Deck 14: Share-Based Payment

ملء الشاشة (f)

سؤال

سؤال

سؤال

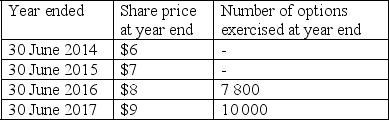

On 1 July 2013 Fantasy Ltd granted 200 options to each of its 100 employees. The share options will vest on 30 June 2015 if the employees remain employed with the company on that date. The share options have a life of four years. The exercise price is $5, which is also Fantasy's share price at the grant date. Fantasy is unable to reliably estimate the fair value of the share options at the grant date.

Fantasy's share price and the number of options exercised are set out below. Share options may only be exercised at year end.

The formula to calculate the remuneration expense for the year ended 30 June 2016 is:

A) 7800 x ($8-$7)

B) 7800 x $8

C) (7800 + 10 000) x ($8-$5)

D) (7800 + 10 000) x ($8-$7)

Fantasy's share price and the number of options exercised are set out below. Share options may only be exercised at year end.

The formula to calculate the remuneration expense for the year ended 30 June 2016 is:

A) 7800 x ($8-$7)

B) 7800 x $8

C) (7800 + 10 000) x ($8-$5)

D) (7800 + 10 000) x ($8-$7)

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

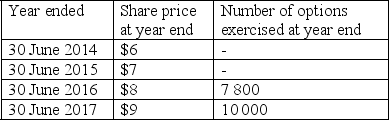

On 1 July 2013 Fantasy Ltd granted 200 options to each of its 100 employees. The share options will vest on 30 June 2015 if the employees remain employed with the company on that date. The share options have a life of four years. The exercise price is $5, which is also Fantasy's share price at the grant date. Fantasy is unable to reliably estimate the fair value of the share options at the grant date.

Fantasy's share price and the number of options exercised are set out below. Share options may only be exercised at year end.

The cumulative remuneration expense to be recognised by Fantasy as at 30 June 2015 is:

A) $7800

B) $17 800

*c) $35 600

D) $124 600

Fantasy's share price and the number of options exercised are set out below. Share options may only be exercised at year end.

The cumulative remuneration expense to be recognised by Fantasy as at 30 June 2015 is:

A) $7800

B) $17 800

*c) $35 600

D) $124 600

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

فتح الحزمة

قم بالتسجيل لفتح البطاقات في هذه المجموعة!

Unlock Deck

Unlock Deck

1/24

العب

ملء الشاشة (f)

Deck 14: Share-Based Payment

1

In a share based payment transaction where the entity has settlement choice:

A) where a present obligation does not exist the entity has a choice of classification as an equity or cash settled share based payment transaction.

B) the entity has a present obligation to settle in cash where it has a past practice or stated policy of settling in cash.

C) the entity must settle in equity unless there is no commercial substance to the transaction.

D) if an entity elects to settle in cash the settlement is accounted for as an expense.

A) where a present obligation does not exist the entity has a choice of classification as an equity or cash settled share based payment transaction.

B) the entity has a present obligation to settle in cash where it has a past practice or stated policy of settling in cash.

C) the entity must settle in equity unless there is no commercial substance to the transaction.

D) if an entity elects to settle in cash the settlement is accounted for as an expense.

B

2

Which of the following is NOT within the scope of AASB 2 Share-based Payment?

A) Transactions in which the entity receives or acquires goods or services as part of the net assets acquired in a business combination to which IFRS 3 Business Combinations applies.

B) Equity instruments granted to employees of the acquiree in a business combination in their capacity as an employee.

C) Cancellation, replacement or other modification of share-based payment arrangements because of a business combination.

D) Cancellation, replacement or other modification of share-based payment arrangements because of other equity restructuring.

A) Transactions in which the entity receives or acquires goods or services as part of the net assets acquired in a business combination to which IFRS 3 Business Combinations applies.

B) Equity instruments granted to employees of the acquiree in a business combination in their capacity as an employee.

C) Cancellation, replacement or other modification of share-based payment arrangements because of a business combination.

D) Cancellation, replacement or other modification of share-based payment arrangements because of other equity restructuring.

A

3

On 1 July 2013 Fantasy Ltd granted 200 options to each of its 100 employees. The share options will vest on 30 June 2015 if the employees remain employed with the company on that date. The share options have a life of four years. The exercise price is $5, which is also Fantasy's share price at the grant date. Fantasy is unable to reliably estimate the fair value of the share options at the grant date.

