Deck 19: Variables Sampling

ملء الشاشة (f)

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

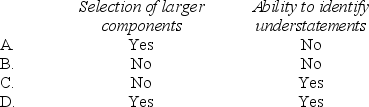

Which of the following is considered to be an advantage of monetary unit sampling compared to classical variables sampling?

سؤال

سؤال

سؤال

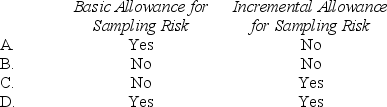

Which of the following components of the upper limit on misstatements is affected by misstatements detected during the audit examination?

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

فتح الحزمة

قم بالتسجيل لفتح البطاقات في هذه المجموعة!

Unlock Deck

Unlock Deck

1/104

العب

ملء الشاشة (f)

Deck 19: Variables Sampling

1

Incorrect rejection occurs when the auditor concludes that the account balance is __ when in fact it is _____.

A)Material; immaterial.

B)Immaterial; material.

C)Fairly stated; misstated.

D)Misstated; fairly stated.

A)Material; immaterial.

B)Immaterial; material.

C)Fairly stated; misstated.

D)Misstated; fairly stated.

D

2

Why is the auditor more concerned with controlling the exposure to the risk of incorrect acceptance than with the risk of incorrect rejection?

A)Only the risk of incorrect acceptance results in an incorrect decision by the auditor.

B)The risk of incorrect rejection is not related to the auditor's substantive procedures.

C)The risk of incorrect rejection can be controlled by performing substantive procedures during the interim period.

D)The risk of incorrect acceptance may ultimately result in the auditor incorrectly issuing an unmodified opinion on the client's financial statements.

A)Only the risk of incorrect acceptance results in an incorrect decision by the auditor.

B)The risk of incorrect rejection is not related to the auditor's substantive procedures.

C)The risk of incorrect rejection can be controlled by performing substantive procedures during the interim period.

D)The risk of incorrect acceptance may ultimately result in the auditor incorrectly issuing an unmodified opinion on the client's financial statements.

D

3

How does monetary unit sampling (MUS)ensure that larger dollar components are selected for examination?

A)MUS requires the auditor to identify all items having a balance greater than performance materiality prior to beginning the sample selection process.

B)MUS requires the auditor to stratify the sample into larger and smaller dollar components prior to beginning the sample selection process.

C)MUS defines the sampling unit as an individual dollar within an account balance or class of transactions.

D)MUS selects components having larger balances in the prior audit.

A)MUS requires the auditor to identify all items having a balance greater than performance materiality prior to beginning the sample selection process.

B)MUS requires the auditor to stratify the sample into larger and smaller dollar components prior to beginning the sample selection process.

C)MUS defines the sampling unit as an individual dollar within an account balance or class of transactions.

D)MUS selects components having larger balances in the prior audit.

C

4

An auditor may decide to increase the risk of incorrect rejection when:

A)Increased reliability from the sample is desired.

B)Many differences are expected.

C)Initial sample results do not support the planned level of control risk.

D)The cost and effort of selecting additional items is low.

A)Increased reliability from the sample is desired.

B)Many differences are expected.

C)Initial sample results do not support the planned level of control risk.

D)The cost and effort of selecting additional items is low.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 104 في هذه المجموعة.

فتح الحزمة

k this deck

5

Which of the following is true with respect to the risk of incorrect acceptance?

A)The risk of incorrect acceptance is determined in the planning stages of the audit prior to the study of internal control.

B)The risk of incorrect acceptance has an inverse relationship with sample size.

C)The risk of incorrect acceptance exposes the auditor to an efficiency loss.

D)The risk of incorrect acceptance may occur when the true (but unknown)account balance is fairly stated.

A)The risk of incorrect acceptance is determined in the planning stages of the audit prior to the study of internal control.

B)The risk of incorrect acceptance has an inverse relationship with sample size.

C)The risk of incorrect acceptance exposes the auditor to an efficiency loss.

D)The risk of incorrect acceptance may occur when the true (but unknown)account balance is fairly stated.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 104 في هذه المجموعة.

فتح الحزمة

k this deck

6

The total amount of misstatement identified in a sample is referred to as the:

A)Projected misstatement.

B)Tolerable misstatement.

C)Actual misstatement.

D)Incremental allowance for sampling risk.

A)Projected misstatement.

B)Tolerable misstatement.

C)Actual misstatement.

D)Incremental allowance for sampling risk.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 104 في هذه المجموعة.

فتح الحزمة

k this deck

7

Which of the following courses of action would an auditor most likely follow in planning a sample of cash disbursements if the auditor is aware of several unusually large cash disbursements?

A)Set the tolerable misstatement at a lower level than originally planned.

B)Stratify the cash disbursements population so that the unusually large disbursements are selected.

C)Increase the sample size to reduce the effect of the unusually large disbursements.

D)Continue to draw new samples until all the unusually large disbursements appear in the sample.

A)Set the tolerable misstatement at a lower level than originally planned.

B)Stratify the cash disbursements population so that the unusually large disbursements are selected.

C)Increase the sample size to reduce the effect of the unusually large disbursements.

D)Continue to draw new samples until all the unusually large disbursements appear in the sample.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 104 في هذه المجموعة.

فتح الحزمة

k this deck

8

How does the auditor typically determine the appropriate level of the risk of incorrect rejection when using classical variables sampling?

A)Based on prior assessments of audit risk,risk of material misstatement,and analytical procedures risk.

B)Based on the recorded amount of the account balance as well as the relationship of the account balance with important financial statement subtotals.

C)Based on the findings in prior audits or based on a small sample taken during the current year.

D)Based on the anticipated cost of conducting additional substantive procedures.

A)Based on prior assessments of audit risk,risk of material misstatement,and analytical procedures risk.

B)Based on the recorded amount of the account balance as well as the relationship of the account balance with important financial statement subtotals.

C)Based on the findings in prior audits or based on a small sample taken during the current year.

D)Based on the anticipated cost of conducting additional substantive procedures.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 104 في هذه المجموعة.

فتح الحزمة

k this deck

9

The auditor's sample would indicate that the client's account balance is fairly stated when the _____ is less than the _____.

A)Upper limit on misstatements; tolerable misstatement.

B)Actual misstatement; tolerable misstatement.

C)Tolerable misstatement; upper limit on misstatements.

D)Tolerable misstatement; actual misstatement.

A)Upper limit on misstatements; tolerable misstatement.

B)Actual misstatement; tolerable misstatement.

