Deck 17: Business Tax Credits and Corporate Alternative Minimum Tax

ملء الشاشة (f)

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

Molly has generated general business credits over the years that have not been utilized. The amounts generated and not utilized follow:

In the current year, 2016, her business generates an additional $15,000 general business credit. In 2016, based on her tax liability before credits, she can utilize a general business credit of up to $20,000. After utilizing the carryforwards and the current year credits, how much of the general business credit generated in 2016 is available for future years?

A)$0.

B)$1,000.

C)$14,000.

D)$15,000.

E)None of the above.

In the current year, 2016, her business generates an additional $15,000 general business credit. In 2016, based on her tax liability before credits, she can utilize a general business credit of up to $20,000. After utilizing the carryforwards and the current year credits, how much of the general business credit generated in 2016 is available for future years?

A)$0.

B)$1,000.

C)$14,000.

D)$15,000.

E)None of the above.

سؤال

سؤال

سؤال

سؤال

During the year, Green, Inc., incurs the following research expenditures:

Green's qualifying research expenditures for the year are:

A)$60,000.

B)$75,000.

C)$79,500.

D)$90,000.

E)None of the above.

Green's qualifying research expenditures for the year are:

A)$60,000.

B)$75,000.

C)$79,500.

D)$90,000.

E)None of the above.

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

Lemon, Inc., has the following items related to the AMT:

The corporation's AMT, if any, is:

A)$0.

B)$755,580.

C)$1,868,080.

D)$2,055,100.

E)None of the above.

The corporation's AMT, if any, is:

A)$0.

B)$755,580.

C)$1,868,080.

D)$2,055,100.

E)None of the above.

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

Use the following selected data to calculate Devon's taxable income prior to any personal exemption taken. Devon does not itemize deductions.

سؤال

سؤال

سؤال

سؤال

سؤال

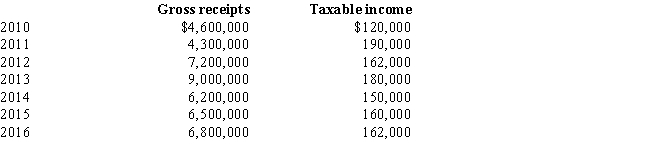

Sage, Inc., has the following gross receipts and taxable income, since its incorporation in 2010.

Is Sage, Inc., subject to the AMT in 2016?

Is Sage, Inc., subject to the AMT in 2016?

سؤال

سؤال

سؤال

سؤال

Mauve, Inc., records the following gross receipts in 2014, 2015, and 2016.

What is Mauve, Inc.'s TMT in each of these three years?

2014 2015 2016

A)$0 $0 $0

B)$0 $0 $1,160,000

C)$0 $1,740,000 $1,160,000

D)$980,000 $1,740,000 $1,160,000

E)$0 $1,740,000) $0

What is Mauve, Inc.'s TMT in each of these three years?

2014 2015 2016

A)$0 $0 $0

B)$0 $0 $1,160,000

C)$0 $1,740,000 $1,160,000

D)$980,000 $1,740,000 $1,160,000

E)$0 $1,740,000) $0

سؤال

سؤال

فتح الحزمة

قم بالتسجيل لفتح البطاقات في هذه المجموعة!

Unlock Deck

Unlock Deck

1/101

العب

ملء الشاشة (f)

Deck 17: Business Tax Credits and Corporate Alternative Minimum Tax

1

The work opportunity tax credit is available only for wages paid to qualifying individuals during their first year of employment.

False

2

The purpose of the tax credit for rehabilitation expenditures is to encourage the relocation of businesses from older, economically distressed areas (i.e., inner city) to newer locations.

False

3

The incremental research activities credit is 20% of the qualified research expenses that exceed the base amount.

True

4

The tax credit for rehabilitation expenditures for certified historic structures differs from that for qualifying structures that are not certified historic structures.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 101 في هذه المجموعة.

فتح الحزمة

k this deck

5

The disabled access credit was enacted to encourage small businesses to make their businesses more accessible to disabled individuals.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 101 في هذه المجموعة.

فتح الحزمة

k this deck

6

All taxpayers are eligible to take the basic research credit.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 101 في هذه المجموعة.

فتح الحزمة

k this deck

7

Some (or all) of the tax credit for rehabilitation expenditures will have to be recaptured if the rehabilitated property is disposed of prematurely or if it ceases to be qualifying property.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 101 في هذه المجموعة.

