Deck 24: Multistate Corporate Taxation

ملء الشاشة (f)

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

Kurt Corporation realized $600,000 taxable income from the sales of its products in States X and Z.Kurt's activities establish nexus for income tax purposes in both states.Kurt's sales,payroll,and property among the states include the following.  Z utilizes an equally weighted three-factor apportionment formula.Kurt is incorporated in X.How much of Kurt's taxable income is apportioned to Z?

Z utilizes an equally weighted three-factor apportionment formula.Kurt is incorporated in X.How much of Kurt's taxable income is apportioned to Z?

A)$2,000,000.

B)$600,000.

C)$300,000.

D)$100,000.

E)$0.

Z utilizes an equally weighted three-factor apportionment formula.Kurt is incorporated in X.How much of Kurt's taxable income is apportioned to Z?A)$2,000,000.

B)$600,000.

C)$300,000.

D)$100,000.

E)$0.

سؤال

سؤال

سؤال

سؤال

José Corporation realized $600,000 taxable income from the sales of its products in States X and Z.José's activities in both states establish nexus for income tax purposes.José's sales,payroll,and property among the states include the following.  X utilizes an equally weighted three-factor apportionment formula.How much of José's taxable income is apportioned to X?

X utilizes an equally weighted three-factor apportionment formula.How much of José's taxable income is apportioned to X?

A)$600,000.

B)$520,200.

C)$200,000.

D)$79,800.

X utilizes an equally weighted three-factor apportionment formula.How much of José's taxable income is apportioned to X?A)$600,000.

B)$520,200.

C)$200,000.

D)$79,800.

سؤال

سؤال

Perez Corporation is subject to tax only in State

A)$630,000.

A)Perez generated the following income and deductions. Federal taxable income is the starting point in computing A taxable income.State income taxes are not deductible for A tax purposes.Perez's A taxable income is:

Federal taxable income is the starting point in computing A taxable income.State income taxes are not deductible for A tax purposes.Perez's A taxable income is:

B)$600,000.

C)$430,000.

D)$400,000.

A)$630,000.

A)Perez generated the following income and deductions.

Federal taxable income is the starting point in computing A taxable income.State income taxes are not deductible for A tax purposes.Perez's A taxable income is:B)$600,000.

C)$430,000.

D)$400,000.

سؤال

Mandy Corporation realized $1,000,000 taxable income from the sales of its products in States X and Z.Mandy's activities establish nexus for income tax purposes only in Z.Mandy's sales,payroll,and property among the states include the following.  X utilizes a double-weighted sales factor in its three-factor apportionment formula.How much of Mandy's taxable income is apportioned to X?

X utilizes a double-weighted sales factor in its three-factor apportionment formula.How much of Mandy's taxable income is apportioned to X?

A)$1,000,000.

B)$543,333.

C)$490,000.

D)$0.

X utilizes a double-weighted sales factor in its three-factor apportionment formula.How much of Mandy's taxable income is apportioned to X?A)$1,000,000.

B)$543,333.

C)$490,000.

D)$0.

سؤال

سؤال

José Corporation realized $600,000 taxable income from the sales of its products in States X and Z.José's activities in both states establish nexus for income tax purposes.José's sales,payroll,and property among the states include the following.  Z utilizes a double-weighted sales factor in its three-factor apportionment formula.How much of José's taxable income is apportioned to Z?

Z utilizes a double-weighted sales factor in its three-factor apportionment formula.How much of José's taxable income is apportioned to Z?

A)$1,000,000.

B)$600,000.

C)$120,000.

D)$80,000.

E)$0.

Z utilizes a double-weighted sales factor in its three-factor apportionment formula.How much of José's taxable income is apportioned to Z?A)$1,000,000.

B)$600,000.

C)$120,000.

D)$80,000.

E)$0.

سؤال

سؤال

Judy,a regional sales manager,has her office in State X.Her region includes several states,as indicated in the sales report below.Determine how much of Judy's $200,000 compensation is assigned to the payroll factor of State X.

A)$0.

B)$50,000.

C)$60,000.

D)$80,000.

E)$200,000.

A)$0.

B)$50,000.

C)$60,000.

D)$80,000.

E)$200,000.

سؤال

سؤال

سؤال

سؤال

Flake Corporation's property holdings in State E are as follows.  Compute the numerator of Flake's E property factor.

Compute the numerator of Flake's E property factor.

A)$150 million.

B)$145 million.

C)$125 million.

D)$120 million.

E)$100 million.

Compute the numerator of Flake's E property factor.A)$150 million.

B)$145 million.

C)$125 million.

D)$120 million.

E)$100 million.

