Deck 4: Cost Behavior and Cost-Volume-Profit Analysis

ملء الشاشة (f)

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

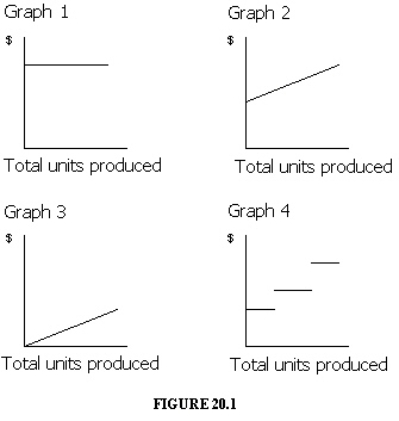

Which of the graphs in Figure 20-1 illustrates the behavior of a total fixed cost?

Which of the graphs in Figure 20-1 illustrates the behavior of a total fixed cost?A) Graph 2

B) Graph 3

C) Graph 4

D) Graph 1

سؤال

سؤال

Which of the graphs in Figure 20-1 illustrates the behavior of a total variable cost?

Which of the graphs in Figure 20-1 illustrates the behavior of a total variable cost?A) Graph 2

B) Graph 3

C) Graph 4

D) Graph 1

سؤال

سؤال

سؤال

سؤال

Which of the graphs in Figure 20-1 illustrates the nature of a mixed cost?

Which of the graphs in Figure 20-1 illustrates the nature of a mixed cost?A) Graph 2

B) Graph 3

C) Graph 4

D) Graph 1

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

فتح الحزمة

قم بالتسجيل لفتح البطاقات في هذه المجموعة!

Unlock Deck

Unlock Deck

1/217

العب

ملء الشاشة (f)

Deck 4: Cost Behavior and Cost-Volume-Profit Analysis

1

Direct materials and direct labor costs are examples of variable costs of production.

True

2

Because variable costs are assumed to change in direct proportion to changes in the activity level, the graph of the variable costs when plotted against the activity level appears as a circle.

False

3

Unit variable cost does not change as the number of units of activity changes.

True

4

Variable costs are costs that remain constant in total dollar amount as the level of activity changes.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 217 في هذه المجموعة.

فتح الحزمة

k this deck

5

Variable costs are costs that vary on a per-unit basis with changes in the activity level.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 217 في هذه المجموعة.

فتح الحزمة

k this deck

6

A mixed cost has characteristics of both a variable and a fixed cost.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 217 في هذه المجموعة.

فتح الحزمة

k this deck

7

Variable costs are costs that vary in total in direct proportion to changes in the activity level.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 217 في هذه المجموعة.

فتح الحزمة

k this deck

8

The fixed cost per unit varies with changes in the level of activity.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 217 في هذه المجموعة.

فتح الحزمة

k this deck

9

In order to choose the proper activity base for a cost, managerial accountants must be familiar with the operations of the entity.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 217 في هذه المجموعة.

فتح الحزمة

k this deck

10

The relevant range is useful for analyzing cost behavior for management decision-making purposes.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 217 في هذه المجموعة.

فتح الحزمة

k this deck

11

Cost behavior refers to the methods used to estimate costs for use in managerial decision making.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 217 في هذه المجموعة.

فتح الحزمة

k this deck

12

The relevant activity base for a cost depends upon which base is most closely associated with the cost and the decision-making needs of management.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 217 في هذه المجموعة.

فتح الحزمة

k this deck

13

The range of activity over which changes in cost are of interest to management is called the relevant range.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 217 في هذه المجموعة.

فتح الحزمة

k this deck

14

Total variable costs change as the level of activity changes.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 217 في هذه المجموعة.

فتح الحزمة

k this deck

15

A production supervisor's salary that does not vary with the number of units produced is an example of a fixed cost.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 217 في هذه المجموعة.

فتح الحزمة

k this deck

16

Variable costs are costs that remain constant on a per-unit basis as the level of activity changes.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 217 في هذه المجموعة.

فتح الحزمة

k this deck

17

Rental charges of $40,000 per year plus $3 for each machine hour over 18,000 hours is an example of a fixed cost.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 217 في هذه المجموعة.

فتح الحزمة

k this deck

18

Cost behavior refers to the manner in which a cost changes as the related activity changes.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 217 في هذه المجموعة.

فتح الحزمة

k this deck

19

Direct materials cost that varies with the number of units produced is an example of a fixed cost of production.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 217 في هذه المجموعة.

فتح الحزمة

k this deck

20

Total fixed costs change as the level of activity changes.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 217 في هذه المجموعة.

فتح الحزمة

k this deck

21

If sales total $2,000,000, fixed costs total $800,000, and variable costs are 60% of sales, the contribution margin ratio is 60%.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 217 في هذه المجموعة.

