Deck 20: Performance Evaluation of Managed Funds

ملء الشاشة (f)

سؤال

سؤال

Which of the following relies upon the security market line?

سؤال

Which of the following assumes that the CAPM is the appropriate benchmark?

سؤال

سؤال

Which of the following is based upon the capital market line?

سؤال

سؤال

سؤال

A tracking error is one way that an index portfolio manager's performance can be evaluated.Two such measures that compare this are:

سؤال

There are several well-known performance measures that have been traditionally used to measure fund performance,such as:

سؤال

For which of the following reasons may a mimicking portfolio fail to accurately track an index?

سؤال

Given a portfolio return of 5%,10%,-2% and 4%,and a tracking portfolio of 6%,7%,2% and 5%,calculate the average absolute tracking performance of the portfolio.

سؤال

سؤال

سؤال

سؤال

A criticism of Jensen's alpha is that:

سؤال

سؤال

A portfolio with a beta of 0.5 has a return of 5% and a standard deviation of 10%.If the risk-free rate is 2% and the market return is 9%,calculate the Jensen's alpha measure for the portfolio.

سؤال

Carhart's Alpha is a measure of enhanced operation after controlling for the forces generated by:

سؤال

سؤال

سؤال

Robson (1986)examines managed funds in Australia over the period 1969-78 and reports generally _________values of Jensen's alpha and _________ consistency in performance across time.

سؤال

The performance persistence study by Carhart in 1997 found that persistence could be explained by:

سؤال

An English survey of 2000 investors conducted in 2001 found that ___ of respondents regard performance as the most important factor to consider.

سؤال

Blake,Lehmann and Timmerman (1999)find that the ____ is of prime importance.

سؤال

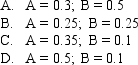

Portfolio A has a return of 5% and a standard deviation of 10%.Portfolio B has a return of 8% and a standard deviation of 12%.If the risk-free rate is 2% portfolio,then the Sharpe indices of A and B are:

سؤال

Faff,Gallagher and Wu (2005)in their research find that fund managers have been ________ to deliver superior returns through _________________,although there is evidence of value enhancement in the Australian equities asset class.

سؤال

You want to evaluate three mutual funds using the Sharpe measure for performance evaluation.The risk-free return during the sample period is 6%.The average returns,standard deviations and betas for the three funds are given below,as is the data for the S&P 500 index.

The fund with the highest Sharpe measure is __________.

A)Fund A

B)Fund B

C)Fund C

D)Funds A and B are tied for highest

The fund with the highest Sharpe measure is __________.

A)Fund A

B)Fund B

C)Fund C

D)Funds A and B are tied for highest

سؤال

سؤال

Blake,Elton and Gruber (1993)find that most bond funds have __________ indicating underperformance.

سؤال

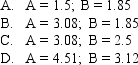

Portfolio A has a return of 9% and a standard deviation of 25%.Portfolio B has a return of 21% and a standard deviation of 33%.If the risk-free rate is 6% portfolio,then the Sharpe indices of A and B are:

سؤال

Dissatisfaction with the traditional performance measures has led to the development of a new generation of performance measures such as

سؤال

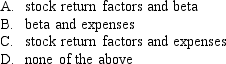

The major criticism of the Sharpe index is that it relies on:

سؤال

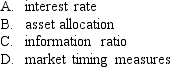

The information ratio is claimed to be an _____________measure.The _____________ requires that a bench mark be specified.

سؤال

The model proposed by Grinblatt and Titman (1989)is called:

سؤال

Volkman and Wohar (1995)find that __________ is associated with low management fees,whereas __________ tends to be associated with funds charging high management fees.

سؤال

The window of superior performance is:

سؤال

Studies appear to exhibit mild evidence that well performing funds exhibit performance __________,but stronger evidence that poor performing funds __________.

سؤال

A portfolio with a beta of 1.7 has a return of 15% and a standard deviation of 10%.If the risk-free rate is 5% and the market return is 119%,calculate the Jensen's alpha measure for the portfolio.

سؤال

Portfolio A has a return of 41% and a standard deviation of 25%.Portfolio B has a return of 21% and a standard deviation of 6%.If the risk-free rate is 4% portfolio,then the Sharpe indices of A and B are:

سؤال

Droms and Walker (1994)find no evidence of consistent __________ performance of international equity funds.

فتح الحزمة

قم بالتسجيل لفتح البطاقات في هذه المجموعة!

