Deck 20: Option Applications and Corporate Finance

ملء الشاشة (f)

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

Use the figure for the question(s)below.

You pay $4.75 for a call option on Vartan Industries that expires in six months with an exercise price of $45.00. Six months later, at expiration, Vartan Industries is trading at $47.00 per share. Your profit per share on this transaction is closest to:

A)-$2.75.

B)$1.50.

C)-$1.50.

D)$2.75.

You pay $4.75 for a call option on Vartan Industries that expires in six months with an exercise price of $45.00. Six months later, at expiration, Vartan Industries is trading at $47.00 per share. Your profit per share on this transaction is closest to:

A)-$2.75.

B)$1.50.

C)-$1.50.

D)$2.75.

سؤال

سؤال

Use the figure for the question(s)below.

You have shorted a call option on WSJ stock with an exercise price of $50. The option will expire in exactly six months. If the share is trading at $60 in three months, what will you owe for each share in the contract?

A)$60

B)$10

C)$0

D)$50

You have shorted a call option on WSJ stock with an exercise price of $50. The option will expire in exactly six months. If the share is trading at $60 in three months, what will you owe for each share in the contract?

A)$60

B)$10

C)$0

D)$50

سؤال

Use the figure for the question(s)below.

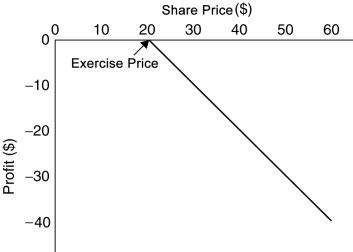

This graph depicts the payoffs of

A)a long position in a put option at expiration.

B)a long position in a call option at expiration.

C)a short position in a put option at expiration.

D)a short position in a call option at expiration.

This graph depicts the payoffs of

A)a long position in a put option at expiration.

B)a long position in a call option at expiration.

C)a short position in a put option at expiration.

D)a short position in a call option at expiration.

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

Use the figure for the question(s)below.

This graph depicts the payoffs of

A)a short position in a put option at expiration.

B)a long position in a put option at expiration.

C)a short position in a call option at expiration.

D)a long position in a call option at expiration.

This graph depicts the payoffs of

A)a short position in a put option at expiration.

B)a long position in a put option at expiration.

C)a short position in a call option at expiration.

D)a long position in a call option at expiration.

سؤال

سؤال

سؤال

Use the figure for the question(s)below.

You have shorted a call option on WSJ stock with an exercise price of $50. The option will expire in exactly six months. If the share is trading at $45 in three month, what will you owe for each share in the contract?

A)$60

B)$50

C)$10

D)$0

You have shorted a call option on WSJ stock with an exercise price of $50. The option will expire in exactly six months. If the share is trading at $45 in three month, what will you owe for each share in the contract?

A)$60

B)$50

C)$10

D)$0

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

فتح الحزمة

قم بالتسجيل لفتح البطاقات في هذه المجموعة!

Unlock Deck

Unlock Deck

1/95

العب

ملء الشاشة (f)

Deck 20: Option Applications and Corporate Finance

1

Which of the following statements is FALSE?

A)A 'put option' gives the owner the right to sell the asset.

B)A 'call option' gives the owner the right to buy the asset.

C)A 'financial options contract' gives the writer the right (but not the obligation)to purchase or sell an asset at a fixed price at some future date.

D)A 'share option' gives the holder the option to buy or sell a share on or before a given date for a given price.

A)A 'put option' gives the owner the right to sell the asset.

B)A 'call option' gives the owner the right to buy the asset.

C)A 'financial options contract' gives the writer the right (but not the obligation)to purchase or sell an asset at a fixed price at some future date.

D)A 'share option' gives the holder the option to buy or sell a share on or before a given date for a given price.

A 'financial options contract' gives the writer the right (but not the obligation)to purchase or sell an asset at a fixed price at some future date.

