Deck 10: Interest Rate and Currency Swaps

ملء الشاشة (f)

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

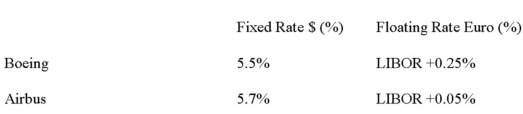

The following information is given.

Boeing and Airbus have agreed to swap their debt payments so that each firm gets its preferred debt terms.Each firm will save the same amount in percentage terms.

Boeing and Airbus have agreed to swap their debt payments so that each firm gets its preferred debt terms.Each firm will save the same amount in percentage terms.

a)Does Boeing prefer fixed or floating rate debt? What rate does it pay on its preferred debt?

b)Does Airbus prefer fixed or floating rate debt? What rate does it pay on its preferred debt?

c)What are the total interest savings available in this interest rate swap?

d)Which company has the advantage in fixed rate debt?

Boeing and Airbus have agreed to swap their debt payments so that each firm gets its preferred debt terms.Each firm will save the same amount in percentage terms.a)Does Boeing prefer fixed or floating rate debt? What rate does it pay on its preferred debt?

b)Does Airbus prefer fixed or floating rate debt? What rate does it pay on its preferred debt?

c)What are the total interest savings available in this interest rate swap?

d)Which company has the advantage in fixed rate debt?

سؤال

سؤال

سؤال

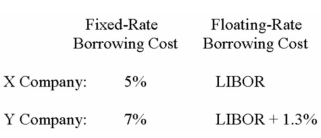

The following information is given:

Both parties want to engage in an interest rate swap.Assume that S Bank will arrange for an interest rate swap between X Company and Y Company for 0.1%.Also,assume that X Company gets 2/3 of the interest savings available.

Both parties want to engage in an interest rate swap.Assume that S Bank will arrange for an interest rate swap between X Company and Y Company for 0.1%.Also,assume that X Company gets 2/3 of the interest savings available.

a)Which company has a better credit rating?

b)What is the quality spread differential?

c)What is X Company's preferred type of debt? What rate of interest does it pay on this debt after the swap?

d)What is Y Company's preferred type of debt? What rate of interest does it pay on this debt after the swap?

e)Illustrate the cash flows from this swap.Assume that X Company pays LIBOR to S Bank.

Both parties want to engage in an interest rate swap.Assume that S Bank will arrange for an interest rate swap between X Company and Y Company for 0.1%.Also,assume that X Company gets 2/3 of the interest savings available.a)Which company has a better credit rating?

b)What is the quality spread differential?

c)What is X Company's preferred type of debt? What rate of interest does it pay on this debt after the swap?

d)What is Y Company's preferred type of debt? What rate of interest does it pay on this debt after the swap?

e)Illustrate the cash flows from this swap.Assume that X Company pays LIBOR to S Bank.

سؤال

سؤال

فتح الحزمة

قم بالتسجيل لفتح البطاقات في هذه المجموعة!

Unlock Deck

Unlock Deck

1/27

العب

ملء الشاشة (f)

Deck 10: Interest Rate and Currency Swaps

1

-If company A and company B share the interest savings from the interest rate swap equally,company A will pay after the swap on its preferred debt:

A) 5.5%.

B) 5.75%.

C) LIBOR - 0.75%.

D) LIBOR.

5.75%.

2

Company A swaps fixed-rate US dollar debt with Company B for floating-rate Canadian dollar debt.This is a:

A) single-currency interest rate swap.

B) currency swap.

C) cross-currency interest rate swap.

D) None of these.

A) single-currency interest rate swap.

B) currency swap.

C) cross-currency interest rate swap.

D) None of these.

C

3

Swap bank quotes 5.40-5.70 for the euro.This means the swap bank will:

A) receive 5.40 percent semi-annual fixed payments against paying six-month LIBOR.

