Deck 13: Management Control Systems, the Balanced Scorecard, and Responsibility Accounting

ملء الشاشة (f)

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

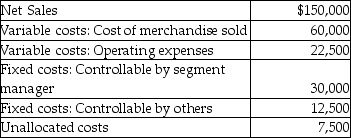

The following information pertains to the Southern Territory of Nordeen Company:

The contribution margin is

A) $37,500.

B) $82,500.

C) $67,500.

D) $25,000.

The contribution margin is

A) $37,500.

B) $82,500.

C) $67,500.

D) $25,000.

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

The following information pertains to the Southern Territory of Nordeen Company:

The contribution controllable by segment manager is

A) $67,500.

B) $37,500.

C) $25,000.

D) $17,500.

The contribution controllable by segment manager is

A) $67,500.

B) $37,500.

C) $25,000.

D) $17,500.

سؤال

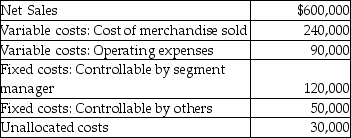

The following information pertains to the Northwest Territory of Jordan, Inc.:

The contribution margin is

A) $150,000.

B) $330,000.

C) $270,000.

D) $100,000.

The contribution margin is

A) $150,000.

B) $330,000.

C) $270,000.

D) $100,000.

سؤال

سؤال

سؤال

The following information pertains to the Northwest Territory of Jordan, Inc.:

The contribution by segment is

A) $100,000.

B) $150,000.

C) $ 70,000.

D) $270,000.

The contribution by segment is

A) $100,000.

B) $150,000.

C) $ 70,000.

D) $270,000.

سؤال

The following information pertains to the Northwest Territory of Jordan, Inc.:

The contribution controllable by segment manager is

A) $270,000.

B) $150,000.

C) $100,000.

D) $ 70,000.

The contribution controllable by segment manager is

A) $270,000.

B) $150,000.

C) $100,000.

D) $ 70,000.

سؤال

سؤال

سؤال

The following information pertains to the Southern Territory of Nordeen Company:

The contribution by segment is

A) $25,000.

B) $37,500.

C) $17,500.

D) $67,500.

The contribution by segment is

A) $25,000.

B) $37,500.

C) $17,500.

D) $67,500.

سؤال

سؤال

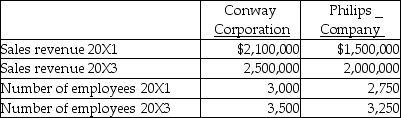

Conway Corporation and Philips Company are computer companies. Comparative data for 20X1 and 20X3 are given below.

Assume that each 20X1 dollar is equivalent to 1.45 of the 20X3 dollars, due to inflation.

Assume that each 20X1 dollar is equivalent to 1.45 of the 20X3 dollars, due to inflation.

What is Conway's 20X3 productivity measure in terms of revenues per employee?

A) $1,015.00

B) $700.00

C) $714.29

D) $870.00

Assume that each 20X1 dollar is equivalent to 1.45 of the 20X3 dollars, due to inflation.What is Conway's 20X3 productivity measure in terms of revenues per employee?

A) $1,015.00

B) $700.00

C) $714.29

D) $870.00

سؤال

سؤال

Conway Corporation and Philips Company are computer companies. Comparative data for 20X1 and 20X3 are given below.

Assume that each 20X1 dollar is equivalent to 1.45 of the 20X3 dollars, due to inflation.

What is Philips' 20X3 productivity measure in terms of revenues per employee?

A) $892.31

B) $615.39

C) $790.91

D) $545.45

Assume that each 20X1 dollar is equivalent to 1.45 of the 20X3 dollars, due to inflation.What is Philips' 20X3 productivity measure in terms of revenues per employee?

A) $892.31

B) $615.39

C) $790.91

D) $545.45

سؤال

Conway Corporation and Philips Company are computer companies. Comparative data for 20X1 and 20X3 are given below.

Assume that each 20X1 dollar is equivalent to 1.45 of the 20X3 dollars, due to inflation.

What is Conway's 20X1 revenues per employee in term of 20X3 dollars?

A) $1,015.00.

B) $700.00.

C) $714.29.

D) $870.00.

Assume that each 20X1 dollar is equivalent to 1.45 of the 20X3 dollars, due to inflation.What is Conway's 20X1 revenues per employee in term of 20X3 dollars?

A) $1,015.00.

B) $700.00.

C) $714.29.

D) $870.00.

