Deck 13: Jurisdictional Issues in Business Taxation

ملء الشاشة (f)

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

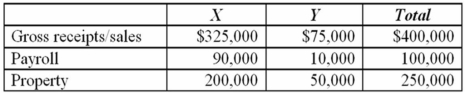

Cambridge, Inc. conducts business in states X and Y. This year, its before-tax income was $150,000. Below is information regarding its sales, payroll, and property factors in both states.  Both states apply an equally-weighted three-factor formula to apportion income. State X has a 10% corporate income tax and state Y has a 5% corporate income tax. Compute the state tax savings if Cambridge could relocate $100,000 of property and $50,000 of payroll from state X to state Y.

Both states apply an equally-weighted three-factor formula to apportion income. State X has a 10% corporate income tax and state Y has a 5% corporate income tax. Compute the state tax savings if Cambridge could relocate $100,000 of property and $50,000 of payroll from state X to state Y.

A)$2,250

B)$12,563

C)$11,532

D)$9,094

Both states apply an equally-weighted three-factor formula to apportion income. State X has a 10% corporate income tax and state Y has a 5% corporate income tax. Compute the state tax savings if Cambridge could relocate $100,000 of property and $50,000 of payroll from state X to state Y.A)$2,250

B)$12,563

C)$11,532

D)$9,094

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

Tri-State's, Inc. operates in Arkansas, Oklahoma, and Kansas. Assume that each state has adopted the UDITPA formula. During the corporation's tax year ended December 31, the apportionment data indicated:  Which of the following statements is true?

Which of the following statements is true?

A)The sales factor for Arkansas is approximately 35%.

B)Arkansas payroll percentage is approximately 11.1%.

C)The property factor for Arkansas is approximately 7.14%.

D)All of the above factors for Arkansas are correct.

Which of the following statements is true?A)The sales factor for Arkansas is approximately 35%.

B)Arkansas payroll percentage is approximately 11.1%.

C)The property factor for Arkansas is approximately 7.14%.

D)All of the above factors for Arkansas are correct.

سؤال

Tri-State's, Inc. operates in Arkansas, Oklahoma, and Kansas. Assume that each state has adopted the UDITPA formula. During the corporation's tax year ended December 31, the apportionment data indicated:  Tri-State's income for the current year is $250,000. Approximately how much income will be taxed by Oklahoma?

Tri-State's income for the current year is $250,000. Approximately how much income will be taxed by Oklahoma?

A)$250,000

B)$218,125

C)$44,375

D)$173,750

Tri-State's income for the current year is $250,000. Approximately how much income will be taxed by Oklahoma?A)$250,000

B)$218,125

C)$44,375

D)$173,750

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

Tri-State's, Inc. operates in Arkansas, Oklahoma, and Kansas. Assume that each state has adopted the UDITPA formula. During the corporation's tax year ended December 31, the apportionment data indicated:  Tri-State's income for the current year is $250,000. Approximately how much will be taxed by Kansas?

Tri-State's income for the current year is $250,000. Approximately how much will be taxed by Kansas?

A)$83,000

B)$95,000

C)$32,000

D)$170,000

Tri-State's income for the current year is $250,000. Approximately how much will be taxed by Kansas?A)$83,000

B)$95,000

C)$32,000

D)$170,000

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

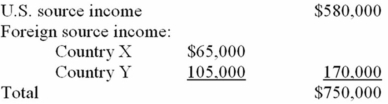

Pennworth Corporation operates in the United States and foreign country M. Its domestic subsidiary Delco, Inc. operates in foreign country N. This year, the two corporations report the following.  If Pennworth and Delco file a consolidated U.S. tax return, compute consolidated income tax liability.

If Pennworth and Delco file a consolidated U.S. tax return, compute consolidated income tax liability.

A)$1,200,000

B)$1,260,000

C)$1,700,000

D)$1,020,000

If Pennworth and Delco file a consolidated U.S. tax return, compute consolidated income tax liability.A)$1,200,000

B)$1,260,000

C)$1,700,000

D)$1,020,000

سؤال

سؤال

سؤال

Many Mountains, Inc. is a U.S. multinational corporation. This year, it had the following income.  Many Mountains paid $15,000 income tax to Country X and $28,500 income tax to Country Y. Compute Many Mountains' allowable foreign tax credit.

Many Mountains paid $15,000 income tax to Country X and $28,500 income tax to Country Y. Compute Many Mountains' allowable foreign tax credit.

A)$57,800

B)$49,550

C)$43,500

D)$49,650

Many Mountains paid $15,000 income tax to Country X and $28,500 income tax to Country Y. Compute Many Mountains' allowable foreign tax credit.A)$57,800

B)$49,550

C)$43,500

D)$49,650

سؤال

San Carlos Corporation, a U.S. multinational, had pretax U.S. source income and foreign source income as follows.  San Carlos paid $100,000 income tax to Country W. Calculate San Carlos' tax savings if it takes a foreign tax credit rather than deducting this tax.

San Carlos paid $100,000 income tax to Country W. Calculate San Carlos' tax savings if it takes a foreign tax credit rather than deducting this tax.

A)$100,000

B)$66,000

C)$34,000

D)$0

San Carlos paid $100,000 income tax to Country W. Calculate San Carlos' tax savings if it takes a foreign tax credit rather than deducting this tax.A)$100,000

B)$66,000

C)$34,000

D)$0

سؤال

سؤال

Fleming Corporation, a U.S. multinational, has pretax U.S. source income and foreign source income as follows.  Fleming paid $200,000 income tax to CountryA. If Fleming takes the foreign tax credit, compute its worldwide tax burden as a percentage of its pretax income.