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

Trayne Corporation's sales office and manufacturing plant are located in State X.Trayne also maintains a manufacturing plant and sales office in State W.For purposes of apportionment,X defines payroll as all compensation paid to employees,including elective contributions to § 401(k)deferred compensation plans.Under the statutes of W,neither compensation paid to officers nor contributions to § 401(k)plans are included in the payroll factor.Trayne incurred the following personnel costs.  Trayne's payroll factor for State X is:

Trayne's payroll factor for State X is:

A)100.00%.

B)80.00%.

C)73.68%.

D)71.43%.

E)50.00%.

Trayne's payroll factor for State X is:A)100.00%.

B)80.00%.

C)73.68%.

D)71.43%.

E)50.00%.

سؤال

سؤال

سؤال

Net Corporation's sales office and manufacturing plant are located in State X.Net also maintains a manufacturing plant and sales office in State W.For purposes of apportionment,X defines payroll as all compensation paid to employees,including contributions to § 401(k)deferred compensation plans.Under the statutes of W,neither compensation paid to officers nor contributions to § 401(k)plans are included in the payroll factor.Net incurred the following personnel costs.  Net's payroll factor for State W is:

Net's payroll factor for State W is:

A)50.00%.

B)28.57%.

C)26.32%.

D)20.00%.

E)0%.

Net's payroll factor for State W is:A)50.00%.

B)28.57%.

C)26.32%.

D)20.00%.

E)0%.

سؤال

State D has adopted the principles of UDITPA.Given the following transactions for the year,determine Comp Corporation's D payroll factor denominator.

A)$700,000.

B)$800,000.

C)$900,000.

D)$1,000,000.

A)$700,000.

B)$800,000.

C)$900,000.

D)$1,000,000.

سؤال

سؤال

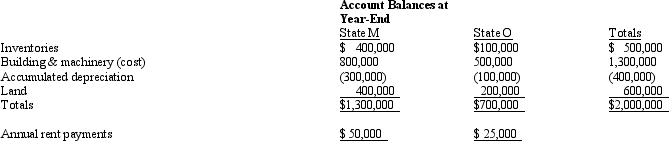

Bert Corporation,a calendar-year taxpayer,owns property in States M and O.Both M and O require that the average value of assets be included in the property factor.M requires that the property be valued at its historical cost,and O requires that the property be included in the property factor at its net depreciated book value.

Bert's M property factor is:

Bert's M property factor is:

A)75.0%.

B)66.7%.

C)64.9%.

D)64.5%.

Bert's M property factor is:A)75.0%.

B)66.7%.

C)64.9%.

D)64.5%.

سؤال

Valdez Corporation,a calendar-year taxpayer,owns property in States M and O.Both M and O require that the average value of assets be included in the property factor.M requires that the property be valued at its historical cost,and O requires that the property be included in the property factor at its net depreciated book value.

Valdez's O property factor is:

Valdez's O property factor is:

A)35.0%.

B)37.2%.

C)39.5%.

D)53.8%.

Valdez's O property factor is:A)35.0%.

B)37.2%.

C)39.5%.

D)53.8%.

سؤال

فتح الحزمة

قم بالتسجيل لفتح البطاقات في هذه المجموعة!

Unlock Deck

Unlock Deck

1/119

العب

ملء الشاشة (f)

Deck 24: Multistate Corporate Taxation

1

If a state follows Federal income tax rules,tax compliance and enforcement become easier to accomplish.

True

2

A typical state taxable income addition modification is the Federal income tax expense.

False

3

Politicians use tax devices to create economic development incentives.

True

4

States use a common apportionment formula and set of factors,known as the Streamlined Sales Tax Method.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 119 في هذه المجموعة.

فتح الحزمة

k this deck

5

Typical indicators of nexus include the presence of employees based in the state,and the ownership or lease of realty there.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 119 في هذه المجموعة.

فتح الحزمة

k this deck

6

Only a few states have adopted an alternative minimum tax,similar to the Federal system.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 119 في هذه المجموعة.

فتح الحزمة

k this deck

7

Roughly one-fifth of all taxes paid by businesses in the U.S.are to state,local,and municipal jurisdictions.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 119 في هذه المجموعة.

فتح الحزمة

k this deck

8

A typical state taxable income addition modification is the income tax paid to the state for the year.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 119 في هذه المجموعة.

فتح الحزمة

k this deck

9

Double weighting the sales factor effectively increases the tax burden on taxpayers based in the state,such as corporations with in-state headquarters.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 119 في هذه المجموعة.

فتح الحزمة

k this deck

10

The corporate income tax provides about one-half of the annual tax revenues for the typical U.S.state.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 119 في هذه المجموعة.

