Deck 10: Property, Plant, and Equipment and Intangible Assets: Acquisition

ملء الشاشة (f)

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

A company has the following expenditures during the year.  The company believes that these efforts have increased the fair value of the entire company by $325,000. How much goodwill can the company recognize at the end of the year associated with these expenditures?

The company believes that these efforts have increased the fair value of the entire company by $325,000. How much goodwill can the company recognize at the end of the year associated with these expenditures?

A) $0.

B) $80,000.

C) $230,000.

D) $325,000.

The company believes that these efforts have increased the fair value of the entire company by $325,000. How much goodwill can the company recognize at the end of the year associated with these expenditures?A) $0.

B) $80,000.

C) $230,000.

D) $325,000.

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

On July 1, 2018, Larkin Co. purchased a $400,000 tract of land that is intended to be the site of a new office complex. Larkin incurred additional costs and realized salvage proceeds during 2018 as follows:  What would be the balance in the land account as of December 31, 2018?

What would be the balance in the land account as of December 31, 2018?

A) $400,000.

B) $475,000.

C) $477,000.

D) $487,000.

What would be the balance in the land account as of December 31, 2018?A) $400,000.

B) $475,000.

C) $477,000.

D) $487,000.

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

Juliana Corporation purchased all of the outstanding stock of Caldwell Inc., paying $2,700,000 cash. Juliana assumed all of the liabilities of Caldwell. Book values and fair values of acquired assets and liabilities were:  Juliana would record goodwill of:

Juliana would record goodwill of:

A) $1,180,000.

B) $600,000.

C) $880,000.

D) $100,000.

Juliana would record goodwill of:A) $1,180,000.

B) $600,000.

C) $880,000.

D) $100,000.

سؤال

سؤال

سؤال

سؤال

سؤال

Simpson and Homer Corporation acquired an office building on three acres of land for a lump-sum price of $2,400,000. The building was completely furnished. According to independent appraisals, the fair values were $1,300,000, $780,000, and $520,000 for the building, land, and furniture and fixtures, respectively. The initial values of the building, land, and furniture and fixtures would be:

A) Option A

B) Option B

C) Option C

D) Option D

A) Option A

B) Option B

C) Option C

D) Option D

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

Cantor Corporation acquired a manufacturing facility on four acres of land for a lump-sum price of $8,000,000. The building included used but functional equipment. According to independent appraisals, the fair values were $4,500,000, $3,000,000, and $2,500,000 for the building, land, and equipment, respectively. The initial values of the building, land, and equipment would be:

A) Option A

B) Option B

C) Option C

D) Option D

A) Option A

B) Option B

C) Option C

D) Option D

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

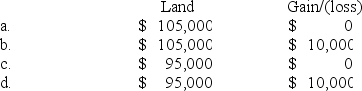

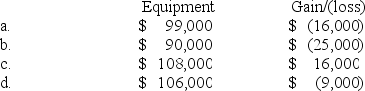

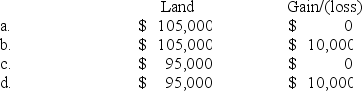

Bloomington Inc. exchanged land for equipment and $3,000 in cash. The book value and the fair value of the land were $104,000 and $90,000, respectively. Assuming that the exchange has commercial substance, Bloomington would record equipment and a gain/(loss) of:

A) Option A

B) Option B

C) Option C

D) Option D

A) Option A

B) Option B

C) Option C

D) Option D

سؤال

سؤال

Horton Stores exchanged land and cash of $5,000 for similar land. The book value and the fair value of the land were $90,000 and $100,000, respectively. Assuming that the exchange has commercial substance, Horton would record land-new and a gain/(loss) of:

A) Option A

B) Option B

C) Option C

D) Option D

A) Option A

B) Option B

C) Option C

D) Option D

سؤال

سؤال

سؤال

سؤال

سؤال

P. Chang & Co. exchanged land and $9,000 cash for equipment. The book value and the fair value of the land were $106,000 and $90,000, respectively. Assuming that the exchange has commercial substance, Chang would record equipment and a gain/(loss) of:

A) Option A

B) Option B

C) Option C

D) Option D

A) Option A

B) Option B

C) Option C

D) Option D

سؤال

Horton Stores exchanged land and cash of $5,000 for similar land. The book value and the fair value of the land were $90,000 and $100,000, respectively. Assuming that the exchange lacks commercial substance, Horton would record land-new and a gain/(loss) of:

A) Option A

B) Option B

C) Option C

D) Option D

A) Option A

B) Option B

C) Option C

D) Option D

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

فتح الحزمة

قم بالتسجيل لفتح البطاقات في هذه المجموعة!

Unlock Deck

Unlock Deck

1/149

العب

ملء الشاشة (f)

Deck 10: Property, Plant, and Equipment and Intangible Assets: Acquisition

1

Productive assets that are physically consumed in operations are:

A) Equipment.

B) Land.

C) Land improvements.

D) Natural resources.

A) Equipment.

B) Land.

C) Land improvements.

D) Natural resources.

D

2

A distinguishing characteristic of intangible assets is that the extent and timing of their future benefits typically are highly uncertain.

True

3

Sales tax paid on equipment acquired for use in the business is not capitalized.

False

4

Property, plant, and equipment and intangible assets are long-term, revenue producing assets.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 149 في هذه المجموعة.

فتح الحزمة

k this deck

5

An exclusive 20-year right to manufacture a product or use a process is a:

A) Patent.