2

Which of the following statements is FALSE?

A)When the exercise price of an option is equal to the current share price, the option is said to be 'at-the-money'.

B)Because the 'long side' has the option to exercise, the 'short side' has an obligation to fulfil the contract.

C)A holder would not exercise an 'in-the-money' option.

D)The 'option seller', also called the 'option writer', sells (or writes)the option and has a short position in the contract.

A)When the exercise price of an option is equal to the current share price, the option is said to be 'at-the-money'.

B)Because the 'long side' has the option to exercise, the 'short side' has an obligation to fulfil the contract.

C)A holder would not exercise an 'in-the-money' option.

D)The 'option seller', also called the 'option writer', sells (or writes)the option and has a short position in the contract.

A holder would not exercise an 'in-the-money' option.

3

Which of the following statements is FALSE?

A)The market price of the option is also called the 'exercise price'.

B)As with other financial assets, options can be bought and sold. Standard share options are traded on organised exchanges, while more specialised options are sold through dealers.

C)The 'option buyer', also called the 'option holder', holds the right to exercise the option and has a long position in the contract.

D)If the payoff from exercising an option immediately is positive, the option is said to be 'in-the-money'.

A)The market price of the option is also called the 'exercise price'.

B)As with other financial assets, options can be bought and sold. Standard share options are traded on organised exchanges, while more specialised options are sold through dealers.

C)The 'option buyer', also called the 'option holder', holds the right to exercise the option and has a long position in the contract.

D)If the payoff from exercising an option immediately is positive, the option is said to be 'in-the-money'.

The market price of the option is also called the 'exercise price'.

4

A 'call option' gives the owner the right to ________ an asset at a fixed price at some future date.

A)sell

B)hold

C)buy

D)None of the above.

A)sell

B)hold

C)buy

D)None of the above.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 95 في هذه المجموعة.

فتح الحزمة

k this deck

5

Which of the following statements is FALSE?

A)Because an option is a contract between two parties, for every owner of a financial option, there is also an option writer, the person who takes the other side of the contract.

B)There are two kinds of options. European options allow their holders to exercise the option on any date up to and including a final date called the expiration date.

C)When a holder of an option enforces the agreement and buys or sells a share at the agreed-upon price, he is 'exercising the option'.

D)The price at which the holder buys or sells the share when the option is exercised is called the 'exercise price'.

A)Because an option is a contract between two parties, for every owner of a financial option, there is also an option writer, the person who takes the other side of the contract.

B)There are two kinds of options. European options allow their holders to exercise the option on any date up to and including a final date called the expiration date.

C)When a holder of an option enforces the agreement and buys or sells a share at the agreed-upon price, he is 'exercising the option'.

D)The price at which the holder buys or sells the share when the option is exercised is called the 'exercise price'.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 95 في هذه المجموعة.

فتح الحزمة

k this deck

6

For every owner of a call option, there is also an option writer (the person who takes the other side).

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 95 في هذه المجموعة.

فتح الحزمة

k this deck

7

An options contract obligates the owner to buy or sell an asset at a fixed price at some future date.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 95 في هذه المجموعة.

فتح الحزمة

k this deck

8

When the exercise price of an option is equal to the current share price, the option is said to be

A)at-the-money.

B)in-the-money.

C)out-of-the-money.

D)None of the above.

A)at-the-money.

B)in-the-money.

C)out-of-the-money.

D)None of the above.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 95 في هذه المجموعة.

فتح الحزمة

k this deck

9

________ options allow the holder to exercise the option on any date up to and including the expiration date.

A)European

B)American

C)Preference

D)None of the above.

A)European

B)American

C)Preference

D)None of the above.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 95 في هذه المجموعة.

فتح الحزمة

k this deck

10

When the exercise price of a call option is lower than the current share price, the option is said to be

A)at-the-money.

B)in-the-money.

C)out-of-the-money.

D)None of the above.

