Deck 3: Consolidation: Wholly Owned Subsidiaries

ملء الشاشة (f)

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

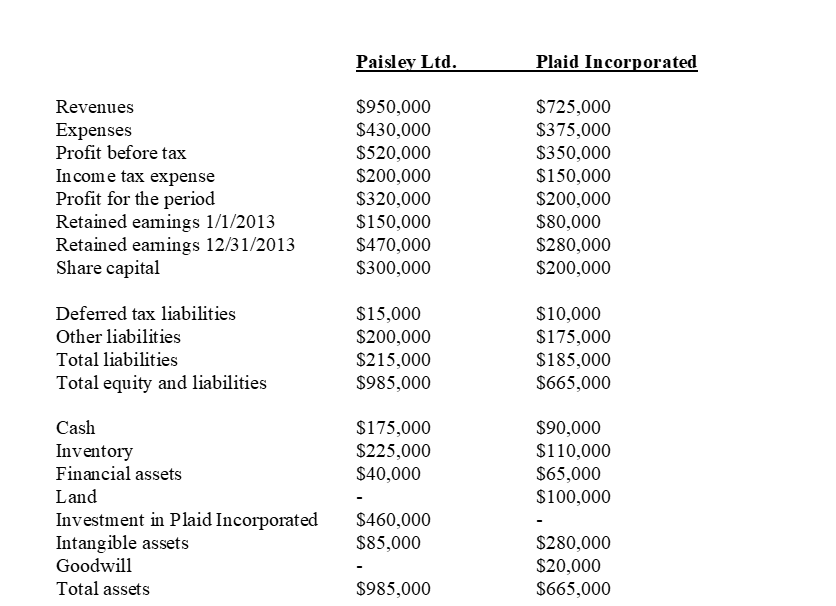

On January 1, 2013 Paisley Ltd. Acquired 100% of the issued shares of Plaid Incorporated. The fair value of the consideration paid was measured at $460,000. At this date, records of Plaid Incorporated included the following information:

As at January 1, 2013, all the identifiable assets and liabilities of Plaid were recorded in the subsidiary's books at fair value except for the following assets:

As at January 1, 2013, all the identifiable assets and liabilities of Plaid were recorded in the subsidiary's books at fair value except for the following assets:

The inventory was all sold by December 31, 2013. The land is still remaining with Plaid as at December 31, 2013. Goodwill has not been deemed to be impaired. The tax rate is 40%.

The inventory was all sold by December 31, 2013. The land is still remaining with Plaid as at December 31, 2013. Goodwill has not been deemed to be impaired. The tax rate is 40%.

The summarized financial statements of both entities as at December 31, 2013 are shown below.

Required:.

Prepare the consolidated financial statements of Paisley Ltd. As at December 31, 2013.

As at January 1, 2013, all the identifiable assets and liabilities of Plaid were recorded in the subsidiary's books at fair value except for the following assets: The inventory was all sold by December 31, 2013. The land is still remaining with Plaid as at December 31, 2013. Goodwill has not been deemed to be impaired. The tax rate is 40%.The summarized financial statements of both entities as at December 31, 2013 are shown below.

Required:.

Prepare the consolidated financial statements of Paisley Ltd. As at December 31, 2013.

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

On January 1, 2012 Finn Ltd. Acquired 75% of the shares of Ewe Corporation for $10 per share in cash. The equity of Ewe as at that date was:

Finn had previously acquired 25% of the shares of Ewe for $10,000. The fair value of this investment as at January 1, 2012 was $50,000.

Finn had previously acquired 25% of the shares of Ewe for $10,000. The fair value of this investment as at January 1, 2012 was $50,000.

At the acquisition date all of the identifiable assets and liabilities of Ewe were recorded at fair value except for a plant and inventory, whose carrying amounts were $15,000 and $5,000 respectively less than their fair value. All of the inventory was subsequently sold during 2012 and the plant had a remaining useful life at the acquisition date of 5 years. The tax rate is 40%.

Ewe had been actively researching a new process, which is part of the reason why Finn acquired the remaining outstanding shares of Ewe. Finn estimated the value of this intangible to be $10,000 and that it would have an indefinite useful life.

Required: Prepare the acquisition analysis and the consolidation adjustments of Finn and Ewe as at December 31, 2013.

Finn had previously acquired 25% of the shares of Ewe for $10,000. The fair value of this investment as at January 1, 2012 was $50,000.At the acquisition date all of the identifiable assets and liabilities of Ewe were recorded at fair value except for a plant and inventory, whose carrying amounts were $15,000 and $5,000 respectively less than their fair value. All of the inventory was subsequently sold during 2012 and the plant had a remaining useful life at the acquisition date of 5 years. The tax rate is 40%.

Ewe had been actively researching a new process, which is part of the reason why Finn acquired the remaining outstanding shares of Ewe. Finn estimated the value of this intangible to be $10,000 and that it would have an indefinite useful life.