B) Copyright.

C) Trademark.

D) Franchise.

A) Patent.

B) Copyright.

C) Trademark.

D) Franchise.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 149 في هذه المجموعة.

فتح الحزمة

k this deck

6

The relative fair values are used to determine the valuation of individual assets acquired in a lump-sum purchase.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 149 في هذه المجموعة.

فتح الحزمة

k this deck

7

A company that prepares its financial statements according to International Financial Reporting Standards (IFRS) accounts for a government grant by recognizing revenue for the amount of the grant.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 149 في هذه المجموعة.

فتح الحزمة

k this deck

8

The fair value of the asset, debt, or equity securities given in a noncash acquisition should determine the value of the consideration received.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 149 في هذه المجموعة.

فتح الحزمة

k this deck

9

The FASB's required accounting treatment for research and development costs often understates both net income and assets.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 149 في هذه المجموعة.

فتح الحزمة

k this deck

10

Costs incurred after discovery of a natural resource but before production begins are reported as expenses of the period in which the expenditures are made.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 149 في هذه المجموعة.

فتح الحزمة

k this deck

11

The successful efforts method of accounting for oil and gas exploration costs allows costs incurred in searching for oil and gas within a large geographical area to be capitalized.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 149 في هذه المجموعة.

فتح الحزمة

k this deck

12

Goodwill is:

A) Amortized over the greater of its estimated life or 40 years.

B) Only recorded by the seller of a business.

C) The excess of the fair value of a business over the fair value of all net identifiable assets.

D) None of these answer choices are correct.

A) Amortized over the greater of its estimated life or 40 years.

B) Only recorded by the seller of a business.

C) The excess of the fair value of a business over the fair value of all net identifiable assets.

D) None of these answer choices are correct.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 149 في هذه المجموعة.

فتح الحزمة

k this deck

13

Under current GAAP, fair value is used to measure the components of all nonmonetary exchanges.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 149 في هذه المجموعة.

فتح الحزمة

k this deck

14

The interest capitalization period for a self-constructed asset ends either when the asset is substantially complete and ready for use or when interest costs no longer are being incurred.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 149 في هذه المجموعة.

فتح الحزمة

k this deck

15

A company that prepares its financial statements according to International Financial Reporting Standards (IFRS) must calculate amortization of capitalized software development costs in the same way as under U.S. GAAP.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 149 في هذه المجموعة.

فتح الحزمة

k this deck

16

According to International Financial Reporting Standards (IFRS), all research and development expenditures are expensed in the period incurred.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 149 في هذه المجموعة.

فتح الحزمة

k this deck

17

The acquisition costs of property, plant, and equipment do not include:

A) The ordinary and necessary costs to bring the asset to its desired condition and location for use.

B) The net invoice price.

C) Legal fees, delivery charges, installation, and any applicable sales tax.

D) Maintenance costs during the first 30 days of use.

A) The ordinary and necessary costs to bring the asset to its desired condition and location for use.

B) The net invoice price.

C) Legal fees, delivery charges, installation, and any applicable sales tax.

D) Maintenance costs during the first 30 days of use.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 149 في هذه المجموعة.

فتح الحزمة

k this deck

18

Property, plant, and equipment and intangible assets are:

A) Created by the normal operation of the business and include accounts receivable.

B) All assets except cash and cash equivalents.

C) Current and long-term assets used in the production of either goods or services.

D) Long-term revenue-producing assets.

A) Created by the normal operation of the business and include accounts receivable.

B) All assets except cash and cash equivalents.

C) Current and long-term assets used in the production of either goods or services.

D) Long-term revenue-producing assets.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 149 في هذه المجموعة.

فتح الحزمة

k this deck

19

Demolition costs to remove an old building from land purchased as a site for a new building are considered part of the cost of the new building.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 149 في هذه المجموعة.

فتح الحزمة

k this deck

20

The initial cost of property, plant, and equipment includes all the identifiable expenditures necessary to bring the asset to its desired condition and location for use.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 149 في هذه المجموعة.

فتح الحزمة

k this deck

21

The cost of constructing a new parking lot at the company's office building would be recorded as:

A) Land.

B) Land improvement.

C) Building.

D) Equipment.

A) Land.

B) Land improvement.

C) Building.

D) Equipment.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 149 في هذه المجموعة.

فتح الحزمة

k this deck

22

Grab Manufacturing Co. purchased a 10-ton draw press at a cost of $180,000 with terms of 5/15, n/45. Payment was made within the discount period. Shipping costs were $4,600, which included $200 for insurance in transit. Installation costs totaled $12,000, which included $4,000 for taking out a section of a wall and rebuilding it because the press was too large for the doorway. The capitalized cost of the 10-ton draw press is:

A) $171,000.

B) $183,600.

C) $187,600.

D) $185,760.

A) $171,000.

B) $183,600.

C) $187,600.

D) $185,760.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 149 في هذه المجموعة.

فتح الحزمة

k this deck

23

On March 1, 2018, Shipley Resources entered into an agreement with the state of Alaska to obtain the rights to operate a mineral mine for $6 million. The mine is expected to produce 100,000 tons of mineral. As part of the agreement, Shipley agrees to restore the land to its original condition after mining operations are completed in approximately five years. Management has provided the following possible outflows for the restoration costs that will occur five years from now: Shipley's credit-adjusted risk-free interest rate is 10%. During 2018, Shipley extracted 18,000 tons of ore from the mine. How much accretion expense will the company record in its income statement for the 2018 fiscal year?