B) receive 5.70 percent semi-annual fixed payments against paying six-month LIBOR.

C) pay 5.70 percent semi-annual fixed payments against receiving six-month LIBOR.

D) None of these.

A) receive 5.40 percent semi-annual fixed payments against paying six-month LIBOR.

B) receive 5.70 percent semi-annual fixed payments against paying six-month LIBOR.

C) pay 5.70 percent semi-annual fixed payments against receiving six-month LIBOR.

D) None of these.

B

4

The Canadian firm wants to borrow in euros and the French firm wants to borrow in Canadian dollars.

-Which firms will benefit from a currency swap?

A) Neither firm.

B) The Canadian firm only.

C) Both firms.

D) Need more information.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 27 في هذه المجموعة.

فتح الحزمة

k this deck

5

-Calculate the quality spread differential (QSD):

A) 0.50%.

B) 1.00%.

C) 1.50%.

D) 2.00%.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 27 في هذه المجموعة.

فتح الحزمة

k this deck

6

Which combination of the following statements is true about a swap bank?

(i)- It is a generic term to describe a financial institution that facilitates swaps between counterparties.

(ii)- It can be an international commercial bank.

(iii)- It can be an investment bank.

(iv)- It can be a merchant bank.

(v)- It can be an independent operator.

A) (i) and (ii)

B) (i), (ii) and (iii)

C) (i), (ii), (iii) and (iv)

D) (i), (ii), (iii), (iv) and (v)

(i)- It is a generic term to describe a financial institution that facilitates swaps between counterparties.

(ii)- It can be an international commercial bank.

(iii)- It can be an investment bank.

(iv)- It can be a merchant bank.

(v)- It can be an independent operator.

A) (i) and (ii)

B) (i), (ii) and (iii)

C) (i), (ii), (iii) and (iv)

D) (i), (ii), (iii), (iv) and (v)

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 27 في هذه المجموعة.

فتح الحزمة

k this deck

7

-What rate would company A have to pay on its floating rate debt so that an interest rate swap would no longer benefit each party?

A) LIBOR - 0.5

B) LIBOR

C) LIBOR + 0.5

D) An interest swap is always beneficial for both parties involved.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 27 في هذه المجموعة.

فتح الحزمة

k this deck

8

Which of the following swaps are also knows as "plain vanilla" swaps?

A) "Fixed-for-fixed" single currency swap.

B) "Fixed-for-floating" single currency swap.

C) "Fixed-for-fixed" currency swap involving two different currencies.

D) "Floating -for- floating" currency swap involving two different currencies.

A) "Fixed-for-fixed" single currency swap.

B) "Fixed-for-floating" single currency swap.

C) "Fixed-for-fixed" currency swap involving two different currencies.

D) "Floating -for- floating" currency swap involving two different currencies.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 27 في هذه المجموعة.

فتح الحزمة

k this deck

9

Which of the following are possible swaps?

A) Floating-for-floating.

B) Zero-coupon for floating.

C) Fixed for floating.

D) All of these.

A) Floating-for-floating.

B) Zero-coupon for floating.

C) Fixed for floating.

D) All of these.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 27 في هذه المجموعة.

فتح الحزمة

k this deck

10

Examples of "single-currency interest rate swap" and "cross-currency interest rate swap" is/are:

A) fixed-for-floating rate interest rate swap, where one counterparty exchanges the principal payment of a floating-rate debt obligations for fixed-rate principal payment of the other counter party.

B) fixed-for-fixed rate debt service (currency swap), where one counterparty exchanges the debt service obligations of a bond denominated in one currency for the debt service obligations of the other counter party denominated in same currency.

C) fixed-for-floating rate interest rate swap, where one counterparty exchanges the interest payments of a floating-rate debt obligations for fixed-rate interest payments of the other counter party.

D) None of these

A) fixed-for-floating rate interest rate swap, where one counterparty exchanges the principal payment of a floating-rate debt obligations for fixed-rate principal payment of the other counter party.