A)at-the-money.

B)in-the-money.

C)out-of-the-money.

D)None of the above.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 95 في هذه المجموعة.

فتح الحزمة

k this deck

11

The ________ is the total number of contracts of a particular option that have been written and not yet closed.

A)turnover

B)local turnover

C)open interest

D)mark interest

A)turnover

B)local turnover

C)open interest

D)mark interest

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 95 في هذه المجموعة.

فتح الحزمة

k this deck

12

The ________ side of an options contract has the option to exercise, while the ________ side has an obligation to fulfil the contract.

A)long, short

B)short, long

C)short, short

D)long, long

A)long, short

B)short, long

C)short, short

D)long, long

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 95 في هذه المجموعة.

فتح الحزمة

k this deck

13

Using an option to reduce the risk of a portfolio is called ________, while using options to bet on the direction of the market or an asset is called ________.

A)verification, hedging

B)speculation, hedging

C)hedging, verification

D)hedging, speculation

A)verification, hedging

B)speculation, hedging

C)hedging, verification

D)hedging, speculation

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 95 في هذه المجموعة.

فتح الحزمة

k this deck

14

Options are also called 'derivative assets' because they derive their value solely from the price of another asset.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 95 في هذه المجموعة.

فتح الحزمة

k this deck

15

A 'put option' gives the owner the right to ________ an asset at a fixed price at some future date.

A)hold

B)buy

C)sell

D)None of the above.

A)hold

B)buy

C)sell

D)None of the above.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 95 في هذه المجموعة.

فتح الحزمة

k this deck

16

Standard share options are traded and bought and sold through dealers only and cannot be bought via an exchange.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 95 في هذه المجموعة.

فتح الحزمة

k this deck

17

When the exercise price of a call option is higher than the current share price, the option is said to be

A)at-the-money.

B)in-the-money.

C)out-of-the-money.

D)None of the above.

A)at-the-money.

B)in-the-money.

C)out-of-the-money.

D)None of the above.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 95 في هذه المجموعة.

فتح الحزمة

k this deck

18

________ options allow the holder to exercise the option only on the expiration date.

A)European

B)American

C)Preference

D)None of the above.

A)European

B)American

C)Preference

D)None of the above.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 95 في هذه المجموعة.

فتح الحزمة

k this deck

19

The price at which the holder of an option buys or sells a share when the option is exercised is called the ________ price.

A)maturity

B)dilutive

C)exercise

D)None of the above.

A)maturity

B)dilutive

C)exercise

D)None of the above.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 95 في هذه المجموعة.

فتح الحزمة

k this deck

20

When a company writes a 'call option' on new shares in the company, it is called a

A)put option.

B)stock option.

C)warrant.

D)convertible bond.

A)put option.

B)stock option.

C)warrant.

D)convertible bond.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 95 في هذه المجموعة.

فتح الحزمة

k this deck

21

The option buyer or holder is said to have the 'long position' of an options contract.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 95 في هذه المجموعة.

فتح الحزمة

k this deck

22

Which of the following statements is FALSE?

A)European options allow their holders to exercise the option only on the expiration date-holders cannot exercise before the expiration date.

B)Options also allow investors to speculate, or place a bet, on the direction in which they believe the market is likely to move.

C)Call options with exercise prices above the current share price are in-the-money, as are put options with exercise prices below the current share price.

D)Options where the exercise price and the share price are very far apart are referred to as 'deep in-the-money' or 'deep out-of-the-money'.

A)European options allow their holders to exercise the option only on the expiration date-holders cannot exercise before the expiration date.

B)Options also allow investors to speculate, or place a bet, on the direction in which they believe the market is likely to move.

C)Call options with exercise prices above the current share price are in-the-money, as are put options with exercise prices below the current share price.

D)Options where the exercise price and the share price are very far apart are referred to as 'deep in-the-money' or 'deep out-of-the-money'.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 95 في هذه المجموعة.

