Deck 9: Audit Sampling: Substantive Tests of Details

ملء الشاشة (f)

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

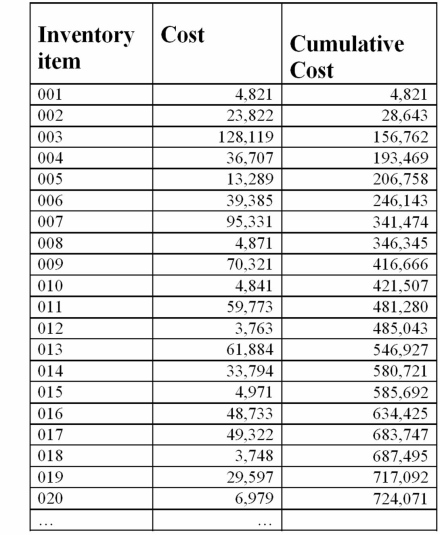

Assume that you are the auditor in charge of designing a sampling plan to evaluate the cost of the year-end inventory balance for BCS,Inc.The company uses FIFO costing to determine the cost of its inventory.Additional information is provided below.The total amount of inventory is $10,800,000.The desired level of assurance is 90% (10% risk of incorrect acceptance).The ratio of estimated misstatement to tolerable misstatement is 0.00.The confidence factor is 2.31 from the table in the chapter.Tolerable misstatement is $1,000,000.A partial list of inventory is given below:

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

فتح الحزمة

قم بالتسجيل لفتح البطاقات في هذه المجموعة!

Unlock Deck

Unlock Deck

1/72

العب

ملء الشاشة (f)

Deck 9: Audit Sampling: Substantive Tests of Details

1

Audit risk can be divided into two categories,inherent risk and control risk.

False

2

The risk of incorrect rejection of the account balance or class of transactions is an error that affects

A)the efficiency of the audit

B)the effectiveness of the audit

C)the reliability of the audit

D)the relevance of the audit

A)the efficiency of the audit

B)the effectiveness of the audit

C)the reliability of the audit

D)the relevance of the audit

A

3

If we find misstatements in the sample

A)we assume that misstatements similar to the misstatements in the population would be found in the sample

B)we conclude that misstatements similar to the misstatements in the sample exist in the population

C)we conclude that the population contains misstatements

D)we assume that misstatements similar to the misstatements in the sample would be found in the population

A)we assume that misstatements similar to the misstatements in the population would be found in the sample

B)we conclude that misstatements similar to the misstatements in the sample exist in the population

C)we conclude that the population contains misstatements

D)we assume that misstatements similar to the misstatements in the sample would be found in the population

D

4

The more serious error of the errors associated with the risk of incorrect acceptance and the risk of incorrect rejection is the error related to the

A)relevance of the audit

B)reliability of the audit

C)effectiveness of the audit

D)efficiency of the audit

A)relevance of the audit

B)reliability of the audit

C)effectiveness of the audit

D)efficiency of the audit

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 72 في هذه المجموعة.

فتح الحزمة

k this deck

5

The auditor gathers evidence about whether balance sheet and income statement accounts are misleading by performing substantive tests of controls.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 72 في هذه المجموعة.

فتح الحزمة

k this deck

6

The auditor uses sampling for substantive tests of balances and for substantive tests of transactions to determine

A)whether the financial statements accounts associated with the account balance or class of transactions are materially misstated

B)whether the financial statements are materially misstated

C)whether the balance sheet accounts associated with the account balance or class of transactions are materially misstated

D)whether the income statement accounts associated with the account balance or class of transactions are materially misstated

A)whether the financial statements accounts associated with the account balance or class of transactions are materially misstated

B)whether the financial statements are materially misstated

C)whether the balance sheet accounts associated with the account balance or class of transactions are materially misstated

D)whether the income statement accounts associated with the account balance or class of transactions are materially misstated

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 72 في هذه المجموعة.

فتح الحزمة

k this deck

7

The items selected for examination are referred to as

A)the population

B)the variables

C)the sample

D)the misstatements

A)the population

B)the variables

C)the sample

D)the misstatements

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 72 في هذه المجموعة.

فتح الحزمة

k this deck

8

Variables sampling is used to determine the accuracy of the recorded amount in the population from the evidence in a sample of the population.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 72 في هذه المجموعة.

فتح الحزمة

k this deck

9

Sampling risk is

A)the risk that the sample is not large enough

B)the risk that the sample is not representative of the population

C)the risk that the sample contains too many errors

D)the risk that the sample does not contain enough errors

A)the risk that the sample is not large enough

B)the risk that the sample is not representative of the population

C)the risk that the sample contains too many errors

D)the risk that the sample does not contain enough errors

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 72 في هذه المجموعة.

