Deck 3: Using Costs in Decision Making

ملء الشاشة (f)

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

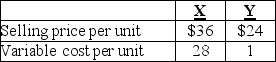

Yurus Manufacturing Company produces two products,X and Y.The following information is presented for both products:

Total fixed costs $234,000

Required:

Assume the sales mix is 3 units of X for every unit of Y:

a.What is the weighted revenue per unit of composite average product,the weighted average variable cost,and the weighted contribution margin per unit of composite average product?

b.What is the break-even point in units of both X and Y?

Total fixed costs $234,000

Required:

Assume the sales mix is 3 units of X for every unit of Y:

a.What is the weighted revenue per unit of composite average product,the weighted average variable cost,and the weighted contribution margin per unit of composite average product?

b.What is the break-even point in units of both X and Y?

سؤال

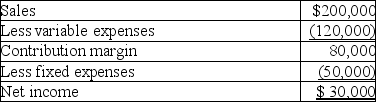

Jeffrey's,Inc.,sells a single product.The company's most recent income statement is given below.

Required:

a.Contribution margin ratio is _______________

b.Break-even point in total sales dollars is _______________

c.To achieve $40,000 in net income,sales must total _______________

d.If sales increase by $50,000 from a $200,000 level,

net income will increase by _______________

Required:

a.Contribution margin ratio is _______________

b.Break-even point in total sales dollars is _______________

c.To achieve $40,000 in net income,sales must total _______________

d.If sales increase by $50,000 from a $200,000 level,

net income will increase by _______________

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

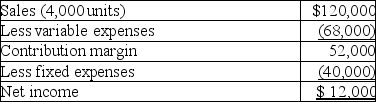

Sunshine,Inc.sells a single product.The company's most recent income statement is given below.

Required:

a.Contribution margin per unit is _______________

b.If sales are doubled to $240,000,

total variable costs will equal _______________

c.If sales are doubled to $240,000,

total fixed costs will equal _______________

d.If Sunshine is past the breakeven point and

10 more units are sold,profits will increase by _______________

e.Compute how many units must be sold to break even. _______________

f.Compute how many units must be sold

to achieve a profit of $20,000. _______________

Required:

a.Contribution margin per unit is _______________

b.If sales are doubled to $240,000,

total variable costs will equal _______________

c.If sales are doubled to $240,000,

total fixed costs will equal _______________

d.If Sunshine is past the breakeven point and

10 more units are sold,profits will increase by _______________

e.Compute how many units must be sold to break even. _______________

f.Compute how many units must be sold

to achieve a profit of $20,000. _______________

سؤال

سؤال

سؤال

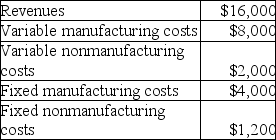

Alistar's Best reported the following for 2011:

Required:

a.Compute the contribution margin.

b.Compute the gross margin.

c.Compute the operating income.

Required:

a.Compute the contribution margin.

b.Compute the gross margin.

c.Compute the operating income.

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

فتح الحزمة

قم بالتسجيل لفتح البطاقات في هذه المجموعة!

Unlock Deck

Unlock Deck

1/128

العب

ملء الشاشة (f)

Deck 3: Using Costs in Decision Making

1

Governments are frequent users of cost reimbursement contracts.

True

2

Fixed costs depend on the resources acquired,not the resources used.

True

3

For external reporting,generally accepted accounting principles require that costs be classified as either variable or fixed costs.

False

4

The salary of the company president is a fixed manufacturing cost.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 128 في هذه المجموعة.

فتح الحزمة

k this deck

5

Fixed costs:

A)may be either direct or indirect costs.

B)vary with production or sales volume.

C)include parts and materials used to manufacture a product.

D)can be adjusted in the short run to meet actual demands.

A)may be either direct or indirect costs.

B)vary with production or sales volume.

C)include parts and materials used to manufacture a product.

D)can be adjusted in the short run to meet actual demands.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 128 في هذه المجموعة.

فتح الحزمة

k this deck

6

To perform cost-volume-profit analysis,a company must be able to separate costs into fixed and variable components.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 128 في هذه المجموعة.