A) $30,326.

B) $20,697.

C) $24,837.

D) $27,294.

A) $30,326.

B) $20,697.

C) $24,837.

D) $27,294.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 149 في هذه المجموعة.

فتح الحزمة

k this deck

24

A company has the following expenditures during the year. The company believes that these efforts have increased the fair value of the entire company by $325,000. How much goodwill can the company recognize at the end of the year associated with these expenditures?

A) $0.

B) $80,000.

C) $230,000.

D) $325,000.

The company believes that these efforts have increased the fair value of the entire company by $325,000. How much goodwill can the company recognize at the end of the year associated with these expenditures?A) $0.

B) $80,000.

C) $230,000.

D) $325,000.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 149 في هذه المجموعة.

فتح الحزمة

k this deck

25

The capitalized cost of equipment excludes:

A) Maintenance.

B) Sales tax.

C) Shipping.

D) Installation.

A) Maintenance.

B) Sales tax.

C) Shipping.

D) Installation.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 149 في هذه المجموعة.

فتح الحزمة

k this deck

26

The exclusive right to benefit from a creative work, such as a film, is a:

A) Patent.

B) Copyright.

C) Trademark.

D) Franchise.

A) Patent.

B) Copyright.

C) Trademark.

D) Franchise.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 149 في هذه المجموعة.

فتح الحزمة

k this deck

27

Holiday Laboratories purchased a high-speed industrial centrifuge at a cost of $420,000. Shipping costs totaled $15,000. Foundation work to house the centrifuge cost $8,000. An additional water line had to be run to the equipment at a cost of $3,000. Labor and testing costs totaled $6,000. Materials used up in testing cost $3,000. The capitalized cost is:

A) $455,000.

B) $446,000.

C) $437,000.

D) $435,000.

A) $455,000.

B) $446,000.

C) $437,000.

D) $435,000.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 149 في هذه المجموعة.

فتح الحزمة

k this deck

28

The capitalized cost of land excludes:

A) The purchase price of the land.

B) Title insurance paid at the time of purchase.

C) Real estate commissions associated with the sale.

D) Property taxes for the first year owned.

A) The purchase price of the land.

B) Title insurance paid at the time of purchase.

C) Real estate commissions associated with the sale.

D) Property taxes for the first year owned.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 149 في هذه المجموعة.

فتح الحزمة

k this deck

29

Montana Mining Co. (MMC) paid $200 million for the right to explore and extract rare metals from land owned by the state of Montana. To obtain the rights, MMC agreed to restore the land to a suitable condition for other uses after its exploration and extraction activities. MMC incurred exploration and development costs of $60 million on the project. MMC has a credit-adjusted risk free interest rate is 7%. It estimates the possible cash flows for restoring the land, three years after its extraction activities begin, as follows:

-The asset retirement obligation (rounded) that should be reported on MMC's balance sheet one year after the extraction activities begin is:

A) $0.

B) $14.7 million.

C) $15.7 million.

D) $19.3 million.

-The asset retirement obligation (rounded) that should be reported on MMC's balance sheet one year after the extraction activities begin is:

A) $0.

B) $14.7 million.

C) $15.7 million.

D) $19.3 million.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 149 في هذه المجموعة.

فتح الحزمة

k this deck

30

If a company incurs legal obligations associated with the retirement of a tangible long-lived asset as a result of acquiring the asset:

A) The company recognizes the obligation at fair value when the asset is acquired.

B) The company recognizes the obligation at fair value when the asset is retired.

C) The company records the difference between the fair value of the asset and the obligation when the asset is acquired.

D) None of these answer choices are correct.

A) The company recognizes the obligation at fair value when the asset is acquired.

B) The company recognizes the obligation at fair value when the asset is retired.

C) The company records the difference between the fair value of the asset and the obligation when the asset is acquired.

D) None of these answer choices are correct.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 149 في هذه المجموعة.

فتح الحزمة

k this deck

31

A contractual arrangement under which one party grants another party the exclusive right to use a trademark or tradename is a:

A) Patent.

B) Copyright.

C) Trademark.

D) Franchise.

A) Patent.

B) Copyright.

C) Trademark.

D) Franchise.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 149 في هذه المجموعة.

فتح الحزمة

k this deck

32

On July 1, 2018, Larkin Co. purchased a $400,000 tract of land that is intended to be the site of a new office complex. Larkin incurred additional costs and realized salvage proceeds during 2018 as follows: What would be the balance in the land account as of December 31, 2018?

A) $400,000.

B) $475,000.

C) $477,000.

D) $487,000.

What would be the balance in the land account as of December 31, 2018?A) $400,000.

B) $475,000.

C) $477,000.

D) $487,000.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 149 في هذه المجموعة.

فتح الحزمة

k this deck

33

The exclusive right to display a symbol of product identification is a:

A) Patent.

B) Copyright.

C) Trademark.

D) Franchise.

A) Patent.

B) Copyright.

C) Trademark.

D) Franchise.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 149 في هذه المجموعة.

فتح الحزمة

k this deck

34

Which of the following does not pertain to accounting for asset retirement obligations?

A) They accrete (increase over time) at the company's credit-adjusted risk-free rate.

B) They must be recognized according to GAAP.

C) Statement of Financial Accounting Concepts No. 7 is applied when adjusting cash flow obligations for uncertainty.