فتح الحزمة

k this deck

10

Sampling risk for substantive testing includes the risk of incorrect acceptance of the account balance or class of transactions and the risk of incorrect rejection of the account balance or class of transactions.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 72 في هذه المجموعة.

فتح الحزمة

k this deck

11

Audit risk is

A)the risk that material misstatements occur in the financial statements

B)the risk that material misstatements occur in the financial statements and are not detected by the auditor

C)the risk that material misstatements occur and are not detected by the auditor

D)the risk that misstatements occur in the financial statements and are not detected by the auditor

A)the risk that material misstatements occur in the financial statements

B)the risk that material misstatements occur in the financial statements and are not detected by the auditor

C)the risk that material misstatements occur and are not detected by the auditor

D)the risk that misstatements occur in the financial statements and are not detected by the auditor

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 72 في هذه المجموعة.

فتح الحزمة

k this deck

12

Sample size requirements are usually determined by statisticians in the head office of an accounting firm.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 72 في هذه المجموعة.

فتح الحزمة

k this deck

13

Both statistical and nonstatistical samples require professional judgment in planning the sample,performing the procedures,and evaluating the evidence.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 72 في هذه المجموعة.

فتح الحزمة

k this deck

14

We use evidence from the variables sample to arrive at a conclusion about the sample.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 72 في هذه المجموعة.

فتح الحزمة

k this deck

15

Sampling risk for substantive testing includes

A)the risk of incorrect sample selection

B)the risk of incorrect sample evaluation

C)the risk of incorrect planning for sample selection

D)the risk of incorrect acceptance of the account balance or class of transactions

E)the risk of incorrect rejection of the account balance or class of transactions

F)both A and C

G)both B and E

Both D and E

A)the risk of incorrect sample selection

B)the risk of incorrect sample evaluation

C)the risk of incorrect planning for sample selection

D)the risk of incorrect acceptance of the account balance or class of transactions

E)the risk of incorrect rejection of the account balance or class of transactions

F)both A and C

G)both B and E

Both D and E

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 72 في هذه المجموعة.

فتح الحزمة

k this deck

16

Variables sampling is the application of an audit procedure to less than 100% of an account balance or class of transactions to determine whether the recorded amount is materially misstated.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 72 في هذه المجموعة.

فتح الحزمة

k this deck

17

The auditor believes that the characteristics of the population

A)will be represented in a sample

B)will not be represented in a random sample

C)will likely be represented in a random sample

D)may be represented in a sample

A)will be represented in a sample

B)will not be represented in a random sample

C)will likely be represented in a random sample

D)may be represented in a sample

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 72 في هذه المجموعة.

فتح الحزمة

k this deck

18

The risk of incorrect acceptance of the account balance or class of transactions is an error that affects

A)the efficiency of the audit

B)the effectiveness of the audit

C)the reliability of the audit

D)the relevance of the audit

A)the efficiency of the audit

B)the effectiveness of the audit

C)the reliability of the audit

D)the relevance of the audit

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 72 في هذه المجموعة.

فتح الحزمة

k this deck

19

For a statistical sample,sampling risk is determined by auditor judgment.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 72 في هذه المجموعة.

فتح الحزمة

k this deck

20

Any misstatements that are not corrected by the client will be recorded as proposed audit adjustments.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 72 في هذه المجموعة.

فتح الحزمة

k this deck

21

When the auditor uses systematic random sampling with an individual dollar amount as the sampling unit,we refer to this method of sampling as

A)probability monetary sampling

B)proportionate monetary sampling

C)monetary proportionate to size sampling

D)monetary unit sampling

E)probability proportionate to size sampling

F)both A and B

G)both C and D

Both D and E

A)probability monetary sampling

B)proportionate monetary sampling

C)monetary proportionate to size sampling

D)monetary unit sampling

E)probability proportionate to size sampling

F)both A and B

G)both C and D

Both D and E

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 72 في هذه المجموعة.

فتح الحزمة

k this deck

22

The population for a substantive test of details consists of

A)all events in the accounts or class of transactions

B)all material items in the accounts or class of transactions

C)all material events in the accounts or class of transactions

D)all items in the accounts at the end of the year

E)all transactions in the class of transactions for the entire year

F)both A and B

G)both C and D

Both D and E

A)all events in the accounts or class of transactions

B)all material items in the accounts or class of transactions

C)all material events in the accounts or class of transactions

D)all items in the accounts at the end of the year

E)all transactions in the class of transactions for the entire year

F)both A and B

G)both C and D

Both D and E

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 72 في هذه المجموعة.