فتح الحزمة

k this deck

8

An employer's tax deduction for wages is affected by the work opportunity tax credit.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 101 في هذه المجموعة.

فتح الحزمة

k this deck

9

A LIFO method is applied to general business credit carryovers, carrybacks, and utilization of credits earned during a particular year.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 101 في هذه المجموعة.

فتح الحزمة

k this deck

10

A small employer incurs $1,500 for consulting fees related to establishing a qualified retirement plan for its 75 employees. As a result, the employer may claim the credit for small employer pension plan startup costs for $750.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 101 في هذه المجموعة.

فتح الحزمة

k this deck

11

Qualified research and experimentation expenditures are not only eligible for the 20% tax credit, but also can be expensed in the year incurred.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 101 في هذه المجموعة.

فتح الحزمة

k this deck

12

Qualified rehabilitation expenditures include the cost of acquiring the building, but not the cost of acquiring the land.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 101 في هذه المجموعة.

فتح الحزمة

k this deck

13

If a taxpayer is required to recapture any tax credit for rehabilitation expenditures, the recapture amount need not be added to the adjusted basis of the rehabilitation expenditures.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 101 في هذه المجموعة.

فتح الحزمة

k this deck

14

If the cost of a building constructed and placed into service by an eligible small business in the current year includes the cost of a wheelchair ramp, the cost of the ramp qualifies for the disabled access credit.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 101 في هذه المجموعة.

فتح الحزمة

k this deck

15

The tax benefit received from a tax credit is never affected by the tax rate of the taxpayer.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 101 في هذه المجموعة.

فتح الحزمة

k this deck

16

The disabled access credit is computed at the rate of 50% of all access expenditures incurred by the taxpayer during the year.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 101 في هذه المجموعة.

فتح الحزمة

k this deck

17

The purpose of the work opportunity tax credit is to encourage employers to hire individuals from specified target groups traditionally subject to high rates of unemployment.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 101 في هذه المجموعة.

فتح الحزمة

k this deck

18

Any unused general business credit must be carried back 3 years and then forward for 20 years.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 101 في هذه المجموعة.

فتح الحزمة

k this deck

19

Employers are encouraged by the work opportunity tax credit to hire individuals who have been long-term recipients of family assistance welfare benefits.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 101 في هذه المجموعة.

فتح الحزمة

k this deck

20

The tax benefits resulting from tax credits and tax deductions are affected by the tax rate bracket of the taxpayer.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 101 في هذه المجموعة.

فتح الحزمة

k this deck

21

Keosha acquires 10-year personal property to use in her business in 2016 and takes the maximum cost recovery deduction for regular income tax purposes. As a result of this, Keosha will incur a positive AMT adjustment in 2016.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 101 في هذه المجموعة.

فتح الحزمة

k this deck

22

Elmer exercises an incentive stock option (ISO) in 2016 for $6,000 (fair market value of the stock on the exercise date is $7,600). If Elmer sells the stock later in 2016 for $8,000, the AMT positive adjustment is $1,600 and the AMT negative adjustment is $2,000.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 101 في هذه المجموعة.

فتح الحزمة

k this deck

23

All foreign taxes qualify for the foreign tax credit.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 101 في هذه المجموعة.

فتح الحزمة

k this deck

24

Paul incurred circulation expenditures of $180,000 in 2016 and deducted that amount for regular income tax purposes. Paul has a $60,000 negative AMT adjustment for each of 2017, 2018, and for 2019.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 101 في هذه المجموعة.

فتح الحزمة

k this deck

25

Unless circulation expenditures are amortized over a three-year period for regular income tax purposes, there will be an AMT adjustment.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 101 في هذه المجموعة.

فتح الحزمة

k this deck

26

After personal property is fully depreciated for both regular income tax purposes and AMT purposes, the positive and negative adjustments that have been made for AMT purposes will net to zero.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 101 في هذه المجموعة.

فتح الحزمة

k this deck

27

Income from some long-term contracts can be reported using the completed contract method for regular income tax purposes, but the percentage of completion method is required for AMT purposes for all long-term contracts.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 101 في هذه المجموعة.

فتح الحزمة

k this deck

28

The sale of business property might result in an AMT adjustment.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 101 في هذه المجموعة.

