Deck 17: Additional Topics in Variance Analysis

ملء الشاشة (f)

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

The exhibit below reflects a summary of performance for a single item of a retail store's inventory for the month ended April 30: (CIA adapted) T

he sales volume variance is:

he sales volume variance is:

A) $20,000 favorable.

B) $20,000 unfavorable.

C) $11,000 favorable.

D) $12,000 unfavorable.

he sales volume variance is:A) $20,000 favorable.

B) $20,000 unfavorable.

C) $11,000 favorable.

D) $12,000 unfavorable.

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

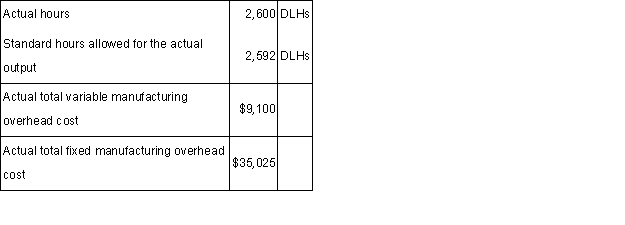

A manufacturer of industrial equipment has a standard costing system based on standard direct labor-hours (DLHs)as the measure of activity.Data from the company's flexible budget for manufacturing overhead are given below:

The following data pertain to operations for the most recent period:

How much overhead was applied to products during the period to the nearest dollar?

How much overhead was applied to products during the period to the nearest dollar?

A) $44,712.

B) $44,125.

C) $43,125.

D) $44,850.

The following data pertain to operations for the most recent period:

How much overhead was applied to products during the period to the nearest dollar?A) $44,712.

B) $44,125.

C) $43,125.

D) $44,850.

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

فتح الحزمة

قم بالتسجيل لفتح البطاقات في هذه المجموعة!

Unlock Deck

Unlock Deck

1/134

العب

ملء الشاشة (f)

Deck 17: Additional Topics in Variance Analysis

1

The market share variance is more controllable by the marketing department than the industry volume variance.

True

2

The production cost yield variance is conceptually the same as the sales quantity variance.

True

3

The direct material price variance is based on the quantity of materials purchased when the quantity purchased is different from the quantity used.

True

4

The only variances that should be investigated are those for which the expected benefits of correction exceed the costs of investigating and correcting.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 134 في هذه المجموعة.

فتح الحزمة

k this deck

5

Labor variances are more important than material variances in service organizations.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 134 في هذه المجموعة.

فتح الحزمة

k this deck

6

The production mix variance measures the impact of substituting one material for another material during the production process.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 134 في هذه المجموعة.

فتح الحزمة

k this deck

7

The direct labor yield variance is unfavorable when the total hours worked during a period are less than the total standard hours allowed for the actual number of units produced.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 134 في هذه المجموعة.

فتح الحزمة

k this deck

8

If variances are not prorated at the end of the accounting period,they are closed to the Cost of Goods Sold.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 134 في هذه المجموعة.

فتح الحزمة

k this deck

9

The industry volume variance is the portion of the sales activity variance due to a change in the company's proportion of sales in the markets in which they operate.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 134 في هذه المجموعة.

فتح الحزمة

k this deck

10

If the number of units produced exceeds the number of units sold,the full-absorption operating profit will be lower than variable costing operating profit.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 134 في هذه المجموعة.

فتح الحزمة

k this deck

11

If a company sells two products,it is possible for both products to have a favorable sales mix variance.another.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 134 في هذه المجموعة.

فتح الحزمة

k this deck

12

Two important characteristics to consider when deciding how many variances to review are how large the variance is and the extent to which the variance can be managed.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 134 في هذه المجموعة.

فتح الحزمة

k this deck

13

Professional accounting firms could not compute a labor mix and labor yield variance for their auditors because labor in accounting is not substitutable.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 134 في هذه المجموعة.

فتح الحزمة

k this deck

14

The basic variance analysis framework used for manufacturing companies can also be used in service organizations.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 134 في هذه المجموعة.

فتح الحزمة

k this deck

15

Output is usually defined as sales units in merchandising,but service organizations use measures of activity units,like patient days.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 134 في هذه المجموعة.

فتح الحزمة

k this deck

16

An increase in an industry's volume and a decrease in a company's market share implies that the company's sales price variance is unfavorable.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 134 في هذه المجموعة.

فتح الحزمة

k this deck

17

The general approach in variance analysis is to separate the variance into components based on a budgeting formula.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 134 في هذه المجموعة.

فتح الحزمة

k this deck

18

The variable production cost variances are computed using the units produced instead of the units sold.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 134 في هذه المجموعة.

فتح الحزمة

k this deck

19

If a company sells two products,it is possible for both products to have an unfavorable sales quantity variance.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 134 في هذه المجموعة.

فتح الحزمة

k this deck

20

The sales quantity variance is the same as the sales activity variance on a flexible budget performance report.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 134 في هذه المجموعة.

فتح الحزمة

k this deck

21

The Fantasy Gifts Company,a maker of Holiday novelties,needs your help immediately.The company's accountant resigned without leaving adequate records or explanations for what she did.In reviewing the records,you find the following information for May:

You find a copy of the budget which shows that materials were budgeted at $0.60/unit.You know that the materials price variance is recorded at the time of purchase and you find some handwritten notes among the accountant's work papers,which indicate the following:

What was the total standard cost of direct materials allowed during May?

