Deck 5: Uncertainty

ملء الشاشة (f)

سؤال

سؤال

Suppose a person's utility of wealth is given by

And his or her initial wealth is 10,000.What is the maximum amount he or she would pay for insurance against a 50 percent chance of losing 3,600?

A)1,800

B)1,900

C)2,000

D)2,100

And his or her initial wealth is 10,000.What is the maximum amount he or she would pay for insurance against a 50 percent chance of losing 3,600?

A)1,800

B)1,900

C)2,000

D)2,100

سؤال

سؤال

سؤال

An individual whose utility function is given by

(where Wi is wealth in state i)will:

A)never gamble no matter how favorable the odds.

B)only gamble if the expected value of the bet is positive.

C)gamble if the bet is not too unfair.

D)always gamble,no matter how unfavorable the odds.

(where Wi is wealth in state i)will:

A)never gamble no matter how favorable the odds.

B)only gamble if the expected value of the bet is positive.

C)gamble if the bet is not too unfair.

D)always gamble,no matter how unfavorable the odds.

سؤال

سؤال

Which of the following utility functions would indicate the most (relative)risk-averse behavior?

A)

B)

C)

D)

A)

B)

C)

D)

سؤال

سؤال

سؤال

سؤال

The formula for the Pratt measure of risk aversion is:

A)

B)

C)

D)

A)

B)

C)

D)

سؤال

سؤال

سؤال

Which of the following utility functions exhibits constant absolute risk aversion?

A)

B)

C)

D)

A)

B)

C)

D)

سؤال

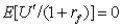

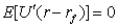

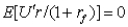

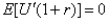

The condition for optimal portfolio choice can be represented by:

A)

B)

C)

D)

A)

B)

C)

D)

سؤال

Which of the following utility functions exhibits constant relative risk aversion?

A)

B)

C)

D)

A)

B)

C)

D)

سؤال

سؤال

سؤال

فتح الحزمة

قم بالتسجيل لفتح البطاقات في هذه المجموعة!

Unlock Deck

Unlock Deck

1/19

العب

ملء الشاشة (f)

Deck 5: Uncertainty

1

An option may add value to a transaction because:

A)interest charges are reduced.

B)the price of the good is reduced.

C)additional information may become available.

D)options provide buyers with monopsony power.

A)interest charges are reduced.

B)the price of the good is reduced.

C)additional information may become available.

D)options provide buyers with monopsony power.

additional information may become available.

2

Suppose a person's utility of wealth is given by

And his or her initial wealth is 10,000.What is the maximum amount he or she would pay for insurance against a 50 percent chance of losing 3,600?

A)1,800

B)1,900

C)2,000

D)2,100

And his or her initial wealth is 10,000.What is the maximum amount he or she would pay for insurance against a 50 percent chance of losing 3,600?

A)1,800

B)1,900

C)2,000

D)2,100

1,900

3

An individual will never buy complete insurance if:

A)he or she is risk averse.

B)insurance premiums are unfair.

C)he or she is a risk taker.

D)insurance premiums are fair.

A)he or she is risk averse.

B)insurance premiums are unfair.

C)he or she is a risk taker.

D)insurance premiums are fair.

he or she is a risk taker.

4

A risk-averse individual is offered a gamble that promises a gain of $1000 with probability 0.25 and a loss of $300 with probability 0.75.Given this situation,he or she will:

A)definitely take the gamble.

B)definitely not take the gamble.

C)definitely take the gamble if his or her income is high enough.

D)take an action that cannot be determined given the information available.

A)definitely take the gamble.

B)definitely not take the gamble.

C)definitely take the gamble if his or her income is high enough.

D)take an action that cannot be determined given the information available.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 19 في هذه المجموعة.

فتح الحزمة

k this deck

5

An individual whose utility function is given by

(where Wi is wealth in state i)will:

A)never gamble no matter how favorable the odds.

B)only gamble if the expected value of the bet is positive.

C)gamble if the bet is not too unfair.

D)always gamble,no matter how unfavorable the odds.

(where Wi is wealth in state i)will:

A)never gamble no matter how favorable the odds.

B)only gamble if the expected value of the bet is positive.

C)gamble if the bet is not too unfair.

D)always gamble,no matter how unfavorable the odds.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 19 في هذه المجموعة.

فتح الحزمة

k this deck

6

People who always choose not to participate in fair games are called:

A)risk takers.

B)risk averse.

C)risk neutral.

D)broke.

A)risk takers.

B)risk averse.

C)risk neutral.

