Deck 8: Interest Rate Risk I

ملء الشاشة (f)

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

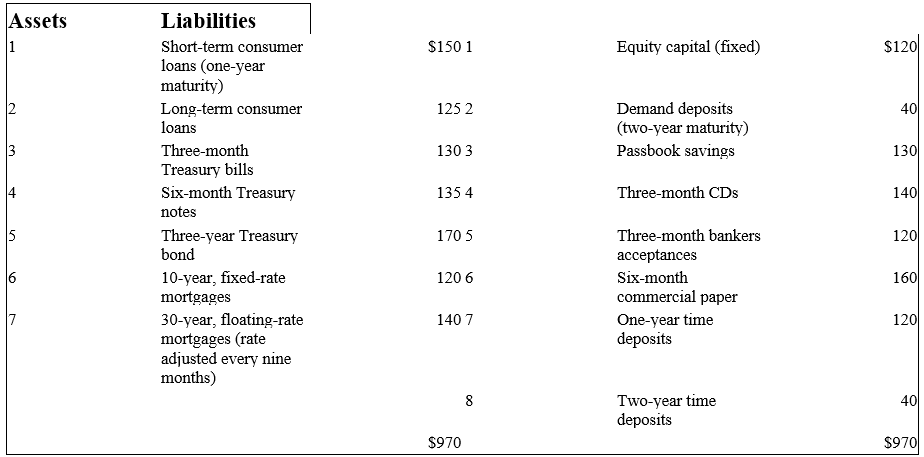

The balance sheet of XYZ Bank appears below. All figures in millions of U.S. dollars.

-Total one-year rate-sensitive assets is

A)$540 million.

B)$580 million.

C)$555 million.

D)$415 million.

-Total one-year rate-sensitive assets is

A)$540 million.

B)$580 million.

C)$555 million.

D)$415 million.

سؤال

سؤال

سؤال

سؤال

سؤال

The balance sheet of XYZ Bank appears below. All figures in millions of U.S. dollars.

-Total one-year rate-sensitive liabilities is

A)$540 million.

B)$580 million.

C)$555 million.

D)$415 million.

-Total one-year rate-sensitive liabilities is

A)$540 million.

B)$580 million.

C)$555 million.

D)$415 million.

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

فتح الحزمة

قم بالتسجيل لفتح البطاقات في هذه المجموعة!

Unlock Deck

Unlock Deck

1/124

العب

ملء الشاشة (f)

Deck 8: Interest Rate Risk I

1

The repricing model is a simplistic approach to focusing on the exposure of net interest income to changes in market levels of interest rates for given maturity periods.

True

2

One reason to exclude NOW accounts when estimating a bank's repricing gap is because the interest rates paid on these accounts typically do not change with the level of market rates.

True

3

Large banks have adopted interest rate risk measurement models based on market value accounting and duration.

True

4

When a bank's repricing gap is positive,net interest income is positively related to changes in interest rates.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 124 في هذه المجموعة.

فتح الحزمة

k this deck

5

One reason to include demand deposits when estimating a bank's repricing gap is because rising interest rates could lead to high withdrawals from these accounts.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 124 في هذه المجموعة.

فتح الحزمة

k this deck

6

All FIs tend to mismatch the maturities of their assets and liabilities to some extent.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 124 في هذه المجموعة.

فتح الحزمة

k this deck

7

The Bank for International Settlements (BISs)requires depository institutions to have interest rate risk management systems.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 124 في هذه المجموعة.

فتح الحزمة

k this deck

8

Changes in short term interest rates rarely affect the entire term structure of interest rates.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 124 في هذه المجموعة.

فتح الحزمة

k this deck

9

The repricing model estimates the difference between interest earned and interest paid during a given period of time.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 124 في هذه المجموعة.

فتح الحزمة

k this deck

10

The repricing gap model is a book value accounting based model.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 124 في هذه المجموعة.

فتح الحزمة

k this deck

11

When the Fed finds it necessary to slow economic activity,it allows interest rates to fall.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 124 في هذه المجموعة.

فتح الحزمة

k this deck

12

A bank with a negative repricing (or funding)gap faces refinancing risk.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 124 في هذه المجموعة.

فتح الحزمة

k this deck

13

In the repricing gap model,assets or liabilities are rate-sensitive within a given time period if the dollar values of each are subject to receiving a different interest rate should market rates change.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 124 في هذه المجموعة.

