Deck 16: Consolidation: Wholly Owned Subsidiaries

ملء الشاشة (f)

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

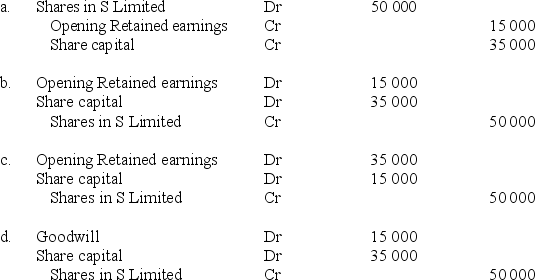

On 1 July 20X6,P Limited acquired all the issued shares of S Limited for $50 000 when the equity of S Limited consisted of:

The pre-acquisition entry at 1 July 20X6 is:

The pre-acquisition entry at 1 July 20X6 is:

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

فتح الحزمة

قم بالتسجيل لفتح البطاقات في هذه المجموعة!

Unlock Deck

Unlock Deck

1/24

العب

ملء الشاشة (f)

Deck 16: Consolidation: Wholly Owned Subsidiaries

1

If the cost of a business combination is greater than the acquired interest in the net fair value of the identifiable assets,liabilities and contingent liabilities of the acquiree:

A)a gain on bargain purchase results

B)goodwill has been purchased and must be recognised

C)the difference is treated as a special equity reserve in the acquirer's accounting records

D)the difference is treated as a loss and immediately charged to profit or loss of the period in which the business combination occurred.

A)a gain on bargain purchase results

B)goodwill has been purchased and must be recognised

C)the difference is treated as a special equity reserve in the acquirer's accounting records

D)the difference is treated as a loss and immediately charged to profit or loss of the period in which the business combination occurred.

B

2

Eeny Limited has two subsidiary entities,Meeny Limited and Miney Limited.Eeny Limited owns 100% of the shares in both entities.Details of issued share capital are:

-Eeny Limited $100 000

-Meeny Limited $30 000

-Miney Limited $15 000

The consolidated share capital amount of the Eeny Meeny Miney group is:

A)$45 000

B)$55 000

C)$100 000

D)$145 000.

-Eeny Limited $100 000

-Meeny Limited $30 000

-Miney Limited $15 000

The consolidated share capital amount of the Eeny Meeny Miney group is:

A)$45 000

B)$55 000

C)$100 000

D)$145 000.

$100 000

3

The key principle relating to the disclosure of information about business combinations is to disclose information that:

A)enables users to evaluate the nature and financial effect of business combinations that occurred during the period

B)enables the preparation of the consolidated financial statements in the most cost-effective manner

C)does not give an advantage to the competitors of a business group

D)provides users with information about the parent entity only.

A)enables users to evaluate the nature and financial effect of business combinations that occurred during the period

B)enables the preparation of the consolidated financial statements in the most cost-effective manner

C)does not give an advantage to the competitors of a business group

D)provides users with information about the parent entity only.

A

4

At the date of acquisition a subsidiary had recorded a dividend payable of $10 000.The consolidation adjustment needed at the date of acquisition in relation to this event is:

A)DR Dividend payable $10 000 CR Dividend receivable $10 000

B)DR Dividend revenue $10 000 CR Dividend declared $10 000

C)DR Shares in subsidiary $10 000 CR Dividend receivable $10 000

D)DR Cash $10 000 CR Shares in subsidiary $10 000.

A)DR Dividend payable $10 000 CR Dividend receivable $10 000

B)DR Dividend revenue $10 000 CR Dividend declared $10 000

C)DR Shares in subsidiary $10 000 CR Dividend receivable $10 000

D)DR Cash $10 000 CR Shares in subsidiary $10 000.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 24 في هذه المجموعة.

فتح الحزمة

k this deck

5

In a business combination the revaluation of non-current assets in the records of the subsidiary means that the subsidiary has effectively adopted the:

A)parent-entity model of consolidation

B)proprietary model of accounting

C)cost model of accounting

D)revaluation model of accounting.