Fleming paid $200,000 income tax to CountryA. If Fleming takes the foreign tax credit, compute its worldwide tax burden as a percentage of its pretax income.

A)34%

B)35%

C)36%

D)44%

Fleming paid $200,000 income tax to CountryA. If Fleming takes the foreign tax credit, compute its worldwide tax burden as a percentage of its pretax income.A)34%

B)35%

C)36%

D)44%

سؤال

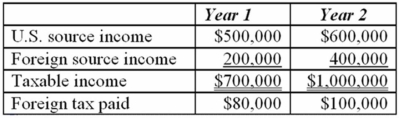

Jenkin Corporation reported the following for its first two taxable years.  Calculate Jenkin's U.S. tax liability for Year 2.

Calculate Jenkin's U.S. tax liability for Year 2.

A)$340,000

B)$240,000

C)$228,000

D)$204,000

Calculate Jenkin's U.S. tax liability for Year 2.A)$340,000

B)$240,000

C)$228,000

D)$204,000

سؤال

سؤال

World Sales, Inc., a U.S. multinational, had pretax U.S. source income and foreign source income as follows.  World Sales paid $50,000 income taxes to Country O. What is World Sale's U.S. tax liability if it deducts the foreign taxes paid?

World Sales paid $50,000 income taxes to Country O. What is World Sale's U.S. tax liability if it deducts the foreign taxes paid?

A)$213,000

B)$204,000

C)$221,000

D)$238,000

World Sales paid $50,000 income taxes to Country O. What is World Sale's U.S. tax liability if it deducts the foreign taxes paid?A)$213,000

B)$204,000

C)$221,000

D)$238,000

سؤال

Fleming Corporation, a U.S. multinational, has pretax U.S. source income and foreign source income as follows.  Fleming paid $50,000 income tax to Country A. If Fleming takes the foreign tax credit, compute its worldwide tax burden as a percentage of its pretax income.

Fleming paid $50,000 income tax to Country A. If Fleming takes the foreign tax credit, compute its worldwide tax burden as a percentage of its pretax income.

A)34%

B)35%

C)44%

D)45%

Fleming paid $50,000 income tax to Country A. If Fleming takes the foreign tax credit, compute its worldwide tax burden as a percentage of its pretax income.A)34%

B)35%

C)44%

D)45%

سؤال

سؤال

Mega, Inc., a U.S. multinational, has pretax U.S. source income and foreign source income as follows.  Mega paid $20,000 income tax to Country M. Mega has a $25,000 foreign tax credit carryforward. What is Mega's U.S. tax liability if it takes the foreign tax credit?

Mega paid $20,000 income tax to Country M. Mega has a $25,000 foreign tax credit carryforward. What is Mega's U.S. tax liability if it takes the foreign tax credit?

A)$265,600

B)$240,600

C)$285,600

D)$258,400

Mega paid $20,000 income tax to Country M. Mega has a $25,000 foreign tax credit carryforward. What is Mega's U.S. tax liability if it takes the foreign tax credit?A)$265,600

B)$240,600

C)$285,600

D)$258,400

سؤال

سؤال

سؤال

Global Corporation, a U.S. multinational, began operations this year. Global had pretax U.S. source income and foreign source income as follows.  Global paid $25,000 income tax to Country X. What is Global's U.S. tax liability if it takes the foreign tax credit?

Global paid $25,000 income tax to Country X. What is Global's U.S. tax liability if it takes the foreign tax credit?

A)$247,000

B)$238,000

C)$222,000

D)$272,000

Global paid $25,000 income tax to Country X. What is Global's U.S. tax liability if it takes the foreign tax credit?A)$247,000

B)$238,000

C)$222,000

D)$272,000

سؤال

سؤال

سؤال

Jokar Inc., a U.S. multinational, began operations this year. Jokar had pretax U.S. source income and foreign source income as follows.  Jokar paid $50,000 income tax to Country O. Compute Jokar's U.S. tax liability if it takes the foreign tax credit.

Jokar paid $50,000 income tax to Country O. Compute Jokar's U.S. tax liability if it takes the foreign tax credit.

A)$213,000

B)$221,000

C)$204,000

D)$238,000

Jokar paid $50,000 income tax to Country O. Compute Jokar's U.S. tax liability if it takes the foreign tax credit.A)$213,000

B)$221,000

C)$204,000

D)$238,000

سؤال

فتح الحزمة

قم بالتسجيل لفتح البطاقات في هذه المجموعة!

Unlock Deck

Unlock Deck

1/102

العب

ملء الشاشة (f)

Deck 13: Jurisdictional Issues in Business Taxation

1

If Gamma Inc. is incorporated in Ohio and has its commercial domicile in Cleveland, the state of Ohio has jurisdiction to tax 100% of Gamma's business income.

False

2

In the United States, corporations are subject only to taxes imposed by the federal government.

False

3

Article 1 of the U.S. Constitution, referred to as the commerce clause, prohibits state governments from using a tax to discriminate against interstate commerce.

True

4

Article 1 of the U.S. Constitution, referred to as the commerce clause, prohibits a state from charging an extra 10 cent tax per gallon on gasoline sold to trucks with out-of-state license plates.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 102 في هذه المجموعة.

