Deck 27: Short Run Decision Analysis

ملء الشاشة (f)

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

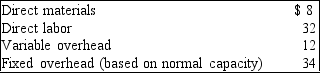

Anderson Co. makes and uses 5,000 components each year in its manufacturing operations. An outside supplier has offered to supply the components to Anderson at $66 per unit. Anderson's production costs are as follows:  If Anderson accepts the order, $8 of fixed overhead per unit will be eliminated.

If Anderson accepts the order, $8 of fixed overhead per unit will be eliminated.

If the offer is accepted, operating income will

A) increase by $100,000.

B) decrease by $70,000.

C) decrease by $30,000.

D) increase by $60,000.

If Anderson accepts the order, $8 of fixed overhead per unit will be eliminated.If the offer is accepted, operating income will

A) increase by $100,000.

B) decrease by $70,000.

C) decrease by $30,000.

D) increase by $60,000.

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

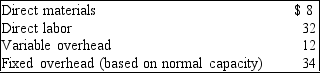

Anderson Co. makes and uses 5,000 components each year in its manufacturing operations. An outside supplier has offered to supply the components to Anderson at $66 per unit. Anderson's production costs are as follows:  If Anderson accepts the order, $8 of fixed overhead per unit will be eliminated.

If Anderson accepts the order, $8 of fixed overhead per unit will be eliminated.

What is the relevant cost to produce one unit?

A) $86

B) $52

C) $78

D) $60

If Anderson accepts the order, $8 of fixed overhead per unit will be eliminated.What is the relevant cost to produce one unit?

A) $86

B) $52

C) $78

D) $60

سؤال

فتح الحزمة

قم بالتسجيل لفتح البطاقات في هذه المجموعة!

Unlock Deck

Unlock Deck

1/90

العب

ملء الشاشة (f)

Deck 27: Short Run Decision Analysis

1

Outsourcing is the use of suppliers outside the organization to perform services or produce goods that cannot be performed or produced internally.

False

2

In choosing among alternatives, managers are guided by historical cost information.

False

3

Many of the decisions that managers make does not affect their organization's activities in the short run.

False

4

Many management decisions are unique and hence incompatible with strict rules, steps, or timetables.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 90 في هذه المجموعة.

فتح الحزمة

k this deck

5

Opportunity costs are irrelevant costs.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 90 في هذه المجموعة.

فتح الحزمة

k this deck

6

Competition, social issues, and timeliness are examples of qualitative factors.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 90 في هذه المجموعة.

فتح الحزمة

k this deck

7

Outsourcing production or operating activities does not help in reducing a company's investment in physical assets and human resources.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 90 في هذه المجموعة.

فتح الحزمة

k this deck

8

Make-or-buy decisions, such as whether to make a part internally or buy it from an external supplier, may lead to outsourcing.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 90 في هذه المجموعة.

فتح الحزمة

k this deck

9

A cost that does not change between the alternatives is known as a differential cost.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 90 في هذه المجموعة.

فتح الحزمة

k this deck

10

The first step in the incremental analysis is to eliminate any irrelevant revenues and costs.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 90 في هذه المجموعة.

فتح الحزمة

k this deck

11

While performing an incremental analysis for outsourcing decision, information such as depreciation and other fixed costs are not relevant. A special order decision is not considered a capital expenditure decision.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 90 في هذه المجموعة.

فتح الحزمة

k this deck

12

Opportunity costs arise when the choice of one course of action eliminates the possibility of another course of action.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 90 في هذه المجموعة.

فتح الحزمة

k this deck

13

Incremental analysis is a technique used not only by businesses but also by individuals to solve daily problems.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 90 في هذه المجموعة.

فتح الحزمة

k this deck

14

Incremental analysis identifies both the benefits and the drawbacks of each alternative.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 90 في هذه المجموعة.

فتح الحزمة

k this deck

15

Managers rely strictly on financial information when faced with decisions.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 90 في هذه المجموعة.

فتح الحزمة

k this deck

16

The cost of a previously purchased machine is an example of a sunk cost.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 90 في هذه المجموعة.

فتح الحزمة

k this deck

17

The idea behind incremental analysis is to review decision data that differ between alternatives; information that is the same for all alternatives is considered irrelevant to the decision process.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 90 في هذه المجموعة.