C)Tolerable misstatement; upper limit on misstatements.

D)Tolerable misstatement; actual misstatement.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 104 في هذه المجموعة.

فتح الحزمة

k this deck

10

The amount at which an item would be recorded assuming no mistakes in judgment or incorrect applications of generally accepted accounting principles were made is the:

A)Audited value.

B)Expected misstatement.

C)Recorded balance.

D)Tolerable misstatement.

A)Audited value.

B)Expected misstatement.

C)Recorded balance.

D)Tolerable misstatement.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 104 في هذه المجموعة.

فتح الحزمة

k this deck

11

The sampling method used to examine a population when the auditor wants to estimate a continuous amount (or value)of the population is:

A)Attributes sampling.

B)Balance sampling.

C)Discovery sampling.

D)Variables sampling.

A)Attributes sampling.

B)Balance sampling.

C)Discovery sampling.

D)Variables sampling.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 104 في هذه المجموعة.

فتح الحزمة

k this deck

12

When performing substantive procedures,auditors run the sampling risk(s)of:

A)Assessing control risk too high or too low.

B)Incorrect acceptance and incorrect rejection.

C)Assessing control risk too low only.

D)Incorrect acceptance only.

A)Assessing control risk too high or too low.

B)Incorrect acceptance and incorrect rejection.

C)Assessing control risk too low only.

D)Incorrect acceptance only.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 104 في هذه المجموعة.

فتح الحزمة

k this deck

13

Which component of the expanded audit risk model is most closely associated with the risk of incorrect acceptance?

A)Analytical procedures risk.

B)Risk of material misstatement.

C)Nonsampling risk.

D)Test of details risk.

A)Analytical procedures risk.

B)Risk of material misstatement.

C)Nonsampling risk.

D)Test of details risk.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 104 في هذه المجموعة.

فتح الحزمة

k this deck

14

When the ___ exceeds the___,the audit team is exposed to the risk of incorrect acceptance

A)Upper limit on misstatements; tolerable misstatement.

B)Tolerable misstatement; expected misstatement.

C)Tolerable misstatement; upper limit on misstatements.

D)Upper limit on misstatements; expected misstatement.

A)Upper limit on misstatements; tolerable misstatement.

B)Tolerable misstatement; expected misstatement.

C)Tolerable misstatement; upper limit on misstatements.

D)Upper limit on misstatements; expected misstatement.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 104 في هذه المجموعة.

فتح الحزمة

k this deck

15

The risk of incorrect acceptance relates to the:

A)Effectiveness of the audit.

B)Efficiency of the audit.

C)Preliminary estimate of materiality.

D)Allowable risk of tolerable misstatement.

A)Effectiveness of the audit.

B)Efficiency of the audit.

C)Preliminary estimate of materiality.

D)Allowable risk of tolerable misstatement.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 104 في هذه المجموعة.

فتح الحزمة

k this deck

16

Which of the following is not an advantage associated with monetary unit sampling (MUS)?

A)MUS methods typically include transactions or components reflecting relatively large dollar amounts.

B)MUS methods are more effective in identifying overstatement errors.

C)MUS methods provide a conservative (higher)estimate of misstatement in the account balance or class of transactions.

D)MUS methods typically result in relatively small sample sizes.

A)MUS methods typically include transactions or components reflecting relatively large dollar amounts.

B)MUS methods are more effective in identifying overstatement errors.

C)MUS methods provide a conservative (higher)estimate of misstatement in the account balance or class of transactions.

D)MUS methods typically result in relatively small sample sizes.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 104 في هذه المجموعة.

فتح الحزمة

k this deck

17

Which of the following is not true with respect to the risk of incorrect acceptance?

A)This risk provides the auditor with an efficiency loss.

B)This risk results in the auditor making an incorrect conclusion about the client's account balance or class of transactions.

C)This risk occurs when the sample results suggest that the account balance is fairly stated.

D)This risk is controlled by the auditor in determining sample size under monetary unit sampling (MUS).

A)This risk provides the auditor with an efficiency loss.

B)This risk results in the auditor making an incorrect conclusion about the client's account balance or class of transactions.

C)This risk occurs when the sample results suggest that the account balance is fairly stated.

D)This risk is controlled by the auditor in determining sample size under monetary unit sampling (MUS).

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 104 في هذه المجموعة.

فتح الحزمة

k this deck

18

Which of the following is not true with respect to the risk of incorrect rejection?

A)Incorrect rejection occurs when the auditor concludes that the account balance is not fairly stated.

B)The risk of incorrect rejection has an inverse relationship with sample size.

C)The risk of incorrect rejection exposes the auditor to an efficiency loss.

D)Incorrect rejection occurs when the true (but unknown)account balance is materially misstated.

A)Incorrect rejection occurs when the auditor concludes that the account balance is not fairly stated.

B)The risk of incorrect rejection has an inverse relationship with sample size.

C)The risk of incorrect rejection exposes the auditor to an efficiency loss.

D)Incorrect rejection occurs when the true (but unknown)account balance is materially misstated.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 104 في هذه المجموعة.

فتح الحزمة

k this deck

19

Which of the following would not be estimated using variables sampling?

A)The balance in the client's accounts receivable.

B)The extent to which an internal control procedure is not functioning as intended.

C)The amount of misstatement in a client's inventory.

D)All of the above would be estimated using variables sampling.

A)The balance in the client's accounts receivable.

B)The extent to which an internal control procedure is not functioning as intended.

C)The amount of misstatement in a client's inventory.

D)All of the above would be estimated using variables sampling.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 104 في هذه المجموعة.

فتح الحزمة

k this deck

20

Which of the following would not result in a lower level of the risk of incorrect acceptance?

A)An increase in the acceptable level of audit risk from 5 percent to 10 percent.

B)The inability of the auditor to rely on the internal control as planned.

C)An increase in the susceptibility of the account balance to misstatement.

D)A reduction in the utilization of analytical procedures in the audit examination.

A)An increase in the acceptable level of audit risk from 5 percent to 10 percent.

B)The inability of the auditor to rely on the internal control as planned.

C)An increase in the susceptibility of the account balance to misstatement.

D)A reduction in the utilization of analytical procedures in the audit examination.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 104 في هذه المجموعة.

فتح الحزمة

k this deck

21

Under monetary unit sampling,the sampling interval is determined by dividing the _____ by the _____.

A)Sample size; population size.

B)Population size; sample size.

C)Tolerable misstatement; population size.

D)Population size; tolerable misstatement.

A)Sample size; population size.

B)Population size; sample size.