فتح الحزمة

k this deck

5

International tax treaties generally allow a government to tax a non-resident firm that maintains a permanent residence in the treaty country.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 102 في هذه المجموعة.

فتح الحزمة

k this deck

6

The UDITPA formula for state income tax apportionment consists of three factors: sales, payroll, and profit.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 102 في هذه المجموعة.

فتح الحزمة

k this deck

7

The payroll factor in the UDITPA state income tax apportionment formula always includes executive compensation.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 102 في هذه المجموعة.

فتح الحزمة

k this deck

8

A corporation is usually subject to tax by any state in which it engages in any business transactions.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 102 في هذه المجموعة.

فتح الحزمة

k this deck

9

The federal income tax deduction allowed for state income taxes paid decreases the cost of the state taxes.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 102 في هذه المجموعة.

فتح الحزمة

k this deck

10

Luttrix Inc. does business in Nebraska (6% tax rate) and Colorado (3% tax rate). All other factors being equal, Luttrix will reduce state taxes if it constructs a new manufacturing plant in Colorado.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 102 في هذه المجموعة.

فتح الحزمة

k this deck

11

According to Public Law 86-272, the sale of tangible goods to residents of a state is not sufficient to establish nexus in that state.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 102 في هذه المجموعة.

فتح الحزمة

k this deck

12

All states assessing an income tax use the same formula for apportionment purposes.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 102 في هذه المجموعة.

فتح الحزمة

k this deck

13

If a corporation with a 35% marginal federal income tax rate pays $20,000 state income tax, the after-tax cost of the state tax is $13,000.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 102 في هذه المجموعة.

فتح الحزمة

k this deck

14

Multi-State, Inc. does business in two states. Its apportionment percentage in state A is 63%. Its apportionment percentage in the other state can be no more than 37%.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 102 في هذه المجموعة.

فتح الحزمة

k this deck

15

BiState Inc. conducts business in North Carolina and South Carolina. If BiState's apportionment percentage in North Carolina is 63%, its apportionment percentage in South Carolina can be no more than 37%.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 102 في هذه المجموعة.

فتح الحزمة

k this deck

16

The UDITPA formula for apportioning income among states is based on four equally weighted factors.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 102 في هذه المجموعة.

فتح الحزمة

k this deck

17

Non-resident firms selling tangible goods to in-state residents can use P.L. 86-272 to avoid having income tax nexus in a state.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 102 في هذه المجموعة.

فتح الحزمة

k this deck

18

Supplies, Inc. does business in Georgia (6% tax rate) and Alabama (5% tax rate). All other factors being equal, the company will reduce state taxes if it increases the compensation paid to its employees in Alabama.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 102 في هذه المجموعة.

فتح الحزمة

k this deck

19

The sales factor in the UDITPA state income tax apportionment formula equals out-of-state sales divided by total sales.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 102 في هذه المجموعة.

فتح الحزمة

k this deck

20

The sales factor in the UDITPA state income tax apportionment formula equals in-state sales divided by total sales.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 102 في هذه المجموعة.

فتح الحزمة

k this deck

21

A foreign branch operation of a U.S. corporation is not a separate legal entity.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 102 في هذه المجموعة.

فتح الحزمة

k this deck

22

Cross-crediting allows multinational corporations to use excess credits generated in low- tax jurisdictions to offset excess limitations generated in high-tax jurisdictions.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 102 في هذه المجموعة.

فتح الحزمة

k this deck

23

Excess foreign tax credits can only be carried to future tax years.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 102 في هذه المجموعة.

فتح الحزمة

k this deck

24

A bilateral agreement between the governments of England and France defining and limiting each party's respective tax jurisdiction is an example of a tax treaty.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 102 في هذه المجموعة.

فتح الحزمة

k this deck

25

A U.S. taxpayer can make an annual election to take a credit or a deduction for foreign income taxes paid.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 102 في هذه المجموعة.

فتح الحزمة

k this deck

26

The foreign tax credit can reduce a corporation's alternative minimum tax.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 102 في هذه المجموعة.

فتح الحزمة

k this deck

27

The term "tax haven" refers to a foreign country that imposes an income tax at a rate higher than the U.S. rate.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 102 في هذه المجموعة.

فتح الحزمة

k this deck

28

The United States has jurisdiction to tax income earned by any foreign corporation that is a controlled subsidiary of a U.S. parent corporation.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 102 في هذه المجموعة.

فتح الحزمة

k this deck

29

The foreign tax credit is available for both income and property taxes paid to a foreign jurisdiction.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 102 في هذه المجموعة.

فتح الحزمة

k this deck

30

The foreign tax credit is available for income taxes paid to a foreign country.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 102 في هذه المجموعة.

فتح الحزمة

k this deck

31

The foreign subsidiaries of a U.S. corporation cannot be included in a U.S. consolidated tax return.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 102 في هذه المجموعة.

فتح الحزمة

k this deck

32

Under the U.S. tax system, a domestic corporation pays U.S. tax only on the portion of its business income earned in the United States.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 102 في هذه المجموعة.

فتح الحزمة

k this deck

33

The United States taxes its citizens on their worldwide incomes.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 102 في هذه المجموعة.

فتح الحزمة

k this deck

34

Foreign value-added taxes and excise taxes are eligible for the U.S. foreign tax credit.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 102 في هذه المجموعة.

فتح الحزمة

k this deck

35

The deemed paid foreign tax credit is available only to U.S. corporations that own 30% or more of the voting stock of a foreign corporation that paid dividends during the taxable year.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 102 في هذه المجموعة.

