Deck 16: Fundamentals of Variance Analysis

ملء الشاشة (f)

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

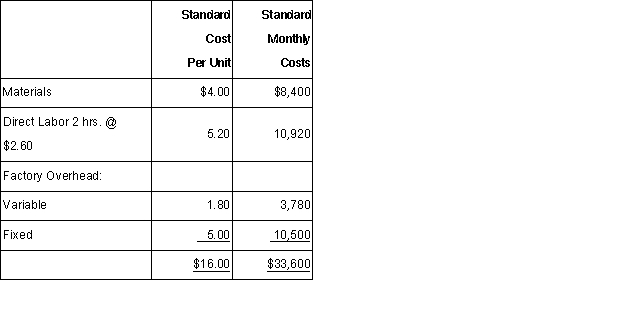

The following information summarizes the standard cost for producing one metal tennis racket frame at Spaulding Industries.In addition,the variances for one month's production are given.Assume that all inventory accounts have zero balances at the beginning of the month.  What was the actual quantity of materials used during the month?

What was the actual quantity of materials used during the month?

A) 2,156.

B) 2,100.

C) 2,225.

D) 1,975.

What was the actual quantity of materials used during the month?A) 2,156.

B) 2,100.

C) 2,225.

D) 1,975.

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

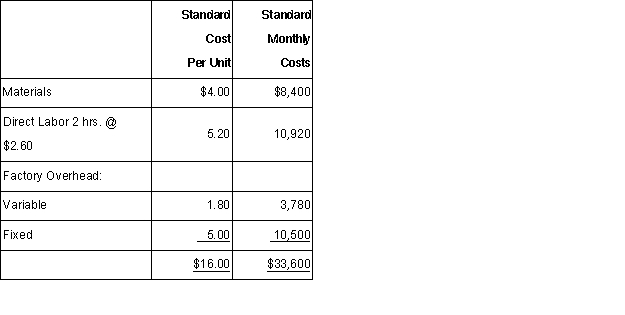

The following information summarizes the standard cost for producing one metal tennis racket frame at Spaulding Industries.In addition,the variances for one month's production are given.Assume that all inventory accounts have zero balances at the beginning of the month.  What was the actual price paid for the direct material during the month,assuming all materials purchased were put into production?

What was the actual price paid for the direct material during the month,assuming all materials purchased were put into production?

A) $4.34.

B) $4.22.

C) $4.11.

D) $4.00.

What was the actual price paid for the direct material during the month,assuming all materials purchased were put into production? A) $4.34.

B) $4.22.

C) $4.11.

D) $4.00.

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

فتح الحزمة

قم بالتسجيل لفتح البطاقات في هذه المجموعة!

Unlock Deck

Unlock Deck

1/147

العب

ملء الشاشة (f)

Deck 16: Fundamentals of Variance Analysis

1

The budget (or spending)variance for fixed production costs is the difference between the actual fixed costs and the budgeted fixed costs on the master budget.

True

2

The standard cost for a unit of output is the standard price per unit of input times the standard number of inputs per one unit of output.

True

3

The production volume variance is the difference between fixed costs on the flexible budget and the fixed costs on the master budget.

False

4

Variances are the difference between actual results and budgeted results.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 147 في هذه المجموعة.

فتح الحزمة

k this deck

5

The materials price variance is computed by multiplying the difference between the actual price and the standard price by the actual quantity of materials used in production.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 147 في هذه المجموعة.

فتح الحزمة

k this deck

6

The direct labor efficiency variance can be the result of poor supervision or poor scheduling by divisional managers.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 147 في هذه المجموعة.

فتح الحزمة

k this deck

7

Production cost variances are input variances,while sales activity variances are output variances.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 147 في هذه المجموعة.

فتح الحزمة

k this deck

8

The terms "master budget" and "flexible budget" mean the same thing and can be used interchangeably.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 147 في هذه المجموعة.

فتح الحزمة

k this deck

9

It is possible to have a favorable direct material price variance and an unfavorable direct material efficiency variance.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 147 في هذه المجموعة.

فتح الحزمة

k this deck

10

The sales activity variance is the result of a difference between budgeted units sold and actual units sold.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 147 في هذه المجموعة.

فتح الحزمة

k this deck

11

The difference between operating profits in the master budget and operating profits in the flexible budget is called a sales price variance.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 147 في هذه المجموعة.

فتح الحزمة

k this deck

12

In general,and holding all other things constant,an unfavorable variance decreases operating profits.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 147 في هذه المجموعة.