Required: Prepare the acquisition analysis and the consolidation adjustments of Finn and Ewe as at December 31, 2013.

سؤال

سؤال

فتح الحزمة

قم بالتسجيل لفتح البطاقات في هذه المجموعة!

Unlock Deck

Unlock Deck

1/56

العب

ملء الشاشة (f)

Deck 3: Consolidation: Wholly Owned Subsidiaries

1

Fair value increments on depreciable assets should be amortized in accordance with the subsidiary's depreciation policies.

True

2

If a consolidation is done at the day of acquisition, only the ______________ need be adjusted since all of the subsidiaries equity will be pre-acquisition and therefore eliminated.

A)statement of financial position

B)income statement

C)cash flow statement

D)statement of changes in equity.

A)statement of financial position

B)income statement

C)cash flow statement

D)statement of changes in equity.

A

3

The pre-acquisition adjustments are required to eliminate the carrying amount of the parent's investment in the subsidiary and the parent's portion of pre-acquisition equity.

True

4

The goodwill impairment test does not involve elimination of all goodwill as a consequence.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 56 في هذه المجموعة.

فتح الحزمة

k this deck

5

The first step in the consolidation process, regardless of which year is being reported, is to undertake the eliminations.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 56 في هذه المجموعة.

فتح الحزمة

k this deck

6

The starting point for the preparation of the consolidated financial statements is the parent company's individual statements at year end.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 56 في هذه المجموعة.

فتح الحزمة

k this deck

7

Fair value adjustments (FVAs)are used to recognize the identifiable assets and liabilities of the subsidiary at fair values and goodwill measured as a residual amount.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 56 في هذه المجموعة.

فتح الحزمة

k this deck

8

A parent can acquire the shares in a subsidiary on a "cum div." or an "ex div." basis.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 56 في هذه المجموعة.

فتح الحزمة

k this deck

9

A parent company can report an investment in its subsidiary on its Separate financial statements under either the cost or equity method.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 56 في هذه المجموعة.

فتح الحزمة

k this deck

10

When there is a gain on bargain purchase at the acquisition date, the net fair value of the identifiable assets and liabilities of the subsidiary is less than the consideration transferred.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 56 في هذه المجموعة.

فتح الحزمة

k this deck

11

The fair value adjustments are required to eliminate the carrying amount of the parent's investment in the subsidiary and the parent's portion of pre-acquisition equity.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 56 في هذه المجموعة.

فتح الحزمة

k this deck

12

The consolidation process will involve replacing the investment account that is recorded in the books of the acquirer with the specific net assets acquired from the acquiree.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 56 في هذه المجموعة.

فتح الحزمة

k this deck

13

The consolidation process will involve replacing the investment account that is recorded in the books of the acquirer with the goodwill acquired from the acquiree.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 56 في هذه المجموعة.

فتح الحزمة

k this deck

14

Which of the following statements about the consolidation process is FALSE?

A)The consolidation process will involve replacing the investment account that is recorded in the books of the acquirer with the specific net assets acquired from the acquiree.

B)Consolidation is achieved by combining the financial statements of both the parent and its subsidiary.

C)The consolidated financial statements of a parent and its subsidiary include information about a subsidiary from the date the parent obtains physical possession of the subsidiary.

D)A subsidiary continues to be included in the parent's consolidated financial statements until the parent no longer controls that entity.

A)The consolidation process will involve replacing the investment account that is recorded in the books of the acquirer with the specific net assets acquired from the acquiree.

B)Consolidation is achieved by combining the financial statements of both the parent and its subsidiary.

C)The consolidated financial statements of a parent and its subsidiary include information about a subsidiary from the date the parent obtains physical possession of the subsidiary.

D)A subsidiary continues to be included in the parent's consolidated financial statements until the parent no longer controls that entity.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 56 في هذه المجموعة.

فتح الحزمة

k this deck

15

The acquisition analysis may include the recognition of assets and liabilities not recognized in the records of the subsidiary.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 56 في هذه المجموعة.

فتح الحزمة

k this deck

16

Which of the following statements is true regarding the consolidation process under ASPE?

A)Under ASPE, the parent has the option of not consolidating with its subsidiary.

B)Under ASPE, the parent must consolidate with its subsidiary.

C)Under ASPE, the parent must use the cost or the equity method to account for its subsidiary.

D)None of the above is true.

A)Under ASPE, the parent has the option of not consolidating with its subsidiary.

B)Under ASPE, the parent must consolidate with its subsidiary.

C)Under ASPE, the parent must use the cost or the equity method to account for its subsidiary.

D)None of the above is true.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 56 في هذه المجموعة.

فتح الحزمة

k this deck

17

Since taxes are paid by the individual companies, the CCA claim is based on the amount recorded in the records of the acquiree.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 56 في هذه المجموعة.

