Deck 5: Non-Controlling Interest

ملء الشاشة (f)

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

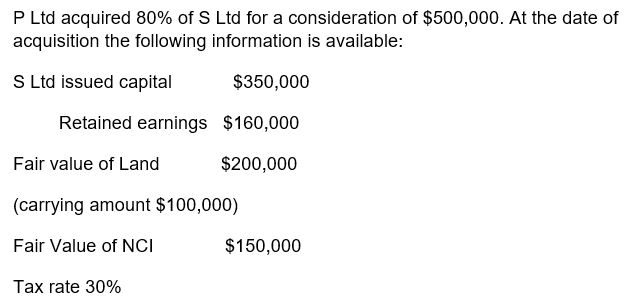

Using the fair value (100% goodwill)method the goodwill on acquisition is:

A) $140,000

B) $186,000

C) $70,000

D) none of the above

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

Under the fair value (100% of goodwill)method used in Question 14 the NCI in goodwill is:

A) $34,000

B) $104,000

C) $150,000

D) none of the above

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

Using the proportionate interest goodwill method,goodwill on acquisition is:

A) $92,000

B) $12,000

C) $36,000

D) none of the above

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

فتح الحزمة

قم بالتسجيل لفتح البطاقات في هذه المجموعة!

Unlock Deck

Unlock Deck

1/37

العب

ملء الشاشة (f)

Deck 5: Non-Controlling Interest

1

The shareholders' interest in a subsidiary that is termed a 'minority interest' derives its name because,in comparison to the interest held be the shareholders of the parent entity,the minority interest:

A) Has less equity in the subsidiary.

B) Has less voting power in the subsidiary.

C) Has less equity and less voting power in the subsidiary.

D) None of the above.

A) Has less equity in the subsidiary.

B) Has less voting power in the subsidiary.

C) Has less equity and less voting power in the subsidiary.

D) None of the above.

D

2

The disclosure of non controlling interest proportion of each equity balance in the consolidated financial statements provides useful information on:

A) dividend payment capacity

B) business activity results

C) Segment activity results

D) all the above

A) dividend payment capacity

B) business activity results

C) Segment activity results

D) all the above

D

3

The shareholders of the parent entity in a group are entitled to:

A) total profits of all group members

B) parent entity interest in consolidated group profit

C) non controlling interest in consolidated group profit

D) none of the above

A) total profits of all group members

B) parent entity interest in consolidated group profit

C) non controlling interest in consolidated group profit

D) none of the above

B

4

A subsidiary's recorded profits and retained earnings must be adjusted for unrealised profits prior to calculation of NCI allocation.The adjustments apply to:

A) upstream transactions

B) downstream transactions

C) both upstream and downstream transactions

D) none of the above

A) upstream transactions

B) downstream transactions

C) both upstream and downstream transactions

D) none of the above

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 37 في هذه المجموعة.

فتح الحزمة

k this deck

5

Company A owns 40% of Company B and this ownership is deemed to represent control.The non controlling interest in B is:

A) 40%

B) 60%

C) 100%

D) No non controlling interest

A) 40%

B) 60%

C) 100%

D) No non controlling interest

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 37 في هذه المجموعة.

فتح الحزمة

k this deck

6

Non controlling interest at date of acquisition must be measured using:

A) the fair value method

B) the proportionate interest goodwill method

C) either A or B

D) none of the above

A) the fair value method

B) the proportionate interest goodwill method

C) either A or B

D) none of the above

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 37 في هذه المجموعة.

فتح الحزمة

k this deck

7

Which of the following statements is correct?

A) The minority interest cannot have the majority of the equity in a subsidiary since it would not then be a minority interest.

B) The minority interest cannot have the majority of voting power in a subsidiary since a majority would give that interest the power to control a subsidiary.

C) The minority interest may have the majority of the equity and a majority of the voting power in a subsidiary but still remain a minority interest.

D) None of the above.

A) The minority interest cannot have the majority of the equity in a subsidiary since it would not then be a minority interest.

B) The minority interest cannot have the majority of voting power in a subsidiary since a majority would give that interest the power to control a subsidiary.

C) The minority interest may have the majority of the equity and a majority of the voting power in a subsidiary but still remain a minority interest.

D) None of the above.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 37 في هذه المجموعة.

فتح الحزمة

k this deck

8

Using the fair value (100% goodwill)method the goodwill on acquisition is:

A) $140,000

B) $186,000

C) $70,000

D) none of the above

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 37 في هذه المجموعة.