سؤال

سؤال

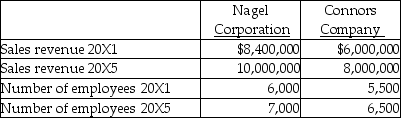

Nagel Corporation and Connors Company are computer companies. Comparative data for 20X1 and 20X5 are given below.

Assume that each 20X1 dollar is equivalent to 1.60 of the 20X5 dollars, due to inflation.

Assume that each 20X1 dollar is equivalent to 1.60 of the 20X5 dollars, due to inflation.

What is Connors' 20X5 productivity measure in terms of revenues per employee?

A) $1,476.93

B) $1,230.77

C) $1,969.23

D) $1,090.91

Assume that each 20X1 dollar is equivalent to 1.60 of the 20X5 dollars, due to inflation.What is Connors' 20X5 productivity measure in terms of revenues per employee?

A) $1,476.93

B) $1,230.77

C) $1,969.23

D) $1,090.91

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

Conway Corporation and Philips Company are computer companies. Comparative data for 20X1 and 20X3 are given below.

Assume that each 20X1 dollar is equivalent to 1.45 of the 20X3 dollars, due to inflation.

What is Philips' revenues per employee in terms of 20X3 dollars?

A) $892.31

B) $615.39

C) $790.91

D) $545.45

Assume that each 20X1 dollar is equivalent to 1.45 of the 20X3 dollars, due to inflation.What is Philips' revenues per employee in terms of 20X3 dollars?

A) $892.31

B) $615.39

C) $790.91

D) $545.45

سؤال

سؤال

Nagel Corporation and Connors Company are computer companies. Comparative data for 20X1 and 20X5 are given below.

Assume that each 20X1 dollar is equivalent to 1.60 of the 20X5 dollars, due to inflation.

What is Nagel's 20X5 productivity measure in terms of revenues per employee?

A) $2,240.00

B) $1,400.00

C) $1,428.57

D) $1,200.00

Assume that each 20X1 dollar is equivalent to 1.60 of the 20X5 dollars, due to inflation.What is Nagel's 20X5 productivity measure in terms of revenues per employee?

A) $2,240.00

B) $1,400.00

C) $1,428.57

D) $1,200.00

سؤال

سؤال

Nagel Corporation and Connors Company are computer companies. Comparative data for 20X1 and 20X5 are given below.

Assume that each 20X1 dollar is equivalent to 1.60 of the 20X5 dollars, due to inflation.

What is Nagel's 20X1 revenues per employee in terms of 20X5 dollars?

A) $2,240.00

B) $1,400.00

C) $1,428.57

D) $1,200.00

Assume that each 20X1 dollar is equivalent to 1.60 of the 20X5 dollars, due to inflation.What is Nagel's 20X1 revenues per employee in terms of 20X5 dollars?

A) $2,240.00

B) $1,400.00

C) $1,428.57

D) $1,200.00

سؤال

سؤال

فتح الحزمة

قم بالتسجيل لفتح البطاقات في هذه المجموعة!

Unlock Deck

Unlock Deck

1/94

العب

ملء الشاشة (f)

Deck 13: Management Control Systems, the Balanced Scorecard, and Responsibility Accounting

1

Which of the following would NOT be a step in the design of a successful management control system?

A) Specify organizational goals, subgoals and objectives.

B) Identify responsibility centres.

C) Measure and report financial performance but not nonfinancial performance.

D) Develop measures of performance for motivation and goal congruence.

A) Specify organizational goals, subgoals and objectives.

B) Identify responsibility centres.

C) Measure and report financial performance but not nonfinancial performance.

D) Develop measures of performance for motivation and goal congruence.

C

2

The management control system is distinguished from a financial accounting system by its focus on all of the following EXCEPT

A) generally accepted accounting principles.

B) organizational goals and objectives.

C) internal management decision making.

D) motivation and evaluation of performance consistent with the organization's goals.

A) generally accepted accounting principles.

B) organizational goals and objectives.

C) internal management decision making.

D) motivation and evaluation of performance consistent with the organization's goals.

A

3

Once a management control system is designed for an organization, it will meet the organization's goals indefinitely.

False

4

Segments are responsibility centres for which a separate measure of revenues and costs is obtained.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 94 في هذه المجموعة.

فتح الحزمة

k this deck

5

A management control system is a logical integration of management accounting tools to gather and report data and to evaluate performance.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 94 في هذه المجموعة.

فتح الحزمة

k this deck

6

Which of the following is NOT a characteristic of a management control system?

