Deck 9: Audit Sampling: An Application to Substantive Tests of Account Balances

ملء الشاشة (f)

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

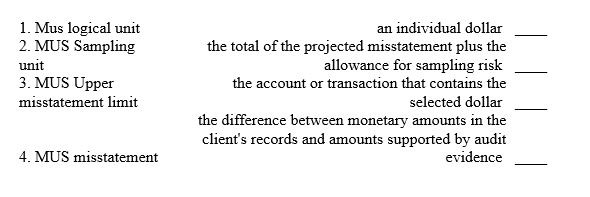

Matching

سؤال

سؤال

سؤال

سؤال

سؤال

Match between columns

فتح الحزمة

قم بالتسجيل لفتح البطاقات في هذه المجموعة!

Unlock Deck

Unlock Deck

1/54

العب

ملء الشاشة (f)

Deck 9: Audit Sampling: An Application to Substantive Tests of Account Balances

1

While performing a substantive test of details during an audit,the auditor determined that the sample results supported the conclusion that the recorded account balance was materially misstated.It was,in fact,not materially misstated.Such a situation illustrates the risk of

A) Incorrect rejection.

B) Incorrect acceptance.

C) Assessing control risk too high.

D) Assessing control risk too low.

A) Incorrect rejection.

B) Incorrect acceptance.

C) Assessing control risk too high.

D) Assessing control risk too low.

A

2

The risk of incorrect acceptance and the risk of overreliance relate to the

A) Preliminary estimates of materiality levels.

B) Allowable risk of tolerable error.

C) Efficiency of the audit.

D) Effectiveness of the audit.

A) Preliminary estimates of materiality levels.

B) Allowable risk of tolerable error.

C) Efficiency of the audit.

D) Effectiveness of the audit.

D

3

Confidence level is inversely related to sample size.

False

4

After a sample is drawn randomly,the allowance for sampling risk must be statistically quantified within a specified level of confidence.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 54 في هذه المجموعة.

فتح الحزمة

k this deck

5

An auditor is preparing to sample a client's customer receivables for overstatement.A statistical sampling method that automatically provides stratification when using systematic selection is

A) Attribute sampling.

B) Ratio-estimation sampling.

C) Monetary-unit sampling.

D) Mean-per-unit sampling.

A) Attribute sampling.

B) Ratio-estimation sampling.

C) Monetary-unit sampling.

D) Mean-per-unit sampling.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 54 في هذه المجموعة.

فتح الحزمة

k this deck

6

Which of the following sample planning factors would influence the sample size for a substantive test of details for a specific account?

A) Expected amount of misstatement but not the measure of tolerable misstatement.

B) Expected amount of misstatement and the measure of tolerable misstatement.

C) Measure of tolerable misstatement but not the expected amount of misstatement.

D) Neither the expected amount of misstatement nor the measure of tolerable misstatement.

A) Expected amount of misstatement but not the measure of tolerable misstatement.

B) Expected amount of misstatement and the measure of tolerable misstatement.

C) Measure of tolerable misstatement but not the expected amount of misstatement.

D) Neither the expected amount of misstatement nor the measure of tolerable misstatement.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 54 في هذه المجموعة.

فتح الحزمة

k this deck

7

Monetary-unit sampling should not be used if

A) The population includes several large items.

B) The auditor expects overstatement errors.

C) Many items in the account are expected to have errors.

D) No items in the account are expected to have errors.

A) The population includes several large items.

B) The auditor expects overstatement errors.

C) Many items in the account are expected to have errors.

D) No items in the account are expected to have errors.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 54 في هذه المجموعة.

فتح الحزمة

k this deck

8

Classical variables sampling uses normal distribution theory to evaluate the characteristics of a population based on sample data.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 54 في هذه المجموعة.

فتح الحزمة

k this deck

9

For monetary-unit sampling,the number of items tested is

A) Always equal to sample size.

B) Always greater than sample size.

C) Always greater than or equal to sample size.

D) Always less than or equal to sample size.

A) Always equal to sample size.

B) Always greater than sample size.

C) Always greater than or equal to sample size.