فتح الحزمة

k this deck

14

The cumulative repricing gap position of an FI for a given extended time period is the sum of the repricing gap values for the individual time periods that make up the extended time period.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 124 في هذه المجموعة.

فتح الحزمة

k this deck

15

Because of its complexity,small depository institutions rarely use the repricing,or funding gap,model.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 124 في هذه المجموعة.

فتح الحزمة

k this deck

16

The maturity model of measuring interest rate risk was a first attempt to include the impact on profitability of interest rate changes.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 124 في هذه المجموعة.

فتح الحزمة

k this deck

17

A positive repricing gap implies that a decrease in interest rates will cause interest expense to decrease more than the decrease in interest income.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 124 في هذه المجموعة.

فتح الحزمة

k this deck

18

The economic insolvency of many thrift institutions during the 1980s was due,at least in part,to unexpected increases in interest rates.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 124 في هذه المجموعة.

فتح الحزمة

k this deck

19

A bank with a negative repricing (or funding)gap faces reinvestment risk.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 124 في هذه المجموعة.

فتح الحزمة

k this deck

20

Because the increased level of financial market integration has increased the speed with which interest rate changes are transmitted among countries,control of U.S.interest rates by the Federal Reserve is more difficult and less certain.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 124 في هذه المجموعة.

فتح الحزمة

k this deck

21

For a given change in interest rates,the change in price for each additional year of maturity of a fixed-rate asset is smaller as the maturity increases.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 124 في هذه المجموعة.

فتح الحزمة

k this deck

22

The market value of a fixed-rate liability will increase as interest rates rise,although the market value of a fixed-rate asset will decrease as interest rates rise.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 124 في هذه المجموعة.

فتح الحزمة

k this deck

23

Runoff in demand deposits in a repricing model is typically lower during periods of falling interest rates.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 124 في هذه المجموعة.

فتح الحزمة

k this deck

24

To be more precise in measuring interest rate risk,the runoff component of long-term mortgages should be considered in the time buckets in which the maturities actually occur.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 124 في هذه المجموعة.

فتح الحزمة

k this deck

25

Defining buckets of time over wider intervals creates greater accuracy in the use of the repricing model because fewer calculations are required.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 124 في هذه المجموعة.

فتح الحزمة

k this deck

26

If the interest rate spread between rate sensitive-assets and rate sensitive liabilities increases for a bank,future increases in interest rates will lead to an increase in net interest income.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 124 في هذه المجموعة.

فتح الحزمة

k this deck

27

Few DIs consider demand deposits to be "core" or long-term sources of funds.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 124 في هذه المجموعة.

فتح الحزمة

k this deck

28

For a given change in interest rates,fixed-rate liabilities with longer-term maturities will have smaller changes in price than liabilities with shorter maturities.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 124 في هذه المجموعة.

فتح الحزمة

k this deck

29

For a given change in interest rates,fixed-rate assets with long-term maturities will have smaller changes in price than assets with shorter maturities.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 124 في هذه المجموعة.

فتح الحزمة

k this deck

30

An assumption of the repricing model is that interest rate changes will equally affect rate-sensitive assets and rate-sensitive liabilities.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 124 في هذه المجموعة.

فتح الحزمة

k this deck

31

When interest rates increase,banks are more likely to be forced to increase rate-sensitive liabilities to replace decreased balances in demand deposits and savings accounts.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 124 في هذه المجموعة.

فتح الحزمة

k this deck

32

Because the repricing model ignores the market value effect of changing interest rates,the repricing gap is an incomplete measure of the true interest rate risk exposure of an FI.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 124 في هذه المجموعة.

فتح الحزمة

k this deck

33

Defining buckets of time over a range of maturities assures the capture of all relevant information necessary to accurately assess the interest rate risk exposure of an FI.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 124 في هذه المجموعة.

فتح الحزمة

k this deck

34

The market value of a fixed-rate liability will decrease as interest rates rise,just as the market value of a fixed-rate asset will decrease as interest rates rise.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 124 في هذه المجموعة.

فتح الحزمة

k this deck

35

If the average maturity of assets is 4 years and the average maturity of liabilities is 4 years,then the FI has no interest rate risk exposure.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 124 في هذه المجموعة.

فتح الحزمة

k this deck

36

The maturity of a portfolio of assets or liabilities is a weighted average of the maturities of the assets or liabilities that comprise that portfolio.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 124 في هذه المجموعة.

