Deck 8: Consolidated Cash Flows and Changes in Ownership

ملء الشاشة (f)

سؤال

On January 1, 2019, Hanson Inc. purchased 54,000 voting shares out of Marvin Inc.'s 90,000 outstanding voting shares for $240,000. On that date, Marvin's common shares and retained earnings were valued at $60,000 and $90,000, respectively. Marvin's book values approximated its fair values on the acquisition date with the exception of the company's equipment, which was estimated to have a fair value that was $50,000 in excess of its recorded book value. The equipment was estimated to have a useful life of eight years. Both companies use straight line amortization exclusively. On January 1, 2020, Hanson purchased an additional 9,000 shares of Marvin Inc. on the open market for $45,000. On this date, Marvin's book values were equal to its fair values with the exception of the company's equipment, which is now thought to be undervalued by $60,000. Moreover, the equipment's estimated useful life was revised to 5 years on this date.

Marvin's net income and dividends for 2019 and 2020 are as follows:

Marvin's goodwill suffered an impairment loss of $5,000 during 2019. Hanson Inc. uses the equity method to account for its investment in Marvin Inc.

Marvin's goodwill suffered an impairment loss of $5,000 during 2019. Hanson Inc. uses the equity method to account for its investment in Marvin Inc.

What is the amount of the acquisition differential amortization for 2019 (excluding goodwill impairment)?

A) $4,375

B) $5,625

C) $6,250

D) $12,000

Marvin's net income and dividends for 2019 and 2020 are as follows:

Marvin's goodwill suffered an impairment loss of $5,000 during 2019. Hanson Inc. uses the equity method to account for its investment in Marvin Inc.What is the amount of the acquisition differential amortization for 2019 (excluding goodwill impairment)?

A) $4,375

B) $5,625

C) $6,250

D) $12,000

سؤال

سؤال

On January 1, 2019, Hanson Inc. purchased 54,000 voting shares out of Marvin Inc.'s 90,000 outstanding voting shares for $240,000. On that date, Marvin's common shares and retained earnings were valued at $60,000 and $90,000, respectively. Marvin's book values approximated its fair values on the acquisition date with the exception of the company's equipment, which was estimated to have a fair value that was $50,000 in excess of its recorded book value. The equipment was estimated to have a useful life of eight years. Both companies use straight line amortization exclusively. On January 1, 2020, Hanson purchased an additional 9,000 shares of Marvin Inc. on the open market for $45,000. On this date, Marvin's book values were equal to its fair values with the exception of the company's equipment, which is now thought to be undervalued by $60,000. Moreover, the equipment's estimated useful life was revised to 5 years on this date.

Marvin's net income and dividends for 2019 and 2020 are as follows:

Marvin's goodwill suffered an impairment loss of $5,000 during 2019. Hanson Inc. uses the equity method to account for its investment in Marvin Inc.

Marvin's goodwill suffered an impairment loss of $5,000 during 2019. Hanson Inc. uses the equity method to account for its investment in Marvin Inc.

Assuming that Hanson had no recorded goodwill prior to January 1, 2019, what would be the amount of goodwill appearing on Hanson's December 31, 2020 Consolidated Balance Sheet?

A) $75,000

B) $136,500

C) $195,000

D) $209,900

Marvin's net income and dividends for 2019 and 2020 are as follows:

Marvin's goodwill suffered an impairment loss of $5,000 during 2019. Hanson Inc. uses the equity method to account for its investment in Marvin Inc.Assuming that Hanson had no recorded goodwill prior to January 1, 2019, what would be the amount of goodwill appearing on Hanson's December 31, 2020 Consolidated Balance Sheet?

A) $75,000

B) $136,500

C) $195,000

D) $209,900

سؤال

سؤال

On January 1, 2019, Hanson Inc. purchased 54,000 voting shares out of Marvin Inc.'s 90,000 outstanding voting shares for $240,000. On that date, Marvin's common shares and retained earnings were valued at $60,000 and $90,000, respectively. Marvin's book values approximated its fair values on the acquisition date with the exception of the company's equipment, which was estimated to have a fair value that was $50,000 in excess of its recorded book value. The equipment was estimated to have a useful life of eight years. Both companies use straight line amortization exclusively. On January 1, 2020, Hanson purchased an additional 9,000 shares of Marvin Inc. on the open market for $45,000. On this date, Marvin's book values were equal to its fair values with the exception of the company's equipment, which is now thought to be undervalued by $60,000. Moreover, the equipment's estimated useful life was revised to 5 years on this date.

Marvin's net income and dividends for 2019 and 2020 are as follows:

Marvin's goodwill suffered an impairment loss of $5,000 during 2019. Hanson Inc. uses the equity method to account for its investment in Marvin Inc.

Marvin's goodwill suffered an impairment loss of $5,000 during 2019. Hanson Inc. uses the equity method to account for its investment in Marvin Inc.

What would be the amount of the unamortized acquisition differential (excluding goodwill) at the end of 2020?

A) Nil.

B) $35,000

C) $37,500

D) $42,000

Marvin's net income and dividends for 2019 and 2020 are as follows:

Marvin's goodwill suffered an impairment loss of $5,000 during 2019. Hanson Inc. uses the equity method to account for its investment in Marvin Inc.What would be the amount of the unamortized acquisition differential (excluding goodwill) at the end of 2020?

A) Nil.

B) $35,000

C) $37,500

D) $42,000

سؤال

سؤال

سؤال

On January 1, 2019, Hanson Inc. purchased 54,000 voting shares out of Marvin Inc.'s 90,000 outstanding voting shares for $240,000. On that date, Marvin's common shares and retained earnings were valued at $60,000 and $90,000, respectively. Marvin's book values approximated its fair values on the acquisition date with the exception of the company's equipment, which was estimated to have a fair value that was $50,000 in excess of its recorded book value. The equipment was estimated to have a useful life of eight years. Both companies use straight line amortization exclusively. On January 1, 2020, Hanson purchased an additional 9,000 shares of Marvin Inc. on the open market for $45,000. On this date, Marvin's book values were equal to its fair values with the exception of the company's equipment, which is now thought to be undervalued by $60,000. Moreover, the equipment's estimated useful life was revised to 5 years on this date.

Marvin's net income and dividends for 2019 and 2020 are as follows:

Marvin's goodwill suffered an impairment loss of $5,000 during 2019. Hanson Inc. uses the equity method to account for its investment in Marvin Inc.

Marvin's goodwill suffered an impairment loss of $5,000 during 2019. Hanson Inc. uses the equity method to account for its investment in Marvin Inc.

What is the amount of the acquisition differential amortization (excluding goodwill impairment) for 2020?

A) $1,500

B) $6,250

C) $7,750

D) $8,750

Marvin's net income and dividends for 2019 and 2020 are as follows:

Marvin's goodwill suffered an impairment loss of $5,000 during 2019. Hanson Inc. uses the equity method to account for its investment in Marvin Inc.What is the amount of the acquisition differential amortization (excluding goodwill impairment) for 2020?

A) $1,500

B) $6,250

C) $7,750

D) $8,750

سؤال

سؤال

On January 1, 2019, Hanson Inc. purchased 54,000 voting shares out of Marvin Inc.'s 90,000 outstanding voting shares for $240,000. On that date, Marvin's common shares and retained earnings were valued at $60,000 and $90,000, respectively. Marvin's book values approximated its fair values on the acquisition date with the exception of the company's equipment, which was estimated to have a fair value that was $50,000 in excess of its recorded book value. The equipment was estimated to have a useful life of eight years. Both companies use straight line amortization exclusively. On January 1, 2020, Hanson purchased an additional 9,000 shares of Marvin Inc. on the open market for $45,000. On this date, Marvin's book values were equal to its fair values with the exception of the company's equipment, which is now thought to be undervalued by $60,000. Moreover, the equipment's estimated useful life was revised to 5 years on this date.

Marvin's net income and dividends for 2019 and 2020 are as follows:

Marvin's goodwill suffered an impairment loss of $5,000 during 2019. Hanson Inc. uses the equity method to account for its investment in Marvin Inc.

Marvin's goodwill suffered an impairment loss of $5,000 during 2019. Hanson Inc. uses the equity method to account for its investment in Marvin Inc.

What is Hanson's ownership interest in Marvin after its January 1, 2020 purchase?

A) 60%

B) 70%

C) 80%

D) 90%

Marvin's net income and dividends for 2019 and 2020 are as follows:

Marvin's goodwill suffered an impairment loss of $5,000 during 2019. Hanson Inc. uses the equity method to account for its investment in Marvin Inc.What is Hanson's ownership interest in Marvin after its January 1, 2020 purchase?

A) 60%

B) 70%

C) 80%

D) 90%

سؤال

سؤال

On January 1, 2019, Hanson Inc. purchased 54,000 voting shares out of Marvin Inc.'s 90,000 outstanding voting shares for $240,000. On that date, Marvin's common shares and retained earnings were valued at $60,000 and $90,000, respectively. Marvin's book values approximated its fair values on the acquisition date with the exception of the company's equipment, which was estimated to have a fair value that was $50,000 in excess of its recorded book value. The equipment was estimated to have a useful life of eight years. Both companies use straight line amortization exclusively. On January 1, 2020, Hanson purchased an additional 9,000 shares of Marvin Inc. on the open market for $45,000. On this date, Marvin's book values were equal to its fair values with the exception of the company's equipment, which is now thought to be undervalued by $60,000. Moreover, the equipment's estimated useful life was revised to 5 years on this date.

Marvin's net income and dividends for 2019 and 2020 are as follows:

Marvin's goodwill suffered an impairment loss of $5,000 during 2019. Hanson Inc. uses the equity method to account for its investment in Marvin Inc.