A) $8,260.

B) $8,400.

C) $9,440.

D) $9,600.

You find a copy of the budget which shows that materials were budgeted at $0.60/unit.You know that the materials price variance is recorded at the time of purchase and you find some handwritten notes among the accountant's work papers,which indicate the following:

What was the total standard cost of direct materials allowed during May?

A) $8,260.

B) $8,400.

C) $9,440.

D) $9,600.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 134 في هذه المجموعة.

فتح الحزمة

k this deck

22

Which of the following statements is(are)false?

(A)All variances should be prorated to inventories and cost of goods sold at the end of the accounting period.

(B)If the number of units produced exceeds the number of units sold,the full-absorption operating profit will be lower than variable costing operating profit.

A) Only A is false.

B) Only B is false.

C) Both A and B are false.

D) Neither A nor B is false.

(A)All variances should be prorated to inventories and cost of goods sold at the end of the accounting period.

(B)If the number of units produced exceeds the number of units sold,the full-absorption operating profit will be lower than variable costing operating profit.

A) Only A is false.

B) Only B is false.

C) Both A and B are false.

D) Neither A nor B is false.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 134 في هذه المجموعة.

فتح الحزمة

k this deck

23

In a standard cost system,overhead is applied to production on a basis of:

A) the denominator hours chosen for the period.

B) the budgeted hours for the normal production level of activity.

C) the actual hours required to complete the output of the period.

D) the standard hours allowed to complete the output of the perioD.

Standard costing uses standard hours,not actual or budgeteD.

A) the denominator hours chosen for the period.

B) the budgeted hours for the normal production level of activity.

C) the actual hours required to complete the output of the period.

D) the standard hours allowed to complete the output of the perioD.

Standard costing uses standard hours,not actual or budgeteD.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 134 في هذه المجموعة.

فتح الحزمة

k this deck

24

Ingredient A12H is a raw material used to make Calvin Corporation's major product.The standard cost of Ingredient A12H is $23.00 per ounce and the standard quantity is 3.8 ounces per unit of output.Data concerning the compound for October appear below:

The raw material was purchased on account.The Materials Quantity Variance for October would be recorded as a:

A) credit of $3,680.

B) debit of $4,140.

C) credit of $4,140.

D) debit of $3,680.

The raw material was purchased on account.The Materials Quantity Variance for October would be recorded as a:

A) credit of $3,680.

B) debit of $4,140.

C) credit of $4,140.

D) debit of $3,680.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 134 في هذه المجموعة.

فتح الحزمة

k this deck

25

Which of the following sales variances is further analyzed into the market size and industry volume variances?

A) Quantity.

B) Efficiency.

C) Mix.

D) Activity.

A) Quantity.

B) Efficiency.

C) Mix.

D) Activity.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 134 في هذه المجموعة.

فتح الحزمة

k this deck

26

Ingredient A12H is a raw material used to make Calvin Corporation's major product.The standard cost of Ingredient A12H is $23.00 per ounce and the standard quantity is 3.8 ounces per unit of output.Data concerning the compound for October appear below:

The raw material was purchased on account.The Materials Price Variance for October would be recorded as a:

A) debit of $230.

B) credit of $212.

C) debit of $212.

D) credit of $230.

The raw material was purchased on account.The Materials Price Variance for October would be recorded as a:

A) debit of $230.

B) credit of $212.

C) debit of $212.

D) credit of $230.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 134 في هذه المجموعة.

فتح الحزمة

k this deck

27

Ingredient B4376 is used to make Razor Corporation's major product.The standard cost of Ingredient B4376 is $24.50 per ounce and the standard quantity is 6.1 ounces per unit of output.In the most recent month,5,030 ounces of the compound were used to make 700 units of the output.When recording the use of materials in production,Raw Materials would be:

A) credited for $123,235.

B) debited for $123,235.

C) debited for $104,615.

D) credited for $104,615.

A) credited for $123,235.

B) debited for $123,235.

C) debited for $104,615.

D) credited for $104,615.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 134 في هذه المجموعة.

فتح الحزمة

k this deck

28

Some variances are the result of accounting errors and omissions,including timing differences.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 134 في هذه المجموعة.

فتح الحزمة

k this deck

29

When the actual amount of a raw material used in production is greater than the standard amount allowed for the actual output,the journal entry would include:

A) debit to Raw Materials;credit to Materials Quantity Variance.

B) debit to Work-In-Process;credit to Materials Quantity Variance.

C) debit to Raw Materials;debit to Materials Quantity Variance.

D) debit to Work-In-Process;debit to Materials Quantity Variance.

A) debit to Raw Materials;credit to Materials Quantity Variance.

B) debit to Work-In-Process;credit to Materials Quantity Variance.

C) debit to Raw Materials;debit to Materials Quantity Variance.

D) debit to Work-In-Process;debit to Materials Quantity Variance.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 134 في هذه المجموعة.

فتح الحزمة

k this deck

30

Which of the following statements is(are)true? (A)If variances are prorated at the end of the accounting period,an unfavorable direct materials price variance will,when prorated,increase the value of the Finished Goods Inventory.

(B)Insignificant variances are not generally prorated at the end of the accounting period and are closed to the Cost of Goods Sold.

A) Only A is true.

B) Only B is true.

C) Both A and B are true.

D) Neither A nor B is true.

(B)Insignificant variances are not generally prorated at the end of the accounting period and are closed to the Cost of Goods Sold.