D) All of these answer choices pertain to accounting for asset retirement obligations.

A) They accrete (increase over time) at the company's credit-adjusted risk-free rate.

B) They must be recognized according to GAAP.

C) Statement of Financial Accounting Concepts No. 7 is applied when adjusting cash flow obligations for uncertainty.

D) All of these answer choices pertain to accounting for asset retirement obligations.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 149 في هذه المجموعة.

فتح الحزمة

k this deck

35

Montana Mining Co. (MMC) paid $200 million for the right to explore and extract rare metals from land owned by the state of Montana. To obtain the rights, MMC agreed to restore the land to a suitable condition for other uses after its exploration and extraction activities. MMC incurred exploration and development costs of $60 million on the project. MMC has a credit-adjusted risk free interest rate is 7%. It estimates the possible cash flows for restoring the land, three years after its extraction activities begin, as follows:

- The asset retirement obligation (rounded) that should be recognized by MMC at the beginning of the extraction activities is:

A) $8.2 million.

B) $14.7 million.

C) $18 million.

D) $30 million.

- The asset retirement obligation (rounded) that should be recognized by MMC at the beginning of the extraction activities is:

A) $8.2 million.

B) $14.7 million.

C) $18 million.

D) $30 million.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 149 في هذه المجموعة.

فتح الحزمة

k this deck

36

Vijay Inc. purchased a three-acre tract of land for a building site for $320,000. On the land was a building with an appraised value of $120,000. The company demolished the old building at a cost of $12,000, but was able to sell scrap from the building for $1,500. The cost of title insurance was $900 and attorney fees for reviewing the contract were $500. Property taxes paid were $3,000, of which $250 covered the period subsequent to the purchase date. The capitalized cost of the land is:

A) $336,400.

B) $336,150.

C) $334,650.

D) $201,150.

A) $336,400.

B) $336,150.

C) $334,650.

D) $201,150.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 149 في هذه المجموعة.

فتح الحزمة

k this deck

37

Lake Incorporated purchased all of the outstanding stock of Huron Company paying $950,000 cash. Lake assumed all of the liabilities of Huron. Book values and fair values of acquired assets and liabilities were: Lake would record goodwill of:

A) $0.

B) $75,000.

C) $445,000.

D) $250,000.

A) $0.

B) $75,000.

C) $445,000.

D) $250,000.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 149 في هذه المجموعة.

فتح الحزمة

k this deck

38

Assets acquired in a lump-sum purchase are valued based on:

A) Their assessed valuation.

B) Their relative fair values.

C) The present value of their future cash flows.

D) Their cost plus the difference between their cost and fair values.

A) Their assessed valuation.

B) Their relative fair values.

C) The present value of their future cash flows.

D) Their cost plus the difference between their cost and fair values.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 149 في هذه المجموعة.

فتح الحزمة

k this deck

39

Asset retirement obligations:

A) Increase the balance in the related asset account.

B) Are measured at fair value in the balance sheet.

C) Are liabilities associated with the restoration of a long-term asset.

D) All of these answer choices are correct.

A) Increase the balance in the related asset account.

B) Are measured at fair value in the balance sheet.

C) Are liabilities associated with the restoration of a long-term asset.

D) All of these answer choices are correct.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 149 في هذه المجموعة.

فتح الحزمة

k this deck

40

Juliana Corporation purchased all of the outstanding stock of Caldwell Inc., paying $2,700,000 cash. Juliana assumed all of the liabilities of Caldwell. Book values and fair values of acquired assets and liabilities were: Juliana would record goodwill of:

A) $1,180,000.

B) $600,000.

C) $880,000.

D) $100,000.

Juliana would record goodwill of:A) $1,180,000.

B) $600,000.

C) $880,000.

D) $100,000.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 149 في هذه المجموعة.

فتح الحزمة

k this deck

41

The basic principle used to value an asset acquired in a nonmonetary exchange is to value it at:

A) Fair value of the asset(s) given up.

B) The book value of the asset given plus any cash or other monetary consideration received.

C) Fair value or book value, whichever is smaller.

D) Book value of the asset given.

A) Fair value of the asset(s) given up.

B) The book value of the asset given plus any cash or other monetary consideration received.

C) Fair value or book value, whichever is smaller.

D) Book value of the asset given.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 149 في هذه المجموعة.

فتح الحزمة

k this deck

42

An asset acquired using a long-term note payable always will be recorded at the face amount of the note under which scenario?

A) The note payable explicitly requires the payment of interest at a realistic interest rate.

B) The note is a noninterest-bearing note.

C) The company expects to use the asset for its entire physical life.

D) Interest on the note is not payable until the note is due.

A) The note payable explicitly requires the payment of interest at a realistic interest rate.

B) The note is a noninterest-bearing note.

C) The company expects to use the asset for its entire physical life.

D) Interest on the note is not payable until the note is due.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 149 في هذه المجموعة.

فتح الحزمة

k this deck

43

On July 1, 2018, Markwell Company acquired equipment. Markwell paid $160,000 in cash on July 1, 2018, and signed a $640,000 noninterest-bearing note for the remaining balance which is due on July 1, 2019. An interest rate of 5% reflects the time value of money for this type of loan agreement.

-For what amount will Markwell record the purchase of equipment?

A) $761,905.

B) $769,523.

C) $609,523.

D) $800,000.

-For what amount will Markwell record the purchase of equipment?