Marvin's goodwill suffered an impairment loss of $5,000 during 2019. Hanson Inc. uses the equity method to account for its investment in Marvin Inc.

By how much would the non-controlling interest amount have changed as a result of Hanson's second purchase of shares on January 1, 2020?

A) A decrease of $43,975.

B) A decrease of $43,350.

C) An increase of $37,857.

D) An increase of $43,975.

Marvin's net income and dividends for 2019 and 2020 are as follows:

Marvin's goodwill suffered an impairment loss of $5,000 during 2019. Hanson Inc. uses the equity method to account for its investment in Marvin Inc.By how much would the non-controlling interest amount have changed as a result of Hanson's second purchase of shares on January 1, 2020?

A) A decrease of $43,975.

B) A decrease of $43,350.

C) An increase of $37,857.

D) An increase of $43,975.

سؤال

On January 1, 2019, Hanson Inc. purchased 54,000 voting shares out of Marvin Inc.'s 90,000 outstanding voting shares for $240,000. On that date, Marvin's common shares and retained earnings were valued at $60,000 and $90,000, respectively. Marvin's book values approximated its fair values on the acquisition date with the exception of the company's equipment, which was estimated to have a fair value that was $50,000 in excess of its recorded book value. The equipment was estimated to have a useful life of eight years. Both companies use straight line amortization exclusively. On January 1, 2020, Hanson purchased an additional 9,000 shares of Marvin Inc. on the open market for $45,000. On this date, Marvin's book values were equal to its fair values with the exception of the company's equipment, which is now thought to be undervalued by $60,000. Moreover, the equipment's estimated useful life was revised to 5 years on this date.

Marvin's net income and dividends for 2019 and 2020 are as follows:

Marvin's goodwill suffered an impairment loss of $5,000 during 2019. Hanson Inc. uses the equity method to account for its investment in Marvin Inc.

Marvin's goodwill suffered an impairment loss of $5,000 during 2019. Hanson Inc. uses the equity method to account for its investment in Marvin Inc.

What is the amount of goodwill arising from Hanson's January 1, 2019 acquisition?

A) $50,000

B) $60,000

C) $80,000

D) $200,000

Marvin's net income and dividends for 2019 and 2020 are as follows:

Marvin's goodwill suffered an impairment loss of $5,000 during 2019. Hanson Inc. uses the equity method to account for its investment in Marvin Inc.What is the amount of goodwill arising from Hanson's January 1, 2019 acquisition?

A) $50,000

B) $60,000

C) $80,000

D) $200,000

سؤال

On January 1, 2019, Hanson Inc. purchased 54,000 voting shares out of Marvin Inc.'s 90,000 outstanding voting shares for $240,000. On that date, Marvin's common shares and retained earnings were valued at $60,000 and $90,000, respectively. Marvin's book values approximated its fair values on the acquisition date with the exception of the company's equipment, which was estimated to have a fair value that was $50,000 in excess of its recorded book value. The equipment was estimated to have a useful life of eight years. Both companies use straight line amortization exclusively. On January 1, 2020, Hanson purchased an additional 9,000 shares of Marvin Inc. on the open market for $45,000. On this date, Marvin's book values were equal to its fair values with the exception of the company's equipment, which is now thought to be undervalued by $60,000. Moreover, the equipment's estimated useful life was revised to 5 years on this date.

Marvin's net income and dividends for 2019 and 2020 are as follows:

Marvin's goodwill suffered an impairment loss of $5,000 during 2019. Hanson Inc. uses the equity method to account for its investment in Marvin Inc.

Marvin's goodwill suffered an impairment loss of $5,000 during 2019. Hanson Inc. uses the equity method to account for its investment in Marvin Inc.

Assuming that Hanson had no recorded goodwill prior to January 1, 2019, what would be the amount of goodwill appearing on Hanson's December 31, 2019 consolidated balance sheet?

A) $75,000

B) $80,000

C) $117,000

D) $195,000

Marvin's net income and dividends for 2019 and 2020 are as follows:

Marvin's goodwill suffered an impairment loss of $5,000 during 2019. Hanson Inc. uses the equity method to account for its investment in Marvin Inc.Assuming that Hanson had no recorded goodwill prior to January 1, 2019, what would be the amount of goodwill appearing on Hanson's December 31, 2019 consolidated balance sheet?

A) $75,000

B) $80,000

C) $117,000

D) $195,000

سؤال

سؤال

On January 1, 2019, Hanson Inc. purchased 54,000 voting shares out of Marvin Inc.'s 90,000 outstanding voting shares for $240,000. On that date, Marvin's common shares and retained earnings were valued at $60,000 and $90,000, respectively. Marvin's book values approximated its fair values on the acquisition date with the exception of the company's equipment, which was estimated to have a fair value that was $50,000 in excess of its recorded book value. The equipment was estimated to have a useful life of eight years. Both companies use straight line amortization exclusively. On January 1, 2020, Hanson purchased an additional 9,000 shares of Marvin Inc. on the open market for $45,000. On this date, Marvin's book values were equal to its fair values with the exception of the company's equipment, which is now thought to be undervalued by $60,000. Moreover, the equipment's estimated useful life was revised to 5 years on this date.

Marvin's net income and dividends for 2019 and 2020 are as follows:

Marvin's goodwill suffered an impairment loss of $5,000 during 2019. Hanson Inc. uses the equity method to account for its investment in Marvin Inc.

Marvin's goodwill suffered an impairment loss of $5,000 during 2019. Hanson Inc. uses the equity method to account for its investment in Marvin Inc.

What effect (if any) would Hanson's January 1, 2020 purchase have on the company's consolidated cash flows for the year?

A) There would be no effect.

B) There would be a decrease in cash of $45,000 to the consolidated entity.

C) There would be a decrease in cash of $200,000 to the consolidated entity.

D) There would be a decrease in cash of $236,000 to the consolidated entity.

Marvin's net income and dividends for 2019 and 2020 are as follows:

Marvin's goodwill suffered an impairment loss of $5,000 during 2019. Hanson Inc. uses the equity method to account for its investment in Marvin Inc.What effect (if any) would Hanson's January 1, 2020 purchase have on the company's consolidated cash flows for the year?

A) There would be no effect.

B) There would be a decrease in cash of $45,000 to the consolidated entity.

C) There would be a decrease in cash of $200,000 to the consolidated entity.

D) There would be a decrease in cash of $236,000 to the consolidated entity.

سؤال

On January 1, 2019, Hanson Inc. purchased 54,000 voting shares out of Marvin Inc.'s 90,000 outstanding voting shares for $240,000. On that date, Marvin's common shares and retained earnings were valued at $60,000 and $90,000, respectively. Marvin's book values approximated its fair values on the acquisition date with the exception of the company's equipment, which was estimated to have a fair value that was $50,000 in excess of its recorded book value. The equipment was estimated to have a useful life of eight years. Both companies use straight line amortization exclusively. On January 1, 2020, Hanson purchased an additional 9,000 shares of Marvin Inc. on the open market for $45,000. On this date, Marvin's book values were equal to its fair values with the exception of the company's equipment, which is now thought to be undervalued by $60,000. Moreover, the equipment's estimated useful life was revised to 5 years on this date.

Marvin's net income and dividends for 2019 and 2020 are as follows:

Marvin's goodwill suffered an impairment loss of $5,000 during 2019. Hanson Inc. uses the equity method to account for its investment in Marvin Inc.

Marvin's goodwill suffered an impairment loss of $5,000 during 2019. Hanson Inc. uses the equity method to account for its investment in Marvin Inc.

What percentage of Marvin's shares was purchased by Hanson on January 1, 2019?

A) 10%

B) 60%

C) 70%

D) 90%

Marvin's net income and dividends for 2019 and 2020 are as follows:

Marvin's goodwill suffered an impairment loss of $5,000 during 2019. Hanson Inc. uses the equity method to account for its investment in Marvin Inc.What percentage of Marvin's shares was purchased by Hanson on January 1, 2019?

A) 10%

B) 60%

C) 70%

D) 90%

سؤال

سؤال

سؤال

سؤال

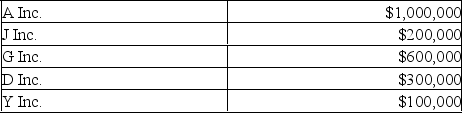

The following information pertains to the shareholdings of an affiliated group of companies. The respective ownership interest of each company is outlined below. A Inc.:

A Inc. owns 75% of J Inc. and 60% of G Inc.

J Inc.:

J Inc. owns 60% of D Inc. and 20% of G Inc.

G Inc.:

G Inc. owns 10% of D Inc. and 80% of Y Inc.

All intercompany investments are accounted for using the equity method.

The Net Incomes for these companies for the year ended December 31, 2020 were as follows:

Unrealized intercompany profits (pre-tax) earned by the various companies for the year ended December 31, 2020 are shown below:

Unrealized intercompany profits (pre-tax) earned by the various companies for the year ended December 31, 2020 are shown below:

All companies are subject to a 25% tax rate.

All companies are subject to a 25% tax rate.

How much is A Inc.'s Consolidated Net Income for 2020?

A) $1,510,000

B) $1,773,625

C) $1,796,125

D) $2,170,000

A Inc. owns 75% of J Inc. and 60% of G Inc.

J Inc.:

J Inc. owns 60% of D Inc. and 20% of G Inc.

G Inc.:

G Inc. owns 10% of D Inc. and 80% of Y Inc.

All intercompany investments are accounted for using the equity method.