A) Only A is true.

B) Only B is true.

C) Both A and B are true.

D) Neither A nor B is true.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 134 في هذه المجموعة.

فتح الحزمة

k this deck

31

Some variances are the result of standards that are inaccurate or do not reflect the current production process.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 134 في هذه المجموعة.

فتح الحزمة

k this deck

32

Barium Corporation has provided the following data concerning its most important raw material,Compound XYY2:

When recording the use of materials in production,Raw Materials would be:

A) debited for $55,930.

B) debited for $54,264.

C) credited for $55,930.

D) credited for $54,264.

When recording the use of materials in production,Raw Materials would be:

A) debited for $55,930.

B) debited for $54,264.

C) credited for $55,930.

D) credited for $54,264.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 134 في هذه المجموعة.

فتح الحزمة

k this deck

33

Standard costs should be based on:

A) perfect performance.

B) an average of past costs.

C) most likely level of performance.

D) reasonably attainable levels of efficiency.

A) perfect performance.

B) an average of past costs.

C) most likely level of performance.

D) reasonably attainable levels of efficiency.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 134 في هذه المجموعة.

فتح الحزمة

k this deck

34

If raw materials are carried in the Direct Materials Inventory at standard cost,then it is reasonable to assume that the:

A) price variance is recognized when materials are purchased.

B) price variance is recognized when materials are placed into production.

C) company does not follow generally accepted accounting principles.

D) efficiency variance is recognized when the materials are purchaseD.

To be carried at standard,price variations need to be removeD.

Standard cost for materials inventory means standard price × actual quantities in the inventory.

A) price variance is recognized when materials are purchased.

B) price variance is recognized when materials are placed into production.

C) company does not follow generally accepted accounting principles.

D) efficiency variance is recognized when the materials are purchaseD.

To be carried at standard,price variations need to be removeD.

Standard cost for materials inventory means standard price × actual quantities in the inventory.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 134 في هذه المجموعة.

فتح الحزمة

k this deck

35

Which of the following statements is(are)true?

(A)The market share variance is more controllable by the marketing department than the industry volume variance.

(B)The industry volume variance is the portion of the sales activity variance due to a change in the company's proportion of sales in the markets in which they operate.

A) Only A is true.

B) Only B is true.

C) Both A and B are true.

D) Neither A nor B is true.

(A)The market share variance is more controllable by the marketing department than the industry volume variance.

(B)The industry volume variance is the portion of the sales activity variance due to a change in the company's proportion of sales in the markets in which they operate.

A) Only A is true.

B) Only B is true.

C) Both A and B are true.

D) Neither A nor B is true.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 134 في هذه المجموعة.

فتح الحزمة

k this deck

36

Ingredient A12H is a raw material used to make Calvin Corporation's major product.The standard cost of Ingredient A12H is $23.00 per ounce and the standard quantity is 3.8 ounces per unit of output.Data concerning the compound for October appear below:

The raw material was purchased on account.The debit to the Raw Materials account for October would total:

A) $52,900.

B) $52,440.

C) $48,760.

D) $53,130.

The raw material was purchased on account.The debit to the Raw Materials account for October would total:

A) $52,900.

B) $52,440.

C) $48,760.

D) $53,130.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 134 في هذه المجموعة.

فتح الحزمة

k this deck

37

Ingredient A12H is a raw material used to make Calvin Corporation's major product.The standard cost of Ingredient A12H is $23.00 per ounce and the standard quantity is 3.8 ounces per unit of output.Data concerning the compound for October appear below:

The raw material was purchased on account.The credit to the Raw Materials account for October would total:

A) $52,440.

B) $48,760.

C) $52,900.

D) $53,130.

The raw material was purchased on account.The credit to the Raw Materials account for October would total:

A) $52,440.

B) $48,760.

C) $52,900.

D) $53,130.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 134 في هذه المجموعة.

فتح الحزمة

k this deck

38

The Fantasy Gifts Company,a maker of Holiday novelties,needs your help immediately.The company's accountant resigned without leaving adequate records or explanations for what she did.In reviewing the records,you find the following information for May:

You find a copy of the budget which shows that materials were budgeted at $0.60/unit.You know that the materials price variance is recorded at the time of purchase and you find some handwritten notes among the accountant's work papers,which indicate the following:

What was the total standard cost of direct materials purchased during May?

A) $9,150.

B) $11,800.

C) $12,000.

D) $12,200.

You find a copy of the budget which shows that materials were budgeted at $0.60/unit.You know that the materials price variance is recorded at the time of purchase and you find some handwritten notes among the accountant's work papers,which indicate the following:

What was the total standard cost of direct materials purchased during May?

A) $9,150.

B) $11,800.

C) $12,000.

D) $12,200.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 134 في هذه المجموعة.

فتح الحزمة

k this deck

39

One feature of a standard cost system is that it:

A) makes the record keeping process more complex and difficult.

B) never requires updating if standard costs have been carefully determined.

C) reduces the amount of information available to a manager.

D) simplifies the record keeping process by allowing amounts to be carried at standard cost rather than actual cost in the accounting records.

A) makes the record keeping process more complex and difficult.

B) never requires updating if standard costs have been carefully determined.

C) reduces the amount of information available to a manager.

D) simplifies the record keeping process by allowing amounts to be carried at standard cost rather than actual cost in the accounting records.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 134 في هذه المجموعة.