فتح الحزمة

k this deck

29

BlueCo incurs $900,000 during the year to construct a facility that will be used exclusively for the care of its employees' pre-school age children during normal working hours. The credit for employer-provided child care available to BlueCo this year is $225,000.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 101 في هذه المجموعة.

فتح الحزمة

k this deck

30

Unused foreign tax credits can be carried back three years and forward fifteen years.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 101 في هذه المجموعة.

فتح الحزمة

k this deck

31

The required adjustment for AMT purposes for pollution control facilities placed in service this year is equal to the difference between the amortization deduction allowed for regular income tax purposes and the depreciation deduction computed under ADS.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 101 في هذه المجموعة.

فتح الحزمة

k this deck

32

Joel placed real property in service in 2016 that cost $900,000 and used MACRS depreciation for regular income tax purposes. He is required to make a positive adjustment for AMT purposes in 2016 for the excess of depreciation calculated for regular income tax purposes over the depreciation calculated for AMT purposes.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 101 في هذه المجموعة.

فتح الحزمة

k this deck

33

Since most tax preferences are merely timing differences, they eventually will reverse and net to zero.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 101 في هذه المجموعة.

فتح الحزمة

k this deck

34

A taxpayer who expenses circulation expenditures in the year incurred for regular income tax purposes will have a positive AMT adjustment in the following year.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 101 في هذه المجموعة.

فتح الحزمة

k this deck

35

Cardinal Company incurs $800,000 during the year to construct a facility that will be used exclusively for the care of its employees' pre-school age children during normal working hours. Assuming Cardinal claims the credit for employer-provided child care this year, its basis in the newly constructed facility is $640,000.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 101 في هذه المجموعة.

فتح الحزمة

k this deck

36

In deciding to enact the alternative minimum tax, Congress was concerned about the inequity that resulted when taxpayers with substantial economic incomes could avoid paying regular income tax.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 101 في هذه المجموعة.

فتح الحزمة

k this deck

37

In computing the foreign tax credit, the greater of the foreign income taxes paid or the overall limitation is allowed.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 101 في هذه المجموعة.

فتح الحزمة

k this deck

38

Evan is a contractor who constructs both commercial and residential buildings. Even though some of the contracts could qualify for the use of the completed contract method, Evan decides to use the percentage of the completion method for all of his contracts. This increases Evan's AMT adjustment associated with long-term contracts for the current year.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 101 في هذه المجموعة.

فتح الحزمة

k this deck

39

AMT adjustments can be positive or negative, whereas AMT preferences are always positive.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 101 في هذه المجموعة.

فتح الحزمة

k this deck

40

Because current U.S. corporate income tax rates are higher than many foreign corporate income tax rates only infrequently will the credit's, the overall limitation yield a lower foreign tax credit than the amount of foreign taxes actually paid.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 101 في هذه المجموعة.

فتح الحزمة

k this deck

41

Cardinal Corporation hires two persons certified to be eligible employees for the work opportunity tax credit under the general rules (e.g., food stamp recipients), each of whom is paid $9,000 during the year. As a result of this event, Cardinal Corporation may claim a work opportunity credit of:

A)$1,440.

B)$2,880.

C)$4,800.

D)$7,200.

E)None of the above.

A)$1,440.

B)$2,880.

C)$4,800.

D)$7,200.

E)None of the above.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 101 في هذه المجموعة.

فتح الحزمة

k this deck

42

Which of the following correctly describes the tax credit for rehabilitation expenditures?

A)The cost of enlarging any existing business building is a qualifying expenditure.

B)The cost of facilities related to the building (e.g., a parking lot) is a qualifying expenditure.

C)No recapture provisions apply.

D)No credit is allowed for the rehabilitation of personal use property.

E)None of the above.

A)The cost of enlarging any existing business building is a qualifying expenditure.

B)The cost of facilities related to the building (e.g., a parking lot) is a qualifying expenditure.

C)No recapture provisions apply.

D)No credit is allowed for the rehabilitation of personal use property.

E)None of the above.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 101 في هذه المجموعة.

فتح الحزمة

k this deck

43

Several years ago, Tom purchased a structure for $300,000 that was placed in service in 1929. Three and one-half years ago he incurred qualifying rehabilitation expenditures of $600,000. In the current year, Tom sold the property in a taxable transaction. Calculate the amount of the recapture of the tax credit for rehabilitation expenditures.

A)$0

B)$24,000

C)$36,000

D)$48,000

E)None of the above

A)$0

B)$24,000

C)$36,000

D)$48,000

E)None of the above

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 101 في هذه المجموعة.