فتح الحزمة

k this deck

13

The flexible and master budget amounts are the same for fixed marketing and administrative costs.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 147 في هذه المجموعة.

فتح الحزمة

k this deck

14

If the budgeted activity level is greater than the actual activity level,then the total budgeted costs of the master budget will be greater than the total budgeted costs of the flexible budget.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 147 في هذه المجموعة.

فتح الحزمة

k this deck

15

Both the actual material used and the standard quantity allowed for material is based on the actual output attained.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 147 في هذه المجموعة.

فتح الحزمة

k this deck

16

Variance analysis for fixed production costs is virtually the same as for variable production costs.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 147 في هذه المجموعة.

فتح الحزمة

k this deck

17

The sales price variance is the actual selling price per unit times the difference between budgeted number of units and the actual number of units sold..

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 147 في هذه المجموعة.

فتح الحزمة

k this deck

18

A flexible budget adjusts the static budget to reflect the actual activity level achieved during the period.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 147 في هذه المجموعة.

فتح الحزمة

k this deck

19

In essence,the terms "master budget" and "operating budget" mean the same thing and can be used interchangeably.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 147 في هذه المجموعة.

فتح الحزمة

k this deck

20

A favorable variance is not necessarily good,and an unfavorable variance is not necessarily bad.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 147 في هذه المجموعة.

فتح الحزمة

k this deck

21

An operating budget would not include a:

A) cash budget.

B) sales budget.

C) labor budget.

D) production budget.

A) cash budget.

B) sales budget.

C) labor budget.

D) production budget.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 147 في هذه المجموعة.

فتح الحزمة

k this deck

22

Which of the following statements regarding variances is(are)false?

(A)In general and holding all other things constant,an unfavorable variance decreases operating profits.

(B)A favorable variance is not always good,and an unfavorable variance is not always bad.

A) Only A is false.

B) Only B is false.

C) Both A and B are false.

D) Neither A nor B is false.

(A)In general and holding all other things constant,an unfavorable variance decreases operating profits.

(B)A favorable variance is not always good,and an unfavorable variance is not always bad.

A) Only A is false.

B) Only B is false.

C) Both A and B are false.

D) Neither A nor B is false.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 147 في هذه المجموعة.

فتح الحزمة

k this deck

23

What is the actual sales revenue?

A) $156,000.

B) $169,000.

C) $180,000.

D) $191,000.

A) $156,000.

B) $169,000.

C) $180,000.

D) $191,000.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 147 في هذه المجموعة.

فتح الحزمة

k this deck

24

The Valenti Company uses flexible budgeting for cost control.Valenti produced 10,800 units of product during October,incurring indirect material costs of $13,000.Its master budget for the reflected indirect material costs of $180,000 at a production volume of 144,000 units.What was the flexible budget variance for the indirect material costs in October?

A) $1,100 favorable.

B) $1,100 unfavorable.

C) $2,000 favorable.

D) $500 favorable.

A) $1,100 favorable.

B) $1,100 unfavorable.

C) $2,000 favorable.

D) $500 favorable.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 147 في هذه المجموعة.

فتح الحزمة

k this deck

25

Which of the following statements is(are)true?

(A)A favorable variance is not necessarily good,and an unfavorable variance is not necessarily bad.

(B)The master budget includes operating budgets (e.g. ,production budget)and financial budgets (e.g. ,cash budget).

A) Only A is true.

B) Only B is true.

C) Both A and B are true.

D) Neither A nor B is true.

(A)A favorable variance is not necessarily good,and an unfavorable variance is not necessarily bad.

(B)The master budget includes operating budgets (e.g. ,production budget)and financial budgets (e.g. ,cash budget).

A) Only A is true.

B) Only B is true.

C) Both A and B are true.

D) Neither A nor B is true.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 147 في هذه المجموعة.

فتح الحزمة

k this deck

26

Standards and budgets are the same thing.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 147 في هذه المجموعة.

فتح الحزمة

k this deck

27

Which of the following variances will always be favorable when actual sales exceeds budgeted sales?

A) Variable cost.

B) Fixed cost.

C) Sales activity.

D) Operating profit.

A) Variable cost.

B) Fixed cost.

C) Sales activity.

D) Operating profit.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 147 في هذه المجموعة.

