Deck 11: Auditing the Purchasing Process

ملء الشاشة (f)

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

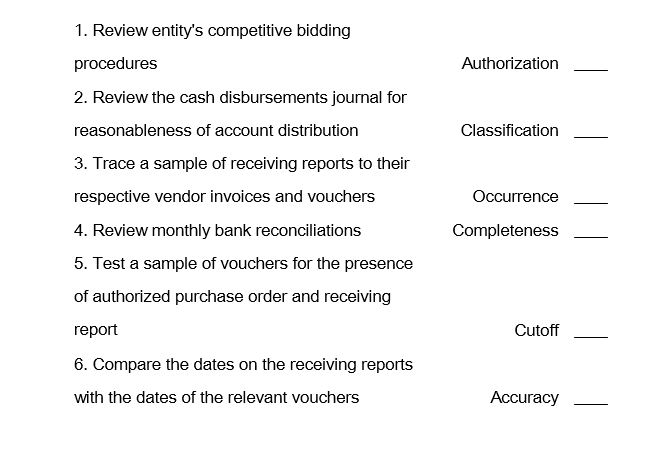

Match the test of controls described below to the appropriate assertion it is used to test.

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

فتح الحزمة

قم بالتسجيل لفتح البطاقات في هذه المجموعة!

Unlock Deck

Unlock Deck

1/80

العب

ملء الشاشة (f)

Deck 11: Auditing the Purchasing Process

1

A debit memo

A) reduces the amount of accounts payable due to a vendor.

B) reduces accounts payable when payment is made.

C) is used by vendors to record cash payments received.

D) authorizes a debit to purchases when goods are received.

A) reduces the amount of accounts payable due to a vendor.

B) reduces accounts payable when payment is made.

C) is used by vendors to record cash payments received.

D) authorizes a debit to purchases when goods are received.

A

2

A purchase transaction usually begins with the preparation of a purchase order.

False

3

The cutoff assertion for accounts payable includes

A) determining whether all accounts payable are recorded.

B) determining whether all accounts payable actually are liabilities.

C) determining whether all accounts payable are recorded in the proper period.

D) determining whether all accounts payable are properly classified in the financial statements.

A) determining whether all accounts payable are recorded.

B) determining whether all accounts payable actually are liabilities.

C) determining whether all accounts payable are recorded in the proper period.

D) determining whether all accounts payable are properly classified in the financial statements.

C

4

The principal business objectives of the purchasing process are acquiring goods and services and paying for those goods and services.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 80 في هذه المجموعة.

فتح الحزمة

k this deck

5

Analytical procedures can be used to examine the reasonableness of accounts payable and accrued expenses.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 80 في هذه المجموعة.

فتح الحزمة

k this deck

6

A receiving report is used to document the ordering of goods.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 80 في هذه المجموعة.

فتح الحزمة

k this deck

7

Product costs should be matched directly with specific transactions and are recognized upon recognition of revenue.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 80 في هذه المجموعة.

فتح الحزمة

k this deck

8

The occurrence assertion for accounts payable includes

A) determining whether all accounts payable are recorded.

B) determining whether all accounts payable actually are liabilities.

C) determining whether all accounts payable are recorded in the proper period.

D) determining whether all accounts payable are properly classified in the financial statements.

A) determining whether all accounts payable are recorded.

B) determining whether all accounts payable actually are liabilities.

C) determining whether all accounts payable are recorded in the proper period.

D) determining whether all accounts payable are properly classified in the financial statements.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 80 في هذه المجموعة.

فتح الحزمة

k this deck

9

A product cost is

A) an expense allocated by a systematic procedure.

B) recognized during the period in which a liability is incurred.

C) recognized in the period during which related revenue is recognized.

D) recognized in the period in which cash is spent.

A) an expense allocated by a systematic procedure.

B) recognized during the period in which a liability is incurred.

C) recognized in the period during which related revenue is recognized.

D) recognized in the period in which cash is spent.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 80 في هذه المجموعة.

فتح الحزمة

k this deck

10

In assessing control risk for purchases,an auditor vouches a sample of entries in the voucher register to the supporting documents.Which assertion would this test of controls most likely support?

A) Completeness.

B) Occurrence.

C) Accuracy.

D) Classification.

A) Completeness.

B) Occurrence.

C) Accuracy.

D) Classification.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 80 في هذه المجموعة.

فتح الحزمة

k this deck

11

Unrecorded liabilities are most likely to be found during the review of which of the following documents?

A) Unpaid bills.

B) Shipping records.

C) Bills of lading.

D) Unmatched sales invoices.

A) Unpaid bills.

B) Shipping records.

C) Bills of lading.

D) Unmatched sales invoices.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 80 في هذه المجموعة.

فتح الحزمة

k this deck

12

The accounts payable department is responsible for ensuring that all vendor invoices,cash disbursements,and adjustments are recorded in the accounts payable records.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 80 في هذه المجموعة.