The Net Incomes for these companies for the year ended December 31, 2020 were as follows:

Unrealized intercompany profits (pre-tax) earned by the various companies for the year ended December 31, 2020 are shown below: All companies are subject to a 25% tax rate.How much is A Inc.'s Consolidated Net Income for 2020?

A) $1,510,000

B) $1,773,625

C) $1,796,125

D) $2,170,000

سؤال

سؤال

سؤال

On January 1, 2019, Hanson Inc. purchased 54,000 voting shares out of Marvin Inc.'s 90,000 outstanding voting shares for $240,000. On that date, Marvin's common shares and retained earnings were valued at $60,000 and $90,000, respectively. Marvin's book values approximated its fair values on the acquisition date with the exception of the company's equipment, which was estimated to have a fair value that was $50,000 in excess of its recorded book value. The equipment was estimated to have a useful life of eight years. Both companies use straight line amortization exclusively. On January 1, 2020, Hanson purchased an additional 9,000 shares of Marvin Inc. on the open market for $45,000. On this date, Marvin's book values were equal to its fair values with the exception of the company's equipment, which is now thought to be undervalued by $60,000. Moreover, the equipment's estimated useful life was revised to 5 years on this date.

Marvin's net income and dividends for 2019 and 2020 are as follows:

Marvin's goodwill suffered an impairment loss of $5,000 during 2019. Hanson Inc. uses the equity method to account for its investment in Marvin Inc.

Marvin's goodwill suffered an impairment loss of $5,000 during 2019. Hanson Inc. uses the equity method to account for its investment in Marvin Inc.

What effect would the purchase at January 1, 2020 have on the consolidated equity of Hanson?

A) There would be no effect.

B) There would be a reduction in consolidated retained earnings of $1,025.

C) There would be a reduction in consolidated contributed surplus of $1,025.

D) There would be an increase in consolidated retained earnings of $1,025.

Marvin's net income and dividends for 2019 and 2020 are as follows:

Marvin's goodwill suffered an impairment loss of $5,000 during 2019. Hanson Inc. uses the equity method to account for its investment in Marvin Inc.What effect would the purchase at January 1, 2020 have on the consolidated equity of Hanson?

A) There would be no effect.

B) There would be a reduction in consolidated retained earnings of $1,025.

C) There would be a reduction in consolidated contributed surplus of $1,025.

D) There would be an increase in consolidated retained earnings of $1,025.

سؤال

سؤال

سؤال

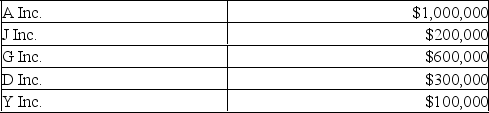

The following information pertains to the shareholdings of an affiliated group of companies. The respective ownership interest of each company is outlined below. A Inc.:

A Inc. owns 75% of J Inc. and 60% of G Inc.

J Inc.:

J Inc. owns 60% of D Inc. and 20% of G Inc.

G Inc.:

G Inc. owns 10% of D Inc. and 80% of Y Inc.

All intercompany investments are accounted for using the equity method.

The Net Incomes for these companies for the year ended December 31, 2020 were as follows:

Unrealized intercompany profits (pre-tax) earned by the various companies for the year ended December 31, 2020 are shown below:

Unrealized intercompany profits (pre-tax) earned by the various companies for the year ended December 31, 2020 are shown below:

All companies are subject to a 25% tax rate.

All companies are subject to a 25% tax rate.

What is the Consolidated Net Income for the year attributable to the shareholders of A Inc.?

A) $1,510,000

B) $1,796,125

C) $1,817,500

D) $2,170,000

A Inc. owns 75% of J Inc. and 60% of G Inc.

J Inc.:

J Inc. owns 60% of D Inc. and 20% of G Inc.

G Inc.:

G Inc. owns 10% of D Inc. and 80% of Y Inc.

All intercompany investments are accounted for using the equity method.

The Net Incomes for these companies for the year ended December 31, 2020 were as follows:

Unrealized intercompany profits (pre-tax) earned by the various companies for the year ended December 31, 2020 are shown below: All companies are subject to a 25% tax rate.What is the Consolidated Net Income for the year attributable to the shareholders of A Inc.?

A) $1,510,000

B) $1,796,125

C) $1,817,500

D) $2,170,000

سؤال

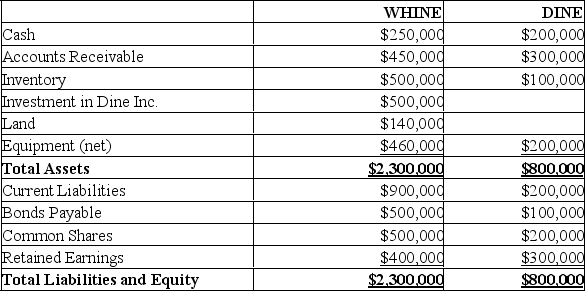

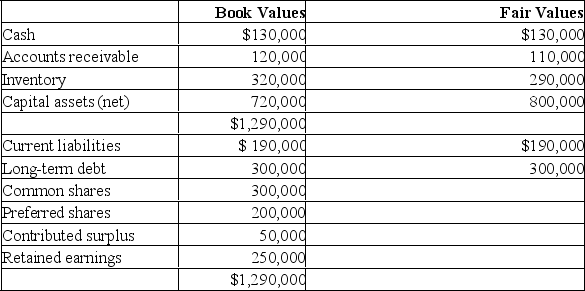

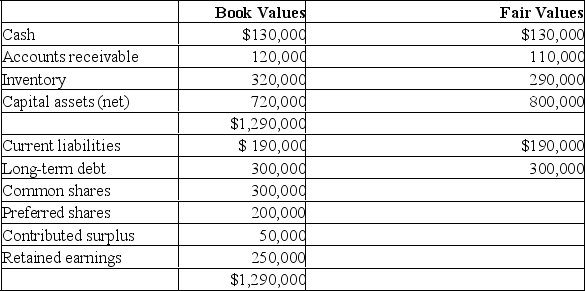

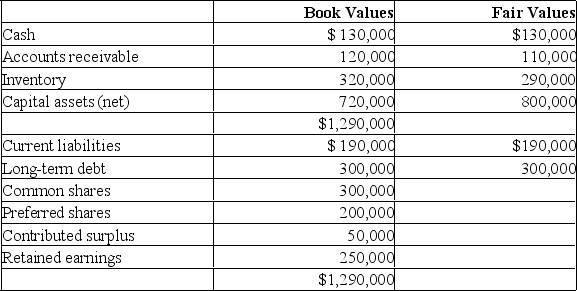

Whine purchased 80% of the outstanding voting shares of Dine Inc. on December 31, 2020. The balance sheets of both companies on that date are shown below (after Whine acquired the shares):  Also on December 31, 2020 (after the financial statements appearing above had been prepared) Chompster Inc., one of Whine's main competitors has agreed to acquire an equity interest in Dine Inc. As a result of the agreement, Dine Inc. would issue another 8,000 shares (over and above the 32,000 shares it currently has outstanding) to Chompster for $20 per share.

Also on December 31, 2020 (after the financial statements appearing above had been prepared) Chompster Inc., one of Whine's main competitors has agreed to acquire an equity interest in Dine Inc. As a result of the agreement, Dine Inc. would issue another 8,000 shares (over and above the 32,000 shares it currently has outstanding) to Chompster for $20 per share.

The acquisition differential on the date of acquisition was attributed entirely to equipment, which had a remaining useful life of ten years from the date of acquisition.

Whine Inc. uses the equity method to account for its investment in Dine Inc.

There were no unrealized intercompany profits on December 31, 2020.

What would be the amount of cash appearing on Whine's December 31, 2020 consolidated balance sheet (after the issue of shares to Chompster)?

A) $450,000

B) $610,000

C) $850,000

D) $810,000

Also on December 31, 2020 (after the financial statements appearing above had been prepared) Chompster Inc., one of Whine's main competitors has agreed to acquire an equity interest in Dine Inc. As a result of the agreement, Dine Inc. would issue another 8,000 shares (over and above the 32,000 shares it currently has outstanding) to Chompster for $20 per share.The acquisition differential on the date of acquisition was attributed entirely to equipment, which had a remaining useful life of ten years from the date of acquisition.

Whine Inc. uses the equity method to account for its investment in Dine Inc.

There were no unrealized intercompany profits on December 31, 2020.

What would be the amount of cash appearing on Whine's December 31, 2020 consolidated balance sheet (after the issue of shares to Chompster)?

A) $450,000

B) $610,000

C) $850,000

D) $810,000

سؤال

سؤال

سؤال

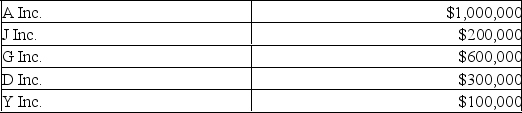

The following information pertains to the shareholdings of an affiliated group of companies. The respective ownership interest of each company is outlined below. A Inc.:

A Inc. owns 75% of J Inc. and 60% of G Inc.

J Inc.:

J Inc. owns 60% of D Inc. and 20% of G Inc.

G Inc.:

G Inc. owns 10% of D Inc. and 80% of Y Inc.

All intercompany investments are accounted for using the equity method.

The Net Incomes for these companies for the year ended December 31, 2020 were as follows:

Unrealized intercompany profits (pre-tax) earned by the various companies for the year ended December 31, 2020 are shown below:

Unrealized intercompany profits (pre-tax) earned by the various companies for the year ended December 31, 2020 are shown below:

All companies are subject to a 25% tax rate.

All companies are subject to a 25% tax rate.