فتح الحزمة

k this deck

28

When a manager is concerned with monitoring total cost,total revenue,and net profit conditioned upon the level of productivity,an accountant should normally recommend: (CPA adapted)

A) Option A

B) Option B

C) Option C

D) Option D

A) Option A

B) Option B

C) Option C

D) Option D

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 147 في هذه المجموعة.

فتح الحزمة

k this deck

29

Based on past experience,Moss Company has developed the following budget formula for estimating its shipping expenses.The company's shipments average 12 lbs.per shipment: Shipping costs = $16,000 + ($0.50 × lbs.shipped).The planned activity and actual activity regarding orders and shipments for the current month are given in the following schedule:

The actual shipping costs for the month amounted to $21,000.The appropriate monthly flexible budget allowance for shipping costs for the purpose of performance evaluation would be: (CMA adapted)

A) $20,680.

B) $20,920.

C) $20,800.

D) $22,150.

The actual shipping costs for the month amounted to $21,000.The appropriate monthly flexible budget allowance for shipping costs for the purpose of performance evaluation would be: (CMA adapted)

A) $20,680.

B) $20,920.

C) $20,800.

D) $22,150.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 147 في هذه المجموعة.

فتح الحزمة

k this deck

30

In general,the terms favorable and unfavorable are used to describe the effect of a variance on:

A) net income.

B) sales revenue.

C) production costs.

D) operating expenses.

A) net income.

B) sales revenue.

C) production costs.

D) operating expenses.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 147 في هذه المجموعة.

فتح الحزمة

k this deck

31

The intercept of the flexible budget-line is total:

A) sales.

B) variable costs.

C) fixed costs.

D) contribution margin.

A) sales.

B) variable costs.

C) fixed costs.

D) contribution margin.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 147 في هذه المجموعة.

فتح الحزمة

k this deck

32

A variance can best be described as:

A) benchmarks common to other firms in the same industry.

B) differences between planned results and actual results.

C) useful for performance evaluations but not making decisions.

D) generally accepted accounting principles when standards are useD.

Variances are internal to a company and are useful for decision making as well as performance evaluation.The statement is a basic explanation of a variance.

A) benchmarks common to other firms in the same industry.

B) differences between planned results and actual results.

C) useful for performance evaluations but not making decisions.

D) generally accepted accounting principles when standards are useD.

Variances are internal to a company and are useful for decision making as well as performance evaluation.The statement is a basic explanation of a variance.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 147 في هذه المجموعة.

فتح الحزمة

k this deck

33

The slope of the flexible budget-line is the:

A) selling price per unit.

B) variable cost per unit.

C) fixed cost per unit.

D) contribution margin per unit.

A) selling price per unit.

B) variable cost per unit.

C) fixed cost per unit.

D) contribution margin per unit.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 147 في هذه المجموعة.

فتح الحزمة

k this deck

34

A standard cost system may be used in: (CPA adapted)

A) job-order costing but not process costing.

B) either job-order costing or process costing.

C) process costing but not job-order costing.

D) neither process costing nor job-order costing.

A) job-order costing but not process costing.

B) either job-order costing or process costing.

C) process costing but not job-order costing.

D) neither process costing nor job-order costing.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 147 في هذه المجموعة.

فتح الحزمة

k this deck

35

When using standard costing,costs are transferred through the production process at their standard costs.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 147 في هذه المجموعة.

فتح الحزمة

k this deck

36

The basic difference between a master budget and a flexible budget is that a:

A) flexible budget considers only variable costs but a master budget considers all costs.

B) flexible budget allows management latitude in meeting goals whereas a master budget is based upon a fixed standard.

C) master budget is for an entire production facility but a flexible budget is applicable to single departments only.

D) master budget is based on one specific level of production and a flexible budget can be prepared for any production level within a relevant range.

A) flexible budget considers only variable costs but a master budget considers all costs.

B) flexible budget allows management latitude in meeting goals whereas a master budget is based upon a fixed standard.

C) master budget is for an entire production facility but a flexible budget is applicable to single departments only.

D) master budget is based on one specific level of production and a flexible budget can be prepared for any production level within a relevant range.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 147 في هذه المجموعة.

فتح الحزمة

k this deck

37

When using a flexible budget,what will happen to variable costs on a per-unit basis as production increases within the relevant range?

A) Decrease.

B) Increase.

C) Remain unchanged.

D) Fixed costs are not considered in flexible budgeting.

A) Decrease.

B) Increase.

C) Remain unchanged.

D) Fixed costs are not considered in flexible budgeting.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 147 في هذه المجموعة.