فتح الحزمة

k this deck

36

A foreign source dividend received by a U.S. corporation is eligible for the 70% dividends-received deduction.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 102 في هذه المجموعة.

فتح الحزمة

k this deck

37

Under most tax treaties, income attributable to a permanent establishment through which a foreign taxpayer conducts business can be taxed only by the taxpayer's country of residence.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 102 في هذه المجموعة.

فتح الحزمة

k this deck

38

The income earned by a foreign branch operation of a U.S. corporation is taxable by the United States only when repatriated.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 102 في هذه المجموعة.

فتح الحزمة

k this deck

39

A U.S. parent corporation that receives a dividend from a wholly-owned foreign subsidiary that pays a 45% income tax to its home country does not owe any U.S. tax on the dividend.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 102 في هذه المجموعة.

فتح الحزمة

k this deck

40

The deemed paid foreign tax credit treats a U.S. corporation that receives a foreign source dividend as if the corporation paid tax directly to a foreign jurisdiction.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 102 في هذه المجموعة.

فتح الحزمة

k this deck

41

Cambridge, Inc. conducts business in states X and Y. This year, its before-tax income was $150,000. Below is information regarding its sales, payroll, and property factors in both states. Both states apply an equally-weighted three-factor formula to apportion income. State X has a 10% corporate income tax and state Y has a 5% corporate income tax. Compute the state tax savings if Cambridge could relocate $100,000 of property and $50,000 of payroll from state X to state Y.

A)$2,250

B)$12,563

C)$11,532

D)$9,094

Both states apply an equally-weighted three-factor formula to apportion income. State X has a 10% corporate income tax and state Y has a 5% corporate income tax. Compute the state tax savings if Cambridge could relocate $100,000 of property and $50,000 of payroll from state X to state Y.A)$2,250

B)$12,563

C)$11,532

D)$9,094

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 102 في هذه المجموعة.

فتح الحزمة

k this deck

42

Harris Corporation's before-tax income was $400,000. It does business entirely in Pennsylvania, which has a 6% corporate income tax. Compute Harris' federal income tax.

A)$24,000

B)$136,000

C)$131,600

D)$127,840

A)$24,000

B)$136,000

C)$131,600

D)$127,840

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 102 في هذه المجموعة.

فتح الحزمة

k this deck

43

Which of the following could result in a corporation having more than 100% of its income subject to state taxation?

A)Some of the states in which the corporation conducts business have not adopted the Uniform Division of Income for Tax Purposes Act formula.

B)The states in which the corporation conducts business have adopted different definitions of the specific components of the UDITPA formula.

C)Some of the states in which the corporation conducts business strictly apply the UDITPA formula while others double-weight the sales factor.

D)All of these factors could result in a corporation having more than 100% of its income subject to state taxation.

A)Some of the states in which the corporation conducts business have not adopted the Uniform Division of Income for Tax Purposes Act formula.

B)The states in which the corporation conducts business have adopted different definitions of the specific components of the UDITPA formula.

C)Some of the states in which the corporation conducts business strictly apply the UDITPA formula while others double-weight the sales factor.

D)All of these factors could result in a corporation having more than 100% of its income subject to state taxation.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 102 في هذه المجموعة.

فتح الحزمة

k this deck

44

Which of the following statements about the Uniform Division of Income for Tax Purposes Act (UDITPA) is false?

A)UDITPA requires all states to use the same method for apportioning income of multistate businesses.

B)UDITPA recommends an equally-weighted three-factor formula for apportioning income of multistate businesses.

C)The UDITPA property factor equals the cost of real or tangible personal property located in a state divided by the total cost of such property.

D)The UDITPA payroll factor equals the compensation paid to employees working in a state divided by total compensation.

A)UDITPA requires all states to use the same method for apportioning income of multistate businesses.

B)UDITPA recommends an equally-weighted three-factor formula for apportioning income of multistate businesses.

C)The UDITPA property factor equals the cost of real or tangible personal property located in a state divided by the total cost of such property.

D)The UDITPA payroll factor equals the compensation paid to employees working in a state divided by total compensation.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 102 في هذه المجموعة.

فتح الحزمة

k this deck

45

Which of the following activities create state income tax nexus?

A)Selling products over the Internet to customers in the state.The products are delivered by U.S.mail.

B)Traveling salespersons soliciting orders for tangible goods from customers in the state.

C)Ownership of manufacturing and distribution facilities within the state.

D)All of the above activities create state income tax nexus

A)Selling products over the Internet to customers in the state.The products are delivered by U.S.mail.

B)Traveling salespersons soliciting orders for tangible goods from customers in the state.

C)Ownership of manufacturing and distribution facilities within the state.

D)All of the above activities create state income tax nexus

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 102 في هذه المجموعة.

فتح الحزمة

k this deck

46

Section 482 of the Internal Revenue Code gives the IRS the authority to apportion or allocate gross income, deductions, or credits between/among related parties to correct any distortion resulting from unrealistic prices charged by members of the group to each other for goods or services.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 102 في هذه المجموعة.

فتح الحزمة

k this deck

47

Tri-State's, Inc. operates in Arkansas, Oklahoma, and Kansas. Assume that each state has adopted the UDITPA formula. During the corporation's tax year ended December 31, the apportionment data indicated: Which of the following statements is true?

A)The sales factor for Arkansas is approximately 35%.

B)Arkansas payroll percentage is approximately 11.1%.