فتح الحزمة

k this deck

23

The test objective for a substantive test is to determine

A)if the account balance or class of transactions is correctly stated

B)if the account balance or class of transactions is materially misstated

C)if the sample selected was appropriate for the audit

D)if the sample resulted in the expected deviation rate

A)if the account balance or class of transactions is correctly stated

B)if the account balance or class of transactions is materially misstated

C)if the sample selected was appropriate for the audit

D)if the sample resulted in the expected deviation rate

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 72 في هذه المجموعة.

فتح الحزمة

k this deck

24

Which of the following is a statistical audit sampling technique that the auditor may decide to use?

A)judgmental sampling

B)haphazard sampling

C)monetary unit sampling

D)classical variables sampling

E)non random number sampling

F)both A and C

G)both B and E

Both C and D

A)judgmental sampling

B)haphazard sampling

C)monetary unit sampling

D)classical variables sampling

E)non random number sampling

F)both A and C

G)both B and E

Both C and D

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 72 في هذه المجموعة.

فتح الحزمة

k this deck

25

Sampling methods for substantive samples include

A)skip random sampling

B)organized sampling

C)simple random sampling

D)systematic non random sampling

E)haphazard sampling

F)both A and B

G)both C and E

H)both D and E

A)skip random sampling

B)organized sampling

C)simple random sampling

D)systematic non random sampling

E)haphazard sampling

F)both A and B

G)both C and E

H)both D and E

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 72 في هذه المجموعة.

فتح الحزمة

k this deck

26

Nonsampling risk includes

A)all aspects of audit risk that are not related to sampling

B)all aspects of audit risk that are related to sampling

C)all aspects of control risk that are not related to sampling

D)all aspects of control risk that are related to sampling

A)all aspects of audit risk that are not related to sampling

B)all aspects of audit risk that are related to sampling

C)all aspects of control risk that are not related to sampling

D)all aspects of control risk that are related to sampling

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 72 في هذه المجموعة.

فتح الحزمة

k this deck

27

The auditor must define the sampling unit in a way that is

A)consistent with the assertion being tested

B)consistent with the account balance being tested

C)consistent with the transaction being tested

D)consistent with the population being tested

A)consistent with the assertion being tested

B)consistent with the account balance being tested

C)consistent with the transaction being tested

D)consistent with the population being tested

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 72 في هذه المجموعة.

فتح الحزمة

k this deck

28

Tolerable misstatement is defined as

A)the level of assurance that the account balance or class of transactions is not misstated

B)the amount of misstatement,on the basis of the auditor's professional judgment,that should be present in the account balance or class of transactions

C)the maximum misstatement in the account balance or class of transactions that the auditor is willing to accept

D)the level of audit risk the auditor is willing to accept

A)the level of assurance that the account balance or class of transactions is not misstated

B)the amount of misstatement,on the basis of the auditor's professional judgment,that should be present in the account balance or class of transactions

C)the maximum misstatement in the account balance or class of transactions that the auditor is willing to accept

D)the level of audit risk the auditor is willing to accept

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 72 في هذه المجموعة.

فتح الحزمة

k this deck

29

Auditors control nonsampling risk by

A)quantifying the risk

B)planning and supervising employees

C)performing analytical procedures

D)performing tests of controls

A)quantifying the risk

B)planning and supervising employees

C)performing analytical procedures

D)performing tests of controls

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 72 في هذه المجموعة.

فتح الحزمة

k this deck

30

The only thing(s)that must change when the auditor moves from statistical sampling to nonstatistical sampling is (are)

A)the sample testing method

B)the way the auditor evaluates the sample results

C)the sample evaluation method

D)the way the auditor obtains the sample results

E)the sample selection method

A)the sample testing method

B)the way the auditor evaluates the sample results

C)the sample evaluation method

D)the way the auditor obtains the sample results

E)the sample selection method

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 72 في هذه المجموعة.

فتح الحزمة

k this deck

31

If the auditor has a choice of sample size,he should consider which of the following factors in selecting the correct sample size?

A)desired level of assurance

B)tolerable level of assurance

C)expected misstatement

D)stratification of the misstatements

E)actual misstatement

F)both A and C

G)both A and E

H)both B and D

A)desired level of assurance

B)tolerable level of assurance

C)expected misstatement

D)stratification of the misstatements

E)actual misstatement

F)both A and C

G)both A and E

H)both B and D

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 72 في هذه المجموعة.

فتح الحزمة

k this deck

32

The auditor gathers evidence about whether balance sheet and income statement accounts are materially misstated by

A)performing tests of controls

B)the sample selection method

C)the sample evaluation method

D)performing substantive tests of details

A)performing tests of controls

B)the sample selection method

C)the sample evaluation method

D)performing substantive tests of details

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 72 في هذه المجموعة.

