Deck 6: Intangible Assets

ملء الشاشة (f)

سؤال

سؤال

The measurement of fair value is determined in accordance with AASB 13 Fair Value Measurement. AASB 13 defines fair value as one that has all of the following conditions:

A) I.

B) II.

C) III.

D) IV.

A) I.

B) II.

C) III.

D) IV.

سؤال

سؤال

سؤال

Paragraph 63 of AASB 138 Intangibles, prohibits the recognition of the following internally generated identifiable intangibles:

A) I.

B) II.

C) III.

D) IV.

A) I.

B) II.

C) III.

D) IV.

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

فتح الحزمة

قم بالتسجيل لفتح البطاقات في هذه المجموعة!

Unlock Deck

Unlock Deck

1/24

العب

ملء الشاشة (f)

Deck 6: Intangible Assets

1

Items such as market knowledge, effective advertising programs, fundraising capabilities and trained staff are NOT regarded as assets because they:

A) are monetary items.

B) cannot be measured.

C) are not controlled by the entity.

D) are too difficult to manage.

A) are monetary items.

B) cannot be measured.

C) are not controlled by the entity.

D) are too difficult to manage.

C

2

The measurement of fair value is determined in accordance with AASB 13 Fair Value Measurement. AASB 13 defines fair value as one that has all of the following conditions:

A) I.

B) II.

C) III.

D) IV.

A) I.

B) II.

C) III.

D) IV.

D

3

For an asset to be classified as an identifiable intangible, AASB 138 Intangibles requires that it meet which of the following criteria:

I) It arises from a contractual or legal right.

II) Its fair value must be able to be reliably measured.

III) It is separable from the entity.

IV) Its cost must reliably measurable.

A) I or IV only.

B) I or II only.

C) II or III only.

D) I or III only.

I) It arises from a contractual or legal right.

II) Its fair value must be able to be reliably measured.

III) It is separable from the entity.

IV) Its cost must reliably measurable.

A) I or IV only.

B) I or II only.

C) II or III only.

D) I or III only.

D

4

Parsons Limited was involved in a highly successful plastics manufacturing business. It commenced a project to design a more efficient extrusion system for its plastic pipes. The following outlays occurred: January, research salaries $50 000; February, research materials $30 000; March, re-development of the extrusion plant $400 000; April, final adjustments to the extrusion plant $25 000. The amount to be expensed by this company at the end of the financial year, 30 June, is:

A) $30 000.

B) $50 000.

C) $80 000.

D) $480 000.

A) $30 000.

B) $50 000.

C) $80 000.

D) $480 000.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 24 في هذه المجموعة.

فتح الحزمة

k this deck

5

Paragraph 63 of AASB 138 Intangibles, prohibits the recognition of the following internally generated identifiable intangibles:

A) I.

B) II.

C) III.

D) IV.

A) I.

B) II.

C) III.

D) IV.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 24 في هذه المجموعة.

فتح الحزمة

k this deck

6

A key characteristic that separates assets such as property, plant and equipment from intangible assets is:

A) separability.

B) length of useful life.

C) lack of physical substance.

D) reliability.

A) separability.

B) length of useful life.

C) lack of physical substance.

D) reliability.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 24 في هذه المجموعة.

فتح الحزمة

k this deck

7

The characteristic that distinguishes the goodwill from other intangible assets is:

A) identifiability.

B) its nature as a monetary asset.

C) that is has a physical embodiment.

D) it can be separated from the entity and sold individually.

A) identifiability.

B) its nature as a monetary asset.

C) that is has a physical embodiment.

D) it can be separated from the entity and sold individually.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 24 في هذه المجموعة.

فتح الحزمة

k this deck

8

According to the definition provided in AASB 138 Intangibles, activities undertaken in the 'research' phase of the generation of an asset may include:

A) the application of knowledge to a design for the production of new materials.

B) original and planned investigation with the prospect of gaining new scientific knowledge.

C) the use of research findings to create a substantially improved product.

D) using knowledge to materially improve a manufacturing device.