D)broke.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 19 في هذه المجموعة.

فتح الحزمة

k this deck

7

Which of the following utility functions would indicate the most (relative)risk-averse behavior?

A)

B)

C)

D)

A)

B)

C)

D)

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 19 في هذه المجموعة.

فتح الحزمة

k this deck

8

If a fair game is played many times the monetary losses or gains will:

A)approach zero.

B)be negative.

C)be positive.

D)result in an outcome that cannot be determined without more information.

A)approach zero.

B)be negative.

C)be positive.

D)result in an outcome that cannot be determined without more information.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 19 في هذه المجموعة.

فتح الحزمة

k this deck

9

A risk-neutral individual is offered a gamble that promises a gain of $1000 with probability 0.25 and a loss of $300 with probability 0.75.Given this situation,he or she will:

A)definitely take the gamble.

B)definitely not take the gamble.

C)definitely take the gamble if his or her income is high enough.

D)take an action that cannot be determined given the information available.

A)definitely take the gamble.

B)definitely not take the gamble.

C)definitely take the gamble if his or her income is high enough.

D)take an action that cannot be determined given the information available.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 19 في هذه المجموعة.

فتح الحزمة

k this deck

10

Risk-averse individuals will diversify their investments because this will:

A)increase their expected returns.

B)provide them with some much-needed variety.

C)reduce the variability of their returns.

D)reduce their transaction costs.

A)increase their expected returns.

B)provide them with some much-needed variety.

C)reduce the variability of their returns.

D)reduce their transaction costs.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 19 في هذه المجموعة.

فتح الحزمة

k this deck

11

The formula for the Pratt measure of risk aversion is:

A)

B)

C)

D)

A)

B)

C)

D)

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 19 في هذه المجموعة.

فتح الحزمة

k this deck

12

Risk aversion is best explained by:

A)timidness.

B)increasing marginal utility of wealth.

C)constant marginal utility of wealth.

D)decreasing marginal utility of wealth.

A)timidness.

B)increasing marginal utility of wealth.

C)constant marginal utility of wealth.

D)decreasing marginal utility of wealth.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 19 في هذه المجموعة.

فتح الحزمة

k this deck

13

The expected value of a random variable is:

A)the measure of its variability.

B)the most likely outcome.

C)the outcome that will occur on average.

D)the relative frequency of a realization.

A)the measure of its variability.

B)the most likely outcome.

C)the outcome that will occur on average.

D)the relative frequency of a realization.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 19 في هذه المجموعة.

فتح الحزمة

k this deck

14

Which of the following utility functions exhibits constant absolute risk aversion?

A)

B)

C)

D)

A)

B)

C)

D)

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 19 في هذه المجموعة.

فتح الحزمة

k this deck

15

The condition for optimal portfolio choice can be represented by:

A)

B)

C)

D)

A)

B)

C)

D)

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 19 في هذه المجموعة.

فتح الحزمة

k this deck

16

Which of the following utility functions exhibits constant relative risk aversion?

A)

B)

C)

D)

A)

B)

C)

D)

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 19 في هذه المجموعة.

فتح الحزمة

k this deck

17

More risk-averse people will:

A)hold fewer risky assets because marginal utility is rapidly diminishing.

B)hold fewer risky assets because marginal utility is greater.

C)hold fewer risky assets because rates of return are more uncertain.

D)hold fewer risky assets because marginal utility is negative.

A)hold fewer risky assets because marginal utility is rapidly diminishing.

B)hold fewer risky assets because marginal utility is greater.

C)hold fewer risky assets because rates of return are more uncertain.

D)hold fewer risky assets because marginal utility is negative.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 19 في هذه المجموعة.

فتح الحزمة

k this deck

18

What property of the von-Neumann Morgenstern utility function is related to risk aversion?

A)Its upward slope

B)Its downward slope

C)Its convexity

D)Its concavity

A)Its upward slope

B)Its downward slope

C)Its convexity

D)Its concavity

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 19 في هذه المجموعة.

فتح الحزمة

k this deck

19

Faced with an uncertain situation,the best decision for a person obeying the von-Neumann Morgenstern axioms:

A)minimizes loss relative to the status quo.

B)minimizes variability across possible outcomes.

C)maximizes the expected payoff.

D)maximizes expected utility.

A)minimizes loss relative to the status quo.

B)minimizes variability across possible outcomes.

C)maximizes the expected payoff.

D)maximizes expected utility.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 19 في هذه المجموعة.

فتح الحزمة

k this deck

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 19 في هذه المجموعة.