فتح الحزمة

k this deck

11

State and local politicians tend to apply new and increased taxes to taxpayers who are visitors to the jurisdiction and cannot vote to reelect the lawmaker.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 119 في هذه المجموعة.

فتح الحزمة

k this deck

12

All but a few states have adopted a tax based on net taxable income.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 119 في هذه المجموعة.

فتح الحزمة

k this deck

13

States collect the most tax dollars from the sales/use tax.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 119 في هذه المجموعة.

فتح الحزمة

k this deck

14

A state cannot levy a tax on a business unless the business was incorporated in the state.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 119 في هذه المجموعة.

فتح الحزمة

k this deck

15

Under P.L.86-272,the taxpayer is exempt from state taxes on income resulting from the mere solicitation of orders for the sale of tangible personal property in the state.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 119 في هذه المجموعة.

فتح الحزمة

k this deck

16

Usually a business chooses a location where it will build a new plant based chiefly on tax considerations.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 119 في هذه المجموعة.

فتح الحزمة

k this deck

17

In most states,a taxpayer's income is apportioned on the basis of a formula measuring the extent of business contact,and allocated according to the location of property owned or used.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 119 في هذه المجموعة.

فتح الحزمة

k this deck

18

A state or local tax on a corporation's income might be called a franchise tax or a business privilege tax.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 119 في هذه المجموعة.

فتح الحزمة

k this deck

19

Nonbusiness income includes rentals of investment property.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 119 في هذه المجموعة.

فتح الحزمة

k this deck

20

Most states begin the computation of taxable income with an amount from the Federal income tax return.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 119 في هذه المجموعة.

فتح الحزمة

k this deck

21

Typically exempt from the sales/use tax base is the purchase of computer and cell phone equipment by a large consulting firm that is incorporated in the state.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 119 في هذه المجموعة.

فتح الحزمة

k this deck

22

Typically exempt from the sales/use tax base is the purchase of inventory from a competitor who is closing down a long-lived business.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 119 في هذه المجموعة.

فتح الحزمة

k this deck

23

A unitary business is treated as a single entity for state tax purposes,with a combined apportionment formula including data from all of the operations of the business.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 119 في هذه المجموعة.

فتح الحزمة

k this deck

24

Most states waive the collection of sales tax on groceries.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 119 في هذه المجموعة.

فتح الحزمة

k this deck

25

The use tax is designed to complement the sales tax.A use tax typically covers purchases made out of state and brought into the jurisdiction.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 119 في هذه المجموعة.

فتح الحزمة

k this deck

26

S corporations must withhold taxes on the portions of the entity's income allocated to its shareholders.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 119 في هذه المجموعة.

فتح الحزمة

k this deck

27

The property factor includes assets that the taxpayer owns,but not those merely used under a lease agreement.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 119 في هذه المجموعة.

فتح الحزمة

k this deck

28

Almost all of the states assess some form of consumer-level sales tax.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 119 في هذه المجموعة.

فتح الحزمة

k this deck

29

Most states' consumer sales taxes apply directly to the final purchaser of the taxable asset,with the purchaser remitting the tax to the state treasury.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 119 في هذه المجموعة.

فتح الحزمة

k this deck

30

Typically exempt from the sales/use tax base is the purchase of seed and feed by a farmer.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 119 في هذه المجموعة.

فتح الحزمة

k this deck

31

An LLC apportions and allocates its annual taxable income in the same manner used by any other business operating in the state.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 119 في هذه المجموعة.

فتح الحزمة

k this deck

32

A service engineer spends 60% of her time maintaining the employer's productive business property and 40% maintaining the employer's nonbusiness rental properties.This year,her compensation totaled $90,000.The payroll factor assigns $90,000 to the state in which the employer is based.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 119 في هذه المجموعة.

فتح الحزمة

k this deck

33

A few states recognize an entity's S corporation status,such that taxable income flows through directly to shareholders,but they also assess a state-level tax on the entity.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 119 في هذه المجموعة.

فتح الحزمة

k this deck

34

Typically exempt from the sales/use tax base is the purchase of lumber by a do-it-yourself homeowner,when she builds a deck onto her patio.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 119 في هذه المجموعة.

فتح الحزمة

k this deck

35

Typically exempt from the sales/use tax base is the purchase of prescription medicines by an individual.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 119 في هذه المجموعة.

فتح الحزمة

k this deck

36

The property factor includes real property and construction in progress.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 119 في هذه المجموعة.

فتح الحزمة

k this deck

37

Typically exempt from the sales/use tax base is the purchase by a church of printed music for its choir.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 119 في هذه المجموعة.