فتح الحزمة

k this deck

18

At the date of acquisition, the assets and liabilities of the subsidiary are carried forward into the consolidated statement of financial position at fair value.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 56 في هذه المجموعة.

فتح الحزمة

k this deck

19

Which of the following statements regarding the consolidation process is FALSE?

A)Where the parent entity and the subsidiary have different ends of reporting periods, adjustments must be made to the subsidiary's statements before the preparation of the consolidated financial statements.

B)Because IFRS 3 Business Combinations requires that, under the acquisition method, the identifiable assets and liabilities of the acquirer are to be reported at fair value, fair value adjustments are prepared as part of the consolidation process.

C)Where the parent entity holds shares in the subsidiary, pre-acquisition adjustments are not part of the consolidation process.

D)The consolidation process requires the addition of the financial statements of the parent and its subsidiaries.

A)Where the parent entity and the subsidiary have different ends of reporting periods, adjustments must be made to the subsidiary's statements before the preparation of the consolidated financial statements.

B)Because IFRS 3 Business Combinations requires that, under the acquisition method, the identifiable assets and liabilities of the acquirer are to be reported at fair value, fair value adjustments are prepared as part of the consolidation process.

C)Where the parent entity holds shares in the subsidiary, pre-acquisition adjustments are not part of the consolidation process.

D)The consolidation process requires the addition of the financial statements of the parent and its subsidiaries.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 56 في هذه المجموعة.

فتح الحزمة

k this deck

20

The goodwill impairment test does not involve ________.

A)elimination of all goodwill as a consequence.

B)estimation and judgment on the part of management.

C)an opportunity for a "big bath."

D)an allocation of goodwill to reporting units.

A)elimination of all goodwill as a consequence.

B)estimation and judgment on the part of management.

C)an opportunity for a "big bath."

D)an allocation of goodwill to reporting units.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 56 في هذه المجموعة.

فتح الحزمة

k this deck

21

Fair value increments on depreciable assets ________.

A)should be amortized in accordance with the parent company's depreciation policies.

B)should always be recorded on the subsidiary's books.

C)should be expensed immediately.

D)should be amortized in accordance with the subsidiary's depreciation policies.

A)should be amortized in accordance with the parent company's depreciation policies.

B)should always be recorded on the subsidiary's books.

C)should be expensed immediately.

D)should be amortized in accordance with the subsidiary's depreciation policies.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 56 في هذه المجموعة.

فتح الحزمة

k this deck

22

Which of the following statements regarding pre-acquisition adjustments is FALSE?

A)The adjustments involve the investment account Investment in Subsidiary as shown in the financial statements of the parent.

B)The adjustments involve the equity of the subsidiary at the acquisition date (i.e. the pre-acquisition equity).

C)A deferred tax liability is recognized to increase the goodwill carrying amount.

D)The pre-acquisition adjustment is necessary to avoid overstating the equity and net assets of the group.

A)The adjustments involve the investment account Investment in Subsidiary as shown in the financial statements of the parent.

B)The adjustments involve the equity of the subsidiary at the acquisition date (i.e. the pre-acquisition equity).

C)A deferred tax liability is recognized to increase the goodwill carrying amount.

D)The pre-acquisition adjustment is necessary to avoid overstating the equity and net assets of the group.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 56 في هذه المجموعة.

فتح الحزمة

k this deck

23

The _______________ are required to eliminate the carrying amount of the parent's investment in the subsidiary and the parent's portion of pre-acquisition equity.

A)goodwill calculations

B)fair value adjustments

C)post-acquisition adjustments.

D)pre-acquisition adjustments.

A)goodwill calculations

B)fair value adjustments

C)post-acquisition adjustments.

D)pre-acquisition adjustments.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 56 في هذه المجموعة.

فتح الحزمة

k this deck

24

Which of the following statements regarding consolidated financial statements at the date of acquisition is FALSE?

A)Fair value adjustments are used to recognize the identifiable assets and liabilities of the subsidiary at fair values and goodwill measured as a residual amount.

B)The pre-acquisition adjustments eliminate the pre-acquisition equity of the subsidiary and the investment account recorded by the parent.

C)When the subsidiary has recorded goodwill at acquisition date, adjustments must be made in the acquisition analysis to determine the amount of goodwill to be adjusted in the consolidation process.

D)When the subsidiary has recorded a dividend payable at acquisition date, this must be excluded when calculating the consideration received.

A)Fair value adjustments are used to recognize the identifiable assets and liabilities of the subsidiary at fair values and goodwill measured as a residual amount.

B)The pre-acquisition adjustments eliminate the pre-acquisition equity of the subsidiary and the investment account recorded by the parent.

C)When the subsidiary has recorded goodwill at acquisition date, adjustments must be made in the acquisition analysis to determine the amount of goodwill to be adjusted in the consolidation process.

D)When the subsidiary has recorded a dividend payable at acquisition date, this must be excluded when calculating the consideration received.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 56 في هذه المجموعة.