فتح الحزمة

k this deck

23

Using options to reduce risk is called

A)a naked position.

B)speculation.

C)a covered position.

D)hedging.

A)a naked position.

B)speculation.

C)a covered position.

D)hedging.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 95 في هذه المجموعة.

فتح الحزمة

k this deck

24

What are 'European options'?

_____________________________________________________________________________________________

_____________________________________________________________________________________________

_____________________________________________________________________________________________

_____________________________________________________________________________________________

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 95 في هذه المجموعة.

فتح الحزمة

k this deck

25

Suppose that a share of Callidus Corp sells at a price of $45 on the expiration date. Compute the price of a put option if the exercise price is $50.

A)$45

B)$5

C)$50

D)-$5

A)$45

B)$5

C)$50

D)-$5

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 95 في هذه المجموعة.

فتح الحزمة

k this deck

26

The writer of a call option has

A)the obligation to sell a security for a given price.

B)the right to buy a security for a given price.

C)the obligation to buy a security for a given price.

D)the right to sell a security for a given price.

A)the obligation to sell a security for a given price.

B)the right to buy a security for a given price.

C)the obligation to buy a security for a given price.

D)the right to sell a security for a given price.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 95 في هذه المجموعة.

فتح الحزمة

k this deck

27

Suppose that a share of Callidus Corp sells at a price of $30 on the expiration date. Compute the price of a call option if the exercise price is $40.

A)$10

B)-$10

C)$0

D)$20

A)$10

B)-$10

C)$0

D)$20

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 95 في هذه المجموعة.

فتح الحزمة

k this deck

28

What is a 'call option'?

_____________________________________________________________________________________________

_____________________________________________________________________________________________

_____________________________________________________________________________________________

_____________________________________________________________________________________________

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 95 في هذه المجموعة.

فتح الحزمة

k this deck

29

The option seller or writer is said to have the 'short position' of an options contract. In fact, it is not an option for the short position holder, but an obligation.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 95 في هذه المجموعة.

فتح الحزمة

k this deck

30

Although the payouts on a long position in an options contract are never negative, the profit from purchasing and holding it could be negative.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 95 في هذه المجموعة.

فتح الحزمة

k this deck

31

When a share price increases by a certain percentage, the price of a call option on the same share increases by a lower percentage amount.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 95 في هذه المجموعة.

فتح الحزمة

k this deck

32

When is an option 'in-the-money'?

_____________________________________________________________________________________________

_____________________________________________________________________________________________

_____________________________________________________________________________________________

_____________________________________________________________________________________________

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 95 في هذه المجموعة.

فتح الحزمة

k this deck

33

What are 'American options'?

_____________________________________________________________________________________________

_____________________________________________________________________________________________

_____________________________________________________________________________________________

_____________________________________________________________________________________________

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 95 في هذه المجموعة.

فتح الحزمة

k this deck

34

When is an option 'out-of-the-money'?

_____________________________________________________________________________________________

_____________________________________________________________________________________________

_____________________________________________________________________________________________

_____________________________________________________________________________________________

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 95 في هذه المجموعة.

فتح الحزمة

k this deck

35

Using options to place a bet on the direction in which you believe the market is likely to move is called

A)speculation.

B)a naked position.

C)hedging.

D)a covered position.

A)speculation.

B)a naked position.

C)hedging.

D)a covered position.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 95 في هذه المجموعة.

فتح الحزمة

k this deck

36

Suppose that a share of Callidus Corp sells at a price of $45 on the expiration date. Compute the price of a call option if the exercise price is $45.

A)$10

B)$5

C)$45

D)$0

A)$10

B)$5

C)$45

D)$0

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 95 في هذه المجموعة.

فتح الحزمة

k this deck

37

What is a 'put option'?

_____________________________________________________________________________________________

_____________________________________________________________________________________________

_____________________________________________________________________________________________

_____________________________________________________________________________________________

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 95 في هذه المجموعة.

