up to the splitoff point, where two products (X and Y) are obtained and sold. The following information was collected for the month of November.

Direct materials processed:

10,000 litres (10,000 litres yield 9,500 litres of good product and 500 litres of shrinkage)

The cost of purchasing 10,000 litres of direct materials and processing it up to the splitoff point to yield a total of 9,500 litres of good products was $975,000.

The beginning inventories totalled 50 litres for X and 25 litres for Y. Ending inventory amounts reflected 300 litres of product X and 525 litres of product Y. October costs were per unit were the same as November.

-What are the respective physical volume proportions for products X and Y?

A) 55.00% and 45.00%

B) 54.00% and 46.00%

C) 52.63% and 47.37%

D) 47.37% and 53.63%

E) 36.36 % and 63.64%

سؤال

Use the information below to answer the following question(s).

Chem Manufacturing Company processes direct materials up to the splitoff point, where two products (X and Y) are obtained and sold. The following information was collected for the month of November.

Direct materials processed:

10,000 litres (10,000 litres yield 9,500 litres of good product and 500 litres of shrinkage)

The cost of purchasing 10,000 litres of direct materials and processing it up to the splitoff point to yield a total of 9,500 litres of good products was $975,000.

The beginning inventories totalled 50 litres for X and 25 litres for Y. Ending inventory amounts reflected 300 litres of product X and 525 litres of product Y. October costs were per unit were the same as November.

-What is the approximate portion of the joint costs that should be allocated to products X and Y, respectively, using a physical volume measure?

A) $461,858 and $513,142

B) $487,500 and $487,500

C) $513,142 and $461,858

D) $529,285 and $445,715

E) $530,000 and $470,000

Chem Manufacturing Company processes direct materials up to the splitoff point, where two products (X and Y) are obtained and sold. The following information was collected for the month of November.

Direct materials processed:

10,000 litres (10,000 litres yield 9,500 litres of good product and 500 litres of shrinkage)

The cost of purchasing 10,000 litres of direct materials and processing it up to the splitoff point to yield a total of 9,500 litres of good products was $975,000.

The beginning inventories totalled 50 litres for X and 25 litres for Y. Ending inventory amounts reflected 300 litres of product X and 525 litres of product Y. October costs were per unit were the same as November.

-What is the approximate portion of the joint costs that should be allocated to products X and Y, respectively, using a physical volume measure?

A) $461,858 and $513,142

B) $487,500 and $487,500

C) $513,142 and $461,858

D) $529,285 and $445,715

E) $530,000 and $470,000

سؤال

سؤال

سؤال

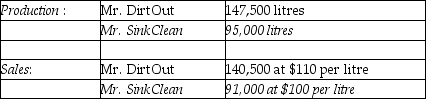

Answer the following question(s) using the information below.

The Oxnard Corporation processes a liquid component up to the splitoff point where two products, Mr. DirtOut and Mr. SinkClean, are produced and sold. There was no beginning inventory. The following material was collected for the month of January:

Direct materials processed: 250,000 litres (242,500 litres of good product)

The cost of purchasing 250,000 litres of direct materials and processing it up to the splitoff point to yield a total of 242,500 litres of good product was $380,000.

The cost of purchasing 250,000 litres of direct materials and processing it up to the splitoff point to yield a total of 242,500 litres of good product was $380,000.

-What are the physical volume proportions to allocate joint costs for Mr. DirtOut and Mr. SinkClean, respectively?

A) 59.00% and 41.00%

B) 60.82% and 39.18%

C) 39.18% and 60.82%

D) 59.79% and 40.21%

E) 41.00% and 59.00%

The Oxnard Corporation processes a liquid component up to the splitoff point where two products, Mr. DirtOut and Mr. SinkClean, are produced and sold. There was no beginning inventory. The following material was collected for the month of January:

Direct materials processed: 250,000 litres (242,500 litres of good product)

The cost of purchasing 250,000 litres of direct materials and processing it up to the splitoff point to yield a total of 242,500 litres of good product was $380,000.-What are the physical volume proportions to allocate joint costs for Mr. DirtOut and Mr. SinkClean, respectively?

A) 59.00% and 41.00%

B) 60.82% and 39.18%

C) 39.18% and 60.82%

D) 59.79% and 40.21%

E) 41.00% and 59.00%

سؤال

Answer the following question(s) using the information below.

The Oxnard Corporation processes a liquid component up to the splitoff point where two products, Mr. DirtOut and Mr. SinkClean, are produced and sold. There was no beginning inventory. The following material was collected for the month of January:

Direct materials processed: 250,000 litres (242,500 litres of good product)

The cost of purchasing 250,000 litres of direct materials and processing it up to the splitoff point to yield a total of 242,500 litres of good product was $380,000.

-When using a physical volume measure, what is the approximate amount of joint costs that will be allocated to Mr. DirtOut and Mr. SinkClean?

A) $231,116 and $148,884

B) $224,200 and $155,800

C) $227,202 and $152,798

D) $155,800 and $224,200

E) $148,884 and $231,116

The Oxnard Corporation processes a liquid component up to the splitoff point where two products, Mr. DirtOut and Mr. SinkClean, are produced and sold. There was no beginning inventory. The following material was collected for the month of January:

Direct materials processed: 250,000 litres (242,500 litres of good product)

The cost of purchasing 250,000 litres of direct materials and processing it up to the splitoff point to yield a total of 242,500 litres of good product was $380,000.-When using a physical volume measure, what is the approximate amount of joint costs that will be allocated to Mr. DirtOut and Mr. SinkClean?

A) $231,116 and $148,884

B) $224,200 and $155,800

C) $227,202 and $152,798

D) $155,800 and $224,200

E) $148,884 and $231,116

سؤال

Answer the following question(s) using the information below.

The Oxnard Corporation processes a liquid component up to the splitoff point where two products, Mr. DirtOut and Mr. SinkClean, are produced and sold. There was no beginning inventory. The following material was collected for the month of January:

Direct materials processed: 250,000 litres (242,500 litres of good product)

The cost of purchasing 250,000 litres of direct materials and processing it up to the splitoff point to yield a total of 242,500 litres of good product was $380,000.

-When using the physical measures method, what is Mr. DirtOut's approximate production cost per unit?

A) $1.52

B) $1.54

C) $1.57

D) $1.61

E) $1.01

The Oxnard Corporation processes a liquid component up to the splitoff point where two products, Mr. DirtOut and Mr. SinkClean, are produced and sold. There was no beginning inventory. The following material was collected for the month of January:

Direct materials processed: 250,000 litres (242,500 litres of good product)

The cost of purchasing 250,000 litres of direct materials and processing it up to the splitoff point to yield a total of 242,500 litres of good product was $380,000.-When using the physical measures method, what is Mr. DirtOut's approximate production cost per unit?

A) $1.52

B) $1.54

C) $1.57

D) $1.61

E) $1.01

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

Yip Manufacturing purchases trees from Cheney Lumber and processes them up to the splitoff point where two products (paper and pencil casings) are obtained. The products are then sold to an independent company that markets and distributes them to retail outlets. The following information was collected for the month of May:

The cost of purchasing 100 trees and processing them up to the splitoff point to yield 70,000 sheets of paper and 60,000 pencil casings is $3,000.

Yip's Manufacturing's accounting department reported no beginning inventories and an ending inventory of 2,000 sheets of paper.

What are the paper's and the pencils' approximate weighted cost proportions using the sales value at splitoff method, respectively?

A) 50.00% and 50.00%

B) 33.33% and 66.67%

C) 31.82% and 68.18%

D) 54.00% and 46.00%

E) 53.00% and 47.00%

The cost of purchasing 100 trees and processing them up to the splitoff point to yield 70,000 sheets of paper and 60,000 pencil casings is $3,000.