فتح الحزمة

k this deck

38

Only a few states require that Federal S corporations make a separate state-level election of the flow-through status.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 119 في هذه المجموعة.

فتح الحزمة

k this deck

39

An assembly worker earns a $30,000 salary and receives a fringe benefit package worth $15,000.The payroll factor assigns $45,000 for this employee.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 119 في هذه المجموعة.

فتح الحزمة

k this deck

40

By making a water's edge election,the multinational taxpayer can limit the reach of the unitary theory to U.S.-based factors and income.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 119 في هذه المجموعة.

فتح الحزمة

k this deck

41

The throwback rule requires that:

A)Sales of services are attributed to the state of commercial domicile.

B)Capital gain/loss is attributed to the state of commercial domicile.

C)Services are attributed to the state of commercial domicile of the taxpayer,and are not taxable in the state where they were performed.

D)Sales of tangible personal property are attributed to the state where they originated,if the taxpayer is not taxable in the state of destination.

A)Sales of services are attributed to the state of commercial domicile.

B)Capital gain/loss is attributed to the state of commercial domicile.

C)Services are attributed to the state of commercial domicile of the taxpayer,and are not taxable in the state where they were performed.

D)Sales of tangible personal property are attributed to the state where they originated,if the taxpayer is not taxable in the state of destination.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 119 في هذه المجموعة.

فتح الحزمة

k this deck

42

The typical local property tax falls on both an investor's real estate and her stock portfolio.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 119 في هذه المجموعة.

فتح الحزمة

k this deck

43

Use tax would be due if an individual purchased an auto in State A and used it at his home in State

B.

B.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 119 في هذه المجموعة.

فتح الحزمة

k this deck

44

Which of the following is not immune from state income taxation,even if P.L.86-272 is in effect?

A)Sale of a share of corporate stock.

B)Sale of office equipment that constitutes inventory to the purchaser.

C)Sale of office equipment to be used in the taxpayer's business.

D)All of the above are protected by P.L.86-272 immunity provisions.

A)Sale of a share of corporate stock.

B)Sale of office equipment that constitutes inventory to the purchaser.

C)Sale of office equipment to be used in the taxpayer's business.

D)All of the above are protected by P.L.86-272 immunity provisions.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 119 في هذه المجموعة.

فتح الحزمة

k this deck

45

Under most local property tax laws,the value of an asset is fixed after an appraisal by the taxing jurisdiction.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 119 في هذه المجموعة.

فتح الحزمة

k this deck

46

Federal taxable income is used as the starting point in computing the state's income tax base,but numerous state adjustments or modifications generally are required to:

A)Reflect differences between state and Federal tax statutes.

B)Remove income that a state is constitutionally prohibited from taxing.

C)Allow for all of the states to use the same definition of taxable income.

D)a.and b.

A)Reflect differences between state and Federal tax statutes.

B)Remove income that a state is constitutionally prohibited from taxing.

C)Allow for all of the states to use the same definition of taxable income.

D)a.and b.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 119 في هذه المجموعة.

فتح الحزمة

k this deck

47

Norman Corporation owns and operates two manufacturing facilities,one in State X and the other in State Y.Due to a temporary decline in the corporation's sales,Norman has rented 20% of its Y facility to an unaffiliated corporation.Norman generated $1,000,000 net rental income and $2,000,000 income from manufacturing. Norman is incorporated in Y.For X and Y purposes,rental income is classified as allocable nonbusiness income.By applying the statutes of each state,Norman determined that its apportionment factors are .75 for X and .25 for Y.

Norman's income attributed to X is:

A)$0.

B)$1,000,000.

C)$1,500,000.

D)$2,000,000.

E)$3,000,000.

Norman's income attributed to X is:

A)$0.

B)$1,000,000.

C)$1,500,000.

D)$2,000,000.

E)$3,000,000.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 119 في هذه المجموعة.

فتح الحزمة

k this deck

48

In determining state taxable income,all of the following are adjustments to Federal income except:

A)Net operating loss.

B)Federal income tax expense.

C)Cost of goods sold.

D)State income tax refunds.

A)Net operating loss.

B)Federal income tax expense.

C)Cost of goods sold.

D)State income tax refunds.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 119 في هذه المجموعة.

فتح الحزمة

k this deck

49

State A applies a throwback rule.General Corporation is taxable in a number of states.This year,General made a $100,000 sale from its A headquarters to an agency of the U.S.government.In which state(s)will the sale be included in the sales factor?

A)

A)All in

B)In none of the states,under the doctrine of indeterminate destination.