A) $761,905.

B) $769,523.

C) $609,523.

D) $800,000.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 149 في هذه المجموعة.

فتح الحزمة

k this deck

44

Assets acquired under multi-year deferred payment contracts are:

A) Valued at their fair value on the date of the final payment.

B) Valued at the present value of the payments required by the contract.

C) Valued at the sum of the payments required by the contract.

D) None of these answer choices are correct.

A) Valued at their fair value on the date of the final payment.

B) Valued at the present value of the payments required by the contract.

C) Valued at the sum of the payments required by the contract.

D) None of these answer choices are correct.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 149 في هذه المجموعة.

فتح الحزمة

k this deck

45

Simpson and Homer Corporation acquired an office building on three acres of land for a lump-sum price of $2,400,000. The building was completely furnished. According to independent appraisals, the fair values were $1,300,000, $780,000, and $520,000 for the building, land, and furniture and fixtures, respectively. The initial values of the building, land, and furniture and fixtures would be:

A) Option A

B) Option B

C) Option C

D) Option D

A) Option A

B) Option B

C) Option C

D) Option D

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 149 في هذه المجموعة.

فتح الحزمة

k this deck

46

Assets acquired by the issuance of equity securities are valued based on:

A) Their fair values.

B) The fair value of the equity securities.

C) The fair value of the assets acquired or the fair value of the equity securities, whichever is more reasonably determinable.

D) The fair value of the assets acquired or the fair value of the equity securities, whichever is smaller.

A) Their fair values.

B) The fair value of the equity securities.

C) The fair value of the assets acquired or the fair value of the equity securities, whichever is more reasonably determinable.

D) The fair value of the assets acquired or the fair value of the equity securities, whichever is smaller.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 149 في هذه المجموعة.

فتح الحزمة

k this deck

47

The fixed-asset turnover ratio provides:

A) The rate of decline in asset lives.

B) The rate of replacement of fixed assets.

C) The amount of sales generated per dollar of fixed assets.

D) The decline in book value of fixed assets compared to capital expenditures.

A) The rate of decline in asset lives.

B) The rate of replacement of fixed assets.

C) The amount of sales generated per dollar of fixed assets.

D) The decline in book value of fixed assets compared to capital expenditures.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 149 في هذه المجموعة.

فتح الحزمة

k this deck

48

On June 17, the Lattern Company issued 120,000 shares of its $0.10 par value common stock in exchange for land. On the date of the transaction, the fair value of the common stock, evidenced by its market price, was $10 per share. The journal entry to record this transaction includes:

A) Debt: Land, $1,200,000.

B) Credit: Cash, $1,200,000.

C) Debit: Land, $12,000.

D) No entry for this exchange.

A) Debt: Land, $1,200,000.

B) Credit: Cash, $1,200,000.

C) Debit: Land, $12,000.

D) No entry for this exchange.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 149 في هذه المجموعة.

فتح الحزمة

k this deck

49

On September 30, 2018, Corso Steel acquired a patent from Thermo Steel. The agreement specified that Corso will pay Thermo $1,000,000 immediately and then another $1,000,000 on September 30, 2020. An interest rate of 8% reflects the time value of money for this type of loan agreement.

-What amount of interest expense, if any, would Corso record on December 31, 2019, the company's fiscal year end?

A) $68,687.

B) $60,000.

C) $80,000.

D) $69,959.

-What amount of interest expense, if any, would Corso record on December 31, 2019, the company's fiscal year end?

A) $68,687.

B) $60,000.

C) $80,000.

D) $69,959.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 149 في هذه المجموعة.

فتح الحزمة

k this deck

50

Donated assets are recorded at:

A) Zero (memo entry only).

B) The donor's book value.

C) The donee's stated value.

D) Fair value.

A) Zero (memo entry only).

B) The donor's book value.

C) The donee's stated value.

D) Fair value.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 149 في هذه المجموعة.

فتح الحزمة

k this deck

51

On September 30, 2018, Corso Steel acquired a patent from Thermo Steel. The agreement specified that Corso will pay Thermo $1,000,000 immediately and then another $1,000,000 on September 30, 2020. An interest rate of 8% reflects the time value of money for this type of loan agreement.

- Corso should record the acquisition of the patent on September 30, 2018, for what amount?

A) $2,000,000.

B) $1,912,385.

C) $1,857,340.

D) $1,714,678.

- Corso should record the acquisition of the patent on September 30, 2018, for what amount?

A) $2,000,000.

B) $1,912,385.

C) $1,857,340.

D) $1,714,678.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 149 في هذه المجموعة.

فتح الحزمة

k this deck

52

Savings Mart is a national retail chain. To entice the company to open a mega store in its jurisdiction, the city of Populationville donated a 20-acre tract of land to be used for construction. The land was originally purchased by the city for $250,000 three years ago. The appraisal value at the time of the donation was $300,000. For what amount should Savings Mart record the donated land?

A) $250,000.

B) $275,000.

C) $300,000.

D) $0; Donated assets are not recorded.

A) $250,000.

B) $275,000.

C) $300,000.

D) $0; Donated assets are not recorded.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 149 في هذه المجموعة.

فتح الحزمة

k this deck

53

On July 1, 2018, Markwell Company acquired equipment. Markwell paid $160,000 in cash on July 1, 2018, and signed a $640,000 noninterest-bearing note for the remaining balance which is due on July 1, 2019. An interest rate of 5% reflects the time value of money for this type of loan agreement.