فتح الحزمة

k this deck

44

After 1993, the corporate AMT no longer applies for small C corporations.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 101 في هذه المجموعة.

فتح الحزمة

k this deck

45

The AMT exemption for a C corporation is $50,000 reduced by 25% of the amount by which AMTI exceeds $150,000.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 101 في هذه المجموعة.

فتح الحزمة

k this deck

46

The ACE adjustment can be positive or negative.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 101 في هذه المجموعة.

فتح الحزمة

k this deck

47

Roger is considering making a $6,000 investment in a venture that its promoter promises will generate immediate tax benefits for him. Roger, who does not anticipate itemizing his deductions, is in the 30% marginal income tax bracket. If the investment is of a type that produces a tax credit of 40% of the amount of the expenditure, by how much will Roger's tax liability decline because of the investment?

A)$0

B)$1,800

C)$2,200

D)$2,400

E)None of the above

A)$0

B)$1,800

C)$2,200

D)$2,400

E)None of the above

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 101 في هذه المجموعة.

فتح الحزمة

k this deck

48

A negative ACE adjustment is beneficial to a corporation.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 101 في هذه المجموعة.

فتح الحزمة

k this deck

49

AMTI may be defined as regular taxable income after AMT adjustments (other than the NOL and ACE adjustments) and after tax preferences.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 101 في هذه المجموعة.

فتح الحزمة

k this deck

50

Cher sold undeveloped land that originally cost $150,000 for $225,000. There is a positive AMT adjustment of $75,000 associated with the sale of the land.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 101 في هذه المجموعة.

فتح الحزمة

k this deck

51

Molly has generated general business credits over the years that have not been utilized. The amounts generated and not utilized follow:

In the current year, 2016, her business generates an additional $15,000 general business credit. In 2016, based on her tax liability before credits, she can utilize a general business credit of up to $20,000. After utilizing the carryforwards and the current year credits, how much of the general business credit generated in 2016 is available for future years?

A)$0.

B)$1,000.

C)$14,000.

D)$15,000.

E)None of the above.

In the current year, 2016, her business generates an additional $15,000 general business credit. In 2016, based on her tax liability before credits, she can utilize a general business credit of up to $20,000. After utilizing the carryforwards and the current year credits, how much of the general business credit generated in 2016 is available for future years?

A)$0.

B)$1,000.

C)$14,000.

D)$15,000.

E)None of the above.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 101 في هذه المجموعة.

فتح الحزمة

k this deck

52

C corporations are not required to make AMT adjustments for depreciation.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 101 في هذه المجموعة.

فتح الحزمة

k this deck

53

The AMT exemption for a corporation with $225,000 of AMTI is $18,750.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 101 في هذه المجموعة.

فتح الحزمة

k this deck

54

Because passive losses are not deductible in computing either taxable income or AMTI, no AMT adjustment for passive losses is required.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 101 في هذه المجموعة.

فتح الحزمة

k this deck

55

During the year, Green, Inc., incurs the following research expenditures:

Green's qualifying research expenditures for the year are:

A)$60,000.

B)$75,000.

C)$79,500.

D)$90,000.

E)None of the above.

Green's qualifying research expenditures for the year are:

A)$60,000.

B)$75,000.

C)$79,500.

D)$90,000.

E)None of the above.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 101 في هذه المجموعة.

فتح الحزمة

k this deck

56

In March 2016, Gray Corporation hired two individuals, both of whom were certified as long-term recipients of family assistance benefits. Each employee was paid $11,000 during 2016. Only one of the individuals continued to work for Gray Corporation in 2017, earning $9,000 during the year. No additional workers were hired in 2017. Gray Corporation's work opportunity tax credit amounts for 2016 and 2017 are:

A)$4,000 in 2016, $4,000 in 2017.

B)$8,000 in 2016, $4,500 in 2017.

C)$8,000 in 2016, $5,000 in 2017.

D)$8,000 in 2016, $9,000 in 2017.

A)$4,000 in 2016, $4,000 in 2017.

B)$8,000 in 2016, $4,500 in 2017.

C)$8,000 in 2016, $5,000 in 2017.

D)$8,000 in 2016, $9,000 in 2017.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 101 في هذه المجموعة.