A)parent-entity model of consolidation

B)proprietary model of accounting

C)cost model of accounting

D)revaluation model of accounting.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 24 في هذه المجموعة.

فتح الحزمة

k this deck

6

On 1 July 20X6 Possum acquired a 100% interest in Echidna.At that time Echidna had goodwill of $5 000 recorded in its statement of financial position as a result of a previous business combination.The total goodwill arising on Possum's acquisition of Echidna was $12,000.The goodwill recognised on consolidation as a result of Possum's acquisition of Echidna is:

A)nil

B)$5 000

C)$7 000

D)$12 000

A)nil

B)$5 000

C)$7 000

D)$12 000

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 24 في هذه المجموعة.

فتح الحزمة

k this deck

7

When a parent entity has previously held an investment in a subsidiary prior to gaining control the effect on the consolidation process is as follows:

A)there is no impact

B)the change in the fair value of the previously held interest is recognised in profit or loss

C)the change in the fair value of the previously held interest is recognised in retained earnings

D)the change in the fair value of the previously held interest is recognised in other comprehensive income

A)there is no impact

B)the change in the fair value of the previously held interest is recognised in profit or loss

C)the change in the fair value of the previously held interest is recognised in retained earnings

D)the change in the fair value of the previously held interest is recognised in other comprehensive income

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 24 في هذه المجموعة.

فتح الحزمة

k this deck

8

When preparing consolidated financial statements,adjustments for pre-acquisition equity and inter-entity transactions are recorded:

A)in the accounting records of the parent entity

B)in the accounting records of the subsidiary

C)on a consolidation worksheet

D)in the accounting records of the reporting entity.

A)in the accounting records of the parent entity

B)in the accounting records of the subsidiary

C)on a consolidation worksheet

D)in the accounting records of the reporting entity.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 24 في هذه المجموعة.

فتح الحزمة

k this deck

9

In relation to pre-acquisition of a subsidiary entity,which of the following events can cause a change in the pre-acquisition entry subsequent to acquisition date?

I Transfers from post-acquisition retained earnings

II Dividends paid from pre-acquisition reserves

III Transfers from pre-acquisition retained earnings

IV Impairment of goodwill

A)I,II,III and IV

B)I,III and IV only

C)II and III only

D)III and IV only.

I Transfers from post-acquisition retained earnings

II Dividends paid from pre-acquisition reserves

III Transfers from pre-acquisition retained earnings

IV Impairment of goodwill

A)I,II,III and IV

B)I,III and IV only

C)II and III only

D)III and IV only.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 24 في هذه المجموعة.

فتح الحزمة

k this deck

10

Parent Limited acquired 100% of a subsidiary on 1 July 20X7.At acquisition date the subsidiary had the following equity items:

-Retained earnings $24 000

-Share capital $33 000

-Business combination revaluation reserve $10 000

In the year following the acquisition the subsidiary paid a bonus dividend of $14 000 out of pre-acquisition retained earnings.The following consolidation adjustment is needed in the consolidation worksheet for 30 June 20X8:

A)DR Share capital $14 000 CR Bonus dividend paid $14 000

B)DR Shares in subsidiary 14 000 CR Share capital $14 000

C)DR Bonus dividend paid $14 000 CR Retained earnings $14 000

D)DR Retained earnings $14 000 CR Share capital $14 000.

-Retained earnings $24 000

-Share capital $33 000

-Business combination revaluation reserve $10 000

In the year following the acquisition the subsidiary paid a bonus dividend of $14 000 out of pre-acquisition retained earnings.The following consolidation adjustment is needed in the consolidation worksheet for 30 June 20X8:

A)DR Share capital $14 000 CR Bonus dividend paid $14 000

B)DR Shares in subsidiary 14 000 CR Share capital $14 000

C)DR Bonus dividend paid $14 000 CR Retained earnings $14 000

D)DR Retained earnings $14 000 CR Share capital $14 000.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 24 في هذه المجموعة.