Yip's Manufacturing's accounting department reported no beginning inventories and an ending inventory of 2,000 sheets of paper.

What are the paper's and the pencils' approximate weighted cost proportions using the sales value at splitoff method, respectively?

A) 50.00% and 50.00%

B) 33.33% and 66.67%

C) 31.82% and 68.18%

D) 54.00% and 46.00%

E) 53.00% and 47.00%

سؤال

Use the information below to answer the following questions:

Argon Manufacturing Company processes direct materials up to the splitoff point where two products (U and V) are obtained and sold. The following information was collected for last quarter of the calendar year:

The cost of purchasing 20,000 gallons of direct materials and processing it up to the splitoff point to yield a total of 19,000 gallons of good products was $1,950,000.

Beginning inventories totaled 100 gallons for U and 50 gallons for V. Ending inventory amounts reflected 600 gallons of Product U and 1,050 gallons of Product V. October costs per unit were the same as November.

-What are the physical-volume proportions for products U and V, respectively?

A) 47.37% and 53.63%

B) 55.00% and 45.00%

C) 52.63% and 47.37%

D) 54.00% and 46.00%

E) 46.00% and 54.00%

Argon Manufacturing Company processes direct materials up to the splitoff point where two products (U and V) are obtained and sold. The following information was collected for last quarter of the calendar year:

The cost of purchasing 20,000 gallons of direct materials and processing it up to the splitoff point to yield a total of 19,000 gallons of good products was $1,950,000.

Beginning inventories totaled 100 gallons for U and 50 gallons for V. Ending inventory amounts reflected 600 gallons of Product U and 1,050 gallons of Product V. October costs per unit were the same as November.

-What are the physical-volume proportions for products U and V, respectively?

A) 47.37% and 53.63%

B) 55.00% and 45.00%

C) 52.63% and 47.37%

D) 54.00% and 46.00%

E) 46.00% and 54.00%

سؤال

Use the information below to answer the following questions:

Argon Manufacturing Company processes direct materials up to the splitoff point where two products (U and V) are obtained and sold. The following information was collected for last quarter of the calendar year:

The cost of purchasing 20,000 gallons of direct materials and processing it up to the splitoff point to yield a total of 19,000 gallons of good products was $1,950,000.

Beginning inventories totaled 100 gallons for U and 50 gallons for V. Ending inventory amounts reflected 600 gallons of Product U and 1,050 gallons of Product V. October costs per unit were the same as November.

-What is the joint cost allocation to product U using the sales value at splitoff method?

A) $1,218,750

B) $731,250

C) $1,248,876

D) $701,124

E) $1,026,285

Argon Manufacturing Company processes direct materials up to the splitoff point where two products (U and V) are obtained and sold. The following information was collected for last quarter of the calendar year:

The cost of purchasing 20,000 gallons of direct materials and processing it up to the splitoff point to yield a total of 19,000 gallons of good products was $1,950,000.

Beginning inventories totaled 100 gallons for U and 50 gallons for V. Ending inventory amounts reflected 600 gallons of Product U and 1,050 gallons of Product V. October costs per unit were the same as November.

-What is the joint cost allocation to product U using the sales value at splitoff method?

A) $1,218,750

B) $731,250

C) $1,248,876

D) $701,124

E) $1,026,285

سؤال

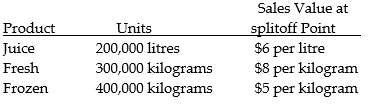

Peachland Fruit Ltd. harvests blueberries. After harvest, the company sells some berries fresh, freezes others, and processes some into juice. During the summer the joint costs of processing the berry products were $620,000. Any separable costs for each product are negligible and are not traced. There were no beginning or ending inventories for the summer. Production and sales value information for the summer were as follows:

Required:

Determine the amount allocated to each product if the sales value at splitoff method is used and compute the cost per case for each product.

Required:

Determine the amount allocated to each product if the sales value at splitoff method is used and compute the cost per case for each product.

سؤال

سؤال

سؤال

Use the information below to answer the following question(s).

Beverage Drink Company processes direct materials up to the splitoff point, where two products, A and B, are obtained. The following information was collected for the month of July:

Direct materials processed: 2,500 litres (with 20 percent shrinkage)

Cost of purchasing 2,500 litres of direct materials and processing it up to the splitoff point to yield a total of 2,000 litres of good products was $4,500. There were no inventory balances of A and B.

Cost of purchasing 2,500 litres of direct materials and processing it up to the splitoff point to yield a total of 2,000 litres of good products was $4,500. There were no inventory balances of A and B.

Product A may be processed further to yield 1,375 litres of Product Z5 for an additional processing cost of $150. Product Z5 is sold for $25.00 per litre. There was no beginning inventory and ending inventory was 125 litres.

Product B may be processed further to yield 375 litres of Product W3 for an additional processing cost of $275. Product W3 is sold for $30.00 per litre. There was no beginning inventory and ending inventory was 25 litres.

-What are the expected final sales values of production if Product Z5 and Product W3 are produced?

A) $11,250 and $34,375

B) $22,500 and $5,000

C) $31,250 and $10,500

D) $34,375 and $10,500

E) $34,375 and $11,250

Beverage Drink Company processes direct materials up to the splitoff point, where two products, A and B, are obtained. The following information was collected for the month of July:

Direct materials processed: 2,500 litres (with 20 percent shrinkage)

Cost of purchasing 2,500 litres of direct materials and processing it up to the splitoff point to yield a total of 2,000 litres of good products was $4,500. There were no inventory balances of A and B.Product A may be processed further to yield 1,375 litres of Product Z5 for an additional processing cost of $150. Product Z5 is sold for $25.00 per litre. There was no beginning inventory and ending inventory was 125 litres.

Product B may be processed further to yield 375 litres of Product W3 for an additional processing cost of $275. Product W3 is sold for $30.00 per litre. There was no beginning inventory and ending inventory was 25 litres.

-What are the expected final sales values of production if Product Z5 and Product W3 are produced?

A) $11,250 and $34,375

B) $22,500 and $5,000

C) $31,250 and $10,500

D) $34,375 and $10,500

E) $34,375 and $11,250

سؤال

Use the information below to answer the following question(s).

Beverage Drink Company processes direct materials up to the splitoff point, where two products, A and B, are obtained. The following information was collected for the month of July:

Direct materials processed: 2,500 litres (with 20 percent shrinkage)

Cost of purchasing 2,500 litres of direct materials and processing it up to the splitoff point to yield a total of 2,000 litres of good products was $4,500. There were no inventory balances of A and B.

Product A may be processed further to yield 1,375 litres of Product Z5 for an additional processing cost of $150. Product Z5 is sold for $25.00 per litre. There was no beginning inventory and ending inventory was 125 litres.

Product B may be processed further to yield 375 litres of Product W3 for an additional processing cost of $275. Product W3 is sold for $30.00 per litre. There was no beginning inventory and ending inventory was 25 litres.

-What is Product Z5's estimated net realizable value?

A) $11,100

B) $22,350

C) $34,225

D) $34,375

E) $34,525

Beverage Drink Company processes direct materials up to the splitoff point, where two products, A and B, are obtained. The following information was collected for the month of July:

Direct materials processed: 2,500 litres (with 20 percent shrinkage)

Cost of purchasing 2,500 litres of direct materials and processing it up to the splitoff point to yield a total of 2,000 litres of good products was $4,500. There were no inventory balances of A and B.Product A may be processed further to yield 1,375 litres of Product Z5 for an additional processing cost of $150. Product Z5 is sold for $25.00 per litre. There was no beginning inventory and ending inventory was 125 litres.

