Deck 6: Inventories and Cost of Sales

ملء الشاشة (f)

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

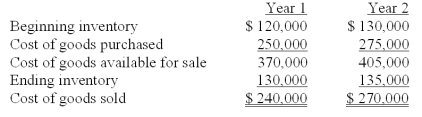

Thelma Company reported cost of goods sold for Year 1 and Year 2 as follows:  Thelma Company made two errors: 1) ending inventory at the end of Year 1 was understated by $15,000 and 2) ending inventory at the end of Year 2 was overstated by $6,000. Given this information, the correct cost of goods sold figure for Year 2 would be:

Thelma Company made two errors: 1) ending inventory at the end of Year 1 was understated by $15,000 and 2) ending inventory at the end of Year 2 was overstated by $6,000. Given this information, the correct cost of goods sold figure for Year 2 would be:

A) $291,000

B) $276,000

C) $264,000

D) $285,000

E) $249,000

Thelma Company made two errors: 1) ending inventory at the end of Year 1 was understated by $15,000 and 2) ending inventory at the end of Year 2 was overstated by $6,000. Given this information, the correct cost of goods sold figure for Year 2 would be:A) $291,000

B) $276,000

C) $264,000

D) $285,000

E) $249,000

سؤال

سؤال

سؤال

فتح الحزمة

قم بالتسجيل لفتح البطاقات في هذه المجموعة!

Unlock Deck

Unlock Deck

1/198

العب

ملء الشاشة (f)

Deck 6: Inventories and Cost of Sales

1

If obsolete or damaged goods can be sold, they will be included in inventory at their net realizable value.

True

2

The full disclosure principle requires that the notes to the financial statements report a change in accounting method for inventory.

True

3

When taking a physical count of inventory, the use of prenumbered inventory tickets is an application of internal control.

True

4

The cost of an inventory item includes its invoice cost minus any discount, and plus any added or incidental costs necessary to put it in a place and condition for sale.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 198 في هذه المجموعة.

فتح الحزمة

k this deck

5

LIFO is preferred when purchase costs are rising and managers have incentives to report higher income for reasons such as bonus plans, job security, and reputation.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 198 في هذه المجموعة.

فتح الحزمة

k this deck

6

The matching principle is used by some companies to avoid allocating incidental inventory costs to cost of goods sold.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 198 في هذه المجموعة.

فتح الحزمة

k this deck

7

In a period of rising purchase costs, FIFO usually gives a lower taxable income and therefore, yields a tax advantage.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 198 في هذه المجموعة.

فتح الحزمة

k this deck

8

An advantage of LIFO is that it assigns the most recent costs to cost of goods sold, and does a better job of matching current costs with revenues on the income statement.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 198 في هذه المجموعة.

فتح الحزمة

k this deck

9

The LIFO method of inventory valuation can result in a company's ending inventory being valued at less than the inventory's replacement cost because LIFO inventory leaves the oldest costs in inventory.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 198 في هذه المجموعة.

فتح الحزمة

k this deck

10

Few companies take a physical count of inventory each year, and rely on inventory records alone to determine the inventory value.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 198 في هذه المجموعة.

فتح الحزمة

k this deck

11

An advantage of the weighted average inventory method is that it tends to smooth out erratic changes in costs.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 198 في هذه المجموعة.

فتح الحزمة

k this deck

12

Whether purchase costs are rising or falling, FIFO always will yield the highest gross profit and net income.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 198 في هذه المجموعة.

فتح الحزمة

k this deck

13

Incidental costs often added to the costs of inventory include import duties, freight, storage, and insurance.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 198 في هذه المجموعة.

فتح الحزمة

k this deck

14

The Inventory account is a controlling account for the inventory subsidiary ledger that contains a separate record for each separate product.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 198 في هذه المجموعة.

فتح الحزمة

k this deck

15

Net realizable value for damaged or obsolete goods is sales price plus the cost of making the sale.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 198 في هذه المجموعة.

فتح الحزمة

k this deck

16

Goods on consignment are goods shipped by their owner, called the consignee, to another party called the consignor.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 198 في هذه المجموعة.

فتح الحزمة

k this deck

17

The consistency concept prescribes that a company use the same accounting methods period after period, so that financial statements are comparable across periods.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 198 في هذه المجموعة.

فتح الحزمة

k this deck

18

A company can change its inventory costing method without mentioning this change in its financial statements because it is an internal management decision.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 198 في هذه المجموعة.