Fantasy's share price and the number of options exercised are set out below. Share options may only be exercised at year end.

The formula to calculate the remuneration expense for the year ended 30 June 2016 is:

A) 7800 x ($8-$7)

B) 7800 x $8

C) (7800 + 10 000) x ($8-$5)

D) (7800 + 10 000) x ($8-$7)

Fantasy's share price and the number of options exercised are set out below. Share options may only be exercised at year end.

The formula to calculate the remuneration expense for the year ended 30 June 2016 is:

A) 7800 x ($8-$7)

B) 7800 x $8

C) (7800 + 10 000) x ($8-$5)

D) (7800 + 10 000) x ($8-$7)

D

4

On 1 July 2013, Diamond Ltd granted 800 share options with an exercise price of $35 to the CFO, conditional on the CFO remaining in employment with the company until 30 June 2016. The exercise price will drop to $30 if Diamond's earnings increase by an average of 8% per year over the three year period. On 1 July 2013 the estimated fair value of the share options with an exercise price of $35 is $10 per option, and if the exercise price is $30, the estimated fair value of the options is $12 per option.

During the year ended 30 June 2014 Diamond's earnings increased by 10% and they are expected to continue to increase at this rate over the next two years.

During the year ended 30 June 2015 Diamond's earnings increased by 5% and Diamond management expected that the earnings target would be achieved.

During the year ended 30 June 2016 Diamond's earnings increased by 11%.

When calculating the remuneration expense to be recognised for the year ended 30 June 2015 which of the following dollar values should be included in the calculation?

A) $10.

B) $12.

C) $30.

D) $35.

During the year ended 30 June 2014 Diamond's earnings increased by 10% and they are expected to continue to increase at this rate over the next two years.

During the year ended 30 June 2015 Diamond's earnings increased by 5% and Diamond management expected that the earnings target would be achieved.

During the year ended 30 June 2016 Diamond's earnings increased by 11%.

When calculating the remuneration expense to be recognised for the year ended 30 June 2015 which of the following dollar values should be included in the calculation?

A) $10.

B) $12.

C) $30.

D) $35.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 24 في هذه المجموعة.

فتح الحزمة

k this deck

5

Pepper Limited grants 500 share options to each of its 30 employees. Each grant is conditional on the employee working for the company for the next three years. The fair value of each option is estimated to be $5.00 at grant date and $7.50 at vesting date.

The amount to be recognised as an expense by Pepper in year 2 is:

A) $25 000.

B) $37 500.

C) $50 000.

D) $75 000.

The amount to be recognised as an expense by Pepper in year 2 is:

A) $25 000.

B) $37 500.

C) $50 000.

D) $75 000.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 24 في هذه المجموعة.

فتح الحزمة

k this deck

6

On 1 July 2013 Pearl Pty Ltd granted 800 share options with an exercise price of $35 to the CFO, conditional on the CFO remaining in employment with the company until 30 June 2016. The fair value of Pearl's shares at that time were assessed to be $40. The exercise price will drop to $30 if Pearl's earnings increase by an average of 8% per year over the three year period. On 1 July 2013 the estimated fair value of the share options with an exercise price of $35 is $10 per option, and if the exercise price is $30, the estimated fair value of the options is $12 per option.

During the year ended 30 June 2014 Pearl's earnings increased by 10% and they are expected to continue to increase at this rate over the next two years.

During the year ended 30 June 2015 Pearl's earnings increased by 9% and Pearl management continued to expect that the earnings target would be achieved.

During the year ended 30 June 2016 Pearl's earnings increased by only 2%. At 30 June 2016 the share price is $23.

The remuneration expense to be recognised for the year ended 30 June 2014 is:

A) $2667.

B) $3200.

C) $8000.

D) $9600.

During the year ended 30 June 2014 Pearl's earnings increased by 10% and they are expected to continue to increase at this rate over the next two years.

During the year ended 30 June 2015 Pearl's earnings increased by 9% and Pearl management continued to expect that the earnings target would be achieved.

During the year ended 30 June 2016 Pearl's earnings increased by only 2%. At 30 June 2016 the share price is $23.

The remuneration expense to be recognised for the year ended 30 June 2014 is:

A) $2667.

B) $3200.

C) $8000.

D) $9600.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 24 في هذه المجموعة.