How much is the non-controlling interest in A Inc.'s Consolidated Net Income for 2020?

A) Nil

B) $382,500

C) $373,875

D) $400,000

A Inc. owns 75% of J Inc. and 60% of G Inc.

J Inc.:

J Inc. owns 60% of D Inc. and 20% of G Inc.

G Inc.:

G Inc. owns 10% of D Inc. and 80% of Y Inc.

All intercompany investments are accounted for using the equity method.

The Net Incomes for these companies for the year ended December 31, 2020 were as follows:

Unrealized intercompany profits (pre-tax) earned by the various companies for the year ended December 31, 2020 are shown below: All companies are subject to a 25% tax rate.How much is the non-controlling interest in A Inc.'s Consolidated Net Income for 2020?

A) Nil

B) $382,500

C) $373,875

D) $400,000

سؤال

سؤال

سؤال

On January 1, 2019, Hanson Inc. purchased 54,000 voting shares out of Marvin Inc.'s 90,000 outstanding voting shares for $240,000. On that date, Marvin's common shares and retained earnings were valued at $60,000 and $90,000, respectively. Marvin's book values approximated its fair values on the acquisition date with the exception of the company's equipment, which was estimated to have a fair value that was $50,000 in excess of its recorded book value. The equipment was estimated to have a useful life of eight years. Both companies use straight line amortization exclusively. On January 1, 2020, Hanson purchased an additional 9,000 shares of Marvin Inc. on the open market for $45,000. On this date, Marvin's book values were equal to its fair values with the exception of the company's equipment, which is now thought to be undervalued by $60,000. Moreover, the equipment's estimated useful life was revised to 5 years on this date.

Marvin's net income and dividends for 2019 and 2020 are as follows:

Marvin's goodwill suffered an impairment loss of $5,000 during 2019. Hanson Inc. uses the equity method to account for its investment in Marvin Inc.

Marvin's goodwill suffered an impairment loss of $5,000 during 2019. Hanson Inc. uses the equity method to account for its investment in Marvin Inc.

What would be the balance in Hanson's investment in Marvin account on December 31, 2020?

A) $303,000

B) $347,900

C) $348,925

D) $349,650

Marvin's net income and dividends for 2019 and 2020 are as follows:

Marvin's goodwill suffered an impairment loss of $5,000 during 2019. Hanson Inc. uses the equity method to account for its investment in Marvin Inc.What would be the balance in Hanson's investment in Marvin account on December 31, 2020?

A) $303,000

B) $347,900

C) $348,925

D) $349,650

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

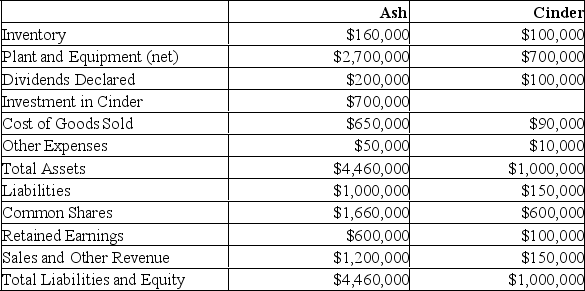

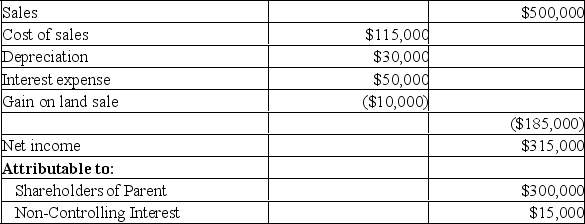

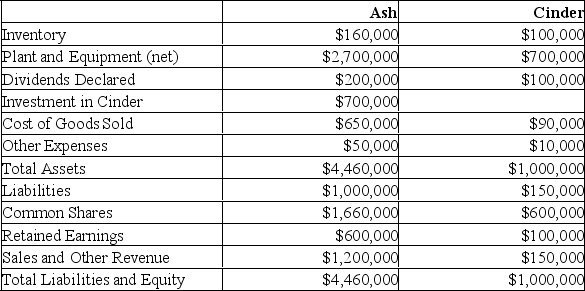

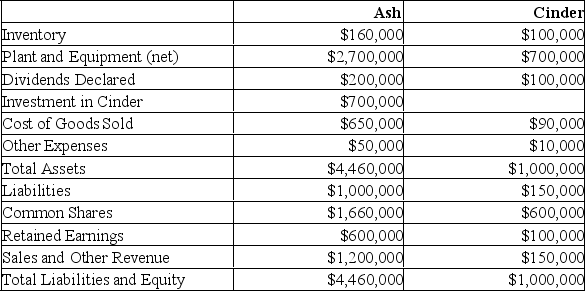

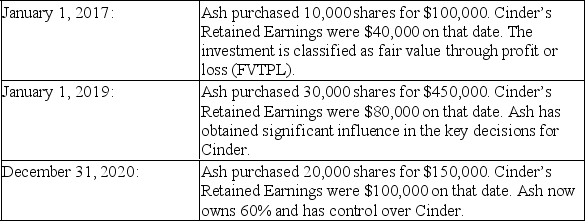

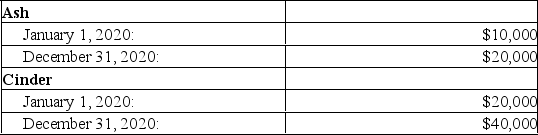

The trial balances of Ash Inc. and its subsidiary Cinder Corp. on December 31, 2020 are shown below:

Other Information:

Other Information:

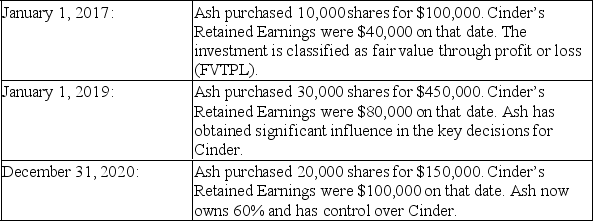

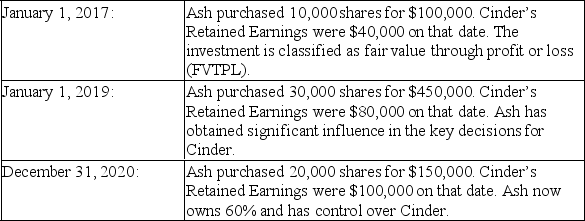

Ash acquired Cinder in three stages:

Cinder was incorporated on January 1, 2015. On that date, Cinder issued 100,000 voting shares.

Cinder was incorporated on January 1, 2015. On that date, Cinder issued 100,000 voting shares.

Any difference between the cost and book value is attributable entirely to trademarks, which are to be amortized over 5 years. The company has neither issued nor retired shares since the date of its incorporation.

Ash sold depreciable assets to Cinder at a loss of $20,000 on January 1, 2019. These assets had a 10 year remaining life.

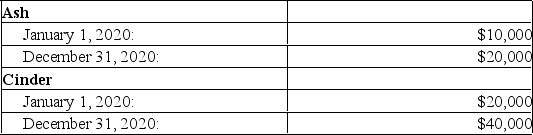

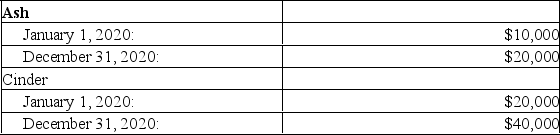

Intercompany sales of inventory during 2020 amounted to $250,000. Unrealized inventory profits for each company are shown below for 2020. The amounts indicate the amount of profit in each company's inventory.

All inventories on hand at the start of 2020 were sold to outsiders during the year. The net incomes of both companies are evenly earned throughout the year. Both companies are subject to an effective corporate tax rate of 20%.

All inventories on hand at the start of 2020 were sold to outsiders during the year. The net incomes of both companies are evenly earned throughout the year. Both companies are subject to an effective corporate tax rate of 20%.

Compute the Consolidated Cost of Goods Sold for 2020.

Other Information:Ash acquired Cinder in three stages:

Cinder was incorporated on January 1, 2015. On that date, Cinder issued 100,000 voting shares.Any difference between the cost and book value is attributable entirely to trademarks, which are to be amortized over 5 years. The company has neither issued nor retired shares since the date of its incorporation.

Ash sold depreciable assets to Cinder at a loss of $20,000 on January 1, 2019. These assets had a 10 year remaining life.

Intercompany sales of inventory during 2020 amounted to $250,000. Unrealized inventory profits for each company are shown below for 2020. The amounts indicate the amount of profit in each company's inventory.

All inventories on hand at the start of 2020 were sold to outsiders during the year. The net incomes of both companies are evenly earned throughout the year. Both companies are subject to an effective corporate tax rate of 20%.Compute the Consolidated Cost of Goods Sold for 2020.

سؤال

Beta Corp. owns 80% of Gamma Corp. The Consolidated Financial Statements of Beta Corp. for 2019 and 2020 are shown below:

Beta Corp.

Consolidated Balance Sheet

Beta Corp.

Beta Corp.

Consolidated Income Statement,

For the year ended December 31, 2020

Other Information:

Other Information:

Beta purchased its interest in Gamma on January 1, 2016 for $360,000 when the company's net assets were valued at $300,000. The acquisition differential was allocated equally between goodwill and equipment, which was estimated to have a remaining useful life of ten years from the acquisition date.

Gamma reported a net income of $75,000 and paid dividends of $5,000 during 2020.

Beta issued $300,000 in bonds during the year. Beta reported an equity method net Income of $300,000 and paid $70,000 in dividends to its shareholders.

Required:

Prepare a Consolidated Statement of Cash Flows for Beta Corp. for 2020.