فتح الحزمة

k this deck

37

The change in economic value of a fixed-rate liability for a decrease in interest rates is considered to be good news.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 124 في هذه المجموعة.

فتح الحزمة

k this deck

38

In general,the interest rate spread (spread effect)between rate-sensitive assets and rate sensitive liabilities is positively related to the change in net interest income.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 124 في هذه المجموعة.

فتح الحزمة

k this deck

39

The gap ratio is useful because it indicates the scale of the interest rate exposure by dividing the gap by the asset size of the institution.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 124 في هذه المجموعة.

فتح الحزمة

k this deck

40

Retail passbook savings accounts are included as part of rate-sensitive liabilities because the rates on these accounts rarely change.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 124 في هذه المجموعة.

فتح الحزمة

k this deck

41

Because of its simplicity,smaller depository institutions still use this model as their primary measure of interest rate risk.

A)The repricing model.

B)The maturity model.

C)The duration model.

D)The convexity model.

A)The repricing model.

B)The maturity model.

C)The duration model.

D)The convexity model.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 124 في هذه المجموعة.

فتح الحزمة

k this deck

42

The maturity gap for a bank is the weighted average maturity of the assets minus the weighted average maturity of the liabilities.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 124 في هذه المجموعة.

فتح الحزمة

k this deck

43

The spread effect demonstrates that,regardless of the direction of a change in market interest rates,a positive relation exists between the changes in spread and changes in net interest income.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 124 في هذه المجموعة.

فتح الحزمة

k this deck

44

The repricing model incorporates cash flow effects of off-balance sheet activities of DIs.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 124 في هذه المجموعة.

فتح الحزمة

k this deck

45

If interest rates decrease 50 basis points for an FI that has a gap of +$5 million,the expected change in net interest income is

A)+$2,500.

B)+$25,000.

C)+$250,000.

D)-$250,000.

E)-$25,000.

A)+$2,500.

B)+$25,000.

C)+$250,000.

D)-$250,000.

E)-$25,000.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 124 في هذه المجموعة.

فتح الحزمة

k this deck

46

A positive gap implies that an increase in interest rates will cause _______ in net interest income.

A)no change

B)a decrease

C)an increase

D)an unpredictable change

A)no change

B)a decrease

C)an increase

D)an unpredictable change

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 124 في هذه المجموعة.

فتح الحزمة

k this deck

47

If interest rates increase 75 basis points for an FI that has a gap of -$15 million,the expected change in net interest income is

A)-$112,500.

B)+$112,500.

C)+$1,125,0000.

D)-$1,125,0000.

A)-$112,500.

B)+$112,500.

C)+$1,125,0000.

D)-$1,125,0000.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 124 في هذه المجموعة.

فتح الحزمة

k this deck

48

The repricing model ignores market value effects of interest rate changes.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 124 في هذه المجموعة.

فتح الحزمة

k this deck

49

Overaggregation within maturity buckets using the repricing model causes inaccurate accounting of asset and liability cash flows and,ultimately,net interest income.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 124 في هذه المجموعة.

فتح الحزمة

k this deck

50

The gap ratio expresses the reprice gap for a given time period as a percentage of

A)equity.

B)total liabilities.

C)current liabilities.

D)total assets.

A)equity.

B)total liabilities.

C)current liabilities.

D)total assets.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 124 في هذه المجموعة.

فتح الحزمة

k this deck

51

An FI finances a $250,000 2-year fixed-rate loan with a $200,000 1-year fixed-rate CD.Use the repricing model to determine (a)the FI's repricing (or funding)gap using a 1-year maturity bucket,and (b)the impact of a 100 basis point (0.01)decrease in interest rates on the FI's annual net interest income?

A)$0;$0.

B)-$200,000;+$2,000.

C)-$200,000;-$2,000.

D)+$50,000;-$500.

A)$0;$0.

B)-$200,000;+$2,000.

C)-$200,000;-$2,000.

D)+$50,000;-$500.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 124 في هذه المجموعة.

فتح الحزمة

k this deck

52

If interest rates decrease 40 basis points (0.40 percent)for an FI that has a cumulative gap of -$25 million,the expected change in net interest income is

A)+$100,000.

B)-$100,000.

C)-$625,000.

D)-$250,000.

A)+$100,000.

B)-$100,000.

C)-$625,000.