فتح الحزمة

k this deck

33

Sampling methods for substantive samples include

A)skip random sampling

B)organized sampling

C)simple non random sampling

D)systematic random sampling

E)haphazard sampling

F)both A and C

G)both B and C

Both D and E

A)skip random sampling

B)organized sampling

C)simple non random sampling

D)systematic random sampling

E)haphazard sampling

F)both A and C

G)both B and C

Both D and E

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 72 في هذه المجموعة.

فتح الحزمة

k this deck

34

Expected misstatement is defined as

A)the level of assurance that the account balance or class of transactions is not misstated

B)the amount of misstatement,on the basis of the auditor's professional judgment,that should be present in the account balance or class of transactions

C)the maximum misstatement in the account balance or class of transactions that the auditor is willing to accept

D)the level of audit risk the auditor is willing to accept

A)the level of assurance that the account balance or class of transactions is not misstated

B)the amount of misstatement,on the basis of the auditor's professional judgment,that should be present in the account balance or class of transactions

C)the maximum misstatement in the account balance or class of transactions that the auditor is willing to accept

D)the level of audit risk the auditor is willing to accept

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 72 في هذه المجموعة.

فتح الحزمة

k this deck

35

If the auditor has a choice of sample size,he should consider which of the following factors in selecting the correct sample size?

A)desired level of misstatement

B)tolerable misstatement

C)expected level of assurance

D)stratification of the population when performed

E)actual misstatement

F)both A and C

G)both A and E

Both B and D

A)desired level of misstatement

B)tolerable misstatement

C)expected level of assurance

D)stratification of the population when performed

E)actual misstatement

F)both A and C

G)both A and E

Both B and D

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 72 في هذه المجموعة.

فتح الحزمة

k this deck

36

The desired level of assurance is defined as

A)the level of assurance that the account balance or class of transactions is not misstated

B)the amount of misstatement,on the basis of the auditor's professional judgment,that should be present in the account balance or class of transactions

C)the maximum misstatement in the account balance or class of transactions that the auditor is willing to accept

D)the level of audit risk the auditor is willing to accept

A)the level of assurance that the account balance or class of transactions is not misstated

B)the amount of misstatement,on the basis of the auditor's professional judgment,that should be present in the account balance or class of transactions

C)the maximum misstatement in the account balance or class of transactions that the auditor is willing to accept

D)the level of audit risk the auditor is willing to accept

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 72 في هذه المجموعة.

فتح الحزمة

k this deck

37

Sampling methods for substantive samples include

A)skip random sampling

B)organized sampling

C)simple random sampling

D)systematic random sampling

E)haphazard random sampling

F)both A and B

G)both C and D

H)both D and E

A)skip random sampling

B)organized sampling

C)simple random sampling

D)systematic random sampling

E)haphazard random sampling

F)both A and B

G)both C and D

H)both D and E

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 72 في هذه المجموعة.

فتح الحزمة

k this deck

38

Nonstatistical sampling

A)is never a more effective way to gather evidence

B)is a less efficient way to gather evidence

C)may be a less efficient way to gather evidence

D)should be viewed as a less effective way to gather evidence

E)should not be viewed as a less effective way to gather evidence

F)both A and C

G)both B and D

Both C and E

A)is never a more effective way to gather evidence

B)is a less efficient way to gather evidence

C)may be a less efficient way to gather evidence

D)should be viewed as a less effective way to gather evidence

E)should not be viewed as a less effective way to gather evidence

F)both A and C

G)both B and D

Both C and E

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 72 في هذه المجموعة.

فتح الحزمة

k this deck

39

Which of the following is a nonstatistical method of selecting a sample that the auditor may decide to use?

A)judgmental sampling

B)haphazard sampling

C)monetary unit sampling

D)classical variables sampling

E)random number sampling

F)both B and C

G)both C and E

H)both D and E

A)judgmental sampling

B)haphazard sampling

C)monetary unit sampling

D)classical variables sampling

E)random number sampling

F)both B and C

G)both C and E

H)both D and E

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 72 في هذه المجموعة.

فتح الحزمة

k this deck

40

With nonstatistical sampling,sampling risk is controlled by

A)quantifying sampling risk to keep the risk to an acceptable number

B)quantifying control risk to keep the risk to an acceptable number

C)selecting appropriate sample sizes

D)taking a random sample so the sample is representative of the population

E)evaluating sample results to consider control risk in the evaluation of the results

A)quantifying sampling risk to keep the risk to an acceptable number

B)quantifying control risk to keep the risk to an acceptable number

C)selecting appropriate sample sizes

D)taking a random sample so the sample is representative of the population

E)evaluating sample results to consider control risk in the evaluation of the results

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 72 في هذه المجموعة.

فتح الحزمة

k this deck

41

Sampling would not be used to

A)recalculate

B)observe

C)confirm

D)perform analytical procedures

E)reperform

F)both A and B

G)both B and D

H)both C and E

A)recalculate

B)observe

C)confirm

D)perform analytical procedures

E)reperform

F)both A and B

G)both B and D

H)both C and E

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 72 في هذه المجموعة.