Beta Corp.

Consolidated Statement of Cash Flows

Beta Corp.

Consolidated Balance Sheet

Beta Corp.Consolidated Income Statement,

For the year ended December 31, 2020

Other Information:Beta purchased its interest in Gamma on January 1, 2016 for $360,000 when the company's net assets were valued at $300,000. The acquisition differential was allocated equally between goodwill and equipment, which was estimated to have a remaining useful life of ten years from the acquisition date.

Gamma reported a net income of $75,000 and paid dividends of $5,000 during 2020.

Beta issued $300,000 in bonds during the year. Beta reported an equity method net Income of $300,000 and paid $70,000 in dividends to its shareholders.

Required:

Prepare a Consolidated Statement of Cash Flows for Beta Corp. for 2020.

Beta Corp.

Consolidated Statement of Cash Flows

سؤال

سؤال

سؤال

The trial balances of Ash Inc. and its subsidiary Cinder Corp. on December 31, 2020 are shown below:

Other Information:

Other Information:

Ash acquired Cinder in three stages:

Cinder was incorporated on January 1, 2015. On that date, Cinder issued 100,000 voting shares.

Cinder was incorporated on January 1, 2015. On that date, Cinder issued 100,000 voting shares.

Any difference between the cost and book value is attributable entirely to trademarks, which are to be amortized over 5 years. The company has neither issued nor retired shares since the date of its incorporation.

Ash sold depreciable assets to Cinder at a loss of $20,000 on January 1, 2019. These assets had a 10 year remaining life.

Intercompany sales of inventory during 2020 amounted to $250,000. Unrealized inventory profits for each company are shown below for 2020. The amounts indicate the amount of profit in each company's inventory.

All inventories on hand at the start of 2020 were sold to outsiders during the year. The net incomes of both companies are evenly earned throughout the year. Both companies are subject to an effective corporate tax rate of 20%.

All inventories on hand at the start of 2020 were sold to outsiders during the year. The net incomes of both companies are evenly earned throughout the year. Both companies are subject to an effective corporate tax rate of 20%.

What amount will be shown in the consolidated balance sheet of Ash as at December 31, 2020, for trademarks?

Other Information:Ash acquired Cinder in three stages:

Cinder was incorporated on January 1, 2015. On that date, Cinder issued 100,000 voting shares.Any difference between the cost and book value is attributable entirely to trademarks, which are to be amortized over 5 years. The company has neither issued nor retired shares since the date of its incorporation.

Ash sold depreciable assets to Cinder at a loss of $20,000 on January 1, 2019. These assets had a 10 year remaining life.

Intercompany sales of inventory during 2020 amounted to $250,000. Unrealized inventory profits for each company are shown below for 2020. The amounts indicate the amount of profit in each company's inventory.

All inventories on hand at the start of 2020 were sold to outsiders during the year. The net incomes of both companies are evenly earned throughout the year. Both companies are subject to an effective corporate tax rate of 20%.What amount will be shown in the consolidated balance sheet of Ash as at December 31, 2020, for trademarks?

سؤال

سؤال

سؤال

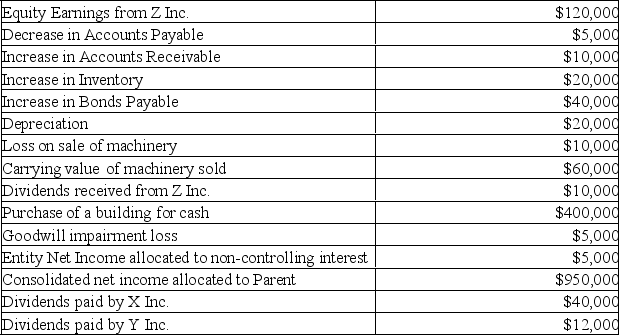

The following information was derived from the 2020consolidated financial statements of X Inc., which owns 80% of Y Inc. as well as 40% of Z Inc.:

The cash balance at the start of 2020 was $200,000.

The cash balance at the start of 2020 was $200,000.

Required:

Prepare the consolidated statement of cash flows for Lime Inc for the year ended December 31, 2020.

X Inc.

Consolidated Statement of Cash Flows

The cash balance at the start of 2020 was $200,000.Required:

Prepare the consolidated statement of cash flows for Lime Inc for the year ended December 31, 2020.

X Inc.

Consolidated Statement of Cash Flows

سؤال

سؤال

سؤال

The trial balances of Ash Inc. and its subsidiary Cinder Corp. on December 31, 2020 are shown below:

Other Information:

Other Information:

Ash acquired Cinder in three stages:

Cinder was incorporated on January 1, 2015. On that date, Cinder issued 100,000 voting shares.

Cinder was incorporated on January 1, 2015. On that date, Cinder issued 100,000 voting shares.

Any difference between the cost and book value is attributable entirely to trademarks, which are to be amortized over 5 years. The company has neither issued nor retired shares since the date of its incorporation.

Ash sold depreciable assets to Cinder at a loss of $20,000 on January 1, 2019. These assets had a 10 year remaining life.

Intercompany sales of inventory during 2020 amounted to $250,000. Unrealized inventory profits for each company are shown below for 2020. The amounts indicate the amount of profit in each company's inventory.

All inventories on hand at the start of 2020 were sold to outsiders during the year. The net incomes of both companies are evenly earned throughout the year. Both companies are subject to an effective corporate tax rate of 20%.

All inventories on hand at the start of 2020 were sold to outsiders during the year. The net incomes of both companies are evenly earned throughout the year. Both companies are subject to an effective corporate tax rate of 20%.

Compute consolidated inventory for Ash as at December 31, 2020.

Other Information:Ash acquired Cinder in three stages:

Cinder was incorporated on January 1, 2015. On that date, Cinder issued 100,000 voting shares.Any difference between the cost and book value is attributable entirely to trademarks, which are to be amortized over 5 years. The company has neither issued nor retired shares since the date of its incorporation.

Ash sold depreciable assets to Cinder at a loss of $20,000 on January 1, 2019. These assets had a 10 year remaining life.

Intercompany sales of inventory during 2020 amounted to $250,000. Unrealized inventory profits for each company are shown below for 2020. The amounts indicate the amount of profit in each company's inventory.

All inventories on hand at the start of 2020 were sold to outsiders during the year. The net incomes of both companies are evenly earned throughout the year. Both companies are subject to an effective corporate tax rate of 20%.Compute consolidated inventory for Ash as at December 31, 2020.

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

Parrot Company purchased 75% of the outstanding common shares and 50% of the outstanding preference shares of Saltines Inc. on January 1, 2020, on which date the balance sheet and fair values of Saltines' assets and liabilities were as follows:

Saltines Inc.

Balance Sheet

as at December 31, 2019

Saltines Inc.

Balance Sheet

as at December 31, 2019

سؤال

Parrot Company purchased 75% of the outstanding common shares and 50% of the outstanding preference shares of Saltines Inc. on January 1, 2020, on which date the balance sheet and fair values of Saltines' assets and liabilities were as follows:

Saltines Inc.

Balance Sheet

as at December 31, 2019

Parrot paid $460,000 for the common shares and $105,000 for the preference shares. The contributed surplus arose from the issue of the preferred shares at a price higher than their stated value. The preferred shares paid cumulative dividends of 5% of their stated value but dividends for 2018 and 2019 were unpaid. The shares were redeemable, at the option of the issuer, at a premium of 8%.

Parrot paid $460,000 for the common shares and $105,000 for the preference shares. The contributed surplus arose from the issue of the preferred shares at a price higher than their stated value. The preferred shares paid cumulative dividends of 5% of their stated value but dividends for 2018 and 2019 were unpaid. The shares were redeemable, at the option of the issuer, at a premium of 8%.

The capital assets of Saltines had a remaining useful life of ten years at January 1, 2010. Any unallocated acquisition differential would be treated as goodwill, which is assessed annually for impairment. Parrot accounts for its interest in Saltines using the cost method and accounts for the non-controlling interest in its consolidated financial statements using the fair value enterprise method.

Parrot's net income for 2020 was $300,000 and Parrot paid dividends of $150,000 on December 31, 2020. Saltines' net income for 2020 was $120,000 before a loss from discontinued operations of $60,000 (net of tax). Saltines paid dividends of $75,000 in 2020. (Parrot included all dividends received in its income for 2020.)

Calculate the amount of the non-controlling interest on the consolidated balance sheet of Parrot and its subsidiary as at December 31, 2020.

Saltines Inc.

Balance Sheet

as at December 31, 2019

Parrot paid $460,000 for the common shares and $105,000 for the preference shares. The contributed surplus arose from the issue of the preferred shares at a price higher than their stated value. The preferred shares paid cumulative dividends of 5% of their stated value but dividends for 2018 and 2019 were unpaid. The shares were redeemable, at the option of the issuer, at a premium of 8%.The capital assets of Saltines had a remaining useful life of ten years at January 1, 2010. Any unallocated acquisition differential would be treated as goodwill, which is assessed annually for impairment. Parrot accounts for its interest in Saltines using the cost method and accounts for the non-controlling interest in its consolidated financial statements using the fair value enterprise method.

Parrot's net income for 2020 was $300,000 and Parrot paid dividends of $150,000 on December 31, 2020. Saltines' net income for 2020 was $120,000 before a loss from discontinued operations of $60,000 (net of tax). Saltines paid dividends of $75,000 in 2020. (Parrot included all dividends received in its income for 2020.)

Calculate the amount of the non-controlling interest on the consolidated balance sheet of Parrot and its subsidiary as at December 31, 2020.