فتح الحزمة

k this deck

13

The cash disbursements journal is also called the

A) voucher register.

B) purchases journal.

C) check register.

D) accounts payable subsidiary ledger.

A) voucher register.

B) purchases journal.

C) check register.

D) accounts payable subsidiary ledger.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 80 في هذه المجموعة.

فتح الحزمة

k this deck

14

Accounts payable confirmations are used less frequently by auditors than accounts receivable confirmations.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 80 في هذه المجموعة.

فتح الحزمة

k this deck

15

The purchase journal is referred to as a check register.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 80 في هذه المجموعة.

فتح الحزمة

k this deck

16

After the controls are tested,the auditor sets the achieved level of control risk.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 80 في هذه المجموعة.

فتح الحزمة

k this deck

17

To determine whether accounts payable are complete,an auditor performs a test to verify that all merchandise received is recorded.The population of documents for this test consists of all

A) payment vouchers.

B) receiving reports.

C) purchase requisitions.

D) vendors' invoices.

A) payment vouchers.

B) receiving reports.

C) purchase requisitions.

D) vendors' invoices.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 80 في هذه المجموعة.

فتح الحزمة

k this deck

18

The accounts payable department receives the purchase order form to accomplish all of the following except to:

A) compare invoice price to purchase order price.

B) ensure that the purchase had been properly authorized.

C) ensure that the goods had been received by the party requesting the goods.

D) compare quantity ordered to quantity purchased.

A) compare invoice price to purchase order price.

B) ensure that the purchase had been properly authorized.

C) ensure that the goods had been received by the party requesting the goods.

D) compare quantity ordered to quantity purchased.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 80 في هذه المجموعة.

فتح الحزمة

k this deck

19

Which of the following accounts is not affected by cash disbursement transactions?

A) Cash.

B) Accounts payable.

C) Purchase discounts.

D) Purchase returns.

A) Cash.

B) Accounts payable.

C) Purchase discounts.

D) Purchase returns.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 80 في هذه المجموعة.

فتح الحزمة

k this deck

20

Because of the low volume of purchase return transactions,the auditor normally does not test the controls associated with these transactions.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 80 في هذه المجموعة.

فتح الحزمة

k this deck

21

As an in-charge auditor,you are reviewing a summary of control weaknesses in cash disbursement procedures.Which one of the following weaknesses,standing alone,should cause you the least concern?

A) Checks are signed by only one person.

B) Signed checks are distributed by the controller to approved payees.

C) Treasurer fails to establish validity of names and addresses of check payees.

D) Cash disbursements are made directly out of cash receipts.

A) Checks are signed by only one person.

B) Signed checks are distributed by the controller to approved payees.

C) Treasurer fails to establish validity of names and addresses of check payees.

D) Cash disbursements are made directly out of cash receipts.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 80 في هذه المجموعة.

فتح الحزمة

k this deck

22

For effective internal control,the accounts payable department should compare the information on each vendor's invoice with the

A) receiving report and the purchase order.

B) receiving report and the voucher.

C) vendor's packing slip and the purchase order.

D) vendor's packing slip and the voucher.

A) receiving report and the purchase order.

B) receiving report and the voucher.

C) vendor's packing slip and the purchase order.

D) vendor's packing slip and the voucher.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 80 في هذه المجموعة.

فتح الحزمة

k this deck

23

In testing controls over cash disbursements,an auditor most likely would determine that the person who signs the checks also

A) reviews the monthly bank reconciliation.

B) returns the checks to accounts payable.

C) is denied access to the supporting documents.

D) is responsible for mailing the checks.

A) reviews the monthly bank reconciliation.

B) returns the checks to accounts payable.

C) is denied access to the supporting documents.

D) is responsible for mailing the checks.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 80 في هذه المجموعة.

فتح الحزمة

k this deck

24

An auditor performs a test to determine whether all merchandise was received for which the entity was billed.The population for this test consists of all

A) merchandise received.

B) vendors' invoices.

C) canceled checks.

D) receiving reports.

A) merchandise received.

B) vendors' invoices.

C) canceled checks.

D) receiving reports.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 80 في هذه المجموعة.

فتح الحزمة

k this deck

25

An important primary purpose of the auditor's review of the entity's procurement system should be to determine the effectiveness of the activities to protect against

A) improper materials handling.

B) unauthorized persons issuing purchase orders.

C) mispostings of purchase returns.

D) excessive shrinkage or spoilage.

A) improper materials handling.

B) unauthorized persons issuing purchase orders.

C) mispostings of purchase returns.

D) excessive shrinkage or spoilage.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 80 في هذه المجموعة.

فتح الحزمة

k this deck

26

Tests designed to detect purchases made before the end of the year that have been recorded in the subsequent year most likely would provide assurance about management's assertion of

A) accuracy.

B) occurrence.

C) cutoff.

D) classification.

A) accuracy.

B) occurrence.

C) cutoff.

D) classification.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 80 في هذه المجموعة.