D) Always less than or equal to sample size.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 54 في هذه المجموعة.

فتح الحزمة

k this deck

10

The objective of monetary-unit sampling is to test the assertion that no material misstatements exist in an account balance or class of transactions.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 54 في هذه المجموعة.

فتح الحزمة

k this deck

11

The size of the upper limit on misstatement is largely dependent on the sample size,which is inversely related to the desired confidence level.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 54 في هذه المجموعة.

فتح الحزمة

k this deck

12

Monetary-unit sampling is based on attribute sampling concepts.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 54 في هذه المجموعة.

فتح الحزمة

k this deck

13

A number of factors influence the sample size for a substantive test of details of an account balance.All other factors being equal,which of the following would lead to a larger sample size?

A) Greater reliance on internal controls.

B) Greater reliance on analytical procedures.

C) Smaller expected frequency of misstatements.

D) Smaller measure of tolerable misstatements.

A) Greater reliance on internal controls.

B) Greater reliance on analytical procedures.

C) Smaller expected frequency of misstatements.

D) Smaller measure of tolerable misstatements.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 54 في هذه المجموعة.

فتح الحزمة

k this deck

14

In monetary-unit sampling,population size is

A) The dollar balance in an account.

B) The number of items in an account.

C) Unrelated to sample size.

D) Included in the denominator of the formula to determine sample size.

A) The dollar balance in an account.

B) The number of items in an account.

C) Unrelated to sample size.

D) Included in the denominator of the formula to determine sample size.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 54 في هذه المجموعة.

فتح الحزمة

k this deck

15

Haphazard selection allows the auditor to select items judgmentally.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 54 في هذه المجموعة.

فتح الحزمة

k this deck

16

The purpose of audit sampling is to draw inferences about the entire population from the results of a sample.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 54 في هذه المجموعة.

فتح الحزمة

k this deck

17

Expected misstatement is directly related to sample size.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 54 في هذه المجموعة.

فتح الحزمة

k this deck

18

Monetary-unit sampling is commonly used by auditors to test controls.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 54 في هذه المجموعة.

فتح الحزمة

k this deck

19

In statistical or nonstatistical sampling methods used in substantive testing,an auditor most likely would stratify a population into meaningful groups if

A) Monetary-unit sampling (MUS) is used.

B) The population contains both very high and very low recorded amounts.

C) The auditor's estimated tolerable misstatement is extremely small.

D) The standard deviation of recorded amounts is relatively small.

A) Monetary-unit sampling (MUS) is used.

B) The population contains both very high and very low recorded amounts.

C) The auditor's estimated tolerable misstatement is extremely small.

D) The standard deviation of recorded amounts is relatively small.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 54 في هذه المجموعة.

فتح الحزمة

k this deck

20

Which of the following statements best describes an inherent limitation of the monetary-unit sampling method?

A) It can only be used for substantive testing of asset accounts.

B) It requires the use of a computer system to perform the required calculations.

C) Misstatement rates must be large and the misstatements must be overstatements.

D) Misstatement rates must be small and the misstatements must be overstatements.

A) It can only be used for substantive testing of asset accounts.

B) It requires the use of a computer system to perform the required calculations.

C) Misstatement rates must be large and the misstatements must be overstatements.

D) Misstatement rates must be small and the misstatements must be overstatements.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 54 في هذه المجموعة.

فتح الحزمة

k this deck

21

Which one of the following statements is true regarding two random samples,drawn in the same way,from the same population,one of size 30 and one of size 300?

A) The two samples are expected to have the same sample mean.

B) The larger sample is more likely to produce a large sample mean.

C) The smaller sample will have a smaller 95% confidence interval for the mean.

D) The smaller sample will, on average, produce a lower estimate of the variance of the population.

A) The two samples are expected to have the same sample mean.

B) The larger sample is more likely to produce a large sample mean.

C) The smaller sample will have a smaller 95% confidence interval for the mean.

D) The smaller sample will, on average, produce a lower estimate of the variance of the population.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 54 في هذه المجموعة.