فتح الحزمة

k this deck

57

Black Company paid wages of $180,000, of which $40,000 was qualified wages for the work opportunity tax credit under the general rules. Black Company's deduction for wages for the year is:

A)$140,000.

B)$164,000.

C)$166,000.

D)$180,000.

E)None of the above.

A)$140,000.

B)$164,000.

C)$166,000.

D)$180,000.

E)None of the above.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 101 في هذه المجموعة.

فتح الحزمة

k this deck

58

Certain adjustments apply in calculating the corporate AMT that do not apply in calculating the noncorporate AMT and certain adjustments apply in calculating the noncorporate AMT that do not apply in calculating the corporate AMT.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 101 في هذه المجموعة.

فتح الحزمة

k this deck

59

All of a C corporation's AMT is available for carryover as a minimum tax credit, regardless of whether the adjustments and preferences originate from timing differences or AMT preferences.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 101 في هذه المجموعة.

فتح الحزمة

k this deck

60

Several years ago, Sarah purchased a structure for $150,000 that was placed in service in 1929. In the current year, she incurred qualifying rehabilitation expenditures of $200,000. The amount of the tax credit for rehabilitation expenditures, and the amount by which the building's basis for cost recovery would increase as a result of the rehabilitation expenditures are the following amounts.

A)$20,000 credit, $180,000 basis.

B)$20,000 credit, $200,000 basis.

C)$20,000 credit, $350,000 basis.

D)$40,000 credit, $160,000 basis.

A)$20,000 credit, $180,000 basis.

B)$20,000 credit, $200,000 basis.

C)$20,000 credit, $350,000 basis.

D)$40,000 credit, $160,000 basis.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 101 في هذه المجموعة.

فتح الحزمة

k this deck

61

Lemon, Inc., has the following items related to the AMT:

The corporation's AMT, if any, is:

A)$0.

B)$755,580.

C)$1,868,080.

D)$2,055,100.

E)None of the above.

The corporation's AMT, if any, is:

A)$0.

B)$755,580.

C)$1,868,080.

D)$2,055,100.

E)None of the above.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 101 في هذه المجموعة.

فتح الحزمة

k this deck

62

Dale owns and operates Dale's Emporium as a sole proprietorship. On January 30, 1998, Dale's Emporium acquired a warehouse for $100,000. For regular income tax purposes in 2016, depreciation was deducted under MACRS using a rate of 2.564%. Determine the AMT adjustment for depreciation and indicate whether it is positive or negative.

A)$64 negative adjustment.

B)$64 positive adjustment.

C)No adjustment is required because Dale's Emporium used the Alternative Depreciation System (ADS) to compute depreciation on the property for AMT purposes.

D)No adjustment is required because Dale's Emporium used MACRS to compute the depreciation of the property for regular income tax purposes.

A)$64 negative adjustment.

B)$64 positive adjustment.

C)No adjustment is required because Dale's Emporium used the Alternative Depreciation System (ADS) to compute depreciation on the property for AMT purposes.

D)No adjustment is required because Dale's Emporium used MACRS to compute the depreciation of the property for regular income tax purposes.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 101 في هذه المجموعة.

فتح الحزمة

k this deck

63

In January 2016, Tammy acquired an office building in downtown Syracuse, New York for $400,000. The building was constructed in 1932. Of the $400,000 cost, $40,000 was allocated to the land. Tammy immediately placed the building into service, but she quickly realized that substantial renovation would be required to keep and attract new tenants. The renovations, costing $600,000, were of the type that qualifies for the rehabilitation credit. The improvements were completed in October 2016.

a.Compute Tammy's rehabilitation tax credit for the year of acquisition.

b.Determine the cost recovery deduction for 2016.

c.What is the basis in the property at the end of its first year of use by Tammy?

a.Compute Tammy's rehabilitation tax credit for the year of acquisition.

b.Determine the cost recovery deduction for 2016.

c.What is the basis in the property at the end of its first year of use by Tammy?

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 101 في هذه المجموعة.

فتح الحزمة

k this deck

64

During the year, Purple Corporation (a U.S. Corporation) has U.S.-source income of $1,800,000 and foreign income of $600,000. The foreign-source income generates foreign income taxes of $150,000. The U.S. income tax before the foreign tax credit is $816,000. Purple Corporation's foreign tax credit is:

A)$112,500.

B)$150,000.

C)$204,000.

D)$816,000.

A)$112,500.

B)$150,000.

C)$204,000.

D)$816,000.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 101 في هذه المجموعة.

