Deck 11: Overall audit plan and audit program

ملء الشاشة (f)

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

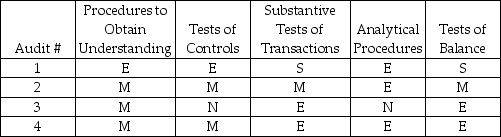

The evidence mix which the auditor chose in each of four different audits is shown below:

Amount of testing: E = extensive M = medium S = small N = none

In which audit did the client company have sophisticated internal controls and in which audit did the client have insufficient controls?

A) sophisticated in #2 and insufficient in #3

B) sophisticated in #1 and insufficient in #2

C) sophisticated in #1 and insufficient in #3

D) sophisticated in #4 and insufficient in #2

Amount of testing: E = extensive M = medium S = small N = none

In which audit did the client company have sophisticated internal controls and in which audit did the client have insufficient controls?

A) sophisticated in #2 and insufficient in #3

B) sophisticated in #1 and insufficient in #2

C) sophisticated in #1 and insufficient in #3

D) sophisticated in #4 and insufficient in #2

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

فتح الحزمة

قم بالتسجيل لفتح البطاقات في هذه المجموعة!

Unlock Deck

Unlock Deck

1/105

العب

ملء الشاشة (f)

Deck 11: Overall audit plan and audit program

1

Tests of controls are directed toward the control's:

A) efficiency.

B) effectiveness.

C) efficiency and effectiveness.

D) cost benefit ratio.

A) efficiency.

B) effectiveness.

C) efficiency and effectiveness.

D) cost benefit ratio.

B

2

Substantive tests of transactions and tests of controls are often conducted simultaneously.

True

3

Which one of the following statements is False?

A) Tests of controls are concerned with evaluating whether controls are sufficiently effective to justify reducing control risk and thereby reducing analytical review procedures.

B) Analytical procedures emphasise the overall reasonableness of transactions and the general ledger balances.

C) Substantive tests of transactions emphasise the verification of transactions recorded in the journals and then posted in the general ledger.

D) Tests of details of balances emphasise the ending balances in the general ledger.

A) Tests of controls are concerned with evaluating whether controls are sufficiently effective to justify reducing control risk and thereby reducing analytical review procedures.

B) Analytical procedures emphasise the overall reasonableness of transactions and the general ledger balances.

C) Substantive tests of transactions emphasise the verification of transactions recorded in the journals and then posted in the general ledger.

D) Tests of details of balances emphasise the ending balances in the general ledger.

A

4

In the context of an audit of financial statements, substantive tests are audit procedures that:

A) assess the detection risk of each audit objective.

B) assess the control risk for each audit objective.

C) test whether transactions are correct.

D) test for dollar misstatements.

A) assess the detection risk of each audit objective.

B) assess the control risk for each audit objective.

C) test whether transactions are correct.

D) test for dollar misstatements.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 105 في هذه المجموعة.

فتح الحزمة

k this deck

5

Shown below (1-5)are the five types of tests which auditors use to determine whether financial statements are fairly stated.Which three are substantive tests?

1) procedures to obtain an understanding of internal control

2) tests of controls

3) tests of transactions

4) analytical procedures

5) tests of balances

A) 2, 3 and 4

B) 1, 2 and 3

C) 3, 4 and 5

D) 2, 3 and 5

1) procedures to obtain an understanding of internal control

2) tests of controls

3) tests of transactions

4) analytical procedures

5) tests of balances

A) 2, 3 and 4

B) 1, 2 and 3

C) 3, 4 and 5

D) 2, 3 and 5

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 105 في هذه المجموعة.

فتح الحزمة

k this deck

6

In which stage(s)of an audit can analytical procedures be performed?

A) in conjunction with tests of transactions and tests of details of balances

B) in the completion stage

C) in the planning stage

D) all of the above

A) in conjunction with tests of transactions and tests of details of balances

B) in the completion stage

C) in the planning stage

D) all of the above

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 105 في هذه المجموعة.

فتح الحزمة

k this deck

7

Which of the following is a procedure designed to test for monetary errors or irregularities directly affecting the correctness of financial statement balances?