فتح الحزمة

k this deck

25

Nuworth Co. acquired Wellam Co. in a business combination at December 31, 2012. Wellam has a capital asset that it has been amortizing at a rate of $20,000 per year. At the time of the acquisition, the asset had a book value of $140,000 and a fair value of $154,000. The asset has a remaining life of 7 years. With respect to this asset, how much amortization expense should Nuworth report on its December 31, 2013 consolidated financial statements?

A)$ 2,000

B)$ 5,400

C)$20,000

D)$22,000

A)$ 2,000

B)$ 5,400

C)$20,000

D)$22,000

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 56 في هذه المجموعة.

فتح الحزمة

k this deck

26

Azra Company purchased 100% of the outstanding common shares of Hassan Company on December 31, 2011 for $170,000. At that date, Hassan had $100,000 of outstanding common stock and retained earnings of $30,000. It was agreed that the net assets were fairly valued except that the fair value of the capital assets exceeded their net book value by $20,000 and the carrying value of the inventory exceeded its fair value by $10,000. The capital assets had a remaining useful life of eight years as of the acquisition date and have no salvage value. Inventory turns over four times a year. Both companies pay tax at the rate of 40%. What adjustment should be made to the consolidated financial statements for the year ended December 31, 2014 for the fair value increment related to the capital assets?

A)The retained earnings at January 1, 2014 will be increased by $12,000.

B)Amortization expense on the capital assets for 2014 will be increased by $7,500.

C)Amortization expense on the capital assets for 2014 will be increased by $2,500.

D)Retained earnings at the end of 2014 will be increased by $7,500.

A)The retained earnings at January 1, 2014 will be increased by $12,000.

B)Amortization expense on the capital assets for 2014 will be increased by $7,500.

C)Amortization expense on the capital assets for 2014 will be increased by $2,500.

D)Retained earnings at the end of 2014 will be increased by $7,500.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 56 في هذه المجموعة.

فتح الحزمة

k this deck

27

Kizmit Ltd. acquired Nuance Ltd. in a business combination. One of the main reasons for the acquisition is that Kizmit wanted access to Nuance's extensive customer list. The list is not recorded on Nuance's books and has an estimated value of $100,000 and an estimated life of 7 years. On Kizmit's consolidated statement of financial position, what value should be shown for Nuance's customer list?

A)$0, since it was not recorded on Nuance's books.

B)$100,000 less any accumulated amortization (calculated over 7 years)and any impairment losses.

C)$100,000 less any impairment losses.

D)$100,000 less any accumulated amortization (calculated over 5 years)and any impairment losses.

A)$0, since it was not recorded on Nuance's books.

B)$100,000 less any accumulated amortization (calculated over 7 years)and any impairment losses.

C)$100,000 less any impairment losses.

D)$100,000 less any accumulated amortization (calculated over 5 years)and any impairment losses.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 56 في هذه المجموعة.

فتح الحزمة

k this deck

28

The first step in the consolidation process, regardless of which year is being reported, is to undertake the __________.

A)acquisition analysis.

B)goodwill calculation.

C)eliminations.

D)pre-acquisition adjustments.

A)acquisition analysis.

B)goodwill calculation.

C)eliminations.

D)pre-acquisition adjustments.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 56 في هذه المجموعة.

فتح الحزمة

k this deck

29

Helly Company purchased 100% of the outstanding common shares of Cobra Company on December 31, 2012 for $170,000. At that date, Cobra had $100,000 of outstanding common stock and retained earnings of $30,000. It was agreed that the net assets were fairly valued except that the fair value of the capital assets exceeded their net book value by $20,000 and the carrying value of the inventory exceeded its fair value by $10,000. The capital assets had a remaining useful life of eight years as of the acquisition date and have no salvage value. Inventory turns over four times a year. Both companies pay tax at a rate of 30%. What adjustment should be made to the consolidated financial statements for the year ended December 31, 2013 for the difference in inventory valuation?

A)Cost of goods sold for 2013 will be decreased by $10,000.

B)Retained earnings at the end of 2013 will be decreased by $10,000.

C)Inventory at December 31, 2013 will be decreased by $10,000.

D)Cost of goods sold for 2013 will be increased by $10,000.

A)Cost of goods sold for 2013 will be decreased by $10,000.

B)Retained earnings at the end of 2013 will be decreased by $10,000.

C)Inventory at December 31, 2013 will be decreased by $10,000.

D)Cost of goods sold for 2013 will be increased by $10,000.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 56 في هذه المجموعة.

فتح الحزمة

k this deck

30

The consolidation process will involve replacing the investment account that is recorded in the books of the acquirer with the ____________ acquired from the acquiree.

A)goodwill

B)specific net assets

C)negative goodwill

D)retained earnings.

A)goodwill

B)specific net assets

C)negative goodwill

D)retained earnings.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 56 في هذه المجموعة.