C)In all of the states,according to the apportionment formulas of each,as the U.S.government is present in all states.

D)One-half in A,with the balance exempted from other states' sales factors under the Colgate doctrine.

A)

A)All in

B)In none of the states,under the doctrine of indeterminate destination.

C)In all of the states,according to the apportionment formulas of each,as the U.S.government is present in all states.

D)One-half in A,with the balance exempted from other states' sales factors under the Colgate doctrine.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 119 في هذه المجموعة.

فتح الحزمة

k this deck

50

Dough Company sold an asset on the first day of the tax year for $500,000.Dough's Federal tax basis for the asset was $300,000.Because of differences in cost recovery schedules,the state regular-tax basis in the asset was $350,000.What adjustment,if any,should be made to Federal taxable income in determining the correct taxable income for the typical state?

A)($50,000).

B)$35,000.

C)$50,000.

D)$0.

A)($50,000).

B)$35,000.

C)$50,000.

D)$0.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 119 في هذه المجموعة.

فتح الحزمة

k this deck

51

Kurt Corporation realized $600,000 taxable income from the sales of its products in States X and Z.Kurt's activities establish nexus for income tax purposes in both states.Kurt's sales,payroll,and property among the states include the following. Z utilizes an equally weighted three-factor apportionment formula.Kurt is incorporated in X.How much of Kurt's taxable income is apportioned to Z?

A)$2,000,000.

B)$600,000.

C)$300,000.

D)$100,000.

E)$0.

Z utilizes an equally weighted three-factor apportionment formula.Kurt is incorporated in X.How much of Kurt's taxable income is apportioned to Z?A)$2,000,000.

B)$600,000.

C)$300,000.

D)$100,000.

E)$0.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 119 في هذه المجموعة.

فتح الحزمة

k this deck

52

In determining a corporation's taxable income for state income tax purposes,which of the following does not constitute a subtraction from Federal income?

A)Interest on U.S.obligations.

B)Expenses that are directly or indirectly related to state and municipal interest that is taxable for state purposes.

C)The amount by which the Federal deduction for depreciation exceeds the depreciation deduction permitted for state tax purposes.

D)The amount by which the state loss from the disposal of assets exceeds the Federal loss from such disposal.

A)Interest on U.S.obligations.

B)Expenses that are directly or indirectly related to state and municipal interest that is taxable for state purposes.

C)The amount by which the Federal deduction for depreciation exceeds the depreciation deduction permitted for state tax purposes.

D)The amount by which the state loss from the disposal of assets exceeds the Federal loss from such disposal.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 119 في هذه المجموعة.

فتح الحزمة

k this deck

53

Under P.L.86-272,which of the following transactions by itself would create nexus with a state?

A)Inspection by a sales employee of the customer's inventory for specific product lines.

B)Using an independent contractor who acts as a manufacturer's representative for the taxpayer through a sales office in the state.

C)Executing a sales campaign,using an advertising agency acting as an independent contractor for the taxpayer.

D)Maintenance of inventory in the state by an independent contractor under a consignment plan.

A)Inspection by a sales employee of the customer's inventory for specific product lines.

B)Using an independent contractor who acts as a manufacturer's representative for the taxpayer through a sales office in the state.

C)Executing a sales campaign,using an advertising agency acting as an independent contractor for the taxpayer.

D)Maintenance of inventory in the state by an independent contractor under a consignment plan.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 119 في هذه المجموعة.

فتح الحزمة

k this deck

54

Wailes Corporation is subject to a corporate income tax only in State X.The starting point in computing X taxable income is Federal taxable income.Wailes' Federal taxable income is $750,000,which includes a $75,000 deduction for state income taxes.During the year,Wailes received $20,000 interest on Federal obligations.X tax law does not allow a deduction for state income tax payments. Wailes' taxable income for X purposes is:

A)$825,000.

B)$805,000.

C)$750,000.

D)$680,000.

A)$825,000.

B)$805,000.

C)$750,000.

D)$680,000.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 119 في هذه المجموعة.

فتح الحزمة

k this deck

55

José Corporation realized $600,000 taxable income from the sales of its products in States X and Z.José's activities in both states establish nexus for income tax purposes.José's sales,payroll,and property among the states include the following. X utilizes an equally weighted three-factor apportionment formula.How much of José's taxable income is apportioned to X?

A)$600,000.

B)$520,200.

C)$200,000.

D)$79,800.

X utilizes an equally weighted three-factor apportionment formula.How much of José's taxable income is apportioned to X?A)$600,000.

B)$520,200.

C)$200,000.

D)$79,800.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 119 في هذه المجموعة.