فتح الحزمة

k this deck

27

The auditor is most likely to verify accrued commissions payable in conjunction with the

A) sales cutoff review.

B) verification of employees.

C) review of post balance sheet date disbursements.

D) examination of trade accounts payable.

A) sales cutoff review.

B) verification of employees.

C) review of post balance sheet date disbursements.

D) examination of trade accounts payable.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 80 في هذه المجموعة.

فتح الحزمة

k this deck

28

The audit procedures used to verify accrued liabilities differ from those employed for the verification of accounts payable because

A) accrued liabilities usually pertain to services of a continuing nature, while accounts payable are the result of completed transactions.

B) accrued liability balances are less material than accounts payable balances.

C) evidence supporting accrued liabilities is nonexistent, while evidence supporting accounts payable is readily available.

D) accrued liabilities at year-end will become accounts payable during the following year.

A) accrued liabilities usually pertain to services of a continuing nature, while accounts payable are the result of completed transactions.

B) accrued liability balances are less material than accounts payable balances.

C) evidence supporting accrued liabilities is nonexistent, while evidence supporting accounts payable is readily available.

D) accrued liabilities at year-end will become accounts payable during the following year.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 80 في هذه المجموعة.

فتح الحزمة

k this deck

29

An entity's procurement system ends with the assumption of a liability and the eventual payment of the liability.Which of the following best describes the auditor's primary concern with respect to liabilities resulting from the procurement system?

A) Accounts payable are not materially understated.

B) Authority to incur liabilities is restricted to one designated person.

C) Acquisition of materials is not made from one vendor or one group of vendors.

D) Commitments for all purchases are made only after established competitive bidding procedures are followed.

A) Accounts payable are not materially understated.

B) Authority to incur liabilities is restricted to one designated person.

C) Acquisition of materials is not made from one vendor or one group of vendors.

D) Commitments for all purchases are made only after established competitive bidding procedures are followed.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 80 في هذه المجموعة.

فتح الحزمة

k this deck

30

Which of the following audit procedures is least likely to detect an unrecorded liability?

A) Analysis and recomputation of interest expense.

B) Analysis and recomputation of depreciation expense.

C) Mailing of standard bank confirmation forms.

D) Reading of the minutes of meetings of the board of directors.

A) Analysis and recomputation of interest expense.

B) Analysis and recomputation of depreciation expense.

C) Mailing of standard bank confirmation forms.

D) Reading of the minutes of meetings of the board of directors.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 80 في هذه المجموعة.

فتح الحزمة

k this deck

31

The authority to accept incoming goods in receiving should be based on a(an)

A) vendor's invoice.

B) materials requisition.

C) bill of lading.

D) approved purchase order.

A) vendor's invoice.

B) materials requisition.

C) bill of lading.

D) approved purchase order.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 80 في هذه المجموعة.

فتح الحزمة

k this deck

32

Tests of controls for the occurrence assertion for purchases include all of the following except:

A) evaluating proper segregation of duties.

B) testing a sample of vouchers for an authorized purchase order.

C) testing a sample of vouchers for matching receiving reports.

D) tracing a sample of vouchers to purchases journal.

A) evaluating proper segregation of duties.

B) testing a sample of vouchers for an authorized purchase order.

C) testing a sample of vouchers for matching receiving reports.

D) tracing a sample of vouchers to purchases journal.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 80 في هذه المجموعة.

فتح الحزمة

k this deck

33

Operating control over the check signature plate normally should be the responsibility of the

A) Secretary.

B) Chief accountant.

C) Vice President of Finance.

D) Treasurer.

A) Secretary.

B) Chief accountant.

C) Vice President of Finance.

D) Treasurer.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 80 في هذه المجموعة.

فتح الحزمة

k this deck

34

Which of the following procedures relating to the examination of accounts payable could the auditor delegate entirely to the entity's employees?

A) Test footings in the accounts payable ledger.

B) Reconcile unpaid invoices to vendors' statements.

C) Prepare a schedule of accounts payable.

D) Mail confirmations for selected account balances.

A) Test footings in the accounts payable ledger.

B) Reconcile unpaid invoices to vendors' statements.

C) Prepare a schedule of accounts payable.

D) Mail confirmations for selected account balances.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 80 في هذه المجموعة.

فتح الحزمة

k this deck

35

With respect to a small company's system of purchasing supplies,an auditor's primary concern should be to obtain satisfaction that supplies ordered and paid for have been

A) requested and approved by authorized individuals who have no incompatible duties.

B) received, counted, and checked to quantities and amounts on purchase orders and invoices.

C) properly recorded as assets and systematically amortized over the estimated useful life of the supplies.

D) used in the course of business and solely for business purposes during the year under audit.

A) requested and approved by authorized individuals who have no incompatible duties.

B) received, counted, and checked to quantities and amounts on purchase orders and invoices.

C) properly recorded as assets and systematically amortized over the estimated useful life of the supplies.

D) used in the course of business and solely for business purposes during the year under audit.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 80 في هذه المجموعة.