فتح الحزمة

k this deck

22

In statistical sampling,setting the appropriate confidence level and desired sample precision are decisions made by the auditor that will affect sample size for a substantive procedure.Which of the following should not be a factor in the choice of desired precision?

A) The sampling risk.

B) The size of an account balance misstatement considered material.

C) The audit resources available for execution of the sampling plan.

D) The objectives of the audit test being conducted.

A) The sampling risk.

B) The size of an account balance misstatement considered material.

C) The audit resources available for execution of the sampling plan.

D) The objectives of the audit test being conducted.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 54 في هذه المجموعة.

فتح الحزمة

k this deck

23

Which of the following courses of action would an auditor most likely follow in planning a sample of cash disbursements if the auditor is aware of several unusually large cash disbursements?

A) Set the tolerable deviation rate at a lower level than originally planned.

B) Identify the large and unusual disbursements as individually significant and test 100 percent.

C) Increase the sample size to reduce the effect of the unusually large disbursements.

D) Continue to draw new samples until all the unusually large disbursements appear in the sample.

A) Set the tolerable deviation rate at a lower level than originally planned.

B) Identify the large and unusual disbursements as individually significant and test 100 percent.

C) Increase the sample size to reduce the effect of the unusually large disbursements.

D) Continue to draw new samples until all the unusually large disbursements appear in the sample.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 54 في هذه المجموعة.

فتح الحزمة

k this deck

24

In a monetary-unit sample with a sampling interval of $5,000,an auditor discovers that a selected account receivable with a recorded amount of $10,000 has an audit amount of $8,000.If this were the only error discovered by the auditor,the projected misstatement for this sample would be

A) $5,000.

B) $4,000.

C) $2,000.

D) $1,000.

A) $5,000.

B) $4,000.

C) $2,000.

D) $1,000.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 54 في هذه المجموعة.

فتح الحزمة

k this deck

25

In a monetary-unit sampling plan,the upper misstatement limit is $11,200 and the risk of incorrect acceptance is 5%.This means that

A) Tolerable misstatement is $11,200.

B) There is a 95% chance that the actual misstatement in the account is $11,200 or more.

C) There is a 95% chance that the actual misstatement in the account is $11,200.

D) There is a 95% chance that the actual misstatement in the account is $11,200 or less.

A) Tolerable misstatement is $11,200.

B) There is a 95% chance that the actual misstatement in the account is $11,200 or more.

C) There is a 95% chance that the actual misstatement in the account is $11,200.

D) There is a 95% chance that the actual misstatement in the account is $11,200 or less.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 54 في هذه المجموعة.

فتح الحزمة

k this deck

26

The use of the ratio projection is most effective when

A) The dollar amount of the misstatement is expected to relate to the dollar amount of items tested.

B) A small number of differences exist in the population.

C) Estimating populations whose records consist of quantities but not book values.

D) Large understatement differences exist in the population.

A) The dollar amount of the misstatement is expected to relate to the dollar amount of items tested.

B) A small number of differences exist in the population.

C) Estimating populations whose records consist of quantities but not book values.

D) Large understatement differences exist in the population.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 54 في هذه المجموعة.

فتح الحزمة

k this deck

27

Which of the following sampling methods would be used to estimate a numerical measurement of population,such as the dollar value of an account?

A) Attributes sampling.

B) Stop-or-go sampling.

C) Classical variables sampling.

D) Random-number sampling.

A) Attributes sampling.

B) Stop-or-go sampling.

C) Classical variables sampling.

D) Random-number sampling.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 54 في هذه المجموعة.

فتح الحزمة

k this deck

28

The accounting department reports that the balance of accounts receivable is $210,000.You are willing to accept that balance if audit sampling suggests it is within $15,000 of the actual balance.Using a classical variables sampling plan,you compute a 95% confidence interval of $208,000 to $225,000.You would therefore

A) Not be able to determine the acceptability of the receivable balance.

B) Accept the balance but with a lower level of confidence.

C) Take a larger sample before totally rejecting the balance and requiring adjustments.

D) Accept the $210,000 balance because the confidence interval is within the materiality limits.

A) Not be able to determine the acceptability of the receivable balance.