فتح الحزمة

k this deck

19

Goods in transit are automatically included in inventory.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 198 في هذه المجموعة.

فتح الحزمة

k this deck

20

If the seller is responsible for paying freight charges, then ownership of inventory passes when goods arrive at their destination.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 198 في هذه المجموعة.

فتح الحزمة

k this deck

21

An understatement of ending inventory will cause an understatement of assets and equity on the balance sheet.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 198 في هذه المجموعة.

فتح الحزمة

k this deck

22

A company's cost of goods sold was $15,500 and its average merchandise inventory was $4,500. Its inventory turnover equals 3.4.

15,500/4,500 = 3.4

15,500/4,500 = 3.4

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 198 في هذه المجموعة.

فتح الحزمة

k this deck

23

It can be expected that companies selling perishable goods have a higher inventory turnover than companies selling nonperishable goods.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 198 في هذه المجموعة.

فتح الحزمة

k this deck

24

When units are purchased at different costs over time, determining the cost per unit assigned to inventory items is simple.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 198 في هذه المجموعة.

فتح الحزمة

k this deck

25

The inventory turnover ratio is computed by dividing average merchandise inventory by cost of goods sold.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 198 في هذه المجموعة.

فتح الحزمة

k this deck

26

A merchandiser's ability to pay its short-term obligations depends on many factors including how quickly it sells its merchandise inventory.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 198 في هذه المجموعة.

فتح الحزمة

k this deck

27

LIFO assumes that inventory costs flow in the order incurred.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 198 في هذه المجموعة.

فتح الحزمة

k this deck

28

Errors in the period-end inventory balance only affect the current period's records and financial statements.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 198 في هذه المجموعة.

فتح الحزمة

k this deck

29

The FIFO inventory method assumes that costs for the earliest units purchased are the first to be charged to the cost of goods sold.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 198 في هذه المجموعة.

فتح الحزمة

k this deck

30

There is no simple rule for inventory turnover, except that a high ratio is preferable provided inventory is adequate to meet demand.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 198 في هذه المجموعة.

فتح الحزمة

k this deck

31

An inventory error is sometimes said to be self-correcting because it causes an offsetting error in the next period.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 198 في هذه المجموعة.

فتح الحزمة

k this deck

32

One of the most important decisions in accounting for inventory is determining the unit costs assigned to inventory items.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 198 في هذه المجموعة.

فتح الحزمة

k this deck

33

Companies are allowed to use FIFO for financial reporting and LIFO for tax reporting, according to IRS requirements.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 198 في هذه المجموعة.

فتح الحزمة

k this deck

34

An understatement of the ending inventory balance will understate cost of goods sold and overstate net income.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 198 في هذه المجموعة.

فتح الحزمة

k this deck

35

The assignment of costs to cost of goods sold and inventory using weighted average usually yields different results depending on whether a perpetual or periodic system is used.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 198 في هذه المجموعة.

فتح الحزمة

k this deck

36

Tops had cost of goods sold of $8,321 million and its ending inventory was $2,027 million. Therefore its days' sales in inventory equals 89 days.

2,027/8,321*365 = 89

2,027/8,321*365 = 89

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 198 في هذه المجموعة.

فتح الحزمة

k this deck

37

An overstatement of ending inventory will cause an overstatement of assets and an understatement of equity on the balance sheet.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 198 في هذه المجموعة.

فتح الحزمة

k this deck

38

The days' sales in inventory ratio is computed by dividing ending inventory by cost of goods sold and multiplying the result by 365.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 198 في هذه المجموعة.

فتح الحزمة

k this deck

39

An error in the period-end inventory balance will cause an error in the calculation of cost of goods sold.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 198 في هذه المجموعة.

فتح الحزمة

k this deck

40

An understatement of the beginning inventory balance will understate cost of goods sold and overstate net income.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 198 في هذه المجموعة.

فتح الحزمة

k this deck

41

In the retail inventory method of inventory valuation, the retail amount of inventory refers to its dollar amount measured using selling prices of inventory items.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 198 في هذه المجموعة.

فتح الحزمة

k this deck

42

The reasoning behind the retail inventory method is that if we can get a good estimate of the cost-to-retail ratio, we can multiply ending inventory at retail by this ratio to estimate ending inventory at cost.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 198 في هذه المجموعة.

فتح الحزمة

k this deck

43

The assignment of costs to the cost of goods sold and to ending inventory using FIFO is the same for both the perpetual and periodic inventory systems.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 198 في هذه المجموعة.