فتح الحزمة

k this deck

38

Suppose that a share of Callidus Corp sells at a price of $45 on the expiration date. Compute the price of a call option if the exercise price is $40.

A)$40

B)$10

C)$5

D)$45

A)$40

B)$10

C)$5

D)$45

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 95 في هذه المجموعة.

فتح الحزمة

k this deck

39

The holder of a put option has

A)the right to sell a security for a given price.

B)the right to buy a security for a given price.

C)the obligation to buy a security for a given price.

D)the obligation to sell a security for a given price.

A)the right to sell a security for a given price.

B)the right to buy a security for a given price.

C)the obligation to buy a security for a given price.

D)the obligation to sell a security for a given price.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 95 في هذه المجموعة.

فتح الحزمة

k this deck

40

When is an option 'at-the-money'?

_____________________________________________________________________________________________

_____________________________________________________________________________________________

_____________________________________________________________________________________________

_____________________________________________________________________________________________

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 95 في هذه المجموعة.

فتح الحزمة

k this deck

41

Use the figure for the question(s)below.

You pay $4.75 for a call option on Vartan Industries that expires in six months with an exercise price of $45.00. Six months later, at expiration, Vartan Industries is trading at $47.00 per share. Your profit per share on this transaction is closest to:

A)-$2.75.

B)$1.50.

C)-$1.50.

D)$2.75.

You pay $4.75 for a call option on Vartan Industries that expires in six months with an exercise price of $45.00. Six months later, at expiration, Vartan Industries is trading at $47.00 per share. Your profit per share on this transaction is closest to:

A)-$2.75.

B)$1.50.

C)-$1.50.

D)$2.75.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 95 في هذه المجموعة.

فتح الحزمة

k this deck

42

Suppose that a share of Callidus Corp sells at a price of $45 on the expiration date. Compute the payoff to the seller of a call option if the exercise price is $40.

A)-$5

B)-$40

C)-$45

D)$0

A)-$5

B)-$40

C)-$45

D)$0

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 95 في هذه المجموعة.

فتح الحزمة

k this deck

43

Use the figure for the question(s)below.

You have shorted a call option on WSJ stock with an exercise price of $50. The option will expire in exactly six months. If the share is trading at $60 in three months, what will you owe for each share in the contract?

A)$60

B)$10

C)$0

D)$50

You have shorted a call option on WSJ stock with an exercise price of $50. The option will expire in exactly six months. If the share is trading at $60 in three months, what will you owe for each share in the contract?

A)$60

B)$10

C)$0

D)$50

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 95 في هذه المجموعة.

فتح الحزمة

k this deck

44

Use the figure for the question(s)below.

This graph depicts the payoffs of

A)a long position in a put option at expiration.

B)a long position in a call option at expiration.

C)a short position in a put option at expiration.

D)a short position in a call option at expiration.

This graph depicts the payoffs of

A)a long position in a put option at expiration.

B)a long position in a call option at expiration.

C)a short position in a put option at expiration.

D)a short position in a call option at expiration.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 95 في هذه المجموعة.

فتح الحزمة

k this deck

45

Suppose that a share of Callidus Corp sells at a price of $50 on the expiration date. Compute the price of a put option if the exercise price is $50.

A)$0

B)$50

C)$10

D)$20

A)$0

B)$50

C)$10

D)$20

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 95 في هذه المجموعة.

فتح الحزمة

k this deck

46

Suppose that a share of Callidus Corp sells at a price of $45 on the expiration date. Compute the payoff to the seller of a call option if the exercise price is $45.

A)-$20

B)$0

C)-$50

D)-$30

A)-$20

B)$0

C)-$50

D)-$30

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 95 في هذه المجموعة.

فتح الحزمة

k this deck

47

The payoff to the holder of a put option is given by

A)P = max(K - S, 0).