C)Tolerable misstatement; population size.

D)Population size; tolerable misstatement.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 104 في هذه المجموعة.

فتح الحزمة

k this deck

22

What is the projected misstatement?

A)$5,000.

B)$10,000.

C)$15,000.

D)$30,000.

A)$5,000.

B)$10,000.

C)$15,000.

D)$30,000.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 104 في هذه المجموعة.

فتح الحزمة

k this deck

23

Using an incremental confidence factor of 1.58 (corresponding to the risk of incorrect acceptance of 10 percent),what is the incremental allowance for sampling risk?

A)$5,000.

B)$7,900.

C)$8,700.

D)$23,700.

A)$5,000.

B)$7,900.

C)$8,700.

D)$23,700.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 104 في هذه المجموعة.

فتح الحزمة

k this deck

24

Which of the following components of the upper limit on misstatements will exist in all monetary unit sampling applications,even in those where no misstatements are found?

A)Basic allowance for sampling risk.

B)Computed allowance for sampling risk.

C)Incremental allowance for sampling risk.

D)Projected misstatement.

A)Basic allowance for sampling risk.

B)Computed allowance for sampling risk.

C)Incremental allowance for sampling risk.

D)Projected misstatement.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 104 في هذه المجموعة.

فتح الحزمة

k this deck

25

Which of the following is not considered in establishing the sample size in a monetary unit sampling application?

A)Expected misstatement.

B)Population size.

C)Risk of incorrect acceptance.

D)All of the above are considered.

A)Expected misstatement.

B)Population size.

C)Risk of incorrect acceptance.

D)All of the above are considered.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 104 في هذه المجموعة.

فتح الحزمة

k this deck

26

Which of the following expresses the relationship between changes in the factors and changes in sample size in variables sampling?

A)Tolerable misstatement: Direct; Expected misstatement: Inverse; Risk of incorrect rejection: Direct

B)Tolerable misstatement: Inverse; Expected misstatement: Direct; Risk of incorrect rejection: Inverse

C)Tolerable misstatement: Inverse; Expected misstatement: Inverse; Risk of incorrect rejection: Inverse

D)Tolerable misstatement: Inverse; Expected misstatement: Inverse; Risk of incorrect rejection: Direct

A)Tolerable misstatement: Direct; Expected misstatement: Inverse; Risk of incorrect rejection: Direct

B)Tolerable misstatement: Inverse; Expected misstatement: Direct; Risk of incorrect rejection: Inverse

C)Tolerable misstatement: Inverse; Expected misstatement: Inverse; Risk of incorrect rejection: Inverse

D)Tolerable misstatement: Inverse; Expected misstatement: Inverse; Risk of incorrect rejection: Direct

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 104 في هذه المجموعة.

فتح الحزمة

k this deck

27

Which of the following factors that affect sample size can be determined by considering the recorded account balance of the account or class of transactions as well as the relationship between the recorded account balance or class of transactions with important financial statement subtotals?

A)Expected misstatement.

B)Population size.

C)Risk of incorrect acceptance.

D)Tolerable misstatement.

A)Expected misstatement.

B)Population size.

C)Risk of incorrect acceptance.

D)Tolerable misstatement.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 104 في هذه المجموعة.

فتح الحزمة

k this deck

28

Which of the following factors has a direct relationship with sample size in a variables sampling application?

A)Tolerable misstatement: Yes; Expected misstatement: Yes

B)Tolerable misstatement: No; Expected misstatement: Yes

C)Tolerable misstatement: Yes; Expected misstatement: No

D)Tolerable misstatement: No; Expected misstatement: No

A)Tolerable misstatement: Yes; Expected misstatement: Yes

B)Tolerable misstatement: No; Expected misstatement: Yes

C)Tolerable misstatement: Yes; Expected misstatement: No

D)Tolerable misstatement: No; Expected misstatement: No

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 104 في هذه المجموعة.

فتح الحزمة

k this deck

29

What is the appropriate sampling interval?

A)$60.

B)$250.

C)$500.

D)$30,000.

A)$60.

B)$250.

C)$500.

D)$30,000.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 104 في هذه المجموعة.

فتح الحزمة

k this deck

30

All other factors being equal,as the risk of incorrect acceptance and tolerable misstatement increase,the sample size will:

A)Not be affected.

B)Increase.

C)Decrease.

D)Cannot determine from the information given.

A)Not be affected.

B)Increase.

C)Decrease.

D)Cannot determine from the information given.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 104 في هذه المجموعة.

فتح الحزمة

k this deck

31

Which of the following set of conditions would provide the auditor with the smallest sample size under monetary unit sampling (RIA = risk of incorrect acceptance,EM = expected misstatement,TM = tolerable misstatement,PS = population size)?

A)RIA = 5 percent,EM = $7,500,TM = $15,000,PS = $150,000.

B)RIA = 5 percent,EM = $5,000,TM = $10,000,PS = $200,000.

C)RIA = 5 percent,EM = $2,000,TM = $10,000,PS = $100,000.

D)RIA = 5 percent,EM = $7,500,TM = $15,000,PS = $300,000.

A)RIA = 5 percent,EM = $7,500,TM = $15,000,PS = $150,000.

B)RIA = 5 percent,EM = $5,000,TM = $10,000,PS = $200,000.

C)RIA = 5 percent,EM = $2,000,TM = $10,000,PS = $100,000.

D)RIA = 5 percent,EM = $7,500,TM = $15,000,PS = $300,000.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 104 في هذه المجموعة.

فتح الحزمة

k this deck

32

A number of factors influence the sample size for a variables sampling application.All other factors held constant,which of the following would lead to a larger sample size?

A)A lower assessed level of risk of material misstatement.

B)Increased use of analytical procedures to obtain evidence about particular assertions.

C)Lower frequency and magnitude of misstatements.

D)Lower levels of tolerable misstatement.

A)A lower assessed level of risk of material misstatement.

B)Increased use of analytical procedures to obtain evidence about particular assertions.

C)Lower frequency and magnitude of misstatements.

D)Lower levels of tolerable misstatement.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 104 في هذه المجموعة.

فتح الحزمة

k this deck

33

Which of the following factors is most likely established based on the results of prior audit examinations?

A)Expected misstatement.

B)Population size.

C)Risk of incorrect acceptance.

D)Tolerable misstatement.

A)Expected misstatement.

B)Population size.

C)Risk of incorrect acceptance.

D)Tolerable misstatement.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 104 في هذه المجموعة.