فتح الحزمة

k this deck

7

Selling price per unit is $60,variable cost per unit is $30,and fixed cost per unit is $20.When this company operates above the break-even point,the sale of one more unit will increase net income by $10.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 128 في هذه المجموعة.

فتح الحزمة

k this deck

8

Break-even point is NOT an important concept since the goal of business is to make a profit.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 128 في هذه المجموعة.

فتح الحزمة

k this deck

9

In markets where the organization faces a market-determined price,the organization can set its price using cost plus pricing.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 128 في هذه المجموعة.

فتح الحزمة

k this deck

10

Currently,most companies consider annual salary costs as:

A)a fixed cost.

B)a variable cost.

C)an opportunity cost.

D)a period cost.

A)a fixed cost.

B)a variable cost.

C)an opportunity cost.

D)a period cost.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 128 في هذه المجموعة.

فتح الحزمة

k this deck

11

The time over which a decision maker can adjust capacity is referred to as the short run.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 128 في هذه المجموعة.

فتح الحزمة

k this deck

12

Which of the following describes a variable cost?

A)Variable cost are always indirect costs.

B)Variable costs increase in total when the actual level of activity increases.

C)Variable costs include most personnel costs and depreciation on machinery.

D)Variable costs can always be traced directly to the cost object.

A)Variable cost are always indirect costs.

B)Variable costs increase in total when the actual level of activity increases.

C)Variable costs include most personnel costs and depreciation on machinery.

D)Variable costs can always be traced directly to the cost object.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 128 في هذه المجموعة.

فتح الحزمة

k this deck

13

Currently,most personnel costs are classified as fixed costs.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 128 في هذه المجموعة.

فتح الحزمة

k this deck

14

In recent years,fixed costs have decreased as a proportion of total manufacturing costs.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 128 في هذه المجموعة.

فتح الحزمة

k this deck

15

Describe a variable cost.Describe a fixed cost.Explain why the distinction between variable and fixed costs is important in management accounting.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 128 في هذه المجموعة.

فتح الحزمة

k this deck

16

Variable costs vary with the level of production or sales volume.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 128 في هذه المجموعة.

فتح الحزمة

k this deck

17

Cost-volume-profit analysis may be used for single-product and multiproduct analysis but not in a service environment.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 128 في هذه المجموعة.

فتح الحزمة

k this deck

18

Fixed costs depend on:

A)the amount of resources used.

B)the amount of resources acquired.

C)the volume of production.

D)the volume of sales.

A)the amount of resources used.

B)the amount of resources acquired.

C)the volume of production.

D)the volume of sales.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 128 في هذه المجموعة.

فتح الحزمة

k this deck

19

For general customers,the price charged for a product must cover its long-run cost to the organization.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 128 في هذه المجموعة.

فتح الحزمة

k this deck

20

The most widespread use of cost information is in budgeting.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 128 في هذه المجموعة.

فتح الحزمة

k this deck

21

A company with sales of $100,000,variable costs of $70,000,and fixed costs of $50,000 will reach its break-even point if sales are increased by $20,000.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 128 في هذه المجموعة.

فتح الحزمة

k this deck

22

The break-even point in units for a year is:

A)2,000 units.

B)3,000 units.

C)5,000 units.

D)10,000 units.

A)2,000 units.

B)3,000 units.

C)5,000 units.

D)10,000 units.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 128 في هذه المجموعة.

فتح الحزمة

k this deck

23

The contribution margin per unit is:

A)$6.50.

B)$3.50.

C)$3.00.

D)$1.75.

A)$6.50.

B)$3.50.

C)$3.00.

D)$1.75.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 128 في هذه المجموعة.

فتح الحزمة

k this deck

24

The number of units that must be sold annually to achieve $52,500 of profits is:

A)20,000 units.

B)15,000 units.

C)10,000 units.

D)5,000 units.

A)20,000 units.

B)15,000 units.

C)10,000 units.

D)5,000 units.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 128 في هذه المجموعة.

فتح الحزمة

k this deck

25

All of the following are assumed in a cost-volume-profit analysis EXCEPT:

A)a constant product mix.