سؤال

Parrot Company purchased 75% of the outstanding common shares and 50% of the outstanding preference shares of Saltines Inc. on January 1, 2020, on which date the balance sheet and fair values of Saltines' assets and liabilities were as follows:

Saltines Inc.

Balance Sheet

as at December 31, 2019

Parrot paid $460,000 for the common shares and $105,000 for the preference shares. The contributed surplus arose from the issue of the preferred shares at a price higher than their stated value. The preferred shares paid cumulative dividends of 5% of their stated value but dividends for 2018 and 2019 were unpaid. The shares were redeemable, at the option of the issuer, at a premium of 8%.

Parrot paid $460,000 for the common shares and $105,000 for the preference shares. The contributed surplus arose from the issue of the preferred shares at a price higher than their stated value. The preferred shares paid cumulative dividends of 5% of their stated value but dividends for 2018 and 2019 were unpaid. The shares were redeemable, at the option of the issuer, at a premium of 8%.

The capital assets of Saltines had a remaining useful life of ten years at January 1, 2010. Any unallocated acquisition differential would be treated as goodwill, which is assessed annually for impairment. Parrot accounts for its interest in Saltines using the cost method and accounts for the non-controlling interest in its consolidated financial statements using the fair value enterprise method.

Parrot's net income for 2020 was $300,000 and Parrot paid dividends of $150,000 on December 31, 2020. Saltines' net income for 2020 was $120,000 before a loss from discontinued operations of $60,000 (net of tax). Saltines paid dividends of $75,000 in 2020. (Parrot included all dividends received in its income for 2020.)

Calculate the consolidated net income of Parrot and its subsidiary as at December 31, 2020.

Saltines Inc.

Balance Sheet

as at December 31, 2019

Parrot paid $460,000 for the common shares and $105,000 for the preference shares. The contributed surplus arose from the issue of the preferred shares at a price higher than their stated value. The preferred shares paid cumulative dividends of 5% of their stated value but dividends for 2018 and 2019 were unpaid. The shares were redeemable, at the option of the issuer, at a premium of 8%.The capital assets of Saltines had a remaining useful life of ten years at January 1, 2010. Any unallocated acquisition differential would be treated as goodwill, which is assessed annually for impairment. Parrot accounts for its interest in Saltines using the cost method and accounts for the non-controlling interest in its consolidated financial statements using the fair value enterprise method.

Parrot's net income for 2020 was $300,000 and Parrot paid dividends of $150,000 on December 31, 2020. Saltines' net income for 2020 was $120,000 before a loss from discontinued operations of $60,000 (net of tax). Saltines paid dividends of $75,000 in 2020. (Parrot included all dividends received in its income for 2020.)

Calculate the consolidated net income of Parrot and its subsidiary as at December 31, 2020.

فتح الحزمة

قم بالتسجيل لفتح البطاقات في هذه المجموعة!

Unlock Deck

Unlock Deck

1/64

العب

ملء الشاشة (f)

Deck 8: Consolidated Cash Flows and Changes in Ownership

1

On January 1, 2019, Hanson Inc. purchased 54,000 voting shares out of Marvin Inc.'s 90,000 outstanding voting shares for $240,000. On that date, Marvin's common shares and retained earnings were valued at $60,000 and $90,000, respectively. Marvin's book values approximated its fair values on the acquisition date with the exception of the company's equipment, which was estimated to have a fair value that was $50,000 in excess of its recorded book value. The equipment was estimated to have a useful life of eight years. Both companies use straight line amortization exclusively. On January 1, 2020, Hanson purchased an additional 9,000 shares of Marvin Inc. on the open market for $45,000. On this date, Marvin's book values were equal to its fair values with the exception of the company's equipment, which is now thought to be undervalued by $60,000. Moreover, the equipment's estimated useful life was revised to 5 years on this date.

Marvin's net income and dividends for 2019 and 2020 are as follows:

Marvin's goodwill suffered an impairment loss of $5,000 during 2019. Hanson Inc. uses the equity method to account for its investment in Marvin Inc.

What is the amount of the acquisition differential amortization for 2019 (excluding goodwill impairment)?

A) $4,375

B) $5,625

C) $6,250

D) $12,000

Marvin's net income and dividends for 2019 and 2020 are as follows:

Marvin's goodwill suffered an impairment loss of $5,000 during 2019. Hanson Inc. uses the equity method to account for its investment in Marvin Inc.What is the amount of the acquisition differential amortization for 2019 (excluding goodwill impairment)?

A) $4,375

B) $5,625

C) $6,250

D) $12,000

C

2

ABC Inc. purchased 35,000 voting shares out of 123 Inc.'s 50,000 outstanding voting shares for $350,000 on January 1, 2020. On the date of acquisition, 123's common shares and retained earnings were valued at $120,000 and $180,000, respectively. 123's book values approximated its fair values on the acquisition date with the exception of a patent and a trademark, neither of which had been previously recorded. The fair values of the patent and trademark on the date of acquisition were $30,000 and $20,000 respectively.

On January 2, 2020, ABC sold 7,000 shares of 123 on the open market for $57,750.

ABC Inc. uses the equity method to account for its investment in 123 Inc.

What is the amount of undepleted acquisition differential (including goodwill) after the sale?

A) $84,000

B) $140,000

C) $200,000

D) $300,000

On January 2, 2020, ABC sold 7,000 shares of 123 on the open market for $57,750.

ABC Inc. uses the equity method to account for its investment in 123 Inc.

What is the amount of undepleted acquisition differential (including goodwill) after the sale?

A) $84,000

B) $140,000

C) $200,000

D) $300,000

C

3

On January 1, 2019, Hanson Inc. purchased 54,000 voting shares out of Marvin Inc.'s 90,000 outstanding voting shares for $240,000. On that date, Marvin's common shares and retained earnings were valued at $60,000 and $90,000, respectively. Marvin's book values approximated its fair values on the acquisition date with the exception of the company's equipment, which was estimated to have a fair value that was $50,000 in excess of its recorded book value. The equipment was estimated to have a useful life of eight years. Both companies use straight line amortization exclusively. On January 1, 2020, Hanson purchased an additional 9,000 shares of Marvin Inc. on the open market for $45,000. On this date, Marvin's book values were equal to its fair values with the exception of the company's equipment, which is now thought to be undervalued by $60,000. Moreover, the equipment's estimated useful life was revised to 5 years on this date.

Marvin's net income and dividends for 2019 and 2020 are as follows:

Marvin's goodwill suffered an impairment loss of $5,000 during 2019. Hanson Inc. uses the equity method to account for its investment in Marvin Inc.

Assuming that Hanson had no recorded goodwill prior to January 1, 2019, what would be the amount of goodwill appearing on Hanson's December 31, 2020 Consolidated Balance Sheet?

A) $75,000

B) $136,500

C) $195,000

D) $209,900

Marvin's net income and dividends for 2019 and 2020 are as follows:

Marvin's goodwill suffered an impairment loss of $5,000 during 2019. Hanson Inc. uses the equity method to account for its investment in Marvin Inc.Assuming that Hanson had no recorded goodwill prior to January 1, 2019, what would be the amount of goodwill appearing on Hanson's December 31, 2020 Consolidated Balance Sheet?

A) $75,000

B) $136,500

C) $195,000

D) $209,900

C

4

ABC Inc. purchased 35,000 voting shares out of 123 Inc.'s 50,000 outstanding voting shares for $350,000 on January 1, 2020. On the date of acquisition, 123's common shares and retained earnings were valued at $120,000 and $180,000, respectively. 123's book values approximated its fair values on the acquisition date with the exception of a patent and a trademark, neither of which had been previously recorded. The fair values of the patent and trademark on the date of acquisition were $30,000 and $20,000 respectively.

On January 2, 2020, ABC sold 7,000 shares of 123 on the open market for $57,750.

ABC Inc. uses the equity method to account for its investment in 123 Inc.

What would be the carrying amount of the "Investment in 123 Inc." account after the sale?

A) $350,000.

B) $70,000.

C) $280,000.

D) $292,250.

On January 2, 2020, ABC sold 7,000 shares of 123 on the open market for $57,750.

ABC Inc. uses the equity method to account for its investment in 123 Inc.

What would be the carrying amount of the "Investment in 123 Inc." account after the sale?

A) $350,000.

B) $70,000.

C) $280,000.

D) $292,250.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 64 في هذه المجموعة.

فتح الحزمة

k this deck

5

On January 1, 2019, Hanson Inc. purchased 54,000 voting shares out of Marvin Inc.'s 90,000 outstanding voting shares for $240,000. On that date, Marvin's common shares and retained earnings were valued at $60,000 and $90,000, respectively. Marvin's book values approximated its fair values on the acquisition date with the exception of the company's equipment, which was estimated to have a fair value that was $50,000 in excess of its recorded book value. The equipment was estimated to have a useful life of eight years. Both companies use straight line amortization exclusively. On January 1, 2020, Hanson purchased an additional 9,000 shares of Marvin Inc. on the open market for $45,000. On this date, Marvin's book values were equal to its fair values with the exception of the company's equipment, which is now thought to be undervalued by $60,000. Moreover, the equipment's estimated useful life was revised to 5 years on this date.

Marvin's net income and dividends for 2019 and 2020 are as follows:

Marvin's goodwill suffered an impairment loss of $5,000 during 2019. Hanson Inc. uses the equity method to account for its investment in Marvin Inc.

What would be the amount of the unamortized acquisition differential (excluding goodwill) at the end of 2020?

A) Nil.