فتح الحزمة

k this deck

44

Damaged and obsolete goods that can be sold:

A) Are never counted as inventory.

B) Are included in inventory at their full cost.

C) Are included in inventory at their net realizable value.

D) Should be disposed of immediately.

E) Are assigned a value of zero.

A) Are never counted as inventory.

B) Are included in inventory at their full cost.

C) Are included in inventory at their net realizable value.

D) Should be disposed of immediately.

E) Are assigned a value of zero.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 198 في هذه المجموعة.

فتح الحزمة

k this deck

45

The lower of cost or market rule for inventory valuation must be applied to each individual unit separately, and not to major categories of inventory or to the entire inventory.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 198 في هذه المجموعة.

فتح الحزمة

k this deck

46

Under LIFO, the most recent costs are assigned to ending inventory.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 198 في هذه المجموعة.

فتح الحزمة

k this deck

47

The retail inventory method estimates the cost of ending inventory by applying the gross profit ratio to net sales.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 198 في هذه المجموعة.

فتح الحزمة

k this deck

48

In applying the lower of cost or market method to inventory valuation, market is defined as the current selling price.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 198 في هذه المجموعة.

فتح الحزمة

k this deck

49

Merchandise inventory includes:

A) All goods owned by a company and held for sale.

B) All goods in transit.

C) All goods on consignment.

D) Only damaged goods.

E) Only non-damaged goods.

A) All goods owned by a company and held for sale.

B) All goods in transit.

C) All goods on consignment.

D) Only damaged goods.

E) Only non-damaged goods.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 198 في هذه المجموعة.

فتح الحزمة

k this deck

50

Using the retail inventory method, if the cost to retail ratio is 60% and ending inventory at retail is $45,000, then estimated ending inventory at cost is $27,000.

$45,000 * .60 = $27,000

$45,000 * .60 = $27,000

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 198 في هذه المجموعة.

فتح الحزمة

k this deck

51

The conservatism constraint requires that when more than one estimate of the amounts to be received or paid in the future exists and these estimates are about equally likely, then the less optimistic amount is used.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 198 في هذه المجموعة.

فتح الحزمة

k this deck

52

The choice of an inventory valuation method can have a major impact on gross profit and cost of sales.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 198 في هذه المجموعة.

فتح الحزمة

k this deck

53

In applying the lower of cost or market method to inventory valuation, market is defined as the current replacement cost.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 198 في هذه المجموعة.

فتح الحزمة

k this deck

54

The costs of goods purchased will vary under the different inventory methods of specific identification, FIFO, LIFO, and weighted average.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 198 في هذه المجموعة.

فتح الحزمة

k this deck

55

A company's total cost of inventory was $305,000 and its market value is $297,000. Under the lower cost or market, the amount reported should be $305,000.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 198 في هذه المجموعة.

فتح الحزمة

k this deck

56

To avoid the time-consuming process of taking an inventory each year, most companies use the gross profit method to estimate ending inventory.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 198 في هذه المجموعة.

فتح الحزمة

k this deck

57

A company has inventory with a market value of $217,000 and a cost of $241,000. According to the lower of cost or market, the inventory should be written down to $217,000.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 198 في هذه المجموعة.

فتح الحزمة

k this deck

58

The reliability of the gross profit method depends on a good estimate of the gross profit ratio.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 198 في هذه المجموعة.

فتح الحزمة

k this deck

59

When LIFO is used with the periodic inventory system, cost of goods sold is assigned costs from the most recent purchases at the point of each sale, rather than from the most recent purchases for the period.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 198 في هذه المجموعة.

فتح الحزمة

k this deck

60

A company's cost of inventory was $317,500. Due to phenomenal demand the market value of its inventory increased to $323,000. This company should write up the value of its inventory according to the consistency principle.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 198 في هذه المجموعة.

فتح الحزمة

k this deck

61

Goods on consignment:

A) Are goods shipped by the owner to the consignee who sells the goods for the owner.

B) Are reported in the consignee's books as inventory.

C) Are goods shipped to the consignor who sells the goods for the owner.

D) Are not reported in the consignor's inventory since they do not have possession of the inventory.

E) Are always paid for by the consignee when they take possession.

A) Are goods shipped by the owner to the consignee who sells the goods for the owner.

B) Are reported in the consignee's books as inventory.

C) Are goods shipped to the consignor who sells the goods for the owner.

D) Are not reported in the consignor's inventory since they do not have possession of the inventory.