D)-$250,000.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 124 في هذه المجموعة.

فتح الحزمة

k this deck

53

When repricing all interest-sensitive assets and all interest-sensitive liabilities in a balance sheet,the cumulative gap will be

A)zero.

B)one.

C)greater than one.

D)a negative value.

A)zero.

B)one.

C)greater than one.

D)a negative value.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 124 في هذه المجموعة.

فتح الحزمة

k this deck

54

Which of the following observations about the repricing model is correct?

A)Its information value is limited.

B)It accounts for the problem of rate-insensitive asset and liability runoffs and prepayments.

C)It accommodates cash flows from off-balance-sheet activities.

D)It helps to determine an FI's profit exposure to interest rate changes.

A)Its information value is limited.

B)It accounts for the problem of rate-insensitive asset and liability runoffs and prepayments.

C)It accommodates cash flows from off-balance-sheet activities.

D)It helps to determine an FI's profit exposure to interest rate changes.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 124 في هذه المجموعة.

فتح الحزمة

k this deck

55

An FI's net interest income reflects

A)its asset-liability structure.

B)rates of interest when the assets and liabilities were put on the books.

C)the riskiness of its loans and investments.

D)the cost of its deposit and non-deposit sources of funds.

E)All of the options.

A)its asset-liability structure.

B)rates of interest when the assets and liabilities were put on the books.

C)the riskiness of its loans and investments.

D)the cost of its deposit and non-deposit sources of funds.

E)All of the options.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 124 في هذه المجموعة.

فتح الحزمة

k this deck

56

The repricing gap approach calculates the gaps in each maturity bucket by subtracting the

A)current assets from the current liabilities.

B)long term liabilities from the fixed assets.

C)rate-sensitive assets from the total assets.

D)rate-sensitive liabilities from the rate-sensitive assets.

A)current assets from the current liabilities.

B)long term liabilities from the fixed assets.

C)rate-sensitive assets from the total assets.

D)rate-sensitive liabilities from the rate-sensitive assets.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 124 في هذه المجموعة.

فتح الحزمة

k this deck

57

The net worth of a bank is the difference between the

A)value of retained earnings and the provision for loan losses.

B)market value of assets and the market value of liabilities.

C)book value of assets and book value of liabilities.

D)rate-sensitive assets and rate-sensitive liabilities.

A)value of retained earnings and the provision for loan losses.

B)market value of assets and the market value of liabilities.

C)book value of assets and book value of liabilities.

D)rate-sensitive assets and rate-sensitive liabilities.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 124 في هذه المجموعة.

فتح الحزمة

k this deck

58

What is spread effect?

A)Periodic cash flow of interest and principal amortization payments on long-term assets that can be reinvested at market rates.

B)The effect that a change in the spread between rates on RSAs and RSLs has on net interest income as interest rates change.

C)The effect of mismatch of asset and liabilities within a maturity bucket.

D)The premium paid to compensate for the future uncertainty in a security's value.

A)Periodic cash flow of interest and principal amortization payments on long-term assets that can be reinvested at market rates.

B)The effect that a change in the spread between rates on RSAs and RSLs has on net interest income as interest rates change.

C)The effect of mismatch of asset and liabilities within a maturity bucket.

D)The premium paid to compensate for the future uncertainty in a security's value.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 124 في هذه المجموعة.

فتح الحزمة

k this deck

59

If the average maturity of assets is 5 years and the average maturity of liabilities is 7 years,then the FI has no interest rate risk exposure.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 124 في هذه المجموعة.

فتح الحزمة

k this deck

60

The repricing gap does not accurately measure FI interest rate risk exposure because

A)FIs cannot accurately predict the magnitude change in future interest rates.

B)FIs cannot accurately predict the direction of change in future interest rates.

C)accounting systems are not accurate enough to allow the calculation of precise gap measures.

D)it does not recognize timing differences in cash flows within the same maturity grouping.

A)FIs cannot accurately predict the magnitude change in future interest rates.

B)FIs cannot accurately predict the direction of change in future interest rates.

C)accounting systems are not accurate enough to allow the calculation of precise gap measures.

D)it does not recognize timing differences in cash flows within the same maturity grouping.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 124 في هذه المجموعة.

فتح الحزمة

k this deck

61

Which of the following statements is true?

A)An increase in interest rates leads to an increase in the market value of financial securities.