A) substantive test

B) monetary-unit sampling test

C) test of control

D) test of attributes

A) substantive test

B) monetary-unit sampling test

C) test of control

D) test of attributes

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 105 في هذه المجموعة.

فتح الحزمة

k this deck

8

The purpose of tests of controls is to provide reasonable assurance that the:

A) entity has complied with requirements of quality control.

B) accounting treatment of transactions and balances is valid and proper.

C) entity has complied with disclosure requirements of generally accepted accounting principles.

D) accounting control procedures are operating effectively.

A) entity has complied with requirements of quality control.

B) accounting treatment of transactions and balances is valid and proper.

C) entity has complied with disclosure requirements of generally accepted accounting principles.

D) accounting control procedures are operating effectively.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 105 في هذه المجموعة.

فتح الحزمة

k this deck

9

ASA 315 requires the auditor to assess the risk of material misstatement in the client's financial report.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 105 في هذه المجموعة.

فتح الحزمة

k this deck

10

Analytical procedures performed during substantive testing are typically ________ those done as part of planning.

A) less focused than

B) about the same as

C) more focused than

D) less extensive than

A) less focused than

B) about the same as

C) more focused than

D) less extensive than

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 105 في هذه المجموعة.

فتح الحزمة

k this deck

11

For efficiency, tests of controls are frequently done at the same time as:

A) analytical procedures.

B) compliance tests.

C) substantive tests of transactions.

D) substantive tests of balances.

A) analytical procedures.

B) compliance tests.

C) substantive tests of transactions.

D) substantive tests of balances.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 105 في هذه المجموعة.

فتح الحزمة

k this deck

12

Tests of controls and substantive tests of transactions are often conducted simultaneously on the same transactions.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 105 في هذه المجموعة.

فتح الحزمة

k this deck

13

Which of the following assessments are affected by substantive tests of transactions?

A) both acceptable audit risk and control risk

B) both control risk and planned detection risk

C) both inherent risk and control risk

D) both inherent risk and planned detection risk

A) both acceptable audit risk and control risk

B) both control risk and planned detection risk

C) both inherent risk and control risk

D) both inherent risk and planned detection risk

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 105 في هذه المجموعة.

فتح الحزمة

k this deck

14

Tests of details of balances are always substantive tests.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 105 في هذه المجموعة.

فتح الحزمة

k this deck

15

After finishing the review phase of the study and evaluation of internal control in an audit engagement, the auditor should perform tests of controls on:

A) those controls that have a material effect upon the financial statement balances.

B) a random sample of the controls that were reviewed.

C) those controls that the auditor plans to rely upon.

D) those controls in which significant deficiencies were identified.

A) those controls that have a material effect upon the financial statement balances.

B) a random sample of the controls that were reviewed.

C) those controls that the auditor plans to rely upon.

D) those controls in which significant deficiencies were identified.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 105 في هذه المجموعة.

فتح الحزمة

k this deck

16

A listing of all the things which the auditor will do to gather sufficient, competent evidence is the:

A) audit procedure.

B) audit plan.

C) audit risk model.

D) audit program.

A) audit procedure.

B) audit plan.

C) audit risk model.

D) audit program.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 105 في هذه المجموعة.

فتح الحزمة

k this deck

17

Which of the following is NOT a type of audit test?

A) substantive tests of transactions

B) authorisation of transactions

C) analytical procedures

D) tests of controls

A) substantive tests of transactions

B) authorisation of transactions

C) analytical procedures

D) tests of controls

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 105 في هذه المجموعة.

فتح الحزمة

k this deck

18

The audit procedure re-performance always simultaneously provides evidence about both internal control effectiveness and monetary correctness.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 105 في هذه المجموعة.

فتح الحزمة

k this deck

19

When controls are effectively designed, the auditor assesses control risk:

A) At a level that does not reflect the effectiveness of those controls.

B) at a level that reflects the effectiveness of those controls.

C) at a reduced level, as the controls are effective.

D) all of the above

A) At a level that does not reflect the effectiveness of those controls.

B) at a level that reflects the effectiveness of those controls.

C) at a reduced level, as the controls are effective.

D) all of the above

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 105 في هذه المجموعة.

فتح الحزمة

k this deck

20

Auditing standards require that tests of controls be performed on every audit engagement.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 105 في هذه المجموعة.