B) fixed-for-fixed rate debt service (currency swap), where one counterparty exchanges the debt service obligations of a bond denominated in one currency for the debt service obligations of the other counter party denominated in same currency.

C) fixed-for-floating rate interest rate swap, where one counterparty exchanges the interest payments of a floating-rate debt obligations for fixed-rate interest payments of the other counter party.

D) None of these

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 27 في هذه المجموعة.

فتح الحزمة

k this deck

11

Which combination of the following statements is true about the risks that a swap dealer confronts:

(i)- interest rate risk

(ii)- basis risk

(iii)- exchange rate risk

(iv)- mismatch risk

(v)- sovereign risk

A) (i), (ii), (iii), and (v)

B) (i), (iii), and (iv)

C) (iii), (iv), and (iv)

D) (i), (ii), (iii), (iv), and (v)

(i)- interest rate risk

(ii)- basis risk

(iii)- exchange rate risk

(iv)- mismatch risk

(v)- sovereign risk

A) (i), (ii), (iii), and (v)

B) (i), (iii), and (iv)

C) (iii), (iv), and (iv)

D) (i), (ii), (iii), (iv), and (v)

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 27 في هذه المجموعة.

فتح الحزمة

k this deck

12

XYZ Corporation enters into a 6-year interest rate swap with a swap bank in which it agrees to pay the swap bank a fixed-rate of 9 percent annually on a notional amount of SF10,000,000 and receive LIBOR - ½ percent.As of the third reset date (i.e.mid-way through the 6 year agreement),calculate the price of the swap,assuming that the fixed-rate at which XYZ can borrow has increased to 10%.(Round your final answer to nearest SF and Do not round intermediate calculations)

A) SF248,685

B) SF900,000

C) SF2,700,000

D) SF7,300,000

A) SF248,685

B) SF900,000

C) SF2,700,000

D) SF7,300,000

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 27 في هذه المجموعة.

فتح الحزمة

k this deck

13

The term interest rate swaps:

A) refers to a "single-currency interest rate swap" shortened to "interest rate swap".

B) involves "counterparties" who make a contractual agreement to exchange cash flows at periodic intervals.

C) can be "fixed-for-floating rate" or "fixed-for-fixed rate".

D) All of these.

A) refers to a "single-currency interest rate swap" shortened to "interest rate swap".

B) involves "counterparties" who make a contractual agreement to exchange cash flows at periodic intervals.

C) can be "fixed-for-floating rate" or "fixed-for-fixed rate".

D) All of these.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 27 في هذه المجموعة.

فتح الحزمة

k this deck

14

Find the QSD.

A) 0%

B) 0.5%

C) 0.8%

D) 1%

A) 0%

B) 0.5%

C) 0.8%

D) 1%

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 27 في هذه المجموعة.

فتح الحزمة

k this deck

15

The primary reasons for a counterparty to use a currency swap are:

A) to hedge and to speculate.

B) to play in the futures and forward markets.

C) to obtain debt financing in the swapped currency at an interest cost reduction brought about through comparative advantages each counterparty has in its national capital market, and the benefit of hedging long-run exchange rate exposure.

D) to gamble in the futures and forward markets.

A) to hedge and to speculate.

B) to play in the futures and forward markets.

C) to obtain debt financing in the swapped currency at an interest cost reduction brought about through comparative advantages each counterparty has in its national capital market, and the benefit of hedging long-run exchange rate exposure.

D) to gamble in the futures and forward markets.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 27 في هذه المجموعة.

فتح الحزمة

k this deck

16

Suppose ABC Investment Banker,Ltd.is quoting swap rates as follows: 7.50 - 7.85 percent annually against six-month dollar LIBOR for dollars,and 11.00 - 11.30 percent annually against six-month dollar LIBOR for British pound sterling.ABC would enter into a $/£ currency swap in which:

A) it would pay annual fixed-rate dollar payments of 7.85% in return for receiving annual fixed-rate £ payments at 11.3%.