B)Value of longer term securities decreases at a diminishing rate for increases in interest rates.

C)Value of longer term securities increases at an increasing rate for any decline in interest rates.

D)The shorter the maturity of a fixed income asset or liability,the greater the fall in market value for any given interest rate increase.

A)An increase in interest rates leads to an increase in the market value of financial securities.

B)Value of longer term securities decreases at a diminishing rate for increases in interest rates.

C)Value of longer term securities increases at an increasing rate for any decline in interest rates.

D)The shorter the maturity of a fixed income asset or liability,the greater the fall in market value for any given interest rate increase.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 124 في هذه المجموعة.

فتح الحزمة

k this deck

62

Which of the following relationships does NOT hold in the pricing of fixed-rate assets given changes in market rate?

A)A decrease in interest rates generally leads to an increase in the value of assets.

B)Longer maturity assets have greater changes in price than shorter maturity assets for given changes in interest rates.

C)The absolute change in price per unit of maturity time for given changes in interest rates decreases over time,although the relative changes actually increase.

D)For a given percentage decrease in interest rates,assets will increase in price more than they will decrease in price for the same,but opposite increase in rates.

A)A decrease in interest rates generally leads to an increase in the value of assets.

B)Longer maturity assets have greater changes in price than shorter maturity assets for given changes in interest rates.

C)The absolute change in price per unit of maturity time for given changes in interest rates decreases over time,although the relative changes actually increase.

D)For a given percentage decrease in interest rates,assets will increase in price more than they will decrease in price for the same,but opposite increase in rates.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 124 في هذه المجموعة.

فتح الحزمة

k this deck

63

The average maturity of the liabilities of an FI's balance sheet is equal to

A)the weighted-average of the liabilities where the weights are determined relative to the total liabilities and equity of the FI.

B)the weighted-average of the liabilities where the weights are determined relative to the total liabilities of the FI.

C)the weighted-average of the liabilities where the weights are determined relative to the total assets of the FI.

D)the weighted-average of the liabilities where the weights are determined using market values of liabilities.

A)the weighted-average of the liabilities where the weights are determined relative to the total liabilities and equity of the FI.

B)the weighted-average of the liabilities where the weights are determined relative to the total liabilities of the FI.

C)the weighted-average of the liabilities where the weights are determined relative to the total assets of the FI.

D)the weighted-average of the liabilities where the weights are determined using market values of liabilities.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 124 في هذه المجموعة.

فتح الحزمة

k this deck

64

Can an FI immunize itself against interest rate risk exposure even though its maturity gap is not zero?

A)Yes,because with a maturity gap of zero the change in the market value of assets exactly offsets the change in the market value of liabilities.

B)No,because with a maturity gap of zero the change in the market value of assets exactly offsets the change in the market value of liabilities.

C)Yes,because the maturity model does not consider the timing of cash flows.

D)No,because the timing of cash flows is relevant to immunization against interest rate risk exposure.

A)Yes,because with a maturity gap of zero the change in the market value of assets exactly offsets the change in the market value of liabilities.

B)No,because with a maturity gap of zero the change in the market value of assets exactly offsets the change in the market value of liabilities.

C)Yes,because the maturity model does not consider the timing of cash flows.

D)No,because the timing of cash flows is relevant to immunization against interest rate risk exposure.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 124 في هذه المجموعة.

فتح الحزمة

k this deck

65

A method of measuring the interest rate or gap exposure of an FI is

A)the duration model.

B)the maturity model.

C)the repricing model.

D)the funding gap model.

E)All of the options.

A)the duration model.

B)the maturity model.

C)the repricing model.

D)the funding gap model.

E)All of the options.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 124 في هذه المجموعة.

فتح الحزمة

k this deck

66

If the chosen maturity buckets have a time period that is too long,the repricing model may produce inaccurate results because

A)as the time to maturity increases,the price volatility increases.

B)price changes will be overestimated.

C)there may be large differentials in the time to repricing for different securities within each maturity bucket.

D)the FI will be unable to accurately measure the quantity of rate-sensitive assets.

A)as the time to maturity increases,the price volatility increases.

B)price changes will be overestimated.

C)there may be large differentials in the time to repricing for different securities within each maturity bucket.

D)the FI will be unable to accurately measure the quantity of rate-sensitive assets.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 124 في هذه المجموعة.

فتح الحزمة

k this deck

67

The repricing model is based on an accounting world that reports asset and liability values at

A)their market value.