فتح الحزمة

k this deck

38

The most fundamental variance analysis compares:

A) standard material prices with actual material prices.

B) standard direct labor rates with actual direct labor rates.

C) budgeted sales revenue with actual sales revenue.

D) budgeted operating income with actual operating income.

A) standard material prices with actual material prices.

B) standard direct labor rates with actual direct labor rates.

C) budgeted sales revenue with actual sales revenue.

D) budgeted operating income with actual operating income.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 147 في هذه المجموعة.

فتح الحزمة

k this deck

39

The purpose of the flexible budget is to:

A) allow management some latitude in meeting goals.

B) eliminate cyclical fluctuations in production reports by ignoring variable costs.

C) compare actual and budgeted results at virtually any level of production.

D) reduce the total time in preparing the annual budget.

A) allow management some latitude in meeting goals.

B) eliminate cyclical fluctuations in production reports by ignoring variable costs.

C) compare actual and budgeted results at virtually any level of production.

D) reduce the total time in preparing the annual budget.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 147 في هذه المجموعة.

فتح الحزمة

k this deck

40

Which of the following organizational policies is most likely to result in undesirable managerial behavior? (CMA adapted)

A) Raj Chemicals sponsors television coverage of cricket matches between national teams representing India and Pakistan.The expenses of such media sponsorship are not allocated to its various divisions.

B) Felix Eagle,the chief executive officer of Eagle Rock Brewery,wrote a memorandum to his executives stating,"Operating plans are contracts and they should be met without fail."

C) The budgeting process at Lawrence Manufacturing starts with operating managers providing goals for their respective departments.

D) Gallen Lighting holds quarterly meetings of departmental managers to consider possible changes in the budgeted targets due to changing conditions.

A) Raj Chemicals sponsors television coverage of cricket matches between national teams representing India and Pakistan.The expenses of such media sponsorship are not allocated to its various divisions.

B) Felix Eagle,the chief executive officer of Eagle Rock Brewery,wrote a memorandum to his executives stating,"Operating plans are contracts and they should be met without fail."

C) The budgeting process at Lawrence Manufacturing starts with operating managers providing goals for their respective departments.

D) Gallen Lighting holds quarterly meetings of departmental managers to consider possible changes in the budgeted targets due to changing conditions.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 147 في هذه المجموعة.

فتح الحزمة

k this deck

41

What is the flexible budget contribution margin?

A) $39,000.

B) $45,000.

C) $52,000.

D) $58,000.

A) $39,000.

B) $45,000.

C) $52,000.

D) $58,000.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 147 في هذه المجموعة.

فتح الحزمة

k this deck

42

Which variance will be unfavorable due to employees working more hours than allowed for the actual number of units produced?

A) Price (rate).

B) Efficiency.

C) Sales activity.

D) Production volume.

A) Price (rate).

B) Efficiency.

C) Sales activity.

D) Production volume.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 147 في هذه المجموعة.

فتح الحزمة

k this deck

43

Which of the following is the most probable reason a company would experience an unfavorable labor rate variance and a favorable labor efficiency variance?

A) The mix of workers assigned to the particular job was heavily weighted towards the use of higher paid experienced individuals.

B) The mix of workers assigned to the particular job was heavily weighted towards the use of new relatively low paid unskilled workers.

C) Because of the production schedule,workers from other production areas were assigned to assist this particular process.

D) Defective materials caused more labor to be used in order to produce a standard unit.

A) The mix of workers assigned to the particular job was heavily weighted towards the use of higher paid experienced individuals.

B) The mix of workers assigned to the particular job was heavily weighted towards the use of new relatively low paid unskilled workers.

C) Because of the production schedule,workers from other production areas were assigned to assist this particular process.

D) Defective materials caused more labor to be used in order to produce a standard unit.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 147 في هذه المجموعة.

فتح الحزمة

k this deck

44

In general,the direct labor efficiency variance is the responsibility of the:

A) purchasing agent.

B) company president.

C) production manager.

D) industrial engineering.

A) purchasing agent.

B) company president.

C) production manager.

D) industrial engineering.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 147 في هذه المجموعة.

فتح الحزمة

k this deck

45

Which department is customarily held responsible for an unfavorable materials quantity variance?

A) Quality control.

B) Purchasing.

C) Engineering.

D) Production.

A) Quality control.

B) Purchasing.

C) Engineering.

D) Production.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 147 في هذه المجموعة.