فتح الحزمة

k this deck

21

There are three stages of the audit in which analytical procedures are performed.Please identify each of these three stages, and for each stage, discuss the purpose of performing analytical procedures in that stage.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 105 في هذه المجموعة.

فتح الحزمة

k this deck

22

The results of tests of controls and substantive tests of transactions affect the design of the tests of details of balances.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 105 في هذه المجموعة.

فتح الحزمة

k this deck

23

Which of the following tests determine whether accounting transactions have been properly authorised, correctly recorded and summarised in the journals, and correctly posted to subsidiary ledgers and the general ledgers?

A) substantive tests of balances

B) substantive tests of transactions

C) tests of controls

D) analytical procedures

A) substantive tests of balances

B) substantive tests of transactions

C) tests of controls

D) analytical procedures

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 105 في هذه المجموعة.

فتح الحزمة

k this deck

24

Only when testing details of balances will audit procedures include confirmation and physical examination.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 105 في هذه المجموعة.

فتح الحزمة

k this deck

25

Where is the primary emphasis in most tests of details of balances?

A) income statement accounts

B) cash flow statement account

C) balance sheet accounts

D) all of the above

A) income statement accounts

B) cash flow statement account

C) balance sheet accounts

D) all of the above

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 105 في هذه المجموعة.

فتح الحزمة

k this deck

26

Discuss the purposes of (1)substantive tests of transactions, (2)tests of controls, and (3)tests of details of balances.Give an example of each.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 105 في هذه المجموعة.

فتح الحزمة

k this deck

27

An exception in a substantive test of transactions provides only an indication of the likelihood of monetary misstatements in the financial statements, because substantive tests of transactions do not reveal whether monetary misstatements have actually occurred.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 105 في هذه المجموعة.

فتح الحزمة

k this deck

28

Which one of the following is ordinarily designed to detect possible material dollar errors in the financial statements?

A) computer controls

B) analytical review

C) tests of controls

D) post-audit working paper review

A) computer controls

B) analytical review

C) tests of controls

D) post-audit working paper review

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 105 في هذه المجموعة.

فتح الحزمة

k this deck

29

If tests of controls reveal that controls are sufficiently effective to justify reducing control risk, the auditor is justified in reducing substantive audit tests.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 105 في هذه المجموعة.

فتح الحزمة

k this deck

30

Material dollar misstatements are more likely to exist in the financial statements when control test deviations are considered to be insignificant deficiencies.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 105 في هذه المجموعة.

فتح الحزمة

k this deck

31

Professional auditing standards recognise that in instances where a significant amount of audit evidence is in electronic form, it may not be possible to reduce detection risk to an acceptable level by performing only substantive tests.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 105 في هذه المجموعة.

فتح الحزمة

k this deck

32

An exception in a test of control provides only an indication of the likelihood of monetary misstatements in the financial statements, because tests of controls reveal whether monetary misstatements have actually occurred.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 105 في هذه المجموعة.

فتح الحزمة

k this deck

33

Type(s)of evidence collected during substantive tests of transactions are:

A) inquiries of the client.

B) re-performance.

C) documentation.

D) all of the above

A) inquiries of the client.

B) re-performance.

C) documentation.

D) all of the above

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 105 في هذه المجموعة.

فتح الحزمة

k this deck

34

Describe the five types of audit tests used to determine whether financial statements are stated fairly.Identify which of the five types are substantive tests and which are used to reduce assessed control risk.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 105 في هذه المجموعة.

فتح الحزمة

k this deck

35

Which of the following is correct when controls are effective and assessed control risk is low?

A) There will be heavy emphasis on tests of controls.

B) Some substantive tests of transactions will still be performed.

C) Only substantive tests of transactions will be used.

D) both A and B

A) There will be heavy emphasis on tests of controls.

B) Some substantive tests of transactions will still be performed.

C) Only substantive tests of transactions will be used.

D) both A and B

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 105 في هذه المجموعة.

فتح الحزمة

k this deck

36

There is a trade-off between tests of controls and substantive tests.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 105 في هذه المجموعة.