فتح الحزمة

k this deck

42

Haphazard sampling

A)must be used when the items in the population are not pre-numbered documents

B)is a careless sample

C)does not use a random number method to select the sample

D)may be used when the items in the population are not pre-numbered documents

E)uses a random number method to select the sample

F)both A and C

G)both B and D

H)both D and E

A)must be used when the items in the population are not pre-numbered documents

B)is a careless sample

C)does not use a random number method to select the sample

D)may be used when the items in the population are not pre-numbered documents

E)uses a random number method to select the sample

F)both A and C

G)both B and D

H)both D and E

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 72 في هذه المجموعة.

فتح الحزمة

k this deck

43

The only thing(s)that might change when the auditor moves from statistical sampling to nonstatistical sampling is (are)

A)the sample testing method

B)the way the auditor evaluates the sample results

C)the sample evaluation method

D)the way the auditor obtains the sample results

E)the sample selection method

F)both A and C

G)both B and E

H)both D and E

A)the sample testing method

B)the way the auditor evaluates the sample results

C)the sample evaluation method

D)the way the auditor obtains the sample results

E)the sample selection method

F)both A and C

G)both B and E

H)both D and E

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 72 في هذه المجموعة.

فتح الحزمة

k this deck

44

Sampling would not be used to

A)recalculate

B)observe

C)confirm

D)make inquiries

E)reperform

F)both A and B

G)both C and D

Both B and D

A)recalculate

B)observe

C)confirm

D)make inquiries

E)reperform

F)both A and B

G)both C and D

Both B and D

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 72 في هذه المجموعة.

فتح الحزمة

k this deck

45

If the projected misstatement is greater than the tolerable misstatement,the auditor must

A)give appropriate consideration to the sampling risk in the determination of whether the projected misstatement plus sampling risk is greater than the tolerable misstatement

B)give appropriate consideration to the sampling risk in the determination of whether the projected misstatement plus sampling risk is less than the tolerable misstatement

C)gather additional evidence to determine the amount of the material misstatement

D)gather additional evidence to determine the amount of the actual tolerable misstatement

A)give appropriate consideration to the sampling risk in the determination of whether the projected misstatement plus sampling risk is greater than the tolerable misstatement

B)give appropriate consideration to the sampling risk in the determination of whether the projected misstatement plus sampling risk is less than the tolerable misstatement

C)gather additional evidence to determine the amount of the material misstatement

D)gather additional evidence to determine the amount of the actual tolerable misstatement

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 72 في هذه المجموعة.

فتح الحزمة

k this deck

46

In a nonstatistical substantive test of transactions for an income statement account,the auditor decides that sales revenue is materially misstated.In this case,the auditor might

A)investigate the misstatements in the account and recommend corrections

B)ask the client to investigate the misstatements in the account and correct them

C)increase the sample size and perform additional tests to identify the amount of the total misstatement in the income statement

D)increase the sample size and perform additional tests to reduce the amount of the total misstatement in the account

E)increase the sample size and perform additional tests to identify the amount of the total misstatement in the account

F)both A and B

G)both C and D

Both B and E

A)investigate the misstatements in the account and recommend corrections

B)ask the client to investigate the misstatements in the account and correct them

C)increase the sample size and perform additional tests to identify the amount of the total misstatement in the income statement

D)increase the sample size and perform additional tests to reduce the amount of the total misstatement in the account

E)increase the sample size and perform additional tests to identify the amount of the total misstatement in the account

F)both A and B

G)both C and D

Both B and E

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 72 في هذه المجموعة.

فتح الحزمة

k this deck

47

Sampling would not be used to

A)recalculate

B)make inquiries

C)confirm

D)perform analytical procedures

E)reperform

F)both B and D

G)both C and D

H)both D and E

A)recalculate

B)make inquiries

C)confirm

D)perform analytical procedures

E)reperform

F)both B and D

G)both C and D

H)both D and E

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 72 في هذه المجموعة.

فتح الحزمة

k this deck

48

With monetary unit sampling,estimating the misstatements in the population is

A)best done by assuming the misstatements are relative to the dollar value of the population

B)best done by determining the misstatements are relative to the dollar value of the population

C)must be done by assuming the misstatements are relative to the dollar value of the population

D)must be done by determining the misstatements are relative to the dollar value of the population

A)best done by assuming the misstatements are relative to the dollar value of the population

B)best done by determining the misstatements are relative to the dollar value of the population

C)must be done by assuming the misstatements are relative to the dollar value of the population

D)must be done by determining the misstatements are relative to the dollar value of the population

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 72 في هذه المجموعة.