فتح الحزمة

k this deck

46

If the total materials variance for a given operation is favorable,why must this variance be further evaluated as to price and usage?

A) There is no need to further evaluate the total materials variance if it is favorable.

B) Generally accepted accounting principles require that all variances be analyzed in three stages.

C) All variances must appear in the annual report to equity owners for proper disclosure.

D) A further evaluation lets management evaluate the activities of the purchasing and production functions.

A) There is no need to further evaluate the total materials variance if it is favorable.

B) Generally accepted accounting principles require that all variances be analyzed in three stages.

C) All variances must appear in the annual report to equity owners for proper disclosure.

D) A further evaluation lets management evaluate the activities of the purchasing and production functions.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 147 في هذه المجموعة.

فتح الحزمة

k this deck

47

In the general model,an efficiency variance is calculated as:

A) (SP × AQ)- (SP × SQ)

B) (AP × SQ)- (SP × SQ)

C) (AP × AQ)- (SP × SQ)

D) (AP × AQ)- (SP × AQ)

A) (SP × AQ)- (SP × SQ)

B) (AP × SQ)- (SP × SQ)

C) (AP × AQ)- (SP × SQ)

D) (AP × AQ)- (SP × AQ)

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 147 في هذه المجموعة.

فتح الحزمة

k this deck

48

What is the master budget contribution margin?

A) $52,000.

B) $47,500.

C) $45,000.

D) $39,000.

A) $52,000.

B) $47,500.

C) $45,000.

D) $39,000.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 147 في هذه المجموعة.

فتح الحزمة

k this deck

49

When are the following direct materials variances ideally reported?

A) Option A

B) Option B

C) Option C

D) Option D

A) Option A

B) Option B

C) Option C

D) Option D

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 147 في هذه المجموعة.

فتح الحزمة

k this deck

50

The sales price variance is the difference between the actual sales revenues and the:

A) budgeted selling price multiplied by the budgeted number of units sold.

B) budgeted selling price multiplied by the actual number of units sold.

C) actual selling price multiplied by the budgeted number of units sold.

D) actual selling price multiplied by the actual number of units solD.

The sales price variance is derived from the difference between the actual revenue and budgeted selling price multiplied by the actual number of units solD.

A) budgeted selling price multiplied by the budgeted number of units sold.

B) budgeted selling price multiplied by the actual number of units sold.

C) actual selling price multiplied by the budgeted number of units sold.

D) actual selling price multiplied by the actual number of units solD.

The sales price variance is derived from the difference between the actual revenue and budgeted selling price multiplied by the actual number of units solD.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 147 في هذه المجموعة.

فتح الحزمة

k this deck

51

What is the activity variance for the variable manufacturing costs?

A) $4,000.

B) $14,000.

C) $24,000.

D) $34,000.

A) $4,000.

B) $14,000.

C) $24,000.

D) $34,000.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 147 في هذه المجموعة.

فتح الحزمة

k this deck

52

Which of the following is the name of a form providing standard quantities of inputs used to produce a unit of output and the standard prices for the inputs?

A) A static budget.

B) A standard cost sheet.

C) A variance account.

D) A master budget.

A) A static budget.

B) A standard cost sheet.

C) A variance account.

D) A master budget.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 147 في هذه المجموعة.

فتح الحزمة

k this deck

53

What is the master budget sales revenue?

A) $124,000.

B) $148,000.

C) $156,000.

D) $180,000.

A) $124,000.

B) $148,000.

C) $156,000.

D) $180,000.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 147 في هذه المجموعة.

فتح الحزمة

k this deck

54

What is the sales revenue in the flexible budget?

A) $139,000.

B) $156,000.

C) $169,000.

D) $180,000.

A) $139,000.

B) $156,000.

C) $169,000.

D) $180,000.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 147 في هذه المجموعة.

فتح الحزمة

k this deck

55

Which of the following statements is not true regarding the fixed production cost variance?

A) The fixed production cost variance is the difference between actual and budgeted costs.

B) With respect to this variance,fixed costs are affected by activity levels within a relevant range.

C) The flexible budget's fixed costs equal the master budget's fixed costs.

D) Fixed costs are treated as period costs for purposes of this variance.

A) The fixed production cost variance is the difference between actual and budgeted costs.

B) With respect to this variance,fixed costs are affected by activity levels within a relevant range.

C) The flexible budget's fixed costs equal the master budget's fixed costs.