A) the application of knowledge to a design for the production of new materials.

B) original and planned investigation with the prospect of gaining new scientific knowledge.

C) the use of research findings to create a substantially improved product.

D) using knowledge to materially improve a manufacturing device.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 24 في هذه المجموعة.

فتح الحزمة

k this deck

9

The cost of an intangible asset is comprised of the fair value of the consideration:

A) less legal costs incurred in the purchase.

B) plus directly attributable costs.

C) plus indirect costs.

D) less directly attributable costs.

A) less legal costs incurred in the purchase.

B) plus directly attributable costs.

C) plus indirect costs.

D) less directly attributable costs.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 24 في هذه المجموعة.

فتح الحزمة

k this deck

10

Wojtowicz Limited was involved in a mining exploration business. It commenced a project to design more efficient gold detecting equipment. The following expenditures occurred during the financial year ended 2013: researcher's salary $5000; research consumables $3000; re-development of the detecting equipment $4000; final adjustments to the detecting equipment $2500. The amount to be capitalised by this company as an intangible asset, for the 2013 financial year, is:

A) $6500.

B) $8000.

C) $11 500.

D) $14 500.

A) $6500.

B) $8000.

C) $11 500.

D) $14 500.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 24 في هذه المجموعة.

فتح الحزمة

k this deck

11

Unless acquired under a business combination, intangible assets must be initially measured using which of the following measurement approaches:

A) Discounted cash flows.

B) Fair value.

C) Net present value.

D) Cost.

A) Discounted cash flows.

B) Fair value.

C) Net present value.

D) Cost.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 24 في هذه المجموعة.

فتح الحزمة

k this deck

12

AASB 138 Intangibles, requires that an intangible asset with a finite life:

A) be amortised across its useful life.

B) be amortised across a period of no greater than 20 years.

C) not be amortised in periods when it is been properly maintained.

D) not be subject to amortisation charges.

A) be amortised across its useful life.

B) be amortised across a period of no greater than 20 years.

C) not be amortised in periods when it is been properly maintained.

D) not be subject to amortisation charges.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 24 في هذه المجموعة.

فتح الحزمة

k this deck

13

The recognition criteria that an asset must meet before it may be recognised and presented in the financial statements include:

A) that the recognition of the asset is relevant to user decision making.

B) probability that future economic benefits will flow to the entity.

C) that the information about the asset is neutral.

D) a likelihood that the cost of the asset is verifiable.

A) that the recognition of the asset is relevant to user decision making.

B) probability that future economic benefits will flow to the entity.

C) that the information about the asset is neutral.

D) a likelihood that the cost of the asset is verifiable.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 24 في هذه المجموعة.

فتح الحزمة

k this deck

14

Under AASB 138 Intangibles, an intangible asset with an indefinite useful life is:

A) not able to be recognised by an entity as an asset.

B) not subject to annual amortisation charges.

C) amortised using the straight-line method over a period of no more than 20 years.

D) amortised using the reducing balance method over a period not exceeding 5 years.

A) not able to be recognised by an entity as an asset.

B) not subject to annual amortisation charges.

C) amortised using the straight-line method over a period of no more than 20 years.

D) amortised using the reducing balance method over a period not exceeding 5 years.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 24 في هذه المجموعة.

فتح الحزمة

k this deck

15

Under AASB 138 Intangibles, goodwill may only be recognised as an asset if it:

A) arises as a result of creating new assets within the normal business operations

B) does not exceed its internally recorded cost

C) is internally generated

D) is acquired as part of a business combination.

A) arises as a result of creating new assets within the normal business operations

B) does not exceed its internally recorded cost

C) is internally generated

D) is acquired as part of a business combination.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 24 في هذه المجموعة.

فتح الحزمة

k this deck

16

Which of the following assets is regarded as meeting the identifiability criteria for recognition as an identifiable intangible asset that can be recorded as acquired in a business combination:

A) Customer base.

B) Royalty agreements.

C) Ongoing recruitment programs.

D) Strong and favourable employee relations.

A) Customer base.