Product B may be processed further to yield 375 litres of Product W3 for an additional processing cost of $275. Product W3 is sold for $30.00 per litre. There was no beginning inventory and ending inventory was 25 litres.

-What is Product Z5's estimated net realizable value?

A) $11,100

B) $22,350

C) $34,225

D) $34,375

E) $34,525

سؤال

Answer the following question(s) using the information below:

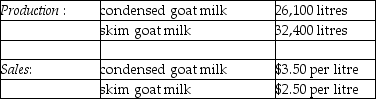

The Morton Company processes unprocessed goat milk up to the splitoff point where two products, condensed goat milk and skim goat milk result. The following information was collected for the month of October:

Direct Materials processed: 65,000 litres (shrinkage was 10%)

The costs of purchasing the 65,000 litres of unprocessed goat milk and processing it up to the splitoff point to yield a total of 58,500 litres of salable product was $72,240. There were no inventory balances of either product.

The costs of purchasing the 65,000 litres of unprocessed goat milk and processing it up to the splitoff point to yield a total of 58,500 litres of salable product was $72,240. There were no inventory balances of either product.

Condensed goat milk may be processed further to yield 19,500 litres (the remainder is shrinkage) of a medicinal milk product, Xyla, for an additional processing cost of $3 per usable litre. Xyla can be sold for $18 per litre.

Skim goat milk can be processed further to yield 28,100 litres of skim goat ice cream, for an additional processing cost per usable litre of $2.50. The product can be sold for $9 per litre.

There are no beginning and ending inventory balances.

-What is the estimated net realizable value of Xyla at the splitoff point?

A) $182,650

B) $252,900

C) $292,500

D) $351,000

E) $280,750

The Morton Company processes unprocessed goat milk up to the splitoff point where two products, condensed goat milk and skim goat milk result. The following information was collected for the month of October:

Direct Materials processed: 65,000 litres (shrinkage was 10%)

The costs of purchasing the 65,000 litres of unprocessed goat milk and processing it up to the splitoff point to yield a total of 58,500 litres of salable product was $72,240. There were no inventory balances of either product.Condensed goat milk may be processed further to yield 19,500 litres (the remainder is shrinkage) of a medicinal milk product, Xyla, for an additional processing cost of $3 per usable litre. Xyla can be sold for $18 per litre.

Skim goat milk can be processed further to yield 28,100 litres of skim goat ice cream, for an additional processing cost per usable litre of $2.50. The product can be sold for $9 per litre.

There are no beginning and ending inventory balances.

-What is the estimated net realizable value of Xyla at the splitoff point?

A) $182,650

B) $252,900

C) $292,500

D) $351,000

E) $280,750

سؤال

Answer the following question(s) using the information below:

The Morton Company processes unprocessed goat milk up to the splitoff point where two products, condensed goat milk and skim goat milk result. The following information was collected for the month of October:

Direct Materials processed: 65,000 litres (shrinkage was 10%)

The costs of purchasing the 65,000 litres of unprocessed goat milk and processing it up to the splitoff point to yield a total of 58,500 litres of salable product was $72,240. There were no inventory balances of either product.

Condensed goat milk may be processed further to yield 19,500 litres (the remainder is shrinkage) of a medicinal milk product, Xyla, for an additional processing cost of $3 per usable litre. Xyla can be sold for $18 per litre.

Skim goat milk can be processed further to yield 28,100 litres of skim goat ice cream, for an additional processing cost per usable litre of $2.50. The product can be sold for $9 per litre.

There are no beginning and ending inventory balances.

-What is the estimated net realizable value of the skim goat ice cream at the splitoff point?

A) $182,650

B) $252,900

C) $110,200

D) $85,450

E) $194,400

The Morton Company processes unprocessed goat milk up to the splitoff point where two products, condensed goat milk and skim goat milk result. The following information was collected for the month of October:

Direct Materials processed: 65,000 litres (shrinkage was 10%)

The costs of purchasing the 65,000 litres of unprocessed goat milk and processing it up to the splitoff point to yield a total of 58,500 litres of salable product was $72,240. There were no inventory balances of either product.Condensed goat milk may be processed further to yield 19,500 litres (the remainder is shrinkage) of a medicinal milk product, Xyla, for an additional processing cost of $3 per usable litre. Xyla can be sold for $18 per litre.

Skim goat milk can be processed further to yield 28,100 litres of skim goat ice cream, for an additional processing cost per usable litre of $2.50. The product can be sold for $9 per litre.

There are no beginning and ending inventory balances.

-What is the estimated net realizable value of the skim goat ice cream at the splitoff point?

A) $182,650

B) $252,900

C) $110,200

D) $85,450

E) $194,400

سؤال

Answer the following question(s) using the information below:

The Morton Company processes unprocessed goat milk up to the splitoff point where two products, condensed goat milk and skim goat milk result. The following information was collected for the month of October:

Direct Materials processed: 65,000 litres (shrinkage was 10%)

The costs of purchasing the 65,000 litres of unprocessed goat milk and processing it up to the splitoff point to yield a total of 58,500 litres of salable product was $72,240. There were no inventory balances of either product.

Condensed goat milk may be processed further to yield 19,500 litres (the remainder is shrinkage) of a medicinal milk product, Xyla, for an additional processing cost of $3 per usable litre. Xyla can be sold for $18 per litre.

Skim goat milk can be processed further to yield 28,100 litres of skim goat ice cream, for an additional processing cost per usable litre of $2.50. The product can be sold for $9 per litre.

There are no beginning and ending inventory balances.

-Using estimated net realizable value, what amount of the $72,240 of joint costs would be allocated Xyla and the skim goat ice cream?

A) $41,971 and $30,269

B) $44,471 and $27,769

C) $32,796 and $39,444

D) $36,120 and $36,120

E) $39,444 and $32,796

The Morton Company processes unprocessed goat milk up to the splitoff point where two products, condensed goat milk and skim goat milk result. The following information was collected for the month of October:

Direct Materials processed: 65,000 litres (shrinkage was 10%)

The costs of purchasing the 65,000 litres of unprocessed goat milk and processing it up to the splitoff point to yield a total of 58,500 litres of salable product was $72,240. There were no inventory balances of either product.Condensed goat milk may be processed further to yield 19,500 litres (the remainder is shrinkage) of a medicinal milk product, Xyla, for an additional processing cost of $3 per usable litre. Xyla can be sold for $18 per litre.

Skim goat milk can be processed further to yield 28,100 litres of skim goat ice cream, for an additional processing cost per usable litre of $2.50. The product can be sold for $9 per litre.

There are no beginning and ending inventory balances.

-Using estimated net realizable value, what amount of the $72,240 of joint costs would be allocated Xyla and the skim goat ice cream?

A) $41,971 and $30,269

B) $44,471 and $27,769

C) $32,796 and $39,444

D) $36,120 and $36,120

E) $39,444 and $32,796

سؤال

سؤال

سؤال

سؤال

سؤال

Blue Paper Company processes wood pulp into two products. During January the joint costs of processing were $144,000. Production and sales value information for the month were as follows:

Paper sells for $2.75 a kilogram and cardboard sells for $3.50 a kilogram.

There were no beginning inventories for January but ending inventories totalled 10,000 kilograms for paper and 12,000 kilograms for cardboard.

Required:

Prepare a product line income statement in gross margin format. Joint costs are allocated using the net realizable value method assuming all available product is sold.

Paper sells for $2.75 a kilogram and cardboard sells for $3.50 a kilogram.