D) Fixed costs are treated as period costs for purposes of this variance.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 147 في هذه المجموعة.

فتح الحزمة

k this deck

56

In the general model,a price variance is calculated as:

A) (AP × AQ)- (AP × SQ)

B) (AP × SQ)- (SP × SQ)

C) (AP × AQ)- (SP × AQ)

D) (AP × AQ)- (SP × SQ)

A) (AP × AQ)- (AP × SQ)

B) (AP × SQ)- (SP × SQ)

C) (AP × AQ)- (SP × AQ)

D) (AP × AQ)- (SP × SQ)

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 147 في هذه المجموعة.

فتح الحزمة

k this deck

57

In analyzing company operations,the controller of the Carson Corporation found a $250,000 favorable flexible budget revenue variance.The variance was calculated by comparing the actual results with the flexible budget.This variance can be wholly explained by: (CMA adapted)

A) the total flexible budget variance.

B) the total static budget variance.

C) changes in unit selling prices.

D) changes in the number of units solD.

Since the flexible budget is based on actual output,the variation could only come from the selling price.

A) the total flexible budget variance.

B) the total static budget variance.

C) changes in unit selling prices.

D) changes in the number of units solD.

Since the flexible budget is based on actual output,the variation could only come from the selling price.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 147 في هذه المجموعة.

فتح الحزمة

k this deck

58

The difference between operating profits in the master budget and operating profits in the flexible budget is called:

A) sales activity variance.

B) flexible budget variance.

C) production volume variance.

D) total operating profit variance.

A) sales activity variance.

B) flexible budget variance.

C) production volume variance.

D) total operating profit variance.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 147 في هذه المجموعة.

فتح الحزمة

k this deck

59

Which of the following statements is(are)true regarding the sales activity variance? (A)The sales activity variance is the actual selling price per unit times the difference between the budgeted units and actual units.(B)If the sales activity variance for sales revenue is unfavorable,then the contribution margin sales activity variance will be unfavorable.

A) Only A is true.

B) Only B is true.

C) Neither A and B is true.

D) Both A and B are true.

A) Only A is true.

B) Only B is true.

C) Neither A and B is true.

D) Both A and B are true.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 147 في هذه المجموعة.

فتح الحزمة

k this deck

60

Which of the following direct labor variances uses the standard hours allowed for the actual number of units produced?

A) Option A

B) Option B

C) Option C

D) Option D

A) Option A

B) Option B

C) Option C

D) Option D

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 147 في هذه المجموعة.

فتح الحزمة

k this deck

61

The following information summarizes the standard cost for producing one metal tennis racket frame at Spaulding Industries.In addition,the variances for one month's production are given.Assume that all inventory accounts have zero balances at the beginning of the month. What was the actual quantity of materials used during the month?

A) 2,156.

B) 2,100.

C) 2,225.

D) 1,975.

What was the actual quantity of materials used during the month?A) 2,156.

B) 2,100.

C) 2,225.

D) 1,975.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 147 في هذه المجموعة.

فتح الحزمة

k this deck

62

TaskMaster Enterprises employs a standard cost system in which direct materials inventory is carried at standard cost.TaskMaster has established the following standards for the prime costs of one unit of product. During November,TaskMaster purchased 160,000 pounds of direct materials at a total cost of $304,000.The total factory wages for November were $42,000,90% of which were for direct labor.TaskMaster manufactured 19,000 units of product during November using 142,500 pounds of direct materials and 5,000 direct labor hours.What is the direct materials price variance for November?

A) $14,250.

B) $14,400.

C) $16,000.

D) $17,100.

A) $14,250.

B) $14,400.

C) $16,000.

D) $17,100.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 147 في هذه المجموعة.

فتح الحزمة

k this deck

63

Data on Gantry Company's direct-labor costs are given below:

What was Gantry's standard direct-labor rate?

A) $3.54.

B) $3.80.

C) $4.00.

D) $5.80.

What was Gantry's standard direct-labor rate?

A) $3.54.

B) $3.80.

C) $4.00.

D) $5.80.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 147 في هذه المجموعة.

فتح الحزمة

k this deck

64

Batson Company produces Trivets.Based on its master budget,the company should produce 1,000 Trivets each month,working 2,500 direct labor hours.During May,only 900 Trivets were produced.The company worked 2,400 direct labor hours.The standard hours allowed for May production would be:

A) 2,500 hours.

B) 2,400 hours.

C) 2,250 hours.

D) 1,800 hours.