فتح الحزمة

k this deck

34

What is the auditor's normal course of action if a "logical unit" is selected twice in monetary unit sampling?

A)The auditor should count the logical unit as a single selection and proceed as normal.

B)The auditor should count the logical unit as two selections and proceed as normal.

C)The auditor should not include the logical unit as a selection,since the dollar amount of this unit is excessively large.

D)The auditor should replicate the sample using an alternative random start.

A)The auditor should count the logical unit as a single selection and proceed as normal.

B)The auditor should count the logical unit as two selections and proceed as normal.

C)The auditor should not include the logical unit as a selection,since the dollar amount of this unit is excessively large.

D)The auditor should replicate the sample using an alternative random start.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 104 في هذه المجموعة.

فتح الحزمة

k this deck

35

Which of the following components of the upper limit on misstatements is determined by multiplying the sampling interval by the confidence factor for the acceptable risk of incorrect acceptance?

A)Basic allowance for sampling risk.

B)Incremental allowance for sampling risk.

C)Projected misstatement.

D)Sampling interval.

A)Basic allowance for sampling risk.

B)Incremental allowance for sampling risk.

C)Projected misstatement.

D)Sampling interval.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 104 في هذه المجموعة.

فتح الحزمة

k this deck

36

The amount by which a projected misstatement in an account balance or class of transactions differs from an actual misstatement as a result of the sample not being representative of the population would typically arise from:

A)A misunderstanding of accounting principles.

B)Sampling risk.

C)Management override of an internal control policy or procedure.

D)Risk of incorrect acceptance.

A)A misunderstanding of accounting principles.

B)Sampling risk.

C)Management override of an internal control policy or procedure.

D)Risk of incorrect acceptance.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 104 في هذه المجموعة.

فتح الحزمة

k this deck

37

How does the auditor establish the level of tolerable misstatement in a variables sampling application?

A)Based on prior assessments of audit risk,risk of material misstatement,and analytical procedures risk.

B)Based on the recorded amount of the account balance as well as the relationship of the account balance with important financial statement subtotals.

C)Based on the findings in prior audits or based on a small sample taken during the current year.

D)Based on the anticipated cost of conducting additional substantive procedures.

A)Based on prior assessments of audit risk,risk of material misstatement,and analytical procedures risk.

B)Based on the recorded amount of the account balance as well as the relationship of the account balance with important financial statement subtotals.

C)Based on the findings in prior audits or based on a small sample taken during the current year.

D)Based on the anticipated cost of conducting additional substantive procedures.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 104 في هذه المجموعة.

فتح الحزمة

k this deck

38

Brown,CPA,was using monetary unit sampling to audit an inventory of $3,000,000 that was comprised of 6,000 items.A sample size of 500 was determined and a tolerable misstatement of $20,000 was established.The sampling interval would be:

A)$500.

B)$5,000.

C)$6,000.

D)$20,000.

A)$500.

B)$5,000.

C)$6,000.

D)$20,000.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 104 في هذه المجموعة.

فتح الحزمة

k this deck

39

Which of the following is found by dividing the amount of misstatement noted in a logical unit by the recorded amount of that logical unit?

A)Sample size.

B)Sampling interval.

C)Projected misstatement.

D)Tainting percentage.

A)Sample size.

B)Sampling interval.

C)Projected misstatement.

D)Tainting percentage.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 104 في هذه المجموعة.

فتح الحزمة

k this deck

40

In a classical variables sampling application,the sample size will be smaller when the:

A)Risk of incorrect acceptance is lower.

B)Risk of incorrect rejection is lower.

C)Tolerable misstatement is lower.

D)Population variability is lower.

A)Risk of incorrect acceptance is lower.

B)Risk of incorrect rejection is lower.

C)Tolerable misstatement is lower.

D)Population variability is lower.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 104 في هذه المجموعة.

فتح الحزمة

k this deck

41

Which of the following would be the most likely situation in which an auditor would use variables sampling?

A)Comparing the recorded balance in accounts receivable to expected balances or prior-years' balances.

B)Selecting customer balances in accounts receivable for confirmation.

C)Evaluating sales invoices for evidence of authorization by client personnel.

D)Mathematically evaluating the client's provision for the allowance for doubtful accounts.

A)Comparing the recorded balance in accounts receivable to expected balances or prior-years' balances.

B)Selecting customer balances in accounts receivable for confirmation.

C)Evaluating sales invoices for evidence of authorization by client personnel.

D)Mathematically evaluating the client's provision for the allowance for doubtful accounts.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 104 في هذه المجموعة.

فتح الحزمة

k this deck

42

Jeter,CPA,performed a nonstatistical sampling plan to examine the inventory balances of Big Apple Company and estimated the account balance based on the ratio of audited value to recorded balances.He audited 200 items from a sample and found an audited value of $36,000.The sample had a recorded balance of $40,000.If the entire inventory contained 3,000 items and the total recorded balance of the inventory was $500,000,the estimated account balance using nonstatistical estimation and projecting the error based on number of items examined is:

A)$393,600.

B)$474,500.

C)$450,000.

D)$540,000.

A)$393,600.

B)$474,500.

C)$450,000.

D)$540,000.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 104 في هذه المجموعة.

فتح الحزمة

k this deck

43

_____ sampling methods use normal distribution theory and the central limit theorem to provide a range estimate of the account balance or class of transactions or the misstatement in the account balance or class of transactions.

A)Attributes.

B)Classical variables.

C)Nonstatistical.

D)Monetary unit sampling (MUS).

A)Attributes.

B)Classical variables.

C)Nonstatistical.

D)Monetary unit sampling (MUS).

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 104 في هذه المجموعة.

فتح الحزمة

k this deck

44

Summitt,CPA,performed a nonstatistical sampling plan to examine the inventory balances of Hero,Inc.Which of the following methods of sample selection are available to her?

A)Random and systematic only.

B)Block and haphazard only.

C)Any method she believes will result in a representative sample.

D)Any method where the results can be probabilistically estimated.

A)Random and systematic only.

B)Block and haphazard only.

C)Any method she believes will result in a representative sample.

D)Any method where the results can be probabilistically estimated.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 104 في هذه المجموعة.

فتح الحزمة

k this deck

45

The process of subdividing a population into more homogeneous subgroups is known as:

A)Classification.

B)Identification.

C)Sampling.

D)Stratification.

A)Classification.

B)Identification.

C)Sampling.

D)Stratification.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 104 في هذه المجموعة.

فتح الحزمة

k this deck

46

In a classical variables sampling application,if the _____ exceeds the maximum difference between the recorded balance and any point within the precision interval,the auditor would decide to _____ the account balance as fairly stated.

