Deck 17: Trusts

ملء الشاشة (f)

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

فتح الحزمة

قم بالتسجيل لفتح البطاقات في هذه المجموعة!

Unlock Deck

Unlock Deck

1/8

العب

ملء الشاشة (f)

Deck 17: Trusts

1

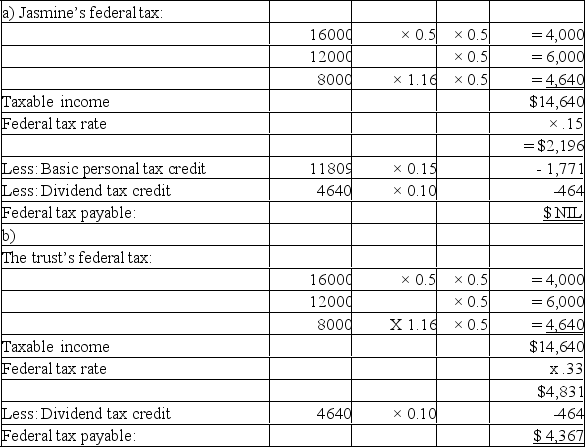

Jasmine is the beneficiary of an inter vivos trust.During 20x4 the trust received the following income:

Capital gains: $16,000

Interest: $12,000

Non-eligible dividends: $8,000

One half of the trust's income from 20x4 was paid to Jasmine,who does not currently have any other sources of income.The remainder of the income remained in the trust.

Required:

a)Determine Jasmine's personal federal tax.

b)Calculate the federal tax for the trust.

(Round all amounts to zero decimal places,and apply tax rates and rules applicable to 2018.)

Capital gains: $16,000

Interest: $12,000

Non-eligible dividends: $8,000

One half of the trust's income from 20x4 was paid to Jasmine,who does not currently have any other sources of income.The remainder of the income remained in the trust.

Required:

a)Determine Jasmine's personal federal tax.

b)Calculate the federal tax for the trust.

(Round all amounts to zero decimal places,and apply tax rates and rules applicable to 2018.)

2

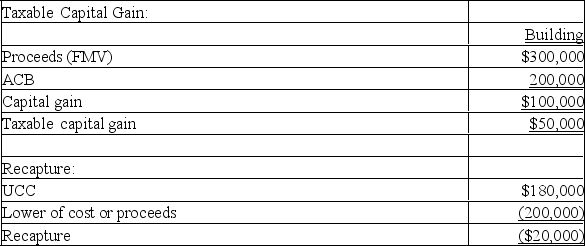

Walter passed away this year,leaving a will bequeathing his wife with $80,000 in cash,in addition to his stocks and land,to be held in a spousal trust on her behalf.The trust will pay her the annual income generated by the trust during her lifetime.

Additionally,Walter's 33 year old son,Steven,is to receive a building to be held in a trust until Steven reaches the age of 45.Steven will also receive the assets in his mother's (Walter's wife)trust upon her death.

The assets transferred to Walter's wife consist of land with an ACB of $100,000 and a FMV of $300,000,and stocks valued at $200,000 with a cost base of $150,000.

The building transferred to Steven has an ACB of $200,000,UCC of $180,000,and FMV of $300,000.

Required:

A)What are the immediate tax consequences (identify the income type and amount)to Walter? Show calculations.

B)What are the immediate tax consequences for the assets received by the trust for Walter's wife?

Additionally,Walter's 33 year old son,Steven,is to receive a building to be held in a trust until Steven reaches the age of 45.Steven will also receive the assets in his mother's (Walter's wife)trust upon her death.

The assets transferred to Walter's wife consist of land with an ACB of $100,000 and a FMV of $300,000,and stocks valued at $200,000 with a cost base of $150,000.

The building transferred to Steven has an ACB of $200,000,UCC of $180,000,and FMV of $300,000.

Required:

A)What are the immediate tax consequences (identify the income type and amount)to Walter? Show calculations.

B)What are the immediate tax consequences for the assets received by the trust for Walter's wife?

A)Walter's estate will have a taxable capital gain of $50,000 and recapture of $20,000 upon the disposal of the building bequeathed to Steven.

Building transferred to Steven's testamentary trust:

B)There will be no tax consequence on the $80,000 cash received by Walter's wife.

B)There will be no tax consequence on the $80,000 cash received by Walter's wife.

The other assets will be transferred to the testamentary spousal trust at their tax values,resulting in no immediate tax effects.

Building transferred to Steven's testamentary trust:

B)There will be no tax consequence on the $80,000 cash received by Walter's wife.The other assets will be transferred to the testamentary spousal trust at their tax values,resulting in no immediate tax effects.