فتح الحزمة

k this deck

36

An auditor compares information on canceled checks with information contained in the cash disbursements journal.The objective of this test is to determine that

A) recorded cash disbursement transactions are properly authorized.

B) proper cash purchase discounts have been recorded.

C) cash disbursements are for goods and services actually received.

D) no discrepancies exist between the data on the checks and the data in the journal.

A) recorded cash disbursement transactions are properly authorized.

B) proper cash purchase discounts have been recorded.

C) cash disbursements are for goods and services actually received.

D) no discrepancies exist between the data on the checks and the data in the journal.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 80 في هذه المجموعة.

فتح الحزمة

k this deck

37

Which of the following procedures would an auditor most likely perform in searching for unrecorded payables?

A) Reconcile receiving reports with related cash payments made just prior to year-end.

B) Contrast the ratio of accounts payable to purchases with the prior year's ratio.

C) Vouch a sample of creditor balances to supporting invoices, receiving reports and purchase orders.

D) Compare cash payments occurring after the balance sheet date with the accounts payable trial balance.

A) Reconcile receiving reports with related cash payments made just prior to year-end.

B) Contrast the ratio of accounts payable to purchases with the prior year's ratio.

C) Vouch a sample of creditor balances to supporting invoices, receiving reports and purchase orders.

D) Compare cash payments occurring after the balance sheet date with the accounts payable trial balance.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 80 في هذه المجموعة.

فتح الحزمة

k this deck

38

An internal control questionnaire indicates that an approved receiving report is required to accompany every check request for payment of merchandise.Which of the following procedures provides the greatest assurance that this control is operating effectively?

A) Select and examine receiving reports and ascertain that the related canceled checks are dated no earlier than the receiving reports.

B) Select and examine receiving reports and ascertain that the related canceled checks are dated no later than the receiving reports.

C) Select and examine canceled checks and ascertain that the related receiving reports are dated no earlier than the checks.

D) Select and examine canceled checks and ascertain that the related receiving reports are dated no later than the checks.

A) Select and examine receiving reports and ascertain that the related canceled checks are dated no earlier than the receiving reports.

B) Select and examine receiving reports and ascertain that the related canceled checks are dated no later than the receiving reports.

C) Select and examine canceled checks and ascertain that the related receiving reports are dated no earlier than the checks.

D) Select and examine canceled checks and ascertain that the related receiving reports are dated no later than the checks.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 80 في هذه المجموعة.

فتح الحزمة

k this deck

39

A voucher

A) is a bill from the vendor.

B) is a document that records the receipt of goods.

C) is a document that requests goods from an authorized individual in the entity.

D) serves as the basis for recording a vendor's invoice in the purchases journal.

A) is a bill from the vendor.

B) is a document that records the receipt of goods.

C) is a document that requests goods from an authorized individual in the entity.

D) serves as the basis for recording a vendor's invoice in the purchases journal.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 80 في هذه المجموعة.

فتح الحزمة

k this deck

40

An entity erroneously recorded a large purchase twice.Which of the following internal controls would be most likely to detect this error in a timely and efficient manner?

A) Footing the purchases journal.

B) Reconciling vendors' monthly statements with subsidiary payable ledger accounts.

C) Tracing totals from the purchases journal to the ledger accounts.

D) Sending written quarterly confirmations to all vendors.

A) Footing the purchases journal.

B) Reconciling vendors' monthly statements with subsidiary payable ledger accounts.

C) Tracing totals from the purchases journal to the ledger accounts.

D) Sending written quarterly confirmations to all vendors.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 80 في هذه المجموعة.

فتح الحزمة

k this deck

41

An entity's internal control requires that for every check request there be an approved voucher,supported by a prenumbered purchase order and a prenumbered receiving report.To determine whether checks are being issued for unauthorized expenditures,an auditor most likely would select items for testing from the population of all

A) purchase orders.

B) canceled checks.

C) receiving reports.

D) approved vouchers.

A) purchase orders.

B) canceled checks.

C) receiving reports.

D) approved vouchers.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 80 في هذه المجموعة.

فتح الحزمة

k this deck

42

Substantive procedures to examine the completeness assertion for accounts payable include

A) selecting a sample of vouchers and agreeing them to authorized purchase orders.

B) selecting a sample of vouchers and tracing them to the purchases journal.

C) comparing dates on vouchers to dates in the purchases journal.

D) recomputing the mathematical accuracy of a sample of vendor invoices.

A) selecting a sample of vouchers and agreeing them to authorized purchase orders.

B) selecting a sample of vouchers and tracing them to the purchases journal.

C) comparing dates on vouchers to dates in the purchases journal.

D) recomputing the mathematical accuracy of a sample of vendor invoices.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 80 في هذه المجموعة.

فتح الحزمة

k this deck

43

In auditing accounts payable,an auditor's procedures most likely would focus primarily on management's assertion of

A) existence.

B) rights and obligations.

C) completeness.

D) valuation and allocation.