فتح الحزمة

k this deck

40

The Fantasy Gifts Company,a maker of Holiday novelties,needs your help immediately.The company's accountant resigned without leaving adequate records or explanations for what she did.In reviewing the records,you find the following information for May:

You find a copy of the budget which shows that materials were budgeted at $0.60/unit.You know that the materials price variance is recorded at the time of purchase and you find some handwritten notes among the accountant's work papers,which indicate the following:

What was the total actual cost of the direct materials purchased during May?

A) $9,000.

B) $11,800.

C) $12,000.

D) $12,200.

You find a copy of the budget which shows that materials were budgeted at $0.60/unit.You know that the materials price variance is recorded at the time of purchase and you find some handwritten notes among the accountant's work papers,which indicate the following:

What was the total actual cost of the direct materials purchased during May?

A) $9,000.

B) $11,800.

C) $12,000.

D) $12,200.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 134 في هذه المجموعة.

فتح الحزمة

k this deck

41

A machine distributor sells two models,basic and deluxe.The following information relates to its master budget.Actual sales were 7,000 basic models and 2,800 deluxe models.The actual sales prices were the same as the budgeted sales prices for both models. What is the sales activity variance for the basic model?

A) $1,280,000.

B) $1,600,000.

C) $11,200,000.

D) $12,800,000.

A) $1,280,000.

B) $1,600,000.

C) $11,200,000.

D) $12,800,000.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 134 في هذه المجموعة.

فتح الحزمة

k this deck

42

Actual and budgeted information about the sales of a product are presented below for June: (CIA adapted)

The sales price variance for June was:

A) $8,000 favorable.

B) $8,000 unfavorable.

C) $10,000 unfavorable.

D) $10,500 unfavorable.

The sales price variance for June was:

A) $8,000 favorable.

B) $8,000 unfavorable.

C) $10,000 unfavorable.

D) $10,500 unfavorable.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 134 في هذه المجموعة.

فتح الحزمة

k this deck

43

A machine distributor sells two models,basic and deluxe.The following information relates to its master budget.Actual sales were 7,000 basic models and 2,800 deluxe models.The actual sales prices were the same as the budgeted sales prices for both models. What is the sales mix variance for the basic model?

A) $256,000.

B) $1,344,000.

C) $1,600,000.

D) $2,520,000.

A) $256,000.

B) $1,344,000.

C) $1,600,000.

D) $2,520,000.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 134 في هذه المجموعة.

فتح الحزمة

k this deck

44

The budget for a given cost during a given period was $80,000.The actual cost for the period was $72,000.Considering these facts,the plant manager has done a better-than-expected job in controlling the cost if: (CPA adapted)

A) the cost is variable and actual production was 90% of budgeted production.

B) the cost is variable and actual production equals budgeted production.

C) the cost is variable and actual production was 80% of budgeted production.

D) the cost is a discretionary fixed cost and actual production equals budgeted production.

A) the cost is variable and actual production was 90% of budgeted production.

B) the cost is variable and actual production equals budgeted production.

C) the cost is variable and actual production was 80% of budgeted production.

D) the cost is a discretionary fixed cost and actual production equals budgeted production.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 134 في هذه المجموعة.

فتح الحزمة

k this deck

45

The sales activity variance is equal to the sum of the market share variance and the:

A) selling price variance.

B) industry volume variance.

C) sales quantity variance.

D) sales mix variance.

A) selling price variance.

B) industry volume variance.

C) sales quantity variance.

D) sales mix variance.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 134 في هذه المجموعة.

فتح الحزمة

k this deck

46

The exhibit below reflects a summary of performance for a single item of a retail store's inventory for the month ended April 30: (CIA adapted) T

he sales volume variance is:

A) $20,000 favorable.

B) $20,000 unfavorable.

C) $11,000 favorable.

D) $12,000 unfavorable.

he sales volume variance is:A) $20,000 favorable.

B) $20,000 unfavorable.

C) $11,000 favorable.

D) $12,000 unfavorable.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 134 في هذه المجموعة.

فتح الحزمة

k this deck

47

Using the abbreviations listed below,what is the formula for the industry volume variance? AMS = actual market share

BMS = budgeted market share

BCM = budgeted contribution margin per unit

ACM = actual contribution margin per unit

ATM = actual total market

BTM = budgeted total market

A) (ATM - BTM)(BMS)(ACM)

B) (ATM - BTM)(BMS)(BCM)

C) (AMS - BMS)(ATM)(ACM)

D) (AMS - BMS)(ATM)(BCM)

BMS = budgeted market share

BCM = budgeted contribution margin per unit

ACM = actual contribution margin per unit

ATM = actual total market

BTM = budgeted total market

A) (ATM - BTM)(BMS)(ACM)

B) (ATM - BTM)(BMS)(BCM)

C) (AMS - BMS)(ATM)(ACM)

D) (AMS - BMS)(ATM)(BCM)

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 134 في هذه المجموعة.

فتح الحزمة

k this deck

48

The Morton Company gathered the following information for the year. What is the total sales mix variance?

A) $705,600.

B) $403,200.

C) $302,400.

D) $100,800.

A) $705,600.

B) $403,200.

C) $302,400.

D) $100,800.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 134 في هذه المجموعة.