3

Which of the following accurately describes one of the rules pertaining to inter vivos trusts?

A)Inter vivos trusts may use the graduated tax rate scale.

B)Inter vivos trusts are allowed the $40,000 exemption in the alternative minimum tax calculation.

C)Inter vivos trusts can deduct personal tax credits.

D)Inter vivos trusts are required to remit quarterly tax instalments.

A)Inter vivos trusts may use the graduated tax rate scale.

B)Inter vivos trusts are allowed the $40,000 exemption in the alternative minimum tax calculation.

C)Inter vivos trusts can deduct personal tax credits.

D)Inter vivos trusts are required to remit quarterly tax instalments.

D

4

A non-spousal trust account holds two buildings as its assets.Building 1 originally cost $150,000 and Building 2 originally cost $210,000.It is now the 21st anniversary of the trust,and the assets have not been transferred to the beneficiary.The undepreciated capital cost of Building 1 is $85,000 and its market value is $200,000.The undepreciated capital cost of Building 2 is $145,000 and its market value is $190,000.Which costs will be the deemed acquisition values of the buildings for the trust?

A)B1 = $150,000; B2 = $210,000

B)B1 = $85,000; B2 = $145,000

C)B1 = $200,000; B2 = $190,000

D)B1 = $200,000; B2 = $210,000

A)B1 = $150,000; B2 = $210,000

B)B1 = $85,000; B2 = $145,000

C)B1 = $200,000; B2 = $190,000

D)B1 = $200,000; B2 = $210,000

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 8 في هذه المجموعة.

فتح الحزمة

k this deck

5

If a trust qualifies as a spousal trust,which of the following is FALSE?

A)Property is deemed to have been sold at its cost amount when transferred to the trust.

B)The trust property is deemed to be sold at market value upon the death of the beneficiary (the spouse).

C)Both the spouse and any adult children may receive the capital of the trust prior to the spouse's death.

D)The 21-year rule is waived for the trust's first 21-year anniversary.

A)Property is deemed to have been sold at its cost amount when transferred to the trust.

B)The trust property is deemed to be sold at market value upon the death of the beneficiary (the spouse).

C)Both the spouse and any adult children may receive the capital of the trust prior to the spouse's death.

D)The 21-year rule is waived for the trust's first 21-year anniversary.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 8 في هذه المجموعة.

فتح الحزمة

k this deck

6

Which of the following statements is TRUE regarding trusts?

A)Losses that exceed income in a trust are allocated to the beneficiary at the end of the year.

B)From a tax perspective, there is little benefit to structuring a business as a royalty trust.

C)Income that is payable to a beneficiary cannot be deducted from the trust's income.

D)The residence of a trust is determined by the residence of the trustees.

A)Losses that exceed income in a trust are allocated to the beneficiary at the end of the year.

B)From a tax perspective, there is little benefit to structuring a business as a royalty trust.

C)Income that is payable to a beneficiary cannot be deducted from the trust's income.

D)The residence of a trust is determined by the residence of the trustees.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 8 في هذه المجموعة.

فتح الحزمة

k this deck

7

Which of the following applies to a testamentary trust that is designated as a graduated rate estate (GRE)?

A)Tax installments are required.

B)A non-calendar year may be used for tax purposes.

C)The highest rate of tax will apply to all income.

D)The GRE will become a normal testamentary trust after 48 months.

A)Tax installments are required.

B)A non-calendar year may be used for tax purposes.

C)The highest rate of tax will apply to all income.

D)The GRE will become a normal testamentary trust after 48 months.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 8 في هذه المجموعة.

فتح الحزمة

k this deck

8

Briefly answer the following questions:

With regard to non-spousal trusts:

A)What is the purpose of the 21-Year Rule?

B)What event occurs on the 21st anniversary of a trust?

C)What types of properties are subject to the 21-Year Rule?

D)How can the consequences of the 21-Year Rule be avoided?

With regard to spousal trusts:

E)What is the exception to the 21-Year Rule for spousal trusts?

With regard to non-spousal trusts:

A)What is the purpose of the 21-Year Rule?

B)What event occurs on the 21st anniversary of a trust?

C)What types of properties are subject to the 21-Year Rule?

D)How can the consequences of the 21-Year Rule be avoided?

With regard to spousal trusts:

E)What is the exception to the 21-Year Rule for spousal trusts?

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 8 في هذه المجموعة.

فتح الحزمة

k this deck

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 8 في هذه المجموعة.