فتح الحزمة

k this deck

11

One year after acquisition date,the goodwill acquired was regarded as having become impaired by $20 000.The appropriate consolidation adjustment in relation to the impairment will include the following line:

A)DR Goodwill $20 000

B)DR Share capital $20 000

C)CR Business combination valuation reserve $20 000

D)CR Accumulated impairment losses $20 000.

A)DR Goodwill $20 000

B)DR Share capital $20 000

C)CR Business combination valuation reserve $20 000

D)CR Accumulated impairment losses $20 000.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 24 في هذه المجموعة.

فتح الحزمة

k this deck

12

A Limited acquired B Limited for $110 000.At acquisition date the fair value of the B Limited's Land asset was $40 000 and the book value was $30 000.If the company tax rate is 30%,which of the following is the appropriate adjustment to recognise the tax effect of the business combination revaluation of land?

A)DR Deferred tax liability $3 000

B)CR Deferred tax liability $3 000

C)DR Deferred tax asset $3 000

D)CR Deferred tax asset $3 000.

A)DR Deferred tax liability $3 000

B)CR Deferred tax liability $3 000

C)DR Deferred tax asset $3 000

D)CR Deferred tax asset $3 000.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 24 في هذه المجموعة.

فتح الحزمة

k this deck

13

On 1 July 20X6,P Limited acquired all the issued shares of S Limited for $50 000 when the equity of S Limited consisted of:

The pre-acquisition entry at 1 July 20X6 is:

The pre-acquisition entry at 1 July 20X6 is:

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 24 في هذه المجموعة.

فتح الحزمة

k this deck

14

Company X acquired Company Y when the carrying value of Company Y's plant was $50 000.The fair value of the plant on acquisition date was $65 000.The company tax rate was 30%.How much is the amount of the business combination valuation reserve that must be recognised?

A)$3 500

B)$10 500

C)$15 000

D)$65 000

A)$3 500

B)$10 500

C)$15 000

D)$65 000

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 24 في هذه المجموعة.

فتح الحزمة

k this deck

15

On 1 January 20X2 A Ltd acquired all the issued shares in B Ltd.At that date the inventory of B Ltd had a carrying amount of $5 000 less than its fair value.The inventory was all sold by 30 June 20X4.At 30 June 20X5 the consolidation adjustment against inventory in relation to the transaction will be:

A)a debit of $5 000

B)a credit of $5 000

C)a debit of $3 500

D)nothing

A)a debit of $5 000

B)a credit of $5 000

C)a debit of $3 500

D)nothing

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 24 في هذه المجموعة.

فتح الحزمة

k this deck

16

Entity A and Entity B agree to merge.The capital structure of each entity is:

Entity A - 100 ordinary shares

Entity B - 60 ordinary shares

Entity A issues 2.5 shares in exchange for each ordinary share of Entity B.All of Entity B's shareholders exchange their shares for Entity A shares.

Which of the following statement is correct?

A)Entity A is both the parent and the acquirer in the transaction.

B)Entity B is both the parent and the acquirer in the transaction.

C)Entity A is the parent and Entity B is the acquirer in the transaction.

D)Entity B is the parent and Entity A is the acquirer in the transaction.

Entity A - 100 ordinary shares

Entity B - 60 ordinary shares

Entity A issues 2.5 shares in exchange for each ordinary share of Entity B.All of Entity B's shareholders exchange their shares for Entity A shares.

Which of the following statement is correct?

A)Entity A is both the parent and the acquirer in the transaction.

B)Entity B is both the parent and the acquirer in the transaction.

C)Entity A is the parent and Entity B is the acquirer in the transaction.

D)Entity B is the parent and Entity A is the acquirer in the transaction.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 24 في هذه المجموعة.