A)Sample estimate; accept.

B)Sample estimate; reject.

C)Tolerable misstatement; accept.

D)Tolerable misstatement; reject.

A)Sample estimate; accept.

B)Sample estimate; reject.

C)Tolerable misstatement; accept.

D)Tolerable misstatement; reject.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 104 في هذه المجموعة.

فتح الحزمة

k this deck

47

Which of the following is the least likely outcome when the upper limit on misstatements exceeds the tolerable misstatement?

A)The auditor would be exposed to the risk of incorrect rejection.

B)The auditor would be exposed to an efficiency loss.

C)The auditor would consider expanding the sample to evaluate additional transactions or components of the account balance.

D)The auditor would conclude that the account balance is fairly stated.

A)The auditor would be exposed to the risk of incorrect rejection.

B)The auditor would be exposed to an efficiency loss.

C)The auditor would consider expanding the sample to evaluate additional transactions or components of the account balance.

D)The auditor would conclude that the account balance is fairly stated.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 104 في هذه المجموعة.

فتح الحزمة

k this deck

48

When conducting variables sampling,auditors typically examine

A)Transactions of components of the account balance or class of transactions.

B)The balances in an account balance or class of transactions from one or more prior years.

C)The separation of duties among client personnel for transactions related to the account balance or class of transactions.

D)Minutes from meetings of the client's board of directors.

A)Transactions of components of the account balance or class of transactions.

B)The balances in an account balance or class of transactions from one or more prior years.

C)The separation of duties among client personnel for transactions related to the account balance or class of transactions.

D)Minutes from meetings of the client's board of directors.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 104 في هذه المجموعة.

فتح الحزمة

k this deck

49

What is one of the primary benefits of stratifying a population?

A)Stratifying the population allows different types of audit procedures to be performed on larger and smaller transactions or components.

B)Stratifying the population allows the auditor to have a higher likelihood of reaching a favorable conclusion with respect to the client's financial statements.

C)Stratifying the population allows the auditor to reduce the necessary sample size.

D)Stratifying the population reduces the auditor's exposure to nonsampling risk.

A)Stratifying the population allows different types of audit procedures to be performed on larger and smaller transactions or components.

B)Stratifying the population allows the auditor to have a higher likelihood of reaching a favorable conclusion with respect to the client's financial statements.

C)Stratifying the population allows the auditor to reduce the necessary sample size.

D)Stratifying the population reduces the auditor's exposure to nonsampling risk.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 104 في هذه المجموعة.

فتح الحزمة

k this deck

50

Pujols,CPA,performed a nonstatistical sampling plan to examine the inventory balances of Wieserbud Brewing,Inc.and estimated the account balance based on the ratio of audited value to recorded balances.He audited 120 items from a sample and found an audited value of $24,600.The sample had a recorded balance of $30,000.If the entire inventory contained 2,400 items and the total recorded balance of the inventory was $480,000,the estimated account balance using nonstatistical methods is:

A)$393,600.

B)$474,500.

C)$480,000.

D)$500,000.

A)$393,600.

B)$474,500.

C)$480,000.

D)$500,000.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 104 في هذه المجموعة.

فتح الحزمة

k this deck

51

Which of the following is considered in determining the sample size in a classical variables sampling application but not in a monetary unit sampling application?

A)Standard deviation: Yes; Risk of incorrect acceptance: Yes

B)Standard deviation: Yes; Risk of incorrect acceptance: No

C)Standard deviation: No; Risk of incorrect acceptance: Yes

D)Standard deviation: No; Risk of incorrect acceptance: No

A)Standard deviation: Yes; Risk of incorrect acceptance: Yes

B)Standard deviation: Yes; Risk of incorrect acceptance: No

C)Standard deviation: No; Risk of incorrect acceptance: Yes

D)Standard deviation: No; Risk of incorrect acceptance: No

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 104 في هذه المجموعة.

فتح الحزمة

k this deck

52

Which of the following statements is not true regarding variables sampling?

A)Two approaches to variables sampling are monetary unit sampling and classical variables sampling.

B)Both statistical and nonstatistical approaches to variables sampling can be used under GAAS.

C)The objective of variables sampling is to estimate either the true balance or the extent of misstatement in an account balance or class of transactions.

D)Variables sampling is appropriate when the distribution of the population is binary in nature.

A)Two approaches to variables sampling are monetary unit sampling and classical variables sampling.

B)Both statistical and nonstatistical approaches to variables sampling can be used under GAAS.

C)The objective of variables sampling is to estimate either the true balance or the extent of misstatement in an account balance or class of transactions.

D)Variables sampling is appropriate when the distribution of the population is binary in nature.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 104 في هذه المجموعة.

فتح الحزمة

k this deck

53

If a customer's account was recorded at $45,000,the audited value was $30,000,and the sampling interval was $30,000,the projected misstatement would be:

A)$10,000.

B)$15,000.

C)$20,000.

D)$30,000.

A)$10,000.

B)$15,000.

C)$20,000.

D)$30,000.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 104 في هذه المجموعة.

فتح الحزمة

k this deck

54

In which of the following situations would the auditor be more likely to use monetary unit sampling as opposed to classical variables sampling?

A)Larger expected misstatement: Yes; Concern with overstatements: Yes

B)Larger expected misstatement: Yes; Concern with overstatements: No

C)Larger expected misstatement: No; Concern with overstatements: Yes

D)Larger expected misstatement: No; Concern with overstatements: No

A)Larger expected misstatement: Yes; Concern with overstatements: Yes

B)Larger expected misstatement: Yes; Concern with overstatements: No

C)Larger expected misstatement: No; Concern with overstatements: Yes

D)Larger expected misstatement: No; Concern with overstatements: No

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 104 في هذه المجموعة.

فتح الحزمة

k this deck

55

Solo,CPA,performed a nonstatistical sampling plan to examine the inventory balances of Hope,Inc.and estimated the account balance by projecting the misstatement based on the number of items examined.In selecting her sample of 70 items,she used an expected misstatement of $40,000 and a tolerable misstatement of $65,000.The account balance consisted of 1,050 items totaling $1,200,000.The sample recorded balance was $80,000,and the audited value was $76,000.What conclusion did Solo draw regarding the account balance?

A)Accept because the expected misstatement is less than the tolerable misstatement.

B)Reject because the expected misstatement is greater than the expected misstatement.

C)Accept because the expected misstatement is less than the expected misstatement.