B) it will receive annual fixed-rate dollar payments at 7.5% against paying annual fixed-rate £ payments at 11%.

C) it would pay annual fixed-rate dollar payments of 7.5% in return for receiving annual fixed-rate £ payments at 11.3%.

D) None of these.

A) it would pay annual fixed-rate dollar payments of 7.85% in return for receiving annual fixed-rate £ payments at 11.3%.

B) it will receive annual fixed-rate dollar payments at 7.5% against paying annual fixed-rate £ payments at 11%.

C) it would pay annual fixed-rate dollar payments of 7.5% in return for receiving annual fixed-rate £ payments at 11.3%.

D) None of these.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 27 في هذه المجموعة.

فتح الحزمة

k this deck

17

Find the profit of the swap bank next year if next year the exchange rate will be $1.65/£.

A) $2000

B) $2500

C) $3000

D) $3500

A) $2000

B) $2500

C) $3000

D) $3500

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 27 في هذه المجموعة.

فتح الحزمة

k this deck

18

Some of the risks that a swap dealer confronts are "basis risk" and "sovereign risk." They are defined as:

A) "basis risk refers" to the probability that a country will impose exchange restrictions on a currency involved in a swap, and "sovereign risk refers" to a situation in which the floating rates of the two counterparties are not pegged to the same index.

B) "basis risk refers" to a situation in which the floating rates of the two counterparties are not pegged to the same index and "sovereign risk" refers to the probability that a country will impose exchange restrictions on a currency involved in a swap.

C) "basis risk" refers to interest rate changing unfavorably before the swap bank can lay off to an opposing counterparty the other side of an interest rate swap entered into with a counterparty, and "sovereign risk" refers to the probability that a country will impose exchange restrictions on a currency involved in a swap.

D) "basis risk" refers to the risk of fluctuating exchange rates, and "sovereign risk refers" to a situation in which the floating rates of the two counterparties are not pegged to the same index.

A) "basis risk refers" to the probability that a country will impose exchange restrictions on a currency involved in a swap, and "sovereign risk refers" to a situation in which the floating rates of the two counterparties are not pegged to the same index.

B) "basis risk refers" to a situation in which the floating rates of the two counterparties are not pegged to the same index and "sovereign risk" refers to the probability that a country will impose exchange restrictions on a currency involved in a swap.

C) "basis risk" refers to interest rate changing unfavorably before the swap bank can lay off to an opposing counterparty the other side of an interest rate swap entered into with a counterparty, and "sovereign risk" refers to the probability that a country will impose exchange restrictions on a currency involved in a swap.

D) "basis risk" refers to the risk of fluctuating exchange rates, and "sovereign risk refers" to a situation in which the floating rates of the two counterparties are not pegged to the same index.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 27 في هذه المجموعة.

فتح الحزمة

k this deck

19

Use the following information to calculate the quality spread differential (QSD):

A) 0.50%

B) 1.00%

C) 1.50%

D) 2.00%

A) 0.50%

B) 1.00%

C) 1.50%

D) 2.00%

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 27 في هذه المجموعة.

فتح الحزمة

k this deck

20

Which of the following is NOT true about swap banks?

A) A swap bank can be an international commercial bank.

B) A swap bank can be an investment bank.

C) A swap bank can be a central bank.

D) A swap bank can be an independent operator.

A) A swap bank can be an international commercial bank.

B) A swap bank can be an investment bank.

C) A swap bank can be a central bank.

D) A swap bank can be an independent operator.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 27 في هذه المجموعة.

فتح الحزمة

k this deck

21

The Canadian firm wants to borrow in euros and the French firm wants to borrow in Canadian dollars.

-Find QSD

A) 1%

B) 1.2%

C) 2.2%

D) 3.2%

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 27 في هذه المجموعة.