B)fixed costs increase when activity increases.

C)revenue per unit does not change as volume changes.

D)all costs can be classified as either fixed or variable.

A)a constant product mix.

B)fixed costs increase when activity increases.

C)revenue per unit does not change as volume changes.

D)all costs can be classified as either fixed or variable.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 128 في هذه المجموعة.

فتح الحزمة

k this deck

26

If the sales mix consists of two units of Product X and one unit of Product Y,what is the break-even point in units for a year?

A)2,000 units of Y and 4,000 units of X

B)2,025 units of Y and 4,050 units of X

C)4,025 units of Y and 8,050 units of X

D)4,000 units of Y and 8,000 units of X

A)2,000 units of Y and 4,000 units of X

B)2,025 units of Y and 4,050 units of X

C)4,025 units of Y and 8,050 units of X

D)4,000 units of Y and 8,000 units of X

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 128 في هذه المجموعة.

فتح الحزمة

k this deck

27

If sales increase by $19,500 in a year,profits will increase by:

A)$10,500.

B)$17,500.

C)$19,500.

D)$35,000.

A)$10,500.

B)$17,500.

C)$19,500.

D)$35,000.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 128 في هذه المجموعة.

فتح الحزمة

k this deck

28

The number of units that EJL must sell annually to make a profit of $75,000 is:

A)7,500 units.

B)18,000 units.

C)21,000 units.

D)30,000 units.

A)7,500 units.

B)18,000 units.

C)21,000 units.

D)30,000 units.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 128 في هذه المجموعة.

فتح الحزمة

k this deck

29

The break-even point is the level at which revenues:

A)equal fixed costs.

B)equal variable costs.

C)equal fixed costs minus flexible costs.

D)equal variable costs plus capacity-related costs.

A)equal fixed costs.

B)equal variable costs.

C)equal fixed costs minus flexible costs.

D)equal variable costs plus capacity-related costs.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 128 في هذه المجموعة.

فتح الحزمة

k this deck

30

Cost-volume-profit analysis assumes all of the following EXCEPT:

A)all costs are purely variable or fixed.

B)units manufactured equal units sold.

C)total variable costs remain the same over the relevant range.

D)total fixed costs remain the same over the relevant range.

A)all costs are purely variable or fixed.

B)units manufactured equal units sold.

C)total variable costs remain the same over the relevant range.

D)total fixed costs remain the same over the relevant range.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 128 في هذه المجموعة.

فتح الحزمة

k this deck

31

What is the operating income for a year,assuming actual sales total 150,000 units,and the sales mix is two units of Product X and one unit of Product Y?

A)$1,200,000

B)$1,250,000

C)$1,750,000

D)None of the above is correct.

A)$1,200,000

B)$1,250,000

C)$1,750,000

D)None of the above is correct.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 128 في هذه المجموعة.

فتح الحزمة

k this deck

32

The number of units that EJL must sell each year to break even is:

A)4,853 units.

B)7,857 units.

C)11,000 units.

D)13,000 units.

A)4,853 units.

B)7,857 units.

C)11,000 units.

D)13,000 units.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 128 في هذه المجموعة.

فتح الحزمة

k this deck

33

The break-even point in units is:

A)total costs divided by variable costs per unit.

B)contribution margin per unit divided by revenue per unit.

C)fixed costs divided by contribution margin per unit.

D)(fixed costs plus variable costs)divided by contribution margin per unit.

A)total costs divided by variable costs per unit.

B)contribution margin per unit divided by revenue per unit.

C)fixed costs divided by contribution margin per unit.

D)(fixed costs plus variable costs)divided by contribution margin per unit.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 128 في هذه المجموعة.

فتح الحزمة

k this deck

34

Contribution margin equals revenues minus:

A)product costs.

B)period costs.

C)variable costs.

D)fixed costs.

A)product costs.

B)period costs.

C)variable costs.

D)fixed costs.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 128 في هذه المجموعة.

فتح الحزمة

k this deck

35

If the sales mix consists of two units of Product X and one unit of Product Y,what is the weighted revenue per unit of composite product?