A) existence.

B) rights and obligations.

C) completeness.

D) valuation and allocation.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 80 في هذه المجموعة.

فتح الحزمة

k this deck

44

An auditor wishes to perform tests of controls on an entity's cash disbursements procedures.If the control activities leave no audit trail of documentary evidence,the auditor most likely will test the procedures by

A) inquiry and analytical procedures.

B) confirmation and observation.

C) observation and inquiry.

D) analytical procedures and confirmation.

A) inquiry and analytical procedures.

B) confirmation and observation.

C) observation and inquiry.

D) analytical procedures and confirmation.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 80 في هذه المجموعة.

فتح الحزمة

k this deck

45

Budd,the purchasing agent for Lake Hardware Wholesalers,has a relative who owns a retail hardware store.Budd arranged for hardware to be delivered by manufacturers to the retail store on a

A) purchase requisitions.

B) cash receipts.

C) perpetual inventory records.

C)O.D. basis, thereby enabling his relative to buy at Lake's wholesale prices. Budd was probably able to accomplish this because of Lake's poor internal control over

D) purchase orders.

A) purchase requisitions.

B) cash receipts.

C) perpetual inventory records.

C)O.D. basis, thereby enabling his relative to buy at Lake's wholesale prices. Budd was probably able to accomplish this because of Lake's poor internal control over

D) purchase orders.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 80 في هذه المجموعة.

فتح الحزمة

k this deck

46

If completeness is a concern for accounts payable,auditors will send accounts payable confirmations to

A) primarily vendors with large accounts payable balances.

B) primarily vendors with small or zero accounts payable balances.

C) all vendors.

D) a random sample of all vendors.

A) primarily vendors with large accounts payable balances.

B) primarily vendors with small or zero accounts payable balances.

C) all vendors.

D) a random sample of all vendors.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 80 في هذه المجموعة.

فتح الحزمة

k this deck

47

An auditor traced a sample of purchase orders and the related receiving reports to the purchases journal and the cash disbursements journal.The purpose of this substantive procedure most likely was to

A) identify unusually large purchases that should be investigated further.

B) verify that cash disbursements were for goods actually received.

C) determine that purchases were properly recorded.

D) test whether payments were for goods actually ordered.

A) identify unusually large purchases that should be investigated further.

B) verify that cash disbursements were for goods actually received.

C) determine that purchases were properly recorded.

D) test whether payments were for goods actually ordered.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 80 في هذه المجموعة.

فتح الحزمة

k this deck

48

Which of the following control activities is not usually performed in the accounts payable department?

A) Determining the mathematical accuracy of the vendor's invoice.

B) Having an authorized person approve the voucher.

C) Controlling the mailing of the check and remittance advice.

D) Matching the receiving report with the purchase order.

A) Determining the mathematical accuracy of the vendor's invoice.

B) Having an authorized person approve the voucher.

C) Controlling the mailing of the check and remittance advice.

D) Matching the receiving report with the purchase order.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 80 في هذه المجموعة.

فتح الحزمة

k this deck

49

When an auditor selects a sample of items from the vouchers payable register for the last month of the period under audit and traces these items to underlying documents,the auditor is gathering evidence primarily in support of the assertion that

A) recorded obligations were paid.

B) incurred obligations were recorded in the correct period.

C) recorded obligations were valid.

D) cash disbursements were recorded as incurred obligations.

A) recorded obligations were paid.

B) incurred obligations were recorded in the correct period.

C) recorded obligations were valid.

D) cash disbursements were recorded as incurred obligations.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 80 في هذه المجموعة.

فتح الحزمة

k this deck

50

When searching for unrecorded liabilities at year-end,the population identified for sampling would be

A) cash receipts from related parties recorded before year-end.

B) creditors whose accounts appear on a subsidiary trial balance of accounts payable.

C) cash disbursements recorded in the period subsequent to year-end.

D) invoices dated a few days before and after year-end.

A) cash receipts from related parties recorded before year-end.

B) creditors whose accounts appear on a subsidiary trial balance of accounts payable.

C) cash disbursements recorded in the period subsequent to year-end.

D) invoices dated a few days before and after year-end.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 80 في هذه المجموعة.

فتح الحزمة

k this deck

51

To provide assurance that each voucher is submitted and paid only once,an auditor most likely would examine a sample of paid vouchers and determine whether each voucher is

A) supported by a vendor's invoice.

B) stamped "paid" by the check signer.

C) prenumbered and accounted for.

D) approved for authorized purchases.

A) supported by a vendor's invoice.

B) stamped "paid" by the check signer.

C) prenumbered and accounted for.

D) approved for authorized purchases.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 80 في هذه المجموعة.

فتح الحزمة

k this deck

52

Which of the following procedures would an auditor least likely perform before the balance sheet date?

A) Assessment of inherent risk.

B) Observation of merchandise inventory.

C) Assessment of control risk.

D) Identification of related parties.

A) Assessment of inherent risk.