A) It aids and coordinates the process of making decisions.

B) It encourages short-term profitability.

C) It motivates individuals throughout the organization to act in concert.

D) It coordinates forecasting sales and cost-driver activities, budgeting, and measuring and evaluating performance.

A) It aids and coordinates the process of making decisions.

B) It encourages short-term profitability.

C) It motivates individuals throughout the organization to act in concert.

D) It coordinates forecasting sales and cost-driver activities, budgeting, and measuring and evaluating performance.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 94 في هذه المجموعة.

فتح الحزمة

k this deck

7

Productivity is a measure of inputs divided by outputs.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 94 في هذه المجموعة.

فتح الحزمة

k this deck

8

Controllable costs should be ignored in evaluating the responsibility centre manager's performance.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 94 في هذه المجموعة.

فتح الحزمة

k this deck

9

A logical integration of management accounting tools to gather and report data and to evaluate performance is a(n)

A) internal control system.

B) quality control system.

C) financial reporting system.

D) management control system.

A) internal control system.

B) quality control system.

C) financial reporting system.

D) management control system.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 94 في هذه المجموعة.

فتح الحزمة

k this deck

10

A responsibility centre for controlling revenues as well as costs is called a profit centre.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 94 في هذه المجموعة.

فتح الحزمة

k this deck

11

Total quality management focuses on prevention of defects and on customer satisfaction.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 94 في هذه المجموعة.

فتح الحزمة

k this deck

12

To achieve goal congruence and managerial effort, designers of management control systems should focus on motivating employees.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 94 في هذه المجموعة.

فتح الحزمة

k this deck

13

Information to support the management control system often comes primarily from the organization's

A) internal control system.

B) top management.

C) stockholders.

D) financial accounting system.

A) internal control system.

B) top management.

C) stockholders.

D) financial accounting system.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 94 في هذه المجموعة.

فتح الحزمة

k this deck

14

Explicit coordination of individuals' activities, actions and choices is the hallmark of the

A) management control system.

B) responsibility centre.

C) internal control system.

D) quality-control chart.

A) management control system.

B) responsibility centre.

C) internal control system.

D) quality-control chart.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 94 في هذه المجموعة.

فتح الحزمة

k this deck

15

Control systems in nonprofit organizations will never be as highly developed as in profit-seeking firms because measurements are more difficult.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 94 في هذه المجموعة.

فتح الحزمة

k this deck

16

A management control system must evolve with changing times, or the organization risks not being able to manage its resources effectively or efficiently.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 94 في هذه المجموعة.

فتح الحزمة

k this deck

17

It is common in Canadian companies to ensure that an internal control system is in place to prevent errors and irregularities and promote operating efficiency.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 94 في هذه المجموعة.

فتح الحزمة

k this deck

18

A well-designed management control system ignores nonfinancial objectives and focuses on financial objectives to develop and report measures of performance.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 94 في هذه المجموعة.

فتح الحزمة

k this deck

19

Goal congruence exists when individuals aim at short-term goals and groups aim at long-term organizational goals.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 94 في هذه المجموعة.

فتح الحزمة

k this deck

20

An investment centre's success is measured only by its income.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 94 في هذه المجموعة.

فتح الحزمة

k this deck

21

Exertion toward a goal or objective, including all conscious actions that result in more efficiency and effectiveness, is referred to as

A) goal congruence.

B) motivation.

C) responsibility accounting.

D) managerial effort.

A) goal congruence.

B) motivation.

C) responsibility accounting.

D) managerial effort.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 94 في هذه المجموعة.

فتح الحزمة

k this deck

22

All of the following are financial objectives of responsibility centres EXCEPT

A) operations budgets.

B) profit targets.

C) customer satisfaction.

D) return on investment.

A) operations budgets.

B) profit targets.

C) customer satisfaction.

D) return on investment.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 94 في هذه المجموعة.

فتح الحزمة

k this deck

23

The drive for some selected goal that creates effort and action toward that goal is called

A) motivation.

B) goal congruence.

C) managerial effort.

D) apathy.

A) motivation.

B) goal congruence.

C) managerial effort.

D) apathy.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 94 في هذه المجموعة.

فتح الحزمة

k this deck

24

Which of the following is NOT a synonym for an organization's subgoals?

A) Critical success factors

B) Critical variables

C) Key result areas

D) Profit centres

A) Critical success factors

B) Critical variables

C) Key result areas

D) Profit centres

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 94 في هذه المجموعة.