فتح الحزمة

k this deck

49

To obtain the projected misstatements for the account balance or class of transactions,auditors

A)divide the known misstatement by the likely misstatement

B)subtract the likely misstatement from the known misstatement

C)add the known misstatement to the likely misstatement

D)subtract the known misstatement from the likely misstatement

A)divide the known misstatement by the likely misstatement

B)subtract the likely misstatement from the known misstatement

C)add the known misstatement to the likely misstatement

D)subtract the known misstatement from the likely misstatement

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 72 في هذه المجموعة.

فتح الحزمة

k this deck

50

Which of the following misstatements may cause the auditor to perform additional tests to determine if there are remaining misstatements in the account balance or class of transactions?

A)misstatements caused by fraud

B)misstatements caused by error

C)misstatements caused by carelessness

D)misstatements caused by lack of understanding of instructions

E)misstatements caused by inattention to detail

F)both A and D

G)both B and C

H)both D and E

A)misstatements caused by fraud

B)misstatements caused by error

C)misstatements caused by carelessness

D)misstatements caused by lack of understanding of instructions

E)misstatements caused by inattention to detail

F)both A and D

G)both B and C

H)both D and E

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 72 في هذه المجموعة.

فتح الحزمة

k this deck

51

With monetary unit sampling,misstatements are

A)evaluated to determine the extent of the misstatement

B)evaluated to determine if the population can be accepted as fairly stated

C)projected to the total population to determine possible misstatement

D)projected to the population in each sampling interval where the misstatements were found

A)evaluated to determine the extent of the misstatement

B)evaluated to determine if the population can be accepted as fairly stated

C)projected to the total population to determine possible misstatement

D)projected to the population in each sampling interval where the misstatements were found

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 72 في هذه المجموعة.

فتح الحزمة

k this deck

52

The population for a substantive test of balances consists of

A)all items in the account for the entire year

B)all material items in the accounts or class of transactions

C)all material events in the accounts or class of transactions

D)all items in the accounts at the end of the year

E)all transactions in the class of transactions for the entire year

A)all items in the account for the entire year

B)all material items in the accounts or class of transactions

C)all material events in the accounts or class of transactions

D)all items in the accounts at the end of the year

E)all transactions in the class of transactions for the entire year

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 72 في هذه المجموعة.

فتح الحزمة

k this deck

53

To evaluate the statistical sample,the auditor uses

A)probability tables

B)professional judgment

C)the level of tolerance

D)the confidence interval

A)probability tables

B)professional judgment

C)the level of tolerance

D)the confidence interval

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 72 في هذه المجموعة.

فتح الحزمة

k this deck

54

The known and likely misstatements will be added to the proposed audit adjustment schedule,so that

A)the auditor can consider these misstatements to determine whether the financial statements as a whole are materially misstated

B)the auditor can consider these misstatements in combination with the other misstatements found to determine whether the financial statements as a whole are materially misstated

C)the auditor can consider these misstatements in combination with the other misstatements found to determine whether the financial statements as a whole are fairly presented

D)the auditor can consider these misstatements to determine whether the financial statements as a whole are fairly presented

A)the auditor can consider these misstatements to determine whether the financial statements as a whole are materially misstated

B)the auditor can consider these misstatements in combination with the other misstatements found to determine whether the financial statements as a whole are materially misstated

C)the auditor can consider these misstatements in combination with the other misstatements found to determine whether the financial statements as a whole are fairly presented

D)the auditor can consider these misstatements to determine whether the financial statements as a whole are fairly presented

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 72 في هذه المجموعة.

فتح الحزمة

k this deck

55

To determine whether the account balance or class of transactions is materially misstated,the auditor

A)determines the tolerable misstatement from the sample results and compares this amount to the projected misstatement allocated to the account balance or class of transactions

B)determines the projected misstatement from the sample results and compares this amount to the tolerable misstatement allocated to the account balance or class of transactions

C)determines the expected deviations from the sample results and compares this amount to the tolerable misstatement allocated to the account balance or class of transactions

D)determines the actual deviations from the sample results and compares this amount to the tolerable misstatement allocated to the account balance or class of transactions

A)determines the tolerable misstatement from the sample results and compares this amount to the projected misstatement allocated to the account balance or class of transactions

B)determines the projected misstatement from the sample results and compares this amount to the tolerable misstatement allocated to the account balance or class of transactions

C)determines the expected deviations from the sample results and compares this amount to the tolerable misstatement allocated to the account balance or class of transactions

D)determines the actual deviations from the sample results and compares this amount to the tolerable misstatement allocated to the account balance or class of transactions

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 72 في هذه المجموعة.