A)$10.00

B)$11.66

C)$13.33

D)$15.00

A)$10.00

B)$11.66

C)$13.33

D)$15.00

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 128 في هذه المجموعة.

فتح الحزمة

k this deck

36

The contribution margin per unit is:

A)$7.50.

B)$10.50.

C)$12.

D)$14.

A)$7.50.

B)$10.50.

C)$12.

D)$14.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 128 في هذه المجموعة.

فتح الحزمة

k this deck

37

Cost-volume-profit analysis is used PRIMARILY by management:

A)as a planning tool.

B)for control purposes.

C)to establish a target net income for next year.

D)to attain extremely accurate financial results.

A)as a planning tool.

B)for control purposes.

C)to establish a target net income for next year.

D)to attain extremely accurate financial results.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 128 في هذه المجموعة.

فتح الحزمة

k this deck

38

In multiproduct situations,when the sales mix shifts toward the product with the highest contribution margin per unit,then:

A)total revenues will decrease.

B)breakeven quantity will increase.

C)total contribution margin will decrease.

D)operating income will increase.

A)total revenues will decrease.

B)breakeven quantity will increase.

C)total contribution margin will decrease.

D)operating income will increase.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 128 في هذه المجموعة.

فتح الحزمة

k this deck

39

If the sales mix shifts to one unit of Product X and two units of Product Y,then the contribution margin per unit of composite product will:

A)increase per unit.

B)stay the same.

C)decrease per unit.

D)be undeterminable.

A)increase per unit.

B)stay the same.

C)decrease per unit.

D)be undeterminable.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 128 في هذه المجموعة.

فتح الحزمة

k this deck

40

In multiproduct situations when the sales mix shifts toward the product with the lowest contribution margin per unit,the break-even quantity will decrease.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 128 في هذه المجموعة.

فتح الحزمة

k this deck

41

An example of a sunk cost is the historical cost paid for equipment.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 128 في هذه المجموعة.

فتح الحزمة

k this deck

42

What is meant by the term break-even point? Why should a manager be concerned about the break-even point?

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 128 في هذه المجموعة.

فتح الحزمة

k this deck

43

Depreciation expense allocated to a product line is a relevant cost when deciding to discontinue that product.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 128 في هذه المجموعة.

فتح الحزمة

k this deck

44

When replacing an old machine with a new machine,the book value of the old machine is a relevant cost.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 128 في هذه المجموعة.

فتح الحزمة

k this deck

45

For a particular decision,differential revenues and costs are always relevant.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 128 في هذه المجموعة.

فتح الحزمة

k this deck

46

Yurus Manufacturing Company produces two products,X and Y.The following information is presented for both products:

Total fixed costs $234,000

Required:

Assume the sales mix is 3 units of X for every unit of Y:

a.What is the weighted revenue per unit of composite average product,the weighted average variable cost,and the weighted contribution margin per unit of composite average product?

b.What is the break-even point in units of both X and Y?

Total fixed costs $234,000

Required:

Assume the sales mix is 3 units of X for every unit of Y:

a.What is the weighted revenue per unit of composite average product,the weighted average variable cost,and the weighted contribution margin per unit of composite average product?

b.What is the break-even point in units of both X and Y?

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 128 في هذه المجموعة.

فتح الحزمة

k this deck

47

Jeffrey's,Inc.,sells a single product.The company's most recent income statement is given below.

Required:

a.Contribution margin ratio is _______________

b.Break-even point in total sales dollars is _______________

c.To achieve $40,000 in net income,sales must total _______________

d.If sales increase by $50,000 from a $200,000 level,

net income will increase by _______________

Required:

a.Contribution margin ratio is _______________

b.Break-even point in total sales dollars is _______________

c.To achieve $40,000 in net income,sales must total _______________

d.If sales increase by $50,000 from a $200,000 level,

net income will increase by _______________

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 128 في هذه المجموعة.

فتح الحزمة

k this deck

48

Explain when a manager would use cost-volume-profit analysis.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 128 في هذه المجموعة.

فتح الحزمة

k this deck

49

In 2011,SSPC Company has sales of 8,000 units at $10 each,variable costs totaling $20,000,and fixed costs of $30,000.In 2008,the company expects annual insurance costs to increase by $4,000 to $9,000.