فتح الحزمة

k this deck

56

Under P.L.86-272,which of the following transactions by itself would create nexus with a state?

A)Order solicitation for a computer,approved and filled from another state.

B)Order solicitation for a marketable security,approved,and filled from another state.

C)Order solicitation for a machine,with credit approval from another state.

D)The conduct of a training seminar for customers as to how to install and operate a new software product.

A)Order solicitation for a computer,approved and filled from another state.

B)Order solicitation for a marketable security,approved,and filled from another state.

C)Order solicitation for a machine,with credit approval from another state.

D)The conduct of a training seminar for customers as to how to install and operate a new software product.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 119 في هذه المجموعة.

فتح الحزمة

k this deck

57

Perez Corporation is subject to tax only in State

A)$630,000.

A)Perez generated the following income and deductions. Federal taxable income is the starting point in computing A taxable income.State income taxes are not deductible for A tax purposes.Perez's A taxable income is:

B)$600,000.

C)$430,000.

D)$400,000.

A)$630,000.

A)Perez generated the following income and deductions.

Federal taxable income is the starting point in computing A taxable income.State income taxes are not deductible for A tax purposes.Perez's A taxable income is:B)$600,000.

C)$430,000.

D)$400,000.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 119 في هذه المجموعة.

فتح الحزمة

k this deck

58

Mandy Corporation realized $1,000,000 taxable income from the sales of its products in States X and Z.Mandy's activities establish nexus for income tax purposes only in Z.Mandy's sales,payroll,and property among the states include the following. X utilizes a double-weighted sales factor in its three-factor apportionment formula.How much of Mandy's taxable income is apportioned to X?

A)$1,000,000.

B)$543,333.

C)$490,000.

D)$0.

X utilizes a double-weighted sales factor in its three-factor apportionment formula.How much of Mandy's taxable income is apportioned to X?A)$1,000,000.

B)$543,333.

C)$490,000.

D)$0.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 119 في هذه المجموعة.

فتح الحزمة

k this deck

59

The typical state sales/use tax falls on sales of both products and services.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 119 في هذه المجموعة.

فتح الحزمة

k this deck

60

José Corporation realized $600,000 taxable income from the sales of its products in States X and Z.José's activities in both states establish nexus for income tax purposes.José's sales,payroll,and property among the states include the following. Z utilizes a double-weighted sales factor in its three-factor apportionment formula.How much of José's taxable income is apportioned to Z?

A)$1,000,000.

B)$600,000.

C)$120,000.

D)$80,000.

E)$0.

Z utilizes a double-weighted sales factor in its three-factor apportionment formula.How much of José's taxable income is apportioned to Z?A)$1,000,000.

B)$600,000.

C)$120,000.

D)$80,000.

E)$0.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 119 في هذه المجموعة.

فتح الحزمة

k this deck

61

A state sales tax usually falls upon:

A)The sale of a used dinette set sold at a rummage sale.

B)The sale of a dinette set by the manufacturer to the retailer.

C)The purchase of a Bible by a member at the church's bookstore.

D)The sale of a case of Bibles by the publisher to a church bookstore.

E)All of the above are exempt transactions.

A)The sale of a used dinette set sold at a rummage sale.

B)The sale of a dinette set by the manufacturer to the retailer.

C)The purchase of a Bible by a member at the church's bookstore.

D)The sale of a case of Bibles by the publisher to a church bookstore.

E)All of the above are exempt transactions.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 119 في هذه المجموعة.

فتح الحزمة

k this deck

62

Judy,a regional sales manager,has her office in State X.Her region includes several states,as indicated in the sales report below.Determine how much of Judy's $200,000 compensation is assigned to the payroll factor of State X.

A)$0.

B)$50,000.

C)$60,000.

D)$80,000.

E)$200,000.

A)$0.

B)$50,000.

C)$60,000.

D)$80,000.

E)$200,000.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 119 في هذه المجموعة.

فتح الحزمة

k this deck

63

In determining taxable income for state income tax purposes,state income tax refunds typically constitute a(n)____________________ modification.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 119 في هذه المجموعة.

فتح الحزمة

k this deck

64

Parent and Junior form a non-unitary group of corporations.Parent is located in a state with an effective tax rate of 3%,while Junior's effective tax rate is 9%.Acting in concert to reduce overall tax liabilities,the group should:

A)Execute an intercompany loan,such that Junior pays deductible interest to Parent.

B)Have Parent charge Junior an annual management fee.

C)Shift Parent's high-cost assembly and distribution operations to Junior.

D)All of the above are effective income-shifting techniques for a non-unitary group.

E)None of the above is an effective income-shifting technique for a non-unitary group.