A) 2,500 hours.

B) 2,400 hours.

C) 2,250 hours.

D) 1,800 hours.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 147 في هذه المجموعة.

فتح الحزمة

k this deck

65

The following data pertains to the direct materials cost for the month of October:

What is the direct materials efficiency (quantity)variance?

A) $950 favorable.

B) $950 unfavorable.

C) $1,000 favorable.

D) $1,000 unfavorable.

What is the direct materials efficiency (quantity)variance?

A) $950 favorable.

B) $950 unfavorable.

C) $1,000 favorable.

D) $1,000 unfavorable.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 147 في هذه المجموعة.

فتح الحزمة

k this deck

66

TaskMaster Enterprises employs a standard cost system in which direct materials inventory is carried at standard cost.TaskMaster has established the following standards for the prime costs of one unit of product. During November,TaskMaster purchased 160,000 pounds of direct materials at a total cost of $304,000.The total factory wages for November were $42,000,90% of which were for direct labor.TaskMaster manufactured 19,000 units of product during November using 142,500 pounds of direct materials and 5,000 direct labor hours.What is the direct labor efficiency variance for November?

A) $1,800.

B) $1,900.

C) $2,000.

D) $2,090.

A) $1,800.

B) $1,900.

C) $2,000.

D) $2,090.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 147 في هذه المجموعة.

فتح الحزمة

k this deck

67

Data on Gantry Company's direct-labor costs are given below:

What was Gantry's actual direct-labor rate?

A) $3.60.

B) $3.80.

C) $4.00.

D) $5.80.

What was Gantry's actual direct-labor rate?

A) $3.60.

B) $3.80.

C) $4.00.

D) $5.80.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 147 في هذه المجموعة.

فتح الحزمة

k this deck

68

The following information summarizes the standard cost for producing one metal tennis racket frame at Spaulding Industries.In addition,the variances for one month's production are given.Assume that all inventory accounts have zero balances at the beginning of the month. What were the actual direct labor hours worked during the month?

A) 5,000.

B) 4,800.

C) 4,200.

D) 4,000.

A) 5,000.

B) 4,800.

C) 4,200.

D) 4,000.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 147 في هذه المجموعة.

فتح الحزمة

k this deck

69

TaskMaster Enterprises employs a standard cost system in which direct materials inventory is carried at standard cost.TaskMaster has established the following standards for the prime costs of one unit of product. During November,TaskMaster purchased 160,000 pounds of direct materials at a total cost of $304,000.The total factory wages for November were $42,000,90% of which were for direct labor.TaskMaster manufactured 19,000 units of product during November using 142,500 pounds of direct materials and 5,000 direct labor hours.What is the direct labor price (rate)variance for November?

A) $1,800.

B) $1,900.

C) $2,000.

D) $2,200.

A) $1,800.

B) $1,900.

C) $2,000.

D) $2,200.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 147 في هذه المجموعة.

فتح الحزمة

k this deck

70

Variable manufacturing overhead is applied to products on the basis of standard direct labor-hours.If the direct labor efficiency variance is unfavorable,the variable overhead efficiency variance will be: (CMA adapted)

A) favorable.

B) unfavorable.

C) either favorable or unfavorable.

D) zero.

A) favorable.

B) unfavorable.

C) either favorable or unfavorable.

D) zero.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 147 في هذه المجموعة.

فتح الحزمة

k this deck

71

The Fellowes Company has developed standards for labor.During June,75 units were scheduled and 100 were produced.Data related to labor are:

What is the labor rate variance for June?

A) $30 unfavorable.

B) $31 favorable.

C) $31 unfavorable.

D) $30 favorable.

What is the labor rate variance for June?

A) $30 unfavorable.

B) $31 favorable.

C) $31 unfavorable.

D) $30 favorable.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 147 في هذه المجموعة.

فتح الحزمة

k this deck

72

Miller Company planned to produce 3,000 units of its single product,Tallium,during November.The standards for one unit of Tallium specify six pounds of materials at $0.30 per pound.Actual production in November was 3,100 units of Tallium.There was a favorable materials price variance of $380 and an unfavorable materials quantity variance of $120.Based on these variances,one could conclude that: (CMA adapted)

A) more materials were purchased than were used.

B) more materials were used than were purchased.

C) the actual cost per pound for materials was less than the standard cost per pound.

D) the actual usage of materials was less than the standard alloweD.

See calculation below.

A) more materials were purchased than were used.