B) $35,000

C) $37,500

D) $42,000

Marvin's net income and dividends for 2019 and 2020 are as follows:

Marvin's goodwill suffered an impairment loss of $5,000 during 2019. Hanson Inc. uses the equity method to account for its investment in Marvin Inc.What would be the amount of the unamortized acquisition differential (excluding goodwill) at the end of 2020?

A) Nil.

B) $35,000

C) $37,500

D) $42,000

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 64 في هذه المجموعة.

فتح الحزمة

k this deck

6

ABC Inc. purchased 35,000 voting shares out of 123 Inc.'s 50,000 outstanding voting shares for $350,000 on January 1, 2020. On the date of acquisition, 123's common shares and retained earnings were valued at $120,000 and $180,000, respectively. 123's book values approximated its fair values on the acquisition date with the exception of a patent and a trademark, neither of which had been previously recorded. The fair values of the patent and trademark on the date of acquisition were $30,000 and $20,000 respectively.

On January 2, 2020, ABC sold 7,000 shares of 123 on the open market for $57,750.

ABC Inc. uses the equity method to account for its investment in 123 Inc.

What would be the amount of the gain or loss on the sale of the 7,000 shares?

A) A loss of $12,250.

B) A loss of $70,000.

C) A gain of $12,250.

D) A gain of $57,750.

On January 2, 2020, ABC sold 7,000 shares of 123 on the open market for $57,750.

ABC Inc. uses the equity method to account for its investment in 123 Inc.

What would be the amount of the gain or loss on the sale of the 7,000 shares?

A) A loss of $12,250.

B) A loss of $70,000.

C) A gain of $12,250.

D) A gain of $57,750.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 64 في هذه المجموعة.

فتح الحزمة

k this deck

7

A Inc. owns 80% of B's outstanding voting shares. Under which of the following scenarios would A's ownership percentage of B change?

A)

A) B Inc. announces a 2-for-1 stock split to all its common shareholders.

B) B issues an additional 10,000 voting shares; A acquires 8,000 shares of the new issue.

C) B issues an additional 10,000 voting shares; A acquires 6,400 shares of the new issue.

D) B retires 20,000 voting share, and in doing so, buy back 16,000 shares from

A)

A) B Inc. announces a 2-for-1 stock split to all its common shareholders.

B) B issues an additional 10,000 voting shares; A acquires 8,000 shares of the new issue.

C) B issues an additional 10,000 voting shares; A acquires 6,400 shares of the new issue.

D) B retires 20,000 voting share, and in doing so, buy back 16,000 shares from

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 64 في هذه المجموعة.

فتح الحزمة

k this deck

8

On January 1, 2019, Hanson Inc. purchased 54,000 voting shares out of Marvin Inc.'s 90,000 outstanding voting shares for $240,000. On that date, Marvin's common shares and retained earnings were valued at $60,000 and $90,000, respectively. Marvin's book values approximated its fair values on the acquisition date with the exception of the company's equipment, which was estimated to have a fair value that was $50,000 in excess of its recorded book value. The equipment was estimated to have a useful life of eight years. Both companies use straight line amortization exclusively. On January 1, 2020, Hanson purchased an additional 9,000 shares of Marvin Inc. on the open market for $45,000. On this date, Marvin's book values were equal to its fair values with the exception of the company's equipment, which is now thought to be undervalued by $60,000. Moreover, the equipment's estimated useful life was revised to 5 years on this date.

Marvin's net income and dividends for 2019 and 2020 are as follows:

Marvin's goodwill suffered an impairment loss of $5,000 during 2019. Hanson Inc. uses the equity method to account for its investment in Marvin Inc.

What is the amount of the acquisition differential amortization (excluding goodwill impairment) for 2020?

A) $1,500

B) $6,250

C) $7,750

D) $8,750

Marvin's net income and dividends for 2019 and 2020 are as follows:

Marvin's goodwill suffered an impairment loss of $5,000 during 2019. Hanson Inc. uses the equity method to account for its investment in Marvin Inc.What is the amount of the acquisition differential amortization (excluding goodwill impairment) for 2020?

A) $1,500

B) $6,250

C) $7,750

D) $8,750

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 64 في هذه المجموعة.

فتح الحزمة

k this deck

9

ABC Inc. purchased 35,000 voting shares out of 123 Inc.'s 50,000 outstanding voting shares for $350,000 on January 1, 2020. On the date of acquisition, 123's common shares and retained earnings were valued at $120,000 and $180,000, respectively. 123's book values approximated its fair values on the acquisition date with the exception of a patent and a trademark, neither of which had been previously recorded. The fair values of the patent and trademark on the date of acquisition were $30,000 and $20,000 respectively.

On January 2, 2020, ABC sold 7,000 shares of 123 on the open market for $57,750.

ABC Inc. uses the equity method to account for its investment in 123 Inc.

What is ABC's ownership interest in 123 after its sale?

A) 70%

B) 14%

C) 42%

D) 56%

On January 2, 2020, ABC sold 7,000 shares of 123 on the open market for $57,750.

ABC Inc. uses the equity method to account for its investment in 123 Inc.

What is ABC's ownership interest in 123 after its sale?

A) 70%

B) 14%

C) 42%

D) 56%

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 64 في هذه المجموعة.

فتح الحزمة

k this deck

10

On January 1, 2019, Hanson Inc. purchased 54,000 voting shares out of Marvin Inc.'s 90,000 outstanding voting shares for $240,000. On that date, Marvin's common shares and retained earnings were valued at $60,000 and $90,000, respectively. Marvin's book values approximated its fair values on the acquisition date with the exception of the company's equipment, which was estimated to have a fair value that was $50,000 in excess of its recorded book value. The equipment was estimated to have a useful life of eight years. Both companies use straight line amortization exclusively. On January 1, 2020, Hanson purchased an additional 9,000 shares of Marvin Inc. on the open market for $45,000. On this date, Marvin's book values were equal to its fair values with the exception of the company's equipment, which is now thought to be undervalued by $60,000. Moreover, the equipment's estimated useful life was revised to 5 years on this date.

Marvin's net income and dividends for 2019 and 2020 are as follows:

Marvin's goodwill suffered an impairment loss of $5,000 during 2019. Hanson Inc. uses the equity method to account for its investment in Marvin Inc.

What is Hanson's ownership interest in Marvin after its January 1, 2020 purchase?

A) 60%

B) 70%

C) 80%

D) 90%

Marvin's net income and dividends for 2019 and 2020 are as follows:

Marvin's goodwill suffered an impairment loss of $5,000 during 2019. Hanson Inc. uses the equity method to account for its investment in Marvin Inc.What is Hanson's ownership interest in Marvin after its January 1, 2020 purchase?

A) 60%

B) 70%

C) 80%

D) 90%

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 64 في هذه المجموعة.

فتح الحزمة

k this deck

11

ABC Inc. purchased 35,000 voting shares out of 123 Inc.'s 50,000 outstanding voting shares for $350,000 on January 1, 2020. On the date of acquisition, 123's common shares and retained earnings were valued at $120,000 and $180,000, respectively. 123's book values approximated its fair values on the acquisition date with the exception of a patent and a trademark, neither of which had been previously recorded. The fair values of the patent and trademark on the date of acquisition were $30,000 and $20,000 respectively.

On January 2, 2020, ABC sold 7,000 shares of 123 on the open market for $57,750.

ABC Inc. uses the equity method to account for its investment in 123 Inc.

What percentage of its Investment in 123 was sold by ABC?

A) 14%

B) 50%

C) 56%

D) 20%

On January 2, 2020, ABC sold 7,000 shares of 123 on the open market for $57,750.

ABC Inc. uses the equity method to account for its investment in 123 Inc.

What percentage of its Investment in 123 was sold by ABC?

A) 14%

B) 50%

C) 56%

D) 20%

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 64 في هذه المجموعة.

فتح الحزمة

k this deck

12

On January 1, 2019, Hanson Inc. purchased 54,000 voting shares out of Marvin Inc.'s 90,000 outstanding voting shares for $240,000. On that date, Marvin's common shares and retained earnings were valued at $60,000 and $90,000, respectively. Marvin's book values approximated its fair values on the acquisition date with the exception of the company's equipment, which was estimated to have a fair value that was $50,000 in excess of its recorded book value. The equipment was estimated to have a useful life of eight years. Both companies use straight line amortization exclusively. On January 1, 2020, Hanson purchased an additional 9,000 shares of Marvin Inc. on the open market for $45,000. On this date, Marvin's book values were equal to its fair values with the exception of the company's equipment, which is now thought to be undervalued by $60,000. Moreover, the equipment's estimated useful life was revised to 5 years on this date.

Marvin's net income and dividends for 2019 and 2020 are as follows:

Marvin's goodwill suffered an impairment loss of $5,000 during 2019. Hanson Inc. uses the equity method to account for its investment in Marvin Inc.

By how much would the non-controlling interest amount have changed as a result of Hanson's second purchase of shares on January 1, 2020?

A) A decrease of $43,975.

B) A decrease of $43,350.

C) An increase of $37,857.

D) An increase of $43,975.

Marvin's net income and dividends for 2019 and 2020 are as follows:

Marvin's goodwill suffered an impairment loss of $5,000 during 2019. Hanson Inc. uses the equity method to account for its investment in Marvin Inc.By how much would the non-controlling interest amount have changed as a result of Hanson's second purchase of shares on January 1, 2020?

A) A decrease of $43,975.

B) A decrease of $43,350.

C) An increase of $37,857.

D) An increase of $43,975.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 64 في هذه المجموعة.