D)Reject because the expected misstatement is greater than the tolerable misstatement.

A)Accept because the expected misstatement is less than the tolerable misstatement.

B)Reject because the expected misstatement is greater than the expected misstatement.

C)Accept because the expected misstatement is less than the expected misstatement.

D)Reject because the expected misstatement is greater than the tolerable misstatement.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 104 في هذه المجموعة.

فتح الحزمة

k this deck

56

Samantha,CPA decided to stratify the population in her statistical sampling plan.Which of the following is the most likely reason she used this approach?

A)It eliminates the need for random selection.

B)The population is relatively homogenous in terms of the dollar amount of components or transactions.

C)It reduces her expected sample size.

D)It eliminates the need for calculating the projected misstatement in the account being examined.

A)It eliminates the need for random selection.

B)The population is relatively homogenous in terms of the dollar amount of components or transactions.

C)It reduces her expected sample size.

D)It eliminates the need for calculating the projected misstatement in the account being examined.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 104 في هذه المجموعة.

فتح الحزمة

k this deck

57

In which of the following circumstances would the auditor most likely use variables sampling?

A)Identifying the susceptibility of the account balance to misstatement.

B)Evaluating the operating effectiveness of specific control procedures.

C)Evaluating the operating design of specific control procedures.

D)Determining whether the client's accounts receivable balance is correctly recorded.

A)Identifying the susceptibility of the account balance to misstatement.

B)Evaluating the operating effectiveness of specific control procedures.

C)Evaluating the operating design of specific control procedures.

D)Determining whether the client's accounts receivable balance is correctly recorded.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 104 في هذه المجموعة.

فتح الحزمة

k this deck

58

An auditor discovers that an account balance believed not to be materially misstated based on an audit sample was materially misstated based on the total population of the account balance.This is an example of which of the following types of sampling risks?

A)Incorrect rejection.

B)Incorrect acceptance.

C)Assessing control risk too low.

D)Assessing control risk too high.

A)Incorrect rejection.

B)Incorrect acceptance.

C)Assessing control risk too low.

D)Assessing control risk too high.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 104 في هذه المجموعة.

فتح الحزمة

k this deck

59

The upper limit on misstatements is:

A)An adjustment of the sample estimate of misstatement to reflect the desired level of sampling risk.

B)An adjustment of the sample deviation rate to reflect the desired level of sampling risk.

C)The maximum rate of deviation that could exist before auditors would reduce the reliance on an internal control.

D)The maximum misstatement that could exist before auditors would conclude that the account balance is not fairly stated.

A)An adjustment of the sample estimate of misstatement to reflect the desired level of sampling risk.

B)An adjustment of the sample deviation rate to reflect the desired level of sampling risk.

C)The maximum rate of deviation that could exist before auditors would reduce the reliance on an internal control.

D)The maximum misstatement that could exist before auditors would conclude that the account balance is not fairly stated.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 104 في هذه المجموعة.

فتح الحزمة

k this deck

60

Green,CPA,performed a mean-per-unit sampling plan to examine the inventory balances of ABC Company.Green audited 120 items from a sample and found an audited value of $24,600.The sample had a recorded balance of $30,000.If the entire inventory contained 2,400 items and the total recorded balance of the inventory was $480,000,the estimated account balance using mean per unit estimation is:

A)$393,600.

B)$474,500.

C)$480,000.

D)$492,000.

A)$393,600.

B)$474,500.

C)$480,000.

D)$492,000.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 104 في هذه المجموعة.

فتح الحزمة

k this deck

61

A client's inventory is recorded at $600,000 and is comprised of 1,000 items.The auditors examined a sample of items with a recorded balance of $100,000 and determined an audited value of $90,000.What is the estimated audited value for inventory?

A)$90,000

B)$540,000

C)$590,000

D)$666,666

A)$90,000

B)$540,000

C)$590,000

D)$666,666

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 104 في هذه المجموعة.

فتح الحزمة

k this deck

62

Which of the following is not true with respect to the use of monetary unit sampling (MUS)?

A)MUS selects individual dollars from an account balance for verification.

B)Compared to classical variables sampling,MUS allows the auditors to more effectively control their exposure to sampling risk.

C)MUS estimates the extent of misstatement in an account balance or class of transactions.

D)MUS provides the auditor with a more conservative estimate of the misstatement than classical variables sampling.

A)MUS selects individual dollars from an account balance for verification.

B)Compared to classical variables sampling,MUS allows the auditors to more effectively control their exposure to sampling risk.

C)MUS estimates the extent of misstatement in an account balance or class of transactions.

D)MUS provides the auditor with a more conservative estimate of the misstatement than classical variables sampling.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 104 في هذه المجموعة.

فتح الحزمة

k this deck

63

Auditors are evaluating an account with a recorded balance of $500,000 using mean-per-unit estimation.This account is comprised of 1,000 individual components.The auditors sampled 100 items and determined a total audited value of $52,500.Using a risk of incorrect acceptance of 10 percent,the auditors determined a precision of $40,000.If the tolerable misstatement is $50,000,which of the following is not true?

A)The estimated recorded balance of this account is $525,000.

B)A 90 percent probability exists that the true population value falls between $460,000 and $540,000.

C)The auditors would conclude that the account balance is fairly stated.

D)The probability that the auditors will incorrectly accept a materially misstated account balance is 10 percent.

A)The estimated recorded balance of this account is $525,000.

B)A 90 percent probability exists that the true population value falls between $460,000 and $540,000.

C)The auditors would conclude that the account balance is fairly stated.

D)The probability that the auditors will incorrectly accept a materially misstated account balance is 10 percent.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 104 في هذه المجموعة.

فتح الحزمة

k this deck

64

Law,CPA is using nonstatistical sampling in his examination of Jye Company's accounts receivable.The recorded balance of Jye's accounts receivable was $750,000.Law selected a sample of customer accounts for examination,which were recorded at $50,000.Based on the responses received from accounts receivable confirmations,Law determined an audited value of $45,000 for the accounts receivable. If tolerable misstatement is $60,000,which of the following statements is not true?

A)The actual misstatement identified by Law is $5,000.

B)The estimated account balance would be $825,000.

C)Law would conclude that the account balance is not fairly stated,since the expected misstatement is greater than the tolerable misstatement.

D)Law is not able to provide a quantitative conclusion as to the exposure to the risk of incorrect acceptance.

A)The actual misstatement identified by Law is $5,000.

B)The estimated account balance would be $825,000.

C)Law would conclude that the account balance is not fairly stated,since the expected misstatement is greater than the tolerable misstatement.