Unlock Deck

Unlock Deck

1/40

العب

ملء الشاشة (f)

Deck 20: Performance Evaluation of Managed Funds

1

The Treynor measure differs from the Sharpe index,because it uses beta risk rather than standard deviation as the risk measure.

True

Explanation: The Treynor (1965)index is very similar to the Sharpe index,except that it is based on the ex-post security market line (rather than the ex-post capital market line).The result is that the standardised measure is beta risk rather than standard deviation.

Explanation: The Treynor (1965)index is very similar to the Sharpe index,except that it is based on the ex-post security market line (rather than the ex-post capital market line).The result is that the standardised measure is beta risk rather than standard deviation.

2

Which of the following relies upon the security market line?

A

Explanation: Jensen's alpha relies upon the security market line.

Explanation: Jensen's alpha relies upon the security market line.

3

Which of the following assumes that the CAPM is the appropriate benchmark?

A

Explanation: Jensen's (1968)alpha relies upon the security market line.According to equation 20.4,page 688,the ex-post capital asset pricing model (CAPM)can be expressed as:

Explanation: Jensen's (1968)alpha relies upon the security market line.According to equation 20.4,page 688,the ex-post capital asset pricing model (CAPM)can be expressed as:

4

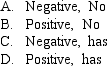

The reward-to-variability ratio is another name for the Treynor index.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 40 في هذه المجموعة.

فتح الحزمة

k this deck

5

Which of the following is based upon the capital market line?

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 40 في هذه المجموعة.

فتح الحزمة

k this deck

6

The Treynor measure captures the risk-premium per unit of overall risk.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 40 في هذه المجموعة.

فتح الحزمة

k this deck

7

Funds persistence states that when using past fund rankings it is never useful in predicting future ranking.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 40 في هذه المجموعة.

فتح الحزمة

k this deck

8

A tracking error is one way that an index portfolio manager's performance can be evaluated.Two such measures that compare this are:

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 40 في هذه المجموعة.

فتح الحزمة

k this deck

9

There are several well-known performance measures that have been traditionally used to measure fund performance,such as:

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 40 في هذه المجموعة.

فتح الحزمة

k this deck

10

For which of the following reasons may a mimicking portfolio fail to accurately track an index?

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 40 في هذه المجموعة.

فتح الحزمة

k this deck

11

Given a portfolio return of 5%,10%,-2% and 4%,and a tracking portfolio of 6%,7%,2% and 5%,calculate the average absolute tracking performance of the portfolio.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 40 في هذه المجموعة.

فتح الحزمة

k this deck

12

Allen,Brailsford,Faff and Soucik (2005)compare performance measurement models across nine benchmark definitions using a large sample of Australian equity funds.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 40 في هذه المجموعة.

فتح الحزمة

k this deck

13

Treynor and Mazuy model active managers' market timing ability by introducing a quadratic term.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 40 في هذه المجموعة.

فتح الحزمة

k this deck

14

Portfolio A has a return of 8% and a standard deviation of 10%.Portfolio B has a return of 12% and a standard deviation of 15%.If the risk-free rate is 4%,portfolio A has the highest Sharpe index.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 40 في هذه المجموعة.

فتح الحزمة

k this deck

15

A criticism of Jensen's alpha is that:

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 40 في هذه المجموعة.

فتح الحزمة

k this deck

16

Past performance is not useful for funds managers.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 40 في هذه المجموعة.

فتح الحزمة

k this deck

17

A portfolio with a beta of 0.5 has a return of 5% and a standard deviation of 10%.If the risk-free rate is 2% and the market return is 9%,calculate the Jensen's alpha measure for the portfolio.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 40 في هذه المجموعة.

فتح الحزمة

k this deck

18

Carhart's Alpha is a measure of enhanced operation after controlling for the forces generated by:

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 40 في هذه المجموعة.

فتح الحزمة

k this deck

19

Henriksson and Merton (1981)measure market timing using the maximum of zero and the market risk premium as a factor.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 40 في هذه المجموعة.

فتح الحزمة

k this deck

20

Sinclair's study in 1990 for Australian mutual funds reports negative returns for market timing.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 40 في هذه المجموعة.

فتح الحزمة

k this deck

21

Robson (1986)examines managed funds in Australia over the period 1969-78 and reports generally _________values of Jensen's alpha and _________ consistency in performance across time.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 40 في هذه المجموعة.

فتح الحزمة

k this deck

22

The performance persistence study by Carhart in 1997 found that persistence could be explained by:

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 40 في هذه المجموعة.