E) Are always paid for by the consignee when they take possession.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 198 في هذه المجموعة.

فتح الحزمة

k this deck

62

Internal controls that should be applied when a business takes a physical count of inventory should include all of the following except:

A) Prenumbered inventory tickets.

B) A manager does not confirm that all inventories are ticketed once, and only once.

C) Counters must confirm the validity of inventory existence, amounts, and quality.

D) Second counts by a different counter.

E) Counters of inventory should not be those who are responsible for the inventory.

A) Prenumbered inventory tickets.

B) A manager does not confirm that all inventories are ticketed once, and only once.

C) Counters must confirm the validity of inventory existence, amounts, and quality.

D) Second counts by a different counter.

E) Counters of inventory should not be those who are responsible for the inventory.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 198 في هذه المجموعة.

فتح الحزمة

k this deck

63

If a period-end inventory amount is reported in error, it can cause a misstatement in all of the following except:

A) Cost of goods sold.

B) Gross profit.

C) Net sales.

D) Current assets.

E) Net income.

A) Cost of goods sold.

B) Gross profit.

C) Net sales.

D) Current assets.

E) Net income.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 198 في هذه المجموعة.

فتح الحزمة

k this deck

64

The full disclosure principle:

A) Prescribes that when a change in inventory valuation method is made, the notes to the statements report the type of change, its justification and its effect on net income.

B) Requires that companies use the same accounting method for inventory valuation period after period.

C) Is not subject to the materiality principle.

D) Is only applied to retailers.

E) Is also called the consistency principle.

A) Prescribes that when a change in inventory valuation method is made, the notes to the statements report the type of change, its justification and its effect on net income.

B) Requires that companies use the same accounting method for inventory valuation period after period.

C) Is not subject to the materiality principle.

D) Is only applied to retailers.

E) Is also called the consistency principle.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 198 في هذه المجموعة.

فتح الحزمة

k this deck

65

The understatement of the ending inventory balance causes:

A) Cost of goods sold to be overstated and net income to be understated.

B) Cost of goods sold to be overstated and net income to be overstated.

C) Cost of goods sold to be understated and net income to be understated.

D) Cost of goods sold to be understated and net income to be overstated.

E) Cost of goods sold to be overstated and net income to be correct.

A) Cost of goods sold to be overstated and net income to be understated.

B) Cost of goods sold to be overstated and net income to be overstated.

C) Cost of goods sold to be understated and net income to be understated.

D) Cost of goods sold to be understated and net income to be overstated.

E) Cost of goods sold to be overstated and net income to be correct.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 198 في هذه المجموعة.

فتح الحزمة

k this deck

66

Regardless of the inventory costing system used, cost of goods available for sale must be allocated between

A) beginning inventory and net purchases during the period.

B) ending inventory and beginning inventory.

C) net purchases during the period and ending inventory.

D) ending inventory and cost of goods sold.

E) beginning inventory and cost of goods sold.

A) beginning inventory and net purchases during the period.

B) ending inventory and beginning inventory.

C) net purchases during the period and ending inventory.

D) ending inventory and cost of goods sold.

E) beginning inventory and cost of goods sold.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 198 في هذه المجموعة.

فتح الحزمة

k this deck

67

The inventory valuation method that has the advantages of assigning an amount to inventory on the balance sheet that approximates its current cost, and also mimics the actual flow of goods for most businesses is:

A) FIFO.

B) Weighted average.

C) LIFO.

D) Specific identification.

E) All of these.

A) FIFO.

B) Weighted average.

C) LIFO.

D) Specific identification.

E) All of these.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 198 في هذه المجموعة.

فتح الحزمة

k this deck

68

The inventory valuation method that tends to smooth out erratic changes in costs is:

A) FIFO.

B) Weighted average.

C) LIFO.

D) Specific identification.

E) WIFO.

A) FIFO.

B) Weighted average.

C) LIFO.

D) Specific identification.

E) WIFO.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 198 في هذه المجموعة.

فتح الحزمة

k this deck

69

Gotham Company reported a December 31 ending inventory balance of $412,000. The following additional information is also available: The ending inventory balance of $412,000 included $72,000 of consigned inventory for which Gotham was the consignor.

The ending inventory balance of $412,000 included $22,000 of office supplies that were stored in the warehouse and were to be used by the company's supervisors and managers during the coming year.

The ending inventory balance of $412,000 did not include goods costing $48,000 that were purchased by Gotham on December 28 and shipped FOB destination on that date. Gotham did not receive the goods until January 2 of the following year.