فتح الحزمة

k this deck

37

Contrast the circumstances in which the auditor would choose not to test controls with those in which he or she would perform tests of controls.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 105 في هذه المجموعة.

فتح الحزمة

k this deck

38

If no material differences are found using analytical procedures, and the auditor concludes that misstatements are not likely to have occurred, then:

A) the number or extent of tests of details of balances may be reduced.

B) it will be necessary to increase the tests of transactions.

C) it will be necessary to increase the tests of balances.

D) it will not be necessary to perform tests of balances.

A) the number or extent of tests of details of balances may be reduced.

B) it will be necessary to increase the tests of transactions.

C) it will be necessary to increase the tests of balances.

D) it will not be necessary to perform tests of balances.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 105 في هذه المجموعة.

فتح الحزمة

k this deck

39

ASA 520 states that analytical procedures can be used as:

A) compliance tests.

B) tests of controls.

C) substantive tests.

D) helpful procedures not possessing the validity of other tests available to the auditor.

A) compliance tests.

B) tests of controls.

C) substantive tests.

D) helpful procedures not possessing the validity of other tests available to the auditor.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 105 في هذه المجموعة.

فتح الحزمة

k this deck

40

If the auditor's preliminary assessment of control risk is decreased from high to medium, tests of controls can be reduced.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 105 في هذه المجموعة.

فتح الحزمة

k this deck

41

Under normal circumstances, there should be no variation in the audit evidence mix from cycle to cycle for a given audit engagement.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 105 في هذه المجموعة.

فتح الحزمة

k this deck

42

Which one of the following audit tests is usually the LEAST costly to perform?

A) analytical procedures

B) tests of balances

C) tests of controls

D) substantive tests of transactions

A) analytical procedures

B) tests of balances

C) tests of controls

D) substantive tests of transactions

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 105 في هذه المجموعة.

فتح الحزمة

k this deck

43

ASA 315 refers to the benefits and risks related to internal controls present in an IT system.What are the implications for the auditor in conducting tests of controls and substantive tests?

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 105 في هذه المجموعة.

فتح الحزمة

k this deck

44

ASA 315 refers to the benefits and risks related to internal controls present in an IT system.What are the implications for the auditor in conducting tests of controls and substantive tests?

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 105 في هذه المجموعة.

فتح الحزمة

k this deck

45

Why does an auditor evaluate the client's system of internal control?

A) to ascertain whether irregularities are probable

B) to ascertain whether any employees have incompatible functions

C) to determine the extent of substantive tests which must be performed

D) to determine the extent of tests of controls which must be performed

A) to ascertain whether irregularities are probable

B) to ascertain whether any employees have incompatible functions

C) to determine the extent of substantive tests which must be performed

D) to determine the extent of tests of controls which must be performed

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 105 في هذه المجموعة.

فتح الحزمة

k this deck

46

There are seven methods of obtaining audit evidence: physical examination, confirmation, documentation, observation, inquiries of the client, re-performance, and analytical procedures.For each of the following types of audit tests, indicate the type(s)of evidence-gathering procedures that can be used during the test: (1)tests of controls, (2)substantive tests of transactions, (3)analytical procedures and (4)tests of details of balances.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 105 في هذه المجموعة.

فتح الحزمة

k this deck

47

Which one of the following statements is NOT correct?

A) Tests of transactions are often performed several months prior to the balance sheet date.

B) It is common to use analytical procedures at any time during the audit.

C) Tests of details of balances are normally the last tests performed.

D) When controls are not considered effective, or when control deviations are discovered, substantive tests will be eliminated.

A) Tests of transactions are often performed several months prior to the balance sheet date.

B) It is common to use analytical procedures at any time during the audit.

C) Tests of details of balances are normally the last tests performed.

D) When controls are not considered effective, or when control deviations are discovered, substantive tests will be eliminated.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 105 في هذه المجموعة.

فتح الحزمة

k this deck

48

Which of the following is true when a significant amount of evidence is in electronic form?

A) Audit risk decreases.

B) It may not be possible to reduce detection risk to an acceptable level by performing only substantive tests.

C) Acceptable assurance usually increases.

D) It is usually impractical to evaluate controls.

A) Audit risk decreases.

B) It may not be possible to reduce detection risk to an acceptable level by performing only substantive tests.