فتح الحزمة

k this deck

18

Sunk costs are not relevant for decisions based on incremental analysis.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 90 في هذه المجموعة.

فتح الحزمة

k this deck

19

Sunk costs can be recovered.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 90 في هذه المجموعة.

فتح الحزمة

k this deck

20

Qualitative data as well as quantitative data are useful in the decision process.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 90 في هذه المجموعة.

فتح الحزمة

k this deck

21

When resources like direct material, labor or time are scarce, the goal is to minimize the contribution margin per unit of scarce resource.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 90 في هذه المجموعة.

فتح الحزمة

k this deck

22

There is no limit on the availability of resources such as machine time, labor hours.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 90 في هذه المجموعة.

فتح الحزمة

k this deck

23

If the incremental costs of processing further is greater than the incremental revenue, the decision to process the product or service further is justified.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 90 في هذه المجموعة.

فتح الحزمة

k this deck

24

The point where joint products or services become separable and identifiable is known as split-off point.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 90 في هذه المجموعة.

فتح الحزمة

k this deck

25

The objective of segment profitability decisions is to identify the segments that have a negative segment margin so that managers can drop them or take corrective actions.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 90 في هذه المجموعة.

فتح الحزمة

k this deck

26

Fixed costs are irrelevant in make-or-buy decisions.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 90 في هذه المجموعة.

فتح الحزمة

k this deck

27

It is not possible for a company to provide the full variety of products or services which the customer demands within a given time.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 90 في هذه المجموعة.

فتح الحزمة

k this deck

28

The fixed costs that are traceable to the segments are called common costs.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 90 في هذه المجموعة.

فتح الحزمة

k this deck

29

The decision analysis, which uses incremental analysis to identify the relevant costs and revenues, consists of two steps.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 90 في هذه المجموعة.

فتح الحزمة

k this deck

30

Outsourcing production or operating activities will help in improving the cash flow by reducing investment in physical assets.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 90 في هذه المجموعة.

فتح الحزمة

k this deck

31

Segment profitability analysis includes the preparation of a segmented income statement.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 90 في هذه المجموعة.

فتح الحزمة

k this deck

32

In manufacturing companies, a common decision facing managers is whether to make or buy some or all of the parts used in product assembly.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 90 في هذه المجموعة.

فتح الحزمة

k this deck

33

A sell or process-further decision is a decision about whether to sell a joint product at the split-off point or sell it after further processing.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 90 في هذه المجموعة.

فتح الحزمة

k this deck

34

A special order should be accepted only if it maximizes operating income.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 90 في هذه المجموعة.

فتح الحزمة

k this deck

35

The objective of a sales mix decision is to select the alternative that maximizes the contribution margin per constrained resource.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 90 في هذه المجموعة.

فتح الحزمة

k this deck

36

There are products or services that can be either sold in a basic form or be processed further.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 90 في هذه المجموعة.

فتح الحزمة

k this deck

37

Special orders should only be considered if unused capacity exists.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 90 في هذه المجموعة.

فتح الحزمة

k this deck

38

Avoidable costs are the direct variable costs and direct fixed costs traceable to the segments.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 90 في هذه المجموعة.

فتح الحزمة

k this deck

39

A segment margin is a segment's sales revenue minus its direct costs.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 90 في هذه المجموعة.

فتح الحزمة

k this deck

40

Special order decisions are the decisions about whether to accept or reject special orders at prices above the normal market prices.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 90 في هذه المجموعة.

فتح الحزمة

k this deck

41

Sunk costs are omitted from decision analysis

A) always.

B) never.

C) sometimes.

D) only if immaterial.

A) always.

B) never.

C) sometimes.

D) only if immaterial.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 90 في هذه المجموعة.

فتح الحزمة

k this deck

42

Cost information for short-run decision making focuses on

A) what happened.

B) what is happening.

C) what will happen.

D) why it happened.

A) what happened.

B) what is happening.

C) what will happen.

D) why it happened.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 90 في هذه المجموعة.

فتح الحزمة

k this deck

43

The purpose of incremental analysis is to find the alternative

A) with the fewest relevant costs.

B) that brings in the most revenue.

C) that contributes the most to profits.

D) with the lowest fixed costs.

A) with the fewest relevant costs.

B) that brings in the most revenue.

C) that contributes the most to profits.

D) with the lowest fixed costs.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 90 في هذه المجموعة.