- Which of the following should be included in the journal entry on July 1, 2018?

A) Credit: Notes payable, $609,523.

B) Debit: Equipment, $800,000.

C) Debit: Discount on notes payable, $30,477.

D) Credit: Notes payable, $609,523 and Debit: Discount on notes payable, $30,477.

- Which of the following should be included in the journal entry on July 1, 2018?

A) Credit: Notes payable, $609,523.

B) Debit: Equipment, $800,000.

C) Debit: Discount on notes payable, $30,477.

D) Credit: Notes payable, $609,523 and Debit: Discount on notes payable, $30,477.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 149 في هذه المجموعة.

فتح الحزمة

k this deck

54

Braxwell Corporation acquired the following assets associated with a manufacturing facility for a lump-sum price of $9,000,000. According to independent appraisals, the fair values were $4,000,000, $2,000,000, $3,000,000, and $1,000,000 for the building, patent, land, and equipment, respectively. The initial value of the patent would be:

A) $2,000,000.

B) $2,250,000.

C) $1,800,000.

D) $0.

A) $2,000,000.

B) $2,250,000.

C) $1,800,000.

D) $0.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 149 في هذه المجموعة.

فتح الحزمة

k this deck

55

Cantor Corporation acquired a manufacturing facility on four acres of land for a lump-sum price of $8,000,000. The building included used but functional equipment. According to independent appraisals, the fair values were $4,500,000, $3,000,000, and $2,500,000 for the building, land, and equipment, respectively. The initial values of the building, land, and equipment would be:

A) Option A

B) Option B

C) Option C

D) Option D

A) Option A

B) Option B

C) Option C

D) Option D

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 149 في هذه المجموعة.

فتح الحزمة

k this deck

56

The balance sheets of Davidson Corporation reported net fixed assets of $320,000 at the end of 2018. The fixed-asset turnover ratio for 2018 was 4.0, and sales for the year totaled $1,480,000. Net fixed assets at the end of 2017 were:

A) $470,000.

B) $370,000.

C) $420,000.

D) None of these answer choices are correct.

A) $470,000.

B) $370,000.

C) $420,000.

D) None of these answer choices are correct.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 149 في هذه المجموعة.

فتح الحزمة

k this deck

57

Maltese is a privately-owned company. On September 3, Maltese exchanged 2,000 shares of its private common stock for equipment. There is no readily available estimate of the stock's fair value. The equipment currently is selling for $80,000. The journal entry to record this transaction includes:

A) Credit: Stock revenue, $80,000.

B) Credit: Cash, $80,000.

C) Debit: Equipment, $80,000.

D) No entry is recorded for this exchange.

A) Credit: Stock revenue, $80,000.

B) Credit: Cash, $80,000.

C) Debit: Equipment, $80,000.

D) No entry is recorded for this exchange.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 149 في هذه المجموعة.

فتح الحزمة

k this deck

58

On September 30, 2018, Corso Steel acquired a patent from Thermo Steel. The agreement specified that Corso will pay Thermo $1,000,000 immediately and then another $1,000,000 on September 30, 2020. An interest rate of 8% reflects the time value of money for this type of loan agreement.

-What amount of interest expense, if any, would Corso record on December 31, 2018, the company's fiscal year end?

A) $17,147.

B) $20,000.

C) $68,687.

D) $80,000.

-What amount of interest expense, if any, would Corso record on December 31, 2018, the company's fiscal year end?

A) $17,147.

B) $20,000.

C) $68,687.

D) $80,000.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 149 في هذه المجموعة.

فتح الحزمة

k this deck

59

On January 1, 2018, Laramie Inc. acquired land for $6.2 million. Laramie paid $1.2 in cash and signed a 6% note requiring the company to pay the remaining $5 million plus interest on December 31, 2019. An interest rate of 6% properly reflects the time value of money for this type of loan agreement. For what amount should Laramie record the purchase of land?

A) $6.8 million.

B) $5.0 million.

C) $5.6 million.

D) $6.2 million.

A) $6.8 million.

B) $5.0 million.

C) $5.6 million.

D) $6.2 million.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 149 في هذه المجموعة.

فتح الحزمة

k this deck

60

A company receiving a donated asset will record:

A) An increase in revenue.

B) An increase in liabilities.

C) A decrease in liabilities.

D) An increase in revenue and A decrease in liabilities.

A) An increase in revenue.

B) An increase in liabilities.

C) A decrease in liabilities.

D) An increase in revenue and A decrease in liabilities.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 149 في هذه المجموعة.

فتح الحزمة

k this deck

61

Bloomington Inc. exchanged land for equipment and $3,000 in cash. The book value and the fair value of the land were $104,000 and $90,000, respectively. Assuming that the exchange has commercial substance, Bloomington would record equipment and a gain/(loss) of:

A) Option A

B) Option B

C) Option C

D) Option D

A) Option A

B) Option B

C) Option C

D) Option D

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 149 في هذه المجموعة.

فتح الحزمة

k this deck

62

Pensacola Inc. exchanged old equipment for new equipment in two exchange transactions. Each transaction has commercial substance.

- For Equipment A, Pensacola would record the new equipment at:

A) $68,000.

B) $63,750.

C) $67,250.

D) $80,000.

- For Equipment A, Pensacola would record the new equipment at:

A) $68,000.

B) $63,750.

C) $67,250.

D) $80,000.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 149 في هذه المجموعة.