فتح الحزمة

k this deck

49

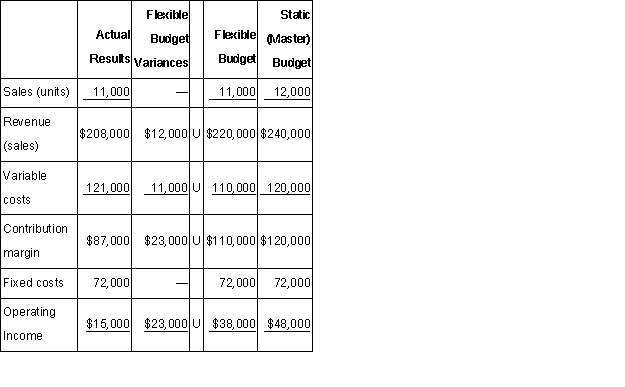

Danner Fashions sells a line of women's dresses.Danner's performance report for November is shown below: (CMA adapted) The company uses a flexible budget to analyze its performance and to measure the effect on operating income of the various factors affecting the difference between budgeted and actual operating income.

The effect of the sales quantity variance on the contribution margin for November is:

A) $30,000 unfavorable.

B) $18,000 unfavorable.

C) $20,000 unfavorable.

D) $15,000 unfavorable.

The effect of the sales quantity variance on the contribution margin for November is:

A) $30,000 unfavorable.

B) $18,000 unfavorable.

C) $20,000 unfavorable.

D) $15,000 unfavorable.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 134 في هذه المجموعة.

فتح الحزمة

k this deck

50

Using the abbreviations listed below,what is the market share variance? AMS = actual market share

BMS = budgeted market share

BCM = budgeted contribution margin per unit

ACM = actual contribution margin per unit

ATM = actual total market

BTM = budgeted total market

A) (ATM - BTM)(BMS)(ACM)

B) (ATM - BTM)(BMS)(BCM)

C) (AMS - BMS)(ATM)(ACM)

D) (AMS - BMS)(ATM)(BCM)

BMS = budgeted market share

BCM = budgeted contribution margin per unit

ACM = actual contribution margin per unit

ATM = actual total market

BTM = budgeted total market

A) (ATM - BTM)(BMS)(ACM)

B) (ATM - BTM)(BMS)(BCM)

C) (AMS - BMS)(ATM)(ACM)

D) (AMS - BMS)(ATM)(BCM)

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 134 في هذه المجموعة.

فتح الحزمة

k this deck

51

A machine distributor sells two models,basic and deluxe.The following information relates to its master budget.Actual sales were 7,000 basic models and 2,800 deluxe models.The actual sales prices were the same as the budgeted sales prices for both models. What is the sales quantity variance for the basic model?

A) $120,000.

B) $256,000.

C) $1,344,000.

D) $1,600,000.

A) $120,000.

B) $256,000.

C) $1,344,000.

D) $1,600,000.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 134 في هذه المجموعة.

فتح الحزمة

k this deck

52

Which of the following income statement items is analyzed using the sales mix and the sales quantity variances?

A) Operating expenses.

B) Cost of goods sold.

C) Gross margin.

D) Contribution margin.

A) Operating expenses.

B) Cost of goods sold.

C) Gross margin.

D) Contribution margin.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 134 في هذه المجموعة.

فتح الحزمة

k this deck

53

Danner Fashions sells a line of women's dresses.Danner's performance report for November is shown below: (CMA adapted) The company uses a flexible budget to analyze its performance and to measure the effect on operating income of the various factors affecting the difference between budgeted and actual operating income.T

he variable cost flexible budget variance for November is:

A) $5,000 favorable.

B) $5,000 unfavorable.

C) $4,000 favorable.

D) $4,000 unfavorable.

he variable cost flexible budget variance for November is:

A) $5,000 favorable.

B) $5,000 unfavorable.

C) $4,000 favorable.

D) $4,000 unfavorable.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 134 في هذه المجموعة.

فتح الحزمة

k this deck

54

The sales mix variance would be:

A) favorable when a company sells relatively fewer of the products that have contribution margins lower than average.

B) favorable when a company sells relatively more of the products that have contribution margins higher than average.

C) unfavorable when a company sells relatively fewer of the products that have selling prices higher than average.

D) unfavorable when a company sells more of the products that have selling prices lower than average.

A) favorable when a company sells relatively fewer of the products that have contribution margins lower than average.

B) favorable when a company sells relatively more of the products that have contribution margins higher than average.

C) unfavorable when a company sells relatively fewer of the products that have selling prices higher than average.

D) unfavorable when a company sells more of the products that have selling prices lower than average.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 134 في هذه المجموعة.

فتح الحزمة

k this deck

55

A machine distributor sells two models,basic and deluxe.The following information relates to its master budget.Actual sales were 7,000 basic models and 2,800 deluxe models.The actual sales prices were the same as the budgeted sales prices for both models. What is the sales activity variance for the deluxe model?

A) $400,000.

B) $800,000.

C) $1,600,000.

D) $2,400,000.

A) $400,000.

B) $800,000.

C) $1,600,000.

D) $2,400,000.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 134 في هذه المجموعة.

فتح الحزمة

k this deck

56

The sales quantity variance would be favorable when a company sells:

A) relatively fewer of the products bearing contribution margins lower than average.

B) relatively more of the products bearing contribution margins higher than average.

C) more total units than budgeted,holding the sales mix constant.

D) less total units than budgeted,holding the sales mix constant.