Required:

a.Calculate operating income and the breakeven point in units for 2011.

b.Calculate the breakeven point in units for 2012.

Required:

a.Calculate operating income and the breakeven point in units for 2011.

b.Calculate the breakeven point in units for 2012.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 128 في هذه المجموعة.

فتح الحزمة

k this deck

50

In make-or-buy decisions,the suppliers' reputation for quality and service is a relevant quantitative factor.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 128 في هذه المجموعة.

فتح الحزمة

k this deck

51

Opportunity costs are implicit costs.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 128 في هذه المجموعة.

فتح الحزمة

k this deck

52

When opportunity costs exist,they are always relevant.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 128 في هذه المجموعة.

فتح الحزمة

k this deck

53

When a firm maximizes profits it will simultaneously minimize opportunity costs.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 128 في هذه المجموعة.

فتح الحزمة

k this deck

54

For decision-making,differential costs assist in choosing between alternatives.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 128 في هذه المجموعة.

فتح الحزمة

k this deck

55

Avoidable costs are eliminated when a product is outsourced.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 128 في هذه المجموعة.

فتح الحزمة

k this deck

56

Sunk costs are always irrelevant costs for decision making.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 128 في هذه المجموعة.

فتح الحزمة

k this deck

57

Sunshine,Inc.sells a single product.The company's most recent income statement is given below.

Required:

a.Contribution margin per unit is _______________

b.If sales are doubled to $240,000,

total variable costs will equal _______________

c.If sales are doubled to $240,000,

total fixed costs will equal _______________

d.If Sunshine is past the breakeven point and

10 more units are sold,profits will increase by _______________

e.Compute how many units must be sold to break even. _______________

f.Compute how many units must be sold

to achieve a profit of $20,000. _______________

Required:

a.Contribution margin per unit is _______________

b.If sales are doubled to $240,000,

total variable costs will equal _______________

c.If sales are doubled to $240,000,

total fixed costs will equal _______________

d.If Sunshine is past the breakeven point and

10 more units are sold,profits will increase by _______________

e.Compute how many units must be sold to break even. _______________

f.Compute how many units must be sold

to achieve a profit of $20,000. _______________

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 128 في هذه المجموعة.

فتح الحزمة

k this deck

58

A cost may be relevant for one decision,but not relevant for a different decision.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 128 في هذه المجموعة.

فتح الحزمة

k this deck

59

If the sales mix shifts to one unit of Product X and two units of Product Y,then the break-even point in units for a year will:

A)increase.

B)stay the same.

C)decrease.

D)be undeterminable.

A)increase.

B)stay the same.

C)decrease.

D)be undeterminable.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 128 في هذه المجموعة.

فتح الحزمة

k this deck

60

Alistar's Best reported the following for 2011:

Required:

a.Compute the contribution margin.

b.Compute the gross margin.

c.Compute the operating income.

Required:

a.Compute the contribution margin.

b.Compute the gross margin.

c.Compute the operating income.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 128 في هذه المجموعة.

فتح الحزمة

k this deck

61

In determining whether to keep or drop a product line,avoidable fixed costs are relevant to the decision.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 128 في هذه المجموعة.

فتح الحزمة

k this deck

62

Bid prices and costs that are relevant for regular orders are the same costs that are relevant for one-time-only special orders.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 128 في هذه المجموعة.

فتح الحزمة

k this deck

63

For decision making,a listing of the relevant costs:

A)will help the decision maker concentrate on the pertinent data.

B)will only include future costs.

C)will only include costs that differ among the decision alternatives.

D)should include all of the above.

A)will help the decision maker concentrate on the pertinent data.

B)will only include future costs.

C)will only include costs that differ among the decision alternatives.

D)should include all of the above.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 128 في هذه المجموعة.

فتح الحزمة

k this deck

64

For one-time-only special orders,variable costs may be relevant but not fixed costs.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 128 في هذه المجموعة.

فتح الحزمة

k this deck

65

If a company is deciding whether to outsource a part,the reliability of the supplier is an important factor to consider.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 128 في هذه المجموعة.