D)Law is not able to provide a quantitative conclusion as to the exposure to the risk of incorrect acceptance.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 104 في هذه المجموعة.

فتح الحزمة

k this deck

65

Auditors are evaluating an account with a recorded balance of $600,000 using classical variables sampling.Based on an allowable risk of incorrect acceptance of 5 percent,the auditors have determined the following: -Estimated account balance = $680,000

-Precision = $20,000

-Tolerable misstatement = $50,000

Which of the following best describes the auditors' decision and rationale for that decision?

A)The auditors would accept the account balance as fairly stated,since the sample estimate falls outside of the precision interval.

B)The auditors would conclude that the account balance is not fairly stated,since the sample estimate falls outside of the precision interval.

C)The auditors would accept the account balance as fairly stated,since the difference between the lower bound of the precision interval and recorded balance exceeds the tolerable misstatement.

D)The auditors would conclude that the account balance is not fairly stated,since the difference between the lower bound of the precision interval and recorded balance exceeds the tolerable misstatement.

-Precision = $20,000

-Tolerable misstatement = $50,000

Which of the following best describes the auditors' decision and rationale for that decision?

A)The auditors would accept the account balance as fairly stated,since the sample estimate falls outside of the precision interval.

B)The auditors would conclude that the account balance is not fairly stated,since the sample estimate falls outside of the precision interval.

C)The auditors would accept the account balance as fairly stated,since the difference between the lower bound of the precision interval and recorded balance exceeds the tolerable misstatement.

D)The auditors would conclude that the account balance is not fairly stated,since the difference between the lower bound of the precision interval and recorded balance exceeds the tolerable misstatement.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 104 في هذه المجموعة.

فتح الحزمة

k this deck

66

As the auditors' assessments of control risk and analytical procedures risk decrease,which of the following statements is true?

A)The sample size will not be affected.

B)The allowable risk of incorrect acceptance will increase.

C)The sample size will increase.

D)The allowable risk of incorrect acceptance will decrease.

A)The sample size will not be affected.

B)The allowable risk of incorrect acceptance will increase.

C)The sample size will increase.

D)The allowable risk of incorrect acceptance will decrease.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 104 في هذه المجموعة.

فتح الحزمة

k this deck

67

A client's inventory is recorded at $300,000 and is comprised of 1,000 items.If auditors examined a sample of 200 items and found a total misstatement of $20,000 (overstatement),what is the estimated audited value for inventory?

A)$20,000

B)$100,000

C)$200,000

D)$400,000

A)$20,000

B)$100,000

C)$200,000

D)$400,000

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 104 في هذه المجموعة.

فتح الحزمة

k this deck

68

Which of the following is not a correct relationship between a factor and sample size in a monetary unit sampling application?

A)Expected misstatement; Inverse.

B)Recorded balance of the account; Direct.

C)Risk of incorrect acceptance; Inverse.

D)Tolerable misstatement; Inverse.

A)Expected misstatement; Inverse.

B)Recorded balance of the account; Direct.

C)Risk of incorrect acceptance; Inverse.

D)Tolerable misstatement; Inverse.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 104 في هذه المجموعة.

فتح الحزمة

k this deck

69

Which of the following components of the upper limit on misstatements is based on the possibility that the sampling interval contains a greater degree of misstatement than the item examined by the auditor?

A)Basic allowance for sampling risk.

B)Incremental allowance for sampling risk.

C)Projected misstatement.

D)Risk of incorrect acceptance.

A)Basic allowance for sampling risk.

B)Incremental allowance for sampling risk.

C)Projected misstatement.

D)Risk of incorrect acceptance.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 104 في هذه المجموعة.

فتح الحزمة

k this deck

70

Which of the following is considered to be an advantage of monetary unit sampling compared to classical variables sampling?

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 104 في هذه المجموعة.

فتح الحزمة

k this deck

71

SCA is auditing a client's accounts receivable balance recorded at $10 million using MUS.The following parameters have been established for this account: -Tolerable misstatement = $500,000

-Expected misstatement = $100,000

-Risk of incorrect acceptance = 10 percent

Which of the following statements would not be true with respect to the sample size in this situation?

A)The correct sample size is 69 customer accounts.

B)Decreasing tolerable misstatement from $500,000 to $200,000 (holding all other factors constant)will reduce the sample size by 331 accounts.

C)If SCA wishes to reduce its exposure to the risk of incorrect acceptance to 5 percent (holding all other factors constant),sample size will be increased by 24 accounts.

D)Increasing expected misstatement to $200,000 (holding all other factors constant)will increase the sample size to 115 customer accounts.

-Expected misstatement = $100,000

-Risk of incorrect acceptance = 10 percent

Which of the following statements would not be true with respect to the sample size in this situation?

A)The correct sample size is 69 customer accounts.

B)Decreasing tolerable misstatement from $500,000 to $200,000 (holding all other factors constant)will reduce the sample size by 331 accounts.

C)If SCA wishes to reduce its exposure to the risk of incorrect acceptance to 5 percent (holding all other factors constant),sample size will be increased by 24 accounts.

D)Increasing expected misstatement to $200,000 (holding all other factors constant)will increase the sample size to 115 customer accounts.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 104 في هذه المجموعة.

فتح الحزمة

k this deck

72

Which of the following selection methods selects individual dollars within an account balance or class of transactions for examination?

A)Attribute sampling.

B)Classical variables sampling.

C)Monetary unit sampling.

D)Nonstatistical variables sampling.

A)Attribute sampling.

B)Classical variables sampling.

C)Monetary unit sampling.

D)Nonstatistical variables sampling.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 104 في هذه المجموعة.

فتح الحزمة

k this deck

73

Which of the following components of the upper limit on misstatements is affected by misstatements detected during the audit examination?

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 104 في هذه المجموعة.

فتح الحزمة

k this deck

74

Which of the following represents a major difference in the use of monetary unit sampling (MUS)and classical variables sampling?

A)MUS is more effective in controlling the auditors' exposure to sampling risk than classical variables sampling.

B)MUS considers both the expected misstatement and tolerable misstatement in the determination of sample size,while classical variables sampling only considers the expected misstatement.

C)MUS defines the sampling unit as a dollar of an account balance while classical variables sampling defines the sampling unit as a component of an account balance.

D)MUS is a nonstatistical sampling method while classical variables sampling is a statistical sampling method.

A)MUS is more effective in controlling the auditors' exposure to sampling risk than classical variables sampling.