A) relatively fewer of the products bearing contribution margins lower than average.

B) relatively more of the products bearing contribution margins higher than average.

C) more total units than budgeted,holding the sales mix constant.

D) less total units than budgeted,holding the sales mix constant.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 134 في هذه المجموعة.

فتح الحزمة

k this deck

57

A machine distributor sells two models,basic and deluxe.The following information relates to its master budget.Actual sales were 7,000 basic models and 2,800 deluxe models.The actual sales prices were the same as the budgeted sales prices for both models. What is the sales mix variance for the deluxe model based?

A) $1,176,000.

B) $1,344,000.

C) $2,400,000.

D) $2,520,000.

A) $1,176,000.

B) $1,344,000.

C) $2,400,000.

D) $2,520,000.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 134 في هذه المجموعة.

فتح الحزمة

k this deck

58

Danner Fashions sells a line of women's dresses.Danner's performance report for November is shown below: (CMA adapted) The company uses a flexible budget to analyze its performance and to measure the effect on operating income of the various factors affecting the difference between budgeted and actual operating income.

The sales price variance for November is:

A) $30,000 unfavorable.

B) $18,000 unfavorable.

C) $20,000 unfavorable.

D) $15,000 unfavorable.

The sales price variance for November is:

A) $30,000 unfavorable.

B) $18,000 unfavorable.

C) $20,000 unfavorable.

D) $15,000 unfavorable.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 134 في هذه المجموعة.

فتح الحزمة

k this deck

59

For a company that produces more than one product,the sales volume variance can be divided into which two of the following additional variances? (CMA adapted)

A) Sales price variance and flexible budget variance.

B) Sales mix variance and sales price variance.

C) Sales efficiency variance and sales price variance.

D) Sales quantity variance and sales mix variance.

A) Sales price variance and flexible budget variance.

B) Sales mix variance and sales price variance.

C) Sales efficiency variance and sales price variance.

D) Sales quantity variance and sales mix variance.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 134 في هذه المجموعة.

فتح الحزمة

k this deck

60

Danner Fashions sells a line of women's dresses.Danner's performance report for November is shown below: (CMA adapted) The company uses a flexible budget to analyze its performance and to measure the effect on operating income of the various factors affecting the difference between budgeted and actual operating income.

What additional information is needed for Danner to calculate the dollar impact of a change in market share on operating income for November? (CMA adapted)

A) Danner's budgeted market share and the budgeted total market size.

B) Danner's budgeted market share,the budgeted total market size,and average market selling price.

C) Danner's budgeted market share and the actual total market size.

D) Danner's actual market share and the actual total market size.

What additional information is needed for Danner to calculate the dollar impact of a change in market share on operating income for November? (CMA adapted)

A) Danner's budgeted market share and the budgeted total market size.

B) Danner's budgeted market share,the budgeted total market size,and average market selling price.

C) Danner's budgeted market share and the actual total market size.

D) Danner's actual market share and the actual total market size.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 134 في هذه المجموعة.

فتح الحزمة

k this deck

61

A company makes a product using two materials,one of which is interchangeable with a third material.The standards for producing one 200-pound batch are presented below.The last 200-pound batch was produced using 140 pounds of M and 90 pounds of O.The price of M was $0.03 per pound and the actual price of O was $0.10. What is the materials yield variance?

A) $1.12.

B) $1.68.

C) $3.00.

D) $1.32.

A) $1.12.

B) $1.68.

C) $3.00.

D) $1.32.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 134 في هذه المجموعة.

فتح الحزمة

k this deck

62

A credit balance in the labor yield variance implies:

A) the total units produced was greater than the expected number of units given the total labor hours actually used.

B) the total units produced was less than the expected number of units given the total labor hours actually used.

C) the total units produced was greater than the expected number of units given the total standard hours allowed.

D) the total units produced was less than the expected number of units given the total standard hours alloweD.

This would be a favorable variance.

A) the total units produced was greater than the expected number of units given the total labor hours actually used.

B) the total units produced was less than the expected number of units given the total labor hours actually used.

C) the total units produced was greater than the expected number of units given the total standard hours allowed.

D) the total units produced was less than the expected number of units given the total standard hours alloweD.

This would be a favorable variance.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 134 في هذه المجموعة.

فتح الحزمة

k this deck

63

What is the correct journal entry to record direct labor when the actual labor mix is favorable and the total standard hours allowed is greater than the total actual hours worked?

A)

B)

C)

D)

A)

B)

C)

D)

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 134 في هذه المجموعة.

فتح الحزمة

k this deck

64

The Becton Enterprises (BE)produces a gasoline additive,Charger Power.This product increases engine efficiency and improves gasoline mileage by creating a more complete burn in the combustion process.Careful controls are required during the production process to insure that the proper mix of input chemicals is achieved and that evaporation is controlled.Loss of output and efficiency may result if the controls are not effective.The standard cost of producing a 500-liter batch of Charger Power is $135.The standard materials mix and related standard cost of each chemical used in a 500-liter batch are: The quantities of chemicals purchased and used during the current production period are shown in the schedule below.A total of 140 batches of Charger Power were manufactured during the current production period.The controller of BE has determined its costs and chemical usage variations at the end of the production period.

If BE recognizes all variances at the earliest possible moment,what is the total material price variance?

A) $160.

B) $540.

C) $890.

D) $1,270.