فتح الحزمة

k this deck

25

A responsibility centre whose success is measured NOT only by its income, but also by relating that income to its invested capital is called a(n)

A) profit centre.

B) cost centre.

C) investment centre.

D) accounting centre.

A) profit centre.

B) cost centre.

C) investment centre.

D) accounting centre.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 94 في هذه المجموعة.

فتح الحزمة

k this deck

26

The first step in designing a management control system is

A) evaluating management's performance.

B) establishing organizational goals.

C) preparing financial statements.

D) distinguishing between profit centres and cost centres.

A) evaluating management's performance.

B) establishing organizational goals.

C) preparing financial statements.

D) distinguishing between profit centres and cost centres.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 94 في هذه المجموعة.

فتح الحزمة

k this deck

27

Profit centres

A) have responsibility for controlling costs as well as revenues.

B) control and report costs only.

C) measure income and relate that income to their invested capital.

D) are the same as investment centres.

A) have responsibility for controlling costs as well as revenues.

B) control and report costs only.

C) measure income and relate that income to their invested capital.

D) are the same as investment centres.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 94 في هذه المجموعة.

فتح الحزمة

k this deck

28

Which of the following statements regarding responsibility centres is false?

A) Responsibility centres usually have one objective.

B) Management control systems monitor responsibility centre objectives.

C) Responsibility centres are usually classified according to their financial responsibility.

D) Cost centres, profit centres and investments centres are all examples of responsibility centres.

A) Responsibility centres usually have one objective.

B) Management control systems monitor responsibility centre objectives.

C) Responsibility centres are usually classified according to their financial responsibility.

D) Cost centres, profit centres and investments centres are all examples of responsibility centres.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 94 في هذه المجموعة.

فتح الحزمة

k this deck

29

An internal control system consists of all of the following EXCEPT

A) methods to prevent errors and irregularities.

B) procedures to promote goal congruence.

C) methods to promote operating efficiency.

D) procedures to detect errors and irregularities.

A) methods to prevent errors and irregularities.

B) procedures to promote goal congruence.

C) methods to promote operating efficiency.

D) procedures to detect errors and irregularities.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 94 في هذه المجموعة.

فتح الحزمة

k this deck

30

To create a management control system that meets the organization's needs, designers need to consider all of the following EXCEPT

A) existing constraints.

B) external reporting requirements.

C) internal controls.

D) costs versus benefits.

A) existing constraints.

B) external reporting requirements.

C) internal controls.

D) costs versus benefits.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 94 في هذه المجموعة.

فتح الحزمة

k this deck

31

An effective management control system gives each lower-level manager responsibility for a group of activities and objectives and then reports on all of the following EXCEPT

A) the results of activities.

B) the manager's influence on those results.

C) effects of uncontrollable events.

D) effects of controllable events.

A) the results of activities.

B) the manager's influence on those results.

C) effects of uncontrollable events.

D) effects of controllable events.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 94 في هذه المجموعة.

فتح الحزمة

k this deck

32

To achieve maximum benefits at minimum cost, a management control system must

A) look at the short term only.

B) motivate managers with quarterly bonuses based on performance.

C) foster goal congruence and managerial effort.

D) be the same as the financial accounting system.

A) look at the short term only.

B) motivate managers with quarterly bonuses based on performance.

C) foster goal congruence and managerial effort.

D) be the same as the financial accounting system.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 94 في هذه المجموعة.

فتح الحزمة

k this deck

33

Specific tangible achievements that can be observed on a short-term basis are called

A) principles.

B) guidelines.

C) objectives.

D) assumptions.

A) principles.

B) guidelines.

C) objectives.

D) assumptions.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 94 في هذه المجموعة.

فتح الحزمة

k this deck

34

Goal congruence exists when

A) managers are looking only at the short run.

B) individuals and groups aim at the same organizational goals.

C) employees make decisions in their own best interest without regard to company goals.

D) employees are stockholders.

A) managers are looking only at the short run.

B) individuals and groups aim at the same organizational goals.

C) employees make decisions in their own best interest without regard to company goals.

D) employees are stockholders.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 94 في هذه المجموعة.

فتح الحزمة

k this deck

35

All of the following are nonfinancial objectives of responsibility centres EXCEPT

A) quality.

B) productivity.

C) operations budgets.

D) customer satisfaction.

A) quality.

B) productivity.

C) operations budgets.

D) customer satisfaction.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 94 في هذه المجموعة.