A)Execute an intercompany loan,such that Junior pays deductible interest to Parent.

B)Have Parent charge Junior an annual management fee.

C)Shift Parent's high-cost assembly and distribution operations to Junior.

D)All of the above are effective income-shifting techniques for a non-unitary group.

E)None of the above is an effective income-shifting technique for a non-unitary group.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 119 في هذه المجموعة.

فتح الحزمة

k this deck

65

In the broadest application of the unitary theory,the U.S.unitary business files a combined tax return using factors and income amounts for all affiliates:

A)Organized in the U.S.

B)Organized anywhere in the world.

C)Organized in NAFTA countries.

D)Owned more than 50% by other affiliates in the group.

A)Organized in the U.S.

B)Organized anywhere in the world.

C)Organized in NAFTA countries.

D)Owned more than 50% by other affiliates in the group.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 119 في هذه المجموعة.

فتح الحزمة

k this deck

66

Flake Corporation's property holdings in State E are as follows. Compute the numerator of Flake's E property factor.

A)$150 million.

B)$145 million.

C)$125 million.

D)$120 million.

E)$100 million.

Compute the numerator of Flake's E property factor.A)$150 million.

B)$145 million.

C)$125 million.

D)$120 million.

E)$100 million.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 119 في هذه المجموعة.

فتح الحزمة

k this deck

67

In determining taxable income for state income tax purposes,a Federal NOL deduction may constitute a(n)____________________ modification.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 119 في هذه المجموعة.

فتح الحزمة

k this deck

68

Parent and Junior form a unitary group of corporations.Parent is located in a state with an effective tax rate of 3%,while Junior's effective tax rate is 9%.Acting in concert to reduce overall tax liabilities,the group should:

A)Execute an intercompany loan,such that Junior pays deductible interest to Parent.

B)Have Parent charge Junior an annual management fee.

C)Shift Parent's high-cost assembly and distribution operations to Junior.

D)All of the above are effective income-shifting techniques for a unitary group.

E)None of the above is an effective income-shifting technique for a unitary group.

A)Execute an intercompany loan,such that Junior pays deductible interest to Parent.

B)Have Parent charge Junior an annual management fee.

C)Shift Parent's high-cost assembly and distribution operations to Junior.

D)All of the above are effective income-shifting techniques for a unitary group.

E)None of the above is an effective income-shifting technique for a unitary group.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 119 في هذه المجموعة.

فتح الحزمة

k this deck

69

When the taxpayer operates in one or more unitary states:

A)Apportionment factors are computed on a group-wide basis.

B)The tax incentive of creating nexus in a low-tax state is enhanced.

C)The tax benefit of a passive investment subsidiary holding company is neutralized.

D)The use of a water's edge election should be considered.

E)All of the above are true.

A)Apportionment factors are computed on a group-wide basis.

B)The tax incentive of creating nexus in a low-tax state is enhanced.

C)The tax benefit of a passive investment subsidiary holding company is neutralized.

D)The use of a water's edge election should be considered.

E)All of the above are true.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 119 في هذه المجموعة.

فتح الحزمة

k this deck

70

A use tax:

A)Applies when a State A resident purchases a new automobile from a State A dealership.

B)Applies when a State A resident purchases a new automobile from a State B dealership,then driving the car home.

C)Applies when a State A resident purchases groceries from a neighborhood store.

D)Applies when a State A resident purchases hardware from sears.com rather than at the Best Buy store at the local mall.

A)Applies when a State A resident purchases a new automobile from a State A dealership.

B)Applies when a State A resident purchases a new automobile from a State B dealership,then driving the car home.

C)Applies when a State A resident purchases groceries from a neighborhood store.

D)Applies when a State A resident purchases hardware from sears.com rather than at the Best Buy store at the local mall.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 119 في هذه المجموعة.

فتح الحزمة

k this deck

71

A state sales tax usually falls upon:

A)Sales of groceries.

B)Sales made to out-of-state customers.

C)Sales made to the U.S.Department of Education.

D)Sales made to the ultimate consumer of the product or service.

A)Sales of groceries.

B)Sales made to out-of-state customers.

C)Sales made to the U.S.Department of Education.

D)Sales made to the ultimate consumer of the product or service.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 119 في هذه المجموعة.

فتح الحزمة

k this deck

72

Trayne Corporation's sales office and manufacturing plant are located in State X.Trayne also maintains a manufacturing plant and sales office in State W.For purposes of apportionment,X defines payroll as all compensation paid to employees,including elective contributions to § 401(k)deferred compensation plans.Under the statutes of W,neither compensation paid to officers nor contributions to § 401(k)plans are included in the payroll factor.Trayne incurred the following personnel costs. Trayne's payroll factor for State X is:

A)100.00%.