There were no beginning inventories for January but ending inventories totalled 10,000 kilograms for paper and 12,000 kilograms for cardboard.

Required:

Prepare a product line income statement in gross margin format. Joint costs are allocated using the net realizable value method assuming all available product is sold.

سؤال

Red Paper Company processes wood pulp into two products. During March the joint costs of processing were $144,000. Production and sales value information for the month were as follows:

Paper sells for $2.75 a kilogram and cardboard sells for $3.50 a kilogram.

There were no beginning inventories for March but ending inventories totalled 10,000 kilograms for paper and 12,000 kilograms for cardboard.

Required:

Prepare a product line income statement assuming that joint costs are allocated on the constant gross margin percentage method based on total production. Present production costs and separable costs individually.

Paper sells for $2.75 a kilogram and cardboard sells for $3.50 a kilogram.

There were no beginning inventories for March but ending inventories totalled 10,000 kilograms for paper and 12,000 kilograms for cardboard.

Required:

Prepare a product line income statement assuming that joint costs are allocated on the constant gross margin percentage method based on total production. Present production costs and separable costs individually.

سؤال

Orange Paper Company processes wood pulp into two products. During April the joint costs of processing were $132,000. Production and sales value information for the month were as follows:

Paper sells for $2.65 a kilogram and cardboard sells for $3.40 a kilogram.

There were no beginning or ending inventories for April.

Required:

1. Determine the amounts to be allocated to each product using the:

a. estimated net realizable value method

b. sales value at splitoff method

2. If the cardboard is sold at the splitoff point then the post splitoff factory capacity can be renovated and leased for the year. The cost of the renovation is budgeted at $125,000 and the annual lease revenue will be $165,000. Determine if it is more profitable for the cardboard to be sold at the splitoff point or at the end of production.

Paper sells for $2.65 a kilogram and cardboard sells for $3.40 a kilogram.

There were no beginning or ending inventories for April.

Required:

1. Determine the amounts to be allocated to each product using the:

a. estimated net realizable value method

b. sales value at splitoff method

2. If the cardboard is sold at the splitoff point then the post splitoff factory capacity can be renovated and leased for the year. The cost of the renovation is budgeted at $125,000 and the annual lease revenue will be $165,000. Determine if it is more profitable for the cardboard to be sold at the splitoff point or at the end of production.

سؤال

Purple Paper Company processes wood pulp into two products. During July the joint costs of processing were $50,000. Production and sales value information for the month were as follows:

Paper sells for $2.71 a kilogram and cardboard sells for $3.10 a kilogram.

There were no beginning or ending inventories for July.

Required:

1. Determine the amounts to be allocated to each product using the:

a. constant gross margin percentage of NRV method

b. physical measure method

2. Should management process these products beyond the splitoff point? Justify your answer. Also comment on how this decision would be affected by the results of the expected profits using the constant gross margin percentage of NRV and physical measure methods.

Paper sells for $2.71 a kilogram and cardboard sells for $3.10 a kilogram.

There were no beginning or ending inventories for July.

Required:

1. Determine the amounts to be allocated to each product using the:

a. constant gross margin percentage of NRV method

b. physical measure method

2. Should management process these products beyond the splitoff point? Justify your answer. Also comment on how this decision would be affected by the results of the expected profits using the constant gross margin percentage of NRV and physical measure methods.

سؤال

Red Sauce Canning Company processes tomatoes into catsup, tomato juice, and canned tomatoes. During the summer the joint costs of processing the tomatoes were $420,000. There was no beginning or ending inventories for the summer. Production and sales value information for the summer were as follows:

Required:

Determine the amount allocated to each product if the estimated net realizable value method is used and compute the cost per case for each product.

Required:

Determine the amount allocated to each product if the estimated net realizable value method is used and compute the cost per case for each product.

سؤال

سؤال

سؤال

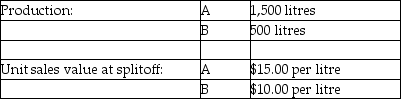

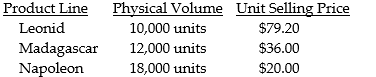

Framingham Ltd. produces three products out of a common process. The company currently uses the physical measures method to allocate joint costs to the three product lines: Leonid (L), Madagascar, (M) and Napoleon (N). The manager of the Napoleon product line is particularly disgruntled. He believes that his product line is allocated a disproportionate share of joint costs. In a recent managers' meeting, he argued that the company should consider using sales value as splitoff as the joint cost allocation method. He stated that his product is sold in a highly competitive market and increasing price is not an option.

The manager of the Leonid product line disagreed strongly. He stated that all products are sold in a competitive market place and that allocating joint costs on physical measures was simple and easily verifiable. The manager of the Madagascar product line sat quietly through the meeting and she did not seem to favour one method over the other.

As the assistant controller, you were asked by the controller to look into the concerns of the product line managers. The following additional information is available:

Product Line Physical Volume Unit Selling Price

Required:

As the assistant controller, prepare a report to the controller.

The manager of the Leonid product line disagreed strongly. He stated that all products are sold in a competitive market place and that allocating joint costs on physical measures was simple and easily verifiable. The manager of the Madagascar product line sat quietly through the meeting and she did not seem to favour one method over the other.

As the assistant controller, you were asked by the controller to look into the concerns of the product line managers. The following additional information is available:

Product Line Physical Volume Unit Selling Price

Required:

As the assistant controller, prepare a report to the controller.

سؤال

سؤال

سؤال

Helen Company processes 30,000 litres of direct materials to produce two products, Zander and Ifso. Zander, a byproduct, sells for $5 per litre, and Ifso, the main product, sells for $70 per litre. The following information is for July:

The manufacturing costs totalled $145,000; beginning inventory $3,000.

Required:

1. Prepare a July income statement assuming that Helen Company recognizes the byproduct net realizable value when production is completed. The company uses FIFO for the inventory flow assumption.

2. Prepare the journal entry to record the byproduct sales.

The manufacturing costs totalled $145,000; beginning inventory $3,000.

Required:

1. Prepare a July income statement assuming that Helen Company recognizes the byproduct net realizable value when production is completed. The company uses FIFO for the inventory flow assumption.

2. Prepare the journal entry to record the byproduct sales.

سؤال

Helen Company processes 30,000 litres of direct materials to produce two products, Zander and Ifso. Zander, a byproduct, sells for $5 per litre, and Ifso, the main product, sells for $70 per litre. The following information is for July:

The manufacturing costs totalled $145,000; beginning inventory $3,000.

Required:

1. Prepare a July income statement assuming that Helen Company recognizes the byproduct revenue at the time of sale. The company uses FIFO for the inventory flow assumption.

2. Prepare the journal entry to record the byproduct sales.

The manufacturing costs totalled $145,000; beginning inventory $3,000.

Required:

1. Prepare a July income statement assuming that Helen Company recognizes the byproduct revenue at the time of sale. The company uses FIFO for the inventory flow assumption.

2. Prepare the journal entry to record the byproduct sales.

سؤال

فتح الحزمة

قم بالتسجيل لفتح البطاقات في هذه المجموعة!

Unlock Deck

Unlock Deck

1/57

العب

ملء الشاشة (f)

Deck 15: Cost Allocation: Joint Products and Byproducts

1

Which of the following is FALSE concerning manufacturing of joint products and joint costing?

A) The number of outputs produced may exceed the number of products.

B) An output from the process may be recycled without any value being added by its production.

C) Some outputs from a joint process have no value and are not recognized in the accounting system.

D) The physical quantity of outputs not recognized in the accounting system, can exceed the quantities of outputs that recognized in the accounting system.