فتح الحزمة

k this deck

22

If fixed costs are $500,000 and variable costs are 60% of break-even sales, profit is zero when sales revenue is $930,000.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 217 في هذه المجموعة.

فتح الحزمة

k this deck

23

If the property tax rates are increased, this change in fixed costs will result in a decrease in the break-even point.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 217 في هذه المجموعة.

فتح الحزمة

k this deck

24

A rental cost of $20,000 plus $.70 per machine hour of use is an example of a mixed cost.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 217 في هذه المجموعة.

فتح الحزمة

k this deck

25

If employees accept a wage contract that increases the unit contribution margin, the break-even point will decrease.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 217 في هذه المجموعة.

فتح الحزمة

k this deck

26

The point in operations at which revenues and expired costs are exactly equal is called the break-even point.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 217 في هذه المجموعة.

فتح الحزمة

k this deck

27

If fixed costs are $850,000 and the unit contribution margin is $50, profit is zero when 15,000 units are sold.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 217 في هذه المجموعة.

فتح الحزمة

k this deck

28

Variable costs as a percentage of sales are equal to 100% minus the contribution margin ratio.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 217 في هذه المجموعة.

فتح الحزمة

k this deck

29

If direct materials cost per unit increases, the break-even point will increase.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 217 في هذه المجموعة.

فتح الحزمة

k this deck

30

The dollars available from each unit of sales to cover fixed cost and profit is the unit variable cost.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 217 في هذه المجموعة.

فتح الحزمة

k this deck

31

For purposes of analysis, mixed costs can generally be separated into their variable and fixed components.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 217 في هذه المجموعة.

فتح الحزمة

k this deck

32

The data required for determining the break-even point for a business are the total estimated fixed costs for a period, stated as a percentage of net sales.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 217 في هذه المجموعة.

فتح الحزمة

k this deck

33

The contribution margin ratio is the same as the profit-volume ratio.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 217 في هذه المجموعة.

فتح الحزمة

k this deck

34

If sales total $2,000,000, fixed costs total $800,000, and variable costs are 60% of sales, the contribution margin ratio is 40%.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 217 في هذه المجموعة.

فتح الحزمة

k this deck

35

If yearly insurance premiums are increased, this change in fixed costs will result in an increase in the break-even point.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 217 في هذه المجموعة.

فتح الحزمة

k this deck

36

If direct materials cost per unit increases, the break-even point will decrease.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 217 في هذه المجموعة.

فتح الحزمة

k this deck

37

If employees accept a wage contract that decreases the unit contribution margin, the break-even point will decrease.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 217 في هذه المجموعة.

فتح الحزمة

k this deck

38

If direct materials cost per unit decreases, the amount of sales necessary to earn a desired amount of profit will decrease.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 217 في هذه المجموعة.

فتح الحزمة

k this deck

39

Break-even analysis is one type of cost-volume-profit analysis.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 217 في هذه المجموعة.

فتح الحزمة

k this deck

40

The ratio that indicates the percentage of each sales dollar available to cover the fixed costs and to provide operating income is termed the contribution margin ratio.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 217 في هذه المجموعة.

فتح الحزمة

k this deck

41

If the volume of sales is $6,000,000 and sales at the break-even point amount to $4,800,000, the margin of safety is 25%.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 217 في هذه المجموعة.

فتح الحزمة

k this deck

42

Cost-volume-profit analysis can be presented in both equation form and graphic form.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 217 في هذه المجموعة.

فتح الحزمة

k this deck

43

If fixed costs are $450,000 and the unit contribution margin is $50, the sales necessary to earn an operating income of $50,000 are 10,000 units.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 217 في هذه المجموعة.

فتح الحزمة

k this deck

44

Even if a business sells six products, it is possible to estimate the break-even point.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 217 في هذه المجموعة.

فتح الحزمة

k this deck

45

If the volume of sales is $7,000,000 and sales at the break-even point amount to $4,800,000, the margin of safety is 45.8%.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 217 في هذه المجموعة.

فتح الحزمة

k this deck

46

Absorption costing is required for financial reporting under generally accepted accounting principles.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 217 في هذه المجموعة.

فتح الحزمة

k this deck

47

The reliability of cost-volume-profit analysis does NOT depend on the assumption that costs can be accurately divided into fixed and variable components.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 217 في هذه المجموعة.

فتح الحزمة

k this deck

48

Only a single line, which represents the difference between total sales revenues and total costs, is plotted on the profit-volume chart.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 217 في هذه المجموعة.

فتح الحزمة

k this deck

49

A low operating leverage is normal for highly automated industries.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 217 في هذه المجموعة.

فتح الحزمة

k this deck

50

Assuming no other changes, operating income will be the same under both the variable and absorption costing methods when the number of units manufactured equals the number of units sold.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 217 في هذه المجموعة.