C) Acceptable assurance usually increases.

D) It is usually impractical to evaluate controls.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 105 في هذه المجموعة.

فتح الحزمة

k this deck

49

Extended performance of tests of controls is most likely when:

A) controls are ineffective and assessed control risk is high.

B) the auditor is doing a 'fraud audit'.

C) controls are effective and assessed control risk is low.

D) it is a first-year audit.

A) controls are ineffective and assessed control risk is high.

B) the auditor is doing a 'fraud audit'.

C) controls are effective and assessed control risk is low.

D) it is a first-year audit.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 105 في هذه المجموعة.

فتح الحزمة

k this deck

50

The actual operation of an internal control system may be most objectively evaluated by:

A) review of the previous year's audit work papers to update the report of internal control evaluation.

B) substantive tests of accounts balances based on the auditor's assessment of internal control strength.

C) selection of items processed by the system and determination of the presence or absence of errors and control test deviations.

D) completing a questionnaire and flowchart related to the accounting system in the year under audit.

A) review of the previous year's audit work papers to update the report of internal control evaluation.

B) substantive tests of accounts balances based on the auditor's assessment of internal control strength.

C) selection of items processed by the system and determination of the presence or absence of errors and control test deviations.

D) completing a questionnaire and flowchart related to the accounting system in the year under audit.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 105 في هذه المجموعة.

فتح الحزمة

k this deck

51

Which of the following is NOT part of the four-step approach used by auditors to reduce assessed control risk?

A) Identify key controls that should reduce control risk for each transaction-related audit objective.

B) Develop appropriate tests of controls for all internal controls that are used to reduce the preliminary assessment of control risk below maximum (key controls).

C) Apply the transaction-related objectives to the class of transactions being tested.

D) Perform analytical procedures on the transaction cycle tested.

A) Identify key controls that should reduce control risk for each transaction-related audit objective.

B) Develop appropriate tests of controls for all internal controls that are used to reduce the preliminary assessment of control risk below maximum (key controls).

C) Apply the transaction-related objectives to the class of transactions being tested.

D) Perform analytical procedures on the transaction cycle tested.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 105 في هذه المجموعة.

فتح الحزمة

k this deck

52

Why are substantive tests of transaction high-cost?

A) The calculations are more difficult and complicated.

B) They involve inquiry, observation, and inspection.

C) A greater extent of testing is required.

D) They require re-calculations and tracing.

A) The calculations are more difficult and complicated.

B) They involve inquiry, observation, and inspection.

C) A greater extent of testing is required.

D) They require re-calculations and tracing.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 105 في هذه المجموعة.

فتح الحزمة

k this deck

53

The reliance placed on substantive tests in relation to the reliance placed on internal control varies in a relationship that is ordinarily:

A) inverse.

B) direct.

C) equal.

D) parallel.

A) inverse.

B) direct.

C) equal.

D) parallel.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 105 في هذه المجموعة.

فتح الحزمة

k this deck

54

Which one of the following audit tests is usually the MOST costly to perform?

A) analytical procedures

B) tests of balances

C) tests of controls

D) substantive tests of transactions

A) analytical procedures

B) tests of balances

C) tests of controls

D) substantive tests of transactions

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 105 في هذه المجموعة.

فتح الحزمة

k this deck

55

The audit client is a medium size business with some controls and a few inherent risks.Discuss the audit evidence mix appropriate for this client.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 105 في هذه المجموعة.

فتح الحزمة

k this deck

56

Which one of the following is NOT a direct outcome of performing analytical procedures?

A) Understand the client's business.

B) Reduce detailed audit tests.

C) Assess the entity's ability to continue as a going concern.

D) Identify specific errors in the accounts.

A) Understand the client's business.

B) Reduce detailed audit tests.

C) Assess the entity's ability to continue as a going concern.

D) Identify specific errors in the accounts.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 105 في هذه المجموعة.

فتح الحزمة

k this deck

57

The highest cost audit will be incurred when the auditor expected that the internal control system would:

A) be effective, but the auditor found extensive control test deviations and significant errors during tests of transactions.

B) have few effective controls, but client's personnel were well-trained and knowledgeable.

C) have few effective controls, and tests of balances found many errors.