فتح الحزمة

k this deck

44

Contribution margin information is not relevant for

A) the elimination of unprofitable segment decisions.

B) pricing decisions for special orders.

C) sales mix with resource constraint decisions.

D) determining the amount that sales exceeded fixed costs.

A) the elimination of unprofitable segment decisions.

B) pricing decisions for special orders.

C) sales mix with resource constraint decisions.

D) determining the amount that sales exceeded fixed costs.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 90 في هذه المجموعة.

فتح الحزمة

k this deck

45

Accountants assign joint costs to products or services while calculating the cost of goods sold because joint costs are also relevant. The most beneficial projects are the ones with the lowest net present value.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 90 في هذه المجموعة.

فتح الحزمة

k this deck

46

Joint costs that are incurred before the split-off point should be ignored while making a decision to sell or process a product further.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 90 في هذه المجموعة.

فتح الحزمة

k this deck

47

Which of the following typically would be considered an incremental cost?

A) Conversion cost

B) Direct product cost

C) Period cost

D) Factory overhead cost

A) Conversion cost

B) Direct product cost

C) Period cost

D) Factory overhead cost

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 90 في هذه المجموعة.

فتح الحزمة

k this deck

48

The difference in total costs between two alternatives is referred to as the

A) incremental cost.

B) sunk cost.

C) opportunity cost.

D) direct cost.

A) incremental cost.

B) sunk cost.

C) opportunity cost.

D) direct cost.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 90 في هذه المجموعة.

فتح الحزمة

k this deck

49

The common costs shared by two or more products before they are split off are called joint costs.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 90 في هذه المجموعة.

فتح الحزمة

k this deck

50

Taylor manufactures 12,000 units of a part used in its production to manufacture guitars. The annual production activities related to this part are as follows: Direct materials, $24,000

Direct labor, $60,000

Variable overhead, $54,000

Fixed overhead, $84,000

Best Guitars, Inc., has offered to sell 12,000 units of the same part to Taylor for $22 per unit. If Taylor were to accept the offer, some of the facilities presently used to manufacture the part could be rented to a third party at an annual rental of $18,000. Moreover, $4 per unit of the fixed overhead applied to the part would be totally eliminated.

What should Taylor's decision be, and what is the total cost savings that would result?

A) Make, $60,000

B) Buy, $60,000

C) Make, $78,000

D) Buy, $78,000

Direct labor, $60,000

Variable overhead, $54,000

Fixed overhead, $84,000

Best Guitars, Inc., has offered to sell 12,000 units of the same part to Taylor for $22 per unit. If Taylor were to accept the offer, some of the facilities presently used to manufacture the part could be rented to a third party at an annual rental of $18,000. Moreover, $4 per unit of the fixed overhead applied to the part would be totally eliminated.

What should Taylor's decision be, and what is the total cost savings that would result?

A) Make, $60,000

B) Buy, $60,000

C) Make, $78,000

D) Buy, $78,000

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 90 في هذه المجموعة.

فتح الحزمة

k this deck

51

If the incremental costs are greater than the incremental revenue, the product should not be processed further and sold at the split-off point.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 90 في هذه المجموعة.

فتح الحزمة

k this deck

52

Estimated future costs that differ between alternative courses of action are termed __________ costs in management decision analysis.

A) variable overhead

B) relevant

C) absorption

D) replacement

A) variable overhead

B) relevant

C) absorption

D) replacement

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 90 في هذه المجموعة.

فتح الحزمة

k this deck

53

Taylor manufactures 12,000 units of a part used in its production to manufacture guitars. The annual production activities related to this part are as follows: Direct materials, $24,000

Direct labor, $60,000

Variable overhead, $54,000

Fixed overhead, $84,000

Best Guitars, Inc., has offered to sell 12,000 units of the same part to Taylor for $22 per unit. If Taylor were to accept the offer, some of the facilities presently used to manufacture the part could be rented to a third party at an annual rental of $18,000. Moreover, $4 per unit of the fixed overhead applied to the part would be totally eliminated.

In the decision to make or buy the part, what is the relevant fixed overhead?

A) $30,000

B) $54,000

C) $84,000

D) $48,000

Direct labor, $60,000

Variable overhead, $54,000

Fixed overhead, $84,000

Best Guitars, Inc., has offered to sell 12,000 units of the same part to Taylor for $22 per unit. If Taylor were to accept the offer, some of the facilities presently used to manufacture the part could be rented to a third party at an annual rental of $18,000. Moreover, $4 per unit of the fixed overhead applied to the part would be totally eliminated.