B)80.00%.

C)73.68%.

D)71.43%.

E)50.00%.

Trayne's payroll factor for State X is:A)100.00%.

B)80.00%.

C)73.68%.

D)71.43%.

E)50.00%.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 119 في هذه المجموعة.

فتح الحزمة

k this deck

73

A taxpayer wishing to reduce the negative tax effects of the application of the unitary theory might:

A)Affiliate with a service division that shows an operating loss,like one in marketing.

B)Disengage unitary operations with the most profitable affiliates.

C)Add a profitable entity to the unitary group.

D)a.and b.

A)Affiliate with a service division that shows an operating loss,like one in marketing.

B)Disengage unitary operations with the most profitable affiliates.

C)Add a profitable entity to the unitary group.

D)a.and b.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 119 في هذه المجموعة.

فتح الحزمة

k this deck

74

For most taxpayers,which of the traditional apportionment factors yields the greatest opportunities for tax reduction?

A)Payroll.

B)Property.

C)Unitary.

D)Sales (gross receipts).

A)Payroll.

B)Property.

C)Unitary.

D)Sales (gross receipts).

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 119 في هذه المجموعة.

فتح الحزمة

k this deck

75

Net Corporation's sales office and manufacturing plant are located in State X.Net also maintains a manufacturing plant and sales office in State W.For purposes of apportionment,X defines payroll as all compensation paid to employees,including contributions to § 401(k)deferred compensation plans.Under the statutes of W,neither compensation paid to officers nor contributions to § 401(k)plans are included in the payroll factor.Net incurred the following personnel costs. Net's payroll factor for State W is:

A)50.00%.

B)28.57%.

C)26.32%.

D)20.00%.

E)0%.

Net's payroll factor for State W is:A)50.00%.

B)28.57%.

C)26.32%.

D)20.00%.

E)0%.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 119 في هذه المجموعة.

فتح الحزمة

k this deck

76

State D has adopted the principles of UDITPA.Given the following transactions for the year,determine Comp Corporation's D payroll factor denominator.

A)$700,000.

B)$800,000.

C)$900,000.

D)$1,000,000.

A)$700,000.

B)$800,000.

C)$900,000.

D)$1,000,000.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 119 في هذه المجموعة.

فتح الحزمة

k this deck

77

In conducting multistate tax planning,the taxpayer should:

A)Review tax opportunities in light of their effect on the overall business.

B)Consider additional administrative costs generated by the plan.

C)Exploit inconsistencies among the statutes and formulas of the states.

D)Recognize that minimizing state tax costs may not always be prudent.

E)All of the above are true.

A)Review tax opportunities in light of their effect on the overall business.

B)Consider additional administrative costs generated by the plan.

C)Exploit inconsistencies among the statutes and formulas of the states.

D)Recognize that minimizing state tax costs may not always be prudent.

E)All of the above are true.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 119 في هذه المجموعة.

فتح الحزمة

k this deck

78

Bert Corporation,a calendar-year taxpayer,owns property in States M and O.Both M and O require that the average value of assets be included in the property factor.M requires that the property be valued at its historical cost,and O requires that the property be included in the property factor at its net depreciated book value. Bert's M property factor is:

A)75.0%.

B)66.7%.

C)64.9%.

D)64.5%.

Bert's M property factor is:A)75.0%.

B)66.7%.

C)64.9%.

D)64.5%.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 119 في هذه المجموعة.

فتح الحزمة

k this deck

79

Valdez Corporation,a calendar-year taxpayer,owns property in States M and O.Both M and O require that the average value of assets be included in the property factor.M requires that the property be valued at its historical cost,and O requires that the property be included in the property factor at its net depreciated book value. Valdez's O property factor is:

A)35.0%.

B)37.2%.

C)39.5%.

D)53.8%.

Valdez's O property factor is:A)35.0%.

B)37.2%.

C)39.5%.

D)53.8%.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 119 في هذه المجموعة.

فتح الحزمة

k this deck

80

In most states,a limited liability company (LLC)is subject to the state income tax:

A)As though it were a C corporation.

B)As though it were a business trust.

C)As a flow-through entity,similar to its Federal income tax treatment.

D)LLCs typically are exempted from state income taxation.

A)As though it were a C corporation.

B)As though it were a business trust.

C)As a flow-through entity,similar to its Federal income tax treatment.

D)LLCs typically are exempted from state income taxation.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 119 في هذه المجموعة.

فتح الحزمة

k this deck

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 119 في هذه المجموعة.