C)The property factor for Arkansas is approximately 7.14%.

D)All of the above factors for Arkansas are correct.

Which of the following statements is true?A)The sales factor for Arkansas is approximately 35%.

B)Arkansas payroll percentage is approximately 11.1%.

C)The property factor for Arkansas is approximately 7.14%.

D)All of the above factors for Arkansas are correct.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 102 في هذه المجموعة.

فتح الحزمة

k this deck

48

Tri-State's, Inc. operates in Arkansas, Oklahoma, and Kansas. Assume that each state has adopted the UDITPA formula. During the corporation's tax year ended December 31, the apportionment data indicated: Tri-State's income for the current year is $250,000. Approximately how much income will be taxed by Oklahoma?

A)$250,000

B)$218,125

C)$44,375

D)$173,750

Tri-State's income for the current year is $250,000. Approximately how much income will be taxed by Oklahoma?A)$250,000

B)$218,125

C)$44,375

D)$173,750

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 102 في هذه المجموعة.

فتح الحزمة

k this deck

49

Which of the following statements concerning the nexus required for a state to tax income is false?

A)Maryland has nexus if the corporate headquarters is located in Baltimore.

B)Company-owned trucks driving through Arizona to deliver goods to customers residing in California creates nexus in Arizona.

C)Maine has nexus if a company has retail outlets located in Maine malls.

D)A New York corporation can send traveling salespeople into Massachusetts to solicit orders for tangible goods without creating nexus in Massachusetts.

A)Maryland has nexus if the corporate headquarters is located in Baltimore.

B)Company-owned trucks driving through Arizona to deliver goods to customers residing in California creates nexus in Arizona.

C)Maine has nexus if a company has retail outlets located in Maine malls.

D)A New York corporation can send traveling salespeople into Massachusetts to solicit orders for tangible goods without creating nexus in Massachusetts.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 102 في هذه المجموعة.

فتح الحزمة

k this deck

50

Economic nexus:

A)May exist even though a firm has no physical presence in a state.

B)Does not create taxing jurisdiction under the Commerce Clause of the U.S.Constitution.

C)Requires a greater physical presence than traditional definitions of nexus.

D)Applies only to Internet business activities.

A)May exist even though a firm has no physical presence in a state.

B)Does not create taxing jurisdiction under the Commerce Clause of the U.S.Constitution.

C)Requires a greater physical presence than traditional definitions of nexus.

D)Applies only to Internet business activities.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 102 في هذه المجموعة.

فتح الحزمة

k this deck

51

Lexington Corporation conducts business in four states. In state A, its sales factor is 50%, its payroll factor is 14%, and its property factor is 29%. State A uses an equally-weighted three-factor apportionment formula, but plans to change to a formula that double-weight the sales factor. Which is of the following statements is true?

A)Lexington's tax liability to state A will increase.

B)Any increase in Lexington's tax liability to state A will be offset by a decline in tax liability to other states.

C)Lexington's tax liability to state A will decrease.

D)Lexington's tax liability to state A will be unaffected by this change.

A)Lexington's tax liability to state A will increase.

B)Any increase in Lexington's tax liability to state A will be offset by a decline in tax liability to other states.

C)Lexington's tax liability to state A will decrease.

D)Lexington's tax liability to state A will be unaffected by this change.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 102 في هذه المجموعة.

فتح الحزمة

k this deck

52

Albany, Inc. does business in states C andD. State C uses an apportionment formula that double-weights the sales factor; state D apportions income using an equally-weighted three-factor formula. Albany's before tax income is $3,000,000, and its sales, payroll, and property factors are as follows.

A)State C, $1,100,000; State D, $1,800,000

B)State C, $1,100,000; State D, $1,900,000

C)State C, $1,200,000; State D, $1,800,000

D)State C, $1,200,000; State D, $1,900,000

A)State C, $1,100,000; State D, $1,800,000

B)State C, $1,100,000; State D, $1,900,000

C)State C, $1,200,000; State D, $1,800,000

D)State C, $1,200,000; State D, $1,900,000

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 102 في هذه المجموعة.

فتح الحزمة

k this deck

53

A controlled foreign corporation is a foreign corporation in which U.S. shareholders own more than 50% of the voting power or stock value.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 102 في هذه المجموعة.

فتح الحزمة

k this deck

54

Tri-State's, Inc. operates in Arkansas, Oklahoma, and Kansas. Assume that each state has adopted the UDITPA formula. During the corporation's tax year ended December 31, the apportionment data indicated: Tri-State's income for the current year is $250,000. Approximately how much will be taxed by Kansas?

A)$83,000

B)$95,000

C)$32,000

D)$170,000

Tri-State's income for the current year is $250,000. Approximately how much will be taxed by Kansas?A)$83,000

B)$95,000

C)$32,000

D)$170,000

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 102 في هذه المجموعة.

فتح الحزمة

k this deck

55

GAAP-based consolidated financial statements include only income earned by the consolidated group's domestic subsidiaries.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 102 في هذه المجموعة.

فتح الحزمة

k this deck

56

Verdi Inc. has before-tax income of $500,000. Verdi operates entirely in state Q, which has a 10% corporate income tax. Compute Verdi's combined federal and state tax burden as a percentage of its before-tax income.

A)44%

B)45%

C)41.5%

D)40.6%

A)44%

B)45%

C)41.5%

D)40.6%

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 102 في هذه المجموعة.