فتح الحزمة

k this deck

56

With monetary unit sampling

A)each individual interval in the population has an equal chance of being selected

B)each individual dollar in the population has an equal chance of being selected

C)each interval of dollars in the population has an equal chance of being selected

D)each dollar within the interval in the population has an equal chance of being selected

A)each individual interval in the population has an equal chance of being selected

B)each individual dollar in the population has an equal chance of being selected

C)each interval of dollars in the population has an equal chance of being selected

D)each dollar within the interval in the population has an equal chance of being selected

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 72 في هذه المجموعة.

فتح الحزمة

k this deck

57

With monetary unit sampling,a random start is

A)a number selected from the random number tables

B)a number selected judgmentally by the auditor

C)a number between 1 and the sampling interval

D)a number equal to the sampling interval

A)a number selected from the random number tables

B)a number selected judgmentally by the auditor

C)a number between 1 and the sampling interval

D)a number equal to the sampling interval

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 72 في هذه المجموعة.

فتح الحزمة

k this deck

58

The population for a substantive test of transactions consists of

A)all items in the class of transactions at the end of the year

B)all material items in the accounts or class of transactions

C)all material events in the accounts or class of transactions

D)all items in the accounts at the end of the year

E)all transactions in the class of transactions for the entire year

A)all items in the class of transactions at the end of the year

B)all material items in the accounts or class of transactions

C)all material events in the accounts or class of transactions

D)all items in the accounts at the end of the year

E)all transactions in the class of transactions for the entire year

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 72 في هذه المجموعة.

فتح الحزمة

k this deck

59

If the projected misstatement is less than the tolerable misstatement,the auditor must

A)give appropriate consideration to the sampling risk in the determination of whether the projected misstatement plus sampling risk is greater than the tolerable misstatement

B)give appropriate consideration to the sampling risk in the determination of whether the projected misstatement plus sampling risk is less than the tolerable misstatement

C)gather additional evidence to determine the amount of the material misstatement

D)gather additional evidence to determine the amount of the actual tolerable misstatement

A)give appropriate consideration to the sampling risk in the determination of whether the projected misstatement plus sampling risk is greater than the tolerable misstatement

B)give appropriate consideration to the sampling risk in the determination of whether the projected misstatement plus sampling risk is less than the tolerable misstatement

C)gather additional evidence to determine the amount of the material misstatement

D)gather additional evidence to determine the amount of the actual tolerable misstatement

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 72 في هذه المجموعة.

فتح الحزمة

k this deck

60

The auditor makes the decision about whether the misstatements found in a substantive test of balances sample are material after

A)determining if the misstatements are within the tolerance level

B)determining if the misstatements are within the assurance level

C)extrapolating misstatements from the sample to the population

D)projecting misstatements from the sample to the population

A)determining if the misstatements are within the tolerance level

B)determining if the misstatements are within the assurance level

C)extrapolating misstatements from the sample to the population

D)projecting misstatements from the sample to the population

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 72 في هذه المجموعة.

فتح الحزمة

k this deck

61

To obtain the likely misstatements for the account balance or class of transactions,auditors

A)divide the known misstatement by the likely misstatement

B)subtract the likely misstatement from the known misstatement

C)add the known misstatement to the likely misstatement

D)subtract the known misstatement from the likely misstatement

E)subtract the known misstatement from the projected misstatement

A)divide the known misstatement by the likely misstatement

B)subtract the likely misstatement from the known misstatement

C)add the known misstatement to the likely misstatement

D)subtract the known misstatement from the likely misstatement

E)subtract the known misstatement from the projected misstatement

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 72 في هذه المجموعة.

فتح الحزمة

k this deck

62

The desired level of assurance is defined as

A)the level of assurance that the account balance or class of transactions is not misstated

B)the amount of misstatement,on the basis of the auditor's professional judgment,that should be present in the account balance or class of transactions

C)the maximum misstatement in the account balance or class of transactions that the auditor is willing to accept

D)the level of audit risk the auditor is willing to accept

E)the level of assurance that the tolerable misstatement is exceeded by the actual misstatement

F)both A and B

G)both C and D

Both D and E

A)the level of assurance that the account balance or class of transactions is not misstated

B)the amount of misstatement,on the basis of the auditor's professional judgment,that should be present in the account balance or class of transactions

C)the maximum misstatement in the account balance or class of transactions that the auditor is willing to accept

D)the level of audit risk the auditor is willing to accept

E)the level of assurance that the tolerable misstatement is exceeded by the actual misstatement

F)both A and B

G)both C and D

Both D and E

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 72 في هذه المجموعة.

فتح الحزمة

k this deck

63

Assume that you are the auditor in charge of designing a sampling plan to evaluate the cost of the year-end inventory balance for BCS,Inc.The company uses FIFO costing to determine the cost of its inventory.Additional information is provided below.The total amount of inventory is $10,800,000.The desired level of assurance is 90% (10% risk of incorrect acceptance).The ratio of estimated misstatement to tolerable misstatement is 0.00.The confidence factor is 2.31 from the table in the chapter.Tolerable misstatement is $1,000,000.A partial list of inventory is given below:

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 72 في هذه المجموعة.