فتح الحزمة

k this deck

36

Good performance measures will do all of the following EXCEPT

A) be subjective.

B) relate to the goals of the organization.

C) balance long-term and short-term concerns.

D) reflect the management of key activities.

A) be subjective.

B) relate to the goals of the organization.

C) balance long-term and short-term concerns.

D) reflect the management of key activities.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 94 في هذه المجموعة.

فتح الحزمة

k this deck

37

A set of activities assigned to a manager or a group of managers or other employees is called a(n)

A) internal control system.

B) management control system.

C) responsibility centre.

D) total quality control system.

A) internal control system.

B) management control system.

C) responsibility centre.

D) total quality control system.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 94 في هذه المجموعة.

فتح الحزمة

k this deck

38

The process of identifying what parts of the organization have primary responsibility for each objective, developing measures of achievement and objectives, and creating reports of these measures by organization subunit or responsibility centre is known as

A) financial accounting.

B) management accounting.

C) total quality accounting.

D) responsibility accounting.

A) financial accounting.

B) management accounting.

C) total quality accounting.

D) responsibility accounting.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 94 في هذه المجموعة.

فتح الحزمة

k this deck

39

A responsibility centre for which costs are accumulated is called a(n)

A) profit centre.

B) cost centre.

C) investment centre.

D) accounting centre.

A) profit centre.

B) cost centre.

C) investment centre.

D) accounting centre.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 94 في هذه المجموعة.

فتح الحزمة

k this deck

40

Who is responsible for developing, maintaining and evaluating internal control systems?

A) Managers

B) Stockholders

C) Accountants

D) Both managers and accountants

A) Managers

B) Stockholders

C) Accountants

D) Both managers and accountants

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 94 في هذه المجموعة.

فتح الحزمة

k this deck

41

The effort to insure that products and services perform to customer requirements is called

A) productivity.

B) cycle time.

C) quality control.

D) managerial effort.

A) productivity.

B) cycle time.

C) quality control.

D) managerial effort.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 94 في هذه المجموعة.

فتح الحزمة

k this deck

42

Any cost that cannot be affected by the management of a responsibility centre within a given time span is a(n)

A) controllable cost.

B) quality cost.

C) uncontrollable cost.

D) opportunity cost.

A) controllable cost.

B) quality cost.

C) uncontrollable cost.

D) opportunity cost.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 94 في هذه المجموعة.

فتح الحزمة

k this deck

43

The following information pertains to the Southern Territory of Nordeen Company:

The contribution margin is

A) $37,500.

B) $82,500.

C) $67,500.

D) $25,000.

The contribution margin is

A) $37,500.

B) $82,500.

C) $67,500.

D) $25,000.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 94 في هذه المجموعة.

فتح الحزمة

k this deck

44

The statistical plot of measures of various product dimensions or attributes is called a

A) quality-control chart.

B) productivity chart.

C) cycle-time chart.

D) conventional chart.

A) quality-control chart.

B) productivity chart.

C) cycle-time chart.

D) conventional chart.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 94 في هذه المجموعة.

فتح الحزمة

k this deck

45

A report that displays the financial impact of quality is called a

A) cycle time report.

B) productivity report.

C) financial report.

D) quality cost report.

A) cycle time report.

B) productivity report.

C) financial report.

D) quality cost report.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 94 في هذه المجموعة.

فتح الحزمة

k this deck

46

A controllable cost

A) should be ignored in evaluating the responsibility centre manager's performance.

B) is a cost that is influenced by a manager's decisions and actions.

C) is a cost that cannot be affected by the management of a responsibility centre within a given time span.

D) is the same as a sunk cost.

A) should be ignored in evaluating the responsibility centre manager's performance.

B) is a cost that is influenced by a manager's decisions and actions.

C) is a cost that cannot be affected by the management of a responsibility centre within a given time span.

D) is the same as a sunk cost.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 94 في هذه المجموعة.

فتح الحزمة

k this deck

47

Managers on all levels are asked to explain the total segment contribution but are held responsible only for the

A) controllable contribution.

B) fixed costs.

C) variable costs.

D) unallocated costs.

A) controllable contribution.

B) fixed costs.

C) variable costs.

D) unallocated costs.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 94 في هذه المجموعة.

فتح الحزمة

k this deck

48

A management control system can be designed to stress all of the following simultaneously EXCEPT

A) cost behaviour.

B) customer satisfaction.

C) controllability.

D) manager performance.

A) cost behaviour.

B) customer satisfaction.

C) controllability.

D) manager performance.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 94 في هذه المجموعة.