فتح الحزمة

k this deck

7

On 1 July 2013, Nelson Pty Ltd granted 250 options to each of its 50 employees. The options are conditional on the employees remaining with the company for the 3 year vesting period. The options have a fair value of $7.50 at vesting date. In addition, the shares will vest as follows:

On 30 June 2014 if the company's earnings have increased by more than 12%

On 30 June 2015 if the company's earnings have increased by more than 10% averaged across the 2 year period

On 30 June 2016 if the company's earnings have increased by more than 8% averaged across the 3 year period

At 30 June 2014 Nelson's earnings have increased by 11% and 3 employees have left.

The company expects that earnings will continue to increase at a similar rate during the year to 30 June 2015 and that the shares will vest at that time. It also expects that a further 4 employees will leave during the year.

The remuneration expense for the year ended 30 June 2014 for Nelson is:

A) $26 875.00.

B) $29 375.00.

C) $40 312.50.

D) $88 125.00.

On 30 June 2014 if the company's earnings have increased by more than 12%

On 30 June 2015 if the company's earnings have increased by more than 10% averaged across the 2 year period

On 30 June 2016 if the company's earnings have increased by more than 8% averaged across the 3 year period

At 30 June 2014 Nelson's earnings have increased by 11% and 3 employees have left.

The company expects that earnings will continue to increase at a similar rate during the year to 30 June 2015 and that the shares will vest at that time. It also expects that a further 4 employees will leave during the year.

The remuneration expense for the year ended 30 June 2014 for Nelson is:

A) $26 875.00.

B) $29 375.00.

C) $40 312.50.

D) $88 125.00.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 24 في هذه المجموعة.

فتح الحزمة

k this deck

8

Question 13 is an example of:

A) an equity-settled share-based payment transaction.

B) a cash-settled share-based payment transaction.

C) a share-based payment transaction where the counterparty has the settlement choice.

D) a share-based payment transaction where the entity has the settlement choice.

A) an equity-settled share-based payment transaction.

B) a cash-settled share-based payment transaction.

C) a share-based payment transaction where the counterparty has the settlement choice.

D) a share-based payment transaction where the entity has the settlement choice.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 24 في هذه المجموعة.

فتح الحزمة

k this deck

9

A share-based payment transaction in which the entity acquires goods or services by incurring liabilities to the supplier for amounts that are based on the value of the entity's shares or other equity instruments of the entity is classified in AASB 2 Share-based Payment as:

A) an equity-settled share-based payment transaction.

B) a cash-settled share-based payment transaction.

C) a liability-settled share-based payment transaction.

D) an "other" share-based payment transaction.

A) an equity-settled share-based payment transaction.

B) a cash-settled share-based payment transaction.

C) a liability-settled share-based payment transaction.

D) an "other" share-based payment transaction.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 24 في هذه المجموعة.

فتح الحزمة

k this deck

10

On 1 July 2013 Fantasy Ltd granted 200 options to each of its 100 employees. The share options will vest on 30 June 2015 if the employees remain employed with the company on that date. The share options have a life of four years. The exercise price is $5, which is also Fantasy's share price at the grant date. Fantasy is unable to reliably estimate the fair value of the share options at the grant date.

Fantasy's share price and the number of options exercised are set out below. Share options may only be exercised at year end.

The cumulative remuneration expense to be recognised by Fantasy as at 30 June 2015 is:

A) $7800

B) $17 800

*c) $35 600

D) $124 600

Fantasy's share price and the number of options exercised are set out below. Share options may only be exercised at year end.

The cumulative remuneration expense to be recognised by Fantasy as at 30 June 2015 is:

A) $7800

B) $17 800

*c) $35 600

D) $124 600

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 24 في هذه المجموعة.

فتح الحزمة

k this deck

11

On 1 July 2013, Leo Limited granted 250 options to each of its 50 employees. The options are conditional on the employees remaining with the company for the 2 year vesting period. The options have a fair value of $10 at vesting date. In addition, the shares will vest as follows:

On 30 June 2014 if the company's earnings have increased by more than 15%

On 30 June 2015 if the company's earnings have increased by more than 12% averaged across the 2 year period

At 30 June 2014 Leo's earnings have increased by 12% and 3 employees have left.

The company expects that earnings will continue to increase at a similar rate during the year to 30 June 2015 and that the shares will vest at that time. It also expects that a further 4 employees will leave during the year.

The remuneration expense for the year ended 30 June 2014 for Leo is:

A) $35 833.

B) $53 750.

C) $58 750.

D) $117 500.

On 30 June 2014 if the company's earnings have increased by more than 15%

On 30 June 2015 if the company's earnings have increased by more than 12% averaged across the 2 year period

At 30 June 2014 Leo's earnings have increased by 12% and 3 employees have left.