فتح الحزمة

k this deck

57

This year, Sutton Corporation's before-tax income was $2,000,000. It paid $175,000 income tax to Nebraska and $300,000 income tax to Iowa. Compute Sutton's federal income tax.

A)$680,000

B)$518,500

C)$700,000

D)$533,750

A)$680,000

B)$518,500

C)$700,000

D)$533,750

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 102 في هذه المجموعة.

فتح الحزمة

k this deck

58

Korn, Co. was incorporated in Delaware. It has production, distribution, and sales facilities in Kansas and Nebraska. All of Korn's customers reside in Kansas or Nebraska. Assume that both states use the UDITPA formula for apportionment of income. The corporation is investing in new equipment that cost $900,000. The equipment could be used in either the Kansas or Nebraska production facilities. Assume that Kansas' corporate income tax rate is 7% and Nebraska's is 8.5%. Should the equipment be placed in Kansas or Nebraska to minimize Korn's state income tax?

A)Kansas.

B)Nebraska.

C)Either state, because state income tax will be unaffected by this choice.

D)Korn should place the equipment in a third state in which it does not have nexus.

A)Kansas.

B)Nebraska.

C)Either state, because state income tax will be unaffected by this choice.

D)Korn should place the equipment in a third state in which it does not have nexus.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 102 في هذه المجموعة.

فتح الحزمة

k this deck

59

Transfer prices cannot be used by U.S. corporations and their foreign affiliates to shift income between taxing jurisdictions.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 102 في هذه المجموعة.

فتح الحزمة

k this deck

60

Albany, Inc. does business in states C and D. State C apportions income using an equally-weighted three-factor formula; state D uses an apportionment formula that double-weights the sales factor. Albany's before tax income is $3,000,000, and its sales, payroll, and property factors are as follows.

A)State C, $1,100,000; State D, $1,800,000

B)State C, $1,100,000; State D, $1,900,000

C)State C, $1,200,000; State D, $1,800,000

D)State C, $1,300,000; State D, $1,700,000

A)State C, $1,100,000; State D, $1,800,000

B)State C, $1,100,000; State D, $1,900,000

C)State C, $1,200,000; State D, $1,800,000

D)State C, $1,300,000; State D, $1,700,000

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 102 في هذه المجموعة.

فتح الحزمة

k this deck

61

Pennworth Corporation operates in the United States and foreign country M. Its domestic subsidiary Delco, Inc. operates in foreign country N. This year, the two corporations report the following. If Pennworth and Delco file a consolidated U.S. tax return, compute consolidated income tax liability.

A)$1,200,000

B)$1,260,000

C)$1,700,000

D)$1,020,000

If Pennworth and Delco file a consolidated U.S. tax return, compute consolidated income tax liability.A)$1,200,000

B)$1,260,000

C)$1,700,000

D)$1,020,000

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 102 في هذه المجموعة.

فتح الحزمة

k this deck

62

Which of the following statements about income tax treaties is false?

A)An income tax treaty is a bilateral agreement between the governments of two countries defining and limiting each country's respective tax jurisdiction.

B)The provisions of income tax treaties pertain only to individuals and corporations that are residents of either treaty country.

C)Under a typical treaty, the non-resident country would only tax a firm's profits if the firm maintained a permanent establishment in that country.

D)Under a typical treaty, a firm's profits would be allocated to the countries in a manner similar to the apportionment of income among states under the UDITPA formula.

A)An income tax treaty is a bilateral agreement between the governments of two countries defining and limiting each country's respective tax jurisdiction.

B)The provisions of income tax treaties pertain only to individuals and corporations that are residents of either treaty country.

C)Under a typical treaty, the non-resident country would only tax a firm's profits if the firm maintained a permanent establishment in that country.

D)Under a typical treaty, a firm's profits would be allocated to the countries in a manner similar to the apportionment of income among states under the UDITPA formula.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 102 في هذه المجموعة.

فتح الحزمة

k this deck

63

Which of the following statements concerning the taxation of a U.S. multinational corporation is true?

A)A U.S.corporation is taxed by the United States only on its U.S.source income.

B)The foreign tax credit ensures that a U.S.corporation will never pay taxes at a higher rate than the one imposed by the U.S.tax law.

C)Cross-crediting allows a U.S.corporation to maximize its foreign tax credit.

D)The foreign tax credit allows a U.S.corporation to defer taxation of its foreign source income until the earnings are repatriated.

A)A U.S.corporation is taxed by the United States only on its U.S.source income.

B)The foreign tax credit ensures that a U.S.corporation will never pay taxes at a higher rate than the one imposed by the U.S.tax law.

C)Cross-crediting allows a U.S.corporation to maximize its foreign tax credit.

D)The foreign tax credit allows a U.S.corporation to defer taxation of its foreign source income until the earnings are repatriated.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 102 في هذه المجموعة.

فتح الحزمة

k this deck

64

Many Mountains, Inc. is a U.S. multinational corporation. This year, it had the following income. Many Mountains paid $15,000 income tax to Country X and $28,500 income tax to Country Y. Compute Many Mountains' allowable foreign tax credit.

A)$57,800

B)$49,550

C)$43,500

D)$49,650

Many Mountains paid $15,000 income tax to Country X and $28,500 income tax to Country Y. Compute Many Mountains' allowable foreign tax credit.A)$57,800

B)$49,550

C)$43,500

D)$49,650

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 102 في هذه المجموعة.