D) be very sophisticated, and the tests of controls confirmed this.

A) be effective, but the auditor found extensive control test deviations and significant errors during tests of transactions.

B) have few effective controls, but client's personnel were well-trained and knowledgeable.

C) have few effective controls, and tests of balances found many errors.

D) be very sophisticated, and the tests of controls confirmed this.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 105 في هذه المجموعة.

فتح الحزمة

k this deck

58

Which one of the following types of evidence would NOT be obtained in tests of controls?

A) re-performance

B) inquiry of the client

C) documentation

D) physical examination

A) re-performance

B) inquiry of the client

C) documentation

D) physical examination

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 105 في هذه المجموعة.

فتح الحزمة

k this deck

59

Which of the following is an exception that is uncovered in a test of controls?

A) justification for issuing the qualified opinion

B) evidence that the financial statements are materially misstated

C) an indication of the likelihood of misstatements in the financial statements

D) a financial statement misstatement

A) justification for issuing the qualified opinion

B) evidence that the financial statements are materially misstated

C) an indication of the likelihood of misstatements in the financial statements

D) a financial statement misstatement

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 105 في هذه المجموعة.

فتح الحزمة

k this deck

60

The evidence mix which the auditor chose in each of four different audits is shown below:

Amount of testing: E = extensive M = medium S = small N = none

In which audit did the client company have sophisticated internal controls and in which audit did the client have insufficient controls?

A) sophisticated in #2 and insufficient in #3

B) sophisticated in #1 and insufficient in #2

C) sophisticated in #1 and insufficient in #3

D) sophisticated in #4 and insufficient in #2

Amount of testing: E = extensive M = medium S = small N = none

In which audit did the client company have sophisticated internal controls and in which audit did the client have insufficient controls?

A) sophisticated in #2 and insufficient in #3

B) sophisticated in #1 and insufficient in #2

C) sophisticated in #1 and insufficient in #3

D) sophisticated in #4 and insufficient in #2

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 105 في هذه المجموعة.

فتح الحزمة

k this deck

61

If the results of the tests of controls, substantive tests of transactions, and analytical procedures are not consistent with the prediction, the tests of details of balances will be:

A) increased.

B) changed.

C) eliminated.

D) unaffected.

A) increased.

B) changed.

C) eliminated.

D) unaffected.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 105 في هذه المجموعة.

فتح الحزمة

k this deck

62

When analytical procedures are performed during substantive testing, they are typically less focused and less extensive than when performed as part of audit planning.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 105 في هذه المجموعة.

فتح الحزمة

k this deck

63

Discuss the assumptions and predictions an auditor needs to make when designing an audit program for tests of details of balances.Why are these assumptions and predictions necessary?

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 105 في هذه المجموعة.

فتح الحزمة

k this deck

64

Even when all transaction-related audit objectives are met, the auditor will still rely primarily on substantive tests of balances to meet the following balance-related audit objective:

A) realisable value

B) presentations and disclosure

C) rights and obligations

D) A and C

A) realisable value

B) presentations and disclosure

C) rights and obligations

D) A and C

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 105 في هذه المجموعة.

فتح الحزمة

k this deck

65

Even when all transaction-related audit objectives are met, the auditor will still rely primarily on substantive tests of balances to meet the following balance-related audit objective(s):

A) realisable value

B) rights and obligations

C) both A and B

D) none of the above

A) realisable value

B) rights and obligations

C) both A and B

D) none of the above

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 105 في هذه المجموعة.

فتح الحزمة

k this deck

66

With respect to the auditor's planning of a year-end examination, which one of the following statements is ALWAYS true?

A) An engagement should not be accepted after the financial year ends.

B) An inventory count must be observed at the balance sheet date.

C) The client's audit committee should not be told of the specific audit procedures that will be performed.

D) It is an acceptable practice to carry out substantial parts of the examination at interim dates.

A) An engagement should not be accepted after the financial year ends.

B) An inventory count must be observed at the balance sheet date.

C) The client's audit committee should not be told of the specific audit procedures that will be performed.

D) It is an acceptable practice to carry out substantial parts of the examination at interim dates.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 105 في هذه المجموعة.