The company expects that earnings will continue to increase at a similar rate during the year to 30 June 2015 and that the shares will vest at that time. It also expects that a further 4 employees will leave during the year.

The remuneration expense for the year ended 30 June 2014 for Leo is:

A) $35 833.

B) $53 750.

C) $58 750.

D) $117 500.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 24 في هذه المجموعة.

فتح الحزمة

k this deck

12

Salt Limited grants 1000 share options to each of its 100 employees. Each grant is conditional on the employee working for the company for the next two years. The fair value of each option is estimated to be $5.00 at grant date and $7.50 at vesting date.

The amount to be recognised as an expense by Salt in year 2 is:

A) $250 000.

B) $375 000.

C) $500 000.

D) $750 000.

The amount to be recognised as an expense by Salt in year 2 is:

A) $250 000.

B) $375 000.

C) $500 000.

D) $750 000.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 24 في هذه المجموعة.

فتح الحزمة

k this deck

13

On 1 July 2013 Pepper Limited granted 500 share options to each of its 100 employees. Each grant is conditional on the employee working for the company for the next two years. The fair value of each option is estimated to be $3.00. Pepper estimates that 8% of its employees will leave during the two year period and therefore forfeit their rights to the share options.

During the year ended 30 June 2014 five employees left. At this time the company revised its estimate of total employee departures over the full two-year period to 10%.

During the year ended 30 June 2015 a further 4 employees left.

The amount to be recognised as an expense by Pepper for the year ended 30 June 2014 is:

A) $67 500.

B) $69 000.

C) $71 250.

D) $135 000.

During the year ended 30 June 2014 five employees left. At this time the company revised its estimate of total employee departures over the full two-year period to 10%.

During the year ended 30 June 2015 a further 4 employees left.

The amount to be recognised as an expense by Pepper for the year ended 30 June 2014 is:

A) $67 500.

B) $69 000.

C) $71 250.

D) $135 000.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 24 في هذه المجموعة.

فتح الحزمة

k this deck

14

Which of the following statements in relation to disclosures required under AASB 2 Share-based Payment is NOT correct?

A) For arrangements that were modified during the year, the incremental fair value granted as a result.

B) The weighted average price at the date of exercise for options exercised during the period.

C) A description of the plan, including the general terms and conditions, vesting requirements, maximum term of options granted and method of settlement must be disclosed.

D) for liabilities arising from share-based payment transactions, the total intrinsic value at the end of the period for liabilities where the counter party's right had not yet vested.

A) For arrangements that were modified during the year, the incremental fair value granted as a result.

B) The weighted average price at the date of exercise for options exercised during the period.

C) A description of the plan, including the general terms and conditions, vesting requirements, maximum term of options granted and method of settlement must be disclosed.

D) for liabilities arising from share-based payment transactions, the total intrinsic value at the end of the period for liabilities where the counter party's right had not yet vested.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 24 في هذه المجموعة.

فتح الحزمة

k this deck

15

In situations where an option-pricing model is required to be used to determine the fair value of equity instruments granted AASB 2 Share-based Payment:

A) requires expected dividends to be taken into account when measuring the shares or options granted.

B) allows the entity to choose the option-pricing model it wishes to use, but contains a number of factors that the option-pricing model selected must take into account as a minimum.

C) requires the use of a binominal option-pricing model.

D) requires the use of the Black-Scholes-Merton formula.

A) requires expected dividends to be taken into account when measuring the shares or options granted.

B) allows the entity to choose the option-pricing model it wishes to use, but contains a number of factors that the option-pricing model selected must take into account as a minimum.

C) requires the use of a binominal option-pricing model.

D) requires the use of the Black-Scholes-Merton formula.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 24 في هذه المجموعة.

فتح الحزمة

k this deck

16

On 1 July 2014 Luca Ltd grants 200 options to each of its 75 employees conditional on the employee remaining in service over the next two years. The fair value of each option is estimated to be $7. Luca estimates that 8 employees will leave over the two year vesting period.

By 30 June 2015 four employees have left and the entity estimates that a further five employees will leave over the next year.

On 30 June 2015 Luca decided to reprice its share options, due to a fall in its share price over the last 12 months. The repriced share options will vest on 30 June 2016. At the date of repricing Luca estimates that the fair value of each original option is $1.50 and the fair value of each repriced option is $3.

During the year ended 30 June 2016 four employees left.

The remuneration expense for the year ended 30 June 2015 is:

A) $34 650.

B) $35 175.

C) $46 200.