فتح الحزمة

k this deck

23

An English survey of 2000 investors conducted in 2001 found that ___ of respondents regard performance as the most important factor to consider.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 40 في هذه المجموعة.

فتح الحزمة

k this deck

24

Blake,Lehmann and Timmerman (1999)find that the ____ is of prime importance.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 40 في هذه المجموعة.

فتح الحزمة

k this deck

25

Portfolio A has a return of 5% and a standard deviation of 10%.Portfolio B has a return of 8% and a standard deviation of 12%.If the risk-free rate is 2% portfolio,then the Sharpe indices of A and B are:

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 40 في هذه المجموعة.

فتح الحزمة

k this deck

26

Faff,Gallagher and Wu (2005)in their research find that fund managers have been ________ to deliver superior returns through _________________,although there is evidence of value enhancement in the Australian equities asset class.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 40 في هذه المجموعة.

فتح الحزمة

k this deck

27

You want to evaluate three mutual funds using the Sharpe measure for performance evaluation.The risk-free return during the sample period is 6%.The average returns,standard deviations and betas for the three funds are given below,as is the data for the S&P 500 index.

The fund with the highest Sharpe measure is __________.

A)Fund A

B)Fund B

C)Fund C

D)Funds A and B are tied for highest

The fund with the highest Sharpe measure is __________.

A)Fund A

B)Fund B

C)Fund C

D)Funds A and B are tied for highest

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 40 في هذه المجموعة.

فتح الحزمة

k this deck

28

Consider the Sharpe and Treynor performance measures.When a pension fund is large

And has many managers,the __________ measure is better for evaluating individual managers while the __________ measure is better for evaluating the manager of a small fund with only one manager responsible for all investments.

A)Sharpe,Sharpe

B)Sharpe,Treynor

C)Treynor,Sharpe

D)Treynor,Treynor

And has many managers,the __________ measure is better for evaluating individual managers while the __________ measure is better for evaluating the manager of a small fund with only one manager responsible for all investments.

A)Sharpe,Sharpe

B)Sharpe,Treynor

C)Treynor,Sharpe

D)Treynor,Treynor

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 40 في هذه المجموعة.

فتح الحزمة

k this deck

29

Blake,Elton and Gruber (1993)find that most bond funds have __________ indicating underperformance.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 40 في هذه المجموعة.

فتح الحزمة

k this deck

30

Portfolio A has a return of 9% and a standard deviation of 25%.Portfolio B has a return of 21% and a standard deviation of 33%.If the risk-free rate is 6% portfolio,then the Sharpe indices of A and B are:

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 40 في هذه المجموعة.

فتح الحزمة

k this deck

31

Dissatisfaction with the traditional performance measures has led to the development of a new generation of performance measures such as

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 40 في هذه المجموعة.

فتح الحزمة

k this deck

32

The major criticism of the Sharpe index is that it relies on:

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 40 في هذه المجموعة.

فتح الحزمة

k this deck

33

The information ratio is claimed to be an _____________measure.The _____________ requires that a bench mark be specified.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 40 في هذه المجموعة.

فتح الحزمة

k this deck

34

The model proposed by Grinblatt and Titman (1989)is called:

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 40 في هذه المجموعة.

فتح الحزمة

k this deck

35

Volkman and Wohar (1995)find that __________ is associated with low management fees,whereas __________ tends to be associated with funds charging high management fees.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 40 في هذه المجموعة.

فتح الحزمة

k this deck

36

The window of superior performance is:

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 40 في هذه المجموعة.

فتح الحزمة

k this deck

37

Studies appear to exhibit mild evidence that well performing funds exhibit performance __________,but stronger evidence that poor performing funds __________.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 40 في هذه المجموعة.

فتح الحزمة

k this deck

38

A portfolio with a beta of 1.7 has a return of 15% and a standard deviation of 10%.If the risk-free rate is 5% and the market return is 119%,calculate the Jensen's alpha measure for the portfolio.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 40 في هذه المجموعة.

فتح الحزمة

k this deck

39

Portfolio A has a return of 41% and a standard deviation of 25%.Portfolio B has a return of 21% and a standard deviation of 6%.If the risk-free rate is 4% portfolio,then the Sharpe indices of A and B are:

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 40 في هذه المجموعة.

فتح الحزمة

k this deck

40

Droms and Walker (1994)find no evidence of consistent __________ performance of international equity funds.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 40 في هذه المجموعة.

فتح الحزمة

k this deck

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 40 في هذه المجموعة.