Deck 23: Foreign Currency Transactions and Forward Exchange Contracts

ملء الشاشة (f)

سؤال

سؤال

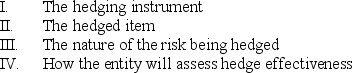

The formal documentation of a hedging relationship must include identification of:

A) I, II and III only.

B) I, II and IV only.

C) II, III and IV only.

D) I, II, III and IV.

A) I, II and III only.

B) I, II and IV only.

C) II, III and IV only.

D) I, II, III and IV.

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

فتح الحزمة

قم بالتسجيل لفتح البطاقات في هذه المجموعة!

Unlock Deck

Unlock Deck

1/20

العب

ملء الشاشة (f)

Deck 23: Foreign Currency Transactions and Forward Exchange Contracts

1

The Australian financial news quoted US$1.00 equals A$0.9399/0.9649. What does this represent?

A) A bid rate of A$0.9649.

B) The direct form of quotation.

C) An offer rate of A$0.9399.

D) A bid-ask spread of A$0.0351.

A) A bid rate of A$0.9649.

B) The direct form of quotation.

C) An offer rate of A$0.9399.

D) A bid-ask spread of A$0.0351.

B

2

The formal documentation of a hedging relationship must include identification of:

A) I, II and III only.

B) I, II and IV only.

C) II, III and IV only.

D) I, II, III and IV.

A) I, II and III only.

B) I, II and IV only.

C) II, III and IV only.

D) I, II, III and IV.

D

3

AASB 121 requires that the financial report disclose which of the following?

A) The net exchange differences recognised in OCI and accumulated in a separate component of equity.

B) The amount of exchange differences recognised in the profit or loss for the period other than those that relate to financial instruments measured at fair value through profit or loss.

C) Any change in functional currency and reason for change.

D) All of the above.

A) The net exchange differences recognised in OCI and accumulated in a separate component of equity.

B) The amount of exchange differences recognised in the profit or loss for the period other than those that relate to financial instruments measured at fair value through profit or loss.

C) Any change in functional currency and reason for change.

D) All of the above.

D

4

The Australian Financial News quoted A$1.00 equals US$1.05/1.08. What does this represent?

A) A bid rate of US$1.08.

B) An offer rate of A$1.08.

C) A bid rate of A$1.05.

D) An offer rate of US$1.08.

A) A bid rate of US$1.08.

B) An offer rate of A$1.08.

C) A bid rate of A$1.05.

D) An offer rate of US$1.08.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 20 في هذه المجموعة.

فتح الحزمة

k this deck

5

All of the following assets can be defined as 'qualifying assets' except:

A) manufacturing plants.

B) inventories purchased ready for sale.

C) power generation facilities.

D) investment properties.

A) manufacturing plants.

B) inventories purchased ready for sale.

C) power generation facilities.

D) investment properties.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 20 في هذه المجموعة.

فتح الحزمة

k this deck

6

All of the following are examples of a fair value hedge, except:

A) a forward contract to sell US$ hedging a recognised trade receivable in US$.

B) a forward contract to buy US$ hedging a highly probable purchase of inventory in US$.

C) a forward contract to buy US$ hedging a recognised trade payable in US$.

D) a forward contract to sell US$ hedging a recognised loan receivable in US$.

A) a forward contract to sell US$ hedging a recognised trade receivable in US$.

B) a forward contract to buy US$ hedging a highly probable purchase of inventory in US$.

C) a forward contract to buy US$ hedging a recognised trade payable in US$.

D) a forward contract to sell US$ hedging a recognised loan receivable in US$.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 20 في هذه المجموعة.

فتح الحزمة

k this deck

7

At the end of the reporting period, a foreign currency monetary item is remeasured using:

A) the foreign currency monetary value.

B) spot exchange rate.

C) US dollars.

D) the closing rate.

A) the foreign currency monetary value.

B) spot exchange rate.

C) US dollars.

D) the closing rate.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 20 في هذه المجموعة.

فتح الحزمة

k this deck

8

All of the following are examples of a cash flow hedge, except:

A) a forward contract to buy US$ hedging recognised borrowings in US$.

B) a forward contract to buy US$ hedging future interest payments on variable rate debt in US$.

C) a forward contract to sell US$ hedging a highly probable sale of inventory in US$.

D) a forward contract to buy US$ hedging an unrecognised firm commitment to purchase goods in US$.

A) a forward contract to buy US$ hedging recognised borrowings in US$.

B) a forward contract to buy US$ hedging future interest payments on variable rate debt in US$.

C) a forward contract to sell US$ hedging a highly probable sale of inventory in US$.

D) a forward contract to buy US$ hedging an unrecognised firm commitment to purchase goods in US$.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 20 في هذه المجموعة.

فتح الحزمة

k this deck

9

If an Australian company enters a forward exchange contract to buy US$15 000, then which of the following applies?

A) The company's contractual obligation (at the forward rate) and contractual right (at the spot rate) are settled on a net basis.

B) The company has a contractual obligation to deliver foreign currency at the settlement date and that obligation is realised at the spot rate.

C) The company has a contractual right to receive US$15 000 at the settlement date and that right is an asset fixed in A$ at the forward rate.

D) The company's forward contract will act as a hedge against a recognised asset.

A) The company's contractual obligation (at the forward rate) and contractual right (at the spot rate) are settled on a net basis.