B)P = min(S - K, 0).

C)P= max(S - K, 0).

D)P = max(K, 0).

A)P = max(K - S, 0).

B)P = min(S - K, 0).

C)P= max(S - K, 0).

D)P = max(K, 0).

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 95 في هذه المجموعة.

فتح الحزمة

k this deck

48

Suppose that a share of Callidus Corp sells at a price of $50 on the expiration date. Compute the price of a put option if the exercise price is $45.

A)$45

B)-$5

C)$5

D)$0

A)$45

B)-$5

C)$5

D)$0

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 95 في هذه المجموعة.

فتح الحزمة

k this deck

49

Suppose you purchase a call option for $5 and an exercise price of $20. On the expiration day, the price of the share is $30. What is the return on the call option if you hold your position until maturity?

A)50%

B)75%

C)100%

D)25%

A)50%

B)75%

C)100%

D)25%

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 95 في هذه المجموعة.

فتح الحزمة

k this deck

50

Suppose that a share of Callidus Corp sells at a price of $30 on the expiration date. Compute the payoff to the seller of a call option if the exercise price is $40.

A)-$20

B)$0

C)-$30

D)-$10

A)-$20

B)$0

C)-$30

D)-$10

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 95 في هذه المجموعة.

فتح الحزمة

k this deck

51

An investor purchases a call option and its underlying share on the same day. If the share appreciates by 25%, the call option will appreciate by

A)less than 25%.

B)exactly 25%.

C)more than 25%.

D)None of the above.

A)less than 25%.

B)exactly 25%.

C)more than 25%.

D)None of the above.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 95 في هذه المجموعة.

فتح الحزمة

k this deck

52

Suppose that a share of Callidus Corp sells at a price of $45 on the expiration date. Compute the payoff to the seller of a put option if the exercise price is $45.

A)-$10

B)$45

C)0

A)-$10

B)$45

C)0

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 95 في هذه المجموعة.

فتح الحزمة

k this deck

53

Suppose that a share of Callidus Corp sells at a price of $30 on the expiration date. Compute the payoff to the seller of a put option if the exercise price is $45.

A)-$20

B)-$15

C)-$10

D)-$45

A)-$20

B)-$15

C)-$10

D)-$45

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 95 في هذه المجموعة.

فتح الحزمة

k this deck

54

The payoff to the holder of a call option is given by

A)C = min(K - S, 0).

B)C = max(S - K, 0).

C)C = min(K, 0).

D)C = max(K - S, 0).

A)C = min(K - S, 0).

B)C = max(S - K, 0).

C)C = min(K, 0).

D)C = max(K - S, 0).

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 95 في هذه المجموعة.

فتح الحزمة

k this deck

55

A European option is more valuable than an otherwise similar American option on the same share.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 95 في هذه المجموعة.

فتح الحزمة

k this deck

56

Use the figure for the question(s)below.

This graph depicts the payoffs of

A)a short position in a put option at expiration.

B)a long position in a put option at expiration.

C)a short position in a call option at expiration.

D)a long position in a call option at expiration.

This graph depicts the payoffs of

A)a short position in a put option at expiration.

B)a long position in a put option at expiration.

C)a short position in a call option at expiration.

D)a long position in a call option at expiration.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 95 في هذه المجموعة.

فتح الحزمة

k this deck

57

Suppose that a share of Callidus Corp sells at a price of $45 on the expiration date. Compute the payoff to the seller of a put option if the exercise price is $30.

A)$0

B)$45

C)-$30

D)-$10

A)$0

B)$45

C)-$30

D)-$10

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 95 في هذه المجموعة.

فتح الحزمة

k this deck

58

Suppose you purchase a call option for $5 and an exercise price of $40. On the expiration day, the price of the share is $55. What is the return on the call option if you hold your position until maturity?

A)200%

B)300%

C)275%

D)125%

A)200%

B)300%

C)275%

D)125%

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 95 في هذه المجموعة.