فتح الحزمة

k this deck

66

A processing cycle efficiency (PCE)of 18% indicates better efficiency than a PCE of 50%.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 128 في هذه المجموعة.

فتح الحزمة

k this deck

67

Outsourcing is risk-free to the purchaser of a part because the supplier now has the responsibility of producing the part.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 128 في هذه المجموعة.

فتح الحزمة

k this deck

68

In linear programming,total fixed costs will remain unchanged regardless of the production plan.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 128 في هذه المجموعة.

فتح الحزمة

k this deck

69

If a company is deciding whether to outsource a part,business-sustaining costs are always unavoidable.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 128 في هذه المجموعة.

فتح الحزمة

k this deck

70

Costs are relevant to a particular decision if they:

A)are variable costs.

B)are fixed costs.

C)differ across, the decision alternatives being considered.

D)remain unchanged across the alternatives being considered.

A)are variable costs.

B)are fixed costs.

C)differ across, the decision alternatives being considered.

D)remain unchanged across the alternatives being considered.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 128 في هذه المجموعة.

فتح الحزمة

k this deck

71

Costs that cannot be changed by any decision made now or in the future are:

A)fixed costs.

B)indirect costs.

C)avoidable costs.

D)sunk costs.

A)fixed costs.

B)indirect costs.

C)avoidable costs.

D)sunk costs.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 128 في هذه المجموعة.

فتح الحزمة

k this deck

72

Problems involving two or more constraints are often solved using linear programming.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 128 في هذه المجموعة.

فتح الحزمة

k this deck

73

Sunk costs include:

A)the original cost of the existing system.

B)the original cost of the new system.

C)the current salvage value of the existing system.

D)the annual operating cost of the new system.

A)the original cost of the existing system.

B)the original cost of the new system.

C)the current salvage value of the existing system.

D)the annual operating cost of the new system.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 128 في هذه المجموعة.

فتح الحزمة

k this deck

74

Which of the following costs are NEVER relevant in the decision-making process?

A)fixed costs

B)historical costs

C)relevant costs

D)variable costs

A)fixed costs

B)historical costs

C)relevant costs

D)variable costs

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 128 في هذه المجموعة.

فتح الحزمة

k this deck

75

Sunk costs:

A)are relevant.

B)are differential.

C)have future implications.

D)are ignored when evaluating alternatives.

A)are relevant.

B)are differential.

C)have future implications.

D)are ignored when evaluating alternatives.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 128 في هذه المجموعة.

فتح الحزمة

k this deck

76

In evaluating different alternatives,it is useful to concentrate on:

A)variable costs.

B)fixed costs.

C)total costs.

D)relevant costs.

A)variable costs.

B)fixed costs.

C)total costs.

D)relevant costs.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 128 في هذه المجموعة.

فتح الحزمة

k this deck

77

Sometimes qualitative factors are the most important factors in make-or-buy decisions.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 128 في هذه المجموعة.

فتح الحزمة

k this deck

78

When deciding to purchase a new cutting machine or continue using the old machine,the following costs are all relevant EXCEPT the:

A)$100,000 cost of the old machine.

B)$40,000 cost of the new machine.

C)$20,000 disposal value of the old machine.

D)$6,000 annual savings in operating costs if the new machine is purchased.

A)$100,000 cost of the old machine.

B)$40,000 cost of the new machine.

C)$20,000 disposal value of the old machine.

D)$6,000 annual savings in operating costs if the new machine is purchased.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 128 في هذه المجموعة.

فتح الحزمة

k this deck

79

The cost of a computer system installed last year is an example of:

A)a sunk cost.

B)a relevant cost.

C)a differential cost.

D)an avoidable cost.

A)a sunk cost.

B)a relevant cost.

C)a differential cost.

D)an avoidable cost.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 128 في هذه المجموعة.

فتح الحزمة

k this deck

80

In determining whether to keep or drop a product line,product contribution is calculated as sales minus variable costs,minus avoidable fixed costs.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 128 في هذه المجموعة.

فتح الحزمة

k this deck

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 128 في هذه المجموعة.