D) $46 900.

By 30 June 2015 four employees have left and the entity estimates that a further five employees will leave over the next year.

On 30 June 2015 Luca decided to reprice its share options, due to a fall in its share price over the last 12 months. The repriced share options will vest on 30 June 2016. At the date of repricing Luca estimates that the fair value of each original option is $1.50 and the fair value of each repriced option is $3.

During the year ended 30 June 2016 four employees left.

The remuneration expense for the year ended 30 June 2015 is:

A) $34 650.

B) $35 175.

C) $46 200.

D) $46 900.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 24 في هذه المجموعة.

فتح الحزمة

k this deck

17

Reload features are accounted for as follows:

A) included in the fair value of the initial options granted at measurement date.

B) separately from the initial options granted.

C) as a market condition.

D) as a modification to the initial terms and conditions of the initial options granted.

A) included in the fair value of the initial options granted at measurement date.

B) separately from the initial options granted.

C) as a market condition.

D) as a modification to the initial terms and conditions of the initial options granted.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 24 في هذه المجموعة.

فتح الحزمة

k this deck

18

Which of the following statements in relation to modifications to the terms and conditions on which equity instruments were granted as part of an employee share scheme is correct?

A) A reduction in the exercise price of options will reduce the fair value of the share options.

B) A reduction in a performance hurdle relating to profitability targets will reduce the fair value of the options.

C) A shortening of the vesting period will increase the fair value of the share options.

D) An increase in the number of equity instruments granted is not an example of a modification.

A) A reduction in the exercise price of options will reduce the fair value of the share options.

B) A reduction in a performance hurdle relating to profitability targets will reduce the fair value of the options.

C) A shortening of the vesting period will increase the fair value of the share options.

D) An increase in the number of equity instruments granted is not an example of a modification.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 24 في هذه المجموعة.

فتح الحزمة

k this deck

19

Which of the following is within the scope of AASB 2 Share-based Payment?

A) Transactions in which the entity receives or acquires goods or services as part of the net assets acquired in a business combination to which IFRS 3 Business Combinations applies.

B) Transaction in which the entity receives or acquired goods or services under a contract which is within the scope of AASB 139 Financial Instruments: Recognition & Measurement.

C) Transactions with employees in the employee's capacity as a holder of equity instruments of the entity.

D) Cancellation, replacement or modification of share-based payments arising because of a business combination or restructuring.

A) Transactions in which the entity receives or acquires goods or services as part of the net assets acquired in a business combination to which IFRS 3 Business Combinations applies.

B) Transaction in which the entity receives or acquired goods or services under a contract which is within the scope of AASB 139 Financial Instruments: Recognition & Measurement.

C) Transactions with employees in the employee's capacity as a holder of equity instruments of the entity.

D) Cancellation, replacement or modification of share-based payments arising because of a business combination or restructuring.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 24 في هذه المجموعة.

فتح الحزمة

k this deck

20

A share-based payment transaction in which the entity receives goods or services as consideration for equity instruments of the entity is classified in AASB 2 Share-based Payment as:

A) an equity-settled share-based payment transaction.

B) a cash-settled share-based payment transaction.

C) a liability-settled share-based payment transaction.

D) an 'other' share-based payment transaction.

A) an equity-settled share-based payment transaction.

B) a cash-settled share-based payment transaction.

C) a liability-settled share-based payment transaction.

D) an 'other' share-based payment transaction.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 24 في هذه المجموعة.

فتح الحزمة

k this deck

21

On 1 July 2013 Poggio Ltd grants 300 options to each of its 100 employees conditional on the employee remaining in service over the next three years. The fair value of each option is estimated to be $12. Poggio estimates that 15 employees will leave over the three year vesting period.

By 30 June 2014 four employees have left and the entity estimates that a further ten employees will leave over the next two years.

On 30 June 2014 Poggio decided to reprice its share options, due to a fall in its share price over the last 12 months. The repriced share options will vest on 30 June 2016. At the date of repricing Poggio estimates that the fair value of each original option is $3 and the fair value of each repriced option is $5.

During the year ended 30 June 2015 a further 6 employees leave and Poggio estimates that another 3 employees will leave during the year ended 30 June 2016.

During the year ended 30 June 2016 four employees left.

The entry at 30 June 2015 to account for the share based payment transaction is:

A) DR Wages expense CR Liability to employee

B) DR Wages expense CR Options issued (equity)

C) DR Wages expense CR Share capital

D) DR Wages expense CR Cash

By 30 June 2014 four employees have left and the entity estimates that a further ten employees will leave over the next two years.