B) more materials were used than were purchased.

C) the actual cost per pound for materials was less than the standard cost per pound.

D) the actual usage of materials was less than the standard alloweD.

See calculation below.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 147 في هذه المجموعة.

فتح الحزمة

k this deck

73

An unfavorable direct labor efficiency variance could be caused by: (CMA adapted)

A) an unfavorable materials quantity variance.

B) an unfavorable variable overhead rate variance.

C) a favorable materials quantity variance.

D) a favorable variable overhead rate variance.

A) an unfavorable materials quantity variance.

B) an unfavorable variable overhead rate variance.

C) a favorable materials quantity variance.

D) a favorable variable overhead rate variance.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 147 في هذه المجموعة.

فتح الحزمة

k this deck

74

The following information summarizes the standard cost for producing one metal tennis racket frame at Spaulding Industries.In addition,the variances for one month's production are given.Assume that all inventory accounts have zero balances at the beginning of the month. What was the actual price paid for the direct material during the month,assuming all materials purchased were put into production?

A) $4.34.

B) $4.22.

C) $4.11.

D) $4.00.

What was the actual price paid for the direct material during the month,assuming all materials purchased were put into production? A) $4.34.

B) $4.22.

C) $4.11.

D) $4.00.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 147 في هذه المجموعة.

فتح الحزمة

k this deck

75

The variable overhead price variance is due to:

A) price items only.

B) efficiency items only.

C) both price and efficiency items.

D) neither price or efficiency items.

A) price items only.

B) efficiency items only.

C) both price and efficiency items.

D) neither price or efficiency items.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 147 في هذه المجموعة.

فتح الحزمة

k this deck

76

Information on Kimble Company's direct labor costs for the month of January is as follows:

What is Kimble's direct labor price (rate)variance?

A) $17,250.

B) $20,700.

C) $18,750.

D) $21,000.

What is Kimble's direct labor price (rate)variance?

A) $17,250.

B) $20,700.

C) $18,750.

D) $21,000.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 147 في هذه المجموعة.

فتح الحزمة

k this deck

77

When computing standard cost variances,the difference between actual and standard price multiplied by actual quantity yields a(n): (CMA adapted)

A) combined price and quantity variance.

B) efficiency variance.

C) price variance.

D) quantity variance.

A) combined price and quantity variance.

B) efficiency variance.

C) price variance.

D) quantity variance.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 147 في هذه المجموعة.

فتح الحزمة

k this deck

78

TaskMaster Enterprises employs a standard cost system in which direct materials inventory is carried at standard cost.TaskMaster has established the following standards for the prime costs of one unit of product. During November,TaskMaster purchased 160,000 pounds of direct materials at a total cost of $304,000.The total factory wages for November were $42,000,90% of which were for direct labor.TaskMaster manufactured 19,000 units of product during November using 142,500 pounds of direct materials and 5,000 direct labor hours.What is the direct materials efficiency (quantity)variance for November?

A) $14,250.

B) $14,400.

C) $16,000.

D) $17,100.

A) $14,250.

B) $14,400.

C) $16,000.

D) $17,100.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 147 في هذه المجموعة.

فتح الحزمة

k this deck

79

Shawn Inc.planned to produce 3,000 units of its single product,Megatron,during November.The standard specifications for one unit of Megatron include six pounds of material at $0.30 per pound.Actual production in November was 3,100 units of Megatron.The accountant computed a favorable materials purchase price variance of $380 and an unfavorable materials quantity variance of $120.Based on these variances,one could conclude that: (CMA adapted)

A) more materials were purchased than were used.

B) more materials were used than were purchased.

C) the actual cost of materials was less than the standard cost.

D) the actual usage of materials was less than the standard alloweD.

See calculation below.

A) more materials were purchased than were used.

B) more materials were used than were purchased.

C) the actual cost of materials was less than the standard cost.

D) the actual usage of materials was less than the standard alloweD.

See calculation below.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 147 في هذه المجموعة.

فتح الحزمة

k this deck

80

If overhead is applied to production using direct labor hours and the direct labor efficiency variance is favorable,then the variable overhead efficiency variance is:

A) favorable.

B) unfavorable.

C) either favorable or unfavorable.

D) neither favorable nor unfavorable.

A) favorable.

B) unfavorable.

C) either favorable or unfavorable.

D) neither favorable nor unfavorable.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 147 في هذه المجموعة.

فتح الحزمة

k this deck

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 147 في هذه المجموعة.