فتح الحزمة

k this deck

65

Ford Corporation, a calendar year corporation, has alternative minimum taxable income (before any exemption) of $1.28 million for 2016. The company is not a small corporation. If the regular corporate tax is $209,000, Ford's alternative minimum tax for 2016 is:

A)$47,000.

B)$209,000.

C)$256,000.

D)$1,280,000.

E)None of the above.

A)$47,000.

B)$209,000.

C)$256,000.

D)$1,280,000.

E)None of the above.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 101 في هذه المجموعة.

فتح الحزمة

k this deck

66

Sand Corporation, a calendar year C corporation, reports alternative minimum taxable income of $900,000 for 2016. Sand's tentative minimum tax for 2016 is:

A)$0.

B)$40,000.

C)$180,000.

D)$191,250.

E)None of the above.

A)$0.

B)$40,000.

C)$180,000.

D)$191,250.

E)None of the above.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 101 في هذه المجموعة.

فتح الحزمة

k this deck

67

Vicki owns and operates a news agency (as a sole proprietorship). During 2016, she incurred expenses of $24,000 to increase circulation of newspapers and magazines that her agency distributes. For regular income tax purposes, she elected to expense the $24,000 in 2016. In addition, Vicki incurred $15,000 in circulation expenditures in 2017 and again elected expense treatment. What AMT adjustments will be required in 2016 and 2017 as a result of the circulation expenditures?

A)$16,000 positive in 2016, $2,000 positive in 2017.

B)$16,000 negative in 2016, $2,000 positive in 2017.

C)$16,000 negative in 2016, $10,000 positive in 2017.

D)$16,000 positive in 2016, $10,000 positive in 2017.

E)None of the above.

A)$16,000 positive in 2016, $2,000 positive in 2017.

B)$16,000 negative in 2016, $2,000 positive in 2017.

C)$16,000 negative in 2016, $10,000 positive in 2017.

D)$16,000 positive in 2016, $10,000 positive in 2017.

E)None of the above.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 101 في هذه المجموعة.

فتح الحزمة

k this deck

68

In June, Della purchases a building for $800,000 to use in her business as an office building. Della uses the depreciation method which will provide her with the greatest deduction for regular income tax purposes.

a.Calculate the AMT adjustment for depreciation in 2016 if Della purchased the building in 2016.

b.Calculate the AMT preference for depreciation in 2016 if Della purchased the building in 1986.

a.Calculate the AMT adjustment for depreciation in 2016 if Della purchased the building in 2016.

b.Calculate the AMT preference for depreciation in 2016 if Della purchased the building in 1986.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 101 في هذه المجموعة.

فتح الحزمة

k this deck

69

Use the following selected data to calculate Devon's taxable income prior to any personal exemption taken. Devon does not itemize deductions.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 101 في هذه المجموعة.

فتح الحزمة

k this deck

70

Which, if any, of the following correctly describes the research activities credit?

A)The research activities credit is the greater of the incremental research credit, the basic research credit, or the energy research credit.

B)If the research activities credit is claimed, no deduction is allowed for research and experimentation expenditures.

C)The credit is not available for research conducted outside the United States.

D)All corporations qualify for the basic research credit.

E)None of the above.

A)The research activities credit is the greater of the incremental research credit, the basic research credit, or the energy research credit.

B)If the research activities credit is claimed, no deduction is allowed for research and experimentation expenditures.

C)The credit is not available for research conducted outside the United States.

D)All corporations qualify for the basic research credit.

E)None of the above.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 101 في هذه المجموعة.

فتح الحزمة

k this deck

71

Steve records a tentative general business credit of $110,000 for the current year. His net regular tax liability before the general business credit is $125,000, and his tentative minimum tax is $100,000. Compute Steve's allowable general business credit for the year.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 101 في هذه المجموعة.

فتح الحزمة

k this deck

72

In 2016, Glenn recorded a $108,000 loss on a passive activity. None of the loss is attributable to AMT adjustments or preferences. She has no other passive activities. Which of the following statements is correct?

A)In 2016, Glenn can deduct $108,000 for regular income tax purposes and for AMT purposes.

B)Glenn reports a $108,000 tax preference in 2016 as a result of the passive activity.

C)For regular income tax purposes, none of the passive activity loss is allowed in 2016.

D)In 2016, Glenn reports a positive adjustment of $25,000 as a result of the passive activity loss.