The ending inventory balance of $412,000 included damaged goods at their original cost of $38,000. The net realizable value of the damaged goods was $10,000.

The ending inventory balance of $412,000 included $43,000 of consigned inventory for which Gotham was the consignee.

Based on this information, the correct balance for ending inventory on December 31 is:

A) $247,000

B) $341,000

C) $362,000

D) $309,000

E) $319,000

The ending inventory balance of $412,000 included $22,000 of office supplies that were stored in the warehouse and were to be used by the company's supervisors and managers during the coming year.

The ending inventory balance of $412,000 did not include goods costing $48,000 that were purchased by Gotham on December 28 and shipped FOB destination on that date. Gotham did not receive the goods until January 2 of the following year.

The ending inventory balance of $412,000 included damaged goods at their original cost of $38,000. The net realizable value of the damaged goods was $10,000.

The ending inventory balance of $412,000 included $43,000 of consigned inventory for which Gotham was the consignee.

Based on this information, the correct balance for ending inventory on December 31 is:

A) $247,000

B) $341,000

C) $362,000

D) $309,000

E) $319,000

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 198 في هذه المجموعة.

فتح الحزمة

k this deck

70

The understatement of the beginning inventory balance causes:

A) Cost of goods sold to be understated and net income to be understated.

B) Cost of goods sold to be understated and net income to be overstated.

C) Cost of goods sold to be overstated and net income to be overstated.

D) Cost of goods sold to be overstated and net income to be understated.

E) Cost of goods sold to be overstated and net income to be correct.

A) Cost of goods sold to be understated and net income to be understated.

B) Cost of goods sold to be understated and net income to be overstated.

C) Cost of goods sold to be overstated and net income to be overstated.

D) Cost of goods sold to be overstated and net income to be understated.

E) Cost of goods sold to be overstated and net income to be correct.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 198 في هذه المجموعة.

فتح الحزمة

k this deck

71

Which of the following inventory costing methods will always result in the same values for ending inventory and cost of goods sold regardless of whether a perpetual or periodic inventory system is used?

A) FIFO and LIFO

B) LIFO and weighted-average cost

C) Specific identification and FIFO

D) FIFO and weighted-average cost

E) LIFO and specific identification

A) FIFO and LIFO

B) LIFO and weighted-average cost

C) Specific identification and FIFO

D) FIFO and weighted-average cost

E) LIFO and specific identification

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 198 في هذه المجموعة.

فتح الحزمة

k this deck

72

The consistency concept:

A) Prescribes a company to consistently apply the same accounting method of inventory valuation, an exception being when a change from one method to another will improve its financial reporting.

B) Requires a company to use one method of inventory valuation exclusively.

C) Requires that all companies in the same industry use the same accounting methods of inventory valuation.

D) Is also called the full disclosure principle.

E) Is also called the matching principle.

A) Prescribes a company to consistently apply the same accounting method of inventory valuation, an exception being when a change from one method to another will improve its financial reporting.

B) Requires a company to use one method of inventory valuation exclusively.

C) Requires that all companies in the same industry use the same accounting methods of inventory valuation.

D) Is also called the full disclosure principle.

E) Is also called the matching principle.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 198 في هذه المجموعة.

فتح الحزمة

k this deck

73

An error in the period-end inventory causes an offsetting error in the next period and therefore:

A) Managers can ignore the error.

B) It is sometimes said to be self-correcting.

C) It affects only income statement accounts.

D) If affects only balance sheet accounts.

E) Is immaterial for managerial decision making.

A) Managers can ignore the error.

B) It is sometimes said to be self-correcting.

C) It affects only income statement accounts.

D) If affects only balance sheet accounts.

E) Is immaterial for managerial decision making.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 198 في هذه المجموعة.

فتح الحزمة

k this deck

74

Physical counts of inventory:

A) Are not necessary under the perpetual system.

B) Are necessary to adjust the Inventory account to the actual inventory available.

C) Must be taken at least once a month.

D) Requires the use of hand-held portable computers.

E) Are not necessary under the cost-to benefit constraint.

A) Are not necessary under the perpetual system.

B) Are necessary to adjust the Inventory account to the actual inventory available.

C) Must be taken at least once a month.

D) Requires the use of hand-held portable computers.

E) Are not necessary under the cost-to benefit constraint.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 198 في هذه المجموعة.