فتح الحزمة

k this deck

9

In the preparation of consolidated financial statements,the measurement of a minority interest in the shareholders' equity of a subsidiary at the reporting date may be affected by:

A) Management fees charged to the subsidiary by the parent entity.

B) Unrealised profits arising from sales of inventories in the previous period by the subsidiary to another subsidiary in the same group.

C) Consolidation adjustments made against the retained earnings of the subsidiary at the end of the previous period.

D) None of the above.

A) Management fees charged to the subsidiary by the parent entity.

B) Unrealised profits arising from sales of inventories in the previous period by the subsidiary to another subsidiary in the same group.

C) Consolidation adjustments made against the retained earnings of the subsidiary at the end of the previous period.

D) None of the above.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 37 في هذه المجموعة.

فتح الحزمة

k this deck

10

The parent interest (PI)in equity will be calculated as follows:

A) consolidated equity less non controlling interest

B) parent equity plus PI share of subsidiary equity

C) parent equity plus non controlling interest

D) none of the above

A) consolidated equity less non controlling interest

B) parent equity plus PI share of subsidiary equity

C) parent equity plus non controlling interest

D) none of the above

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 37 في هذه المجموعة.

فتح الحزمة

k this deck

11

In the calculation of NCI share of profit consolidation adjusting entries which do not change group profit will be:

A) adjusted if they affect the subsidiary's reported profit

B) adjusted if the affect the parent entity's reported profit

C) not adjusted

D) none of the above

A) adjusted if they affect the subsidiary's reported profit

B) adjusted if the affect the parent entity's reported profit

C) not adjusted

D) none of the above

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 37 في هذه المجموعة.

فتح الحزمة

k this deck

12

The ownership interests in a group which includes partly owned subsidiaries consist of:

A) the parent entity shareholders

B) the 'outside' subsidiary entity shareholders

C) both the parent entity and the 'outside' subsidiary entity shareholders

D) none of the above

A) the parent entity shareholders

B) the 'outside' subsidiary entity shareholders

C) both the parent entity and the 'outside' subsidiary entity shareholders

D) none of the above

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 37 في هذه المجموعة.

فتح الحزمة

k this deck

13

Where the shareholder's equity of a subsidiary is negative:

A) the NCI will be included as part of the parent interests

B) the NCI will be shown as a separate amount in the consolidated accounts

C) NCI is ignored for consolidation purposes

D) none of the above

A) the NCI will be included as part of the parent interests

B) the NCI will be shown as a separate amount in the consolidated accounts

C) NCI is ignored for consolidation purposes

D) none of the above

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 37 في هذه المجموعة.

فتح الحزمة

k this deck

14

Under the fair value (100% of goodwill)method used in Question 14 the NCI in goodwill is:

A) $34,000

B) $104,000

C) $150,000

D) none of the above

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 37 في هذه المجموعة.

فتح الحزمة

k this deck

15

In preparing a consolidated financial report,the parent entity consolidates:

A) The financial statements of all entities over which it has the power to exercise control.

B) The financial statements of only those entities over which it has the power to control and in which it holds more than 50% of the voting shares.

C) The financial statements of only those entities in which it holds more than 50% of the ordinary share capital; as a result of which it necessarily has the power to exercise control.

D) None of the above.

A) The financial statements of all entities over which it has the power to exercise control.

B) The financial statements of only those entities over which it has the power to control and in which it holds more than 50% of the voting shares.

C) The financial statements of only those entities in which it holds more than 50% of the ordinary share capital; as a result of which it necessarily has the power to exercise control.

D) None of the above.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 37 في هذه المجموعة.

فتح الحزمة

k this deck

16

Consistent with the entity concept,full consolidation requires that:

A) the parent ownership proportion of the subsidiary income, expenses, assets, liabilities and equity are included in the consolidated financial statements

B) the non controlling ownership interests are included in the consolidated financial statements

C) The full amount of income, expense, assets, liabilities and equity are included in the consolidated financial statements

D) none of the above

A) the parent ownership proportion of the subsidiary income, expenses, assets, liabilities and equity are included in the consolidated financial statements

B) the non controlling ownership interests are included in the consolidated financial statements

C) The full amount of income, expense, assets, liabilities and equity are included in the consolidated financial statements

D) none of the above

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 37 في هذه المجموعة.

فتح الحزمة

k this deck

17

When an investment in a subsidiary is impaired,any impairment losses will be:

A) apportioned between PI and NCI

B) borne by the PI

C) ignored

D) none of the above

A) apportioned between PI and NCI

B) borne by the PI

C) ignored

D) none of the above

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 37 في هذه المجموعة.