فتح الحزمة

k this deck

13

On January 1, 2019, Hanson Inc. purchased 54,000 voting shares out of Marvin Inc.'s 90,000 outstanding voting shares for $240,000. On that date, Marvin's common shares and retained earnings were valued at $60,000 and $90,000, respectively. Marvin's book values approximated its fair values on the acquisition date with the exception of the company's equipment, which was estimated to have a fair value that was $50,000 in excess of its recorded book value. The equipment was estimated to have a useful life of eight years. Both companies use straight line amortization exclusively. On January 1, 2020, Hanson purchased an additional 9,000 shares of Marvin Inc. on the open market for $45,000. On this date, Marvin's book values were equal to its fair values with the exception of the company's equipment, which is now thought to be undervalued by $60,000. Moreover, the equipment's estimated useful life was revised to 5 years on this date.

Marvin's net income and dividends for 2019 and 2020 are as follows:

Marvin's goodwill suffered an impairment loss of $5,000 during 2019. Hanson Inc. uses the equity method to account for its investment in Marvin Inc.

What is the amount of goodwill arising from Hanson's January 1, 2019 acquisition?

A) $50,000

B) $60,000

C) $80,000

D) $200,000

Marvin's net income and dividends for 2019 and 2020 are as follows:

Marvin's goodwill suffered an impairment loss of $5,000 during 2019. Hanson Inc. uses the equity method to account for its investment in Marvin Inc.What is the amount of goodwill arising from Hanson's January 1, 2019 acquisition?

A) $50,000

B) $60,000

C) $80,000

D) $200,000

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 64 في هذه المجموعة.

فتح الحزمة

k this deck

14

On January 1, 2019, Hanson Inc. purchased 54,000 voting shares out of Marvin Inc.'s 90,000 outstanding voting shares for $240,000. On that date, Marvin's common shares and retained earnings were valued at $60,000 and $90,000, respectively. Marvin's book values approximated its fair values on the acquisition date with the exception of the company's equipment, which was estimated to have a fair value that was $50,000 in excess of its recorded book value. The equipment was estimated to have a useful life of eight years. Both companies use straight line amortization exclusively. On January 1, 2020, Hanson purchased an additional 9,000 shares of Marvin Inc. on the open market for $45,000. On this date, Marvin's book values were equal to its fair values with the exception of the company's equipment, which is now thought to be undervalued by $60,000. Moreover, the equipment's estimated useful life was revised to 5 years on this date.

Marvin's net income and dividends for 2019 and 2020 are as follows:

Marvin's goodwill suffered an impairment loss of $5,000 during 2019. Hanson Inc. uses the equity method to account for its investment in Marvin Inc.

Assuming that Hanson had no recorded goodwill prior to January 1, 2019, what would be the amount of goodwill appearing on Hanson's December 31, 2019 consolidated balance sheet?

A) $75,000

B) $80,000

C) $117,000

D) $195,000

Marvin's net income and dividends for 2019 and 2020 are as follows:

Marvin's goodwill suffered an impairment loss of $5,000 during 2019. Hanson Inc. uses the equity method to account for its investment in Marvin Inc.Assuming that Hanson had no recorded goodwill prior to January 1, 2019, what would be the amount of goodwill appearing on Hanson's December 31, 2019 consolidated balance sheet?

A) $75,000

B) $80,000

C) $117,000

D) $195,000

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 64 في هذه المجموعة.

فتح الحزمة

k this deck

15

ABC Inc. purchased 35,000 voting shares out of 123 Inc.'s 50,000 outstanding voting shares for $350,000 on January 1, 2020. On the date of acquisition, 123's common shares and retained earnings were valued at $120,000 and $180,000, respectively. 123's book values approximated its fair values on the acquisition date with the exception of a patent and a trademark, neither of which had been previously recorded. The fair values of the patent and trademark on the date of acquisition were $30,000 and $20,000 respectively.

On January 2, 2020, ABC sold 7,000 shares of 123 on the open market for $57,750.

ABC Inc. uses the equity method to account for its investment in 123 Inc.

What is the amount of the non-controlling interest at acquisition?

A) $8,400.

B) $350,000.

C) $50,000.

D) $150,000.

On January 2, 2020, ABC sold 7,000 shares of 123 on the open market for $57,750.

ABC Inc. uses the equity method to account for its investment in 123 Inc.

What is the amount of the non-controlling interest at acquisition?

A) $8,400.

B) $350,000.

C) $50,000.

D) $150,000.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 64 في هذه المجموعة.

فتح الحزمة

k this deck

16

On January 1, 2019, Hanson Inc. purchased 54,000 voting shares out of Marvin Inc.'s 90,000 outstanding voting shares for $240,000. On that date, Marvin's common shares and retained earnings were valued at $60,000 and $90,000, respectively. Marvin's book values approximated its fair values on the acquisition date with the exception of the company's equipment, which was estimated to have a fair value that was $50,000 in excess of its recorded book value. The equipment was estimated to have a useful life of eight years. Both companies use straight line amortization exclusively. On January 1, 2020, Hanson purchased an additional 9,000 shares of Marvin Inc. on the open market for $45,000. On this date, Marvin's book values were equal to its fair values with the exception of the company's equipment, which is now thought to be undervalued by $60,000. Moreover, the equipment's estimated useful life was revised to 5 years on this date.

Marvin's net income and dividends for 2019 and 2020 are as follows:

Marvin's goodwill suffered an impairment loss of $5,000 during 2019. Hanson Inc. uses the equity method to account for its investment in Marvin Inc.

What effect (if any) would Hanson's January 1, 2020 purchase have on the company's consolidated cash flows for the year?

A) There would be no effect.

B) There would be a decrease in cash of $45,000 to the consolidated entity.

C) There would be a decrease in cash of $200,000 to the consolidated entity.

D) There would be a decrease in cash of $236,000 to the consolidated entity.

Marvin's net income and dividends for 2019 and 2020 are as follows:

Marvin's goodwill suffered an impairment loss of $5,000 during 2019. Hanson Inc. uses the equity method to account for its investment in Marvin Inc.What effect (if any) would Hanson's January 1, 2020 purchase have on the company's consolidated cash flows for the year?

A) There would be no effect.

B) There would be a decrease in cash of $45,000 to the consolidated entity.

C) There would be a decrease in cash of $200,000 to the consolidated entity.

D) There would be a decrease in cash of $236,000 to the consolidated entity.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 64 في هذه المجموعة.

فتح الحزمة

k this deck

17

On January 1, 2019, Hanson Inc. purchased 54,000 voting shares out of Marvin Inc.'s 90,000 outstanding voting shares for $240,000. On that date, Marvin's common shares and retained earnings were valued at $60,000 and $90,000, respectively. Marvin's book values approximated its fair values on the acquisition date with the exception of the company's equipment, which was estimated to have a fair value that was $50,000 in excess of its recorded book value. The equipment was estimated to have a useful life of eight years. Both companies use straight line amortization exclusively. On January 1, 2020, Hanson purchased an additional 9,000 shares of Marvin Inc. on the open market for $45,000. On this date, Marvin's book values were equal to its fair values with the exception of the company's equipment, which is now thought to be undervalued by $60,000. Moreover, the equipment's estimated useful life was revised to 5 years on this date.

Marvin's net income and dividends for 2019 and 2020 are as follows:

Marvin's goodwill suffered an impairment loss of $5,000 during 2019. Hanson Inc. uses the equity method to account for its investment in Marvin Inc.

What percentage of Marvin's shares was purchased by Hanson on January 1, 2019?

A) 10%

B) 60%

C) 70%

D) 90%

Marvin's net income and dividends for 2019 and 2020 are as follows:

Marvin's goodwill suffered an impairment loss of $5,000 during 2019. Hanson Inc. uses the equity method to account for its investment in Marvin Inc.What percentage of Marvin's shares was purchased by Hanson on January 1, 2019?

A) 10%

B) 60%

C) 70%

D) 90%

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 64 في هذه المجموعة.

فتح الحزمة

k this deck

18

ABC Inc. purchased 35,000 voting shares out of 123 Inc.'s 50,000 outstanding voting shares for $350,000 on January 1, 2020. On the date of acquisition, 123's common shares and retained earnings were valued at $120,000 and $180,000, respectively. 123's book values approximated its fair values on the acquisition date with the exception of a patent and a trademark, neither of which had been previously recorded. The fair values of the patent and trademark on the date of acquisition were $30,000 and $20,000 respectively.

On January 2, 2020, ABC sold 7,000 shares of 123 on the open market for $57,750.

ABC Inc. uses the equity method to account for its investment in 123 Inc.

What is the amount of goodwill arising from this business combination?

A) ($5,000)

B) Nil

C) $5,000

D) $150,000

On January 2, 2020, ABC sold 7,000 shares of 123 on the open market for $57,750.

ABC Inc. uses the equity method to account for its investment in 123 Inc.

What is the amount of goodwill arising from this business combination?

A) ($5,000)

B) Nil

C) $5,000

D) $150,000

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 64 في هذه المجموعة.

فتح الحزمة

k this deck

19

Assume that X Corp. controls Y Corp., X constantly purchases and sells Y's voting shares on the open market while always ensuring that it maintains a controlling interest over Y. Which of the following statements pertaining to X buying and selling activity is correct?

A) X's activity has no effect on the non-controlling interest.

B) As X sells shares of Y, the non-controlling interest increases.

C) As X sells shares of Y, the non-controlling interest decreases.

D) As X buys shares of Y, the non-controlling interest increases.

A) X's activity has no effect on the non-controlling interest.

B) As X sells shares of Y, the non-controlling interest increases.

C) As X sells shares of Y, the non-controlling interest decreases.

D) As X buys shares of Y, the non-controlling interest increases.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 64 في هذه المجموعة.

فتح الحزمة

k this deck

20