E) Joint processes always yield either scrap or byproducts.

A) The number of outputs produced may exceed the number of products.

B) An output from the process may be recycled without any value being added by its production.

C) Some outputs from a joint process have no value and are not recognized in the accounting system.

D) The physical quantity of outputs not recognized in the accounting system, can exceed the quantities of outputs that recognized in the accounting system.

E) Joint processes always yield either scrap or byproducts.

Joint processes always yield either scrap or byproducts.

2

A business which enters into a contract to purchase a product (or products) and will compensate the manufacturer under a cost reimbursement formula, should take an active part in the determination of how joint costs are allocated because

A) it is important in the understanding of the cause-and-effect relationship.

B) if the manufacturer successfully allocates a large portion of its costs to these products then it will be able to sell its other nonreimbursed products at lower prices.

C) the ASPE/IFRS requires the business to participate in the cost allocation process.

D) they are used in the calculation of the suppliers inventoriable costs.

E) sales discounts often depend on joint cost allocation amounts.

A) it is important in the understanding of the cause-and-effect relationship.

B) if the manufacturer successfully allocates a large portion of its costs to these products then it will be able to sell its other nonreimbursed products at lower prices.

C) the ASPE/IFRS requires the business to participate in the cost allocation process.

D) they are used in the calculation of the suppliers inventoriable costs.

E) sales discounts often depend on joint cost allocation amounts.

if the manufacturer successfully allocates a large portion of its costs to these products then it will be able to sell its other nonreimbursed products at lower prices.

3

Which of the following is NOT a reason underlying the importance of allocations for inventory costing and cost of goods sold computations?

A) Inventory costing is essential for proper balance sheet presentation.

B) Divisional profitability may affect compensation for divisional managers.

C) Cost of goods sold is an important component in the determination of net income.

D) The information may be required for insurance settlement or litigation.

E) Sell work-in -process or process further decisions prior to the splitoff point.

A) Inventory costing is essential for proper balance sheet presentation.

B) Divisional profitability may affect compensation for divisional managers.

C) Cost of goods sold is an important component in the determination of net income.

D) The information may be required for insurance settlement or litigation.

E) Sell work-in -process or process further decisions prior to the splitoff point.

Sell work-in -process or process further decisions prior to the splitoff point.

4

Which of the following is TRUE regarding the costs of toxic waste disposal, reclamation, and remediation that result from joint production processing?

A) Toxic waste costs are treated in the same manner byproduct costs.

B) Disposal costs should be expensed, other costs charged to cost of goods sold.

C) The costs should be valued in inventory at net realizable value.

D) Toxic waste costs are a life-cycle cost that should be added to joint production costs prior to allocation.

E) All toxic waste costs should be expensed as do not form part of the product.

A) Toxic waste costs are treated in the same manner byproduct costs.

B) Disposal costs should be expensed, other costs charged to cost of goods sold.

C) The costs should be valued in inventory at net realizable value.

D) Toxic waste costs are a life-cycle cost that should be added to joint production costs prior to allocation.

E) All toxic waste costs should be expensed as do not form part of the product.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 57 في هذه المجموعة.

فتح الحزمة

k this deck

5

Match each of the following costs with the appropriate joint production process cost classification.

-Bones from a butcher shop

A) scrap

B) main product

C) byproduct

D) joint product

-Bones from a butcher shop

A) scrap

B) main product

C) byproduct

D) joint product

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 57 في هذه المجموعة.

فتح الحزمة

k this deck

6

Match each of the following costs with the appropriate joint production process cost classification.

-Sawdust from a sawmill

A) scrap

B) main product

C) byproduct

D) joint product

-Sawdust from a sawmill

A) scrap

B) main product

C) byproduct

D) joint product

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 57 في هذه المجموعة.

فتح الحزمة

k this deck

7

Match each of the following costs with the appropriate joint production process cost classification.

-Sawdust from a furniture manufacturer

A) scrap

B) main product

C) byproduct

D) joint product

-Sawdust from a furniture manufacturer

A) scrap

B) main product

C) byproduct

D) joint product

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 57 في هذه المجموعة.

فتح الحزمة

k this deck

8

Match each of the following costs with the appropriate joint production process cost classification.

-Fuel oil from petroleum processing

A) scrap

B) main product

C) byproduct

D) joint product

-Fuel oil from petroleum processing

A) scrap

B) main product

C) byproduct

D) joint product

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 57 في هذه المجموعة.

فتح الحزمة

k this deck

9

Match each of the following costs with the appropriate joint production process cost classification.

-Salt from a salt works process

A) scrap

B) main product

C) byproduct

D) joint product

-Salt from a salt works process

A) scrap

B) main product

C) byproduct

D) joint product

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 57 في هذه المجموعة.

فتح الحزمة

k this deck

10

Match each of the following costs with the appropriate joint production process cost classification.

-Broth from cooking food

A) scrap

B) main product

C) byproduct

D) joint product

-Broth from cooking food

A) scrap

B) main product

C) byproduct

D) joint product

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 57 في هذه المجموعة.

فتح الحزمة

k this deck

11

Match each of the following costs with the appropriate joint production process cost classification.

-Raw milk for dairy processing

A) scrap

B) main product

C) byproduct

D) joint product

-Raw milk for dairy processing

A) scrap

B) main product

C) byproduct

D) joint product

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 57 في هذه المجموعة.

فتح الحزمة

k this deck

12

Match each of the following costs with the appropriate joint production process cost classification.

-Skim milk from dairy processing

A) scrap

B) main product

C) byproduct

D) joint product

-Skim milk from dairy processing

A) scrap

B) main product

C) byproduct

D) joint product

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 57 في هذه المجموعة.

فتح الحزمة

k this deck

13

In each of the following industries, identify possible joint (or severable) products at the splitoff point.

a. Coal

b. Petroleum

c. Dairy

d. Lamb

e. Lumber

f. Cocoa Beans

g. Christmas Trees

h. Salt

i. Cowhide

a. Coal

b. Petroleum

c. Dairy

d. Lamb

e. Lumber

f. Cocoa Beans

g. Christmas Trees

h. Salt

i. Cowhide

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 57 في هذه المجموعة.

فتح الحزمة

k this deck

14

Golden Company uses one raw material, gold ore, for all its products. It spends considerable time getting the gold from the ore before it starts the actual processing of the finished products, rings, lockets, etc. Traditionally, the company made one product at a time and charged the product with all costs of production, from ore to final inspection. However, in recent months the cost accounting reports have been somewhat disturbing to management. It seems that some of the finished products are costing more than they should, even to the point of approaching their retail value. It has been noted by the accounting manager that this problem began when the company started buying ore from different parts of the world, some of which requires difficult extraction methods.

Required:

Can you explain how the company might change its accounting system to better reflect the reporting problems? Are there other problems with the purchasing area?

Required:

Can you explain how the company might change its accounting system to better reflect the reporting problems? Are there other problems with the purchasing area?

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 57 في هذه المجموعة.

فتح الحزمة

k this deck

15

Use the information below to answer the following question(s).

Raynor Manufacturing purchases trees from Tree Nursery and processes them up to the splitoff point, where two products (paper and pencil casings) are obtained. The products are then sold to an independent company that markets and distributes them to retail outlets. The following information was collected for the month of October.

Trees processed:

50 trees (yield is 30,000 sheets of paper and 30,000 pencil casings and no scrap)

Cost of purchasing 50 trees and processing them up to the splitoff point to yield 30,000 sheets of paper and 30,000 pencil casings is $1,500.

Raynor Manufacturing's accounting department reported no beginning inventories; however, ending inventory amounts reflected 1,000 sheets of paper in stock.