فتح الحزمة

k this deck

51

Only a single line, which represents the difference between total sales revenues and total costs, is plotted on the cost-volume-profit chart.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 217 في هذه المجموعة.

فتح الحزمة

k this deck

52

The adoption of variable costing for managerial decision making is based on the premise that fixed factory overhead costs are related to productive capacity of the manufacturing plant and are normally not affected by the number of units produced.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 217 في هذه المجموعة.

فتح الحزمة

k this deck

53

If a business sells two products, it is not possible to estimate the break-even point.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 217 في هذه المجموعة.

فتح الحزمة

k this deck

54

If a business sells four products, it is not possible to estimate the break-even point.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 217 في هذه المجموعة.

فتح الحزمة

k this deck

55

If the unit selling price is $40, the volume of sales is $3,000,000, sales at the break-even point amount to $2,500,000, and the maximum possible sales are $3,300,000, the margin of safety is 11,500 units.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 217 في هذه المجموعة.

فتح الحزمة

k this deck

56

Companies with large amounts of fixed costs will generally have a high operating leverage.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 217 في هذه المجموعة.

فتح الحزمة

k this deck

57

Garmo Co. has an operating leverage of 5. Next year's sales are expected to increase by 10%. The company's operating income will increase by 50%.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 217 في هذه المجموعة.

فتح الحزمة

k this deck

58

If the unit selling price is $40, the volume of sales is $3,000,000, sales at the break-even point amount to $2,500,000, and the maximum possible sales are $3,300,000, the margin of safety is 14,500 units.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 217 في هذه المجموعة.

فتح الحزمة

k this deck

59

If fixed costs are $650,000 and the unit contribution margin is $30, the sales necessary to earn an operating income of $30,000 are 14,000 units.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 217 في هذه المجموعة.

فتح الحزمة

k this deck

60

In an absorption costing income statement, the manufacturing margin is the excess of sales over the variable cost of goods sold.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 217 في هذه المجموعة.

فتح الحزمة

k this deck

61

Which of the graphs in Figure 20-1 illustrates the behavior of a total fixed cost?A) Graph 2

B) Graph 3

C) Graph 4

D) Graph 1

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 217 في هذه المجموعة.

فتح الحزمة

k this deck

62

Which of the following is NOT an example of a cost that varies in total as the number of units produced changes?

A) Electricity per KWH to operate factory equipment

B) Direct materials cost

C) Insurance premiums on factory building

D) Wages of assembly worker

A) Electricity per KWH to operate factory equipment

B) Direct materials cost

C) Insurance premiums on factory building

D) Wages of assembly worker

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 217 في هذه المجموعة.

فتح الحزمة

k this deck

63

Which of the graphs in Figure 20-1 illustrates the behavior of a total variable cost?A) Graph 2

B) Graph 3

C) Graph 4

D) Graph 1

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 217 في هذه المجموعة.

فتح الحزمة

k this deck

64

Which of the following describes the behavior of the variable cost per unit?

A) Varies in increasing proportion with changes in the activity level

B) Varies in decreasing proportion with changes in the activity level

C) Remains constant with changes in the activity level

D) Varies in direct proportion with the activity level

A) Varies in increasing proportion with changes in the activity level

B) Varies in decreasing proportion with changes in the activity level

C) Remains constant with changes in the activity level

D) Varies in direct proportion with the activity level

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 217 في هذه المجموعة.

فتح الحزمة

k this deck

65

Which of the following is an example of a cost that varies in total as the number of units produced changes?

A) Salary of a production supervisor

B) Direct materials cost

C) Property taxes on factory buildings

D) Straight-line depreciation on factory equipment

A) Salary of a production supervisor

B) Direct materials cost

C) Property taxes on factory buildings

D) Straight-line depreciation on factory equipment

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 217 في هذه المجموعة.

فتح الحزمة

k this deck

66

Which of the following activity bases would be the most appropriate for food costs of a hospital?

A) Number of cooks scheduled to work

B) Number of x-rays taken

C) Number of patients who stay in the hospital

D) Number of scheduled surgeries

A) Number of cooks scheduled to work

B) Number of x-rays taken

C) Number of patients who stay in the hospital

D) Number of scheduled surgeries

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 217 في هذه المجموعة.

فتح الحزمة

k this deck

67

Which of the graphs in Figure 20-1 illustrates the nature of a mixed cost?A) Graph 2

B) Graph 3

C) Graph 4

D) Graph 1

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 217 في هذه المجموعة.

فتح الحزمة

k this deck

68

Which of the following costs is an example of a cost that remains the same in total as the number of units produced changes?