B) Observation of merchandise inventory.

C) Assessment of control risk.

D) Identification of related parties.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 80 في هذه المجموعة.

فتح الحزمة

k this deck

53

Accounts payable confirmations are used to test

A) both the existence and completeness audit assertions.

B) only the existence audit assertion.

C) only the completeness audit assertion.

D) either existence or completeness, depending upon the response rate.

A) both the existence and completeness audit assertions.

B) only the existence audit assertion.

C) only the completeness audit assertion.

D) either existence or completeness, depending upon the response rate.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 80 في هذه المجموعة.

فتح الحزمة

k this deck

54

An examination of the balance in the accounts payable account is ordinarily not designed to

A) determine that the amounts represent obligations of the company.

B) verify that accounts payable were properly authorized.

C) ascertain the reasonableness of recorded liabilities.

D) determine that all existing liabilities at the balance sheet date have been recorded.

A) determine that the amounts represent obligations of the company.

B) verify that accounts payable were properly authorized.

C) ascertain the reasonableness of recorded liabilities.

D) determine that all existing liabilities at the balance sheet date have been recorded.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 80 في هذه المجموعة.

فتح الحزمة

k this deck

55

Which of the following is a substantive procedure that an auditor most likely would perform to verify the existence of recorded accounts payable?

A) Investigating the open purchase order file to ascertain that prenumbered purchase orders are used and accounted for.

B) Receiving the entity's mail, unopened, for a reasonable period of time after the year-end to search for unrecorded vendor's invoices.

C) Vouching selected entries in the accounts payable subsidiary ledger to purchase orders and receiving reports.

D) Confirming accounts payable balances with known suppliers who have zero balances.

A) Investigating the open purchase order file to ascertain that prenumbered purchase orders are used and accounted for.

B) Receiving the entity's mail, unopened, for a reasonable period of time after the year-end to search for unrecorded vendor's invoices.

C) Vouching selected entries in the accounts payable subsidiary ledger to purchase orders and receiving reports.

D) Confirming accounts payable balances with known suppliers who have zero balances.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 80 في هذه المجموعة.

فتح الحزمة

k this deck

56

Which of the following procedures would an auditor most likely perform in searching for unrecorded liabilities?

A) Trace a sample of accounts payable entries recorded just before year-end to the unmatched receiving report file.

B) Compare a sample of purchase orders issued just after year-end with the year-end accounts payable trial balance.

C) Vouch a sample of cash disbursements recorded just after year-end to receiving reports and vendor invoices.

D) Scan the cash disbursements entries recorded just before year-end for indications of unusual transactions.

A) Trace a sample of accounts payable entries recorded just before year-end to the unmatched receiving report file.

B) Compare a sample of purchase orders issued just after year-end with the year-end accounts payable trial balance.

C) Vouch a sample of cash disbursements recorded just after year-end to receiving reports and vendor invoices.

D) Scan the cash disbursements entries recorded just before year-end for indications of unusual transactions.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 80 في هذه المجموعة.

فتح الحزمة

k this deck

57

Substantive procedures to examine the occurrence assertion for accounts payable include

A) selecting a sample of vouchers and agreeing them to authorized purchase orders.

B) selecting a sample of vouchers and tracing them to the purchases journal.

C) comparing dates on vouchers to dates in the purchases journal.

D) recomputing the mathematical accuracy of a sample of vendor invoices.

A) selecting a sample of vouchers and agreeing them to authorized purchase orders.

B) selecting a sample of vouchers and tracing them to the purchases journal.

C) comparing dates on vouchers to dates in the purchases journal.

D) recomputing the mathematical accuracy of a sample of vendor invoices.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 80 في هذه المجموعة.

فتح الحزمة

k this deck

58

Purchase cutoff procedures should be designed to test whether or not all inventory

A) purchased and received before the year-end was recorded before year-end.

B) on the year-end balance sheet was carried at lower of cost or market.

C) on the year-end balance sheet was paid for by the company.

D) owned by the company is in the possession of the company.

A) purchased and received before the year-end was recorded before year-end.

B) on the year-end balance sheet was carried at lower of cost or market.

C) on the year-end balance sheet was paid for by the company.

D) owned by the company is in the possession of the company.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 80 في هذه المجموعة.

فتح الحزمة

k this deck

59

Which of the following is the most effective control activity to detect vouchers prepared for the payment of goods that were not received?

A) Counting of goods upon receipt in the storeroom.

B) Matching of purchase order, receiving report, and vendor invoice for each voucher in the accounts payable department.

C) Comparison of goods received with goods requisitioned in the receiving department.

D) Verification of vouchers for accuracy and approval in the internal audit department.

A) Counting of goods upon receipt in the storeroom.

B) Matching of purchase order, receiving report, and vendor invoice for each voucher in the accounts payable department.

C) Comparison of goods received with goods requisitioned in the receiving department.

D) Verification of vouchers for accuracy and approval in the internal audit department.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 80 في هذه المجموعة.