فتح الحزمة

k this deck

49

All of the following are categories of quality costs EXCEPT

A) development.

B) prevention.

C) appraisal.

D) internal failure.

A) development.

B) prevention.

C) appraisal.

D) internal failure.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 94 في هذه المجموعة.

فتح الحزمة

k this deck

50

Quality control is a concern of

A) privately owned companies.

B) nonprofit organizations.

C) government organizations.

D) privately owned companies, nonprofit and government organizations alike.

A) privately owned companies.

B) nonprofit organizations.

C) government organizations.

D) privately owned companies, nonprofit and government organizations alike.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 94 في هذه المجموعة.

فتح الحزمة

k this deck

51

Total quality management

A) is the application of quality principles in the quality control department.

B) involves keeping the responsibility for quality control with the management.

C) has significant implications for organization goals, structure and management control systems.

D) is used by all U.S. companies.

A) is the application of quality principles in the quality control department.

B) involves keeping the responsibility for quality control with the management.

C) has significant implications for organization goals, structure and management control systems.

D) is used by all U.S. companies.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 94 في هذه المجموعة.

فتح الحزمة

k this deck

52

The following information pertains to the Southern Territory of Nordeen Company:

The contribution controllable by segment manager is

A) $67,500.

B) $37,500.

C) $25,000.

D) $17,500.

The contribution controllable by segment manager is

A) $67,500.

B) $37,500.

C) $25,000.

D) $17,500.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 94 في هذه المجموعة.

فتح الحزمة

k this deck

53

The following information pertains to the Northwest Territory of Jordan, Inc.:

The contribution margin is

A) $150,000.

B) $330,000.

C) $270,000.

D) $100,000.

The contribution margin is

A) $150,000.

B) $330,000.

C) $270,000.

D) $100,000.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 94 في هذه المجموعة.

فتح الحزمة

k this deck

54

Internal failure costs include

A) field repairs.

B) rework.

C) returns.

D) warranty expenses.

A) field repairs.

B) rework.

C) returns.

D) warranty expenses.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 94 في هذه المجموعة.

فتح الحزمة

k this deck

55

Uncontrollable costs

A) are influenced by a manager's decisions and actions.

B) provide evidence about a manager's performance.

C) are also referred to as opportunity costs.

D) should be ignored in evaluating the responsibility centre manager's performance.

A) are influenced by a manager's decisions and actions.

B) provide evidence about a manager's performance.

C) are also referred to as opportunity costs.

D) should be ignored in evaluating the responsibility centre manager's performance.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 94 في هذه المجموعة.

فتح الحزمة

k this deck

56

The following information pertains to the Northwest Territory of Jordan, Inc.:

The contribution by segment is

A) $100,000.

B) $150,000.

C) $ 70,000.

D) $270,000.

The contribution by segment is

A) $100,000.

B) $150,000.

C) $ 70,000.

D) $270,000.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 94 في هذه المجموعة.

فتح الحزمة

k this deck

57

The following information pertains to the Northwest Territory of Jordan, Inc.:

The contribution controllable by segment manager is

A) $270,000.

B) $150,000.

C) $100,000.

D) $ 70,000.

The contribution controllable by segment manager is

A) $270,000.

B) $150,000.

C) $100,000.

D) $ 70,000.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 94 في هذه المجموعة.

فتح الحزمة

k this deck

58

The contribution margin

A) is especially helpful for predicting the impact on income of short-run changes in activity volume.

B) is defined as sales revenues less all fixed costs.

C) cannot be used with segments.

D) cannot be calculated for investment centres.

A) is especially helpful for predicting the impact on income of short-run changes in activity volume.

B) is defined as sales revenues less all fixed costs.

C) cannot be used with segments.

D) cannot be calculated for investment centres.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 94 في هذه المجموعة.

فتح الحزمة

k this deck

59

A responsibility centre for which a separate measure of revenues and/or costs is obtained is called a(n)

A) accounting centre.

B) segment.

C) contribution centre.

D) quality control centre.

A) accounting centre.

B) segment.

C) contribution centre.

D) quality control centre.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 94 في هذه المجموعة.

فتح الحزمة

k this deck

60

The following information pertains to the Southern Territory of Nordeen Company:

The contribution by segment is

A) $25,000.

B) $37,500.

C) $17,500.

D) $67,500.

The contribution by segment is

A) $25,000.

B) $37,500.

C) $17,500.

D) $67,500.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 94 في هذه المجموعة.