B) Royalty agreements.

C) Ongoing recruitment programs.

D) Strong and favourable employee relations.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 24 في هذه المجموعة.

فتح الحزمة

k this deck

17

When an intangible asset is acquired by an exchange of assets, which of the following measures will need to be considered in the determination of that cost:

A) The fair value of the asset given up.

B) The initial cost of the asset given up.

C) The carrying amount of the asset received.

D) The replacement cost of the asset received.

A) The fair value of the asset given up.

B) The initial cost of the asset given up.

C) The carrying amount of the asset received.

D) The replacement cost of the asset received.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 24 في هذه المجموعة.

فتح الحزمة

k this deck

18

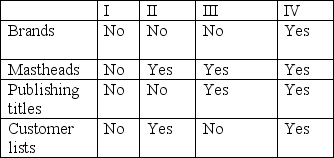

Which of the following assets is regarded as meeting the identifiability criteria for recognition as an identifiable intangible asset that may be acquired in a business combination:

A) Customer service capability.

B) Newspaper mastheads.

C) Favourable government relations.

D) Presence in geographic locations.

A) Customer service capability.

B) Newspaper mastheads.

C) Favourable government relations.

D) Presence in geographic locations.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 24 في هذه المجموعة.

فتح الحزمة

k this deck

19

AASB 138 Intangibles, requires that the following items in relation to intangibles, each be disclosed separately:

A) the opening balance of each intangible.

B) the closing balance of each intangible.

C) any impairment losses reversed in profit or loss during the period.

D) all amounts of intangibles acquired during the period.

A) the opening balance of each intangible.

B) the closing balance of each intangible.

C) any impairment losses reversed in profit or loss during the period.

D) all amounts of intangibles acquired during the period.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 24 في هذه المجموعة.

فتح الحزمة

k this deck

20

The two key characteristics of intangible assets are that they are identifiable and that they:

A) have physical substance.

B) are monetary assets.

C) represent current obligations of the entity.

D) lack physical substance.

A) have physical substance.

B) are monetary assets.

C) represent current obligations of the entity.

D) lack physical substance.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 24 في هذه المجموعة.

فتح الحزمة

k this deck

21

Which of the following statements is correct:

A) AASB 138 requires disclosures about an entity's intangible assets, with disclosures being made on an asset by asset basis.

B) Disclosures about the useful lives of intangibles are required with explanations being required where assets are assessed to have finite useful lives.

C) Where the cost model is used, specific disclosures are required including assumptions made on estimating fair values.

D) Separate disclosures are required for internally generated intangibles.

A) AASB 138 requires disclosures about an entity's intangible assets, with disclosures being made on an asset by asset basis.

B) Disclosures about the useful lives of intangibles are required with explanations being required where assets are assessed to have finite useful lives.

C) Where the cost model is used, specific disclosures are required including assumptions made on estimating fair values.

D) Separate disclosures are required for internally generated intangibles.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 24 في هذه المجموعة.

فتح الحزمة

k this deck

22

The original and planned investigation undertaken with the prospect of gaining new knowledge is described as:

A) exploration.

B) development.

C) investigation.

D) research.

A) exploration.

B) development.

C) investigation.

D) research.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 24 في هذه المجموعة.

فتح الحزمة

k this deck

23

When subsequent expenditure on intangible assets occurs the costs are:

A) recognised directly in retained earnings account.

B) immediately expensed.

C) transferred to a revaluation reserve account.

D) capitalised.

A) recognised directly in retained earnings account.

B) immediately expensed.

C) transferred to a revaluation reserve account.

D) capitalised.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 24 في هذه المجموعة.

فتح الحزمة

k this deck

24

Under the revaluation method of measuring an intangible, the asset is carried at fair value and subject to charges for:

A) amortisation and impairment.

B) inflation in value.

C) interest expense.

D) increment in value.

A) amortisation and impairment.

B) inflation in value.

C) interest expense.

D) increment in value.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 24 في هذه المجموعة.

فتح الحزمة

k this deck

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 24 في هذه المجموعة.