E)None of the above.

A)In 2016, Glenn can deduct $108,000 for regular income tax purposes and for AMT purposes.

B)Glenn reports a $108,000 tax preference in 2016 as a result of the passive activity.

C)For regular income tax purposes, none of the passive activity loss is allowed in 2016.

D)In 2016, Glenn reports a positive adjustment of $25,000 as a result of the passive activity loss.

E)None of the above.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 101 في هذه المجموعة.

فتح الحزمة

k this deck

73

Amber is in the process this year of renovating the office building (placed in service in 1976) used by her business. Because of current Federal Regulations that require the structure to be accessible to handicapped individuals, she incurs an additional $11,000 for various features, such as ramps and widened doorways, to make her office building more accessible. The $11,000 incurred will produce a disabled access credit of what amount?

A)$0

B)$5,000

C)$5,125

D)$5,500

A)$0

B)$5,000

C)$5,125

D)$5,500

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 101 في هذه المجموعة.

فتح الحزمة

k this deck

74

Sage, Inc., has the following gross receipts and taxable income, since its incorporation in 2010.

Is Sage, Inc., subject to the AMT in 2016?

Is Sage, Inc., subject to the AMT in 2016?

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 101 في هذه المجموعة.

فتح الحزمة

k this deck

75

In 2016, Job Corporation, a calendar year taxpayer, has AMTI (before adjustment for adjusted current earnings) of $7 million. If Job Corporation's ACE is $16 million, its tentative minimum tax for 2016 is:

A)$2.55 million.

B)$2.75 million.

C)$3.45 million.

D)$4.2 million.

E)None of the above.

A)$2.55 million.

B)$2.75 million.

C)$3.45 million.

D)$4.2 million.

E)None of the above.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 101 في هذه المجموعة.

فتح الحزمة

k this deck

76

Frederick sells land and building whose adjusted basis for regular income tax purposes is $345,000 and for AMT purposes is $380,000. The sales proceeds are $850,000. Determine the effect on:

a.Taxable income.

b.AMTI.

a.Taxable income.

b.AMTI.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 101 في هذه المجموعة.

فتح الحزمة

k this deck

77

Green Company, in the renovation of its building, incurs $9,000 of expenditures that qualify for the disabled access credit. The disabled access credit is:

A)$8,750.

B)$4,500.

C)$4,375.

D)$4,250.

E)None of the above.

A)$8,750.

B)$4,500.

C)$4,375.

D)$4,250.

E)None of the above.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 101 في هذه المجموعة.

فتح الحزمة

k this deck

78

Mauve, Inc., records the following gross receipts in 2014, 2015, and 2016.

What is Mauve, Inc.'s TMT in each of these three years?

2014 2015 2016

A)$0 $0 $0

B)$0 $0 $1,160,000

C)$0 $1,740,000 $1,160,000

D)$980,000 $1,740,000 $1,160,000

E)$0 $1,740,000) $0

What is Mauve, Inc.'s TMT in each of these three years?

2014 2015 2016

A)$0 $0 $0

B)$0 $0 $1,160,000

C)$0 $1,740,000 $1,160,000

D)$980,000 $1,740,000 $1,160,000

E)$0 $1,740,000) $0

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 101 في هذه المجموعة.

فتح الحزمة

k this deck

79

Omar acquires used 7-year personal property for $100,000 to use in his business in February 2016. Omar does not elect § 179 expensing, but he does take the maximum regular cost recovery deduction. He elects not to take additional first-year depreciation. As a result, Omar incurs a positive AMT adjustment in 2016 of what amount?

A)$0

B)$3,580

C)$10,710

D)$14,290

E)None of the above

A)$0

B)$3,580

C)$10,710

D)$14,290

E)None of the above

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 101 في هذه المجموعة.

فتح الحزمة

k this deck

80

Eula owns a mineral property that had a basis of $23,000 at the beginning of the year. Cost depletion is $19,000. The property qualifies for a 15% depletion rate. Gross income from the property was $200,000 and net income before the percentage depletion deduction was $50,000. What is Eula's tax preference for excess depletion, if she maximized her regular-tax depletion deduction?

A)$15,000

B)$23,000

C)$25,000

D)$2,000

A)$15,000

B)$23,000

C)$25,000

D)$2,000

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 101 في هذه المجموعة.

فتح الحزمة

k this deck

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 101 في هذه المجموعة.