-What is the paper's sales value at the splitoff point?

A) $120

B) $1,160

C) $1,200

D) $1,950

E) $3,000

Raynor Manufacturing purchases trees from Tree Nursery and processes them up to the splitoff point, where two products (paper and pencil casings) are obtained. The products are then sold to an independent company that markets and distributes them to retail outlets. The following information was collected for the month of October.

Trees processed:

50 trees (yield is 30,000 sheets of paper and 30,000 pencil casings and no scrap)

Cost of purchasing 50 trees and processing them up to the splitoff point to yield 30,000 sheets of paper and 30,000 pencil casings is $1,500.Raynor Manufacturing's accounting department reported no beginning inventories; however, ending inventory amounts reflected 1,000 sheets of paper in stock.

-What is the paper's sales value at the splitoff point?

A) $120

B) $1,160

C) $1,200

D) $1,950

E) $3,000

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 57 في هذه المجموعة.

فتح الحزمة

k this deck

16

Use the information below to answer the following question(s).

Raynor Manufacturing purchases trees from Tree Nursery and processes them up to the splitoff point, where two products (paper and pencil casings) are obtained. The products are then sold to an independent company that markets and distributes them to retail outlets. The following information was collected for the month of October.

Trees processed:

50 trees (yield is 30,000 sheets of paper and 30,000 pencil casings and no scrap)

Cost of purchasing 50 trees and processing them up to the splitoff point to yield 30,000 sheets of paper and 30,000 pencil casings is $1,500.

Raynor Manufacturing's accounting department reported no beginning inventories; however, ending inventory amounts reflected 1,000 sheets of paper in stock.

-What are the paper's and the pencil's approximate weighted cost proportions using the sales value at splitoff method, respectively?

A) 28.57% and 71.43%

B) 33.33% and 66.67%

C) 40% and 60%

D) 49.00% and 51.00%

E) 50.00% and 50.00%

Raynor Manufacturing purchases trees from Tree Nursery and processes them up to the splitoff point, where two products (paper and pencil casings) are obtained. The products are then sold to an independent company that markets and distributes them to retail outlets. The following information was collected for the month of October.

Trees processed:

50 trees (yield is 30,000 sheets of paper and 30,000 pencil casings and no scrap)

Cost of purchasing 50 trees and processing them up to the splitoff point to yield 30,000 sheets of paper and 30,000 pencil casings is $1,500.Raynor Manufacturing's accounting department reported no beginning inventories; however, ending inventory amounts reflected 1,000 sheets of paper in stock.

-What are the paper's and the pencil's approximate weighted cost proportions using the sales value at splitoff method, respectively?

A) 28.57% and 71.43%

B) 33.33% and 66.67%

C) 40% and 60%

D) 49.00% and 51.00%

E) 50.00% and 50.00%

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 57 في هذه المجموعة.

فتح الحزمة

k this deck

17

Use the information below to answer the following question(s).

Chem Manufacturing Company processes direct materials up to the splitoff point, where two products (X and Y) are obtained and sold. The following information was collected for the month of November.

Direct materials processed:

10,000 litres (10,000 litres yield 9,500 litres of good product and 500 litres of shrinkage)

The cost of purchasing 10,000 litres of direct materials and processing it up to the splitoff point to yield a total of 9,500 litres of good products was $975,000.

The beginning inventories totalled 50 litres for X and 25 litres for Y. Ending inventory amounts reflected 300 litres of product X and 525 litres of product Y. October costs were per unit were the same as November.

-What are the respective physical volume proportions for products X and Y?

A) 55.00% and 45.00%

B) 54.00% and 46.00%

C) 52.63% and 47.37%

D) 47.37% and 53.63%

E) 36.36 % and 63.64%

Chem Manufacturing Company processes direct materials up to the splitoff point, where two products (X and Y) are obtained and sold. The following information was collected for the month of November.

Direct materials processed:

10,000 litres (10,000 litres yield 9,500 litres of good product and 500 litres of shrinkage)

The cost of purchasing 10,000 litres of direct materials and processing it up to the splitoff point to yield a total of 9,500 litres of good products was $975,000.

The beginning inventories totalled 50 litres for X and 25 litres for Y. Ending inventory amounts reflected 300 litres of product X and 525 litres of product Y. October costs were per unit were the same as November.

-What are the respective physical volume proportions for products X and Y?

A) 55.00% and 45.00%

B) 54.00% and 46.00%

C) 52.63% and 47.37%

D) 47.37% and 53.63%

E) 36.36 % and 63.64%

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 57 في هذه المجموعة.

فتح الحزمة

k this deck

18

Use the information below to answer the following question(s).

Chem Manufacturing Company processes direct materials up to the splitoff point, where two products (X and Y) are obtained and sold. The following information was collected for the month of November.

Direct materials processed:

10,000 litres (10,000 litres yield 9,500 litres of good product and 500 litres of shrinkage)

The cost of purchasing 10,000 litres of direct materials and processing it up to the splitoff point to yield a total of 9,500 litres of good products was $975,000.

The beginning inventories totalled 50 litres for X and 25 litres for Y. Ending inventory amounts reflected 300 litres of product X and 525 litres of product Y. October costs were per unit were the same as November.

-What is the approximate portion of the joint costs that should be allocated to products X and Y, respectively, using a physical volume measure?

A) $461,858 and $513,142

B) $487,500 and $487,500

C) $513,142 and $461,858

D) $529,285 and $445,715

E) $530,000 and $470,000

Chem Manufacturing Company processes direct materials up to the splitoff point, where two products (X and Y) are obtained and sold. The following information was collected for the month of November.

Direct materials processed:

10,000 litres (10,000 litres yield 9,500 litres of good product and 500 litres of shrinkage)

The cost of purchasing 10,000 litres of direct materials and processing it up to the splitoff point to yield a total of 9,500 litres of good products was $975,000.

The beginning inventories totalled 50 litres for X and 25 litres for Y. Ending inventory amounts reflected 300 litres of product X and 525 litres of product Y. October costs were per unit were the same as November.

-What is the approximate portion of the joint costs that should be allocated to products X and Y, respectively, using a physical volume measure?

A) $461,858 and $513,142

B) $487,500 and $487,500

C) $513,142 and $461,858

D) $529,285 and $445,715

E) $530,000 and $470,000

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 57 في هذه المجموعة.

فتح الحزمة

k this deck

19

Which of the following is FALSE concerning the physical measure method?

A) Technical personnel outside of accounting may be required in the joint costing determinations.

B) Using the benefits-received criterion, the physical measure method less preferred than the sales at splitoff method.

C) The physical measure may not reflect each individual product's ability to generate revenues.

D) Using a common physical measure can result in the product with the lowest revenue-producing power having the most costs assigned to it.

E) It results in a constant gross margin for all products.

A) Technical personnel outside of accounting may be required in the joint costing determinations.

B) Using the benefits-received criterion, the physical measure method less preferred than the sales at splitoff method.

C) The physical measure may not reflect each individual product's ability to generate revenues.

D) Using a common physical measure can result in the product with the lowest revenue-producing power having the most costs assigned to it.

E) It results in a constant gross margin for all products.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 57 في هذه المجموعة.

فتح الحزمة

k this deck

20

The Arvid Corporation manufactures widgets, gizmos, and turnbols from a joint process. May production is 4,000 widgets; 7,000 gizmos; and 8,000 turnbols. Respective per unit selling prices at splitoff are $15, $10, and $5. Joint costs up to the splitoff point are $75,000. If joint costs are allocated based upon the sales value at splitoff, what amount of joint costs will be allocated to the widgets?