فتح الحزمة

k this deck

31

Inventory was acquired as part of a business combination at the end of 2012. The inventory was sold in 2013. How should the fair value adjustment for the inventory at acquisition be treated for consolidation at the end of 2013?

A)It should be added to sales.

B)It should be added to the cost of goods sold.

C)It should be added to retained earnings.

D)It should be added to inventory.

A)It should be added to sales.

B)It should be added to the cost of goods sold.

C)It should be added to retained earnings.

D)It should be added to inventory.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 56 في هذه المجموعة.

فتح الحزمة

k this deck

32

Sympo Ltd. acquired 100% of the commons shares of Grotto Co. This business combination resulted in $100,000 of goodwill. Sympo allocated the goodwill to three cash-generating units. At its year-end, Sympo conducts a goodwill impairment test. Which of the following statements about the impairment test is TRUE?

A)The impairment test is applied to Grotto Co. as a whole.

B)The impairment test is applied to the business combination as a whole.

C)Sympo is not required to conduct an impairment test unless its circumstances have changed materially from its previous year.

D)The impairment test is applied to each of the three cash-generating units to which goodwill has been allocated.

A)The impairment test is applied to Grotto Co. as a whole.

B)The impairment test is applied to the business combination as a whole.

C)Sympo is not required to conduct an impairment test unless its circumstances have changed materially from its previous year.

D)The impairment test is applied to each of the three cash-generating units to which goodwill has been allocated.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 56 في هذه المجموعة.

فتح الحزمة

k this deck

33

Which of the following statements regarding the acquisition analysis is FALSE?

A)The acquisition analysis may include the recognition of assets and liabilities not recognized in the records of the subsidiary.

B)Differences between carrying amounts and fair values of the identifiable assets and liabilities of the subsidiary at acquisition date are recognized using fair value adjustments.

C)The acquisition analysis will determine whether any goodwill or gain on bargain purchase has arisen as a part of the business combination.

D)Where at acquisition date the parent holds shares in the subsidiary that it has previously acquired before it was a parent, this investment must not be revalued.

A)The acquisition analysis may include the recognition of assets and liabilities not recognized in the records of the subsidiary.

B)Differences between carrying amounts and fair values of the identifiable assets and liabilities of the subsidiary at acquisition date are recognized using fair value adjustments.

C)The acquisition analysis will determine whether any goodwill or gain on bargain purchase has arisen as a part of the business combination.

D)Where at acquisition date the parent holds shares in the subsidiary that it has previously acquired before it was a parent, this investment must not be revalued.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 56 في هذه المجموعة.

فتح الحزمة

k this deck

34

Which of the following is false regarding making adjustments in relation to the content of the subsidiary's financial statements?

A)It is not necessary to make adjustments in relation to the content of the subsidiary's financial statements.

B)If the end of a subsidiary's reporting period does not coincide with the end of the parent's reporting period, adjustments must be made for the effects of significant transactions and events that occur between those dates.

C)The consolidated financial statements are to be prepared using uniform accounting policies for like transactions and other events in similar circumstances.

D)None of the above is false.

A)It is not necessary to make adjustments in relation to the content of the subsidiary's financial statements.

B)If the end of a subsidiary's reporting period does not coincide with the end of the parent's reporting period, adjustments must be made for the effects of significant transactions and events that occur between those dates.

C)The consolidated financial statements are to be prepared using uniform accounting policies for like transactions and other events in similar circumstances.

D)None of the above is false.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 56 في هذه المجموعة.

فتح الحزمة

k this deck

35

A parent can acquire the shares in a subsidiary on a "cum div." or an "ex div." basis. If the shares are acquired on a cum div. basis:

A)The parent is not entitled to the dividend declared at acquisition date.

B)The parent acquires two assets - the investment in the subsidiary and the dividend receivable.

C)The dividend payable recorded by the subsidiary is a liability of the group.

D)Both the dividend receivable and the dividend payable are not eliminated on the consolidated statements.

A)The parent is not entitled to the dividend declared at acquisition date.

B)The parent acquires two assets - the investment in the subsidiary and the dividend receivable.

C)The dividend payable recorded by the subsidiary is a liability of the group.

D)Both the dividend receivable and the dividend payable are not eliminated on the consolidated statements.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 56 في هذه المجموعة.

فتح الحزمة

k this deck

36

IAS 27, Separate Financial Statements, requires an entity that has a subsidiary and that reports on separate financial statements for a special purpose (for tax purposes), in addition to its consolidated statements, show the investment in that subsidiary at __________.

A)cost.

B)fair value.

C)cost or fair value.

D)carrying value.

A)cost.

B)fair value.

C)cost or fair value.

D)carrying value.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 56 في هذه المجموعة.