فتح الحزمة

k this deck

61

Which of the following statements regarding management control principles is false?

A) Always expect that individuals will be pulled in the direction of their own self-interest.

B) Design incentives so that individuals who pursue their own self-interest are also achieving the organization's objectives.

C) Evaluate actual performance based on expected or planned performance.

D) Consider financial performance over nonfinancial performance.

A) Always expect that individuals will be pulled in the direction of their own self-interest.

B) Design incentives so that individuals who pursue their own self-interest are also achieving the organization's objectives.

C) Evaluate actual performance based on expected or planned performance.

D) Consider financial performance over nonfinancial performance.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 94 في هذه المجموعة.

فتح الحزمة

k this deck

62

Conway Corporation and Philips Company are computer companies. Comparative data for 20X1 and 20X3 are given below.

Assume that each 20X1 dollar is equivalent to 1.45 of the 20X3 dollars, due to inflation.

What is Conway's 20X3 productivity measure in terms of revenues per employee?

A) $1,015.00

B) $700.00

C) $714.29

D) $870.00

Assume that each 20X1 dollar is equivalent to 1.45 of the 20X3 dollars, due to inflation.What is Conway's 20X3 productivity measure in terms of revenues per employee?

A) $1,015.00

B) $700.00

C) $714.29

D) $870.00

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 94 في هذه المجموعة.

فتح الحزمة

k this deck

63

A responsibility centre for controlling revenues as well as costs.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 94 في هذه المجموعة.

فتح الحزمة

k this deck

64

Conway Corporation and Philips Company are computer companies. Comparative data for 20X1 and 20X3 are given below.

Assume that each 20X1 dollar is equivalent to 1.45 of the 20X3 dollars, due to inflation.

What is Philips' 20X3 productivity measure in terms of revenues per employee?

A) $892.31

B) $615.39

C) $790.91

D) $545.45

Assume that each 20X1 dollar is equivalent to 1.45 of the 20X3 dollars, due to inflation.What is Philips' 20X3 productivity measure in terms of revenues per employee?

A) $892.31

B) $615.39

C) $790.91

D) $545.45

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 94 في هذه المجموعة.

فتح الحزمة

k this deck

65

Conway Corporation and Philips Company are computer companies. Comparative data for 20X1 and 20X3 are given below.

Assume that each 20X1 dollar is equivalent to 1.45 of the 20X3 dollars, due to inflation.

What is Conway's 20X1 revenues per employee in term of 20X3 dollars?

A) $1,015.00.

B) $700.00.

C) $714.29.

D) $870.00.

Assume that each 20X1 dollar is equivalent to 1.45 of the 20X3 dollars, due to inflation.What is Conway's 20X1 revenues per employee in term of 20X3 dollars?

A) $1,015.00.

B) $700.00.

C) $714.29.

D) $870.00.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 94 في هذه المجموعة.

فتح الحزمة

k this deck

66

Decreasing cycle time

A) requires a low quality product or service.

B) creates reduced flexibility and slower reactions to customer needs.

C) requires smooth-running processes.

D) results in bringing products or services less quickly to customers.

A) requires a low quality product or service.

B) creates reduced flexibility and slower reactions to customer needs.

C) requires smooth-running processes.

D) results in bringing products or services less quickly to customers.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 94 في هذه المجموعة.

فتح الحزمة

k this deck

67

Nagel Corporation and Connors Company are computer companies. Comparative data for 20X1 and 20X5 are given below.

Assume that each 20X1 dollar is equivalent to 1.60 of the 20X5 dollars, due to inflation.

What is Connors' 20X5 productivity measure in terms of revenues per employee?

A) $1,476.93

B) $1,230.77

C) $1,969.23

D) $1,090.91

Assume that each 20X1 dollar is equivalent to 1.60 of the 20X5 dollars, due to inflation.What is Connors' 20X5 productivity measure in terms of revenues per employee?

A) $1,476.93

B) $1,230.77

C) $1,969.23

D) $1,090.91

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 94 في هذه المجموعة.

فتح الحزمة

k this deck

68

A logical integration of management accounting tools to gather and report data and to evaluate performance.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 94 في هذه المجموعة.

فتح الحزمة

k this deck

69

Exists when individuals and groups aim at the same organizational goals.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 94 في هذه المجموعة.

فتح الحزمة

k this deck

70

Exertion toward a goal or objective, including all conscious actions that result in more efficiency and effectiveness.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 94 في هذه المجموعة.