A) $30,882

B) $26,471

C) $17,647

D) $28,125

E) $60,000

A) $30,882

B) $26,471

C) $17,647

D) $28,125

E) $60,000

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 57 في هذه المجموعة.

فتح الحزمة

k this deck

21

Answer the following question(s) using the information below.

The Oxnard Corporation processes a liquid component up to the splitoff point where two products, Mr. DirtOut and Mr. SinkClean, are produced and sold. There was no beginning inventory. The following material was collected for the month of January:

Direct materials processed: 250,000 litres (242,500 litres of good product)

The cost of purchasing 250,000 litres of direct materials and processing it up to the splitoff point to yield a total of 242,500 litres of good product was $380,000.

-What are the physical volume proportions to allocate joint costs for Mr. DirtOut and Mr. SinkClean, respectively?

A) 59.00% and 41.00%

B) 60.82% and 39.18%

C) 39.18% and 60.82%

D) 59.79% and 40.21%

E) 41.00% and 59.00%

The Oxnard Corporation processes a liquid component up to the splitoff point where two products, Mr. DirtOut and Mr. SinkClean, are produced and sold. There was no beginning inventory. The following material was collected for the month of January:

Direct materials processed: 250,000 litres (242,500 litres of good product)

The cost of purchasing 250,000 litres of direct materials and processing it up to the splitoff point to yield a total of 242,500 litres of good product was $380,000.-What are the physical volume proportions to allocate joint costs for Mr. DirtOut and Mr. SinkClean, respectively?

A) 59.00% and 41.00%

B) 60.82% and 39.18%

C) 39.18% and 60.82%

D) 59.79% and 40.21%

E) 41.00% and 59.00%

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 57 في هذه المجموعة.

فتح الحزمة

k this deck

22

Answer the following question(s) using the information below.

The Oxnard Corporation processes a liquid component up to the splitoff point where two products, Mr. DirtOut and Mr. SinkClean, are produced and sold. There was no beginning inventory. The following material was collected for the month of January:

Direct materials processed: 250,000 litres (242,500 litres of good product)

The cost of purchasing 250,000 litres of direct materials and processing it up to the splitoff point to yield a total of 242,500 litres of good product was $380,000.

-When using a physical volume measure, what is the approximate amount of joint costs that will be allocated to Mr. DirtOut and Mr. SinkClean?

A) $231,116 and $148,884

B) $224,200 and $155,800

C) $227,202 and $152,798

D) $155,800 and $224,200

E) $148,884 and $231,116

The Oxnard Corporation processes a liquid component up to the splitoff point where two products, Mr. DirtOut and Mr. SinkClean, are produced and sold. There was no beginning inventory. The following material was collected for the month of January:

Direct materials processed: 250,000 litres (242,500 litres of good product)

The cost of purchasing 250,000 litres of direct materials and processing it up to the splitoff point to yield a total of 242,500 litres of good product was $380,000.-When using a physical volume measure, what is the approximate amount of joint costs that will be allocated to Mr. DirtOut and Mr. SinkClean?

A) $231,116 and $148,884

B) $224,200 and $155,800

C) $227,202 and $152,798

D) $155,800 and $224,200

E) $148,884 and $231,116

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 57 في هذه المجموعة.

فتح الحزمة

k this deck

23

Answer the following question(s) using the information below.

The Oxnard Corporation processes a liquid component up to the splitoff point where two products, Mr. DirtOut and Mr. SinkClean, are produced and sold. There was no beginning inventory. The following material was collected for the month of January:

Direct materials processed: 250,000 litres (242,500 litres of good product)

The cost of purchasing 250,000 litres of direct materials and processing it up to the splitoff point to yield a total of 242,500 litres of good product was $380,000.

-When using the physical measures method, what is Mr. DirtOut's approximate production cost per unit?

A) $1.52

B) $1.54

C) $1.57

D) $1.61

E) $1.01

The Oxnard Corporation processes a liquid component up to the splitoff point where two products, Mr. DirtOut and Mr. SinkClean, are produced and sold. There was no beginning inventory. The following material was collected for the month of January:

Direct materials processed: 250,000 litres (242,500 litres of good product)

The cost of purchasing 250,000 litres of direct materials and processing it up to the splitoff point to yield a total of 242,500 litres of good product was $380,000.-When using the physical measures method, what is Mr. DirtOut's approximate production cost per unit?

A) $1.52

B) $1.54

C) $1.57

D) $1.61

E) $1.01

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 57 في هذه المجموعة.

فتح الحزمة

k this deck

24

Use the information below to answer the following question(s).

Cranbrook Chemical Ltd. manufactures two industrial compounds. In the month of May, 15,000 litres of direct material costing $160,000 were processed at a cost of $400,000. The joint process yielded 16,000 containers of a compound known as Jarlon and 4,000 containers of a compound known as Kharton. The respective selling prices of Jarlon and Kharton are $38 and $58. Both products may be processed further. Jarlon may be processed into Jaxton at an incremental cost of $8 per jar of the final product while Kharton may be processed into Kraxton at an additional cost of $32 per jar of the final product. The volume of jars of the final product are: 12,000 and 3,000 for Jaxton and Kraxton respectively. The selling price of Jaxton is $48 per jar. The selling price of Kraxton is $102 per jar.

-Using the sales value at splitoff method, the percentage weightings for joint cost allocations for Jarlon and Kharton respectively are

A) 27.62% and 72.38%.

B) 80.00% and 20.00%.

C) 39.58% and 60.42%.

D) 72.38% and 27.62%.

E) 60.42% and 39.58%.

Cranbrook Chemical Ltd. manufactures two industrial compounds. In the month of May, 15,000 litres of direct material costing $160,000 were processed at a cost of $400,000. The joint process yielded 16,000 containers of a compound known as Jarlon and 4,000 containers of a compound known as Kharton. The respective selling prices of Jarlon and Kharton are $38 and $58. Both products may be processed further. Jarlon may be processed into Jaxton at an incremental cost of $8 per jar of the final product while Kharton may be processed into Kraxton at an additional cost of $32 per jar of the final product. The volume of jars of the final product are: 12,000 and 3,000 for Jaxton and Kraxton respectively. The selling price of Jaxton is $48 per jar. The selling price of Kraxton is $102 per jar.

-Using the sales value at splitoff method, the percentage weightings for joint cost allocations for Jarlon and Kharton respectively are

A) 27.62% and 72.38%.

B) 80.00% and 20.00%.

C) 39.58% and 60.42%.

D) 72.38% and 27.62%.

E) 60.42% and 39.58%.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 57 في هذه المجموعة.

فتح الحزمة

k this deck

25

Use the information below to answer the following question(s).

Cranbrook Chemical Ltd. manufactures two industrial compounds. In the month of May, 15,000 litres of direct material costing $160,000 were processed at a cost of $400,000. The joint process yielded 16,000 containers of a compound known as Jarlon and 4,000 containers of a compound known as Kharton. The respective selling prices of Jarlon and Kharton are $38 and $58. Both products may be processed further. Jarlon may be processed into Jaxton at an incremental cost of $8 per jar of the final product while Kharton may be processed into Kraxton at an additional cost of $32 per jar of the final product. The volume of jars of the final product are: 12,000 and 3,000 for Jaxton and Kraxton respectively. The selling price of Jaxton is $48 per jar. The selling price of Kraxton is $102 per jar.

-Using the physical measures method, the weightings for joint cost allocations for Jarlon and Kharton respectively are

A) 27.62% and 72.38%.

B) 80.00% and 20.00%.

C) 39.58% and 60.42%.