In the decision to make or buy the part, what is the relevant fixed overhead?

A) $30,000

B) $54,000

C) $84,000

D) $48,000

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 90 في هذه المجموعة.

فتح الحزمة

k this deck

54

Qualitative factors used by decision makers include all of the following except

A) social issues.

B) revenue from fees.

C) timeliness.

D) competition.

A) social issues.

B) revenue from fees.

C) timeliness.

D) competition.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 90 في هذه المجموعة.

فتح الحزمة

k this deck

55

Which of the following statements about incremental analysis is false?

A) It is based on both historical and future information relevant to the decision at hand.

B) It focuses on the differences between alternatives.

C) It reduces the time taken to select the best course of action.

D) It makes the evaluation process easier for the decision maker.

A) It is based on both historical and future information relevant to the decision at hand.

B) It focuses on the differences between alternatives.

C) It reduces the time taken to select the best course of action.

D) It makes the evaluation process easier for the decision maker.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 90 في هذه المجموعة.

فتح الحزمة

k this deck

56

Irrelevant costs are costs that are

A) different among alternatives.

B) avoidable costs.

C) opportunity costs.

D) sunk costs.

A) different among alternatives.

B) avoidable costs.

C) opportunity costs.

D) sunk costs.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 90 في هذه المجموعة.

فتح الحزمة

k this deck

57

Avoidable costs are important for

A) sales mix decisions.

B) pricing decisions for special orders.

C) sell or process-further decisions.

D) decisions to eliminate unprofitable segments.

A) sales mix decisions.

B) pricing decisions for special orders.

C) sell or process-further decisions.

D) decisions to eliminate unprofitable segments.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 90 في هذه المجموعة.

فتح الحزمة

k this deck

58

Which of the following could not be a relevant cost in deciding whether or not to eliminate a producing department?

A) The current residual value of the department's equipment

B) The salary of a supervisor who would be laid off

C) The carrying value of the department's equipment

D) Revenue that could be generated by renting out the department's space

A) The current residual value of the department's equipment

B) The salary of a supervisor who would be laid off

C) The carrying value of the department's equipment

D) Revenue that could be generated by renting out the department's space

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 90 في هذه المجموعة.

فتح الحزمة

k this deck

59

The term incremental cost refers to

A) the difference in total costs between alternatives.

B) a cost that does not entail any dollar outlay but that is relevant to the decision-making process.

C) the profit forgone by selecting one choice instead of another.

D) a cost that constitutes expenses to be incurred even though there is no activity.

A) the difference in total costs between alternatives.

B) a cost that does not entail any dollar outlay but that is relevant to the decision-making process.

C) the profit forgone by selecting one choice instead of another.

D) a cost that constitutes expenses to be incurred even though there is no activity.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 90 في هذه المجموعة.

فتح الحزمة

k this deck

60

In a proposal to increase the production of clock radios, the sales managers of Rinaldo Electronics reported the total additional cost required to meet the increased production level. The increase in total cost is known as the

A) opportunity cost.

B) out-of-pocket cost.

C) controllable cost.

D) incremental cost.

A) opportunity cost.

B) out-of-pocket cost.

C) controllable cost.

D) incremental cost.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 90 في هذه المجموعة.

فتح الحزمة

k this deck

61

"Variable costs are relevant and fixed costs are irrelevant." Explain why you agree or disagree with this statement.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 90 في هذه المجموعة.

فتح الحزمة

k this deck

62

Discuss the qualitative factors that should be considered in short-run decision making.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 90 في هذه المجموعة.

فتح الحزمة

k this deck

63

Why is the book value of equipment irrelevant when considering the replacement of equipment?

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 90 في هذه المجموعة.

فتح الحزمة

k this deck

64

An old machine that originally cost $9,500 thus far has accumulated depreciation of $1,900. The remaining useful life is four years, with no salvage value at the end of its useful life. A new machine is now available that costs $8,500, with a useful life of five years and no residual value. The old machine could be sold now for $4,200. The annual cash operating costs for the old machine are $5,000, but for the new machine they would be only $2,500. Gross revenue from the products would be $12,000 annually for either machine. The company should

A) keep the old machine to avoid a $4,200 loss on its disposal.