فتح الحزمة

k this deck

65

San Carlos Corporation, a U.S. multinational, had pretax U.S. source income and foreign source income as follows. San Carlos paid $100,000 income tax to Country W. Calculate San Carlos' tax savings if it takes a foreign tax credit rather than deducting this tax.

A)$100,000

B)$66,000

C)$34,000

D)$0

San Carlos paid $100,000 income tax to Country W. Calculate San Carlos' tax savings if it takes a foreign tax credit rather than deducting this tax.A)$100,000

B)$66,000

C)$34,000

D)$0

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 102 في هذه المجموعة.

فتح الحزمة

k this deck

66

Which of the following statements about organizational forms for conducting foreign operations is false?

A)Income from a foreign branch office is reported on the consolidated U.S.income tax return.

B)Income from foreign operations conducted through a domestic subsidiary is reported on the consolidated U.S.income tax return.

C)Income from foreign operations conducted through a foreign subsidiary is reported on the consolidated U.S.income tax return.

D)Dividends received by a U.S.multinational corporation from a foreign subsidiary are reported on the consolidated U.S.income tax return.

A)Income from a foreign branch office is reported on the consolidated U.S.income tax return.

B)Income from foreign operations conducted through a domestic subsidiary is reported on the consolidated U.S.income tax return.

C)Income from foreign operations conducted through a foreign subsidiary is reported on the consolidated U.S.income tax return.

D)Dividends received by a U.S.multinational corporation from a foreign subsidiary are reported on the consolidated U.S.income tax return.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 102 في هذه المجموعة.

فتح الحزمة

k this deck

67

Fleming Corporation, a U.S. multinational, has pretax U.S. source income and foreign source income as follows. Fleming paid $200,000 income tax to CountryA. If Fleming takes the foreign tax credit, compute its worldwide tax burden as a percentage of its pretax income.

A)34%

B)35%

C)36%

D)44%

Fleming paid $200,000 income tax to CountryA. If Fleming takes the foreign tax credit, compute its worldwide tax burden as a percentage of its pretax income.A)34%

B)35%

C)36%

D)44%

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 102 في هذه المجموعة.

فتح الحزمة

k this deck

68

Jenkin Corporation reported the following for its first two taxable years. Calculate Jenkin's U.S. tax liability for Year 2.

A)$340,000

B)$240,000

C)$228,000

D)$204,000

Calculate Jenkin's U.S. tax liability for Year 2.A)$340,000

B)$240,000

C)$228,000

D)$204,000

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 102 في هذه المجموعة.

فتح الحزمة

k this deck

69

Galaxy Corporation conducts business in the U.S. and in Country X. In which of the following situations will Galaxy not be allowed a foreign tax credit for income taxes paid to Country X?

A)Country X operations are conducted through a domestic subsidiary included in Galaxy's consolidate tax return.

B)Country X operations are conducted through a foreign subsidiary that paid no dividends.

C)Country X operations are conducted through a foreign subsidiary that distributed 100% of its after-tax earnings as a dividend to Galaxy.

D)Country X operations are conducted through a foreign branch.

A)Country X operations are conducted through a domestic subsidiary included in Galaxy's consolidate tax return.

B)Country X operations are conducted through a foreign subsidiary that paid no dividends.

C)Country X operations are conducted through a foreign subsidiary that distributed 100% of its after-tax earnings as a dividend to Galaxy.

D)Country X operations are conducted through a foreign branch.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 102 في هذه المجموعة.

فتح الحزمة

k this deck

70

World Sales, Inc., a U.S. multinational, had pretax U.S. source income and foreign source income as follows. World Sales paid $50,000 income taxes to Country O. What is World Sale's U.S. tax liability if it deducts the foreign taxes paid?

A)$213,000

B)$204,000

C)$221,000

D)$238,000

World Sales paid $50,000 income taxes to Country O. What is World Sale's U.S. tax liability if it deducts the foreign taxes paid?A)$213,000

B)$204,000

C)$221,000

D)$238,000

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 102 في هذه المجموعة.

فتح الحزمة

k this deck

71

Fleming Corporation, a U.S. multinational, has pretax U.S. source income and foreign source income as follows. Fleming paid $50,000 income tax to Country A. If Fleming takes the foreign tax credit, compute its worldwide tax burden as a percentage of its pretax income.

A)34%

B)35%

C)44%

D)45%

Fleming paid $50,000 income tax to Country A. If Fleming takes the foreign tax credit, compute its worldwide tax burden as a percentage of its pretax income.A)34%

B)35%

C)44%

D)45%

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 102 في هذه المجموعة.

فتح الحزمة

k this deck

72

If a U.S. multinational corporation incurs start-up losses from foreign operations, which of the following organizational forms provide immediate U.S. tax savings from the deduction of the losses?

A)Operation through a foreign subsidiary

B)Operation through a foreign branch

C)Operation through a domestic subsidiary

D)Both b.and c.

A)Operation through a foreign subsidiary

B)Operation through a foreign branch

C)Operation through a domestic subsidiary

D)Both b.and c.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 102 في هذه المجموعة.

فتح الحزمة

k this deck

73

Mega, Inc., a U.S. multinational, has pretax U.S. source income and foreign source income as follows. Mega paid $20,000 income tax to Country M. Mega has a $25,000 foreign tax credit carryforward. What is Mega's U.S. tax liability if it takes the foreign tax credit?