فتح الحزمة

k this deck

63

Horton Stores exchanged land and cash of $5,000 for similar land. The book value and the fair value of the land were $90,000 and $100,000, respectively. Assuming that the exchange has commercial substance, Horton would record land-new and a gain/(loss) of:

A) Option A

B) Option B

C) Option C

D) Option D

A) Option A

B) Option B

C) Option C

D) Option D

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 149 في هذه المجموعة.

فتح الحزمة

k this deck

64

Interest may be capitalized:

A) On routinely manufactured goods as well as self-constructed assets.

B) On self-constructed assets from the date an entity formally adopts a plan to build a discrete project.

C) Whether or not there is specific borrowing for the construction.

D) Whether or not there are actual interest costs incurred.

A) On routinely manufactured goods as well as self-constructed assets.

B) On self-constructed assets from the date an entity formally adopts a plan to build a discrete project.

C) Whether or not there is specific borrowing for the construction.

D) Whether or not there are actual interest costs incurred.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 149 في هذه المجموعة.

فتح الحزمة

k this deck

65

Interest is eligible to be capitalized as part of an asset's cost, rather than being expensed immediately, when:

A) The interest is incurred during the construction period of the asset.

B) The asset is a discrete construction project for sale or lease.

C) The asset is self-constructed, rather than acquired.

D) All of these answer choices are correct.

A) The interest is incurred during the construction period of the asset.

B) The asset is a discrete construction project for sale or lease.

C) The asset is self-constructed, rather than acquired.

D) All of these answer choices are correct.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 149 في هذه المجموعة.

فتح الحزمة

k this deck

66

On June 1, 2017, the Crocus Company began construction of a new manufacturing plant. The plant was completed on October 31, 2018. Expenditures on the project were as follows ($ in millions): On July 1, 2017, Crocus obtained a $70 million construction loan with a 6% interest rate. The loan was outstanding through the end of October, 2018. The company's only other interest-bearing debt was a long-term note for $100 million with an interest rate of 8%. This note was outstanding during all of 2017 and 2018. The company's fiscal year-end is December 31.

-What is the amount of interest that Crocus should capitalize in 2018, using the specific interest method (rounded to the nearest thousand dollars)?

A) $7,248,000 (rounded).

B) $7,283,000 (rounded).

C) $8,740,000 (rounded).

D) None of these answer choices are correct.

-What is the amount of interest that Crocus should capitalize in 2018, using the specific interest method (rounded to the nearest thousand dollars)?

A) $7,248,000 (rounded).

B) $7,283,000 (rounded).

C) $8,740,000 (rounded).

D) None of these answer choices are correct.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 149 في هذه المجموعة.

فتح الحزمة

k this deck

67

In a nonmonetary exchange of equipment, if the exchange has commercial substance, a gain is recognized if:

A) The fair value of the equipment received exceeds the book value of the equipment received.

B) The book value of the equipment received exceeds the fair value of the equipment given up.

C) The fair value of the equipment surrendered exceeds the book value of the equipment given up.

D) None of these answer choices are correct.

A) The fair value of the equipment received exceeds the book value of the equipment received.

B) The book value of the equipment received exceeds the fair value of the equipment given up.

C) The fair value of the equipment surrendered exceeds the book value of the equipment given up.

D) None of these answer choices are correct.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 149 في هذه المجموعة.

فتح الحزمة

k this deck

68

P. Chang & Co. exchanged land and $9,000 cash for equipment. The book value and the fair value of the land were $106,000 and $90,000, respectively. Assuming that the exchange has commercial substance, Chang would record equipment and a gain/(loss) of:

A) Option A

B) Option B

C) Option C

D) Option D

A) Option A

B) Option B

C) Option C

D) Option D

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 149 في هذه المجموعة.

فتح الحزمة

k this deck

69

Horton Stores exchanged land and cash of $5,000 for similar land. The book value and the fair value of the land were $90,000 and $100,000, respectively. Assuming that the exchange lacks commercial substance, Horton would record land-new and a gain/(loss) of:

A) Option A

B) Option B

C) Option C

D) Option D

A) Option A

B) Option B

C) Option C

D) Option D

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 149 في هذه المجموعة.

فتح الحزمة

k this deck

70

On June 1, 2017, the Crocus Company began construction of a new manufacturing plant. The plant was completed on October 31, 2018. Expenditures on the project were as follows ($ in millions): On July 1, 2017, Crocus obtained a $70 million construction loan with a 6% interest rate. The loan was outstanding through the end of October, 2018. The company's only other interest-bearing debt was a long-term note for $100 million with an interest rate of 8%. This note was outstanding during all of 2017 and 2018. The company's fiscal year-end is December 31.

- What is the amount of interest that Crocus should capitalize in 2017, using the specific interest method?

A) $1.90 million.

B) $1.95 million.

C) $2.96 million.

D) None of these answer choices are correct.

- What is the amount of interest that Crocus should capitalize in 2017, using the specific interest method?

A) $1.90 million.

B) $1.95 million.

C) $2.96 million.

D) None of these answer choices are correct.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 149 في هذه المجموعة.

فتح الحزمة

k this deck

71

Below is information relative to an exchange of similar assets by Grand Forks Corp. Assume the exchange has commercial substance.

-In Case B, Grand Forks would record a gain/(loss) of:

A) $5,000.

B) $3,000.

C) ($5,000).

D) ($3,000).