B) Accept the balance but with a lower level of confidence.

C) Take a larger sample before totally rejecting the balance and requiring adjustments.

D) Accept the $210,000 balance because the confidence interval is within the materiality limits.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 54 في هذه المجموعة.

فتح الحزمة

k this deck

29

The formula for nonstatistical sampling for tests of account balances provided by the AICPA

A) Must be used for nonstatistical sampling.

B) Includes a provision for the risk of incorrect acceptance.

C) Is affected by the nature of other substantive procedures used to test the account balance.

D) Is largely based on the variation of items in the account.

A) Must be used for nonstatistical sampling.

B) Includes a provision for the risk of incorrect acceptance.

C) Is affected by the nature of other substantive procedures used to test the account balance.

D) Is largely based on the variation of items in the account.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 54 في هذه المجموعة.

فتح الحزمة

k this deck

30

In applying classical variables sampling,an auditor attempts to

A) Estimate a qualitative characteristic of interest.

B) Determine various rates of occurrence for specified attributes.

C) Discover at least one instance of a critical deviation.

D) Predict a monetary population value within a range of precision.

A) Estimate a qualitative characteristic of interest.

B) Determine various rates of occurrence for specified attributes.

C) Discover at least one instance of a critical deviation.

D) Predict a monetary population value within a range of precision.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 54 في هذه المجموعة.

فتح الحزمة

k this deck

31

The assurance factor for nonstatistical sampling is based on

A) The number of items in the account.

B) Auditor judgment.

C) The risk of misstatement in the account and the level of desired assurance.

D) Variability in the population and the risk of misstatement in the account.

A) The number of items in the account.

B) Auditor judgment.

C) The risk of misstatement in the account and the level of desired assurance.

D) Variability in the population and the risk of misstatement in the account.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 54 في هذه المجموعة.

فتح الحزمة

k this deck

32

Monetary-unit sampling is said to eliminate the need to stratify the sample because

A) Sample items are selected in proportion to their dollar amount.

B) The risk of incorrect acceptance is inversely related to sample size.

C) Tolerable misstatement is considered when determining sample size.

D) The upper limit on misstatements can be computed based on statistical principles.

A) Sample items are selected in proportion to their dollar amount.

B) The risk of incorrect acceptance is inversely related to sample size.

C) Tolerable misstatement is considered when determining sample size.

D) The upper limit on misstatements can be computed based on statistical principles.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 54 في هذه المجموعة.

فتح الحزمة

k this deck

33

Precision is a statistical measure of the maximum likely difference between the sample estimate and the true but unknown population total and is directly related to

A) Reliability of evidence.

B) Relative risk.

C) Confidence level.

D) Cost benefit analysis.

A) Reliability of evidence.

B) Relative risk.

C) Confidence level.

D) Cost benefit analysis.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 54 في هذه المجموعة.

فتح الحزمة

k this deck

34

Which of the following most likely would be an advantage in using classical variables sampling rather than monetary-unit sampling?

A) An estimate of the standard deviation of the population's recorded amounts is not required.

B) The auditor rarely needs the assistance of a computer program to design an efficient sample.

C) Inclusion of zero and negative balances generally does not require special design considerations.

D) Any amount that is individually significant is automatically identified and selected.

A) An estimate of the standard deviation of the population's recorded amounts is not required.

B) The auditor rarely needs the assistance of a computer program to design an efficient sample.

C) Inclusion of zero and negative balances generally does not require special design considerations.

D) Any amount that is individually significant is automatically identified and selected.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 54 في هذه المجموعة.

فتح الحزمة

k this deck

35

An accounts receivable account balance is $500,000 and the auditor determines a sample size of 30 would provide adequate assurance.The auditor plans to use a monetary-unit sampling plan with systematic sample selection.The auditor notices that there are six customer accounts of at least $15,000 and would like the systematic selection technique to select all items that are at least $15,000,even if that means the sample size is slightly larger than 30.To achieve the auditor's objectives,the sampling interval should be

A) 6.

B) 20.

C) 16,666.

D) 15,000.

A) 6.