فتح الحزمة

k this deck

37

Ursula Ltd. has a subsidiary that has an intangible capital asset. It has not been recorded on the subsidiary's books, but at the date of acquisition, the asset had a fair value of $350,000 and an indefinite economic life. How should Ursula show the asset on its consolidated statement of financial position?

A)$350,000 less accumulated amortization (calculated over 10 years)and any impairment losses.

B)$350,000 less accumulated amortization (calculated over 40 years)and any impairment losses.

C)The company should not show the asset on the consolidated financial statement as the subsidiary does not do so.

D)$350,000 less any impairment losses.

A)$350,000 less accumulated amortization (calculated over 10 years)and any impairment losses.

B)$350,000 less accumulated amortization (calculated over 40 years)and any impairment losses.

C)The company should not show the asset on the consolidated financial statement as the subsidiary does not do so.

D)$350,000 less any impairment losses.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 56 في هذه المجموعة.

فتح الحزمة

k this deck

38

When there is a gain on bargain purchase at the acquisition date, the net fair value of the identifiable assets and liabilities of the subsidiary is greater than the consideration transferred. Which of the following statements in this situation is FALSE?

A)The acquirer must firstly reassess the identification and measurement of the subsidiary's identifiable assets and liabilities as well as the measurement of the consideration transferred.

B)The expectation is that the excess of the net fair value over the consideration transferred is usually the result of measurement errors rather than being a real gain to the acquirer.

C)Having confirmed the identification and measurement of both amounts paid and net assets acquired, if an excess still exists, it is recognized immediately in profit as a gain on bargain purchase.

D)Existence of a gain on bargain purchase has no effect on the fair value adjustments when the subsidiary has previously recorded goodwill.

A)The acquirer must firstly reassess the identification and measurement of the subsidiary's identifiable assets and liabilities as well as the measurement of the consideration transferred.

B)The expectation is that the excess of the net fair value over the consideration transferred is usually the result of measurement errors rather than being a real gain to the acquirer.

C)Having confirmed the identification and measurement of both amounts paid and net assets acquired, if an excess still exists, it is recognized immediately in profit as a gain on bargain purchase.

D)Existence of a gain on bargain purchase has no effect on the fair value adjustments when the subsidiary has previously recorded goodwill.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 56 في هذه المجموعة.

فتح الحزمة

k this deck

39

On January 1, 2013 ABC Company, a public company, acquired 100% of XYZ Ltd. The book value approximated fair value at the time of XYZ's assets and liabilities with the exception of their bond payable which had a fair value $10,000 less than its recorded book value and a remaining life of 20 years. Which of the following statements is false?

A)It is not required to use the effective interest rate method, so it may amortize the fair value adjustment on a straight-line basis.

B)The bond payable must be reflected at the amortized cost using the effective interest rate method.

C)Over the remaining life of the debt of 20 years, the interest expense will need to be adjusted annually using the effective interest rate method.

D)None of the above is false.

A)It is not required to use the effective interest rate method, so it may amortize the fair value adjustment on a straight-line basis.

B)The bond payable must be reflected at the amortized cost using the effective interest rate method.

C)Over the remaining life of the debt of 20 years, the interest expense will need to be adjusted annually using the effective interest rate method.

D)None of the above is false.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 56 في هذه المجموعة.

فتح الحزمة

k this deck

40

Yo Ltd. purchased a commercial food preparation system for $150,000 at the beginning of 2012. The estimated economic life of the system is 10 years and Yo uses straight-line amortization. At the beginning of 2014, Tilbury Ltd. acquired Yo in a business combination. At the time of acquisition, Yo's food preparation system had a fair value of $140,000. At the end of 2014, how much amortization expense should Yo report?

A)$0

B)$14,000

C)$15,000

D)$17,500

A)$0

B)$14,000

C)$15,000

D)$17,500

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 56 في هذه المجموعة.

فتح الحزمة

k this deck

41

On January 1, 2013 Paisley Ltd. Acquired 100% of the issued shares of Plaid Incorporated. The fair value of the consideration paid was measured at $460,000. At this date, records of Plaid Incorporated included the following information:

As at January 1, 2013, all the identifiable assets and liabilities of Plaid were recorded in the subsidiary's books at fair value except for the following assets:

The inventory was all sold by December 31, 2013. The land is still remaining with Plaid as at December 31, 2013. Goodwill has not been deemed to be impaired. The tax rate is 40%.

The summarized financial statements of both entities as at December 31, 2013 are shown below.

Required:.

Prepare the consolidated financial statements of Paisley Ltd. As at December 31, 2013.

As at January 1, 2013, all the identifiable assets and liabilities of Plaid were recorded in the subsidiary's books at fair value except for the following assets: The inventory was all sold by December 31, 2013. The land is still remaining with Plaid as at December 31, 2013. Goodwill has not been deemed to be impaired. The tax rate is 40%.The summarized financial statements of both entities as at December 31, 2013 are shown below.

Required:.