B)their book value.

C)their historic values or costs.

D)their current value or cost.

E)their book value and their historic values or costs.

A)their market value.

B)their book value.

C)their historic values or costs.

D)their current value or cost.

E)their book value and their historic values or costs.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 124 في هذه المجموعة.

فتح الحزمة

k this deck

68

The balance sheet of XYZ Bank appears below. All figures in millions of U.S. dollars.

-Total one-year rate-sensitive assets is

A)$540 million.

B)$580 million.

C)$555 million.

D)$415 million.

-Total one-year rate-sensitive assets is

A)$540 million.

B)$580 million.

C)$555 million.

D)$415 million.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 124 في هذه المجموعة.

فتح الحزمة

k this deck

69

A bank that finances long-term fixed-rate mortgages with short-term deposits is exposed to

A)increases in net interest income and decreases in the market value of equity when interest rates fall.

B)decreases in net interest income and decreases in the market value of equity when interest rates fall.

C)decreases in net interest income and increases in the market value of equity when interest rates increase.

D)increases in net interest income and increases in the market value of equity when interest rates increase.

E)decreases in net interest income and decreases in the market value of equity when interest rates increase.

A)increases in net interest income and decreases in the market value of equity when interest rates fall.

B)decreases in net interest income and decreases in the market value of equity when interest rates fall.

C)decreases in net interest income and increases in the market value of equity when interest rates increase.

D)increases in net interest income and increases in the market value of equity when interest rates increase.

E)decreases in net interest income and decreases in the market value of equity when interest rates increase.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 124 في هذه المجموعة.

فتح الحزمة

k this deck

70

If an FI's repricing gap is less than zero,then

A)it is deficient in its required reserves.

B)it is deficient in its capital ratio requirement.

C)its liability costs are more sensitive to changing market interest rates than are its asset yields.

D)its liability costs are less sensitive to changing market interest rates than are its asset yields.

A)it is deficient in its required reserves.

B)it is deficient in its capital ratio requirement.

C)its liability costs are more sensitive to changing market interest rates than are its asset yields.

D)its liability costs are less sensitive to changing market interest rates than are its asset yields.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 124 في هذه المجموعة.

فتح الحزمة

k this deck

71

Which of the following is a weakness of the repricing model to measure interest rate risk?

A)Potential for overaggregation of assets and liabilities within each maturity bucket.

B)It ignores how changes in interest rates affect the market value of assets and liabilities.

C)It ignores the reinvestment of loan interest and principal payments that are reinvested at current market rates.

D)It fails to recognize off-balance-sheet activities that may be rate-sensitive.

E)All of the options.

A)Potential for overaggregation of assets and liabilities within each maturity bucket.

B)It ignores how changes in interest rates affect the market value of assets and liabilities.

C)It ignores the reinvestment of loan interest and principal payments that are reinvested at current market rates.

D)It fails to recognize off-balance-sheet activities that may be rate-sensitive.

E)All of the options.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 124 في هذه المجموعة.

فتح الحزمة

k this deck

72

Of the following institutions,which will be subject to refinancing risk within a particular reprice bucket?

A)the market value of rate-sensitive liabilities is less than the market value of equity.

B)the book value of rate-sensitive assets is greater than the book value of rate-sensitive liabilities.

C)the market value of rate-sensitive assets is less than the market value of rate-sensitive liabilities.

D)the book value of rate-sensitive liabilities is greater than the book value of rate-sensitive assets.

A)the market value of rate-sensitive liabilities is less than the market value of equity.

B)the book value of rate-sensitive assets is greater than the book value of rate-sensitive liabilities.

C)the market value of rate-sensitive assets is less than the market value of rate-sensitive liabilities.

D)the book value of rate-sensitive liabilities is greater than the book value of rate-sensitive assets.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 124 في هذه المجموعة.

فتح الحزمة

k this deck

73

The balance sheet of XYZ Bank appears below. All figures in millions of U.S. dollars.

-Total one-year rate-sensitive liabilities is

A)$540 million.

B)$580 million.

C)$555 million.

D)$415 million.

-Total one-year rate-sensitive liabilities is

A)$540 million.

B)$580 million.

C)$555 million.

D)$415 million.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 124 في هذه المجموعة.

فتح الحزمة

k this deck

74

Of the following institutions,which will be subject to reinvestment risk within a particular reprice bucket?