B) The company has a contractual obligation to deliver foreign currency at the settlement date and that obligation is realised at the spot rate.

C) The company has a contractual right to receive US$15 000 at the settlement date and that right is an asset fixed in A$ at the forward rate.

D) The company's forward contract will act as a hedge against a recognised asset.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 20 في هذه المجموعة.

فتح الحزمة

k this deck

10

Hedge effectiveness is ascertained from:

A) the hedge ratio of the hedging relationship reflects actual quantities and is consistent with the purpose of hedge accounting.

B) there is an economic relationship between the hedging instrument and the hedged item.

C) the effect of credit risk does not dominate the economic relationship hedging instrument and the hedged item.

D) all of the options are correct.

A) the hedge ratio of the hedging relationship reflects actual quantities and is consistent with the purpose of hedge accounting.

B) there is an economic relationship between the hedging instrument and the hedged item.

C) the effect of credit risk does not dominate the economic relationship hedging instrument and the hedged item.

D) all of the options are correct.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 20 في هذه المجموعة.

فتح الحزمة

k this deck

11

The degree to which changes in the fair value of a forward contract offset changes in the fair value or cash flows of a hedged item, describes:

A) transaction exposure.

B) hedge ineffectiveness.

C) hedge effectiveness.

D) transaction variability.

A) transaction exposure.

B) hedge ineffectiveness.

C) hedge effectiveness.

D) transaction variability.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 20 في هذه المجموعة.

فتح الحزمة

k this deck

12

A decrease in the direct rate of US$1 to A$# results in:

A) an increase in US$ amount for a payable in A$.

B) a decrease in A$ amount for a payable in US$.

C) an exchange loss.

D) an increase in A$ amount for receivable in US$.

A) an increase in US$ amount for a payable in A$.

B) a decrease in A$ amount for a payable in US$.

C) an exchange loss.

D) an increase in A$ amount for receivable in US$.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 20 في هذه المجموعة.

فتح الحزمة

k this deck

13

A forward contact to buy US$40 000 for a planned purchase transaction of US$50 000 has a hedge ratio of:

A) 40%.

B) 125%.

C) 80%.

D) 20%.

A) 40%.

B) 125%.

C) 80%.

D) 20%.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 20 في هذه المجموعة.

فتح الحزمة

k this deck

14

At the date of the transaction, a foreign currency monetary item is initially recognised and measured using:

A) the closing rate.

B) the foreign currency monetary value.

C) spot exchange rate.

D) US dollars.

A) the closing rate.

B) the foreign currency monetary value.

C) spot exchange rate.

D) US dollars.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 20 في هذه المجموعة.

فتح الحزمة

k this deck

15

A realised exchange difference arises:

A) when the exchange rate changes between initial recognition and cash settlement.

B) when the exchange rate changes between initial recognition and end of reporting period.

C) on remeasurement of a monetary liability at the end of the reporting period.

D) on initial recognition of a monetary asset.

A) when the exchange rate changes between initial recognition and cash settlement.

B) when the exchange rate changes between initial recognition and end of reporting period.

C) on remeasurement of a monetary liability at the end of the reporting period.

D) on initial recognition of a monetary asset.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 20 في هذه المجموعة.

فتح الحزمة

k this deck

16

All of the following are foreign currency transactions for a company that has A$ as its functional currency, except:

A) goods sold at prices denominated in Japanese Yen.

B) inventory sold to a customer in Hong Kong who pays in A$.

C) borrowing funds where amounts are payable in NZ$.

D) equipment sold at prices denominated in pounds.

A) goods sold at prices denominated in Japanese Yen.

B) inventory sold to a customer in Hong Kong who pays in A$.

C) borrowing funds where amounts are payable in NZ$.

D) equipment sold at prices denominated in pounds.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 20 في هذه المجموعة.

فتح الحزمة

k this deck

17

Which exchange rate is used at the end of the reporting period?

A) The indirect rate.

B) The spot rate.

C) The closing rate.

D) The ending rate.

A) The indirect rate.

B) The spot rate.

C) The closing rate.

D) The ending rate.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 20 في هذه المجموعة.

فتح الحزمة

k this deck

18

All the following items are 'monetary items' according to AASB 121 except:

A) trade payable of ₤50 000.

B) borrowings €30 000.

C) shares held in BHP Ltd listed on the ASX.

D) trade receivable of US$12 000.

A) trade payable of ₤50 000.

B) borrowings €30 000.

C) shares held in BHP Ltd listed on the ASX.

D) trade receivable of US$12 000.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 20 في هذه المجموعة.

فتح الحزمة

k this deck

19

Foreign exchange risk may relate to:

A) recognised assets and liabilities.

B) planned foreign currency transactions.

C) unrecognised firm commitments.

D) all of the above.

A) recognised assets and liabilities.

B) planned foreign currency transactions.

C) unrecognised firm commitments.

D) all of the above.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 20 في هذه المجموعة.

فتح الحزمة

k this deck

20

The __________ is a hedge of the exposure to the variability in cash flows that is attributable to a particular risk that is associated with all, or some component of, a recognised asset or liability.

A) fair value hedge

B) hedge of a net investment in a foreign operation

C) cash flow hedge

D) all of the above

A) fair value hedge

B) hedge of a net investment in a foreign operation

C) cash flow hedge

D) all of the above

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 20 في هذه المجموعة.

فتح الحزمة

k this deck

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 20 في هذه المجموعة.