A)$265,600

B)$240,600

C)$285,600

D)$258,400

Mega paid $20,000 income tax to Country M. Mega has a $25,000 foreign tax credit carryforward. What is Mega's U.S. tax liability if it takes the foreign tax credit?A)$265,600

B)$240,600

C)$285,600

D)$258,400

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 102 في هذه المجموعة.

فتح الحزمة

k this deck

74

Which of the following would qualify as a permanent establishment for income tax treaty purposes?

A)The presence of corporate employees in the host country for a limited time period.

B)Shipment of goods by the foreign corporation to customers in the host country.

C)Maintenance of a sales office in the host country.

D)All of the above would qualify as a permanent establishment.

A)The presence of corporate employees in the host country for a limited time period.

B)Shipment of goods by the foreign corporation to customers in the host country.

C)Maintenance of a sales office in the host country.

D)All of the above would qualify as a permanent establishment.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 102 في هذه المجموعة.

فتح الحزمة

k this deck

75

Southern, an Alabama corporation, has a $7 million excess FTC carryforward attributable to its foreign branch manufacturing operations. Which of the following strategies should increase Southern's use of its FTC carryforward to reduce U.S. tax?

A)Southern could open a branch manufacturing operation in a foreign country with a 27% corporate income tax.

B)Southern could open a branch manufacturing operation in a foreign country with a 40% corporate income tax.

C)Southern could repatriate foreign source income in the form of dividends from its controlled subsidiary operating in a country with a 38% corporate income tax.

D)None of these strategies would increase the use of the FTC carryforward.

A)Southern could open a branch manufacturing operation in a foreign country with a 27% corporate income tax.

B)Southern could open a branch manufacturing operation in a foreign country with a 40% corporate income tax.

C)Southern could repatriate foreign source income in the form of dividends from its controlled subsidiary operating in a country with a 38% corporate income tax.

D)None of these strategies would increase the use of the FTC carryforward.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 102 في هذه المجموعة.

فتح الحزمة

k this deck

76

Global Corporation, a U.S. multinational, began operations this year. Global had pretax U.S. source income and foreign source income as follows. Global paid $25,000 income tax to Country X. What is Global's U.S. tax liability if it takes the foreign tax credit?

A)$247,000

B)$238,000

C)$222,000

D)$272,000

Global paid $25,000 income tax to Country X. What is Global's U.S. tax liability if it takes the foreign tax credit?A)$247,000

B)$238,000

C)$222,000

D)$272,000

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 102 في هذه المجموعة.

فتح الحزمة

k this deck

77

Which of the following taxes is eligible for the foreign tax credit?

A)Property taxes paid to a foreign country on the value of property owned in that country.

B)Value-added taxes assessed on the value of inventory manufactured in a foreign country.

C)Income tax assessed by a local government within a foreign country.

D)Sales tax assessed on the purchase of consumer goods in a foreign country.

A)Property taxes paid to a foreign country on the value of property owned in that country.

B)Value-added taxes assessed on the value of inventory manufactured in a foreign country.

C)Income tax assessed by a local government within a foreign country.

D)Sales tax assessed on the purchase of consumer goods in a foreign country.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 102 في هذه المجموعة.

فتح الحزمة

k this deck

78

Which of the following statements about the foreign tax credit limitation is false?

A)The foreign tax credit cannot exceed the U.S.tax on foreign source income.

B)Foreign tax credits in excess of the limit can be carried forward indefinitely.

C)Cross-crediting of taxes paid in high-tax and low-tax foreign jurisdictions can increase allowable foreign tax credits.

D)The foreign tax credit limitation is based on the ratio of foreign source income to total taxable income.

A)The foreign tax credit cannot exceed the U.S.tax on foreign source income.

B)Foreign tax credits in excess of the limit can be carried forward indefinitely.

C)Cross-crediting of taxes paid in high-tax and low-tax foreign jurisdictions can increase allowable foreign tax credits.

D)The foreign tax credit limitation is based on the ratio of foreign source income to total taxable income.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 102 في هذه المجموعة.

فتح الحزمة

k this deck

79

Jokar Inc., a U.S. multinational, began operations this year. Jokar had pretax U.S. source income and foreign source income as follows. Jokar paid $50,000 income tax to Country O. Compute Jokar's U.S. tax liability if it takes the foreign tax credit.

A)$213,000

B)$221,000

C)$204,000

D)$238,000

Jokar paid $50,000 income tax to Country O. Compute Jokar's U.S. tax liability if it takes the foreign tax credit.A)$213,000

B)$221,000

C)$204,000

D)$238,000

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 102 في هذه المجموعة.

فتح الحزمة

k this deck

80

Which of the following statements about the foreign tax credit is true?

A)The foreign tax credit allows U.S.companies to defer U.S.tax on foreign source income.

B)The foreign tax credit is available to foreign corporations doing business in the U.S.

C)The foreign tax credit is allowed for all types of foreign taxes.

D)By permitting a foreign tax credit, the U.S.relinquishes its taxing jurisdiction on foreign source income earned by U.S.corporations to the extent that income is taxed by a foreign jurisdiction.

A)The foreign tax credit allows U.S.companies to defer U.S.tax on foreign source income.

B)The foreign tax credit is available to foreign corporations doing business in the U.S.

C)The foreign tax credit is allowed for all types of foreign taxes.

D)By permitting a foreign tax credit, the U.S.relinquishes its taxing jurisdiction on foreign source income earned by U.S.corporations to the extent that income is taxed by a foreign jurisdiction.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 102 في هذه المجموعة.

فتح الحزمة

k this deck

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 102 في هذه المجموعة.