A)the market value of rate-sensitive liabilities is less than the market value of equity.

B)the book value of rate sensitive assets is greater than the book value of rate-sensitive liabilities.

C)the market value of rate-sensitive assets is less than the market value of rate-sensitive liabilities.

D)the book value of rate-sensitive liabilities is greater than the book value of rate-sensitive assets.

A)the market value of rate-sensitive liabilities is less than the market value of equity.

B)the book value of rate sensitive assets is greater than the book value of rate-sensitive liabilities.

C)the market value of rate-sensitive assets is less than the market value of rate-sensitive liabilities.

D)the book value of rate-sensitive liabilities is greater than the book value of rate-sensitive assets.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 124 في هذه المجموعة.

فتح الحزمة

k this deck

75

The repricing model measures the impact of unanticipated changes in interest rates on

A)the market value of equity.

B)net interest income.

C)both market value of equity and net interest income.

D)the FI's capital position.

A)the market value of equity.

B)net interest income.

C)both market value of equity and net interest income.

D)the FI's capital position.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 124 في هذه المجموعة.

فتح الحزمة

k this deck

76

Which of the following indicates a positive gap according to the repricing model?

A)the book value of rate-sensitive liabilities is less than the book value of rate-sensitive assets.

B)the book value of rate-sensitive assets is less than the book value of rate-sensitive liabilities.

C)the market value of rate-sensitive assets is less than the market value of rate-sensitive liabilities.

D)the book value of rate-sensitive liabilities is greater than the book value of rate-sensitive assets.

A)the book value of rate-sensitive liabilities is less than the book value of rate-sensitive assets.

B)the book value of rate-sensitive assets is less than the book value of rate-sensitive liabilities.

C)the market value of rate-sensitive assets is less than the market value of rate-sensitive liabilities.

D)the book value of rate-sensitive liabilities is greater than the book value of rate-sensitive assets.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 124 في هذه المجموعة.

فتح الحزمة

k this deck

77

Which of the following describes the condition known as runoff in the repricing model approach to measuring interest rate risk of an FI?

A)Periodic cash flow of interest and principal amortization payments on long-term assets that can be reinvested at market rates.

B)The effect that a change in the spread between rates on RSAs and RSLs has on net interest income as interest rates change.

C)Mismatch of asset and liabilities within a maturity bucket.

D)The relations between changes in interest rates and changes in net interest income.

A)Periodic cash flow of interest and principal amortization payments on long-term assets that can be reinvested at market rates.

B)The effect that a change in the spread between rates on RSAs and RSLs has on net interest income as interest rates change.

C)Mismatch of asset and liabilities within a maturity bucket.

D)The relations between changes in interest rates and changes in net interest income.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 124 في هذه المجموعة.

فتح الحزمة

k this deck

78

An interest rate increase

A)benefits the FI by increasing the market value of the FI's liabilities.

B)harms the FI by increasing the market value of the FI's liabilities.

C)harms the FI by decreasing the market value of the FI's liabilities.

D)benefits the FI by decreasing the market value of the FI's liabilities.

A)benefits the FI by increasing the market value of the FI's liabilities.

B)harms the FI by increasing the market value of the FI's liabilities.

C)harms the FI by decreasing the market value of the FI's liabilities.

D)benefits the FI by decreasing the market value of the FI's liabilities.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 124 في هذه المجموعة.

فتح الحزمة

k this deck

79

The repricing model ignores information regarding the distribution of assets and liabilities within maturity buckets.This limitation of the model refers to

A)market value effect.

B)overaggregation.

C)runoffs and pre-payments.

D)OBS activities.

A)market value effect.

B)overaggregation.

C)runoffs and pre-payments.

D)OBS activities.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 124 في هذه المجموعة.

فتح الحزمة

k this deck

80

An increase in interest rates

A)increases the market value of the FI's financial assets and liabilities.

B)decreases the market value of the FI's financial assets and liabilities.

C)decreases the book value of the FI's financial assets and liabilities.

D)increases the book value of the FI's financial assets and liabilities.

A)increases the market value of the FI's financial assets and liabilities.

B)decreases the market value of the FI's financial assets and liabilities.

C)decreases the book value of the FI's financial assets and liabilities.

D)increases the book value of the FI's financial assets and liabilities.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 124 في هذه المجموعة.

فتح الحزمة

k this deck

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 124 في هذه المجموعة.