If BE recognizes all variances at the earliest possible moment,what is the total material price variance?

A) $160.

B) $540.

C) $890.

D) $1,270.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 134 في هذه المجموعة.

فتح الحزمة

k this deck

65

The next year's budget for Trend,Inc. ,a multi-product company,is given below: At the end of the year,the total fixed costs and the variable costs per unit were exactly as budgeted,but the following units per product line were sold.Trend,Inc.analyzes the effects its sales variances have on the profitability of the company.

What is the total sales price variance?

A) $22,203.50.

B) $28,442.50.

C) $50,646.50.

D) $79,088.50.

What is the total sales price variance?

A) $22,203.50.

B) $28,442.50.

C) $50,646.50.

D) $79,088.50.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 134 في هذه المجموعة.

فتح الحزمة

k this deck

66

A manufacturer of industrial equipment has a standard costing system based on standard direct labor-hours (DLHs)as the measure of activity.Data from the company's flexible budget for manufacturing overhead are given below:

The following data pertain to operations for the most recent period:

How much overhead was applied to products during the period to the nearest dollar?

A) $44,712.

B) $44,125.

C) $43,125.

D) $44,850.

The following data pertain to operations for the most recent period:

How much overhead was applied to products during the period to the nearest dollar?A) $44,712.

B) $44,125.

C) $43,125.

D) $44,850.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 134 في هذه المجموعة.

فتح الحزمة

k this deck

67

The Vargas Company had the following expectations for the year:

What is Vargas' market share variance?

A) $37,296.88.

B) $40,906.25.

C) $35,700.00.

D) $32,550.00.

What is Vargas' market share variance?

A) $37,296.88.

B) $40,906.25.

C) $35,700.00.

D) $32,550.00.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 134 في هذه المجموعة.

فتح الحزمة

k this deck

68

The Becton Enterprises (BE)produces a gasoline additive,Charger Power.This product increases engine efficiency and improves gasoline mileage by creating a more complete burn in the combustion process.Careful controls are required during the production process to insure that the proper mix of input chemicals is achieved and that evaporation is controlled.Loss of output and efficiency may result if the controls are not effective.The standard cost of producing a 500-liter batch of Charger Power is $135.The standard materials mix and related standard cost of each chemical used in a 500-liter batch are:

The quantities of chemicals purchased and used during the current production period are shown in the schedule below.A total of 140 batches of Charger Power were manufactured during the current production period.The controller of BE has determined its costs and chemical usage variations at the end of the production period.

What is the total materials mix variance?

A) $476.00.

B) $420.00.

C) $388.50.

D) $280.00.

The quantities of chemicals purchased and used during the current production period are shown in the schedule below.A total of 140 batches of Charger Power were manufactured during the current production period.The controller of BE has determined its costs and chemical usage variations at the end of the production period.

What is the total materials mix variance?

A) $476.00.

B) $420.00.

C) $388.50.

D) $280.00.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 134 في هذه المجموعة.

فتح الحزمة

k this deck

69

What is the correct journal entry to record a favorable materials mix variance assuming all material variances are recognized when the direct materials are issued to production?

A)

B)

C)

D)

A)

B)

C)

D)

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 134 في هذه المجموعة.

فتح الحزمة

k this deck

70

The labor yield variance is actual total hours at:

A) actual mix times actual labor rates less actual total hours at actual mix times standard labor rates.

B) actual mix times standard labor rates less standard total hours at standard mix times standard labor rates.

C) actual mix times standard labor rates less actual total hours at standard mix times standard labor rates.

D) standard mix times standard labor rates less standard total hours at standard mix times standard labor rates.

A) actual mix times actual labor rates less actual total hours at actual mix times standard labor rates.

B) actual mix times standard labor rates less standard total hours at standard mix times standard labor rates.

C) actual mix times standard labor rates less actual total hours at standard mix times standard labor rates.

D) standard mix times standard labor rates less standard total hours at standard mix times standard labor rates.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 134 في هذه المجموعة.

فتح الحزمة

k this deck

71

A manufacturer of industrial equipment has a standard costing system based on standard direct labor-hours (DLHs)as the measure of activity.Data from the company's flexible budget for manufacturing overhead are given below:

The following data pertain to operations for the most recent period:

What is the predetermined overhead rate to the nearest cent?

A) $16.97.

B) $17.25.

C) $16.59.

D) $17.65.

The following data pertain to operations for the most recent period:

What is the predetermined overhead rate to the nearest cent?

A) $16.97.

B) $17.25.

C) $16.59.

D) $17.65.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 134 في هذه المجموعة.

فتح الحزمة

k this deck

72

The labor mix variance is actual total hours at:

A) actual mix times actual labor rates less actual total hours at actual mix times standard labor rates.

B) actual mix times standard labor rates less standard total hours at standard mix times standard labor rates.

C) actual mix times standard labor rates less actual total hours at standard mix times standard labor rates.

D) standard mix times standard labor rates less standard total hours at standard mix times standard labor rates.

A) actual mix times actual labor rates less actual total hours at actual mix times standard labor rates.

B) actual mix times standard labor rates less standard total hours at standard mix times standard labor rates.

C) actual mix times standard labor rates less actual total hours at standard mix times standard labor rates.

D) standard mix times standard labor rates less standard total hours at standard mix times standard labor rates.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 134 في هذه المجموعة.