فتح الحزمة

k this deck

22

The following information is given.

Boeing and Airbus have agreed to swap their debt payments so that each firm gets its preferred debt terms.Each firm will save the same amount in percentage terms.

a)Does Boeing prefer fixed or floating rate debt? What rate does it pay on its preferred debt?

b)Does Airbus prefer fixed or floating rate debt? What rate does it pay on its preferred debt?

c)What are the total interest savings available in this interest rate swap?

d)Which company has the advantage in fixed rate debt?

Boeing and Airbus have agreed to swap their debt payments so that each firm gets its preferred debt terms.Each firm will save the same amount in percentage terms.a)Does Boeing prefer fixed or floating rate debt? What rate does it pay on its preferred debt?

b)Does Airbus prefer fixed or floating rate debt? What rate does it pay on its preferred debt?

c)What are the total interest savings available in this interest rate swap?

d)Which company has the advantage in fixed rate debt?

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 27 في هذه المجموعة.

فتح الحزمة

k this deck

23

The Canadian firm wants to borrow in euros and the French firm wants to borrow in Canadian dollars.

-If the Canadian and the French firms share the interest savings from the currency swap equally,the Canadian firm will pay on its French debt after the swap:

A) The same as without the swap.

B) 5%.

C) 5.5%.

D) 6%.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 27 في هذه المجموعة.

فتح الحزمة

k this deck

24

The Canadian firm wants to borrow in euros and the French firm wants to borrow in Canadian dollars.

-What will be the annual GROSS interest payment of firm A to the swap bank? (where "GROSS" means that it does not take into account the payment made by the swap bank to firm A on the loan that firm A made to the swap bank)

A) £66,000

B) £76,000

C) $72,000

D) $216,000

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 27 في هذه المجموعة.

فتح الحزمة

k this deck

25

The following information is given:

Both parties want to engage in an interest rate swap.Assume that S Bank will arrange for an interest rate swap between X Company and Y Company for 0.1%.Also,assume that X Company gets 2/3 of the interest savings available.

a)Which company has a better credit rating?

b)What is the quality spread differential?

c)What is X Company's preferred type of debt? What rate of interest does it pay on this debt after the swap?

d)What is Y Company's preferred type of debt? What rate of interest does it pay on this debt after the swap?

e)Illustrate the cash flows from this swap.Assume that X Company pays LIBOR to S Bank.

Both parties want to engage in an interest rate swap.Assume that S Bank will arrange for an interest rate swap between X Company and Y Company for 0.1%.Also,assume that X Company gets 2/3 of the interest savings available.a)Which company has a better credit rating?

b)What is the quality spread differential?

c)What is X Company's preferred type of debt? What rate of interest does it pay on this debt after the swap?

d)What is Y Company's preferred type of debt? What rate of interest does it pay on this debt after the swap?

e)Illustrate the cash flows from this swap.Assume that X Company pays LIBOR to S Bank.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 27 في هذه المجموعة.

فتح الحزمة

k this deck

26

ABC Corporation has entered into a 10-year interest rate swap with a swap bank.ABC Corp.pays the swap bank a fixed-rate of 6 percent annually on a notional amount of EUR100,000,000 and receives LIBOR - ½ percent.What is the price of the swap on the seventh reset date,assuming that the fixed-rate at which ABC can borrow has decreased to 5%.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 27 في هذه المجموعة.

فتح الحزمة

k this deck

27

Canada Corporation enters into a 2-year interest rate swap with Bank A in which it agrees to pay the swap bank a fixed-rate of 5 percent annually on a notional amount of US$1,000,000 and receive LIBOR - 1 percent.Determine the price of the swap on the first reset date,assuming that the fixed-rate at which Canada Corporation can borrow has stayed unchanged.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 27 في هذه المجموعة.

فتح الحزمة

k this deck

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 27 في هذه المجموعة.