فتح الحزمة

k this deck

18

The non controlling interest share of a subsidiary's retained earnings will be calculated as a percentage of:

A) opening balance of retained earnings

B) profit for the period

C) dividend and other appropriations

D) the sum of all the above

A) opening balance of retained earnings

B) profit for the period

C) dividend and other appropriations

D) the sum of all the above

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 37 في هذه المجموعة.

فتح الحزمة

k this deck

19

Unrealised intra-group profit in opening inventory of a parent company is:

A) added to subsidiary profit in calculating NCI share of profit

B) subtracted from subsidiary profit in calculating NCI share of profit

C) ignored in calculating NCI share of profit

D) none of the above

A) added to subsidiary profit in calculating NCI share of profit

B) subtracted from subsidiary profit in calculating NCI share of profit

C) ignored in calculating NCI share of profit

D) none of the above

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 37 في هذه المجموعة.

فتح الحزمة

k this deck

20

Using the proportionate interest goodwill method,goodwill on acquisition is:

A) $92,000

B) $12,000

C) $36,000

D) none of the above

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 37 في هذه المجموعة.

فتح الحزمة

k this deck

21

Why does AASB3 allow a choice in the measurement of NCI at the date of acquisition?

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 37 في هذه المجموعة.

فتح الحزمة

k this deck

22

If A owns 80% of B and B owns 75% of C,A's ownership interest in B and C is characterised as direct.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 37 في هذه المجموعة.

فتح الحزمة

k this deck

23

The fair value method of measuring NCI includes an amount representing the non controlling shareholder's interest in goodwill.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 37 في هذه المجموعة.

فتح الحزمة

k this deck

24

Where the full goodwill on acquisition is recognised in the consolidated financial statements,any impairment loss will be allocated between parent interest and NCI on the same basis as profit or loss.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 37 في هذه المجموعة.

فتح الحزمة

k this deck

25

How is the fair value of the shares representing an NCI calculated in the absence of an active market for the company's shares?

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 37 في هذه المجموعة.

فتح الحزمة

k this deck

26

Under the entity concept of consolidation the NCI is recognised as a liability.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 37 في هذه المجموعة.

فتح الحزمة

k this deck

27

Preference shares of a subsidiary not owned by the parent company will be included as part of the NCI.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 37 في هذه المجموعة.

فتح الحزمة

k this deck

28

The effect of all intra group transactions must be adjusted in calculating the NCI share of subsidiary profits.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 37 في هذه المجموعة.

فتح الحزمة

k this deck

29

Outline how NCI will be disclosed in the consolidated statement of financial position,

statement of comprehensive income and statement of changes in equity.

statement of comprehensive income and statement of changes in equity.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 37 في هذه المجموعة.

فتح الحزمة

k this deck

30

Under current accounting standards it is not possible to record a negative NCI in consolidated financial statements.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 37 في هذه المجموعة.

فتح الحزمة

k this deck

31

Under full consolidation only the income,expenses,assets,liabilities and equity of wholly owned subsidiaries are included in the consolidated financial statements.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 37 في هذه المجموعة.

فتح الحزمة

k this deck

32

Is the proprietary concept of consolidation is consistent with the proportional consolidation method?

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 37 في هذه المجموعة.

فتح الحزمة

k this deck

33

Discuss the effect of intra group transactions on the calculation of the NCI share of subsidiary profits and retained earnings

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 37 في هذه المجموعة.

فتح الحزمة

k this deck

34

The consolidation technique of 'NCI allocation' is based on the proposition that non controlling shareholders have an ownership interest in group equity

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 37 في هذه المجموعة.

فتح الحزمة

k this deck

35

The measurement of the NCI allocation will be based on the subsidiary company's equity account balances.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 37 في هذه المجموعة.

فتح الحزمة

k this deck

36

Accounting Standard AASB3 Business combinations allows the choice of measuring NCI using either the fair value method or the proportionate interest method.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 37 في هذه المجموعة.

فتح الحزمة

k this deck

37

P Ltd purchased 80% of the issued ordinary shares of S Ltd.S Ltd capital structure is: Ordinary shares 200,000 fully paid shares x $1

Preference shares 50,000 fully paid shares x $1

Preference shares have the same rights as ordinary shares

The NCI in S Ltd is:

A) 20%

B) 16%

C) 36%

D) none of the above

Preference shares 50,000 fully paid shares x $1

Preference shares have the same rights as ordinary shares

The NCI in S Ltd is:

A) 20%

B) 16%

C) 36%

D) none of the above

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 37 في هذه المجموعة.

فتح الحزمة

k this deck

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 37 في هذه المجموعة.