Prepare the consolidated financial statements of Paisley Ltd. As at December 31, 2013.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 56 في هذه المجموعة.

فتح الحزمة

k this deck

42

Kayla Ltd. owns 100% of Milos Ltd. Kayla records its investment at cost. Kayla received $300,000 in dividends from Milos. What adjustment should Kayla make on its consolidated financial statements with respect to the dividends?

A)Decrease Dividend income (Kayla): $300,000

Decrease Dividends declared (Milos): $300,000

B)Increase Dividend income (Kayla): $300,000

Increase Dividends declared (Milos): $300,000

C)Decrease Dividends declared (Milos): $300,000

Decrease Investment in Milos (Kayla): $300,000

D)Increase Dividends declared (Milos): $300,000

Increase Investment in Milos (Kayla): $300,000

A)Decrease Dividend income (Kayla): $300,000

Decrease Dividends declared (Milos): $300,000

B)Increase Dividend income (Kayla): $300,000

Increase Dividends declared (Milos): $300,000

C)Decrease Dividends declared (Milos): $300,000

Decrease Investment in Milos (Kayla): $300,000

D)Increase Dividends declared (Milos): $300,000

Increase Investment in Milos (Kayla): $300,000

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 56 في هذه المجموعة.

فتح الحزمة

k this deck

43

Before undertaking the consolidation process, describe the adjustments that may be necessary in relation to the content of the financial statements of the subsidiary.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 56 في هذه المجموعة.

فتح الحزمة

k this deck

44

Which of the following statements regarding consolidated financial statements at the date of acquistion is FALSE?

A)At the day of acquisition, there is a need to prepare a consolidated statement of income.

B)Regarding the equity accounts, only the parent's balances are carried into the consolidated statement of financial position.

C)At acquisition date, all the equity of the subsidiary is pre-acquisition and eliminated.

D)The assets and liabilities of the subsidiary are carried forward into the consolidated statement of financial position at fair value.

A)At the day of acquisition, there is a need to prepare a consolidated statement of income.

B)Regarding the equity accounts, only the parent's balances are carried into the consolidated statement of financial position.

C)At acquisition date, all the equity of the subsidiary is pre-acquisition and eliminated.

D)The assets and liabilities of the subsidiary are carried forward into the consolidated statement of financial position at fair value.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 56 في هذه المجموعة.

فتح الحزمة

k this deck

45

What adjustments are typically needed when consolidated financial statements are prepared at the acquisition date?

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 56 في هذه المجموعة.

فتح الحزمة

k this deck

46

Fair value adjustments (FVAs)are used to recognize the identifiable assets and liabilities of the subsidiary at fair values and goodwill measured as a residual amount. What happens to the fair value adjustments subsequent to the acquisition date?

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 56 في هذه المجموعة.

فتح الحزمة

k this deck

47

What values should be used for the assets, liabilities, and shareholders' equity to start the consolidation process?

A)Carrying values for the parent company and fair values for the subsidiary company.

B)Fair values for the parent company and carrying values for the subsidiary company.

C)Carrying values for both the parent and the subsidiary companies.

D)Fair values for both the parent and the subsidiary companies.

A)Carrying values for the parent company and fair values for the subsidiary company.

B)Fair values for the parent company and carrying values for the subsidiary company.

C)Carrying values for both the parent and the subsidiary companies.

D)Fair values for both the parent and the subsidiary companies.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 56 في هذه المجموعة.

فتح الحزمة

k this deck

48

Carson Company purchased 100% of the outstanding common shares of Towson Company on December 31, 2011 for $170,000. At that date, Towson had $100,000 of outstanding common stock and retained earnings of $30,000. It was agreed that the net assets were fairly valued except that the fair value of the capital assets exceeded their net book value by $20,000 and the carrying value of the inventory exceeded its fair value by $10,000. The capital assets had a remaining useful life of eight years as of the acquisition date and have no salvage value. Inventory turns over four times a year. Both companies pay tax at the rate of 30%. It is now 2014 and Carson has been very pleased with how profitable its investment in Towson has been. On Carson's consolidated financial statements at December 31, 2014, what balance should be reported for goodwill?

A)$30,000.

B)$33,000.

C)$19,000.

D)$40,000.

A)$30,000.

B)$33,000.

C)$19,000.

D)$40,000.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 56 في هذه المجموعة.

فتح الحزمة

k this deck

49

Regarding the Acquisition Analysis, describe pre-acquisition adjustments and what they aim to accomplish.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 56 في هذه المجموعة.

فتح الحزمة

k this deck

50

When performing the fair value adjustment process, which of the following is true?

A)The deferred income tax is reversed on the same basis as the fair value adjustment is written off

B)The deferred income tax recognized during the acquisition analysis always remains the same.

C)The fair value adjustments are initially recorded on the statement of financial position and are never written off

D)The fair value adjustments are initially recorded on the statement of financial position and are always written off through comprehensive income over a period of 5 years.