-In Case B, Grand Forks would record a gain/(loss) of:

A) $5,000.

B) $3,000.

C) ($5,000).

D) ($3,000).

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 149 في هذه المجموعة.

فتح الحزمة

k this deck

72

In computing capitalized interest, average accumulated expenditures:

A) Is the arithmetic mean of all construction expenditures.

B) Is determined by time-weighting individual expenditures made during the asset construction period.

C) Is multiplied by the company's most recent financing rates.

D) All of these answer choices are correct.

A) Is the arithmetic mean of all construction expenditures.

B) Is determined by time-weighting individual expenditures made during the asset construction period.

C) Is multiplied by the company's most recent financing rates.

D) All of these answer choices are correct.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 149 في هذه المجموعة.

فتح الحزمة

k this deck

73

Interest is not capitalized for:

A) Assets that are constructed as discrete projects for sale or lease.

B) Assets constructed for a company's own use.

C) Inventories routinely and repetitively produced in large quantities.

D) Interest is capitalized for all of these items.

A) Assets that are constructed as discrete projects for sale or lease.

B) Assets constructed for a company's own use.

C) Inventories routinely and repetitively produced in large quantities.

D) Interest is capitalized for all of these items.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 149 في هذه المجموعة.

فتح الحزمة

k this deck

74

Alamos Co. exchanged equipment and $18,000 cash for similar equipment. The book value and the fair value of the old equipment were $82,000 and $90,000, respectively.

- Assuming that the exchange has commercial substance, Alamos would record a gain/(loss) of:

A) $26,000.

B) $8,000.

C) ($8,000).

D) $0.

- Assuming that the exchange has commercial substance, Alamos would record a gain/(loss) of:

A) $26,000.

B) $8,000.

C) ($8,000).

D) $0.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 149 في هذه المجموعة.

فتح الحزمة

k this deck

75

The cost of self-constructed fixed assets should:

A) Include allocated indirect costs just as they are for production of products.

B) Include only incremental indirect costs.

C) Include only specifically identifiable indirect costs.

D) Not include indirect costs.

A) Include allocated indirect costs just as they are for production of products.

B) Include only incremental indirect costs.

C) Include only specifically identifiable indirect costs.

D) Not include indirect costs.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 149 في هذه المجموعة.

فتح الحزمة

k this deck

76

On June 1, 2017, the Crocus Company began construction of a new manufacturing plant. The plant was completed on October 31, 2018. Expenditures on the project were as follows ($ in millions): On July 1, 2017, Crocus obtained a $70 million construction loan with a 6% interest rate. The loan was outstanding through the end of October, 2018. The company's only other interest-bearing debt was a long-term note for $100 million with an interest rate of 8%. This note was outstanding during all of 2017 and 2018. The company's fiscal year-end is December 31.

-In computing the capitalized interest for 2018, Crocus' average accumulated expenditures are:

A) $46.30 million.

B) $103.54 million.

C) $122.30 million.

D) $124.25 million.

-In computing the capitalized interest for 2018, Crocus' average accumulated expenditures are:

A) $46.30 million.

B) $103.54 million.

C) $122.30 million.

D) $124.25 million.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 149 في هذه المجموعة.

فتح الحزمة

k this deck

77

Alamos Co. exchanged equipment and $18,000 cash for similar equipment. The book value and the fair value of the old equipment were $82,000 and $90,000, respectively.

-Assuming that the exchange lacks commercial substance, Alamos would record a gain/(loss) of:

A) $26,000.

B) $8,000.

C) ($8,000).

D) $0.

-Assuming that the exchange lacks commercial substance, Alamos would record a gain/(loss) of:

A) $26,000.

B) $8,000.

C) ($8,000).

D) $0.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 149 في هذه المجموعة.

فتح الحزمة

k this deck

78

Pensacola Inc. exchanged old equipment for new equipment in two exchange transactions. Each transaction has commercial substance.

- For Equipment B, Pensacola would record a gain/(loss) of:

A) $4,000.

B) ($4,000).

C) ($10,000).

D) None of these answer choices are correct.

- For Equipment B, Pensacola would record a gain/(loss) of:

A) $4,000.

B) ($4,000).

C) ($10,000).

D) None of these answer choices are correct.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 149 في هذه المجموعة.

فتح الحزمة

k this deck

79

Average accumulated expenditures:

A) Is an approximation of the average debt a firm would have outstanding if it financed all construction through debt.

B) Is computed as a simple average if all construction expenditures are made at the end of the period.

C) Are irrelevant if the company's total outstanding debt is less than total costs of construction.

D) All of these answer choices are true statements.

A) Is an approximation of the average debt a firm would have outstanding if it financed all construction through debt.

B) Is computed as a simple average if all construction expenditures are made at the end of the period.

C) Are irrelevant if the company's total outstanding debt is less than total costs of construction.

D) All of these answer choices are true statements.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 149 في هذه المجموعة.

فتح الحزمة

k this deck

80

Below is information relative to an exchange of similar assets by Grand Forks Corp. Assume the exchange has commercial substance.

- In Case A, Grand Forks would record the new equipment at:

A) $65,000.

B) $75,000.

C) $50,000.

D) $60,000.

- In Case A, Grand Forks would record the new equipment at:

A) $65,000.

B) $75,000.

C) $50,000.

D) $60,000.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 149 في هذه المجموعة.

فتح الحزمة

k this deck

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 149 في هذه المجموعة.