B) keep the old machine to avoid a $3,400 loss on its disposal.

C) replace the old machine.

D) keep the old machine to avoid an $8,500 decrease in cash.

A) keep the old machine to avoid a $4,200 loss on its disposal.

B) keep the old machine to avoid a $3,400 loss on its disposal.

C) replace the old machine.

D) keep the old machine to avoid an $8,500 decrease in cash.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 90 في هذه المجموعة.

فتح الحزمة

k this deck

65

During 2010, America, Inc., produced, among other products, 9,500 cameras, incurring the following unit costs: $5 in direct materials, $3 in direct labor, $2 in variable overhead, $4 in fixed overhead, $0.50 in variable selling and administrative expenses, and $1 in fixed selling and administrative expenses. An outsider had offered to produce the cameras for $12 each. Assuming that the factory space would have been idle otherwise, acceptance of the outside offer would have

A) lost the company $9,500.

B) saved the company $34,250.

C) saved the company $19,250.

D) lost the company $14,250.

A) lost the company $9,500.

B) saved the company $34,250.

C) saved the company $19,250.

D) lost the company $14,250.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 90 في هذه المجموعة.

فتح الحزمة

k this deck

66

The point at which products are separated in a joint production process is the

A) split-off point.

B) joint product point.

C) separation point.

D) breakeven point.

A) split-off point.

B) joint product point.

C) separation point.

D) breakeven point.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 90 في هذه المجموعة.

فتح الحزمة

k this deck

67

Products Uno, Dos, Tres, and Quatro have contribution margins of $2, $3, $4, and $5, respectively, and require 1.5, 2, 2.5, and 3 machine hours per unit, respectively. Assuming that all units produced could be sold and that total machine hours per month are limited, on which product should the company concentrate its efforts?

A) Dos

B) Quatro

C) Uno

D) Tres

A) Dos

B) Quatro

C) Uno

D) Tres

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 90 في هذه المجموعة.

فتح الحزمة

k this deck

68

Which of the following techniques is most useful for a special order decision?

A) Payback method

B) Present value method

C) Accounting rate-of-return method

D) Incremental analysis

A) Payback method

B) Present value method

C) Accounting rate-of-return method

D) Incremental analysis

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 90 في هذه المجموعة.

فتح الحزمة

k this deck

69

Relevant costs in a sell or process-further decision include

A) costs of additional processing.

B) both additional revenues and additional costs.

C) revenues after additional processing.

D) joint product costs.

A) costs of additional processing.

B) both additional revenues and additional costs.

C) revenues after additional processing.

D) joint product costs.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 90 في هذه المجموعة.

فتح الحزمة

k this deck

70

What two criteria must be met for information to be considered relevant to decision making?

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 90 في هذه المجموعة.

فتح الحزمة

k this deck

71

Anderson Co. makes and uses 5,000 components each year in its manufacturing operations. An outside supplier has offered to supply the components to Anderson at $66 per unit. Anderson's production costs are as follows: If Anderson accepts the order, $8 of fixed overhead per unit will be eliminated.

If the offer is accepted, operating income will

A) increase by $100,000.

B) decrease by $70,000.

C) decrease by $30,000.

D) increase by $60,000.

If Anderson accepts the order, $8 of fixed overhead per unit will be eliminated.If the offer is accepted, operating income will

A) increase by $100,000.

B) decrease by $70,000.

C) decrease by $30,000.

D) increase by $60,000.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 90 في هذه المجموعة.

فتح الحزمة

k this deck

72

The normal selling price of our product is $42 per unit. The costs of production are direct materials, $8; direct labor, $6; variable overhead, $7; and fixed overhead, $4 (based on normal capacity). The company has received a special order for 11,900 units at a unit sales price of $23. There is ample unused capacity to fill the order and $1 per unit will be incurred for additional freight costs. If the order is accepted, operating income will

A) increase by $11,900.

B) decrease by $35,700.

C) increase by $23,800.

D) decrease by $23,800.

A) increase by $11,900.

B) decrease by $35,700.

C) increase by $23,800.

D) decrease by $23,800.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 90 في هذه المجموعة.