فتح الحزمة

k this deck

71

A responsibility centre for which costs are accumulated.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 94 في هذه المجموعة.

فتح الحزمة

k this deck

72

Control systems in nonprofit organizations probably will never be as highly developed as in profit-seeking firms because in nonprofit organizations

A) there is more competitive pressure from other organizations to improve management control systems.

B) the role of budgeting is often more a matter of playing bargaining games with sources of funding to get the largest possible authorization than it is rigorous planning.

C) organizational goals and objectives are more clear.

D) measurements are less difficult to make.

A) there is more competitive pressure from other organizations to improve management control systems.

B) the role of budgeting is often more a matter of playing bargaining games with sources of funding to get the largest possible authorization than it is rigorous planning.

C) organizational goals and objectives are more clear.

D) measurements are less difficult to make.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 94 في هذه المجموعة.

فتح الحزمة

k this deck

73

A set of activities assigned to a manager or a group of managers or other employees.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 94 في هذه المجموعة.

فتح الحزمة

k this deck

74

Conway Corporation and Philips Company are computer companies. Comparative data for 20X1 and 20X3 are given below.

Assume that each 20X1 dollar is equivalent to 1.45 of the 20X3 dollars, due to inflation.

What is Philips' revenues per employee in terms of 20X3 dollars?

A) $892.31

B) $615.39

C) $790.91

D) $545.45

Assume that each 20X1 dollar is equivalent to 1.45 of the 20X3 dollars, due to inflation.What is Philips' revenues per employee in terms of 20X3 dollars?

A) $892.31

B) $615.39

C) $790.91

D) $545.45

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 94 في هذه المجموعة.

فتح الحزمة

k this deck

75

A responsibility centre whose success is measured not only by its income, but also by relating that income to its invested capital, as in a ratio of income to the value of the capital employed.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 94 في هذه المجموعة.

فتح الحزمة

k this deck

76

Nagel Corporation and Connors Company are computer companies. Comparative data for 20X1 and 20X5 are given below.

Assume that each 20X1 dollar is equivalent to 1.60 of the 20X5 dollars, due to inflation.

What is Nagel's 20X5 productivity measure in terms of revenues per employee?

A) $2,240.00

B) $1,400.00

C) $1,428.57

D) $1,200.00

Assume that each 20X1 dollar is equivalent to 1.60 of the 20X5 dollars, due to inflation.What is Nagel's 20X5 productivity measure in terms of revenues per employee?

A) $2,240.00

B) $1,400.00

C) $1,428.57

D) $1,200.00

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 94 في هذه المجموعة.

فتح الحزمة

k this deck

77

Which of the following statements is false?

A) Productivity is a measure of outputs divided by inputs.

B) The fewer inputs needed to produce a given output, the more productive the organization.

C) Inputs and outputs are difficult to measure.

D) In a productivity ratio, the numerator is a measure of the resource that management wishes to control.

A) Productivity is a measure of outputs divided by inputs.

B) The fewer inputs needed to produce a given output, the more productive the organization.

C) Inputs and outputs are difficult to measure.

D) In a productivity ratio, the numerator is a measure of the resource that management wishes to control.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 94 في هذه المجموعة.

فتح الحزمة

k this deck

78

Nagel Corporation and Connors Company are computer companies. Comparative data for 20X1 and 20X5 are given below.

Assume that each 20X1 dollar is equivalent to 1.60 of the 20X5 dollars, due to inflation.

What is Nagel's 20X1 revenues per employee in terms of 20X5 dollars?

A) $2,240.00

B) $1,400.00

C) $1,428.57

D) $1,200.00

Assume that each 20X1 dollar is equivalent to 1.60 of the 20X5 dollars, due to inflation.What is Nagel's 20X1 revenues per employee in terms of 20X5 dollars?

A) $2,240.00

B) $1,400.00

C) $1,428.57

D) $1,200.00

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 94 في هذه المجموعة.

فتح الحزمة

k this deck

79

The process of identifying what parts of the organization have primary responsibility for each objective, developing measures of achievement and objectives, and creating reports of these measures by organization subunit or responsibility centre.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 94 في هذه المجموعة.

فتح الحزمة

k this deck

80

The time taken to complete a product or service or any of the components of a product or service is called the

A) accounting cycle.

B) cycle time.

C) operating cycle.

D) productive time.

A) accounting cycle.

B) cycle time.

C) operating cycle.

D) productive time.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 94 في هذه المجموعة.

فتح الحزمة

k this deck

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 94 في هذه المجموعة.