فتح الحزمة

k this deck

64

You are responsible for planning the audit of fixed asset additions for the BCS Corporation.Describe how you would select a sample to determine whether fixed asset additions have been recorded correctly.Prepare a sampling plan to describe how you will perform the test.The desired level of assurance is 95% (5% risk of incorrect acceptance).The ratio of estimated misstatement to tolerable misstatement is 0.05.The confidence factor is 3.31 from the table in the chapter.Tolerable misstatement is $50,000,000.The balance in the fixed asset additions account is $480,000,000.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 72 في هذه المجموعة.

فتح الحزمة

k this deck

65

The auditor makes the decision about whether the misstatements found in a substantive test of balances sample are material after

A)determining if the misstatements are within the tolerance level

B)determining if the misstatements are within the assurance level

C)extrapolating misstatements from the sample to the population

D)projecting misstatements from the sample to the population

E)extrapolating misstatements from the population to the sample

A)determining if the misstatements are within the tolerance level

B)determining if the misstatements are within the assurance level

C)extrapolating misstatements from the sample to the population

D)projecting misstatements from the sample to the population

E)extrapolating misstatements from the population to the sample

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 72 في هذه المجموعة.

فتح الحزمة

k this deck

66

The auditor makes the decision about whether the misstatements found in a substantive test of balances sample are material after

A)determining if the misstatements are within the tolerance level

B)determining if the misstatements are within the assurance level

C)extrapolating misstatements from the sample to the population

D)projecting misstatements from the sample to the population

E)projecting misstatements from the population to the sample

A)determining if the misstatements are within the tolerance level

B)determining if the misstatements are within the assurance level

C)extrapolating misstatements from the sample to the population

D)projecting misstatements from the sample to the population

E)projecting misstatements from the population to the sample

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 72 في هذه المجموعة.

فتح الحزمة

k this deck

67

To evaluate the non-statistical sample,the auditor uses

A)probability tables

B)professional judgment

C)the level of tolerance

D)the confidence interval

A)probability tables

B)professional judgment

C)the level of tolerance

D)the confidence interval

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 72 في هذه المجموعة.

فتح الحزمة

k this deck

68

Tolerable misstatement is

A)a matter of professional judgment

B)the amount of misstatement,on the basis of the auditor's professional judgment,that should be present in the account balance or class of transactions

C)often stated as 50-75% of materiality level

D)the level of audit risk the auditor is willing to accept

E)both A and C

F)both B and E

G)both C and D

A)a matter of professional judgment

B)the amount of misstatement,on the basis of the auditor's professional judgment,that should be present in the account balance or class of transactions

C)often stated as 50-75% of materiality level

D)the level of audit risk the auditor is willing to accept

E)both A and C

F)both B and E

G)both C and D

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 72 في هذه المجموعة.

فتح الحزمة

k this deck

69

To obtain the known misstatements for the account balance or class of transactions,auditors

A)divide the likely misstatement by the projected misstatement

B)subtract the likely misstatement from the projected misstatement

C)add the projected misstatement to the likely misstatement

D)perform the audit procedure as specified in the audit program and determine the known misstatement from the evidence

A)divide the likely misstatement by the projected misstatement

B)subtract the likely misstatement from the projected misstatement

C)add the projected misstatement to the likely misstatement

D)perform the audit procedure as specified in the audit program and determine the known misstatement from the evidence

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 72 في هذه المجموعة.

فتح الحزمة

k this deck

70

What does it mean to say that an auditor uses statistical or nonstatistical sampling?

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 72 في هذه المجموعة.

فتح الحزمة

k this deck

71

Tolerable misstatement is

A)a matter of professional judgment

B)the amount of misstatement,on the basis of the auditor's professional judgment,that should be present in the account balance or class of transactions

C)the maximum misstatement in the account balance or class of transactions that the auditor is willing to accept

D)the level of audit risk the auditor is willing to accept

E)both A and C

F)both B and D

G)both D and E

A)a matter of professional judgment

B)the amount of misstatement,on the basis of the auditor's professional judgment,that should be present in the account balance or class of transactions

C)the maximum misstatement in the account balance or class of transactions that the auditor is willing to accept

D)the level of audit risk the auditor is willing to accept

E)both A and C

F)both B and D

G)both D and E

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 72 في هذه المجموعة.

فتح الحزمة

k this deck

72

How is variables sampling used in substantive testing?

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 72 في هذه المجموعة.

فتح الحزمة

k this deck

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 72 في هذه المجموعة.