A) Direct labor

B) Salary of a factory supervisor

C) Units of production depreciation on factory equipment

D) Direct materials

A) Direct labor

B) Salary of a factory supervisor

C) Units of production depreciation on factory equipment

D) Direct materials

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 217 في هذه المجموعة.

فتح الحزمة

k this deck

69

Which of the following costs is a mixed cost?

A) Salary of a factory supervisor

B) Electricity costs of $3 per kilowatt-hour

C) Rental costs of $10,000 per month plus $.30 per machine hour of use

D) Straight-line depreciation on factory equipment

A) Salary of a factory supervisor

B) Electricity costs of $3 per kilowatt-hour

C) Rental costs of $10,000 per month plus $.30 per machine hour of use

D) Straight-line depreciation on factory equipment

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 217 في هذه المجموعة.

فتح الحزمة

k this deck

70

The graph of a variable cost when plotted against its related activity base appears as a:

A) circle

B) rectangle

C) straight line

D) curved line

A) circle

B) rectangle

C) straight line

D) curved line

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 217 في هذه المجموعة.

فتح الحزمة

k this deck

71

Costs that remain constant in total dollar amount as the level of activity changes are called:

A) fixed costs

B) mixed costs

C) product costs

D) variable costs

A) fixed costs

B) mixed costs

C) product costs

D) variable costs

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 217 في هذه المجموعة.

فتح الحزمة

k this deck

72

Most operating decisions of management focus on a narrow range of activity called the:

A) relevant range of production

B) strategic level of production

C) optimal level of production

D) tactical operating level of production

A) relevant range of production

B) strategic level of production

C) optimal level of production

D) tactical operating level of production

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 217 في هذه المجموعة.

فتح الحزمة

k this deck

73

Which of the following describes the behavior of the fixed cost per unit?

A) Decreases with increasing production

B) Decreases with decreasing production

C) Remains constant with changes in production

D) Increases with increasing production

A) Decreases with increasing production

B) Decreases with decreasing production

C) Remains constant with changes in production

D) Increases with increasing production

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 217 في هذه المجموعة.

فتح الحزمة

k this deck

74

Cost behavior refers to the manner in which:

A) a cost changes as the related activity changes

B) a cost is allocated to products

C) a cost is used in setting selling prices

D) a cost is estimated

A) a cost changes as the related activity changes

B) a cost is allocated to products

C) a cost is used in setting selling prices

D) a cost is estimated

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 217 في هذه المجموعة.

فتح الحزمة

k this deck

75

Which of the following activity bases would be the most appropriate for gasoline costs of a delivery service, such as United Postal Service?

A) Number of trucks employed

B) Number of miles driven

C) Number of trucks in service

D) Number of packages delivered

A) Number of trucks employed

B) Number of miles driven

C) Number of trucks in service

D) Number of packages delivered

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 217 في هذه المجموعة.

فتح الحزمة

k this deck

76

Which of the following is NOT an example of a cost that varies in total as the number of units produced changes?

A) Electricity per KWH to operate factory equipment

B) Direct materials cost

C) Straight-line depreciation on factory equipment

D) Wages of assembly worker

A) Electricity per KWH to operate factory equipment

B) Direct materials cost

C) Straight-line depreciation on factory equipment

D) Wages of assembly worker

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 217 في هذه المجموعة.

فتح الحزمة

k this deck

77

The three most common cost behavior classifications are:

A) variable costs, product costs, and sunk costs

B) fixed costs, variable costs, and mixed costs

C) variable costs, period costs, and differential costs

D) variable costs, sunk costs, and opportunity costs

A) variable costs, product costs, and sunk costs

B) fixed costs, variable costs, and mixed costs

C) variable costs, period costs, and differential costs

D) variable costs, sunk costs, and opportunity costs

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 217 في هذه المجموعة.

فتح الحزمة

k this deck

78

A cost that has characteristics of both a variable cost and a fixed cost is called a:

A) variable/fixed cost

B) mixed cost

C) discretionary cost

D) sunk cost

A) variable/fixed cost

B) mixed cost

C) discretionary cost

D) sunk cost

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 217 في هذه المجموعة.

فتح الحزمة

k this deck

79

Costs that vary in total in direct proportion to changes in an activity level are called:

A) fixed costs

B) sunk costs

C) variable costs

D) differential costs

A) fixed costs

B) sunk costs

C) variable costs

D) differential costs

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 217 في هذه المجموعة.

فتح الحزمة

k this deck

80

For purposes of analysis, mixed costs are generally:

A) classified as fixed costs

B) classified as variable costs

C) classified as period costs

D) separated into their variable and fixed cost components

A) classified as fixed costs

B) classified as variable costs

C) classified as period costs

D) separated into their variable and fixed cost components

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 217 في هذه المجموعة.

فتح الحزمة

k this deck

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 217 في هذه المجموعة.