B) 20.

C) 16,666.

D) 15,000.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 54 في هذه المجموعة.

فتح الحزمة

k this deck

36

Which of the following would be an improper technique when using monetary-unit statistical sampling in an audit of accounts receivable?

A) Combining negative and positive dollar misstatements in the appraisal of a sample.

B) Using a sampling technique in which the same account balance could be selected more than once.

C) Selecting a random starting point and then sampling every nth dollar.

D) Defining the sampling unit in the population as an individual dollar and not as an individual account balance.

A) Combining negative and positive dollar misstatements in the appraisal of a sample.

B) Using a sampling technique in which the same account balance could be selected more than once.

C) Selecting a random starting point and then sampling every nth dollar.

D) Defining the sampling unit in the population as an individual dollar and not as an individual account balance.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 54 في هذه المجموعة.

فتح الحزمة

k this deck

37

For monetary-unit sampling,a sampling interval of 400 means that

A) Every 400th item in the account will be selected in the sample.

B) The average size of items in the account is 400.

C) Every 400th dollar in the account will be included in the sample.

D) The average misstatement in sample items is $400.

A) Every 400th item in the account will be selected in the sample.

B) The average size of items in the account is 400.

C) Every 400th dollar in the account will be included in the sample.

D) The average misstatement in sample items is $400.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 54 في هذه المجموعة.

فتح الحزمة

k this deck

38

What is the primary objective of testing all individually significant items rather than sample testing?

A) To increase the audit risk at which a decision will be reached from the results of the sample selected.

B) To increase sample size.

C) To accept no sampling risk for items greater than tolerable misstatement.

D) To increase the size of the confidence bound around the projected misstatement.

A) To increase the audit risk at which a decision will be reached from the results of the sample selected.

B) To increase sample size.

C) To accept no sampling risk for items greater than tolerable misstatement.

D) To increase the size of the confidence bound around the projected misstatement.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 54 في هذه المجموعة.

فتح الحزمة

k this deck

39

In examining cash disbursements,an auditor plans to choose a sample using systematic selection with a random start.The primary advantage of such a systematic selection is that population items

A) That include fraud will not be overlooked when the auditor exercises compatible reciprocal options.

B) May occur in a systematic pattern, thus making the sample more representative.

C) May occur more than once in a sample.

D) Do not have to be prenumbered in order for the auditor to use the technique.

A) That include fraud will not be overlooked when the auditor exercises compatible reciprocal options.

B) May occur in a systematic pattern, thus making the sample more representative.

C) May occur more than once in a sample.

D) Do not have to be prenumbered in order for the auditor to use the technique.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 54 في هذه المجموعة.

فتح الحزمة

k this deck

40

If the upper limit on misstatements exceeds tolerable misstatement,the auditor is least likely to

A) Increase sample size.

B) Conduct other substantive procedures.

C) Adjust the account balance.

D) Increase the risk of incorrect rejection.

A) Increase sample size.

B) Conduct other substantive procedures.

C) Adjust the account balance.

D) Increase the risk of incorrect rejection.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 54 في هذه المجموعة.

فتح الحزمة

k this deck

41

When auditing accounts payable using classical variables sampling,Sue finds evidence indicating that the account may be materially misstated.What are Sue's options?

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 54 في هذه المجموعة.

فتح الحزمة

k this deck

42

In a monetary-unit sample with a sampling interval of $10,000,an auditor discovered that a selected account receivable with a recorded amount of $5,000 had an audit amount of $2,000.The projected misstatement of this sample was

A) $3,000.

B) $4,000.

C) $6,000.

D) $8,000.

A) $3,000.

B) $4,000.

C) $6,000.

D) $8,000.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 54 في هذه المجموعة.

فتح الحزمة

k this deck

43

Summarize the concept behind monetary-unit sampling (MUS).How does MUS use attribute-sampling theory?

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 54 في هذه المجموعة.

فتح الحزمة

k this deck

44

An auditor has taken a large sample from an audit population that is skewed in the sense that it contains a large number of small dollar balances.The auditor can conclude

A) The sampling distribution is not normal; therefore MUS sampling will more accurately define the nature of the population.