A)The deferred income tax is reversed on the same basis as the fair value adjustment is written off

B)The deferred income tax recognized during the acquisition analysis always remains the same.

C)The fair value adjustments are initially recorded on the statement of financial position and are never written off

D)The fair value adjustments are initially recorded on the statement of financial position and are always written off through comprehensive income over a period of 5 years.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 56 في هذه المجموعة.

فتح الحزمة

k this deck

51

Since taxes are paid by the individual companies, the CCA claim for the acquiree is based on the amount recorded in the records of the ____________.

A)acquirer.

B)acquiree and acquirer.

C)acquiree.

D)consolidated entity.

A)acquirer.

B)acquiree and acquirer.

C)acquiree.

D)consolidated entity.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 56 في هذه المجموعة.

فتح الحزمة

k this deck

52

When the parent has previously held equity interest in the subsidiary, in accordance with IFRS 3.42, the parent revalues the previously held investment to fair value, recognizing the increment in ___________________.

A)retained earnings.

B)net income.

C)assets.

D)other comprehensive income.

A)retained earnings.

B)net income.

C)assets.

D)other comprehensive income.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 56 في هذه المجموعة.

فتح الحزمة

k this deck

53

The starting point for the preparation of the consolidated financial statements is:

A)The individual company statements at that date.

B)The previous year's consolidated financial statements.

C) The parent company's individual statements at year end.

D)The subsidiary company's individual statements at that date.

A)The individual company statements at that date.

B)The previous year's consolidated financial statements.

C) The parent company's individual statements at year end.

D)The subsidiary company's individual statements at that date.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 56 في هذه المجموعة.

فتح الحزمة

k this deck

54

On January 1, 2012 Finn Ltd. Acquired 75% of the shares of Ewe Corporation for $10 per share in cash. The equity of Ewe as at that date was:

Finn had previously acquired 25% of the shares of Ewe for $10,000. The fair value of this investment as at January 1, 2012 was $50,000.

At the acquisition date all of the identifiable assets and liabilities of Ewe were recorded at fair value except for a plant and inventory, whose carrying amounts were $15,000 and $5,000 respectively less than their fair value. All of the inventory was subsequently sold during 2012 and the plant had a remaining useful life at the acquisition date of 5 years. The tax rate is 40%.

Ewe had been actively researching a new process, which is part of the reason why Finn acquired the remaining outstanding shares of Ewe. Finn estimated the value of this intangible to be $10,000 and that it would have an indefinite useful life.

Required: Prepare the acquisition analysis and the consolidation adjustments of Finn and Ewe as at December 31, 2013.

Finn had previously acquired 25% of the shares of Ewe for $10,000. The fair value of this investment as at January 1, 2012 was $50,000.At the acquisition date all of the identifiable assets and liabilities of Ewe were recorded at fair value except for a plant and inventory, whose carrying amounts were $15,000 and $5,000 respectively less than their fair value. All of the inventory was subsequently sold during 2012 and the plant had a remaining useful life at the acquisition date of 5 years. The tax rate is 40%.

Ewe had been actively researching a new process, which is part of the reason why Finn acquired the remaining outstanding shares of Ewe. Finn estimated the value of this intangible to be $10,000 and that it would have an indefinite useful life.

Required: Prepare the acquisition analysis and the consolidation adjustments of Finn and Ewe as at December 31, 2013.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 56 في هذه المجموعة.

فتح الحزمة

k this deck

55

Goodwill recorded by the subsidiary at the acquisition date is?

A)Added to the goodwill recognized by the parent at the acquisition date.

B)Deducted from the net fair value of the identifiable assets and liabilities of the subsidiary in the performing the acquisition analysis.

C)Is amortized over 25 years.

D)An impairment loss is recognized by the subsidiary for the entire amount.

A)Added to the goodwill recognized by the parent at the acquisition date.

B)Deducted from the net fair value of the identifiable assets and liabilities of the subsidiary in the performing the acquisition analysis.

C)Is amortized over 25 years.

D)An impairment loss is recognized by the subsidiary for the entire amount.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 56 في هذه المجموعة.

فتح الحزمة

k this deck

56

In a business combination that occurred 2 years ago, there was a fair value adjustment due to land as the fair value was greater than its recorded book value by $20,000. The company's tax rate is 40%. What is the required adjustment upon consolidation this year?

A)There is no required adjustment upon consolidation.

B)Increase the carrying value of land by $20,000 and increase the deferred tax liability of $8,000.

C)Increase the carrying value of land by $12,000

D))Recognize goodwill for $20,000

A)There is no required adjustment upon consolidation.

B)Increase the carrying value of land by $20,000 and increase the deferred tax liability of $8,000.

C)Increase the carrying value of land by $12,000

D))Recognize goodwill for $20,000

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 56 في هذه المجموعة.

فتح الحزمة

k this deck

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 56 في هذه المجموعة.