فتح الحزمة

k this deck

73

A machine distributor sells two models,basic and deluxe.The following information relates to its master budget.Actual sales were 7,000 basic models and 2,800 deluxe models.The actual sales prices were the same as the budgeted sales prices for both models. What is the sales quantity variance for the deluxe model?

A) $120,000.

B) $256,000.

C) $1,344,000.

D) $1,600,000.

A) $120,000.

B) $256,000.

C) $1,344,000.

D) $1,600,000.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 134 في هذه المجموعة.

فتح الحزمة

k this deck

74

Bonner Company's direct labor cost for March was as follows:

What was Bonner's direct labor yield variance?

A) $13,450.

B) $9,675.

C) $9,225.

D) $5,000.

What was Bonner's direct labor yield variance?

A) $13,450.

B) $9,675.

C) $9,225.

D) $5,000.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 134 في هذه المجموعة.

فتح الحزمة

k this deck

75

The next year's budget for Trend,Inc. ,a multi-product company,is given below:

At the end of the year,the total fixed costs and the variable costs per unit were exactly as budgeted,but the following units per product line were sold.Trend,Inc.analyzes the effects its sales variances have on the profitability of the company.

What is the total sales quantity variance?

A) $3,570.00.

B) $20,815.00.

C) $33,915.00.

D) $40,553.50.

At the end of the year,the total fixed costs and the variable costs per unit were exactly as budgeted,but the following units per product line were sold.Trend,Inc.analyzes the effects its sales variances have on the profitability of the company.

What is the total sales quantity variance?

A) $3,570.00.

B) $20,815.00.

C) $33,915.00.

D) $40,553.50.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 134 في هذه المجموعة.

فتح الحزمة

k this deck

76

The next year's budget for Trend,Inc. ,a multi-product company,is given below:

At the end of the year,the total fixed costs and the variable costs per unit were exactly as budgeted,but the following units per product line were sold.Trend,Inc.analyzes the effects its sales variances have on the profitability of the company.

What is the total sales mix variance?

A) $12,478.00.

B) $20,815.00.

C) $33,915.00.

D) $40,553.50.

At the end of the year,the total fixed costs and the variable costs per unit were exactly as budgeted,but the following units per product line were sold.Trend,Inc.analyzes the effects its sales variances have on the profitability of the company.

What is the total sales mix variance?

A) $12,478.00.

B) $20,815.00.

C) $33,915.00.

D) $40,553.50.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 134 في هذه المجموعة.

فتح الحزمة

k this deck

77

The Shum Company makes a product,Z,from two materials: X and Y.The standard prices and quantities are as follows:

In May,21,000 units of Z were produced by Shum Company,with the following actual prices and quantities of materials used:

What is the total direct material yield variance for May?

A) $45,000.

B) $81,000.

C) $109,800.

D) $117,000.

In May,21,000 units of Z were produced by Shum Company,with the following actual prices and quantities of materials used:

What is the total direct material yield variance for May?

A) $45,000.

B) $81,000.

C) $109,800.

D) $117,000.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 134 في هذه المجموعة.

فتح الحزمة

k this deck

78

A company makes a product using two materials,one of which is interchangeable with a third material.The standards for producing one 200-pound batch are presented below.The last 200-pound batch was produced using 140 pounds of M and 90 pounds of O.The price of M was $0.03 per pound and the actual price of O was $0.10. What is the materials mix variance?

A) $1.68.

B) $3.00.

C) $1.32.

D) $0.84.

A) $1.68.

B) $3.00.

C) $1.32.

D) $0.84.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 134 في هذه المجموعة.

فتح الحزمة

k this deck

79

The Shum Company makes a product,Z,from two materials: X and Y.The standard prices and quantities are as follows:

In May,21,000 units of Z were produced by Shum Company,with the following actual prices and quantities of materials used:

What is the total direct materials mix variance for May?

A) $12,000.

B) $24,000.

C) $36,000.

D) $60,000.

In May,21,000 units of Z were produced by Shum Company,with the following actual prices and quantities of materials used:

What is the total direct materials mix variance for May?

A) $12,000.

B) $24,000.

C) $36,000.

D) $60,000.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 134 في هذه المجموعة.

فتح الحزمة

k this deck

80

The Becton Enterprises (BE)produces a gasoline additive,Charger Power.This product increases engine efficiency and improves gasoline mileage by creating a more complete burn in the combustion process.Careful controls are required during the production process to insure that the proper mix of input chemicals is achieved and that evaporation is controlled.Loss of output and efficiency may result if the controls are not effective.The standard cost of producing a 500-liter batch of Charger Power is $135.The standard materials mix and related standard cost of each chemical used in a 500-liter batch are:

The quantities of chemicals purchased and used during the current production period are shown in the schedule below.A total of 140 batches of Charger Power were manufactured during the current production period.The controller of BE has determined its costs and chemical usage variations at the end of the production period.

What is the total materials yield variance?

A) $388.50.

B) $294.50.

C) $280.00.

D) $94.50.

The quantities of chemicals purchased and used during the current production period are shown in the schedule below.A total of 140 batches of Charger Power were manufactured during the current production period.The controller of BE has determined its costs and chemical usage variations at the end of the production period.

What is the total materials yield variance?

A) $388.50.

B) $294.50.

C) $280.00.

D) $94.50.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 134 في هذه المجموعة.

فتح الحزمة

k this deck

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 134 في هذه المجموعة.