B) The sampling distribution is normal; therefore the confidence coefficient value can be used to evaluate the sample results.

C) The sampling distribution is not normal; thus attribute sampling is the only alternative statistical tool that can be appropriately used.

D) None of the above answers is correct.

A) The sampling distribution is not normal; therefore MUS sampling will more accurately define the nature of the population.

B) The sampling distribution is normal; therefore the confidence coefficient value can be used to evaluate the sample results.

C) The sampling distribution is not normal; thus attribute sampling is the only alternative statistical tool that can be appropriately used.

D) None of the above answers is correct.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 54 في هذه المجموعة.

فتح الحزمة

k this deck

45

An auditor established a $60,000 tolerable misstatement for an account balance of $1,000,000.The auditor selected a sample of every twentieth item from the population of 1,000 items that represented the asset account balance and discovered overstatements of $3,700 and understatements of $200.Under these circumstances,the auditor most likely would conclude that

A) There is an unacceptably high risk that the actual misstatements in the population exceed the tolerable misstatement because the total projected misstatement is more than the tolerable misstatement.

B) There is an unacceptably high risk that the tolerable misstatement exceeds the sum of actual overstatements and understatements.

C) The asset account is fairly stated because the total projected misstatement is less than the tolerable misstatement.

D) The asset account is fairly stated because the tolerable misstatement exceeds the net of projected actual overstatements and understatements.

A) There is an unacceptably high risk that the actual misstatements in the population exceed the tolerable misstatement because the total projected misstatement is more than the tolerable misstatement.

B) There is an unacceptably high risk that the tolerable misstatement exceeds the sum of actual overstatements and understatements.

C) The asset account is fairly stated because the total projected misstatement is less than the tolerable misstatement.

D) The asset account is fairly stated because the tolerable misstatement exceeds the net of projected actual overstatements and understatements.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 54 في هذه المجموعة.

فتح الحزمة

k this deck

46

In nonstatistical sampling,describe the two methods auditors use to project sample results to the population.How does an auditor determine which method to use?

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 54 في هذه المجموعة.

فتح الحزمة

k this deck

47

Match each factor of sample size to (1)its relationship to sample size (A-Direct or B-Inverse)and (2)the appropriate effect on the sample size if the factor increases (C-Increase or D-Decrease).

1.Tolerable misstatement

2.Population size

3.Desired confidence level

4.Expected misstatement

1.Tolerable misstatement

2.Population size

3.Desired confidence level

4.Expected misstatement

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 54 في هذه المجموعة.

فتح الحزمة

k this deck

48

An auditor is performing substantive procedures of pricing and extension of perpetual inventory balances consisting of a large number of items.Past experience indicates numerous pricing and extension errors.Which of the following statistical sampling approaches is most appropriate?

A) Unstratified mean-per-unit.

B) Monetary-unit sampling.

C) Stop or go.

D) Difference projection.

A) Unstratified mean-per-unit.

B) Monetary-unit sampling.

C) Stop or go.

D) Difference projection.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 54 في هذه المجموعة.

فتح الحزمة

k this deck

49

Matching

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 54 في هذه المجموعة.

فتح الحزمة

k this deck

50

Whenever a statistical method is used,a decision rule determines whether the population is acceptable.The decision rule for monetary-unit sampling is "Accept the conclusion that the book value is not misstated by a material amount if _________________________."

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 54 في هذه المجموعة.

فتح الحزمة

k this deck

51

Describe two advantages and two disadvantages of monetary-use sampling (MUS).

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 54 في هذه المجموعة.

فتح الحزمة

k this deck

52

What is one advantage and one disadvantage of classical variables sampling?

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 54 في هذه المجموعة.

فتح الحزمة

k this deck

53

You are auditing accounts receivable for a small company and have found the following results:

Use ratio projection to project your results.

Use ratio projection to project your results.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 54 في هذه المجموعة.

فتح الحزمة

k this deck

55

Match between columns

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 54 في هذه المجموعة.

فتح الحزمة

k this deck

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 54 في هذه المجموعة.