B)MUS considers both the expected misstatement and tolerable misstatement in the determination of sample size,while classical variables sampling only considers the expected misstatement.

C)MUS defines the sampling unit as a dollar of an account balance while classical variables sampling defines the sampling unit as a component of an account balance.

D)MUS is a nonstatistical sampling method while classical variables sampling is a statistical sampling method.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 104 في هذه المجموعة.

فتح الحزمة

k this deck

75

MES is auditing a client's accounts receivable balance recorded at $2 million using MUS.The following parameters have been established for this account: -Tolerable misstatement = $200,000

-Expected misstatement = $100,000

-Risk of incorrect acceptance = 5 percent

Which of the following statements would not be true with respect to the sample size in this situation?

A)The correct sample size is 116 customer accounts.

B)Increasing tolerable misstatement from $200,000 to $600,000 (holding all other factors constant)will increase the sample size.

C)If MES can accept a risk of incorrect acceptance of 10 percent (holding all other factors constant),sample size will be decreased to 80 accounts.

D)Because the size of the population is relatively large,this element does not affect sample size.

-Expected misstatement = $100,000

-Risk of incorrect acceptance = 5 percent

Which of the following statements would not be true with respect to the sample size in this situation?

A)The correct sample size is 116 customer accounts.

B)Increasing tolerable misstatement from $200,000 to $600,000 (holding all other factors constant)will increase the sample size.

C)If MES can accept a risk of incorrect acceptance of 10 percent (holding all other factors constant),sample size will be decreased to 80 accounts.

D)Because the size of the population is relatively large,this element does not affect sample size.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 104 في هذه المجموعة.

فتح الحزمة

k this deck

76

Auditors are evaluating an account with a recorded balance of $700,000 using classical variables sampling.Based on an allowable risk of incorrect acceptance of 10 percent,the auditors have determined the following: -Estimated account balance = $640,000

-Precision = $20,000

-Tolerable misstatement = $50,000

Which of the following best describes the auditors' decision and rationale for that decision?

A)The auditors would accept the account balance as fairly stated,since the sample estimate falls outside of the precision interval.

B)The auditors would conclude that the account balance is not fairly stated,since the sample estimate falls outside of the precision interval.

C)The auditors would accept the account balance as fairly stated,since the difference between the upper bound of the precision interval and recorded balance is less than the tolerable misstatement.

D)The auditors would conclude that the account balance is not fairly stated,since the difference between the lower bound of the precision interval and recorded balance exceeds the tolerable misstatement.

-Precision = $20,000

-Tolerable misstatement = $50,000

Which of the following best describes the auditors' decision and rationale for that decision?

A)The auditors would accept the account balance as fairly stated,since the sample estimate falls outside of the precision interval.

B)The auditors would conclude that the account balance is not fairly stated,since the sample estimate falls outside of the precision interval.

C)The auditors would accept the account balance as fairly stated,since the difference between the upper bound of the precision interval and recorded balance is less than the tolerable misstatement.

D)The auditors would conclude that the account balance is not fairly stated,since the difference between the lower bound of the precision interval and recorded balance exceeds the tolerable misstatement.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 104 في هذه المجموعة.

فتح الحزمة

k this deck

77

Zimmerman is auditing a client's accounts balance recorded at $1 million using monetary unit sampling.After assessing the appropriate parameters,Zimmerman determined an appropriate sample size of 100 items.The following two misstatements were identified as a result of the substantive tests: Assume that Zimmerman's parameters included a tolerable misstatement of $60,000 and a risk of incorrect acceptance of 5 percent.(Confidence factors for a 5 percent risk of incorrect acceptance are shown below): Which of the following is not true with respect to the above?

A)The actual misstatement detected by Zimmerman is $6,500.

B)The projected misstatement is $7,000.

C)The basic allowance for sampling risk is $30,000.

D)If the upper limit on misstatements is $46,750,Zimmerman should accept the account balance as fairly stated.

A)The actual misstatement detected by Zimmerman is $6,500.

B)The projected misstatement is $7,000.

C)The basic allowance for sampling risk is $30,000.

D)If the upper limit on misstatements is $46,750,Zimmerman should accept the account balance as fairly stated.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 104 في هذه المجموعة.

فتح الحزمة

k this deck

78

Which of the following statements is true regarding performance materiality in a monetary unit sampling application?

A)Performance materiality replaces the overall level of financial statement materiality.

B)Expected misstatement is the application of performance materiality to a particular sampling procedure.

C)Performance materiality addresses the risk that the aggregate of individually material misstatements may not cause the financial statements to be materially misstated.

D)Performance materiality provides auditors with a conservative measure that considers the presence of undetected misstatements.

A)Performance materiality replaces the overall level of financial statement materiality.

B)Expected misstatement is the application of performance materiality to a particular sampling procedure.

C)Performance materiality addresses the risk that the aggregate of individually material misstatements may not cause the financial statements to be materially misstated.

D)Performance materiality provides auditors with a conservative measure that considers the presence of undetected misstatements.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 104 في هذه المجموعة.

فتح الحزمة

k this deck

79

Allister is auditing a client's accounts balance recorded at $500,000 using monetary unit sampling and determined a sample size of 100 items.The following two misstatements were identified as a result of the substantive tests:

Confidence factors for a 5 percent risk of incorrect acceptance are shown below: What is the incremental allowance for sampling risk?

A)$3,500

B)$5,000

C)$8,500

D)$15,000

Confidence factors for a 5 percent risk of incorrect acceptance are shown below: What is the incremental allowance for sampling risk?

A)$3,500

B)$5,000

C)$8,500

D)$15,000

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 104 في هذه المجموعة.

فتح الحزمة

k this deck

80

Holding other factors constant in a classical variables sampling application,an increase in which of these factors will cause sample size to increase?

A)Risk of incorrect rejection: Yes; Risk of incorrect acceptance: No

B)Risk of incorrect rejection: No; Risk of incorrect acceptance: Yes

C)Risk of incorrect rejection: Yes; Risk of incorrect acceptance: Yes

D)Risk of incorrect rejection: No; Risk of incorrect acceptance: No

A)Risk of incorrect rejection: Yes; Risk of incorrect acceptance: No

B)Risk of incorrect rejection: No; Risk of incorrect acceptance: Yes

C)Risk of incorrect rejection: Yes; Risk of incorrect acceptance: Yes

D)Risk of incorrect rejection: No; Risk of incorrect acceptance: No

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 104 في هذه المجموعة.

فتح الحزمة

k this deck

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 104 في هذه المجموعة.