فتح الحزمة

k this deck

75

Costs included in the Merchandise Inventory account can include all of the following except:

A) Invoice price minus any discount.

B) Transportation-in.

C) Storage.

D) Insurance.

E) Damaged inventory that cannot be sold.

A) Invoice price minus any discount.

B) Transportation-in.

C) Storage.

D) Insurance.

E) Damaged inventory that cannot be sold.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 198 في هذه المجموعة.

فتح الحزمة

k this deck

76

During a period of steadily rising costs, the inventory valuation method that yields the lowest reported net income is:

A) Specific identification method.

B) Average cost method.

C) Weighted-average method.

D) FIFO method.

E) LIFO method.

A) Specific identification method.

B) Average cost method.

C) Weighted-average method.

D) FIFO method.

E) LIFO method.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 198 في هذه المجموعة.

فتح الحزمة

k this deck

77

Thelma Company reported cost of goods sold for Year 1 and Year 2 as follows: Thelma Company made two errors: 1) ending inventory at the end of Year 1 was understated by $15,000 and 2) ending inventory at the end of Year 2 was overstated by $6,000. Given this information, the correct cost of goods sold figure for Year 2 would be:

A) $291,000

B) $276,000

C) $264,000

D) $285,000

E) $249,000

Thelma Company made two errors: 1) ending inventory at the end of Year 1 was understated by $15,000 and 2) ending inventory at the end of Year 2 was overstated by $6,000. Given this information, the correct cost of goods sold figure for Year 2 would be:A) $291,000

B) $276,000

C) $264,000

D) $285,000

E) $249,000

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 198 في هذه المجموعة.

فتح الحزمة

k this deck

78

The inventory valuation method that results in the lowest taxable income in a period of inflation is:

A) LIFO method.

B) FIFO method.

C) Weighted-average cost method.

D) Specific identification method.

E) Gross profit method.

A) LIFO method.

B) FIFO method.

C) Weighted-average cost method.

D) Specific identification method.

E) Gross profit method.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 198 في هذه المجموعة.

فتح الحزمة

k this deck

79

On December 31 of the current year, Hewett Company reported an ending inventory balance of $215,000. The following additional information is also available: Hewett sold goods costing $38,000 to Trump Enterprises on December 28 and shipped the goods on that date with shipping terms of FOB shipping point. The goods were not included in the ending inventory amount of $215,000 because they were not in Hewett's warehouse.

Hewett purchased goods costing $44,000 on December 29. The goods were shipped FOB destination and were received by Hewett on January 2 of the following year. The shipment was a rush order that was supposed to arrive by December 31. These goods were included in the ending inventory balance of $215,000.

Hewett's ending inventory balance of $215,000 included $15,000 of goods being held on consignment from Rumsfeld Company. (Hewett Company is the consignee.)

Hewett's ending inventory balance of $215,000 did not include goods costing $95,000 that were shipped to Hewett on December 27 with shipping terms of FOB destination and were still in transit at year-end.

Based on the above information, the correct balance for ending inventory on December 31 is:

A) $194,000

B) $209,000

C) $200,000

D) $171,000

E) $156,000

Hewett purchased goods costing $44,000 on December 29. The goods were shipped FOB destination and were received by Hewett on January 2 of the following year. The shipment was a rush order that was supposed to arrive by December 31. These goods were included in the ending inventory balance of $215,000.

Hewett's ending inventory balance of $215,000 included $15,000 of goods being held on consignment from Rumsfeld Company. (Hewett Company is the consignee.)

Hewett's ending inventory balance of $215,000 did not include goods costing $95,000 that were shipped to Hewett on December 27 with shipping terms of FOB destination and were still in transit at year-end.

Based on the above information, the correct balance for ending inventory on December 31 is:

A) $194,000

B) $209,000

C) $200,000

D) $171,000

E) $156,000

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 198 في هذه المجموعة.

فتح الحزمة

k this deck

80

Goods in transit are included in a purchaser's inventory:

A) At any time during transit.

B) When the purchaser is responsible for paying freight charges.

C) When the supplier is responsible for freight charges.

D) If the goods are shipped FOB destination.

E) After the half-way point between the buyer and seller.

A) At any time during transit.

B) When the purchaser is responsible for paying freight charges.

C) When the supplier is responsible for freight charges.

D) If the goods are shipped FOB destination.

E) After the half-way point between the buyer and seller.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 198 في هذه المجموعة.

فتح الحزمة

k this deck

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 198 في هذه المجموعة.