فتح الحزمة

k this deck

60

Substantive procedures to examine the cutoff assertion for accounts payable include

A) selecting a sample of vouchers and agreeing them to authorized purchase orders.

B) selecting a sample of vouchers and agreeing them to the purchases journal.

C) selecting a sample of receiving reports around year-end and comparing dates on related vouchers to dates in the purchases journal.

D) recomputing the mathematical accuracy of a sample of vendor invoices.

A) selecting a sample of vouchers and agreeing them to authorized purchase orders.

B) selecting a sample of vouchers and agreeing them to the purchases journal.

C) selecting a sample of receiving reports around year-end and comparing dates on related vouchers to dates in the purchases journal.

D) recomputing the mathematical accuracy of a sample of vendor invoices.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 80 في هذه المجموعة.

فتح الحزمة

k this deck

61

Listed below are six assertions regarding the financial presentations made in the purchasing process.For each,give an example of how an auditor could use one of the typical documents in the purchasing process to test the assertion.

Occurrence

Completeness

Authorization

Accuracy

Cutoff

Classification

Occurrence

Completeness

Authorization

Accuracy

Cutoff

Classification

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 80 في هذه المجموعة.

فتح الحزمة

k this deck

62

Which of the following is an internal control that would prevent a paid disbursement voucher from being presented for payment a second time?

A) Vouchers should be prepared by individuals who are responsible for signing disbursement checks.

B) Disbursement vouchers should be approved by at least two responsible management officials.

C) The date on a disbursement voucher should be within a few days of the date the voucher is presented for payment.

D) The official signing the check should compare the check with the voucher and should "cancel" the voucher documents by marking them "paid."

A) Vouchers should be prepared by individuals who are responsible for signing disbursement checks.

B) Disbursement vouchers should be approved by at least two responsible management officials.

C) The date on a disbursement voucher should be within a few days of the date the voucher is presented for payment.

D) The official signing the check should compare the check with the voucher and should "cancel" the voucher documents by marking them "paid."

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 80 في هذه المجموعة.

فتح الحزمة

k this deck

63

Assertions about classes of transactions and events for the period under audit include

A) existence, completeness, and accuracy.

B) existence, completeness, and classification.

C) occurrence, completeness, and cutoff.

D) occurrence, completeness, and valuation and allocation.

A) existence, completeness, and accuracy.

B) existence, completeness, and classification.

C) occurrence, completeness, and cutoff.

D) occurrence, completeness, and valuation and allocation.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 80 في هذه المجموعة.

فتح الحزمة

k this deck

64

Which of the following questions would most likely be included in an internal control questionnaire concerning the completeness assertion for purchases?

A) Is an authorized purchase order required before the receiving department can accept a shipment or the vouchers payable department can record a voucher?

B) Are purchase requisitions prenumbered and independently matched with vendor invoices?

C) Is the unpaid voucher file periodically reconciled with inventory records by an employee who does not have access to purchase requisitions?

D) Are purchase orders, receiving reports, and vouchers prenumbered and periodically accounted for?

A) Is an authorized purchase order required before the receiving department can accept a shipment or the vouchers payable department can record a voucher?

B) Are purchase requisitions prenumbered and independently matched with vendor invoices?

C) Is the unpaid voucher file periodically reconciled with inventory records by an employee who does not have access to purchase requisitions?

D) Are purchase orders, receiving reports, and vouchers prenumbered and periodically accounted for?

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 80 في هذه المجموعة.

فتح الحزمة

k this deck

65

Match the test of controls described below to the appropriate assertion it is used to test.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 80 في هذه المجموعة.

فتح الحزمة

k this deck

66

Which of the following describes a temporary difference?

A) A difference that will be corrected in an amended tax return.

B) A difference arising from an uncertain tax position.

C) A fundamental difference in what constitutes revenue or expense for GAAP and tax purposes.

D) A timing difference between the recognition of revenue or expense under GAAP and tax purposes.

A) A difference that will be corrected in an amended tax return.

B) A difference arising from an uncertain tax position.

C) A fundamental difference in what constitutes revenue or expense for GAAP and tax purposes.

D) A timing difference between the recognition of revenue or expense under GAAP and tax purposes.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 80 في هذه المجموعة.

فتح الحزمة

k this deck

67

Which of the following describes a permanent difference?

A) A difference that will be corrected in an amended tax return.

B) A difference arising from an uncertain tax position.

C) A fundamental difference in what constitutes revenue or expense for GAAP and tax purposes.

D) A timing difference between the recognition of revenue or expense under GAAP and tax purposes.

A) A difference that will be corrected in an amended tax return.

B) A difference arising from an uncertain tax position.

C) A fundamental difference in what constitutes revenue or expense for GAAP and tax purposes.

D) A timing difference between the recognition of revenue or expense under GAAP and tax purposes.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 80 في هذه المجموعة.

فتح الحزمة

k this deck

68

If payables turnover has increased significantly since the prior year,this is an indication that which of the following assertions for accounts payable might be violated?