فتح الحزمة

k this deck

59

Use the figure for the question(s)below.

You have shorted a call option on WSJ stock with an exercise price of $50. The option will expire in exactly six months. If the share is trading at $45 in three month, what will you owe for each share in the contract?

A)$60

B)$50

C)$10

D)$0

You have shorted a call option on WSJ stock with an exercise price of $50. The option will expire in exactly six months. If the share is trading at $45 in three month, what will you owe for each share in the contract?

A)$60

B)$50

C)$10

D)$0

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 95 في هذه المجموعة.

فتح الحزمة

k this deck

60

Suppose you purchase a call option for $4 and an exercise price of $30. On the expiration day, the price of the share is $40. What is the return on the call option if you hold your position until maturity?

A)170%

B)150%

C)130%

D)125%

A)170%

B)150%

C)130%

D)125%

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 95 في هذه المجموعة.

فتح الحزمة

k this deck

61

The value of an otherwise identical American call option is ________ if the exercise date is ________.

A)higher, longer

B)higher, closer

C)lower, longer

D)None of the above.

A)higher, longer

B)higher, closer

C)lower, longer

D)None of the above.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 95 في هذه المجموعة.

فتح الحزمة

k this deck

62

Which of the following statements is FALSE?

A)Put-call parity gives the price of a European call option in terms of the price of a European put, the underlying share, and a zero-coupon bond.

B)Because a put is the right to sell the share, puts with a lower exercise price are less valuable.

C)For a given exercise price, the value of a call option is higher if the current share price is higher, as there is a greater likelihood the option will end up in-the-money.

D)The value of an otherwise identical call option is higher if the exercise price the holder must pay to buy the share is higher.

A)Put-call parity gives the price of a European call option in terms of the price of a European put, the underlying share, and a zero-coupon bond.

B)Because a put is the right to sell the share, puts with a lower exercise price are less valuable.

C)For a given exercise price, the value of a call option is higher if the current share price is higher, as there is a greater likelihood the option will end up in-the-money.

D)The value of an otherwise identical call option is higher if the exercise price the holder must pay to buy the share is higher.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 95 في هذه المجموعة.

فتح الحزمة

k this deck

63

When you purchase a put option while still holding the underlying share, it is known as a

A)speculative put.

B)speculative call.

C)protective call.

D)protective put.

A)speculative put.

B)speculative call.

C)protective call.

D)protective put.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 95 في هذه المجموعة.

فتح الحزمة

k this deck

64

KD Industries is currently trading at $32 per share. Consider a put option on KD with an exercise price of $30. The maximum value of this put option is

A)$30.

B)$32.

C)$0.

D)$2.

A)$30.

B)$32.

C)$0.

D)$2.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 95 في هذه المجموعة.

فتح الحزمة

k this deck

65

Which of the following will NOT increase the value of a put option?

A)an increase in the time to maturity

B)a decrease in the share price

C)an increase in the exercise price

D)a decrease in the share's volatility

A)an increase in the time to maturity

B)a decrease in the share price

C)an increase in the exercise price

D)a decrease in the share's volatility

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 95 في هذه المجموعة.

فتح الحزمة

k this deck

66

For a(n)________ put option, the longer the time to expiration, the greater the value of the option, all other things held constant.

A)American

B)European

C)Asian

D)both A and B

A)American

B)European

C)Asian

D)both A and B

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 95 في هذه المجموعة.

فتح الحزمة

k this deck

67

SC Industries is currently trading at $30 per share. Consider a put option on SC Industries with an exercise price of $32. The intrinsic value of this put option is:

A)$0.

B)$2.

C)-$2.

D)$30.

A)$0.

B)$2.

C)-$2.

D)$30.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 95 في هذه المجموعة.

فتح الحزمة

k this deck

68

Which of the following is NOT used in the Black-Scholes option pricing formula?