On 30 June 2014 Poggio decided to reprice its share options, due to a fall in its share price over the last 12 months. The repriced share options will vest on 30 June 2016. At the date of repricing Poggio estimates that the fair value of each original option is $3 and the fair value of each repriced option is $5.

During the year ended 30 June 2015 a further 6 employees leave and Poggio estimates that another 3 employees will leave during the year ended 30 June 2016.

During the year ended 30 June 2016 four employees left.

The entry at 30 June 2015 to account for the share based payment transaction is:

A) DR Wages expense CR Liability to employee

B) DR Wages expense CR Options issued (equity)

C) DR Wages expense CR Share capital

D) DR Wages expense CR Cash

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 24 في هذه المجموعة.

فتح الحزمة

k this deck

22

On 1 July 2013 Pearl Pty Ltd granted 800 share options with an exercise price of $35 to the CFO, conditional on the CFO remaining in employment with the company until 30 June 2016. The fair value of Pearl's shares at that time were assessed to be $40. The exercise price will drop to $30 if Pearl's earnings increase by an average of 8% per year over the three year period. On 1 July 2013 the estimated fair value of the share options with an exercise price of $35 is $10 per option, and if the exercise price is $30, the estimated fair value of the options is $12 per option.

During the year ended 30 June 2014 Pearl's earnings increased by 10% and they are expected to continue to increase at this rate over the next two years.

During the year ended 30 June 2015 Pearl's earnings increased by 9% and Pearl management continued to expect that the earnings target would be achieved.

During the year ended 30 June 2016 Pearl's earnings increased by only 2%. At 30 June 2016 the share price is $23.

Assuming that the CFO decides NOT to exercise his options at 30 June 2016, the following entry would be recorded:

A) DR Wages expense CR Options issued (equity)

B) DR Options issued (equity) CR Lapsed options reserve

C) DR Options issued (equity) CR Retained earnings

D) DR Options issued (equity) CR Wages expense

During the year ended 30 June 2014 Pearl's earnings increased by 10% and they are expected to continue to increase at this rate over the next two years.

During the year ended 30 June 2015 Pearl's earnings increased by 9% and Pearl management continued to expect that the earnings target would be achieved.

During the year ended 30 June 2016 Pearl's earnings increased by only 2%. At 30 June 2016 the share price is $23.

Assuming that the CFO decides NOT to exercise his options at 30 June 2016, the following entry would be recorded:

A) DR Wages expense CR Options issued (equity)

B) DR Options issued (equity) CR Lapsed options reserve

C) DR Options issued (equity) CR Retained earnings

D) DR Options issued (equity) CR Wages expense

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 24 في هذه المجموعة.

فتح الحزمة

k this deck

23

In relation to equity instruments granted by an entity where the entity makes modifications to the terms and conditions attaching to the grant:

A) the incremental fair value is measured as the difference between the fair value of the modified instrument, estimated at the date of modification and that of the original equity instrument, estimated at the date of original granting.

B) if the modification occurs during the vesting period the incremental fair value is recognised immediately.

C) terms or conditions may not be modified in a manner that is not beneficial to the employee.

D) where the exercise price of options is modified, the fair value of the options changes.

A) the incremental fair value is measured as the difference between the fair value of the modified instrument, estimated at the date of modification and that of the original equity instrument, estimated at the date of original granting.

B) if the modification occurs during the vesting period the incremental fair value is recognised immediately.

C) terms or conditions may not be modified in a manner that is not beneficial to the employee.

D) where the exercise price of options is modified, the fair value of the options changes.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 24 في هذه المجموعة.

فتح الحزمة

k this deck

24

Which of the following statements in relation to disclosures required under AASB 2 Share-based Payment is not correct?

A) Option pricing models used in valuing share options must be identified.

B) The number and weighted average exercise price of share options outstanding at the beginning and end of each period must be disclosed.

C) Information about share-based payment arrangements that are substantially the same may be aggregated.

D) The total expense arising from share-based payment transactions in which the services qualified for recognition as an asset must be disclosed.

A) Option pricing models used in valuing share options must be identified.

B) The number and weighted average exercise price of share options outstanding at the beginning and end of each period must be disclosed.

C) Information about share-based payment arrangements that are substantially the same may be aggregated.

D) The total expense arising from share-based payment transactions in which the services qualified for recognition as an asset must be disclosed.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 24 في هذه المجموعة.

فتح الحزمة

k this deck

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 24 في هذه المجموعة.