فتح الحزمة

k this deck

17

At acquisition date a wholly owned subsidiary had the following equity items:

-Retained earnings $14 000

-Share capital $30 000

-Business combination revaluation reserve $6000

In the year following the acquisition the subsidiary transferred $10 000 from pre-acquisition retained earnings,to a general reserve account.At the reporting date following the reserve transfer,the following consolidation adjustment is needed:

A)DR Retained earnings $10 000 CR General reserve $10 000

B)DR General reserve $10 000 CR Shares in subsidiary $10 000

C)DR Shares in subsidiary $10 000 CR Retained earnings $10 000

D)DR General reserve $10 000 CR Retained earnings $10 000.

-Retained earnings $14 000

-Share capital $30 000

-Business combination revaluation reserve $6000

In the year following the acquisition the subsidiary transferred $10 000 from pre-acquisition retained earnings,to a general reserve account.At the reporting date following the reserve transfer,the following consolidation adjustment is needed:

A)DR Retained earnings $10 000 CR General reserve $10 000

B)DR General reserve $10 000 CR Shares in subsidiary $10 000

C)DR Shares in subsidiary $10 000 CR Retained earnings $10 000

D)DR General reserve $10 000 CR Retained earnings $10 000.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 24 في هذه المجموعة.

فتح الحزمة

k this deck

18

Nelson Limited has two subsidiary entities,Poggi Limited and Holly Limited.Nelson Limited owns 100% of the shares in both entities.Details of issued share capital are:

-Nelson Limited $100 000

-Poggi Limited $30 000

-Holly Limited $15 000

The worksheet adjustment entry made in order to determine the amount of consolidated share capital is:

A)DR Share capital $145 000 CR Shares in subsidiaries $145 000

B)DR Share capital $100 000 CR Shares in subsidiaries $100 000

C)DR Share capital $45 000 CR Shares in Poggi Limited $30 000

CR Shares in Holly Limited $15 000

D)DR Share capital $145 000 CR Shares in Nelson Limited $100 000

CR Shares in Poggi Limited $30 000

CR Shares in Holly Limited $15 000

-Nelson Limited $100 000

-Poggi Limited $30 000

-Holly Limited $15 000

The worksheet adjustment entry made in order to determine the amount of consolidated share capital is:

A)DR Share capital $145 000 CR Shares in subsidiaries $145 000

B)DR Share capital $100 000 CR Shares in subsidiaries $100 000

C)DR Share capital $45 000 CR Shares in Poggi Limited $30 000

CR Shares in Holly Limited $15 000

D)DR Share capital $145 000 CR Shares in Nelson Limited $100 000

CR Shares in Poggi Limited $30 000

CR Shares in Holly Limited $15 000

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 24 في هذه المجموعة.

فتح الحزمة

k this deck

19

For entities wanting to use the cost model of accounting,the revaluation of a subsidiary's assets would be undertaken in the:

A)subsidiary's records

B)parent entity's records

C)consolidation worksheet

D)notes to the consolidated financial statements.

A)subsidiary's records

B)parent entity's records

C)consolidation worksheet

D)notes to the consolidated financial statements.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 24 في هذه المجموعة.

فتح الحزمة

k this deck

20

If a subsidiary's reporting date does not coincide with the parent entity's reporting date,adjustments must be made for the effects of significant events that occur between the two reporting dates as long as the reporting dates differ by no more than:

A)one month

B)three months

C)four months

D)six months

A)one month

B)three months

C)four months

D)six months

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 24 في هذه المجموعة.

فتح الحزمة

k this deck

21

Explain how consolidated financial statements are prepared.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 24 في هذه المجموعة.

فتح الحزمة

k this deck

22

Explain the function of a consolidation worksheet.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 24 في هذه المجموعة.

فتح الحزمة

k this deck

23

Explain why revaluations of the assets of a subsidiary at acquisition date are normally recorded in the consolidation worksheet and not in the accounting records of the subsidiary.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 24 في هذه المجموعة.

فتح الحزمة

k this deck

24

What is the purpose of preparing an acquisition analysis?

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 24 في هذه المجموعة.

فتح الحزمة

k this deck

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 24 في هذه المجموعة.