A) Existence or occurrence.

B) Completeness.

C) Rights and obligations.

D) Valuation and allocation.

A) Existence or occurrence.

B) Completeness.

C) Rights and obligations.

D) Valuation and allocation.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 80 في هذه المجموعة.

فتح الحزمة

k this deck

69

The key inherent risk factors an auditor must consider when auditing the purchasing process are industry factors.Which two are most important and why?

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 80 في هذه المجموعة.

فتح الحزمة

k this deck

70

The auditor can often obtain sufficient appropriate evidence in the audit of a tax provision without the use of a specialist.However,several situations may indicate a need for the auditor to involve a tax specialist.Identify three of these situations.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 80 في هذه المجموعة.

فتح الحزمة

k this deck

71

Which of the following test(s)of details of transactions can be used as a dual-purpose test in conjunction with tests of controls?

A) Test a sample of purchase requisitions for proper authorization.

B) Obtain selected vendors' statements and reconcile to vendor accounts.

C) Obtain listing of accounts payable and compare total to general ledger.

D) Review results of confirmations of selected accounts payable.

A) Test a sample of purchase requisitions for proper authorization.

B) Obtain selected vendors' statements and reconcile to vendor accounts.

C) Obtain listing of accounts payable and compare total to general ledger.

D) Review results of confirmations of selected accounts payable.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 80 في هذه المجموعة.

فتح الحزمة

k this deck

72

Identify the primary functions in the purchases cycle and describe each function.

Functions in the purchasing process include:

Functions in the purchasing process include:

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 80 في هذه المجموعة.

فتح الحزمة

k this deck

73

Assertions about account balances at the period end include

A) existence, completeness, and accuracy.

B) existence, completeness, and classification.

C) existence, rights and obligations, and completeness.

D) existence, rights and obligations, and classification.

A) existence, completeness, and accuracy.

B) existence, completeness, and classification.

C) existence, rights and obligations, and completeness.

D) existence, rights and obligations, and classification.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 80 في هذه المجموعة.

فتح الحزمة

k this deck

74

Identify the types of substantive procedures used by the auditor to test accounts payable and accrued expenses.Provide an example of how the auditor may use each substantive procedure.Identify if any of the substantive procedures can be used as a test of controls or a dual-purpose test.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 80 في هذه المجموعة.

فتح الحزمة

k this deck

75

Listed below are the major functions of the purchasing process.

1)Purchasing function.

2)General ledger function.

3)Invoice-processing function.

4)Disbursement function.

5)Accounts payable function.

6)Requisition and receiving function.

Name four pairs of functions that should be segregated from each other and explain why the segregation is important.

1)Purchasing function.

2)General ledger function.

3)Invoice-processing function.

4)Disbursement function.

5)Accounts payable function.

6)Requisition and receiving function.

Name four pairs of functions that should be segregated from each other and explain why the segregation is important.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 80 في هذه المجموعة.

فتح الحزمة

k this deck

76

The mailing of disbursement checks and remittance advices should be controlled by the employee who

A) signed the checks last.

B) approved the vouchers for payment.

C) matched the receiving reports, purchase orders and vendors' invoices.

D) verified the mathematical accuracy of the vouchers and remittance advices.

A) signed the checks last.

B) approved the vouchers for payment.

C) matched the receiving reports, purchase orders and vendors' invoices.

D) verified the mathematical accuracy of the vouchers and remittance advices.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 80 في هذه المجموعة.

فتح الحزمة

k this deck

77

Which type of confirmation is used more frequently by auditors―accounts receivable confirmations or accounts payable confirmations? Why?

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 80 في هذه المجموعة.

فتح الحزمة

k this deck

78

Describe three categories of expenses outlined in FASB Concept Statement No.5.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 80 في هذه المجموعة.

فتح الحزمة

k this deck

79

Identify whether the following tests are substantive analytical procedures,tests of details of transactions,or tests of details of account balances:

1)Test a sample of purchase requisitions for proper authorization.

2)Test transactions around year-end to determine if they are recorded in the proper period.

3)Review results of confirmation of selected accounts payable.

4)Compare payables turnover to previous years' data.

5)Obtain selected vendors' statements and reconcile to vendor accounts.

6)Compare purchase returns and allowances as a percentage of revenue or cost of sales to industry data.

1)Test a sample of purchase requisitions for proper authorization.

2)Test transactions around year-end to determine if they are recorded in the proper period.

3)Review results of confirmation of selected accounts payable.

4)Compare payables turnover to previous years' data.

5)Obtain selected vendors' statements and reconcile to vendor accounts.

6)Compare purchase returns and allowances as a percentage of revenue or cost of sales to industry data.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 80 في هذه المجموعة.

فتح الحزمة

k this deck

80

There are several important disclosure items to consider when auditing the purchasing process.Discuss what they are and why they are important.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 80 في هذه المجموعة.

فتح الحزمة

k this deck

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 80 في هذه المجموعة.