فتح الحزمة

k this deck

67

Analytical procedures are relatively inexpensive, so many auditors perform them on all audits.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 105 في هذه المجموعة.

فتح الحزمة

k this deck

68

Auditors follow a four-step approach to reduce assessed control risk.What is the order of these four steps?

1) Identify key controls that should reduce control risk for each transaction-related audit objective.

2) Apply the transaction-related objectives to the class of transactions being tested.

3) Develop appropriate tests of controls for all internal controls that are used to reduce the preliminary assessment of control risk below maximum (key controls).

4) For potential types of misstatements related to each transaction-related audit objective, design appropriate substantive tests of transactions.

A) 1, 2, 3, 4

B) 4, 1, 2, 3

C) 2, 1, 3, 4

D) 1, 3, 2, 4

1) Identify key controls that should reduce control risk for each transaction-related audit objective.

2) Apply the transaction-related objectives to the class of transactions being tested.

3) Develop appropriate tests of controls for all internal controls that are used to reduce the preliminary assessment of control risk below maximum (key controls).

4) For potential types of misstatements related to each transaction-related audit objective, design appropriate substantive tests of transactions.

A) 1, 2, 3, 4

B) 4, 1, 2, 3

C) 2, 1, 3, 4

D) 1, 3, 2, 4

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 105 في هذه المجموعة.

فتح الحزمة

k this deck

69

The extent of tests of details of balances can be reduced when transaction-related audit objectives have been satisfied by tests of controls or substantive tests of transactions.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 105 في هذه المجموعة.

فتح الحزمة

k this deck

70

Auditors follow a four-step approach to reduce assessed control risk.Identify and describe these steps.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 105 في هذه المجموعة.

فتح الحزمة

k this deck

71

List the nine balance-related audit objectives in the verification of the ending balance in accounts receivable and provide one specific useful audit procedure for each of the objectives.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 105 في هذه المجموعة.

فتح الحزمة

k this deck

72

Which of the following explains why many auditors perform extensive analytical procedures on all audits?

A) They pinpoint errors in accounts.

B) They are relatively inexpensive.

C) It is required by the auditing standards.

D) all of the above

A) They pinpoint errors in accounts.

B) They are relatively inexpensive.

C) It is required by the auditing standards.

D) all of the above

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 105 في هذه المجموعة.

فتح الحزمة

k this deck

73

A low tolerable error for a given account would result in more testing of details than a higher amount.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 105 في هذه المجموعة.

فتح الحزمة

k this deck

74

The tests of controls and substantive tests of transactions section of the audit program normally includes a descriptive section documenting the understanding obtained about internal control.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 105 في هذه المجموعة.

فتح الحزمة

k this deck

75

When designing an audit program for tests of details of balances, the auditor should make assumptions about inherent risk and control risk, as well as predictions concerning the outcome of tests of controls, substantive tests of transactions, and analytical procedures.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 105 في هذه المجموعة.

فتح الحزمة

k this deck

76

When the auditor plans to use analytical procedures to provide substantive assurance about an account balance, the data used in the calculations must be considered:

A) sufficiently reliable.

B) reasonable.

C) absolutely reliable.

D) sufficiently appropriate.

A) sufficiently reliable.

B) reasonable.

C) absolutely reliable.

D) sufficiently appropriate.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 105 في هذه المجموعة.

فتح الحزمة

k this deck

77

The results of tests of controls and tests of details of balances affect the design of substantive tests of transactions.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 105 في هذه المجموعة.

فتح الحزمة

k this deck

78

Which of the following is NOT part of the methodology used in designing substantive tests of balances?

A) Design and perform analytical procedures.

B) Assess inherent risk.

C) Assess client business risks.

D) Assess control risk.

A) Design and perform analytical procedures.

B) Assess inherent risk.

C) Assess client business risks.

D) Assess control risk.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 105 في هذه المجموعة.

فتح الحزمة

k this deck

79

Audit programs are never computerised as they are unique to each client.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 105 في هذه المجموعة.

فتح الحزمة

k this deck

80

Presentation- and disclosure-related objectives are more important in phase IV of the audit.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 105 في هذه المجموعة.

فتح الحزمة

k this deck

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 105 في هذه المجموعة.