D) 72.38% and 27.62%.

E) 60.42% and 39.58%.

Cranbrook Chemical Ltd. manufactures two industrial compounds. In the month of May, 15,000 litres of direct material costing $160,000 were processed at a cost of $400,000. The joint process yielded 16,000 containers of a compound known as Jarlon and 4,000 containers of a compound known as Kharton. The respective selling prices of Jarlon and Kharton are $38 and $58. Both products may be processed further. Jarlon may be processed into Jaxton at an incremental cost of $8 per jar of the final product while Kharton may be processed into Kraxton at an additional cost of $32 per jar of the final product. The volume of jars of the final product are: 12,000 and 3,000 for Jaxton and Kraxton respectively. The selling price of Jaxton is $48 per jar. The selling price of Kraxton is $102 per jar.

-Using the physical measures method, the weightings for joint cost allocations for Jarlon and Kharton respectively are

A) 27.62% and 72.38%.

B) 80.00% and 20.00%.

C) 39.58% and 60.42%.

D) 72.38% and 27.62%.

E) 60.42% and 39.58%.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 57 في هذه المجموعة.

فتح الحزمة

k this deck

26

Use the information below to answer the following question(s).

Cranbrook Chemical Ltd. manufactures two industrial compounds. In the month of May, 15,000 litres of direct material costing $160,000 were processed at a cost of $400,000. The joint process yielded 16,000 containers of a compound known as Jarlon and 4,000 containers of a compound known as Kharton. The respective selling prices of Jarlon and Kharton are $38 and $58. Both products may be processed further. Jarlon may be processed into Jaxton at an incremental cost of $8 per jar of the final product while Kharton may be processed into Kraxton at an additional cost of $32 per jar of the final product. The volume of jars of the final product are: 12,000 and 3,000 for Jaxton and Kraxton respectively. The selling price of Jaxton is $48 per jar. The selling price of Kraxton is $102 per jar.

-Using the sales value at splitoff method, the joint costs allocated to Jarlon would be

A) $289,520.

B) $115,808.

C) $405,328.

D) $110,480.

E) $154,672.

Cranbrook Chemical Ltd. manufactures two industrial compounds. In the month of May, 15,000 litres of direct material costing $160,000 were processed at a cost of $400,000. The joint process yielded 16,000 containers of a compound known as Jarlon and 4,000 containers of a compound known as Kharton. The respective selling prices of Jarlon and Kharton are $38 and $58. Both products may be processed further. Jarlon may be processed into Jaxton at an incremental cost of $8 per jar of the final product while Kharton may be processed into Kraxton at an additional cost of $32 per jar of the final product. The volume of jars of the final product are: 12,000 and 3,000 for Jaxton and Kraxton respectively. The selling price of Jaxton is $48 per jar. The selling price of Kraxton is $102 per jar.

-Using the sales value at splitoff method, the joint costs allocated to Jarlon would be

A) $289,520.

B) $115,808.

C) $405,328.

D) $110,480.

E) $154,672.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 57 في هذه المجموعة.

فتح الحزمة

k this deck

27

Use the information below to answer the following question(s).

Cranbrook Chemical Ltd. manufactures two industrial compounds. In the month of May, 15,000 litres of direct material costing $160,000 were processed at a cost of $400,000. The joint process yielded 16,000 containers of a compound known as Jarlon and 4,000 containers of a compound known as Kharton. The respective selling prices of Jarlon and Kharton are $38 and $58. Both products may be processed further. Jarlon may be processed into Jaxton at an incremental cost of $8 per jar of the final product while Kharton may be processed into Kraxton at an additional cost of $32 per jar of the final product. The volume of jars of the final product are: 12,000 and 3,000 for Jaxton and Kraxton respectively. The selling price of Jaxton is $48 per jar. The selling price of Kraxton is $102 per jar.

-Using the sales value at splitoff method, the joint costs allocated to Kharton would be

A) $289,520.

B) $115,808.

C) $110,480.

D) $154,672.

E) $405,328.

Cranbrook Chemical Ltd. manufactures two industrial compounds. In the month of May, 15,000 litres of direct material costing $160,000 were processed at a cost of $400,000. The joint process yielded 16,000 containers of a compound known as Jarlon and 4,000 containers of a compound known as Kharton. The respective selling prices of Jarlon and Kharton are $38 and $58. Both products may be processed further. Jarlon may be processed into Jaxton at an incremental cost of $8 per jar of the final product while Kharton may be processed into Kraxton at an additional cost of $32 per jar of the final product. The volume of jars of the final product are: 12,000 and 3,000 for Jaxton and Kraxton respectively. The selling price of Jaxton is $48 per jar. The selling price of Kraxton is $102 per jar.

-Using the sales value at splitoff method, the joint costs allocated to Kharton would be

A) $289,520.

B) $115,808.

C) $110,480.

D) $154,672.

E) $405,328.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 57 في هذه المجموعة.

فتح الحزمة

k this deck

28

Use the information below to answer the following question(s).

Cranbrook Chemical Ltd. manufactures two industrial compounds. In the month of May, 15,000 litres of direct material costing $160,000 were processed at a cost of $400,000. The joint process yielded 16,000 containers of a compound known as Jarlon and 4,000 containers of a compound known as Kharton. The respective selling prices of Jarlon and Kharton are $38 and $58. Both products may be processed further. Jarlon may be processed into Jaxton at an incremental cost of $8 per jar of the final product while Kharton may be processed into Kraxton at an additional cost of $32 per jar of the final product. The volume of jars of the final product are: 12,000 and 3,000 for Jaxton and Kraxton respectively. The selling price of Jaxton is $48 per jar. The selling price of Kraxton is $102 per jar.

-Using the physical measures method, the joint costs allocated to Jarlon would be

A) $320,000.

B) $112,000.

C) $405,328.

D) $448,000.

E) $289,520

Cranbrook Chemical Ltd. manufactures two industrial compounds. In the month of May, 15,000 litres of direct material costing $160,000 were processed at a cost of $400,000. The joint process yielded 16,000 containers of a compound known as Jarlon and 4,000 containers of a compound known as Kharton. The respective selling prices of Jarlon and Kharton are $38 and $58. Both products may be processed further. Jarlon may be processed into Jaxton at an incremental cost of $8 per jar of the final product while Kharton may be processed into Kraxton at an additional cost of $32 per jar of the final product. The volume of jars of the final product are: 12,000 and 3,000 for Jaxton and Kraxton respectively. The selling price of Jaxton is $48 per jar. The selling price of Kraxton is $102 per jar.

-Using the physical measures method, the joint costs allocated to Jarlon would be

A) $320,000.

B) $112,000.

C) $405,328.

D) $448,000.

E) $289,520

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 57 في هذه المجموعة.

فتح الحزمة

k this deck

29

Use the information below to answer the following question(s).

Cranbrook Chemical Ltd. manufactures two industrial compounds. In the month of May, 15,000 litres of direct material costing $160,000 were processed at a cost of $400,000. The joint process yielded 16,000 containers of a compound known as Jarlon and 4,000 containers of a compound known as Kharton. The respective selling prices of Jarlon and Kharton are $38 and $58. Both products may be processed further. Jarlon may be processed into Jaxton at an incremental cost of $8 per jar of the final product while Kharton may be processed into Kraxton at an additional cost of $32 per jar of the final product. The volume of jars of the final product are: 12,000 and 3,000 for Jaxton and Kraxton respectively. The selling price of Jaxton is $48 per jar. The selling price of Kraxton is $102 per jar.

-Using the physical measures method, the joint costs allocated to Kharton would be

A) $320,000.

B) $112,000.

C) $154,672.