A)share price

B)risk-free rate

C)exercise price

D)dividend yield

A)share price

B)risk-free rate

C)exercise price

D)dividend yield

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 95 في هذه المجموعة.

فتح الحزمة

k this deck

69

For a(n)________ put option, the higher the share price, the lower the value of the option.

A)European

B)American

C)Asian

D)both A and B

A)European

B)American

C)Asian

D)both A and B

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 95 في هذه المجموعة.

فتح الحزمة

k this deck

70

The Black-Scholes formula is notable because it does NOT require us to know the

A)volatility of the share.

B)dividend rate on the share.

C)risk-free rate.

D)expected return on a share.

A)volatility of the share.

B)dividend rate on the share.

C)risk-free rate.

D)expected return on a share.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 95 في هذه المجموعة.

فتح الحزمة

k this deck

71

The value of an otherwise identical call option is ________ if the share price is ________.

A)higher, lower

B)lower, higher

C)higher, higher

D)None of the above.

A)higher, lower

B)lower, higher

C)higher, higher

D)None of the above.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 95 في هذه المجموعة.

فتح الحزمة

k this deck

72

The value of a call option increases with the risk-free rate, and the value of a put option decreases with the risk-free rate.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 95 في هذه المجموعة.

فتح الحزمة

k this deck

73

What effect does the volatility of the underlying asset have on the price of the option?

_____________________________________________________________________________________________

_____________________________________________________________________________________________

_____________________________________________________________________________________________

_____________________________________________________________________________________________

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 95 في هذه المجموعة.

فتح الحزمة

k this deck

74

The Black-Scholes formula gives the price of an American call option.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 95 في هذه المجموعة.

فتح الحزمة

k this deck

75

Which of the following statements is FALSE?

A)Put options increase in value as the share price falls.

B)A put option cannot be worth more than its exercise price.

C)A European option cannot be worth less than its American counterpart.

D)The intrinsic value of an option is the value it would have if it expired immediately.

A)Put options increase in value as the share price falls.

B)A put option cannot be worth more than its exercise price.

C)A European option cannot be worth less than its American counterpart.

D)The intrinsic value of an option is the value it would have if it expired immediately.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 95 في هذه المجموعة.

فتح الحزمة

k this deck

76

The value of an otherwise identical call option is ________ if the exercise price the holder must pay to buy the share is ________.

A)lower, lower

B)higher, lower

C)higher, higher

D)None of the above.

A)lower, lower

B)higher, lower

C)higher, higher

D)None of the above.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 95 في هذه المجموعة.

فتح الحزمة

k this deck

77

A European option with a later exercise date may trade potentially for less than an otherwise identical option with an earlier exercise date.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 95 في هذه المجموعة.

فتح الحزمة

k this deck

78

The value of an option decreases with the volatility of the underlying share.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 95 في هذه المجموعة.

فتح الحزمة

k this deck

79

In practice, option prices are not very sensitive to changes in the risk-free rate.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 95 في هذه المجموعة.

فتح الحزمة

k this deck

80

Which of the following statements is FALSE?

A)The value of an option generally decreases with the volatility of the share.

B)The 'intrinsic value' is the amount by which the option is currently in-the-money, or 0 if the option is out-of-the-money.

C)Because an American option cannot be worth less than its intrinsic value, it cannot have a negative time value.

D)An American option with a later exercise date cannot be worth less than an otherwise identical American option with an earlier exercise date.

A)The value of an option generally decreases with the volatility of the share.

B)The 'intrinsic value' is the amount by which the option is currently in-the-money, or 0 if the option is out-of-the-money.

C)Because an American option cannot be worth less than its intrinsic value, it cannot have a negative time value.

D)An American option with a later exercise date cannot be worth less than an otherwise identical American option with an earlier exercise date.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 95 في هذه المجموعة.

فتح الحزمة

k this deck

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 95 في هذه المجموعة.