فتح الحزمة

k this deck

73

The Norran Company needs 15,000 units of a certain part to use in its production cycle. If Norran buys the part from Waterloo Company instead of making it, Norran could not use the released facilities in another activity; thus, all of the fixed overhead applied will continue regardless of what decision is made. Accounting records provide the following data: Cost to Norran to make the part:

Direct materials, $3

Direct labor, $12

Variable overhead, $13

Fixed overhead applied, $8

Cost to buy the part from the Waterloo Company, $27

In deciding whether to make or buy the part, Norran's total relevant costs to make the part are

A) $360,000.

B) $240,000.

C) $420,000.

D) $405,000.

Direct materials, $3

Direct labor, $12

Variable overhead, $13

Fixed overhead applied, $8

Cost to buy the part from the Waterloo Company, $27

In deciding whether to make or buy the part, Norran's total relevant costs to make the part are

A) $360,000.

B) $240,000.

C) $420,000.

D) $405,000.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 90 في هذه المجموعة.

فتح الحزمة

k this deck

74

The Norran Company needs 15,000 units of a certain part to use in its production cycle. If Norran buys the part from Waterloo Company instead of making it, Norran could not use the released facilities in another activity; thus, all of the fixed overhead applied will continue regardless of what decision is made. Accounting records provide the following data: Cost to Norran to make the part:

Direct materials, $3

Direct labor, $12

Variable overhead, $13

Fixed overhead applied, $8

Cost to buy the part from the Waterloo Company, $27

What should Norran's decision be, and what is the total cost savings that would result?

A) Buy, $90,000

B) Buy, $15,000

C) Make, $90,000

D) Make, $15,000

Direct materials, $3

Direct labor, $12

Variable overhead, $13

Fixed overhead applied, $8

Cost to buy the part from the Waterloo Company, $27

What should Norran's decision be, and what is the total cost savings that would result?

A) Buy, $90,000

B) Buy, $15,000

C) Make, $90,000

D) Make, $15,000

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 90 في هذه المجموعة.

فتح الحزمة

k this deck

75

The costs incurred beyond the split-off point are called

A) split-off point costs.

B) incremental costs.

C) joint product costs.

D) by-product costs.

A) split-off point costs.

B) incremental costs.

C) joint product costs.

D) by-product costs.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 90 في هذه المجموعة.

فتح الحزمة

k this deck

76

Candidates for outsourcing would include

A) custodial services.

B) payroll processing.

C) information management.

D) all of these.

A) custodial services.

B) payroll processing.

C) information management.

D) all of these.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 90 في هذه المجموعة.

فتح الحزمة

k this deck

77

California Chemical Co. produces several chemical compounds. Each compound can be sold at the split-off point or processed further. The following results apply to May: After determining which products should be sold at the split-off point and which should be processed further, the total revenue provided by these three products would be

A) $172,500.

B) $199,000.

C) $200,600.

D) $212,500.

A) $172,500.

B) $199,000.

C) $200,600.

D) $212,500.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 90 في هذه المجموعة.

فتح الحزمة

k this deck

78

Products Green, Red, and White have unit contribution margins of $6.50, $12, and $10, respectively, and require 2, 4, and 3 direct labor hours per unit, respectively. If demand currently is far exceeding supply, on which product should the company concentrate its efforts?

A) Green

B) Red

C) White

D) Either Green or Red

A) Green

B) Red

C) White

D) Either Green or Red

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 90 في هذه المجموعة.

فتح الحزمة

k this deck

79

Anderson Co. makes and uses 5,000 components each year in its manufacturing operations. An outside supplier has offered to supply the components to Anderson at $66 per unit. Anderson's production costs are as follows: If Anderson accepts the order, $8 of fixed overhead per unit will be eliminated.

What is the relevant cost to produce one unit?

A) $86

B) $52

C) $78

D) $60

If Anderson accepts the order, $8 of fixed overhead per unit will be eliminated.What is the relevant cost to produce one unit?

A) $86

B) $52

C) $78

D) $60

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 90 في هذه المجموعة.

فتح الحزمة

k this deck

80

All of the following are relevant in a sell or process-further decision except

A) sales value at the split-off point.

B) sales value after further processing.

C) additional processing costs.

D) joint costs.

A) sales value at the split-off point.

B) sales value after further processing.

C) additional processing costs.

D) joint costs.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 90 في هذه المجموعة.

فتح الحزمة

k this deck

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 90 في هذه المجموعة.